Financial Management Report: Planet's Share Valuation and Investment

VerifiedAdded on 2020/12/09

|14

|4145

|326

Report

AI Summary

This financial management report delves into key aspects of corporate finance, beginning with an analysis of share valuation using the dividend growth model. The report calculates the fair price of Planet's shares under different scenarios, considering dividend growth rates and required rates of return. It examines the implications of changes in these factors on share value. The report also addresses the limitations of the dividend growth model. Furthermore, the report explores investment appraisal techniques, specifically Net Present Value (NPV) and Internal Rate of Return (IRR), to assess the economic feasibility of acquiring a machine. It provides recommendations on the project's viability and discusses the benefits and limitations of these appraisal methods, offering valuable insights for financial decision-making. The analysis includes detailed calculations and interpretations to support the recommendations.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Calculation of fair price for Planet’s shares..........................................................................1

(b) Calculation of new price for Planet’s shares.........................................................................2

(c) Problems associated with dividend growth model as a way of valuing shares.....................3

QUESTION 3...................................................................................................................................5

(a) Recommendations related to the economic feasibility of acquiring the machine.................5

(b) Benefits and limitations of various investment appraisal techniques....................................7

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Calculation of fair price for Planet’s shares..........................................................................1

(b) Calculation of new price for Planet’s shares.........................................................................2

(c) Problems associated with dividend growth model as a way of valuing shares.....................3

QUESTION 3...................................................................................................................................5

(a) Recommendations related to the economic feasibility of acquiring the machine.................5

(b) Benefits and limitations of various investment appraisal techniques....................................7

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

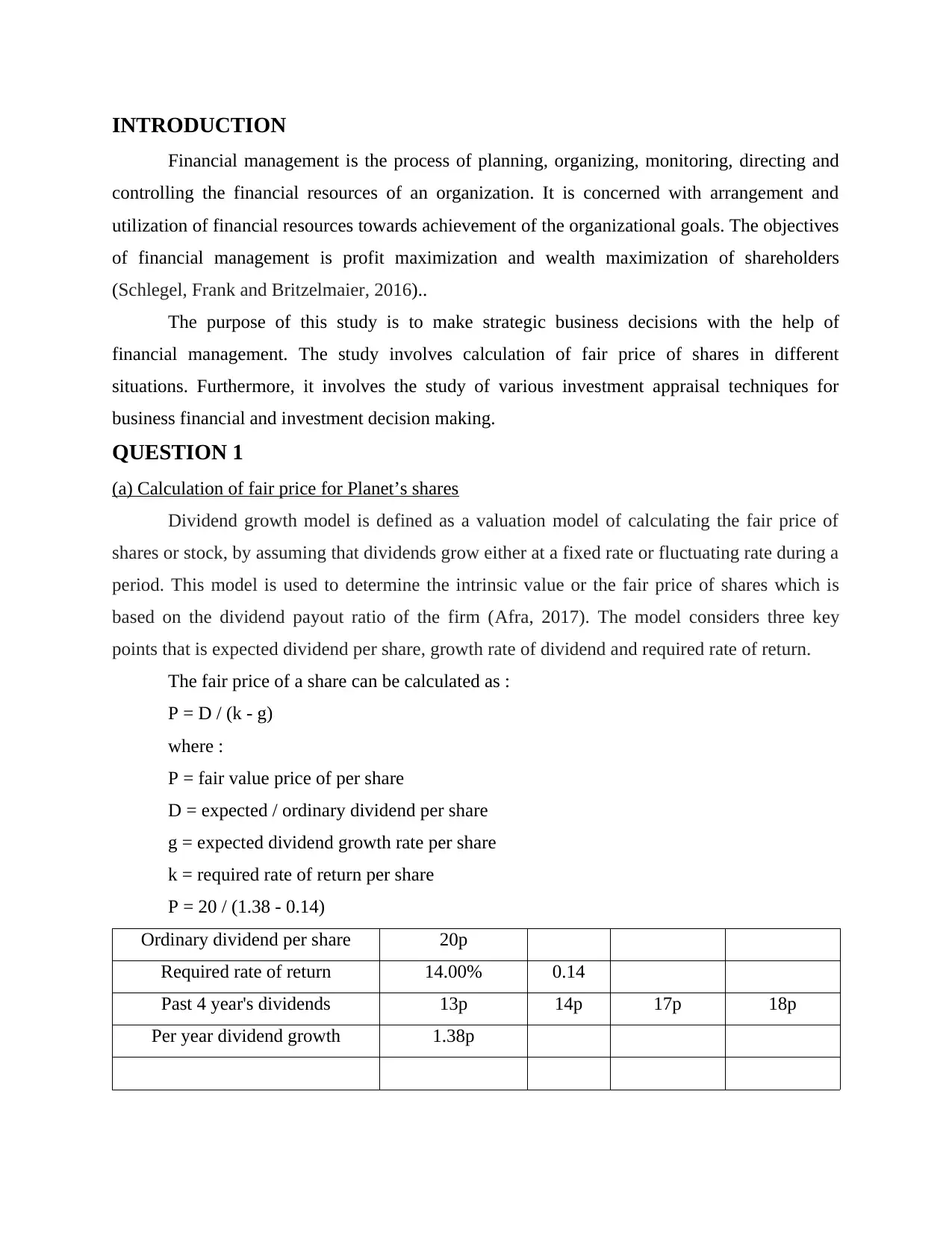

INTRODUCTION

Financial management is the process of planning, organizing, monitoring, directing and

controlling the financial resources of an organization. It is concerned with arrangement and

utilization of financial resources towards achievement of the organizational goals. The objectives

of financial management is profit maximization and wealth maximization of shareholders

(Schlegel, Frank and Britzelmaier, 2016)..

The purpose of this study is to make strategic business decisions with the help of

financial management. The study involves calculation of fair price of shares in different

situations. Furthermore, it involves the study of various investment appraisal techniques for

business financial and investment decision making.

QUESTION 1

(a) Calculation of fair price for Planet’s shares

Dividend growth model is defined as a valuation model of calculating the fair price of

shares or stock, by assuming that dividends grow either at a fixed rate or fluctuating rate during a

period. This model is used to determine the intrinsic value or the fair price of shares which is

based on the dividend payout ratio of the firm (Afra, 2017). The model considers three key

points that is expected dividend per share, growth rate of dividend and required rate of return.

The fair price of a share can be calculated as :

P = D / (k - g)

where :

P = fair value price of per share

D = expected / ordinary dividend per share

g = expected dividend growth rate per share

k = required rate of return per share

P = 20 / (1.38 - 0.14)

Ordinary dividend per share 20p

Required rate of return 14.00% 0.14

Past 4 year's dividends 13p 14p 17p 18p

Per year dividend growth 1.38p

Financial management is the process of planning, organizing, monitoring, directing and

controlling the financial resources of an organization. It is concerned with arrangement and

utilization of financial resources towards achievement of the organizational goals. The objectives

of financial management is profit maximization and wealth maximization of shareholders

(Schlegel, Frank and Britzelmaier, 2016)..

The purpose of this study is to make strategic business decisions with the help of

financial management. The study involves calculation of fair price of shares in different

situations. Furthermore, it involves the study of various investment appraisal techniques for

business financial and investment decision making.

QUESTION 1

(a) Calculation of fair price for Planet’s shares

Dividend growth model is defined as a valuation model of calculating the fair price of

shares or stock, by assuming that dividends grow either at a fixed rate or fluctuating rate during a

period. This model is used to determine the intrinsic value or the fair price of shares which is

based on the dividend payout ratio of the firm (Afra, 2017). The model considers three key

points that is expected dividend per share, growth rate of dividend and required rate of return.

The fair price of a share can be calculated as :

P = D / (k - g)

where :

P = fair value price of per share

D = expected / ordinary dividend per share

g = expected dividend growth rate per share

k = required rate of return per share

P = 20 / (1.38 - 0.14)

Ordinary dividend per share 20p

Required rate of return 14.00% 0.14

Past 4 year's dividends 13p 14p 17p 18p

Per year dividend growth 1.38p

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fair value of shares 16.13p

Fair price of share is calculated for the purpose of comparison between fair price and

current market value of share. Investors use this comparison for determining whether the

particular share is undervalued or overvalued. The investor's purpose behind this is to maximize

their total returns. The model is a quick way to get generalized indications about the value of

projected share prices (Schlegel, Frank and Britzelmaier, 2016)..

In this problem, past 4 years dividends are provided which are 13p, 14p, 17p and 18p.

The above table highlights the per year growth of dividend which is calculated as 18p / 13p that

is equal to 1.38p. Furthermore, the expected or ordinary dividend per share is 20p and the

required rate of return is 14%. The fair price of share is calculated by ordinary dividend per share

divided by the difference of required rate of return and the expected dividend growth rate per

share which gives a value of 16.13p per share. The result thus calculated is expressed as the fair

price of the share. It is the price which reflects the actual worth of a single share by considering

the factors like the growth rate of dividend payout value to investors, the expected dividend

value per share and the required rate of return (Alkaraan, 2016).

The model indicates that if there is a rise in a dividend payout value, the fair price of the

share will decrease, thus decreasing the worth of the shares. If a company pays higher amount of

dividends its value of share will diminish over time. There is an inverse relationship between

dividend payout value and fair price if the share. A growth in the dividend payout ratio devalues

the fair price of the share. The fair price of the share in the dividend growth model solely

depends upon the dividend policy of the company.

(b) Calculation of new price for Planet’s shares

In the present case Planet decides to incorporate more amount of debt in the organization

which will result in increasing the firm's financial risk and burden associated with its equity

shares. As a result, the shareholders of Planet decide to increase their required rate of return to

15.4%. The required rate of return is termed as the minimum amount of return an investor is

ready to accept for holding the stock of the company. A change in required rate of return will

lead to the change of fair price of share.

The new fair price of a share can be calculated as :

P = D / (k - g)

Fair price of share is calculated for the purpose of comparison between fair price and

current market value of share. Investors use this comparison for determining whether the

particular share is undervalued or overvalued. The investor's purpose behind this is to maximize

their total returns. The model is a quick way to get generalized indications about the value of

projected share prices (Schlegel, Frank and Britzelmaier, 2016)..

In this problem, past 4 years dividends are provided which are 13p, 14p, 17p and 18p.

The above table highlights the per year growth of dividend which is calculated as 18p / 13p that

is equal to 1.38p. Furthermore, the expected or ordinary dividend per share is 20p and the

required rate of return is 14%. The fair price of share is calculated by ordinary dividend per share

divided by the difference of required rate of return and the expected dividend growth rate per

share which gives a value of 16.13p per share. The result thus calculated is expressed as the fair

price of the share. It is the price which reflects the actual worth of a single share by considering

the factors like the growth rate of dividend payout value to investors, the expected dividend

value per share and the required rate of return (Alkaraan, 2016).

The model indicates that if there is a rise in a dividend payout value, the fair price of the

share will decrease, thus decreasing the worth of the shares. If a company pays higher amount of

dividends its value of share will diminish over time. There is an inverse relationship between

dividend payout value and fair price if the share. A growth in the dividend payout ratio devalues

the fair price of the share. The fair price of the share in the dividend growth model solely

depends upon the dividend policy of the company.

(b) Calculation of new price for Planet’s shares

In the present case Planet decides to incorporate more amount of debt in the organization

which will result in increasing the firm's financial risk and burden associated with its equity

shares. As a result, the shareholders of Planet decide to increase their required rate of return to

15.4%. The required rate of return is termed as the minimum amount of return an investor is

ready to accept for holding the stock of the company. A change in required rate of return will

lead to the change of fair price of share.

The new fair price of a share can be calculated as :

P = D / (k - g)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

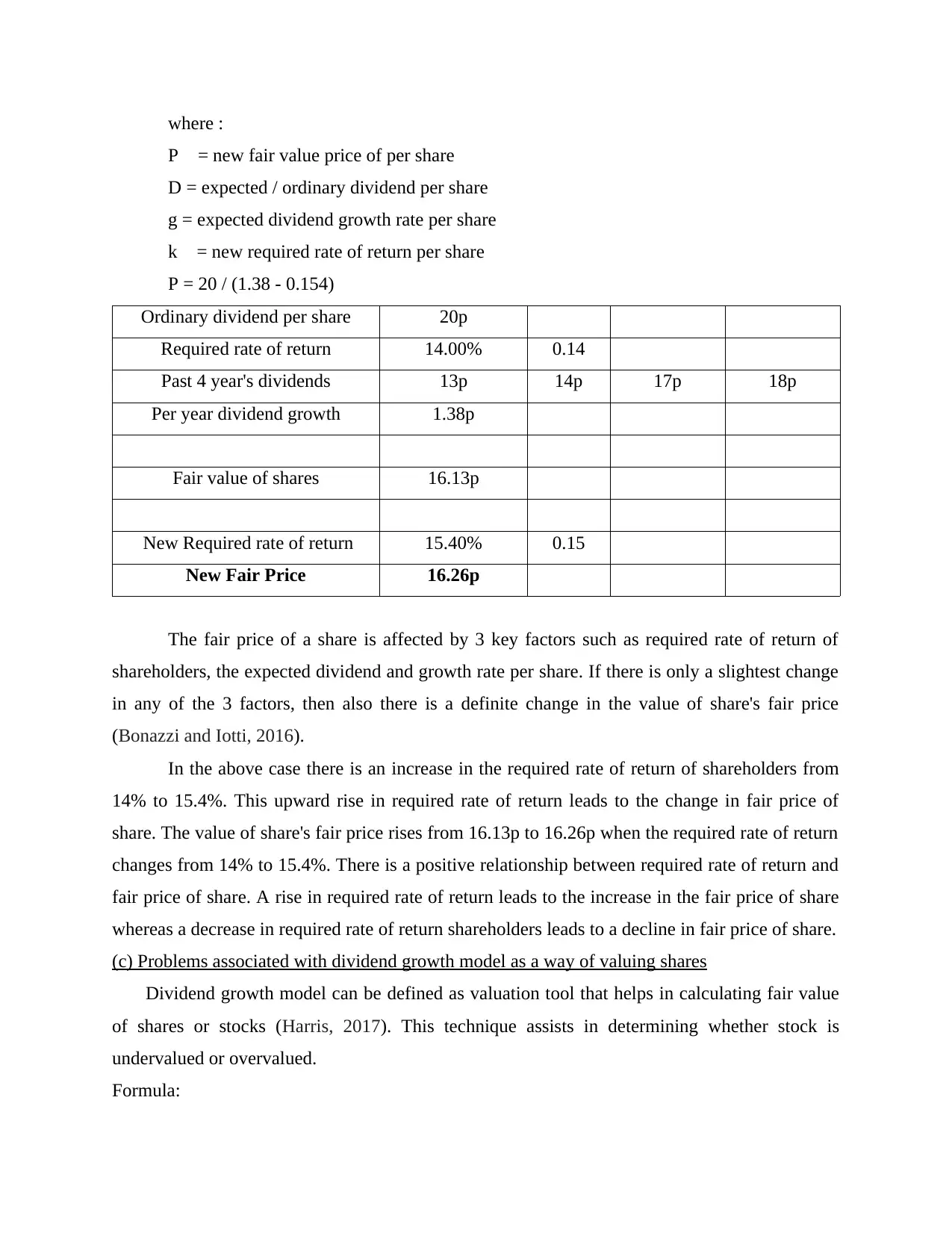

where :

P = new fair value price of per share

D = expected / ordinary dividend per share

g = expected dividend growth rate per share

k = new required rate of return per share

P = 20 / (1.38 - 0.154)

Ordinary dividend per share 20p

Required rate of return 14.00% 0.14

Past 4 year's dividends 13p 14p 17p 18p

Per year dividend growth 1.38p

Fair value of shares 16.13p

New Required rate of return 15.40% 0.15

New Fair Price 16.26p

The fair price of a share is affected by 3 key factors such as required rate of return of

shareholders, the expected dividend and growth rate per share. If there is only a slightest change

in any of the 3 factors, then also there is a definite change in the value of share's fair price

(Bonazzi and Iotti, 2016).

In the above case there is an increase in the required rate of return of shareholders from

14% to 15.4%. This upward rise in required rate of return leads to the change in fair price of

share. The value of share's fair price rises from 16.13p to 16.26p when the required rate of return

changes from 14% to 15.4%. There is a positive relationship between required rate of return and

fair price of share. A rise in required rate of return leads to the increase in the fair price of share

whereas a decrease in required rate of return shareholders leads to a decline in fair price of share.

(c) Problems associated with dividend growth model as a way of valuing shares

Dividend growth model can be defined as valuation tool that helps in calculating fair value

of shares or stocks (Harris, 2017). This technique assists in determining whether stock is

undervalued or overvalued.

Formula:

P = new fair value price of per share

D = expected / ordinary dividend per share

g = expected dividend growth rate per share

k = new required rate of return per share

P = 20 / (1.38 - 0.154)

Ordinary dividend per share 20p

Required rate of return 14.00% 0.14

Past 4 year's dividends 13p 14p 17p 18p

Per year dividend growth 1.38p

Fair value of shares 16.13p

New Required rate of return 15.40% 0.15

New Fair Price 16.26p

The fair price of a share is affected by 3 key factors such as required rate of return of

shareholders, the expected dividend and growth rate per share. If there is only a slightest change

in any of the 3 factors, then also there is a definite change in the value of share's fair price

(Bonazzi and Iotti, 2016).

In the above case there is an increase in the required rate of return of shareholders from

14% to 15.4%. This upward rise in required rate of return leads to the change in fair price of

share. The value of share's fair price rises from 16.13p to 16.26p when the required rate of return

changes from 14% to 15.4%. There is a positive relationship between required rate of return and

fair price of share. A rise in required rate of return leads to the increase in the fair price of share

whereas a decrease in required rate of return shareholders leads to a decline in fair price of share.

(c) Problems associated with dividend growth model as a way of valuing shares

Dividend growth model can be defined as valuation tool that helps in calculating fair value

of shares or stocks (Harris, 2017). This technique assists in determining whether stock is

undervalued or overvalued.

Formula:

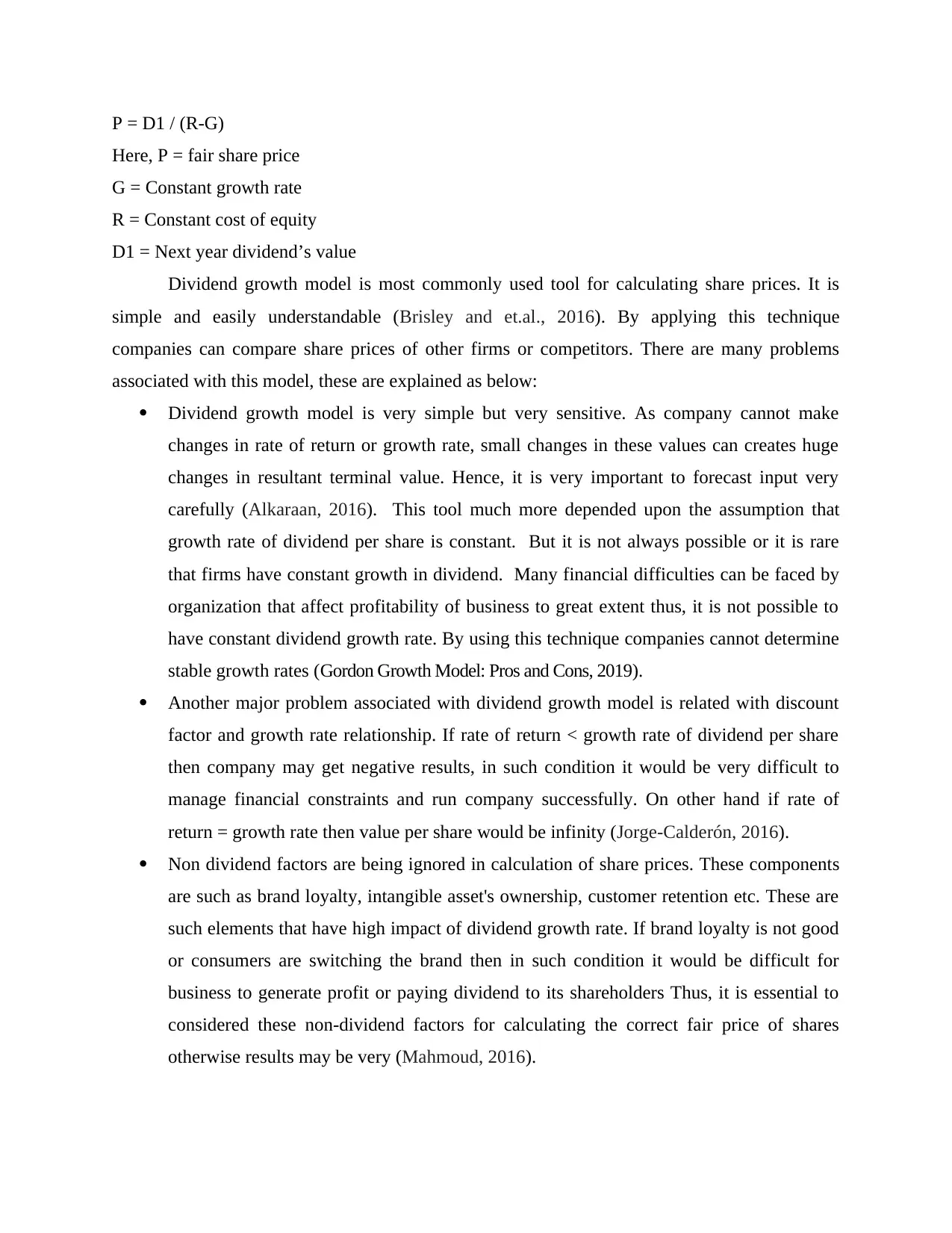

P = D1 / (R-G)

Here, P = fair share price

G = Constant growth rate

R = Constant cost of equity

D1 = Next year dividend’s value

Dividend growth model is most commonly used tool for calculating share prices. It is

simple and easily understandable (Brisley and et.al., 2016). By applying this technique

companies can compare share prices of other firms or competitors. There are many problems

associated with this model, these are explained as below:

Dividend growth model is very simple but very sensitive. As company cannot make

changes in rate of return or growth rate, small changes in these values can creates huge

changes in resultant terminal value. Hence, it is very important to forecast input very

carefully (Alkaraan, 2016). This tool much more depended upon the assumption that

growth rate of dividend per share is constant. But it is not always possible or it is rare

that firms have constant growth in dividend. Many financial difficulties can be faced by

organization that affect profitability of business to great extent thus, it is not possible to

have constant dividend growth rate. By using this technique companies cannot determine

stable growth rates (Gordon Growth Model: Pros and Cons, 2019).

Another major problem associated with dividend growth model is related with discount

factor and growth rate relationship. If rate of return < growth rate of dividend per share

then company may get negative results, in such condition it would be very difficult to

manage financial constraints and run company successfully. On other hand if rate of

return = growth rate then value per share would be infinity (Jorge-Calderón, 2016).

Non dividend factors are being ignored in calculation of share prices. These components

are such as brand loyalty, intangible asset's ownership, customer retention etc. These are

such elements that have high impact of dividend growth rate. If brand loyalty is not good

or consumers are switching the brand then in such condition it would be difficult for

business to generate profit or paying dividend to its shareholders Thus, it is essential to

considered these non-dividend factors for calculating the correct fair price of shares

otherwise results may be very (Mahmoud, 2016).

Here, P = fair share price

G = Constant growth rate

R = Constant cost of equity

D1 = Next year dividend’s value

Dividend growth model is most commonly used tool for calculating share prices. It is

simple and easily understandable (Brisley and et.al., 2016). By applying this technique

companies can compare share prices of other firms or competitors. There are many problems

associated with this model, these are explained as below:

Dividend growth model is very simple but very sensitive. As company cannot make

changes in rate of return or growth rate, small changes in these values can creates huge

changes in resultant terminal value. Hence, it is very important to forecast input very

carefully (Alkaraan, 2016). This tool much more depended upon the assumption that

growth rate of dividend per share is constant. But it is not always possible or it is rare

that firms have constant growth in dividend. Many financial difficulties can be faced by

organization that affect profitability of business to great extent thus, it is not possible to

have constant dividend growth rate. By using this technique companies cannot determine

stable growth rates (Gordon Growth Model: Pros and Cons, 2019).

Another major problem associated with dividend growth model is related with discount

factor and growth rate relationship. If rate of return < growth rate of dividend per share

then company may get negative results, in such condition it would be very difficult to

manage financial constraints and run company successfully. On other hand if rate of

return = growth rate then value per share would be infinity (Jorge-Calderón, 2016).

Non dividend factors are being ignored in calculation of share prices. These components

are such as brand loyalty, intangible asset's ownership, customer retention etc. These are

such elements that have high impact of dividend growth rate. If brand loyalty is not good

or consumers are switching the brand then in such condition it would be difficult for

business to generate profit or paying dividend to its shareholders Thus, it is essential to

considered these non-dividend factors for calculating the correct fair price of shares

otherwise results may be very (Mahmoud, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

If company is not distributing dividend (which happens many times in big organisation

whose stocks are growing well) in such condition it is very difficult to calculate dividend

growth rate thus, this model cannot apply in such kind of conditions. It is essential to

have constant growth rate, constant cost of equity, next year dividend’s value, otherwise

fair value of shares cannot be calculated by using dividend growth model (Schlegel,

Frank and Britzelmaier, 2016).

QUESTION 3

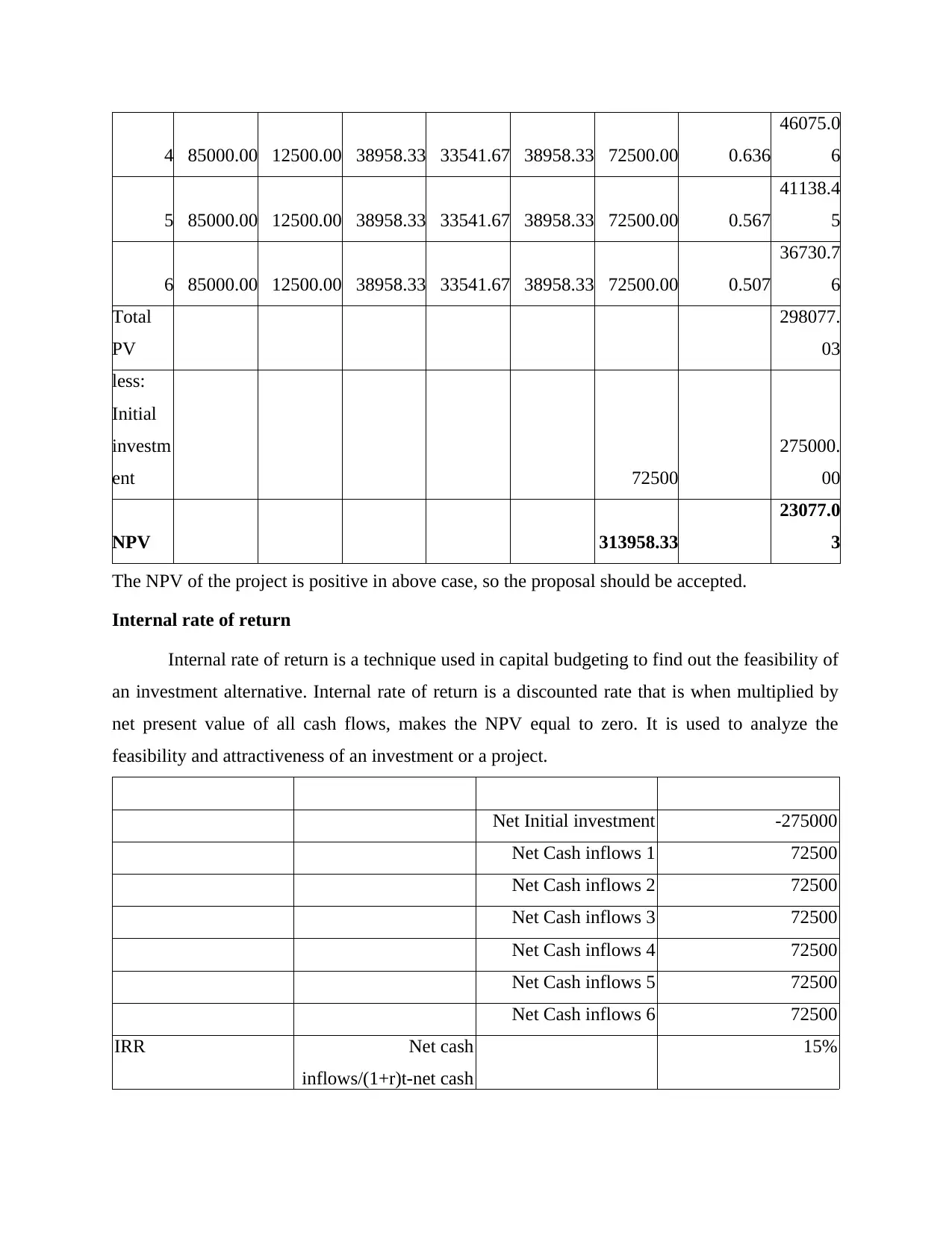

(a) Recommendations related to the economic feasibility of acquiring the machine

Net present Value

Net present value is calculated as the difference of present value of cash inflows v/s

present value of cash outflows over a period of time. NPV can be positive as well as negative. A

project can be accepted if the net present value of the project is positive. An investment

alternative with negative NPV must be rejected.

Depreciation

Machine value 275000

rate 15%

Expected life 6

38958.3333333333

Year Cash flow EBIT

add:

depreciatio

n

Net cash

flow

Discounting

factor

@12%)

Present

value

0 275000

1 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.893

64732.1

4

2 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.797

57796.5

6

3 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.712

51604.0

7

whose stocks are growing well) in such condition it is very difficult to calculate dividend

growth rate thus, this model cannot apply in such kind of conditions. It is essential to

have constant growth rate, constant cost of equity, next year dividend’s value, otherwise

fair value of shares cannot be calculated by using dividend growth model (Schlegel,

Frank and Britzelmaier, 2016).

QUESTION 3

(a) Recommendations related to the economic feasibility of acquiring the machine

Net present Value

Net present value is calculated as the difference of present value of cash inflows v/s

present value of cash outflows over a period of time. NPV can be positive as well as negative. A

project can be accepted if the net present value of the project is positive. An investment

alternative with negative NPV must be rejected.

Depreciation

Machine value 275000

rate 15%

Expected life 6

38958.3333333333

Year Cash flow EBIT

add:

depreciatio

n

Net cash

flow

Discounting

factor

@12%)

Present

value

0 275000

1 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.893

64732.1

4

2 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.797

57796.5

6

3 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.712

51604.0

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.636

46075.0

6

5 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.567

41138.4

5

6 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.507

36730.7

6

Total

PV

298077.

03

less:

Initial

investm

ent 72500

275000.

00

NPV 313958.33

23077.0

3

The NPV of the project is positive in above case, so the proposal should be accepted.

Internal rate of return

Internal rate of return is a technique used in capital budgeting to find out the feasibility of

an investment alternative. Internal rate of return is a discounted rate that is when multiplied by

net present value of all cash flows, makes the NPV equal to zero. It is used to analyze the

feasibility and attractiveness of an investment or a project.

Net Initial investment -275000

Net Cash inflows 1 72500

Net Cash inflows 2 72500

Net Cash inflows 3 72500

Net Cash inflows 4 72500

Net Cash inflows 5 72500

Net Cash inflows 6 72500

IRR Net cash

inflows/(1+r)t-net cash

15%

46075.0

6

5 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.567

41138.4

5

6 85000.00 12500.00 38958.33 33541.67 38958.33 72500.00 0.507

36730.7

6

Total

PV

298077.

03

less:

Initial

investm

ent 72500

275000.

00

NPV 313958.33

23077.0

3

The NPV of the project is positive in above case, so the proposal should be accepted.

Internal rate of return

Internal rate of return is a technique used in capital budgeting to find out the feasibility of

an investment alternative. Internal rate of return is a discounted rate that is when multiplied by

net present value of all cash flows, makes the NPV equal to zero. It is used to analyze the

feasibility and attractiveness of an investment or a project.

Net Initial investment -275000

Net Cash inflows 1 72500

Net Cash inflows 2 72500

Net Cash inflows 3 72500

Net Cash inflows 4 72500

Net Cash inflows 5 72500

Net Cash inflows 6 72500

IRR Net cash

inflows/(1+r)t-net cash

15%

outflow

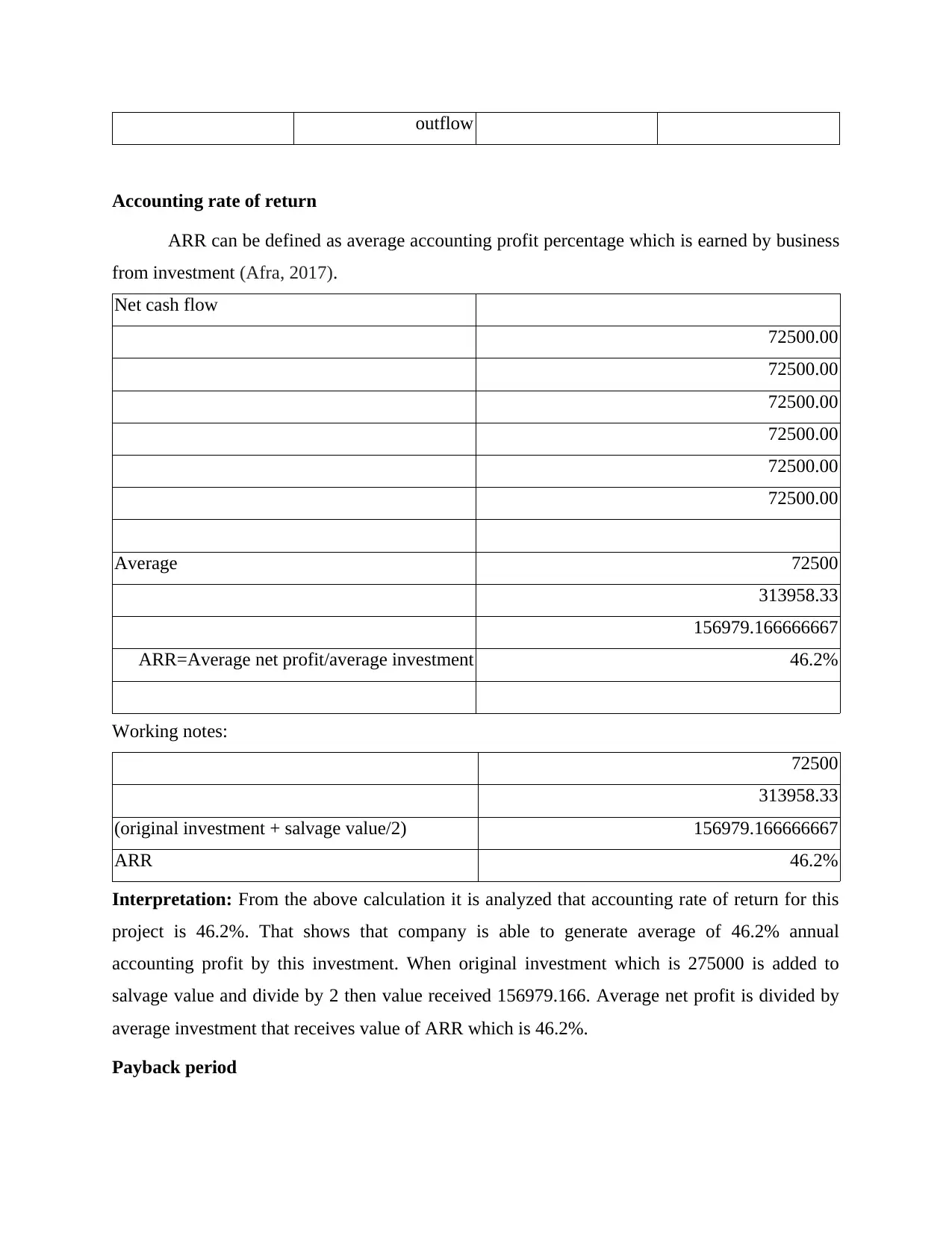

Accounting rate of return

ARR can be defined as average accounting profit percentage which is earned by business

from investment (Afra, 2017).

Net cash flow

72500.00

72500.00

72500.00

72500.00

72500.00

72500.00

Average 72500

313958.33

156979.166666667

ARR=Average net profit/average investment 46.2%

Working notes:

72500

313958.33

(original investment + salvage value/2) 156979.166666667

ARR 46.2%

Interpretation: From the above calculation it is analyzed that accounting rate of return for this

project is 46.2%. That shows that company is able to generate average of 46.2% annual

accounting profit by this investment. When original investment which is 275000 is added to

salvage value and divide by 2 then value received 156979.166. Average net profit is divided by

average investment that receives value of ARR which is 46.2%.

Payback period

Accounting rate of return

ARR can be defined as average accounting profit percentage which is earned by business

from investment (Afra, 2017).

Net cash flow

72500.00

72500.00

72500.00

72500.00

72500.00

72500.00

Average 72500

313958.33

156979.166666667

ARR=Average net profit/average investment 46.2%

Working notes:

72500

313958.33

(original investment + salvage value/2) 156979.166666667

ARR 46.2%

Interpretation: From the above calculation it is analyzed that accounting rate of return for this

project is 46.2%. That shows that company is able to generate average of 46.2% annual

accounting profit by this investment. When original investment which is 275000 is added to

salvage value and divide by 2 then value received 156979.166. Average net profit is divided by

average investment that receives value of ARR which is 46.2%.

Payback period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

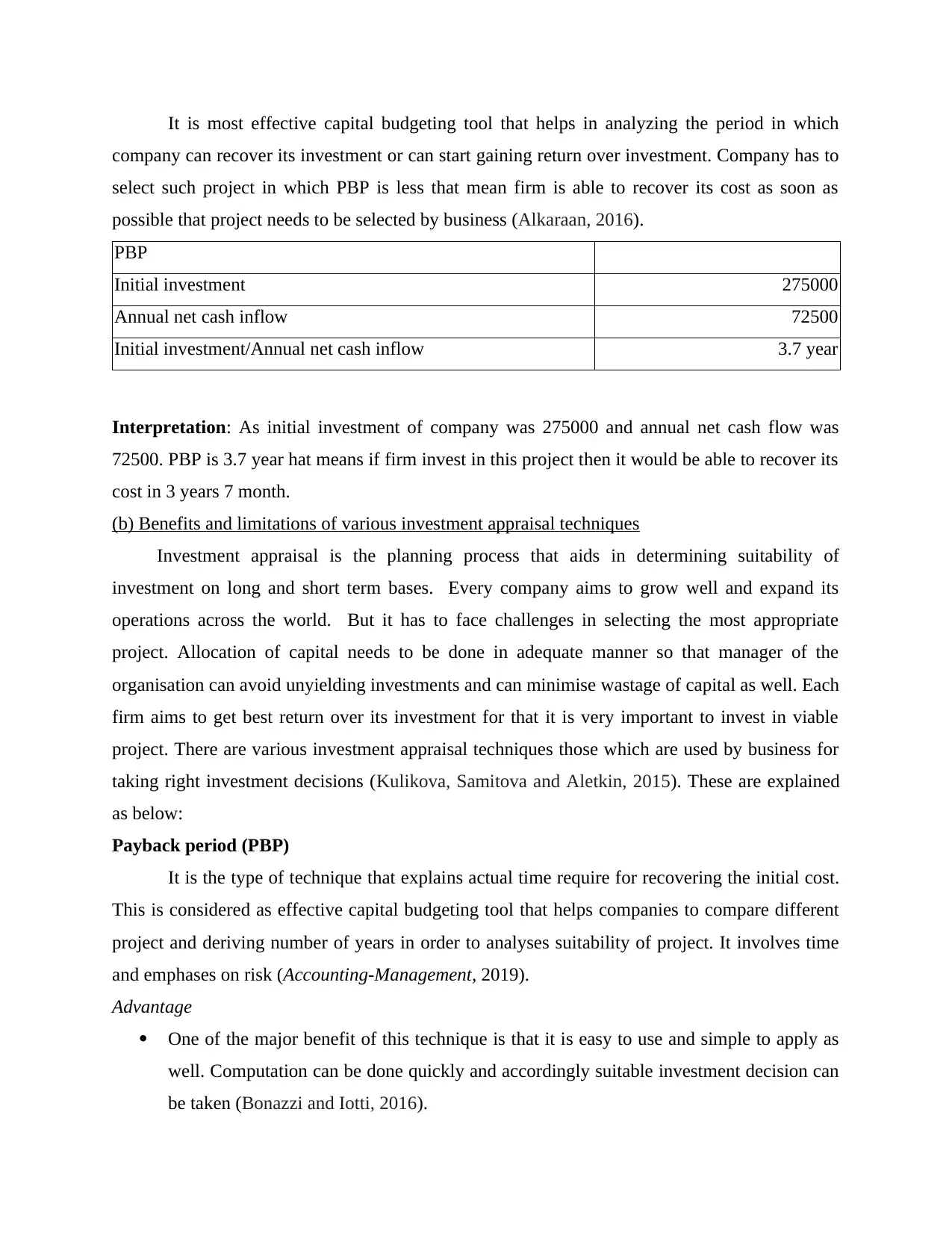

It is most effective capital budgeting tool that helps in analyzing the period in which

company can recover its investment or can start gaining return over investment. Company has to

select such project in which PBP is less that mean firm is able to recover its cost as soon as

possible that project needs to be selected by business (Alkaraan, 2016).

PBP

Initial investment 275000

Annual net cash inflow 72500

Initial investment/Annual net cash inflow 3.7 year

Interpretation: As initial investment of company was 275000 and annual net cash flow was

72500. PBP is 3.7 year hat means if firm invest in this project then it would be able to recover its

cost in 3 years 7 month.

(b) Benefits and limitations of various investment appraisal techniques

Investment appraisal is the planning process that aids in determining suitability of

investment on long and short term bases. Every company aims to grow well and expand its

operations across the world. But it has to face challenges in selecting the most appropriate

project. Allocation of capital needs to be done in adequate manner so that manager of the

organisation can avoid unyielding investments and can minimise wastage of capital as well. Each

firm aims to get best return over its investment for that it is very important to invest in viable

project. There are various investment appraisal techniques those which are used by business for

taking right investment decisions (Kulikova, Samitova and Aletkin, 2015). These are explained

as below:

Payback period (PBP)

It is the type of technique that explains actual time require for recovering the initial cost.

This is considered as effective capital budgeting tool that helps companies to compare different

project and deriving number of years in order to analyses suitability of project. It involves time

and emphases on risk (Accounting-Management, 2019).

Advantage

One of the major benefit of this technique is that it is easy to use and simple to apply as

well. Computation can be done quickly and accordingly suitable investment decision can

be taken (Bonazzi and Iotti, 2016).

company can recover its investment or can start gaining return over investment. Company has to

select such project in which PBP is less that mean firm is able to recover its cost as soon as

possible that project needs to be selected by business (Alkaraan, 2016).

PBP

Initial investment 275000

Annual net cash inflow 72500

Initial investment/Annual net cash inflow 3.7 year

Interpretation: As initial investment of company was 275000 and annual net cash flow was

72500. PBP is 3.7 year hat means if firm invest in this project then it would be able to recover its

cost in 3 years 7 month.

(b) Benefits and limitations of various investment appraisal techniques

Investment appraisal is the planning process that aids in determining suitability of

investment on long and short term bases. Every company aims to grow well and expand its

operations across the world. But it has to face challenges in selecting the most appropriate

project. Allocation of capital needs to be done in adequate manner so that manager of the

organisation can avoid unyielding investments and can minimise wastage of capital as well. Each

firm aims to get best return over its investment for that it is very important to invest in viable

project. There are various investment appraisal techniques those which are used by business for

taking right investment decisions (Kulikova, Samitova and Aletkin, 2015). These are explained

as below:

Payback period (PBP)

It is the type of technique that explains actual time require for recovering the initial cost.

This is considered as effective capital budgeting tool that helps companies to compare different

project and deriving number of years in order to analyses suitability of project. It involves time

and emphases on risk (Accounting-Management, 2019).

Advantage

One of the major benefit of this technique is that it is easy to use and simple to apply as

well. Computation can be done quickly and accordingly suitable investment decision can

be taken (Bonazzi and Iotti, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As PBP emphases more on quick return on investment thus, speedy recovery is possible.

Stressing more on liquidity objective make it unique from other investment appraisal

techniques. Possibility of loss can be minimised through obsolescence.

Limitation

Many times company receives late return on worthwhile projects but PBP ignores annual

cash flow, it only looks at the payback period and accordingly directs viability of project.

This method does not consider or ignores cash flow generated after payback period.

Profitability aspect is being ignored by PBP as it only emphases on liquidity (Miller and

Mustapha, 2016).

Accounting rate of return (ARR)

It is another investment appraisal technique that stresses more on percentage or rate of

return on investment done by business. This capital budgeting tool guides the firm whether to

invest in particular project or not. ARR always make comparison between expected profit on

invested amount and amount which is invested (Afra, 2017).

Advantage

ARR emphases on net earnings on invested project. After deducting tax and depreciation

company can get to know actual worth of any project. This is significant capital budgeting method as it is helpful in meeting with the interest of

all stakeholders and investors.

Disadvantage

Accounting rate of return ignores time value of money. If interest rate is high then it may

affect the profitability of any project hence, it is very important to consider time value of

money (Abidoye and Chan, 2016).

ARR is unable to make comparison among all projects because apart from return it

ignores all the relevant factors such as cost, time, liquidity etc.

Net present value (NPV)

Whenever companies take decision of expansion at that time NPV capital budgeting

method is used by business, as it aids in analysing present value of cash over a period of time. By

this way companies can calculate or assume profitability of particular project and take decision

accordingly. Once concerned firm has met with its financial commitments this technique

Stressing more on liquidity objective make it unique from other investment appraisal

techniques. Possibility of loss can be minimised through obsolescence.

Limitation

Many times company receives late return on worthwhile projects but PBP ignores annual

cash flow, it only looks at the payback period and accordingly directs viability of project.

This method does not consider or ignores cash flow generated after payback period.

Profitability aspect is being ignored by PBP as it only emphases on liquidity (Miller and

Mustapha, 2016).

Accounting rate of return (ARR)

It is another investment appraisal technique that stresses more on percentage or rate of

return on investment done by business. This capital budgeting tool guides the firm whether to

invest in particular project or not. ARR always make comparison between expected profit on

invested amount and amount which is invested (Afra, 2017).

Advantage

ARR emphases on net earnings on invested project. After deducting tax and depreciation

company can get to know actual worth of any project. This is significant capital budgeting method as it is helpful in meeting with the interest of

all stakeholders and investors.

Disadvantage

Accounting rate of return ignores time value of money. If interest rate is high then it may

affect the profitability of any project hence, it is very important to consider time value of

money (Abidoye and Chan, 2016).

ARR is unable to make comparison among all projects because apart from return it

ignores all the relevant factors such as cost, time, liquidity etc.

Net present value (NPV)

Whenever companies take decision of expansion at that time NPV capital budgeting

method is used by business, as it aids in analysing present value of cash over a period of time. By

this way companies can calculate or assume profitability of particular project and take decision

accordingly. Once concerned firm has met with its financial commitments this technique

measures whether there will be cash inflow or shortfall (Top 7 Investment Appraisal Techniques |

Capital Budgeting, 2019).

Advantage

It is considered as effective tool as time value of money is given importance. Risk and

cost of capital both these factors are considered on high priority, that supports business in

making correct decision of investment and receiving high return over investment.

NPV is beneficial in order to maximize value of firm and raising its profitability to great

extent. This is simple process and stockholders can clearly look upon the value generated by the

project (Makokha and et.al., 2017).

Disadvantage

If project’s life is unequal, then NPV is unable to highlight viability of investment.

Manager of the firm has to predict future cash flow hence estimation of cost of capital not

always right.

If manager of concerned firm does not have adequate knowledge of cost of capital, then it

becomes very difficult to assume future cash flow that affect final decision and

sometimes enterprise invest in wrong project that results in financial loss to business unit.

Internal rate of return (IRR)

This is the type of capital budgeting technique that measure profitability extent on

particular investment (Alkaraan, 2016). Time value of money is taken into consideration. If value

of IRR is >pre-set percentage then it is acceptable project whereas if IRR< set percentage target,

then company should not invest in that project as it is not viable. Internal rate of return is

effective tool that describes attractiveness of any project and guide firm whether to invest in that

project or not.

Advantage

Time value of money is considered in IRR no matters cash flow is uneven or even.

IRR emphases more on profitability aspect, effectiveness of project is analysed on the

bases of profit generated by that project. It is helpful in satisfying needs of shareholders as maximization of wealth of shareholders

is the main objective of IRR technique (Brisley and et.al., 2016).

Disadvantage

Capital Budgeting, 2019).

Advantage

It is considered as effective tool as time value of money is given importance. Risk and

cost of capital both these factors are considered on high priority, that supports business in

making correct decision of investment and receiving high return over investment.

NPV is beneficial in order to maximize value of firm and raising its profitability to great

extent. This is simple process and stockholders can clearly look upon the value generated by the

project (Makokha and et.al., 2017).

Disadvantage

If project’s life is unequal, then NPV is unable to highlight viability of investment.

Manager of the firm has to predict future cash flow hence estimation of cost of capital not

always right.

If manager of concerned firm does not have adequate knowledge of cost of capital, then it

becomes very difficult to assume future cash flow that affect final decision and

sometimes enterprise invest in wrong project that results in financial loss to business unit.

Internal rate of return (IRR)

This is the type of capital budgeting technique that measure profitability extent on

particular investment (Alkaraan, 2016). Time value of money is taken into consideration. If value

of IRR is >pre-set percentage then it is acceptable project whereas if IRR< set percentage target,

then company should not invest in that project as it is not viable. Internal rate of return is

effective tool that describes attractiveness of any project and guide firm whether to invest in that

project or not.

Advantage

Time value of money is considered in IRR no matters cash flow is uneven or even.

IRR emphases more on profitability aspect, effectiveness of project is analysed on the

bases of profit generated by that project. It is helpful in satisfying needs of shareholders as maximization of wealth of shareholders

is the main objective of IRR technique (Brisley and et.al., 2016).

Disadvantage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.