Financial Resources Management in Health and Social Care Sector

VerifiedAdded on 2020/01/15

|13

|4336

|200

Report

AI Summary

This report delves into the intricacies of managing financial resources within the healthcare sector, using the Mid-Staffordshire case as a foundation. It begins by outlining the principles of costing and business control systems, emphasizing their importance in financial management. The report then explores the information required to effectively manage financial resources, including cash flow, budgeting, and regulatory requirements. It examines diverse income sources, such as government budgets and prescription charges, and analyzes factors influencing financial resource availability. The report further discusses different types of budget expenditures and evaluates systems for managing financial resources, along with decision-making processes. It also assesses budget monitoring arrangements and the impact of financial considerations on individuals and services, concluding with recommendations for improvement. The report provides a detailed analysis of the financial aspects involved in running a healthcare organization.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MANAGING FINANCIAL RESOURCES....................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Principles of costing and business control system,................................................................1

1.2 Information needed to hospital to manage its financial resources.........................................2

1.3 Regulatory requirements for managing financial resources..................................................3

TASK 2............................................................................................................................................4

2.1 Diverse sources of income encountered in health and social care.........................................4

2.2 Factors influencing the availability of financial resources in social and health care

organisation..................................................................................................................................4

2.3 Different types of budgets expenditure in health and social care organisation.....................5

TASK 3............................................................................................................................................7

TASK 4............................................................................................................................................7

1.4 Evaluation of the system for managing financial resources in health or care organisation...7

2.4 Evaluation of how decisions about expenditure are made within a health or social care

organisation..................................................................................................................................7

3.3 Evaluation of budget monitoring arrangements....................................................................8

4.1 Identify information required to make financial decisions....................................................8

4.2 Relationship between a health and social care service delivered, costs and expenditure....9

4.3 Evaluation of how financial considerations impact upon an individual................................9

4.4 Ways to improve the health and social care service through changes to financial systems

and processes...............................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

MANAGING FINANCIAL RESOURCES....................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Principles of costing and business control system,................................................................1

1.2 Information needed to hospital to manage its financial resources.........................................2

1.3 Regulatory requirements for managing financial resources..................................................3

TASK 2............................................................................................................................................4

2.1 Diverse sources of income encountered in health and social care.........................................4

2.2 Factors influencing the availability of financial resources in social and health care

organisation..................................................................................................................................4

2.3 Different types of budgets expenditure in health and social care organisation.....................5

TASK 3............................................................................................................................................7

TASK 4............................................................................................................................................7

1.4 Evaluation of the system for managing financial resources in health or care organisation...7

2.4 Evaluation of how decisions about expenditure are made within a health or social care

organisation..................................................................................................................................7

3.3 Evaluation of budget monitoring arrangements....................................................................8

4.1 Identify information required to make financial decisions....................................................8

4.2 Relationship between a health and social care service delivered, costs and expenditure....9

4.3 Evaluation of how financial considerations impact upon an individual................................9

4.4 Ways to improve the health and social care service through changes to financial systems

and processes...............................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial resource management refers to the planning, organising, directing and

controlling of all the financial activities that take place within business organisation such as

utilization of resources and its procurement. Mid-Staffordshire is the foundation trust which is

succeeding two hospitals in Staffordshire, England. This trust was established in 1993.

Therefore, in the following report principles of costing, business control system and various

regulatory systems are measured that are required for managing financial resources is interpreted

(Brooks and et.al, 2012). In addition to these factors that affects the availability of financial

resources in health and social care is mentioned. Along with this, some of the actions that can be

taken by the company in order to overcome various suspected frauds. At last, in this report,

systems have been evaluated and various budgets are monitored with an aim to evaluate the

arrangements in health and social care.

TASK 1

1.1 Principles of costing and business control system,

As per the given scenario, some of the principles of costing have been identified in health

and social care center. Principles of costing are as follows:

Cost of the company is always related to itsorigin: Cost and origin have direct

relationship. Both of them are equally proportionate with each other. Cost that can be incurred by

Mid- Staffordshire depends on the nature of the allocation and analysis of figures and resources.

Past cost are included at the time of calculating new costs: Another principle of costing

says that no cost that is related to past will not be included at the time of calculating new future

cost. As per this principle, if past cost has future considerations, then achieving that future cost

can create problem for the company (Siano, Kitchenand Confetto, 2010).

In costing Abnormal cost incurred by the company is not charged: The abnormal cost that

can be beard by the company due to theft or fire will not be included in future cost. Only the

normal cost that is related with the manufacturing should be charged by the company at cost

centers.

Business control system

Financial resource management refers to the planning, organising, directing and

controlling of all the financial activities that take place within business organisation such as

utilization of resources and its procurement. Mid-Staffordshire is the foundation trust which is

succeeding two hospitals in Staffordshire, England. This trust was established in 1993.

Therefore, in the following report principles of costing, business control system and various

regulatory systems are measured that are required for managing financial resources is interpreted

(Brooks and et.al, 2012). In addition to these factors that affects the availability of financial

resources in health and social care is mentioned. Along with this, some of the actions that can be

taken by the company in order to overcome various suspected frauds. At last, in this report,

systems have been evaluated and various budgets are monitored with an aim to evaluate the

arrangements in health and social care.

TASK 1

1.1 Principles of costing and business control system,

As per the given scenario, some of the principles of costing have been identified in health

and social care center. Principles of costing are as follows:

Cost of the company is always related to itsorigin: Cost and origin have direct

relationship. Both of them are equally proportionate with each other. Cost that can be incurred by

Mid- Staffordshire depends on the nature of the allocation and analysis of figures and resources.

Past cost are included at the time of calculating new costs: Another principle of costing

says that no cost that is related to past will not be included at the time of calculating new future

cost. As per this principle, if past cost has future considerations, then achieving that future cost

can create problem for the company (Siano, Kitchenand Confetto, 2010).

In costing Abnormal cost incurred by the company is not charged: The abnormal cost that

can be beard by the company due to theft or fire will not be included in future cost. Only the

normal cost that is related with the manufacturing should be charged by the company at cost

centers.

Business control system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business control system is the concept that is considered by the company at the time of

managing the internal and external environment of the entity. In addition to this, it is also used

by the company to make an internal environment corruption free and discourages embezzlement

activities that are taken into considerations by management and staff (Teruya and Pourajali,

2009).In addition to this, it is used by the company in order to undertake the recruitment

procedure with an aim to select thehighly competent staff. In order to properly implement the

business control system, Mid Staffordshire takes into considerations various policies. These

policies assist the company to provide training to employees with an aim to achieve integrity.

In short, it can be said that costing and business control system help the company in

conducting cost benefits analysis, monitoring financial information, calculating profit and break

even analysis, controlling cost andincome (Strebel, 2011).

1.2 Information needed to hospital to manage its financial resources

There are variety of information that are required by the social and health care industry in

order to manage all its financial resources in an effective manner. Mid-Staffordshire requires

information that is related to the management of cash flow and working capital. Wants of an

organisation depend on its operational activities, managerial and financial activities (Theeke and

Mitchell, 2008). Various organisational activities that take place within an organisation help the

company in determining the allotment of financial resources:

Budgets that are prepared by the organisation includes several things through which

financial aspects can be managed. In order to achieve the information that is associated to

the finance includes various crises that are related to insolvency advices and cash flow.

In addition to this, Mid-Staffordshire hospital also requires the retrieval of full costs, bad

debts, cash flow forecasting, and allocation of assets (Elearn, 2013).

Along with this, Mid-Staffordshire hospital is also required to have the information about

the fund that is received from the customers, charity received by the government and

non-government enterprises and so on.

Company is required to prepare future development plans in order to estimate the cost

and revenue that is required by the company.

Hospital is also required to plan purchase of fixed assets along with its cost.

In addition to this, Mid-Staffordshire hospital is required to analyse the repayment of loan

that was taken before and other financial facilities. Therefore, these are some of the

2

managing the internal and external environment of the entity. In addition to this, it is also used

by the company to make an internal environment corruption free and discourages embezzlement

activities that are taken into considerations by management and staff (Teruya and Pourajali,

2009).In addition to this, it is used by the company in order to undertake the recruitment

procedure with an aim to select thehighly competent staff. In order to properly implement the

business control system, Mid Staffordshire takes into considerations various policies. These

policies assist the company to provide training to employees with an aim to achieve integrity.

In short, it can be said that costing and business control system help the company in

conducting cost benefits analysis, monitoring financial information, calculating profit and break

even analysis, controlling cost andincome (Strebel, 2011).

1.2 Information needed to hospital to manage its financial resources

There are variety of information that are required by the social and health care industry in

order to manage all its financial resources in an effective manner. Mid-Staffordshire requires

information that is related to the management of cash flow and working capital. Wants of an

organisation depend on its operational activities, managerial and financial activities (Theeke and

Mitchell, 2008). Various organisational activities that take place within an organisation help the

company in determining the allotment of financial resources:

Budgets that are prepared by the organisation includes several things through which

financial aspects can be managed. In order to achieve the information that is associated to

the finance includes various crises that are related to insolvency advices and cash flow.

In addition to this, Mid-Staffordshire hospital also requires the retrieval of full costs, bad

debts, cash flow forecasting, and allocation of assets (Elearn, 2013).

Along with this, Mid-Staffordshire hospital is also required to have the information about

the fund that is received from the customers, charity received by the government and

non-government enterprises and so on.

Company is required to prepare future development plans in order to estimate the cost

and revenue that is required by the company.

Hospital is also required to plan purchase of fixed assets along with its cost.

In addition to this, Mid-Staffordshire hospital is required to analyse the repayment of loan

that was taken before and other financial facilities. Therefore, these are some of the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information which is required by the company to manage the financial resources

available with the company in the future time period (Gibson, 2008). In regard to this,

management of social and health care need to analyse various information like bank

overdraft that can be obtained by the company, short term investments and cash that Mid-

Staffordshire holds in future.

1.3 Regulatory requirements for managing financial resources

There are different types of regulatory requirements that can be faced by mid-

Staffordshire hospital at the time of management of resources and are as follows:

1. Monitor: Monitoring is acting as a regulatory mechanism inhealth and social care centres

at England. This body considers the responsibility of monitoring, authorising and

regulating various financial trust. Main roles of this trust are to analyse the quality of

care that can be considered by the company (Khamees, Al-Fayoumiand Al-Thuneibat,

2010). In addition to this, monitoring also indicated the health and safety of the patient

that provide patient’s protection inrespect to anti-competitive behaviour which are

against the interest of the patients.

2. The Care Act, 2014: In order to analyse thestatutory role of the general Inspector of

hospital, chief inspector of adult Social care and general practice the care act, 2014 was

established. According to this act, the very social and health care centres are liable for

the punishment if they try to supply or publish any hazardous and harmful products

(Grieve, 2013).

3. The Health and Social Care Act, 2012: Formation of this act was proving to be

beneficial for the whole system of the national health services. This act is mainly

responsible for the development of the role of monitor as a sector regulator. In regard to

this, a new trust named health watch England was developed for the welfare of the

patients. This act has also introduced various provisions about the national health

services commission board and clinical commissioning groups.

4. Care Quality Commission: It is the regulatory authority that is working in UK and is

handling all the activities related to health and social care.

Therefore, formation of above mention acts and commission help the country to avoid the

situation that occur with Victoria Climbie, a 18 year old girl, who died with 128 injuries given by

her Aunt. Similarly there is another related case of Baby P that takes place in 2007 (Gibson,

3

available with the company in the future time period (Gibson, 2008). In regard to this,

management of social and health care need to analyse various information like bank

overdraft that can be obtained by the company, short term investments and cash that Mid-

Staffordshire holds in future.

1.3 Regulatory requirements for managing financial resources

There are different types of regulatory requirements that can be faced by mid-

Staffordshire hospital at the time of management of resources and are as follows:

1. Monitor: Monitoring is acting as a regulatory mechanism inhealth and social care centres

at England. This body considers the responsibility of monitoring, authorising and

regulating various financial trust. Main roles of this trust are to analyse the quality of

care that can be considered by the company (Khamees, Al-Fayoumiand Al-Thuneibat,

2010). In addition to this, monitoring also indicated the health and safety of the patient

that provide patient’s protection inrespect to anti-competitive behaviour which are

against the interest of the patients.

2. The Care Act, 2014: In order to analyse thestatutory role of the general Inspector of

hospital, chief inspector of adult Social care and general practice the care act, 2014 was

established. According to this act, the very social and health care centres are liable for

the punishment if they try to supply or publish any hazardous and harmful products

(Grieve, 2013).

3. The Health and Social Care Act, 2012: Formation of this act was proving to be

beneficial for the whole system of the national health services. This act is mainly

responsible for the development of the role of monitor as a sector regulator. In regard to

this, a new trust named health watch England was developed for the welfare of the

patients. This act has also introduced various provisions about the national health

services commission board and clinical commissioning groups.

4. Care Quality Commission: It is the regulatory authority that is working in UK and is

handling all the activities related to health and social care.

Therefore, formation of above mention acts and commission help the country to avoid the

situation that occur with Victoria Climbie, a 18 year old girl, who died with 128 injuries given by

her Aunt. Similarly there is another related case of Baby P that takes place in 2007 (Gibson,

3

2008). In this case, a 17 year old boy died due to the carelessness of the doctors. They were not

able to find out the injury of a boy even after the completion of 48 hours which in turn results in

the death of a child.

TASK 2

2.1 Diverse sources of income encountered in health and social care

Some of the sources through which Mid-Stafford shire can raise its finance are as

follows:- Budgets from the government: Government of England prepares budgets for NHS every

year. A certain amount is fixed by the government for use. Latest confined budgets are

£100.6billion. Every nation which is following under European Union is free to decide

how much capital they want to spend (Guilding, 2007). This is one of trustworthy sources

of finance through which Mid-Staffordshire can raise its capital because it comes from

the legal bodies. Central taxation UK: This is one of the important sources through which large amount of

income can be raised from health and social care enterprises. The tax that is paid by the

citizen of the country is utilized as financial resources for the development of these firms.

This is one of the stable sources because taxes are paid by the citizens on a regular basis. Prescription charges: By collecting the prescription charges, Mid-Stafford Shire can

raise its capital. At present in England, every patient is paying the prescription charges of

£8.20 at the time of meeting the doctor. They collect these charges on the drugs and

medicines that are suggested by them (Khamees, Al-Fayoumi and Al-Thuneibat, 2010).

Other sources: In regard to the above mentioned regular options, there are many more

methods that can be used by the company to finance. Mid-Staffordshire can charge

further income from the persons who are utilizing the car parking facility and telephonic

services. In addition to this, company can also charge for seeing overseas patients and

customers.

2.2 Factors influencing the availability of financial resources in social and health care

organisation

Private finance: - This is the source that has been used by the government over past 2

decades in order to develop health and social facilities. It is the method of raising capital from

4

able to find out the injury of a boy even after the completion of 48 hours which in turn results in

the death of a child.

TASK 2

2.1 Diverse sources of income encountered in health and social care

Some of the sources through which Mid-Stafford shire can raise its finance are as

follows:- Budgets from the government: Government of England prepares budgets for NHS every

year. A certain amount is fixed by the government for use. Latest confined budgets are

£100.6billion. Every nation which is following under European Union is free to decide

how much capital they want to spend (Guilding, 2007). This is one of trustworthy sources

of finance through which Mid-Staffordshire can raise its capital because it comes from

the legal bodies. Central taxation UK: This is one of the important sources through which large amount of

income can be raised from health and social care enterprises. The tax that is paid by the

citizen of the country is utilized as financial resources for the development of these firms.

This is one of the stable sources because taxes are paid by the citizens on a regular basis. Prescription charges: By collecting the prescription charges, Mid-Stafford Shire can

raise its capital. At present in England, every patient is paying the prescription charges of

£8.20 at the time of meeting the doctor. They collect these charges on the drugs and

medicines that are suggested by them (Khamees, Al-Fayoumi and Al-Thuneibat, 2010).

Other sources: In regard to the above mentioned regular options, there are many more

methods that can be used by the company to finance. Mid-Staffordshire can charge

further income from the persons who are utilizing the car parking facility and telephonic

services. In addition to this, company can also charge for seeing overseas patients and

customers.

2.2 Factors influencing the availability of financial resources in social and health care

organisation

Private finance: - This is the source that has been used by the government over past 2

decades in order to develop health and social facilities. It is the method of raising capital from

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

private sources not from public. These private finance imitative includes government that is

borrowing from private sector for the development of hospital and other care centres (Helfert,

2004).

Government policies and funding priorities: - The present long term economic plan

reflects the value of a nation. Government of the nation has the responsibility to pass out an

affordable level of debts to the next generation. In addition to this government should make an

efforts to eliminate the deficit in a balanced and sensible manner (Atrilland McLaney, 2007).

This in turn will help the government in spending more on the development of NHS sector and to

reduce the amount of income tax for 30 million working persons. In addition to this capital can

also be available from private banks which in turn will help company to get high and long term

loans.

Agency objectives and policies:- The department of social and health care in UK alter the

enterprises to provide various services according to the set priorities. All these department are

required to work in a coordination with the government in order to achieve the success. The

Secretary of State for health plays a main role in assuring that whole health industry works

together to order to fulfil the requirements of the patients (Chapman, 2011).

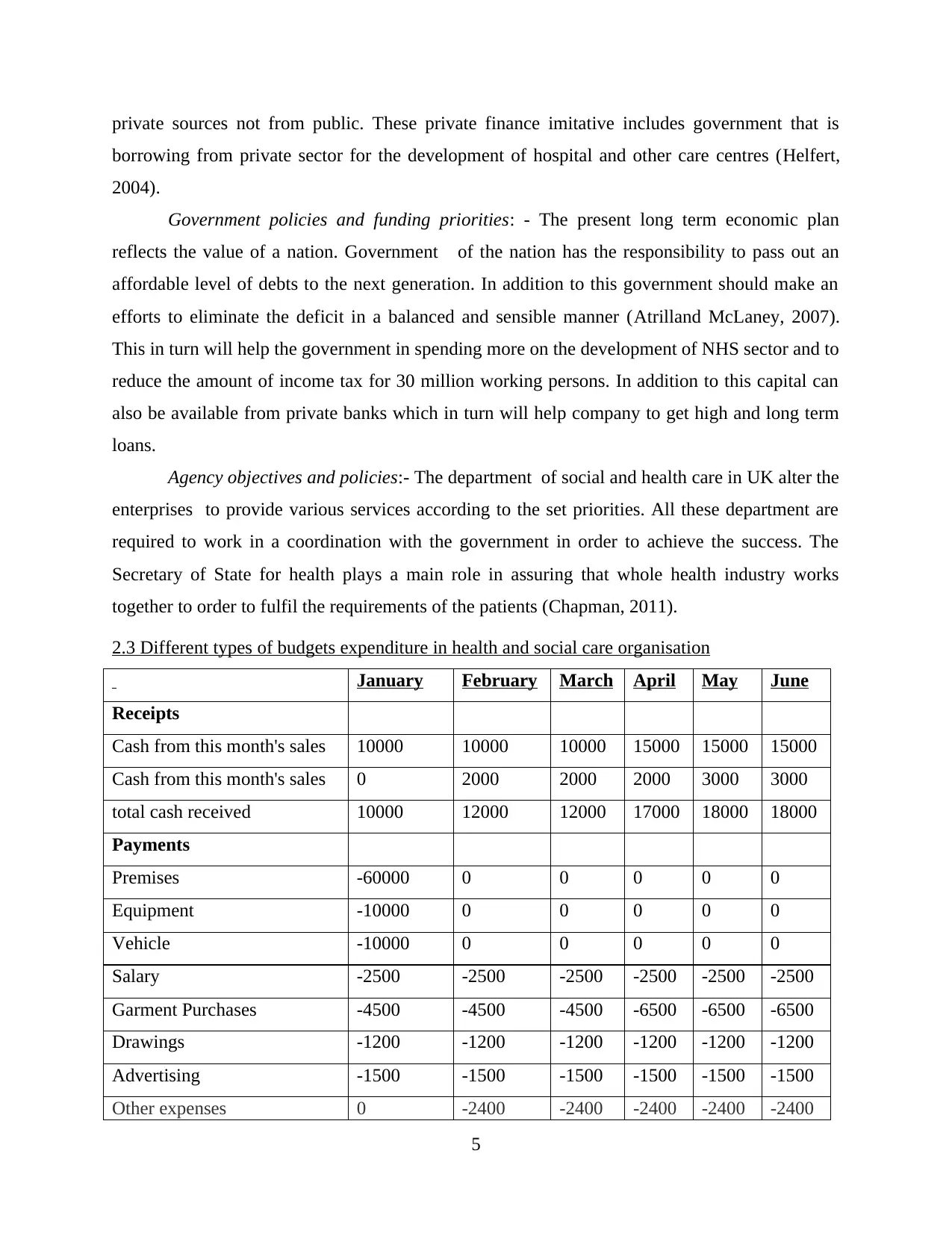

2.3 Different types of budgets expenditure in health and social care organisation

January February March April May June

Receipts

Cash from this month's sales 10000 10000 10000 15000 15000 15000

Cash from this month's sales 0 2000 2000 2000 3000 3000

total cash received 10000 12000 12000 17000 18000 18000

Payments

Premises -60000 0 0 0 0 0

Equipment -10000 0 0 0 0 0

Vehicle -10000 0 0 0 0 0

Salary -2500 -2500 -2500 -2500 -2500 -2500

Garment Purchases -4500 -4500 -4500 -6500 -6500 -6500

Drawings -1200 -1200 -1200 -1200 -1200 -1200

Advertising -1500 -1500 -1500 -1500 -1500 -1500

Other expenses 0 -2400 -2400 -2400 -2400 -2400

5

borrowing from private sector for the development of hospital and other care centres (Helfert,

2004).

Government policies and funding priorities: - The present long term economic plan

reflects the value of a nation. Government of the nation has the responsibility to pass out an

affordable level of debts to the next generation. In addition to this government should make an

efforts to eliminate the deficit in a balanced and sensible manner (Atrilland McLaney, 2007).

This in turn will help the government in spending more on the development of NHS sector and to

reduce the amount of income tax for 30 million working persons. In addition to this capital can

also be available from private banks which in turn will help company to get high and long term

loans.

Agency objectives and policies:- The department of social and health care in UK alter the

enterprises to provide various services according to the set priorities. All these department are

required to work in a coordination with the government in order to achieve the success. The

Secretary of State for health plays a main role in assuring that whole health industry works

together to order to fulfil the requirements of the patients (Chapman, 2011).

2.3 Different types of budgets expenditure in health and social care organisation

January February March April May June

Receipts

Cash from this month's sales 10000 10000 10000 15000 15000 15000

Cash from this month's sales 0 2000 2000 2000 3000 3000

total cash received 10000 12000 12000 17000 18000 18000

Payments

Premises -60000 0 0 0 0 0

Equipment -10000 0 0 0 0 0

Vehicle -10000 0 0 0 0 0

Salary -2500 -2500 -2500 -2500 -2500 -2500

Garment Purchases -4500 -4500 -4500 -6500 -6500 -6500

Drawings -1200 -1200 -1200 -1200 -1200 -1200

Advertising -1500 -1500 -1500 -1500 -1500 -1500

Other expenses 0 -2400 -2400 -2400 -2400 -2400

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

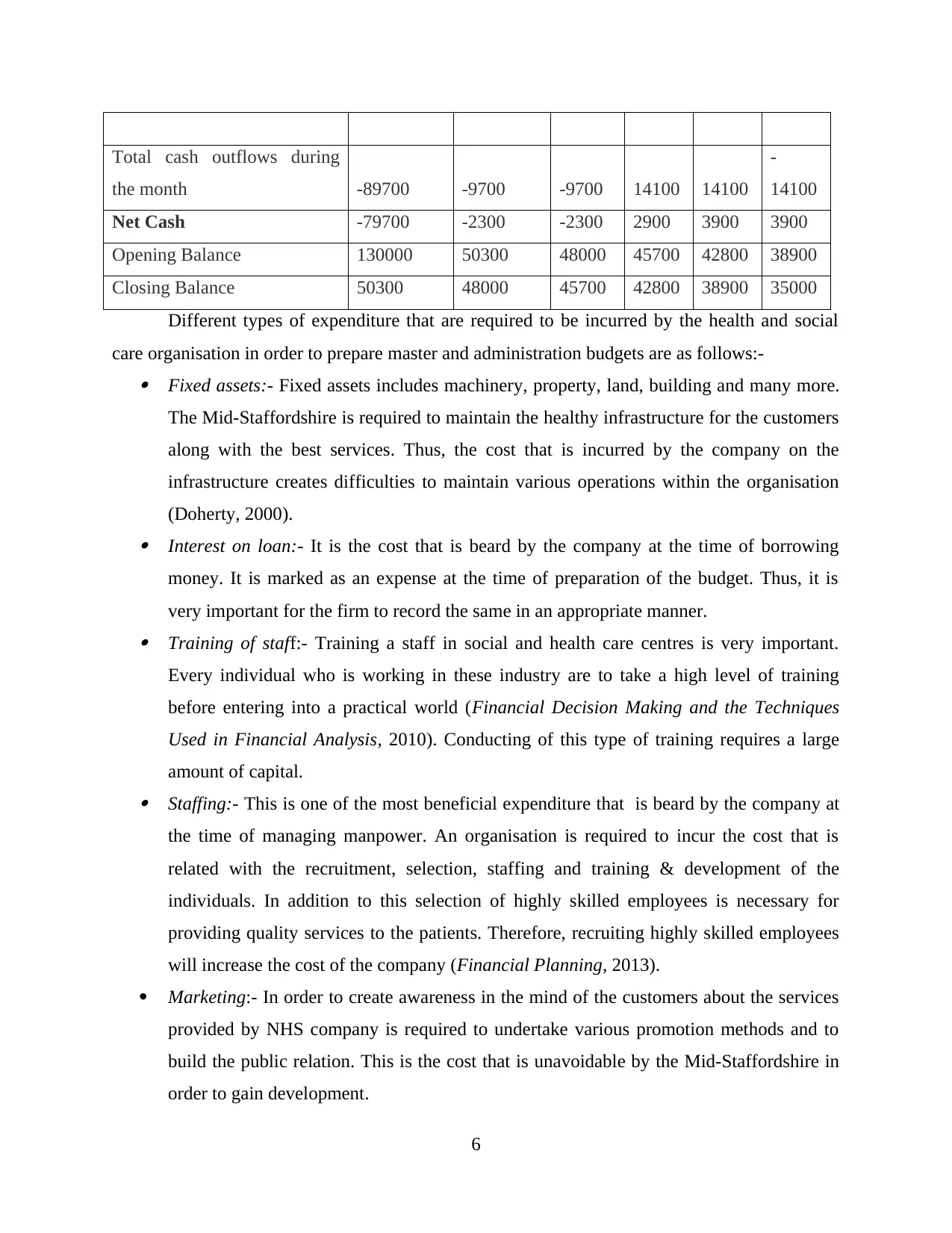

Total cash outflows during

the month -89700 -9700 -9700 14100 14100

-

14100

Net Cash -79700 -2300 -2300 2900 3900 3900

Opening Balance 130000 50300 48000 45700 42800 38900

Closing Balance 50300 48000 45700 42800 38900 35000

Different types of expenditure that are required to be incurred by the health and social

care organisation in order to prepare master and administration budgets are as follows:- Fixed assets:- Fixed assets includes machinery, property, land, building and many more.

The Mid-Staffordshire is required to maintain the healthy infrastructure for the customers

along with the best services. Thus, the cost that is incurred by the company on the

infrastructure creates difficulties to maintain various operations within the organisation

(Doherty, 2000). Interest on loan:- It is the cost that is beard by the company at the time of borrowing

money. It is marked as an expense at the time of preparation of the budget. Thus, it is

very important for the firm to record the same in an appropriate manner. Training of staff:- Training a staff in social and health care centres is very important.

Every individual who is working in these industry are to take a high level of training

before entering into a practical world (Financial Decision Making and the Techniques

Used in Financial Analysis, 2010). Conducting of this type of training requires a large

amount of capital. Staffing:- This is one of the most beneficial expenditure that is beard by the company at

the time of managing manpower. An organisation is required to incur the cost that is

related with the recruitment, selection, staffing and training & development of the

individuals. In addition to this selection of highly skilled employees is necessary for

providing quality services to the patients. Therefore, recruiting highly skilled employees

will increase the cost of the company (Financial Planning, 2013).

Marketing:- In order to create awareness in the mind of the customers about the services

provided by NHS company is required to undertake various promotion methods and to

build the public relation. This is the cost that is unavoidable by the Mid-Staffordshire in

order to gain development.

6

the month -89700 -9700 -9700 14100 14100

-

14100

Net Cash -79700 -2300 -2300 2900 3900 3900

Opening Balance 130000 50300 48000 45700 42800 38900

Closing Balance 50300 48000 45700 42800 38900 35000

Different types of expenditure that are required to be incurred by the health and social

care organisation in order to prepare master and administration budgets are as follows:- Fixed assets:- Fixed assets includes machinery, property, land, building and many more.

The Mid-Staffordshire is required to maintain the healthy infrastructure for the customers

along with the best services. Thus, the cost that is incurred by the company on the

infrastructure creates difficulties to maintain various operations within the organisation

(Doherty, 2000). Interest on loan:- It is the cost that is beard by the company at the time of borrowing

money. It is marked as an expense at the time of preparation of the budget. Thus, it is

very important for the firm to record the same in an appropriate manner. Training of staff:- Training a staff in social and health care centres is very important.

Every individual who is working in these industry are to take a high level of training

before entering into a practical world (Financial Decision Making and the Techniques

Used in Financial Analysis, 2010). Conducting of this type of training requires a large

amount of capital. Staffing:- This is one of the most beneficial expenditure that is beard by the company at

the time of managing manpower. An organisation is required to incur the cost that is

related with the recruitment, selection, staffing and training & development of the

individuals. In addition to this selection of highly skilled employees is necessary for

providing quality services to the patients. Therefore, recruiting highly skilled employees

will increase the cost of the company (Financial Planning, 2013).

Marketing:- In order to create awareness in the mind of the customers about the services

provided by NHS company is required to undertake various promotion methods and to

build the public relation. This is the cost that is unavoidable by the Mid-Staffordshire in

order to gain development.

6

TASK 3

Enclosed in ppt

TASK 4

1.4 Evaluation of the system for managing financial resources in health or care organisation

In order to manage all its financial resources Mid-Stafford shire has taken into

considerations the following systems. Detail about these systems are described below.

Financial Management system:- This system is normally composed of various tools and

process that in turn will help the organisation to control allocation of resources in an effective

manner. This system also assist the company in tracking the expenditure that are beard by the

organisation (Introduction to capital Budgeting, 2013). In addition to this this system also aid

the Mid-Stafford shire to utilise the financial report that are prepared by the firm and then

comparing the data with the budget prepare and analysing the cost.

Open Accounts:- It is the widely used system for managing financial resources. This

system has the capability to remove the burden of finance department within an organisation. In

addition to this preparation of these accounts offers large amount of information to the

management across various level that take place within an organisation in an effective manner

(Elearn, 2013). Along with this it also reduces the costs of the various activities and enhance the

financial visibility.

International Financial Reporting Standards:- IFRS is known as a common global

language for succeeding business affairs. This in turn help the company in managing and

comparing the various accounts of the company situated in international boundaries (Strebel,

2011).

2.4 Evaluationof how decisions about expenditure are made within a health or social care

organisation

Some of the factors that can be taken into considerations are at the time taking various

decisions are:-

Availability of finance:- This is one of the basic factor that is checked by the company

before making an decisions. This factor has a great impact at the time of taking various

decisions. In this case cost benefit analysis can prove to be very effective method (Gibson,

2008).

7

Enclosed in ppt

TASK 4

1.4 Evaluation of the system for managing financial resources in health or care organisation

In order to manage all its financial resources Mid-Stafford shire has taken into

considerations the following systems. Detail about these systems are described below.

Financial Management system:- This system is normally composed of various tools and

process that in turn will help the organisation to control allocation of resources in an effective

manner. This system also assist the company in tracking the expenditure that are beard by the

organisation (Introduction to capital Budgeting, 2013). In addition to this this system also aid

the Mid-Stafford shire to utilise the financial report that are prepared by the firm and then

comparing the data with the budget prepare and analysing the cost.

Open Accounts:- It is the widely used system for managing financial resources. This

system has the capability to remove the burden of finance department within an organisation. In

addition to this preparation of these accounts offers large amount of information to the

management across various level that take place within an organisation in an effective manner

(Elearn, 2013). Along with this it also reduces the costs of the various activities and enhance the

financial visibility.

International Financial Reporting Standards:- IFRS is known as a common global

language for succeeding business affairs. This in turn help the company in managing and

comparing the various accounts of the company situated in international boundaries (Strebel,

2011).

2.4 Evaluationof how decisions about expenditure are made within a health or social care

organisation

Some of the factors that can be taken into considerations are at the time taking various

decisions are:-

Availability of finance:- This is one of the basic factor that is checked by the company

before making an decisions. This factor has a great impact at the time of taking various

decisions. In this case cost benefit analysis can prove to be very effective method (Gibson,

2008).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Location:- Location also affects the decision and expenditure of the company. Selection

of right place for rendering the health and social care services is very important. Location should

be eco-friendly and free from pollution.

Government policies: - Government should develop various policies and norms in such a

way that it provides various goodness to the customers and service providers.

3.3 Evaluation of budget monitoring arrangements

The process of budget monitoring appraise the capability of the organisation who is

responsible for meeting up the financial goals as per the budget prepared. Monitoring budget

help the company in analyse the effectiveness of the financial activities that take place within

and outside the business organisation (Khamees, Al-Fayoumiand Al-Thuneibat, 2010). This

budget is approved by the Financial Advisory group of UK. In addition to this internal and

external audit perform by the organisation help them to monitor budget arrangements. Internal

audit is done by analysing the internal working conditions and external audit is done in regard to

the various laws and rules.

4.1 Identify information required to make financial decisions

The process of managing all the finance resources depends on the management of the

financial activities and analyses of the future needs that take place within an organisation. Some

of the financial documents that are required to be prepared by Mid-Stafford shire in order to

evaluate the system for managing is financial resources are as follows. This organization is

required to prepare cash flow statements, income statements, balance sheet, cost sheet, break

even analysis, annual report and International Financial Reporting Standards (Brooks and et. al,

2012). Detail of the statements that are required to be prepare are as follows:-

Financial statements:- These statements are prepared by the company in order to

manager all its activities with an aim to achieve the desired objectives. Preparation of these

statements help the company to find out its actual financial position and its flow of cash.

Budgets:- Budgets are prepared by the organisation in order to take various necessary

decisions related to finance. These budgets demonstration the prediction of income and expenses

that can take place within the business organisation (Chapman, 2011). Different types of budgets

are prepared by different organisation, some of them are cash budget, master budget, purchase

budget, sales budget, and administration budgets and so on.

8

of right place for rendering the health and social care services is very important. Location should

be eco-friendly and free from pollution.

Government policies: - Government should develop various policies and norms in such a

way that it provides various goodness to the customers and service providers.

3.3 Evaluation of budget monitoring arrangements

The process of budget monitoring appraise the capability of the organisation who is

responsible for meeting up the financial goals as per the budget prepared. Monitoring budget

help the company in analyse the effectiveness of the financial activities that take place within

and outside the business organisation (Khamees, Al-Fayoumiand Al-Thuneibat, 2010). This

budget is approved by the Financial Advisory group of UK. In addition to this internal and

external audit perform by the organisation help them to monitor budget arrangements. Internal

audit is done by analysing the internal working conditions and external audit is done in regard to

the various laws and rules.

4.1 Identify information required to make financial decisions

The process of managing all the finance resources depends on the management of the

financial activities and analyses of the future needs that take place within an organisation. Some

of the financial documents that are required to be prepared by Mid-Stafford shire in order to

evaluate the system for managing is financial resources are as follows. This organization is

required to prepare cash flow statements, income statements, balance sheet, cost sheet, break

even analysis, annual report and International Financial Reporting Standards (Brooks and et. al,

2012). Detail of the statements that are required to be prepare are as follows:-

Financial statements:- These statements are prepared by the company in order to

manager all its activities with an aim to achieve the desired objectives. Preparation of these

statements help the company to find out its actual financial position and its flow of cash.

Budgets:- Budgets are prepared by the organisation in order to take various necessary

decisions related to finance. These budgets demonstration the prediction of income and expenses

that can take place within the business organisation (Chapman, 2011). Different types of budgets

are prepared by different organisation, some of them are cash budget, master budget, purchase

budget, sales budget, and administration budgets and so on.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounts:- These accounts are used by the manager of the company with an

aim to take various necessary decisions for the benefits of the company. These accounts include

data related to strategic, risk and performance management (Doherty, 2000).

4.2 Relationship between a health and social care service delivered, costs and expenditure

Bidding process: - This is one process of the high standards and ethical value. Complete

clearness is required by health and social care service sectors before passing on the tenders of the

services. Those individual who are undertaking this process is required to make sure that nothing

goes wrong.

Transparency with stakeholder:- At the time of delivering various services, maintenance

of transparency with the stakeholder is very necessary. Patients should be clear about the

services that are provided by the company (Guilding, 2007).

4.3 Evaluation of how financial considerations impact upon an individual

There are variety of factors that affects the mind of the patient at the time of availing

various facilitates. Some of the factors are lack of human resource, sudden changes in the level

of services, issues related to the price and so on. In addition to this various problem at staffing

level can also affects the preference of the customers. Availability of these factors can create bad

impression on the mind of the customers which in turn may affects the health and social care

organisations (Teruyaand Pourajali, 2009).

4.4 Ways to improve the health and social care service through changes to financial systems and

processes.

Cost and unit computation per head should be made fir brining control. In addition to this

identification of cost at various level will help the company to provide up to date information

related to the costing to the customers. Along with this reassessment of expenditure can be made

in order to evaluate the expenses from the beginning (Siano, Kitchenand Confetto, 2010). This in

turn will give the brief idea to the company about the defects and faults that has been made

before.

CONCLUSION

From the following report it can be concluded that development of social and health care

services in increased number will lead to the development of various resources. In addition to

this external audit will act as a reflector to the company in analysing its financial position with in

9

aim to take various necessary decisions for the benefits of the company. These accounts include

data related to strategic, risk and performance management (Doherty, 2000).

4.2 Relationship between a health and social care service delivered, costs and expenditure

Bidding process: - This is one process of the high standards and ethical value. Complete

clearness is required by health and social care service sectors before passing on the tenders of the

services. Those individual who are undertaking this process is required to make sure that nothing

goes wrong.

Transparency with stakeholder:- At the time of delivering various services, maintenance

of transparency with the stakeholder is very necessary. Patients should be clear about the

services that are provided by the company (Guilding, 2007).

4.3 Evaluation of how financial considerations impact upon an individual

There are variety of factors that affects the mind of the patient at the time of availing

various facilitates. Some of the factors are lack of human resource, sudden changes in the level

of services, issues related to the price and so on. In addition to this various problem at staffing

level can also affects the preference of the customers. Availability of these factors can create bad

impression on the mind of the customers which in turn may affects the health and social care

organisations (Teruyaand Pourajali, 2009).

4.4 Ways to improve the health and social care service through changes to financial systems and

processes.

Cost and unit computation per head should be made fir brining control. In addition to this

identification of cost at various level will help the company to provide up to date information

related to the costing to the customers. Along with this reassessment of expenditure can be made

in order to evaluate the expenses from the beginning (Siano, Kitchenand Confetto, 2010). This in

turn will give the brief idea to the company about the defects and faults that has been made

before.

CONCLUSION

From the following report it can be concluded that development of social and health care

services in increased number will lead to the development of various resources. In addition to

this external audit will act as a reflector to the company in analysing its financial position with in

9

the market. At last, it can be concluded that IFRS helps in comparing and understanding the

different accounts of the company across geographical boundaries.

10

different accounts of the company across geographical boundaries.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.