Financial Analysis and Budgeting Report: University Finance Module

VerifiedAdded on 2020/03/01

|14

|2121

|414

Report

AI Summary

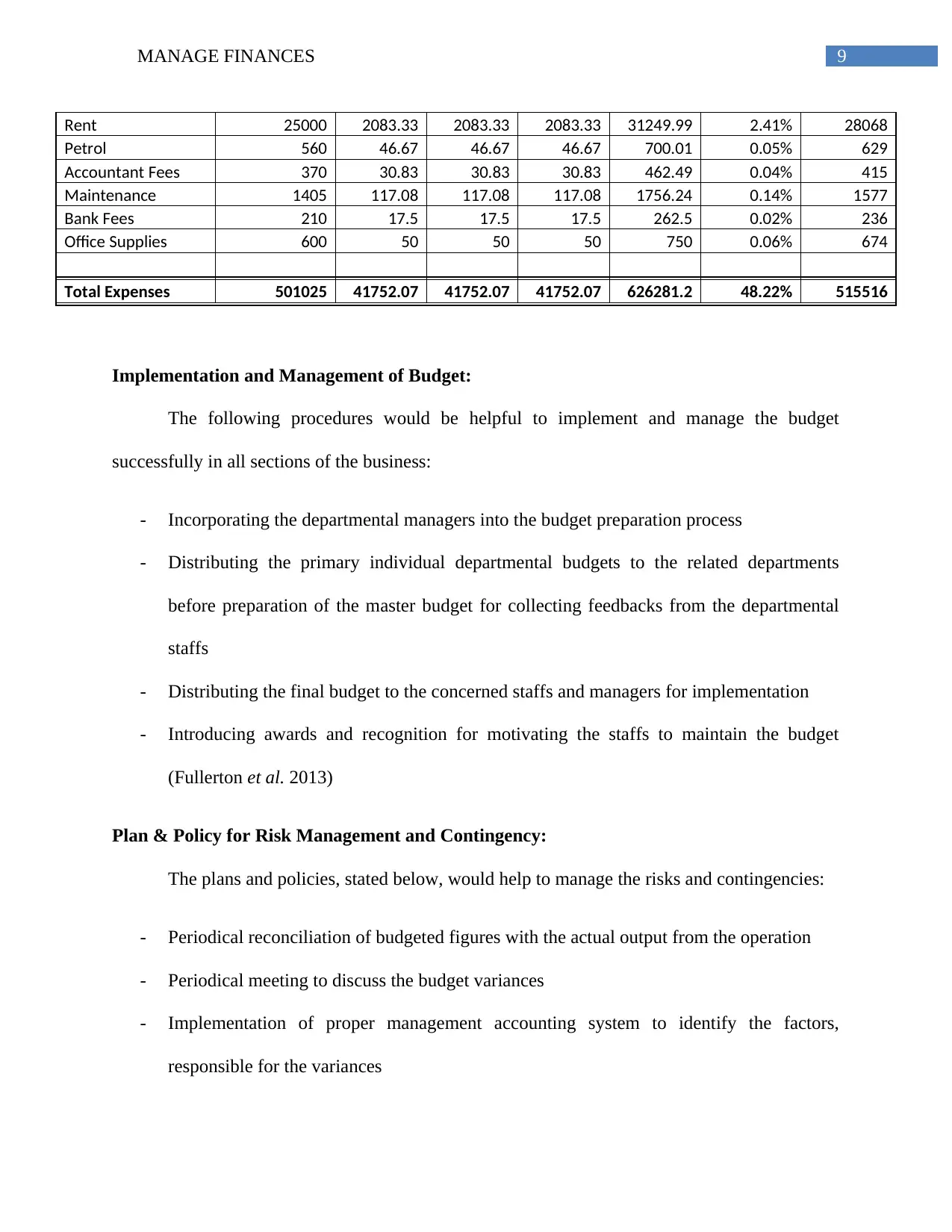

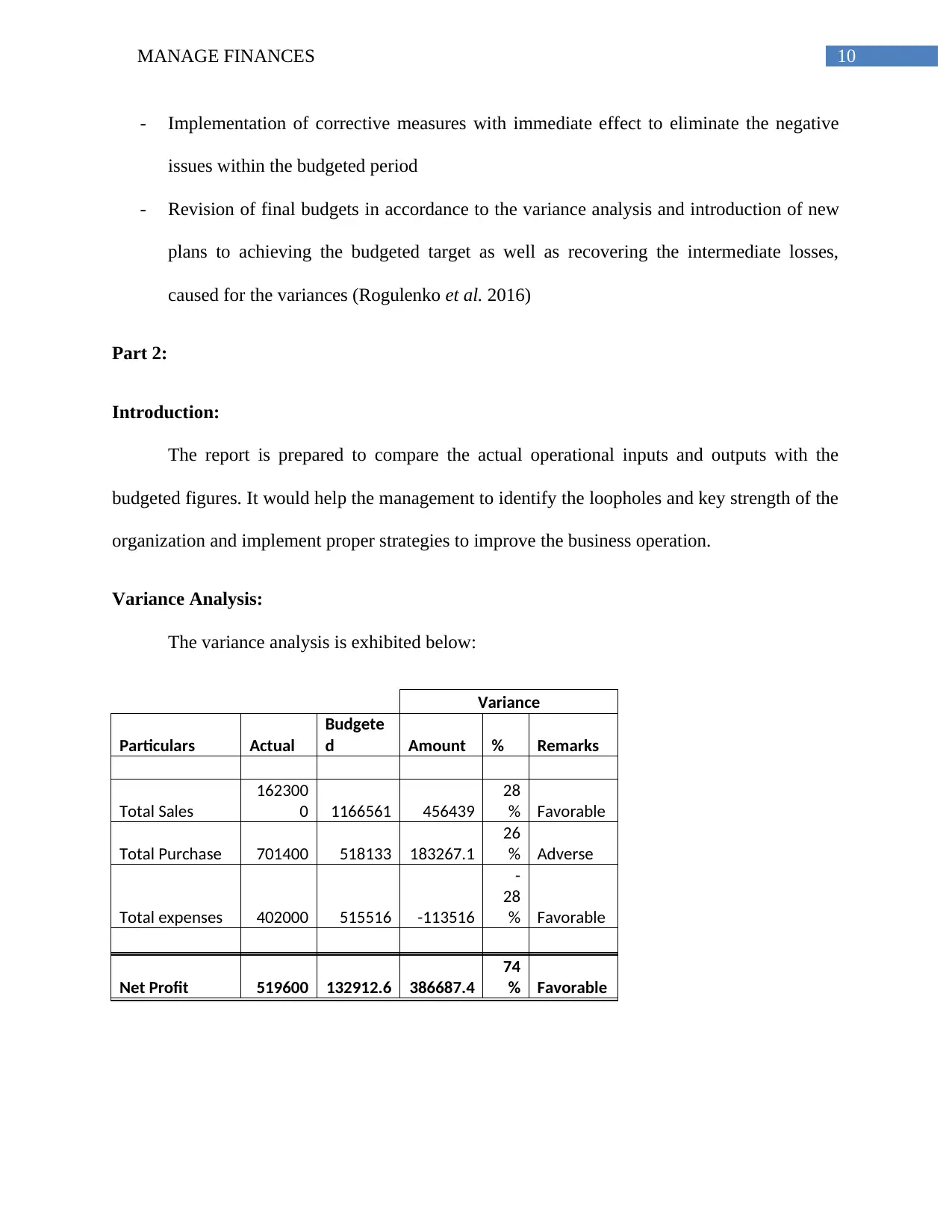

This report provides a comprehensive analysis of financial management, focusing on budgeting, variance analysis, and risk management strategies. It begins with an assessment of key stakeholders to consult before creating an operational plan, emphasizing the importance of engineers, architects, and the finance department. The report then presents projected financial statements, including an income statement, balance sheet, and cash flow statement, along with detailed sales projections. A variance analysis compares budgeted and actual figures, highlighting favorable variances in sales and expenses but an adverse variance in purchase costs. The report recommends implementing standard costing methods and stock control processes. Finally, it outlines plans and policies for budget implementation, risk management, and contingency planning, offering valuable insights into effective financial practices. The report is designed to help in identifying financial loopholes and key strengths of an organization, in order to implement proper strategies to improve business operations.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.