Financial Management Report: Stortford Yachts Ltd Financial Analysis

VerifiedAdded on 2020/06/06

|11

|3224

|148

Report

AI Summary

This report provides a comprehensive analysis of financial management, focusing on the differences between financial and management accounts and their respective purposes. It details the significance of financial information for various stakeholders, including shareholders, buyers, and financial institutions. The report includes an analysis of Stortford Yachts Ltd's financial performance using ratio analysis to assess profitability and liquidity. It also compares profit and non-profit organizations' financial statements and explores the roles of different stakeholders and their crucial data in business decision-making. The report covers income statements, statements of financial position, and cash flow statements, offering a detailed overview of financial reporting and its importance in organizational success. The report is a valuable resource for students studying financial management, providing insights into key concepts and practical applications.

MANGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Deviation between financial accounts and management accounts.....................................1

b) Determine and purpose of different financial statements in an organisation.....................3

C) Different group of stakeholders and analysing their crucial data......................................5

TASK 2............................................................................................................................................6

a) Analysing financial performance of Stortford Yachts Ltd by ratio analysis......................6

b) Financial report to define financial performance of Stortford Yachts Ltd.........................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Deviation between financial accounts and management accounts.....................................1

b) Determine and purpose of different financial statements in an organisation.....................3

C) Different group of stakeholders and analysing their crucial data......................................5

TASK 2............................................................................................................................................6

a) Analysing financial performance of Stortford Yachts Ltd by ratio analysis......................6

b) Financial report to define financial performance of Stortford Yachts Ltd.........................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Better management ad effective operations depends upon adequate management of

financial resources (Broadbent and Cullen, 2012). Financial accounting is one of the branch of

management accounting which assist the organisational structure for better management and

operation. This reports is prepared to define importance of financial management in managing

financial resources. Diversification between management accounts and financial accounts

explained in this report. Significance of financial information for group of stakeholder of

organisation also discussed. Financial performance of Stortford Yachts Ltd analysed by using

ratio analysis. A detailed report is prepared to defined in respect of profitability and liquidity also

elaborated in organisational context.

TASK 1

a) Deviation between financial accounts and management accounts

Management accounts

These are the accounts which helps in decision making and strategic planning. These are

the part of managerial actions and activities which are organised to make effective growth and

development strategies. Management accounts are prepared by accountants and managers subject

to analyse complex business situations and problems (Robb and Woodyard, 2011). It not only

helps to resolve critical business equations but also helps to sort out management plans for

effective decision making. Information which are produced under management accounts helps

management accountants and managers.

Financial accounts

Financial accounts are prepare by finance accountants in order to record day to day

financial transactions. Financial accounts are prepared on periodic basis. With the help of

financial accounts finance managers and accountants easily understand the financial dimensions

and prepare financial plans and strategies. Financial information and financial reports are

prepared in the basis of financial accounts. These reports indicates towards financial strength and

performance of an organisation (Financial planning meaning and definition, 2017).

Basic Financial accounts Management accounts

Definition Financial accounts are important

aspect subject to analyse financial

Management accounts defines the

managerial strength and capacity of an

1

Better management ad effective operations depends upon adequate management of

financial resources (Broadbent and Cullen, 2012). Financial accounting is one of the branch of

management accounting which assist the organisational structure for better management and

operation. This reports is prepared to define importance of financial management in managing

financial resources. Diversification between management accounts and financial accounts

explained in this report. Significance of financial information for group of stakeholder of

organisation also discussed. Financial performance of Stortford Yachts Ltd analysed by using

ratio analysis. A detailed report is prepared to defined in respect of profitability and liquidity also

elaborated in organisational context.

TASK 1

a) Deviation between financial accounts and management accounts

Management accounts

These are the accounts which helps in decision making and strategic planning. These are

the part of managerial actions and activities which are organised to make effective growth and

development strategies. Management accounts are prepared by accountants and managers subject

to analyse complex business situations and problems (Robb and Woodyard, 2011). It not only

helps to resolve critical business equations but also helps to sort out management plans for

effective decision making. Information which are produced under management accounts helps

management accountants and managers.

Financial accounts

Financial accounts are prepare by finance accountants in order to record day to day

financial transactions. Financial accounts are prepared on periodic basis. With the help of

financial accounts finance managers and accountants easily understand the financial dimensions

and prepare financial plans and strategies. Financial information and financial reports are

prepared in the basis of financial accounts. These reports indicates towards financial strength and

performance of an organisation (Financial planning meaning and definition, 2017).

Basic Financial accounts Management accounts

Definition Financial accounts are important

aspect subject to analyse financial

Management accounts defines the

managerial strength and capacity of an

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance and growth of an

organisation. These are the part of

financial planning.

organisation subject to dealing with

management challenges and complex

situations. These are the parts of decision

making process.

Reporting

parties

Financial reports, information,

summarised financial information

are some essential detail remain

essential for stakeholders of

organisation. These are also called

as reporting parties. Shareholders,

buyers, suppliers, banks and

financial institutions are considered

as stakeholders of organisation.

Management accounts helps to analyse

the internal strength and capacity of

organisation. Information and details

which are produced under management

accounts remain important for internal

parties of organisation. Managers, senior

authorities, employees and employers

are considered as internal parties of an

entity.

Regulatory

requirements

Preparing financial accounts and

keeping financial information is

mandatory for business and

organisations. There are some

financial standards and rules made

subject to retain and record

financial records.

There is no any specific regulatory and

rules are made for management

accounts. Organisation prepare

management accounts for making

internal management and operation for

smooth and flexible. Business entities

adopt management accounts as per

suitability and preferences.

Output There are type of financial accounts

are prepared by an organisation

such as profit and loss account,

income statements, cash floe

statements, financial position

statement and change in equity

statement.

Management reports such job cost

reports, budget reports, inventories

reports etc. all these reports helps

managers and accounts for making

decision making process.

Motive Analysing financial performance

and detecting financial requirement

Assisting managerial activities and

functions for managing better and

2

organisation. These are the part of

financial planning.

organisation subject to dealing with

management challenges and complex

situations. These are the parts of decision

making process.

Reporting

parties

Financial reports, information,

summarised financial information

are some essential detail remain

essential for stakeholders of

organisation. These are also called

as reporting parties. Shareholders,

buyers, suppliers, banks and

financial institutions are considered

as stakeholders of organisation.

Management accounts helps to analyse

the internal strength and capacity of

organisation. Information and details

which are produced under management

accounts remain important for internal

parties of organisation. Managers, senior

authorities, employees and employers

are considered as internal parties of an

entity.

Regulatory

requirements

Preparing financial accounts and

keeping financial information is

mandatory for business and

organisations. There are some

financial standards and rules made

subject to retain and record

financial records.

There is no any specific regulatory and

rules are made for management

accounts. Organisation prepare

management accounts for making

internal management and operation for

smooth and flexible. Business entities

adopt management accounts as per

suitability and preferences.

Output There are type of financial accounts

are prepared by an organisation

such as profit and loss account,

income statements, cash floe

statements, financial position

statement and change in equity

statement.

Management reports such job cost

reports, budget reports, inventories

reports etc. all these reports helps

managers and accounts for making

decision making process.

Motive Analysing financial performance

and detecting financial requirement

Assisting managerial activities and

functions for managing better and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

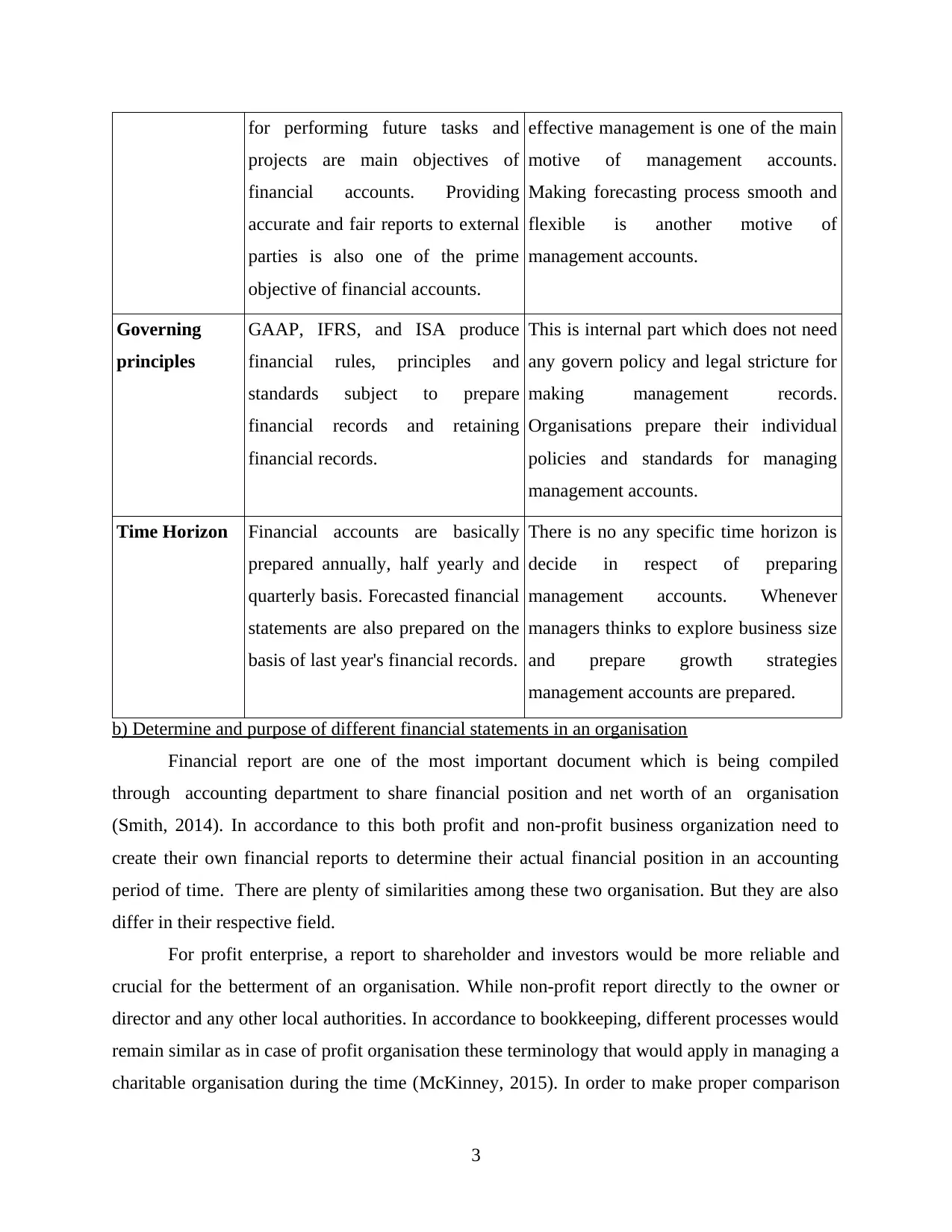

for performing future tasks and

projects are main objectives of

financial accounts. Providing

accurate and fair reports to external

parties is also one of the prime

objective of financial accounts.

effective management is one of the main

motive of management accounts.

Making forecasting process smooth and

flexible is another motive of

management accounts.

Governing

principles

GAAP, IFRS, and ISA produce

financial rules, principles and

standards subject to prepare

financial records and retaining

financial records.

This is internal part which does not need

any govern policy and legal stricture for

making management records.

Organisations prepare their individual

policies and standards for managing

management accounts.

Time Horizon Financial accounts are basically

prepared annually, half yearly and

quarterly basis. Forecasted financial

statements are also prepared on the

basis of last year's financial records.

There is no any specific time horizon is

decide in respect of preparing

management accounts. Whenever

managers thinks to explore business size

and prepare growth strategies

management accounts are prepared.

b) Determine and purpose of different financial statements in an organisation

Financial report are one of the most important document which is being compiled

through accounting department to share financial position and net worth of an organisation

(Smith, 2014). In accordance to this both profit and non-profit business organization need to

create their own financial reports to determine their actual financial position in an accounting

period of time. There are plenty of similarities among these two organisation. But they are also

differ in their respective field.

For profit enterprise, a report to shareholder and investors would be more reliable and

crucial for the betterment of an organisation. While non-profit report directly to the owner or

director and any other local authorities. In accordance to bookkeeping, different processes would

remain similar as in case of profit organisation these terminology that would apply in managing a

charitable organisation during the time (McKinney, 2015). In order to make proper comparison

3

projects are main objectives of

financial accounts. Providing

accurate and fair reports to external

parties is also one of the prime

objective of financial accounts.

effective management is one of the main

motive of management accounts.

Making forecasting process smooth and

flexible is another motive of

management accounts.

Governing

principles

GAAP, IFRS, and ISA produce

financial rules, principles and

standards subject to prepare

financial records and retaining

financial records.

This is internal part which does not need

any govern policy and legal stricture for

making management records.

Organisations prepare their individual

policies and standards for managing

management accounts.

Time Horizon Financial accounts are basically

prepared annually, half yearly and

quarterly basis. Forecasted financial

statements are also prepared on the

basis of last year's financial records.

There is no any specific time horizon is

decide in respect of preparing

management accounts. Whenever

managers thinks to explore business size

and prepare growth strategies

management accounts are prepared.

b) Determine and purpose of different financial statements in an organisation

Financial report are one of the most important document which is being compiled

through accounting department to share financial position and net worth of an organisation

(Smith, 2014). In accordance to this both profit and non-profit business organization need to

create their own financial reports to determine their actual financial position in an accounting

period of time. There are plenty of similarities among these two organisation. But they are also

differ in their respective field.

For profit enterprise, a report to shareholder and investors would be more reliable and

crucial for the betterment of an organisation. While non-profit report directly to the owner or

director and any other local authorities. In accordance to bookkeeping, different processes would

remain similar as in case of profit organisation these terminology that would apply in managing a

charitable organisation during the time (McKinney, 2015). In order to make proper comparison

3

of financial statements of profit to non-profit organisation that would be notice in both specific

reports of financial values. It has been observed that one additional trust as real that does not

operate for the primary motive generating maximum profit from their entire business operations.

Although, profit organisation are working with the aim of increase as much gains as they

can during an accounting year. For this purpose they use to utilise resources in more accurate and

reliable manner (Lusardi and Mitchell, 2014). The only matter which would create maximum

difference can provide right path their future targets. This has been determine as not only

organisation are operating for the motive of increase their gains but they are some which can

work for the aims to serve communities and for the development of an society. Financial reports

are more reliable that are based on various statements which are comply by using collecting vital

data from different department of “Stratford Yachts Ltd”. Every organisation can use to

maintain an effective financial information that can assist in generating more reliable outcomes

during an accounting period of time. It has been seen that both of them are having certain

similarities which make different from each other.

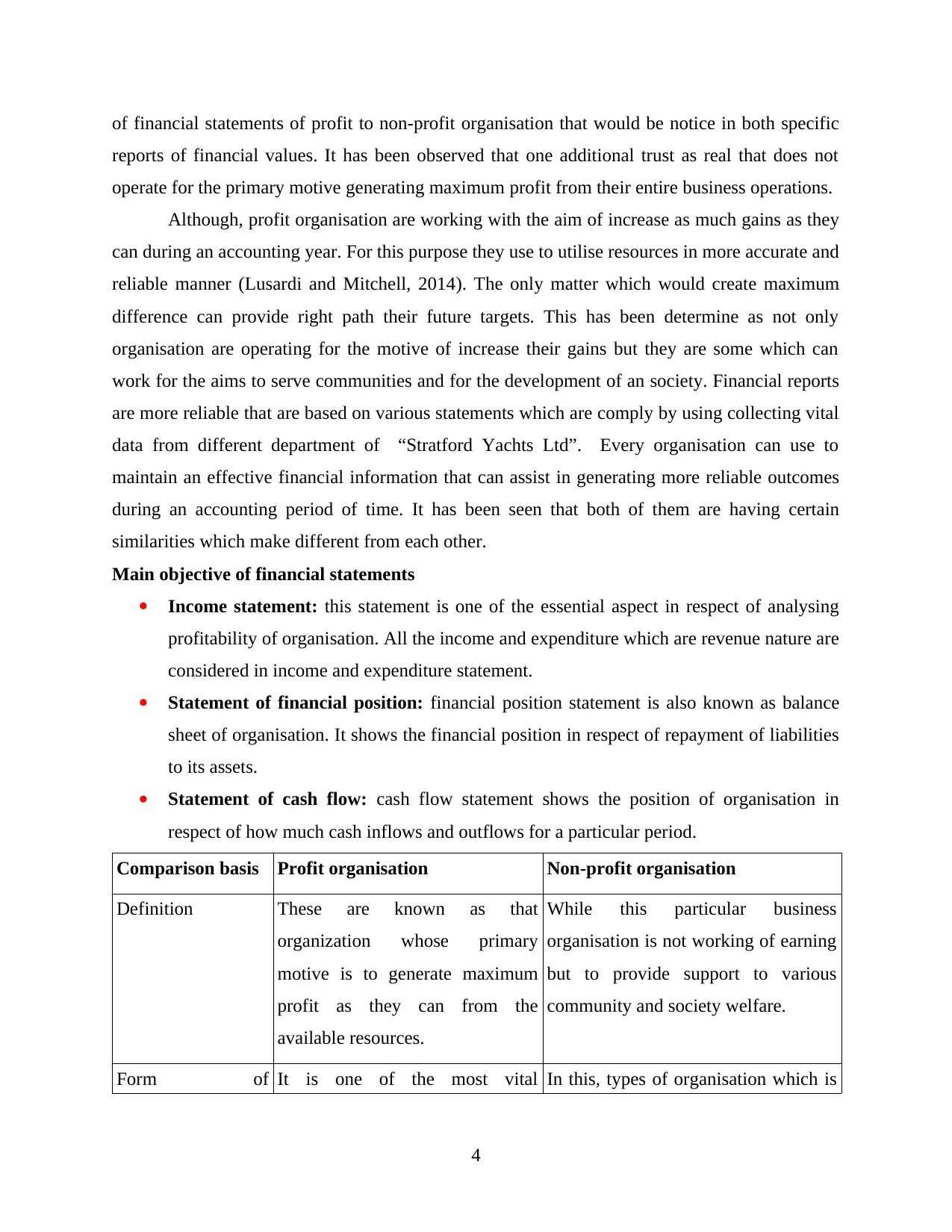

Main objective of financial statements

Income statement: this statement is one of the essential aspect in respect of analysing

profitability of organisation. All the income and expenditure which are revenue nature are

considered in income and expenditure statement.

Statement of financial position: financial position statement is also known as balance

sheet of organisation. It shows the financial position in respect of repayment of liabilities

to its assets.

Statement of cash flow: cash flow statement shows the position of organisation in

respect of how much cash inflows and outflows for a particular period.

Comparison basis Profit organisation Non-profit organisation

Definition These are known as that

organization whose primary

motive is to generate maximum

profit as they can from the

available resources.

While this particular business

organisation is not working of earning

but to provide support to various

community and society welfare.

Form of It is one of the most vital In this, types of organisation which is

4

reports of financial values. It has been observed that one additional trust as real that does not

operate for the primary motive generating maximum profit from their entire business operations.

Although, profit organisation are working with the aim of increase as much gains as they

can during an accounting year. For this purpose they use to utilise resources in more accurate and

reliable manner (Lusardi and Mitchell, 2014). The only matter which would create maximum

difference can provide right path their future targets. This has been determine as not only

organisation are operating for the motive of increase their gains but they are some which can

work for the aims to serve communities and for the development of an society. Financial reports

are more reliable that are based on various statements which are comply by using collecting vital

data from different department of “Stratford Yachts Ltd”. Every organisation can use to

maintain an effective financial information that can assist in generating more reliable outcomes

during an accounting period of time. It has been seen that both of them are having certain

similarities which make different from each other.

Main objective of financial statements

Income statement: this statement is one of the essential aspect in respect of analysing

profitability of organisation. All the income and expenditure which are revenue nature are

considered in income and expenditure statement.

Statement of financial position: financial position statement is also known as balance

sheet of organisation. It shows the financial position in respect of repayment of liabilities

to its assets.

Statement of cash flow: cash flow statement shows the position of organisation in

respect of how much cash inflows and outflows for a particular period.

Comparison basis Profit organisation Non-profit organisation

Definition These are known as that

organization whose primary

motive is to generate maximum

profit as they can from the

available resources.

While this particular business

organisation is not working of earning

but to provide support to various

community and society welfare.

Form of It is one of the most vital In this, types of organisation which is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

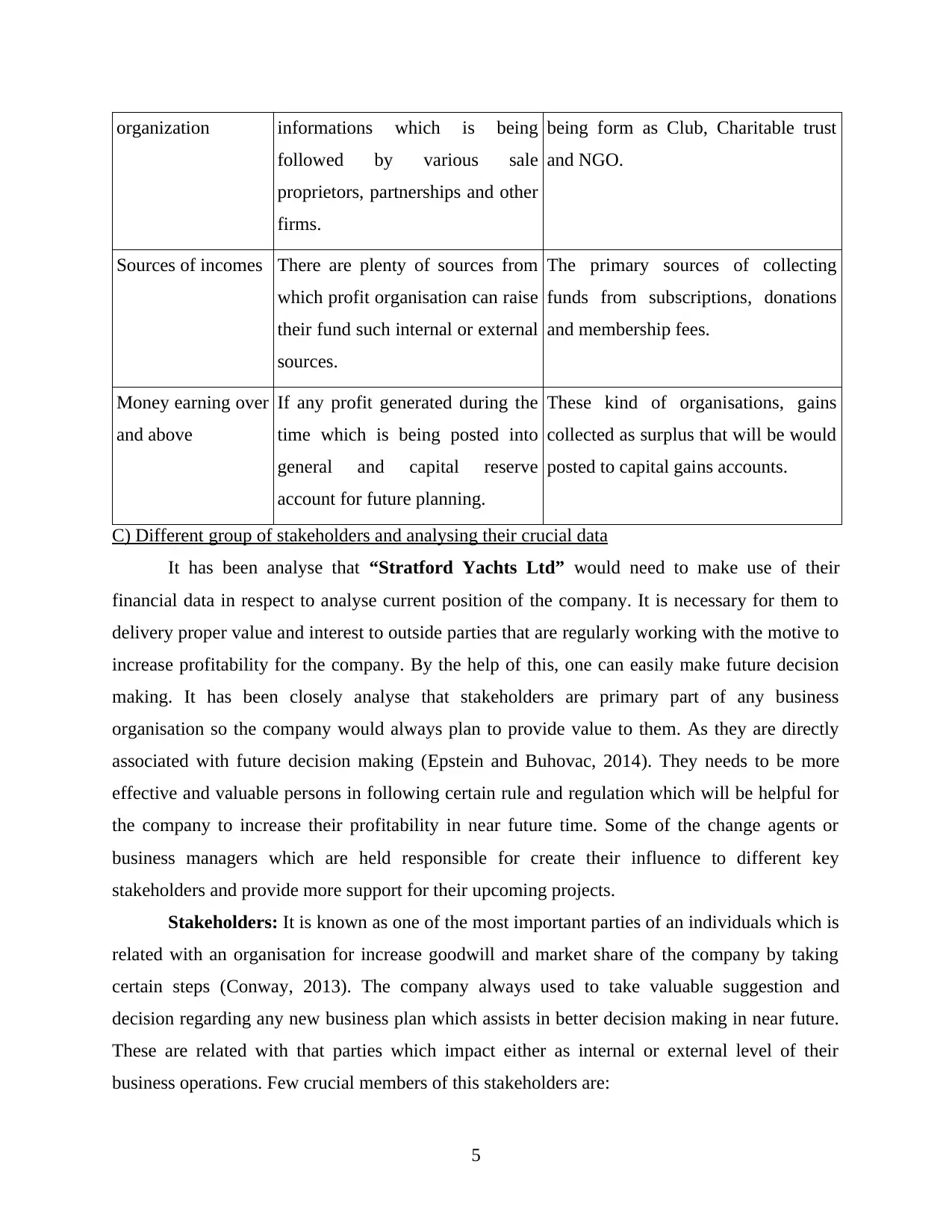

organization informations which is being

followed by various sale

proprietors, partnerships and other

firms.

being form as Club, Charitable trust

and NGO.

Sources of incomes There are plenty of sources from

which profit organisation can raise

their fund such internal or external

sources.

The primary sources of collecting

funds from subscriptions, donations

and membership fees.

Money earning over

and above

If any profit generated during the

time which is being posted into

general and capital reserve

account for future planning.

These kind of organisations, gains

collected as surplus that will be would

posted to capital gains accounts.

C) Different group of stakeholders and analysing their crucial data

It has been analyse that “Stratford Yachts Ltd” would need to make use of their

financial data in respect to analyse current position of the company. It is necessary for them to

delivery proper value and interest to outside parties that are regularly working with the motive to

increase profitability for the company. By the help of this, one can easily make future decision

making. It has been closely analyse that stakeholders are primary part of any business

organisation so the company would always plan to provide value to them. As they are directly

associated with future decision making (Epstein and Buhovac, 2014). They needs to be more

effective and valuable persons in following certain rule and regulation which will be helpful for

the company to increase their profitability in near future time. Some of the change agents or

business managers which are held responsible for create their influence to different key

stakeholders and provide more support for their upcoming projects.

Stakeholders: It is known as one of the most important parties of an individuals which is

related with an organisation for increase goodwill and market share of the company by taking

certain steps (Conway, 2013). The company always used to take valuable suggestion and

decision regarding any new business plan which assists in better decision making in near future.

These are related with that parties which impact either as internal or external level of their

business operations. Few crucial members of this stakeholders are:

5

followed by various sale

proprietors, partnerships and other

firms.

being form as Club, Charitable trust

and NGO.

Sources of incomes There are plenty of sources from

which profit organisation can raise

their fund such internal or external

sources.

The primary sources of collecting

funds from subscriptions, donations

and membership fees.

Money earning over

and above

If any profit generated during the

time which is being posted into

general and capital reserve

account for future planning.

These kind of organisations, gains

collected as surplus that will be would

posted to capital gains accounts.

C) Different group of stakeholders and analysing their crucial data

It has been analyse that “Stratford Yachts Ltd” would need to make use of their

financial data in respect to analyse current position of the company. It is necessary for them to

delivery proper value and interest to outside parties that are regularly working with the motive to

increase profitability for the company. By the help of this, one can easily make future decision

making. It has been closely analyse that stakeholders are primary part of any business

organisation so the company would always plan to provide value to them. As they are directly

associated with future decision making (Epstein and Buhovac, 2014). They needs to be more

effective and valuable persons in following certain rule and regulation which will be helpful for

the company to increase their profitability in near future time. Some of the change agents or

business managers which are held responsible for create their influence to different key

stakeholders and provide more support for their upcoming projects.

Stakeholders: It is known as one of the most important parties of an individuals which is

related with an organisation for increase goodwill and market share of the company by taking

certain steps (Conway, 2013). The company always used to take valuable suggestion and

decision regarding any new business plan which assists in better decision making in near future.

These are related with that parties which impact either as internal or external level of their

business operations. Few crucial members of this stakeholders are:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Primary stakeholders: They are the one which are associated with generating maximum

opportunities in terms of profit and any other aspects by operating activities in more effective

manner (Finkler and et. al., 2016). information and data which remain essential and important

from the perspective of growth and development of organisation are considered in this context.

Operations and administration reports, income and expenditure incurred for assisting

management and operation process are some essential information which remain important for

primary stakeholder of organisation. They are having direct stake in business decision making. It

consists of :

Partner: In accordance important parties as a stakeholder to determine their overall

performance by using growth report and annual statements.

Employees: For these people, their performance report and policies related to extra

benefits are considered.

Customers: All those information those are related with quality and services that are

being delivery by the company are taken into account.

Suppliers: Information associated with credit limits are more reliable for the future

development are helpful.

Secondary stakeholders: It is said to be external parties which is related with

recognising company requirements by overlooking their business operations in more effective

manner. It has been seen that most individual use to accumulate to generate better reputation and

cooperation by increasing other vital activities from outside. financial performance reports.

Analysing profitability and solvency reports are essential aspects which remain essential for

better operation and management of financial resources. Some valuable parties associated with

this are discuss underneath:

Competitor: In accordance with these parties, data related with financial position of the

company are more effective. Such are taken from balance sheet and cash flow statements.

Government: Latest polices and regulation which are being followed by the companies

in their daily business operations are considered for local authorities.

Media: The overall detail data about present performance of the company are taken into

accounts.

Banks: In accordance with banks, they need to have proper information regarding

financial position and statements of the company.

6

opportunities in terms of profit and any other aspects by operating activities in more effective

manner (Finkler and et. al., 2016). information and data which remain essential and important

from the perspective of growth and development of organisation are considered in this context.

Operations and administration reports, income and expenditure incurred for assisting

management and operation process are some essential information which remain important for

primary stakeholder of organisation. They are having direct stake in business decision making. It

consists of :

Partner: In accordance important parties as a stakeholder to determine their overall

performance by using growth report and annual statements.

Employees: For these people, their performance report and policies related to extra

benefits are considered.

Customers: All those information those are related with quality and services that are

being delivery by the company are taken into account.

Suppliers: Information associated with credit limits are more reliable for the future

development are helpful.

Secondary stakeholders: It is said to be external parties which is related with

recognising company requirements by overlooking their business operations in more effective

manner. It has been seen that most individual use to accumulate to generate better reputation and

cooperation by increasing other vital activities from outside. financial performance reports.

Analysing profitability and solvency reports are essential aspects which remain essential for

better operation and management of financial resources. Some valuable parties associated with

this are discuss underneath:

Competitor: In accordance with these parties, data related with financial position of the

company are more effective. Such are taken from balance sheet and cash flow statements.

Government: Latest polices and regulation which are being followed by the companies

in their daily business operations are considered for local authorities.

Media: The overall detail data about present performance of the company are taken into

accounts.

Banks: In accordance with banks, they need to have proper information regarding

financial position and statements of the company.

6

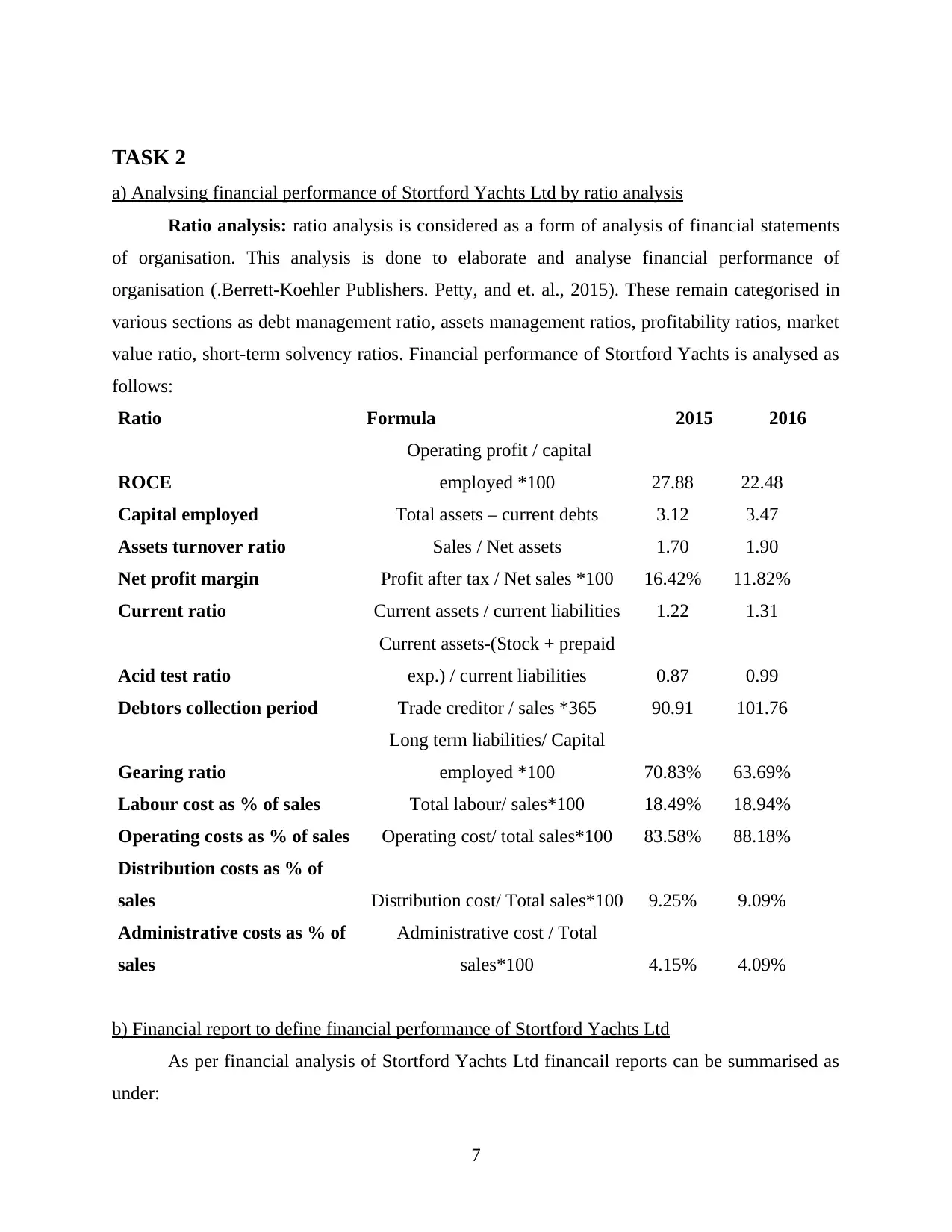

TASK 2

a) Analysing financial performance of Stortford Yachts Ltd by ratio analysis

Ratio analysis: ratio analysis is considered as a form of analysis of financial statements

of organisation. This analysis is done to elaborate and analyse financial performance of

organisation (.Berrett-Koehler Publishers. Petty, and et. al., 2015). These remain categorised in

various sections as debt management ratio, assets management ratios, profitability ratios, market

value ratio, short-term solvency ratios. Financial performance of Stortford Yachts is analysed as

follows:

Ratio Formula 2015 2016

ROCE

Operating profit / capital

employed *100 27.88 22.48

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets 1.70 1.90

Net profit margin Profit after tax / Net sales *100 16.42% 11.82%

Current ratio Current assets / current liabilities 1.22 1.31

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities 0.87 0.99

Debtors collection period Trade creditor / sales *365 90.91 101.76

Gearing ratio

Long term liabilities/ Capital

employed *100 70.83% 63.69%

Labour cost as % of sales Total labour/ sales*100 18.49% 18.94%

Operating costs as % of sales Operating cost/ total sales*100 83.58% 88.18%

Distribution costs as % of

sales Distribution cost/ Total sales*100 9.25% 9.09%

Administrative costs as % of

sales

Administrative cost / Total

sales*100 4.15% 4.09%

b) Financial report to define financial performance of Stortford Yachts Ltd

As per financial analysis of Stortford Yachts Ltd financail reports can be summarised as

under:

7

a) Analysing financial performance of Stortford Yachts Ltd by ratio analysis

Ratio analysis: ratio analysis is considered as a form of analysis of financial statements

of organisation. This analysis is done to elaborate and analyse financial performance of

organisation (.Berrett-Koehler Publishers. Petty, and et. al., 2015). These remain categorised in

various sections as debt management ratio, assets management ratios, profitability ratios, market

value ratio, short-term solvency ratios. Financial performance of Stortford Yachts is analysed as

follows:

Ratio Formula 2015 2016

ROCE

Operating profit / capital

employed *100 27.88 22.48

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets 1.70 1.90

Net profit margin Profit after tax / Net sales *100 16.42% 11.82%

Current ratio Current assets / current liabilities 1.22 1.31

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities 0.87 0.99

Debtors collection period Trade creditor / sales *365 90.91 101.76

Gearing ratio

Long term liabilities/ Capital

employed *100 70.83% 63.69%

Labour cost as % of sales Total labour/ sales*100 18.49% 18.94%

Operating costs as % of sales Operating cost/ total sales*100 83.58% 88.18%

Distribution costs as % of

sales Distribution cost/ Total sales*100 9.25% 9.09%

Administrative costs as % of

sales

Administrative cost / Total

sales*100 4.15% 4.09%

b) Financial report to define financial performance of Stortford Yachts Ltd

As per financial analysis of Stortford Yachts Ltd financail reports can be summarised as

under:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

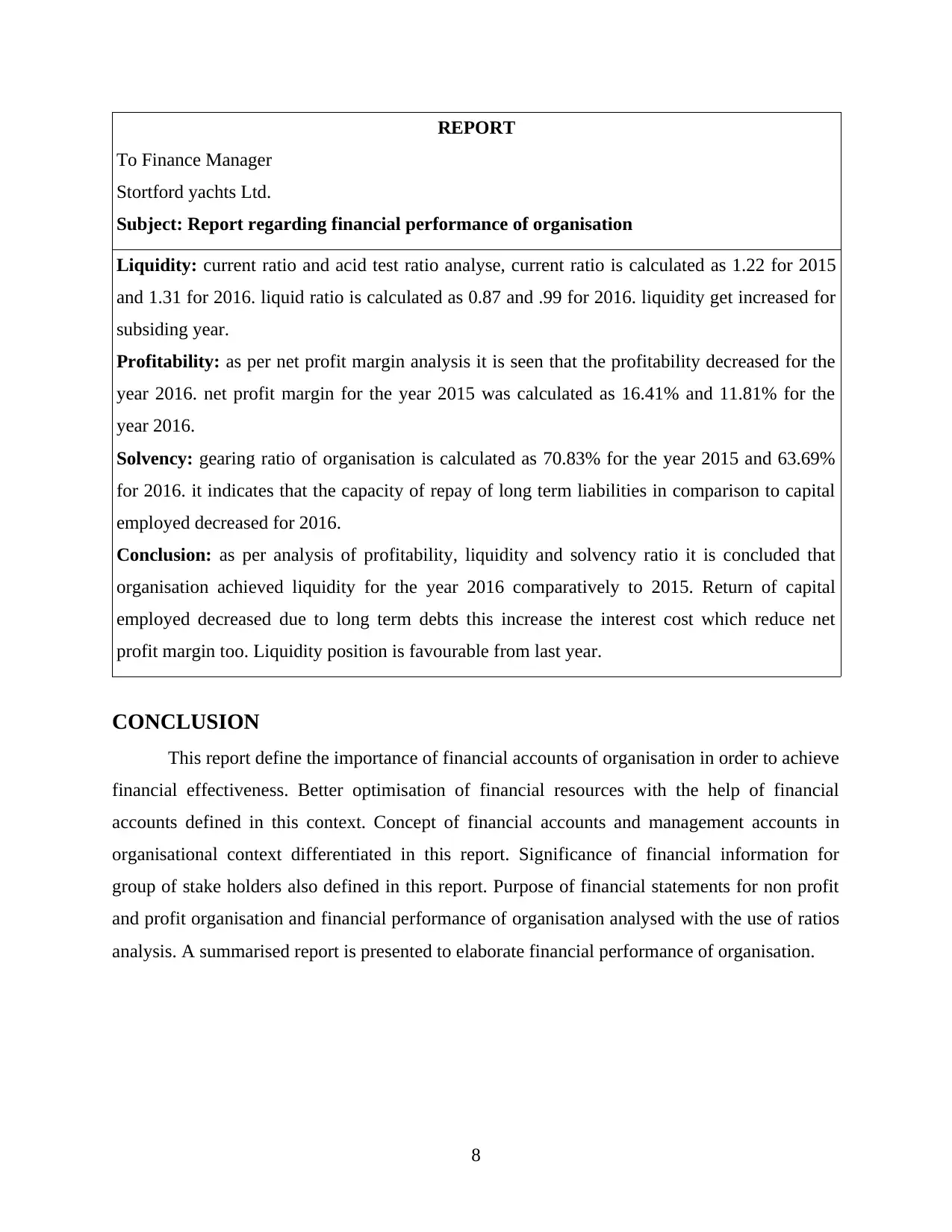

REPORT

To Finance Manager

Stortford yachts Ltd.

Subject: Report regarding financial performance of organisation

Liquidity: current ratio and acid test ratio analyse, current ratio is calculated as 1.22 for 2015

and 1.31 for 2016. liquid ratio is calculated as 0.87 and .99 for 2016. liquidity get increased for

subsiding year.

Profitability: as per net profit margin analysis it is seen that the profitability decreased for the

year 2016. net profit margin for the year 2015 was calculated as 16.41% and 11.81% for the

year 2016.

Solvency: gearing ratio of organisation is calculated as 70.83% for the year 2015 and 63.69%

for 2016. it indicates that the capacity of repay of long term liabilities in comparison to capital

employed decreased for 2016.

Conclusion: as per analysis of profitability, liquidity and solvency ratio it is concluded that

organisation achieved liquidity for the year 2016 comparatively to 2015. Return of capital

employed decreased due to long term debts this increase the interest cost which reduce net

profit margin too. Liquidity position is favourable from last year.

CONCLUSION

This report define the importance of financial accounts of organisation in order to achieve

financial effectiveness. Better optimisation of financial resources with the help of financial

accounts defined in this context. Concept of financial accounts and management accounts in

organisational context differentiated in this report. Significance of financial information for

group of stake holders also defined in this report. Purpose of financial statements for non profit

and profit organisation and financial performance of organisation analysed with the use of ratios

analysis. A summarised report is presented to elaborate financial performance of organisation.

8

To Finance Manager

Stortford yachts Ltd.

Subject: Report regarding financial performance of organisation

Liquidity: current ratio and acid test ratio analyse, current ratio is calculated as 1.22 for 2015

and 1.31 for 2016. liquid ratio is calculated as 0.87 and .99 for 2016. liquidity get increased for

subsiding year.

Profitability: as per net profit margin analysis it is seen that the profitability decreased for the

year 2016. net profit margin for the year 2015 was calculated as 16.41% and 11.81% for the

year 2016.

Solvency: gearing ratio of organisation is calculated as 70.83% for the year 2015 and 63.69%

for 2016. it indicates that the capacity of repay of long term liabilities in comparison to capital

employed decreased for 2016.

Conclusion: as per analysis of profitability, liquidity and solvency ratio it is concluded that

organisation achieved liquidity for the year 2016 comparatively to 2015. Return of capital

employed decreased due to long term debts this increase the interest cost which reduce net

profit margin too. Liquidity position is favourable from last year.

CONCLUSION

This report define the importance of financial accounts of organisation in order to achieve

financial effectiveness. Better optimisation of financial resources with the help of financial

accounts defined in this context. Concept of financial accounts and management accounts in

organisational context differentiated in this report. Significance of financial information for

group of stake holders also defined in this report. Purpose of financial statements for non profit

and profit organisation and financial performance of organisation analysed with the use of ratios

analysis. A summarised report is presented to elaborate financial performance of organisation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Robb, C.A. and Woodyard, A., 2011. Financial knowledge and best practice behavior.

Smith, W.K., 2014. Dynamic decision making: A model of senior leaders managing strategic

paradoxes. Academy of Management Journal. 57(6). pp.1592-1623.

Conway, J.B., 2013. A course in functional analysis (Vol. 96). Springer Science & Business

Media.

Epstein, M. J. and Buhovac, A. R., 2014. Making sustainability work: Best practices in

managing and measuring corporate social, environmental, and economic impacts.

Berrett-Koehler Publishers.Petty, J. W. and et. al., 2015. Financial management: Principles and

applications. Pearson Higher Education AU.

Finkler, S. A. and et. al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Lusardi, A. and Mitchell, O. S., 2014. The economic importance of financial literacy: Theory

and evidence. Journal of Economic Literature. 52(1). pp.5-44.

McKinney, J. B., 2015. Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Online

Financial planning meaning and definition, 2017. [Online]. Available through:

<https://www.managementstudyguide.com/financial-planning.htm>.

9

Books and Journals:

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Robb, C.A. and Woodyard, A., 2011. Financial knowledge and best practice behavior.

Smith, W.K., 2014. Dynamic decision making: A model of senior leaders managing strategic

paradoxes. Academy of Management Journal. 57(6). pp.1592-1623.

Conway, J.B., 2013. A course in functional analysis (Vol. 96). Springer Science & Business

Media.

Epstein, M. J. and Buhovac, A. R., 2014. Making sustainability work: Best practices in

managing and measuring corporate social, environmental, and economic impacts.

Berrett-Koehler Publishers.Petty, J. W. and et. al., 2015. Financial management: Principles and

applications. Pearson Higher Education AU.

Finkler, S. A. and et. al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Lusardi, A. and Mitchell, O. S., 2014. The economic importance of financial literacy: Theory

and evidence. Journal of Economic Literature. 52(1). pp.5-44.

McKinney, J. B., 2015. Effective financial management in public and nonprofit agencies. ABC-

CLIO.

Online

Financial planning meaning and definition, 2017. [Online]. Available through:

<https://www.managementstudyguide.com/financial-planning.htm>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.