Financial Management Report: Analysis of FirstGroup Plc Performance

VerifiedAdded on 2020/01/21

|17

|5263

|61

Report

AI Summary

This report provides a comprehensive analysis of financial management principles, focusing on their application within the context of FirstGroup Plc, a UK transport company. The report begins with an introduction to financial management, emphasizing its role in managing organizational funds effectively. Task 1 examines the process of obtaining and assessing the validity of financial data from various sources, including financial statements and external reports. Task 2 delves into ratio analysis, comparing FirstGroup's financial performance over two years, and includes an analysis of profitability, liquidity, solvency, and efficiency ratios. Task 3 explores budgetary approaches, including incremental budgeting, and discusses the legal requirements and accounting conventions associated with budget preparation. The report then moves on to analyze the budget outcomes against organizational objectives. Finally, Task 5 addresses investment appraisal techniques, identifying criteria for judging investment proposals, analyzing their viability, and evaluating their impact on the company's strategic objectives. The conclusion summarizes the key findings and recommendations, highlighting the importance of sound financial management practices for FirstGroup's continued success.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial management refers to the management of organizational financial sources.

It is the process of collecting, organizing, managing and controlling the business funds in an

adequate manner. It helps to run company's operations without any hazards. Thus, it is clear

that it helps to administrate funds in an appropriate manner and competes effectively.

FirstGroup Plc is a UK transport company that provide bus, coaches and rail services to the

citizens. It is medium sized organization that mainly operates in UK, Ireland, Canada and

United Status. In the present report, the importance of financial management will be

discussed in company's context. Various tool such as budgets and ratio analysis will be

analysed to interpret business performance and ensure optimum allocation of resources.

Further, investment appraisal techniques will be discussed to identify most profitable

proposal and take strategic investment decisions.

Financial management refers to the management of organizational financial sources.

It is the process of collecting, organizing, managing and controlling the business funds in an

adequate manner. It helps to run company's operations without any hazards. Thus, it is clear

that it helps to administrate funds in an appropriate manner and competes effectively.

FirstGroup Plc is a UK transport company that provide bus, coaches and rail services to the

citizens. It is medium sized organization that mainly operates in UK, Ireland, Canada and

United Status. In the present report, the importance of financial management will be

discussed in company's context. Various tool such as budgets and ratio analysis will be

analysed to interpret business performance and ensure optimum allocation of resources.

Further, investment appraisal techniques will be discussed to identify most profitable

proposal and take strategic investment decisions.

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Obtaining financial data and assess its validity........................................................1

AC 1.4 Review and questions financial data.........................................................................2

Task 2.........................................................................................................................................3

AC 1.2, 1.3 Ratio Analysis of FirstGroup and comparative analysis ...................................3

TASK 3......................................................................................................................................5

AC 2.1 Approaches to prepare budget with the legal requirement and accounting

conventions............................................................................................................................5

TASK 4......................................................................................................................................6

AC 2.2 Analyse the budget outcomes against organizational objectives..............................6

TASK 5......................................................................................................................................8

AC 3.1 Identify criteria to judge investment proposals.........................................................8

AC 3.2 Analysing the proposal viability...............................................................................9

AC 3.3 Strength and weaknesses on the proposals.............................................................10

AC 3.4 Evaluate the impact of proposals on the strategic objectives..................................10

CONCLUSION........................................................................................................................11

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Obtaining financial data and assess its validity........................................................1

AC 1.4 Review and questions financial data.........................................................................2

Task 2.........................................................................................................................................3

AC 1.2, 1.3 Ratio Analysis of FirstGroup and comparative analysis ...................................3

TASK 3......................................................................................................................................5

AC 2.1 Approaches to prepare budget with the legal requirement and accounting

conventions............................................................................................................................5

TASK 4......................................................................................................................................6

AC 2.2 Analyse the budget outcomes against organizational objectives..............................6

TASK 5......................................................................................................................................8

AC 3.1 Identify criteria to judge investment proposals.........................................................8

AC 3.2 Analysing the proposal viability...............................................................................9

AC 3.3 Strength and weaknesses on the proposals.............................................................10

AC 3.4 Evaluate the impact of proposals on the strategic objectives..................................10

CONCLUSION........................................................................................................................11

REFERENCES.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management is the process of managing organization’s funds in an efficient

and effective manner. It becomes necessary for every business to collect and manage funds

appropriately. Thus, Certified Financial Officer plays a very important role in managing

funds of the organization. It refers to accomplishing functions such as financial planning,

procuring and collecting the financial resources of the enterprises. Moreover, it helps to

maintain effective administration of funds owned by the companies. This in turn will enable

the company to remove the operating hazards and run successfully. It estimates capital

requirements and fulfil organizational needs through determining an appropriate capital

structure. Thus, firms can collect funds at lower cost. Furthermore, it helps to take effective

capital investment decisions through investment appraisal techniques. The main objective of

financial management is about maximizing business profits and shareholder's wealth. Thus, it

becomes clear that it provides huge assistance to manage cash flows, minimise financial cost

and improve business performance. Hence, organization can compete effectively and survive

for a long term period. In this report, financial management will be discussing in context to

FirstGroup organization. It is a medium sized UK transport company having headquartered in

Aberdeen, Scotland. It provides bus, coach and rail services in UK, Ireland, Canada and US.

TASK 1

AC 1.1 Obtaining financial data and assess its validity

Financial data can be obtained from various internal as well as external sources. Every

organization prepare financial statements provide detailed information about company's

affairs. This statements are available within the organization such as income statement,

balance sheet, statement of retained earnings, cash flow and fund flow statements, statement

of changes in the financial position and others (Brigham and Daves, 2012). However,

economic reports, trade journals and published government reports are outside information

sources.

FirstGroup Company prepares their income statement to know its operational results.

The statement summarizes all the incurred expenses and generated incomes during a

specified time period. The aim of preparing this statement is to determine business profits and

losses. Surplus of revenues over the payments will indicate business loss while high

payments will raise loss to company. However, Balance sheet is a summarized statement of

FirstGroup assets and liabilities helps to determine financial status of the organization

(Kreder, 2015). It provides information regarding liquidity, solvency, efficiency and business

1

Financial management is the process of managing organization’s funds in an efficient

and effective manner. It becomes necessary for every business to collect and manage funds

appropriately. Thus, Certified Financial Officer plays a very important role in managing

funds of the organization. It refers to accomplishing functions such as financial planning,

procuring and collecting the financial resources of the enterprises. Moreover, it helps to

maintain effective administration of funds owned by the companies. This in turn will enable

the company to remove the operating hazards and run successfully. It estimates capital

requirements and fulfil organizational needs through determining an appropriate capital

structure. Thus, firms can collect funds at lower cost. Furthermore, it helps to take effective

capital investment decisions through investment appraisal techniques. The main objective of

financial management is about maximizing business profits and shareholder's wealth. Thus, it

becomes clear that it provides huge assistance to manage cash flows, minimise financial cost

and improve business performance. Hence, organization can compete effectively and survive

for a long term period. In this report, financial management will be discussing in context to

FirstGroup organization. It is a medium sized UK transport company having headquartered in

Aberdeen, Scotland. It provides bus, coach and rail services in UK, Ireland, Canada and US.

TASK 1

AC 1.1 Obtaining financial data and assess its validity

Financial data can be obtained from various internal as well as external sources. Every

organization prepare financial statements provide detailed information about company's

affairs. This statements are available within the organization such as income statement,

balance sheet, statement of retained earnings, cash flow and fund flow statements, statement

of changes in the financial position and others (Brigham and Daves, 2012). However,

economic reports, trade journals and published government reports are outside information

sources.

FirstGroup Company prepares their income statement to know its operational results.

The statement summarizes all the incurred expenses and generated incomes during a

specified time period. The aim of preparing this statement is to determine business profits and

losses. Surplus of revenues over the payments will indicate business loss while high

payments will raise loss to company. However, Balance sheet is a summarized statement of

FirstGroup assets and liabilities helps to determine financial status of the organization

(Kreder, 2015). It provides information regarding liquidity, solvency, efficiency and business

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

turnover. In addition to it, retained earnings statement identifies the changes in retained

profits between two balance sheet dates. Another, cash flow statements is prepared to

determine the cash sources and its application through operating, financing and investing

activities whilst fund flow statement provide information regarding used finance sources and

its application in business. Thus, it became clear that company's accounts make detailed

records of each and every transaction and give information to the users. Moreover,

government publish economic reports and trade journals which provide information regarding

industrial development. It gives information about growth of different sectors thus; users will

be able to take effective trading decisions.

FirstGroup prepare their financial statement as per the set accounting standards,

accounting rules, regulations and necessary principles and conventions (Scott, 2014).

Moreover, the statement are judged or verified by an independent auditor for publishing

purpose. Auditor are the skilled accounting professionals who inspect company's accounts

from necessary documents and give their opinion about whether it represent true and fair

position or not. It assists users in providing more prominent, reliable and valid information

about company's operation and provides assistance in their decisions making process.

AC 1.4 Review and questions financial data

Review of the financial statements is the assurance or conformity that FirstGroup

prepared its accounts in accordance with the provisions of financial reporting framework.

Applicable auditing requirements are the best way of reviewing company's accounts.

Analysing company's inventories, cash, bank, investment and fixed assets helps to review

business assets while liabilities can be reviewed through verifying bills payables, overdraft,

loans, and creditors and so on. High liabilities indicate trouble, manager's inabilities and

ineffective decisions while high amount of company's assets implies better financial

performance (Muller, 2012). In context to FirstGroup, its net assets shows an inclining trend

over the period shows that it is performing better in the market. Furthermore, according to the

profitability statements, increased sales and declined cost will help to increase profitability

and implies qualified operational performance. On contrary, decreased profitability is the sign

of poor or worst performance. FirstGroup Company improved its sales over the previous

period and generated high profits. Therefore, it can be said that FirstGroup is performing

well in the market. This in turn, company is able to operate for a long term period and survive

well.

2

profits between two balance sheet dates. Another, cash flow statements is prepared to

determine the cash sources and its application through operating, financing and investing

activities whilst fund flow statement provide information regarding used finance sources and

its application in business. Thus, it became clear that company's accounts make detailed

records of each and every transaction and give information to the users. Moreover,

government publish economic reports and trade journals which provide information regarding

industrial development. It gives information about growth of different sectors thus; users will

be able to take effective trading decisions.

FirstGroup prepare their financial statement as per the set accounting standards,

accounting rules, regulations and necessary principles and conventions (Scott, 2014).

Moreover, the statement are judged or verified by an independent auditor for publishing

purpose. Auditor are the skilled accounting professionals who inspect company's accounts

from necessary documents and give their opinion about whether it represent true and fair

position or not. It assists users in providing more prominent, reliable and valid information

about company's operation and provides assistance in their decisions making process.

AC 1.4 Review and questions financial data

Review of the financial statements is the assurance or conformity that FirstGroup

prepared its accounts in accordance with the provisions of financial reporting framework.

Applicable auditing requirements are the best way of reviewing company's accounts.

Analysing company's inventories, cash, bank, investment and fixed assets helps to review

business assets while liabilities can be reviewed through verifying bills payables, overdraft,

loans, and creditors and so on. High liabilities indicate trouble, manager's inabilities and

ineffective decisions while high amount of company's assets implies better financial

performance (Muller, 2012). In context to FirstGroup, its net assets shows an inclining trend

over the period shows that it is performing better in the market. Furthermore, according to the

profitability statements, increased sales and declined cost will help to increase profitability

and implies qualified operational performance. On contrary, decreased profitability is the sign

of poor or worst performance. FirstGroup Company improved its sales over the previous

period and generated high profits. Therefore, it can be said that FirstGroup is performing

well in the market. This in turn, company is able to operate for a long term period and survive

well.

2

TASK 2

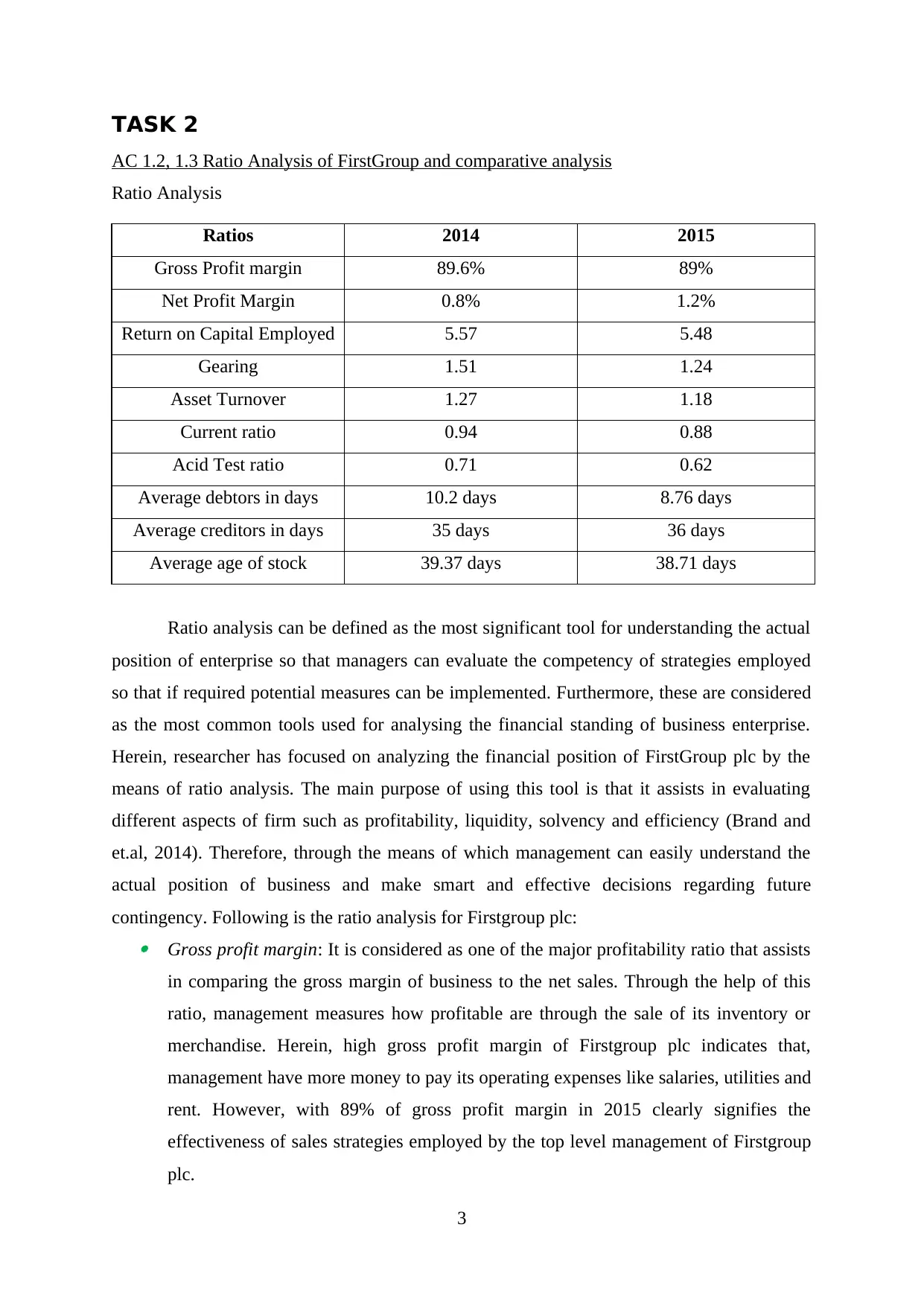

AC 1.2, 1.3 Ratio Analysis of FirstGroup and comparative analysis

Ratio Analysis

Ratios 2014 2015

Gross Profit margin 89.6% 89%

Net Profit Margin 0.8% 1.2%

Return on Capital Employed 5.57 5.48

Gearing 1.51 1.24

Asset Turnover 1.27 1.18

Current ratio 0.94 0.88

Acid Test ratio 0.71 0.62

Average debtors in days 10.2 days 8.76 days

Average creditors in days 35 days 36 days

Average age of stock 39.37 days 38.71 days

Ratio analysis can be defined as the most significant tool for understanding the actual

position of enterprise so that managers can evaluate the competency of strategies employed

so that if required potential measures can be implemented. Furthermore, these are considered

as the most common tools used for analysing the financial standing of business enterprise.

Herein, researcher has focused on analyzing the financial position of FirstGroup plc by the

means of ratio analysis. The main purpose of using this tool is that it assists in evaluating

different aspects of firm such as profitability, liquidity, solvency and efficiency (Brand and

et.al, 2014). Therefore, through the means of which management can easily understand the

actual position of business and make smart and effective decisions regarding future

contingency. Following is the ratio analysis for Firstgroup plc: Gross profit margin: It is considered as one of the major profitability ratio that assists

in comparing the gross margin of business to the net sales. Through the help of this

ratio, management measures how profitable are through the sale of its inventory or

merchandise. Herein, high gross profit margin of Firstgroup plc indicates that,

management have more money to pay its operating expenses like salaries, utilities and

rent. However, with 89% of gross profit margin in 2015 clearly signifies the

effectiveness of sales strategies employed by the top level management of Firstgroup

plc.

3

AC 1.2, 1.3 Ratio Analysis of FirstGroup and comparative analysis

Ratio Analysis

Ratios 2014 2015

Gross Profit margin 89.6% 89%

Net Profit Margin 0.8% 1.2%

Return on Capital Employed 5.57 5.48

Gearing 1.51 1.24

Asset Turnover 1.27 1.18

Current ratio 0.94 0.88

Acid Test ratio 0.71 0.62

Average debtors in days 10.2 days 8.76 days

Average creditors in days 35 days 36 days

Average age of stock 39.37 days 38.71 days

Ratio analysis can be defined as the most significant tool for understanding the actual

position of enterprise so that managers can evaluate the competency of strategies employed

so that if required potential measures can be implemented. Furthermore, these are considered

as the most common tools used for analysing the financial standing of business enterprise.

Herein, researcher has focused on analyzing the financial position of FirstGroup plc by the

means of ratio analysis. The main purpose of using this tool is that it assists in evaluating

different aspects of firm such as profitability, liquidity, solvency and efficiency (Brand and

et.al, 2014). Therefore, through the means of which management can easily understand the

actual position of business and make smart and effective decisions regarding future

contingency. Following is the ratio analysis for Firstgroup plc: Gross profit margin: It is considered as one of the major profitability ratio that assists

in comparing the gross margin of business to the net sales. Through the help of this

ratio, management measures how profitable are through the sale of its inventory or

merchandise. Herein, high gross profit margin of Firstgroup plc indicates that,

management have more money to pay its operating expenses like salaries, utilities and

rent. However, with 89% of gross profit margin in 2015 clearly signifies the

effectiveness of sales strategies employed by the top level management of Firstgroup

plc.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit margin: It assists in measuring what percentage of sales made up of net

income. In simple terms it assist in showing how much profits are produced through

the sale of goods and services. High net profit margin clearly indicates that, top level

management has managed the level of expenditure and increased the sales

performance. Furthermore, with the help of better promotional and marketing

strategies company is able to increase its profit margin and maintain its position in

target market. Return on capital employed: It is also profitability measure which assists in measuring

how efficiently company is making the use of employed capital in generating profits.

Considering the present condition of Firstgroup plc it can be said that slight down fall

in ROCE ratio from 5.57 to 5.48 means that very little decrease in dollars of profits

generated on the each dollar of capital employed. By the means of this ratio, investors

can easily evaluate the capability of firm in generating higher returns so that smart

and effective decisions can be made regarding future investments (Brigham and

Ehrhardt, 2013). Gearing: Debt/equity ratio is important for the stakeholders in understanding the

liabilities that business have during the reporting period. According to the above table,

decreasing gearing ratio from 1.51 to 1.24 indicates that top level management has

raised funds through equity which indeed decreases the liability of business. Asset Turnover: Through the help of this ratio, management can easily evaluate the

ability of company's assets in generating the sales. In the present case, slight downfall

in asset turnover ratio indicates that, Firstgroup plc is unable to make the use of its

assets in optimum manner which indeed leads to decrease the value of asset turnover

from 1.27 to 1.18. Liquidity position: Looking at the liquidity position of Firstgroup plc it can be said

that, ability of firm in making use of current assets in mitigating short term financial

needs is declining due to which both current and quick ratio are showing poor results

(Uechi and et.al., 2015). Decreasing current ratio indicates that firm is unable to

satisfy short financial needs while declining quick ratio indicates that company is

unable to overcome short term financial obligations. Average collection and payment period: On the basis of above ratio analysis table it

can be said that, decreasing debtors collection period means company is collecting

due payment (2015) more quickly in 8.76 days as compared to (2014) within 10.2

days. While on the other hand, goodwill in the market has helped the course of

4

income. In simple terms it assist in showing how much profits are produced through

the sale of goods and services. High net profit margin clearly indicates that, top level

management has managed the level of expenditure and increased the sales

performance. Furthermore, with the help of better promotional and marketing

strategies company is able to increase its profit margin and maintain its position in

target market. Return on capital employed: It is also profitability measure which assists in measuring

how efficiently company is making the use of employed capital in generating profits.

Considering the present condition of Firstgroup plc it can be said that slight down fall

in ROCE ratio from 5.57 to 5.48 means that very little decrease in dollars of profits

generated on the each dollar of capital employed. By the means of this ratio, investors

can easily evaluate the capability of firm in generating higher returns so that smart

and effective decisions can be made regarding future investments (Brigham and

Ehrhardt, 2013). Gearing: Debt/equity ratio is important for the stakeholders in understanding the

liabilities that business have during the reporting period. According to the above table,

decreasing gearing ratio from 1.51 to 1.24 indicates that top level management has

raised funds through equity which indeed decreases the liability of business. Asset Turnover: Through the help of this ratio, management can easily evaluate the

ability of company's assets in generating the sales. In the present case, slight downfall

in asset turnover ratio indicates that, Firstgroup plc is unable to make the use of its

assets in optimum manner which indeed leads to decrease the value of asset turnover

from 1.27 to 1.18. Liquidity position: Looking at the liquidity position of Firstgroup plc it can be said

that, ability of firm in making use of current assets in mitigating short term financial

needs is declining due to which both current and quick ratio are showing poor results

(Uechi and et.al., 2015). Decreasing current ratio indicates that firm is unable to

satisfy short financial needs while declining quick ratio indicates that company is

unable to overcome short term financial obligations. Average collection and payment period: On the basis of above ratio analysis table it

can be said that, decreasing debtors collection period means company is collecting

due payment (2015) more quickly in 8.76 days as compared to (2014) within 10.2

days. While on the other hand, goodwill in the market has helped the course of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Firstgroup plc as creditors has increased the period of payment for the firm which

assist in floating the working capital in more effective way.

Average stock period: Decreasing average age of stock clearly indicates that demand

of Firstgroup plc products and services has increased in the market due to which they

are able to refill the inventory in 38.71 days in 2015 as compared to 2014 39.37 days.

TASK 3

AC 2.1 Approaches to prepare budget with the legal requirement and accounting conventions

Budget: It is a financial tool which is used by the managers to administrate funds.

Managers prepare budget through estimating probable incomes and expenditures for future

period. It assists managers to remove operational difficulties and ensures hazard free

operative functions. The main purpose of budgetary process is to determine forecasted

incomes and expenses and maintain surplus cash availability in the business. Through

communicating strategic plans to various departments’, managers of the companies will be

able to monitor and control resources effectively (Diamond, 2012). Moreover, after ending

the budgetary period, managers evaluate the forecasted figures with the actual business

performance in order to determine variances. Thus, corrective actions can be taken to remove

adverse variances and ensure successful operations.

Incremental budgeting: It is the traditional approach of budget preparation. According

to this approach, every year budget is prepared on the basis of historical data. All the cash

incomes and payments will increases through adding some amount. It does not consider the

market changes and draft budget by increasing historical revenues and expenditures. The

benefit of this budgetary method is that it takes lower time and cost to the company.

Consistency approach is used to construct budget; hence improves comparability. However,

it is not a good method as it does not assess operating functions and their importance in future

context (Jones, Zalányi and Érdi, 2014). It increases all the cash payments without

considering the organization’s need for incurring it. Thus, undesired expenses also get

improved results in high business cost and lower profits. Further, no incentive is available for

the department or division manager for reducing cost.

Zero base budgeting: This method involves the determination of future operational

requirement. As per this method, it is essential for the mangers to identify future operating

activities initially. It helps in more accurate forecasting of revenues and expenditures for FY

(Adams, n.d.). It does not assume that all the historical operating functions will be continuing

for the upcoming period. Hence, it eliminates undesired functions which impose cost on the

5

assist in floating the working capital in more effective way.

Average stock period: Decreasing average age of stock clearly indicates that demand

of Firstgroup plc products and services has increased in the market due to which they

are able to refill the inventory in 38.71 days in 2015 as compared to 2014 39.37 days.

TASK 3

AC 2.1 Approaches to prepare budget with the legal requirement and accounting conventions

Budget: It is a financial tool which is used by the managers to administrate funds.

Managers prepare budget through estimating probable incomes and expenditures for future

period. It assists managers to remove operational difficulties and ensures hazard free

operative functions. The main purpose of budgetary process is to determine forecasted

incomes and expenses and maintain surplus cash availability in the business. Through

communicating strategic plans to various departments’, managers of the companies will be

able to monitor and control resources effectively (Diamond, 2012). Moreover, after ending

the budgetary period, managers evaluate the forecasted figures with the actual business

performance in order to determine variances. Thus, corrective actions can be taken to remove

adverse variances and ensure successful operations.

Incremental budgeting: It is the traditional approach of budget preparation. According

to this approach, every year budget is prepared on the basis of historical data. All the cash

incomes and payments will increases through adding some amount. It does not consider the

market changes and draft budget by increasing historical revenues and expenditures. The

benefit of this budgetary method is that it takes lower time and cost to the company.

Consistency approach is used to construct budget; hence improves comparability. However,

it is not a good method as it does not assess operating functions and their importance in future

context (Jones, Zalányi and Érdi, 2014). It increases all the cash payments without

considering the organization’s need for incurring it. Thus, undesired expenses also get

improved results in high business cost and lower profits. Further, no incentive is available for

the department or division manager for reducing cost.

Zero base budgeting: This method involves the determination of future operational

requirement. As per this method, it is essential for the mangers to identify future operating

activities initially. It helps in more accurate forecasting of revenues and expenditures for FY

(Adams, n.d.). It does not assume that all the historical operating functions will be continuing

for the upcoming period. Hence, it eliminates undesired functions which impose cost on the

5

company. Furthermore, it considers the market changes for budget construction. The

budgeting approach provides huge assistance in optimum allocation of company’s resources

for different functions (Kumar and Sahni, 2016). In addition to it, bottom-down approach

helps to encourage workers as they are involved in budget preparation. On contrary, the

disadvantage of this technique is that it takes lot of time and imposes high cost to the

company. Moreover, high managerial skills are required for drafting a budget.

First Group Company prepare their budget through using this technique. Company’s

managers determine future business receipts and payments to identify the net cash flow. It is

the legal requirement of the managers to draft budget from time-to-time. Budget committee

managers have to determine all the expected future business incomes and allocate business

resources in different operational activities in an efficient manner. They have to define budget

timeline, estimate cost of resources, dates and amount of revenues and expenses to construct

budget. After it, FirstGroup budget committee has to develop final budget and need to present

it to management board for approval to fulfil the legal requirement.

According to UK legislation, it is not the legal obligation to companies for preparing

budget for the future period. It is only a managerial tool which managers can prepare for their

business target achievements. There is no any separate act for drafting budgets in companies.

Moreover, no provision has been made in company’s law for budget construction henceforth,

it can be said that firms have a choice to prepare budget or not without any legal

requirements. But still, it is almost prepared in all the organizations for managing business

functions and to operate successfully.

Moreover, cash basis is used as accounting convention; hence non cash transactions

are eliminated from the budget. Thus, it is different from profit determination which is

helpful in effective cash management. Financial constraints are that without constructing the

budget, FirstGroup is not able to manage funds appropriately (Marina and et.al, 2016).

Moreover, production budget and material requirement budget help to determine the required

business production and able to meet customer’s demand efficiently. Another, flexible budget

provide an estimation of probable future results with varying sales volume. It measures the

ability of managers to take effective decisions. Further, detection and elimination of adverse

variances also provide great assistance to the managers for achieving strategic operational

objectives (Schroeder, Clark and Cathey, 2013).

6

budgeting approach provides huge assistance in optimum allocation of company’s resources

for different functions (Kumar and Sahni, 2016). In addition to it, bottom-down approach

helps to encourage workers as they are involved in budget preparation. On contrary, the

disadvantage of this technique is that it takes lot of time and imposes high cost to the

company. Moreover, high managerial skills are required for drafting a budget.

First Group Company prepare their budget through using this technique. Company’s

managers determine future business receipts and payments to identify the net cash flow. It is

the legal requirement of the managers to draft budget from time-to-time. Budget committee

managers have to determine all the expected future business incomes and allocate business

resources in different operational activities in an efficient manner. They have to define budget

timeline, estimate cost of resources, dates and amount of revenues and expenses to construct

budget. After it, FirstGroup budget committee has to develop final budget and need to present

it to management board for approval to fulfil the legal requirement.

According to UK legislation, it is not the legal obligation to companies for preparing

budget for the future period. It is only a managerial tool which managers can prepare for their

business target achievements. There is no any separate act for drafting budgets in companies.

Moreover, no provision has been made in company’s law for budget construction henceforth,

it can be said that firms have a choice to prepare budget or not without any legal

requirements. But still, it is almost prepared in all the organizations for managing business

functions and to operate successfully.

Moreover, cash basis is used as accounting convention; hence non cash transactions

are eliminated from the budget. Thus, it is different from profit determination which is

helpful in effective cash management. Financial constraints are that without constructing the

budget, FirstGroup is not able to manage funds appropriately (Marina and et.al, 2016).

Moreover, production budget and material requirement budget help to determine the required

business production and able to meet customer’s demand efficiently. Another, flexible budget

provide an estimation of probable future results with varying sales volume. It measures the

ability of managers to take effective decisions. Further, detection and elimination of adverse

variances also provide great assistance to the managers for achieving strategic operational

objectives (Schroeder, Clark and Cathey, 2013).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

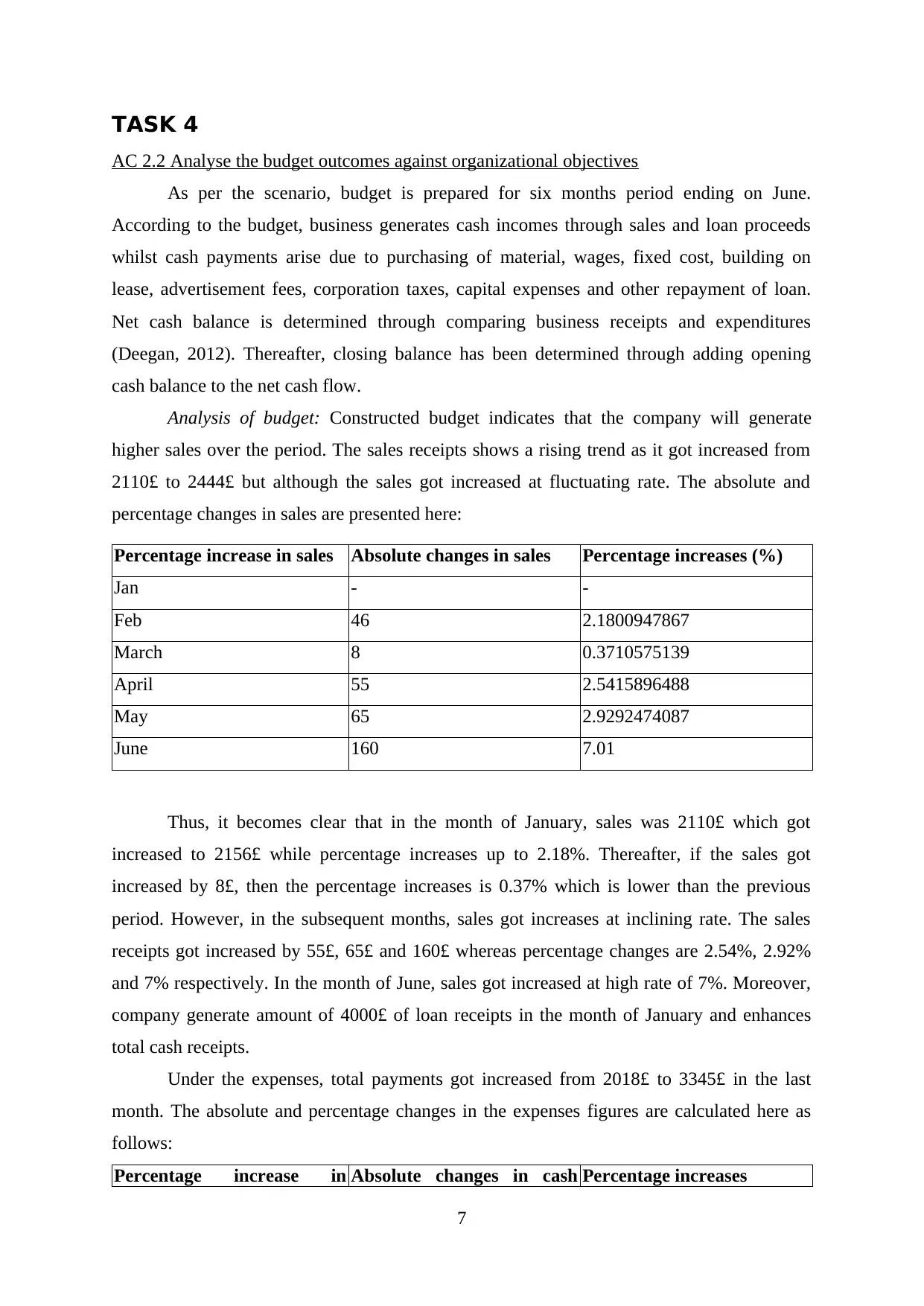

TASK 4

AC 2.2 Analyse the budget outcomes against organizational objectives

As per the scenario, budget is prepared for six months period ending on June.

According to the budget, business generates cash incomes through sales and loan proceeds

whilst cash payments arise due to purchasing of material, wages, fixed cost, building on

lease, advertisement fees, corporation taxes, capital expenses and other repayment of loan.

Net cash balance is determined through comparing business receipts and expenditures

(Deegan, 2012). Thereafter, closing balance has been determined through adding opening

cash balance to the net cash flow.

Analysis of budget: Constructed budget indicates that the company will generate

higher sales over the period. The sales receipts shows a rising trend as it got increased from

2110£ to 2444£ but although the sales got increased at fluctuating rate. The absolute and

percentage changes in sales are presented here:

Percentage increase in sales Absolute changes in sales Percentage increases (%)

Jan - -

Feb 46 2.1800947867

March 8 0.3710575139

April 55 2.5415896488

May 65 2.9292474087

June 160 7.01

Thus, it becomes clear that in the month of January, sales was 2110£ which got

increased to 2156£ while percentage increases up to 2.18%. Thereafter, if the sales got

increased by 8£, then the percentage increases is 0.37% which is lower than the previous

period. However, in the subsequent months, sales got increases at inclining rate. The sales

receipts got increased by 55£, 65£ and 160£ whereas percentage changes are 2.54%, 2.92%

and 7% respectively. In the month of June, sales got increased at high rate of 7%. Moreover,

company generate amount of 4000£ of loan receipts in the month of January and enhances

total cash receipts.

Under the expenses, total payments got increased from 2018£ to 3345£ in the last

month. The absolute and percentage changes in the expenses figures are calculated here as

follows:

Percentage increase in Absolute changes in cash Percentage increases

7

AC 2.2 Analyse the budget outcomes against organizational objectives

As per the scenario, budget is prepared for six months period ending on June.

According to the budget, business generates cash incomes through sales and loan proceeds

whilst cash payments arise due to purchasing of material, wages, fixed cost, building on

lease, advertisement fees, corporation taxes, capital expenses and other repayment of loan.

Net cash balance is determined through comparing business receipts and expenditures

(Deegan, 2012). Thereafter, closing balance has been determined through adding opening

cash balance to the net cash flow.

Analysis of budget: Constructed budget indicates that the company will generate

higher sales over the period. The sales receipts shows a rising trend as it got increased from

2110£ to 2444£ but although the sales got increased at fluctuating rate. The absolute and

percentage changes in sales are presented here:

Percentage increase in sales Absolute changes in sales Percentage increases (%)

Jan - -

Feb 46 2.1800947867

March 8 0.3710575139

April 55 2.5415896488

May 65 2.9292474087

June 160 7.01

Thus, it becomes clear that in the month of January, sales was 2110£ which got

increased to 2156£ while percentage increases up to 2.18%. Thereafter, if the sales got

increased by 8£, then the percentage increases is 0.37% which is lower than the previous

period. However, in the subsequent months, sales got increases at inclining rate. The sales

receipts got increased by 55£, 65£ and 160£ whereas percentage changes are 2.54%, 2.92%

and 7% respectively. In the month of June, sales got increased at high rate of 7%. Moreover,

company generate amount of 4000£ of loan receipts in the month of January and enhances

total cash receipts.

Under the expenses, total payments got increased from 2018£ to 3345£ in the last

month. The absolute and percentage changes in the expenses figures are calculated here as

follows:

Percentage increase in Absolute changes in cash Percentage increases

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses expense

Jan - -

Feb 335 16.6005946482

March 2734 116.1920951976

April -2280 -44.8201297425

May 60 2.1375133595

June 478 16.6724799442

The table indicates that in January, company incurred cash expenditures of

2018£ which inclined to 2353£ in the next period. The absolute and percentage changes

are 335£ and 16.60%. It has been inclined because of increase in the material expense,

taking building on lease and arising advertisement cost. However, in the month of March,

payment shows a very high increase as it got inclined by 2734£ and 116%. The main cause of

such increase is raising capital expenditures of 2750£. On contrary, April shows a declined to

cash payments by 2280£ and 44.82%. Elimination of capital expenses are the reason behind

such decreases. Thereafter, it got enhanced by 2.13% and 16.67% respectively. This is;

because of arising loan repayment and corporation taxes. Due to the impact of

fluctuating incomes and expenses, net cash flow got changed to 4092£ to (901£). Excess of

predicted revenues over the payments avail surplus cash balance while high cash payments

than revenues indicates deficit net cash flow. Furthermore, it impacted the closing cash

balance in both the direction.

Following decisions can be taken to overcome the shortcomings and surplus cash

availability. One of the important ways of mitigating the deficit balance is to improve

the total sales. It can be done by lowering selling prices and effective marketing planning

and strategies. Advertisement and marketing efforts will help to raise public awareness about

the offered products and services (Titman, Martin and Keown, 2015). Moreover, company's

offerings at affordable prices will lead to enhance product’s demand and total sales. Along

with this, maintaining effective control over the expenditures will reduce the company's cost

and results in fall in total payments. This in turn enables business to have surplus cash

availability for operational purpose (McKinney, 2015). Regularly monitoring of the operating

functions will assist managers to control business payments and have sufficient cash available

for running daily functions. Another suggestion to eliminate adverse balance is that company

can make use of overdraft facility as bankers are agreed to provide overdraft to the extent of

8

Jan - -

Feb 335 16.6005946482

March 2734 116.1920951976

April -2280 -44.8201297425

May 60 2.1375133595

June 478 16.6724799442

The table indicates that in January, company incurred cash expenditures of

2018£ which inclined to 2353£ in the next period. The absolute and percentage changes

are 335£ and 16.60%. It has been inclined because of increase in the material expense,

taking building on lease and arising advertisement cost. However, in the month of March,

payment shows a very high increase as it got inclined by 2734£ and 116%. The main cause of

such increase is raising capital expenditures of 2750£. On contrary, April shows a declined to

cash payments by 2280£ and 44.82%. Elimination of capital expenses are the reason behind

such decreases. Thereafter, it got enhanced by 2.13% and 16.67% respectively. This is;

because of arising loan repayment and corporation taxes. Due to the impact of

fluctuating incomes and expenses, net cash flow got changed to 4092£ to (901£). Excess of

predicted revenues over the payments avail surplus cash balance while high cash payments

than revenues indicates deficit net cash flow. Furthermore, it impacted the closing cash

balance in both the direction.

Following decisions can be taken to overcome the shortcomings and surplus cash

availability. One of the important ways of mitigating the deficit balance is to improve

the total sales. It can be done by lowering selling prices and effective marketing planning

and strategies. Advertisement and marketing efforts will help to raise public awareness about

the offered products and services (Titman, Martin and Keown, 2015). Moreover, company's

offerings at affordable prices will lead to enhance product’s demand and total sales. Along

with this, maintaining effective control over the expenditures will reduce the company's cost

and results in fall in total payments. This in turn enables business to have surplus cash

availability for operational purpose (McKinney, 2015). Regularly monitoring of the operating

functions will assist managers to control business payments and have sufficient cash available

for running daily functions. Another suggestion to eliminate adverse balance is that company

can make use of overdraft facility as bankers are agreed to provide overdraft to the extent of

8

750000£. Furthermore, previous month cash can be reinvested; further to earn returns on it. It

helps to improve cash earnings and favourable net cash flow.

TASK 5

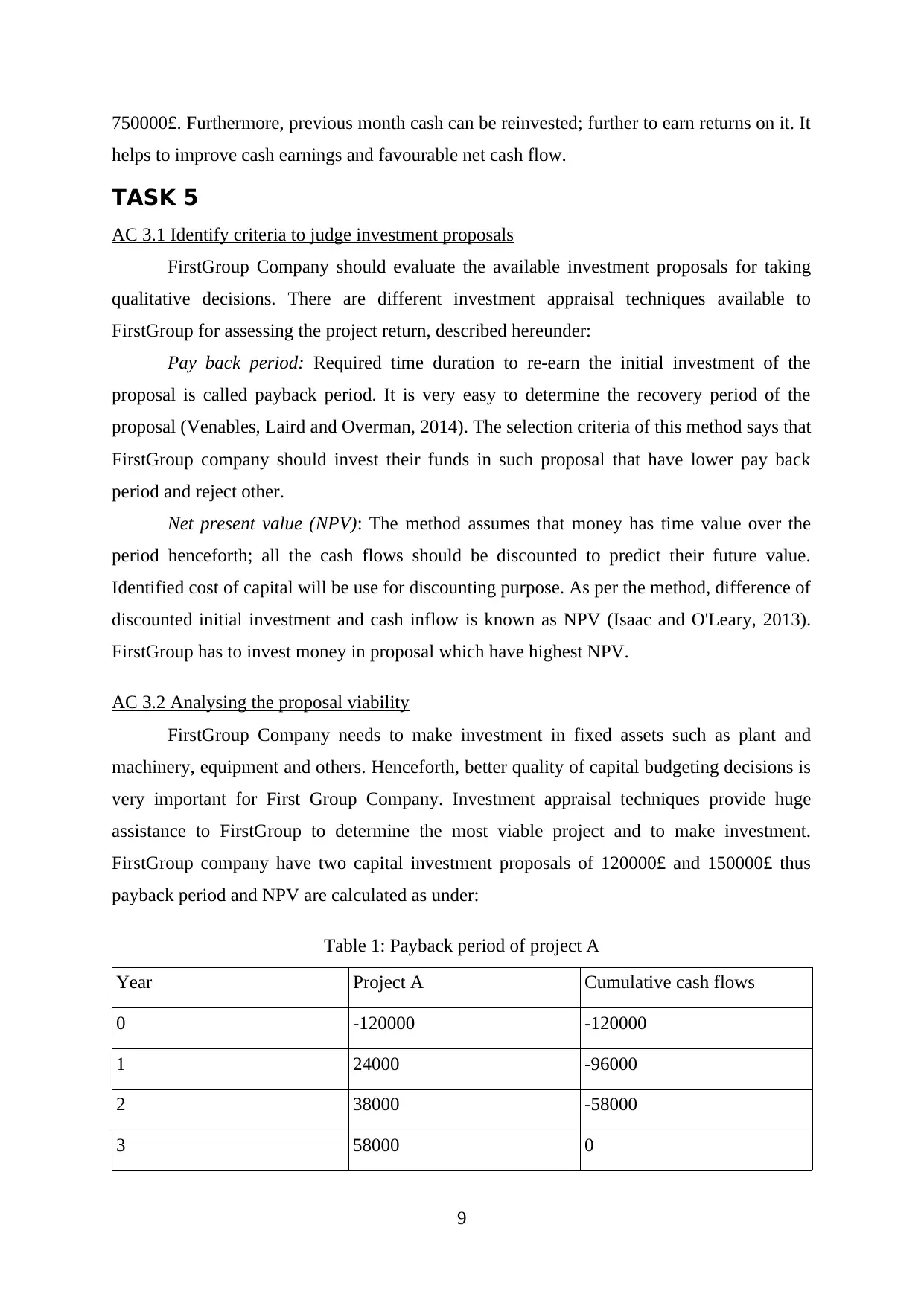

AC 3.1 Identify criteria to judge investment proposals

FirstGroup Company should evaluate the available investment proposals for taking

qualitative decisions. There are different investment appraisal techniques available to

FirstGroup for assessing the project return, described hereunder:

Pay back period: Required time duration to re-earn the initial investment of the

proposal is called payback period. It is very easy to determine the recovery period of the

proposal (Venables, Laird and Overman, 2014). The selection criteria of this method says that

FirstGroup company should invest their funds in such proposal that have lower pay back

period and reject other.

Net present value (NPV): The method assumes that money has time value over the

period henceforth; all the cash flows should be discounted to predict their future value.

Identified cost of capital will be use for discounting purpose. As per the method, difference of

discounted initial investment and cash inflow is known as NPV (Isaac and O'Leary, 2013).

FirstGroup has to invest money in proposal which have highest NPV.

AC 3.2 Analysing the proposal viability

FirstGroup Company needs to make investment in fixed assets such as plant and

machinery, equipment and others. Henceforth, better quality of capital budgeting decisions is

very important for First Group Company. Investment appraisal techniques provide huge

assistance to FirstGroup to determine the most viable project and to make investment.

FirstGroup company have two capital investment proposals of 120000£ and 150000£ thus

payback period and NPV are calculated as under:

Table 1: Payback period of project A

Year Project A Cumulative cash flows

0 -120000 -120000

1 24000 -96000

2 38000 -58000

3 58000 0

9

helps to improve cash earnings and favourable net cash flow.

TASK 5

AC 3.1 Identify criteria to judge investment proposals

FirstGroup Company should evaluate the available investment proposals for taking

qualitative decisions. There are different investment appraisal techniques available to

FirstGroup for assessing the project return, described hereunder:

Pay back period: Required time duration to re-earn the initial investment of the

proposal is called payback period. It is very easy to determine the recovery period of the

proposal (Venables, Laird and Overman, 2014). The selection criteria of this method says that

FirstGroup company should invest their funds in such proposal that have lower pay back

period and reject other.

Net present value (NPV): The method assumes that money has time value over the

period henceforth; all the cash flows should be discounted to predict their future value.

Identified cost of capital will be use for discounting purpose. As per the method, difference of

discounted initial investment and cash inflow is known as NPV (Isaac and O'Leary, 2013).

FirstGroup has to invest money in proposal which have highest NPV.

AC 3.2 Analysing the proposal viability

FirstGroup Company needs to make investment in fixed assets such as plant and

machinery, equipment and others. Henceforth, better quality of capital budgeting decisions is

very important for First Group Company. Investment appraisal techniques provide huge

assistance to FirstGroup to determine the most viable project and to make investment.

FirstGroup company have two capital investment proposals of 120000£ and 150000£ thus

payback period and NPV are calculated as under:

Table 1: Payback period of project A

Year Project A Cumulative cash flows

0 -120000 -120000

1 24000 -96000

2 38000 -58000

3 58000 0

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.