Financial Management Assessment 2: Budgeting, Performance, and Risk

VerifiedAdded on 2020/01/16

|16

|4630

|485

Report

AI Summary

This report presents a comprehensive analysis of financial management principles, focusing on budgeting and performance evaluation for a motorcycle company. It begins with an operational budget that includes sales forecasting for 2013 and a proposed budget for 2014, along with variance analysis. The report delves into stakeholder analysis, outlining the interests of internal and external stakeholders in the budgeting process. It then explores operational budgets, covering inventory, cost of goods sold, and expense budgets by cost center, along with a comparative profit and loss statement. A key component is risk management, with a detailed risk schedule identifying potential threats and mitigation strategies. The report extends to a service business budget, calculating productive hours and break-even points. Finally, it addresses performance monitoring through revenue comparative statements, key performance indicators, forecasting concepts, and staff motivation strategies, culminating in a financial analysis section.

FINANCIAL MANAGEMENT

(ASSESSMENT 2)

1

(ASSESSMENT 2)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1 OPERATIONAL BUDGET – SALES REVENUE................................................................4

PART A BUDGETING FOR YEAR 2014...........................................................................................4

1 Sales Forecast for each Quarter of 2013 and a Budget for each Quarter for the 2014 year........4

2 Comparative Statement of Forecast Sales Revenue for 2013 Budget for 2014 and the Variance 4

PART B REPORTING TO MANAGEMENT......................................................................................5

1. Expected Outcomes and Assumptions.........................................................................................5

2.Internal and External stakeholders................................................................................................5

3.Approaches and Factors for preparing the Budgets......................................................................6

TASK 2 – OPERATIONAL BUDGETS..............................................................................................6

PART A INVENTORY AND COST OF GOODS SOLD...................................................................6

PART B - EXPENSE BUDGET BY COST CENTRE.........................................................................7

1. Expense Budget by Cost Centre..................................................................................................7

2. Comparative Profit and Loss Statement......................................................................................8

PART C – RISK MANAGEMENT......................................................................................................9

Risk Schedule..................................................................................................................................9

TASK 3 Budget – SERVICE BUSINESS..........................................................................................10

PART A...............................................................................................................................................10

1. Calculation of Total Productive hours available to be charged out to the clients.....................10

2. Calculation of average charge per hour.....................................................................................11

3. Complete a brief P&L account for the business.........................................................................11

4. Calculation of productive hours to achieve break-even point...................................................12

PART B...............................................................................................................................................12

TASK 4- MONITORING PERFORMANCE....................................................................................12

1. Calculation of Revenue Comparative Statement.......................................................................12

2. Key points or questions to rise in order to gain an understanding of the business performance

.......................................................................................................................................................13

3. Concept of forecasting and its importance................................................................................13

4. Actions needs to communicate, monitor and motivate staff......................................................13

TASK 5 – MONITORING PERFORMANCE – FINANCIAL ANALYSIS.....................................14

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

2

INTRODUCTION................................................................................................................................4

TASK 1 OPERATIONAL BUDGET – SALES REVENUE................................................................4

PART A BUDGETING FOR YEAR 2014...........................................................................................4

1 Sales Forecast for each Quarter of 2013 and a Budget for each Quarter for the 2014 year........4

2 Comparative Statement of Forecast Sales Revenue for 2013 Budget for 2014 and the Variance 4

PART B REPORTING TO MANAGEMENT......................................................................................5

1. Expected Outcomes and Assumptions.........................................................................................5

2.Internal and External stakeholders................................................................................................5

3.Approaches and Factors for preparing the Budgets......................................................................6

TASK 2 – OPERATIONAL BUDGETS..............................................................................................6

PART A INVENTORY AND COST OF GOODS SOLD...................................................................6

PART B - EXPENSE BUDGET BY COST CENTRE.........................................................................7

1. Expense Budget by Cost Centre..................................................................................................7

2. Comparative Profit and Loss Statement......................................................................................8

PART C – RISK MANAGEMENT......................................................................................................9

Risk Schedule..................................................................................................................................9

TASK 3 Budget – SERVICE BUSINESS..........................................................................................10

PART A...............................................................................................................................................10

1. Calculation of Total Productive hours available to be charged out to the clients.....................10

2. Calculation of average charge per hour.....................................................................................11

3. Complete a brief P&L account for the business.........................................................................11

4. Calculation of productive hours to achieve break-even point...................................................12

PART B...............................................................................................................................................12

TASK 4- MONITORING PERFORMANCE....................................................................................12

1. Calculation of Revenue Comparative Statement.......................................................................12

2. Key points or questions to rise in order to gain an understanding of the business performance

.......................................................................................................................................................13

3. Concept of forecasting and its importance................................................................................13

4. Actions needs to communicate, monitor and motivate staff......................................................13

TASK 5 – MONITORING PERFORMANCE – FINANCIAL ANALYSIS.....................................14

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

2

Index of Tables

Table 1: Forecast Sales for the year ended 31 December 2013............................................................5

Table 2: Proposed Budget for the year ended 31 December 2014.......................................................5

Table 3:Comparative Statement to be presented to Management showing Total Forecast Sales ........5

Table 4: Internal Stakeholders and interest in Budget..........................................................................6

Table 5: External Stakeholders and interest in Budget.........................................................................6

Table 6: Inventory Budget for 2014.....................................................................................................7

Table 7: Purchase Budget for 2014.......................................................................................................7

Table 8: Cost of Sales and Gross Profit Budget...................................................................................7

Table 9: Expense Budget for 2014.......................................................................................................8

Table 10: Master Budget Comparison..................................................................................................9

3

Table 1: Forecast Sales for the year ended 31 December 2013............................................................5

Table 2: Proposed Budget for the year ended 31 December 2014.......................................................5

Table 3:Comparative Statement to be presented to Management showing Total Forecast Sales ........5

Table 4: Internal Stakeholders and interest in Budget..........................................................................6

Table 5: External Stakeholders and interest in Budget.........................................................................6

Table 6: Inventory Budget for 2014.....................................................................................................7

Table 7: Purchase Budget for 2014.......................................................................................................7

Table 8: Cost of Sales and Gross Profit Budget...................................................................................7

Table 9: Expense Budget for 2014.......................................................................................................8

Table 10: Master Budget Comparison..................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

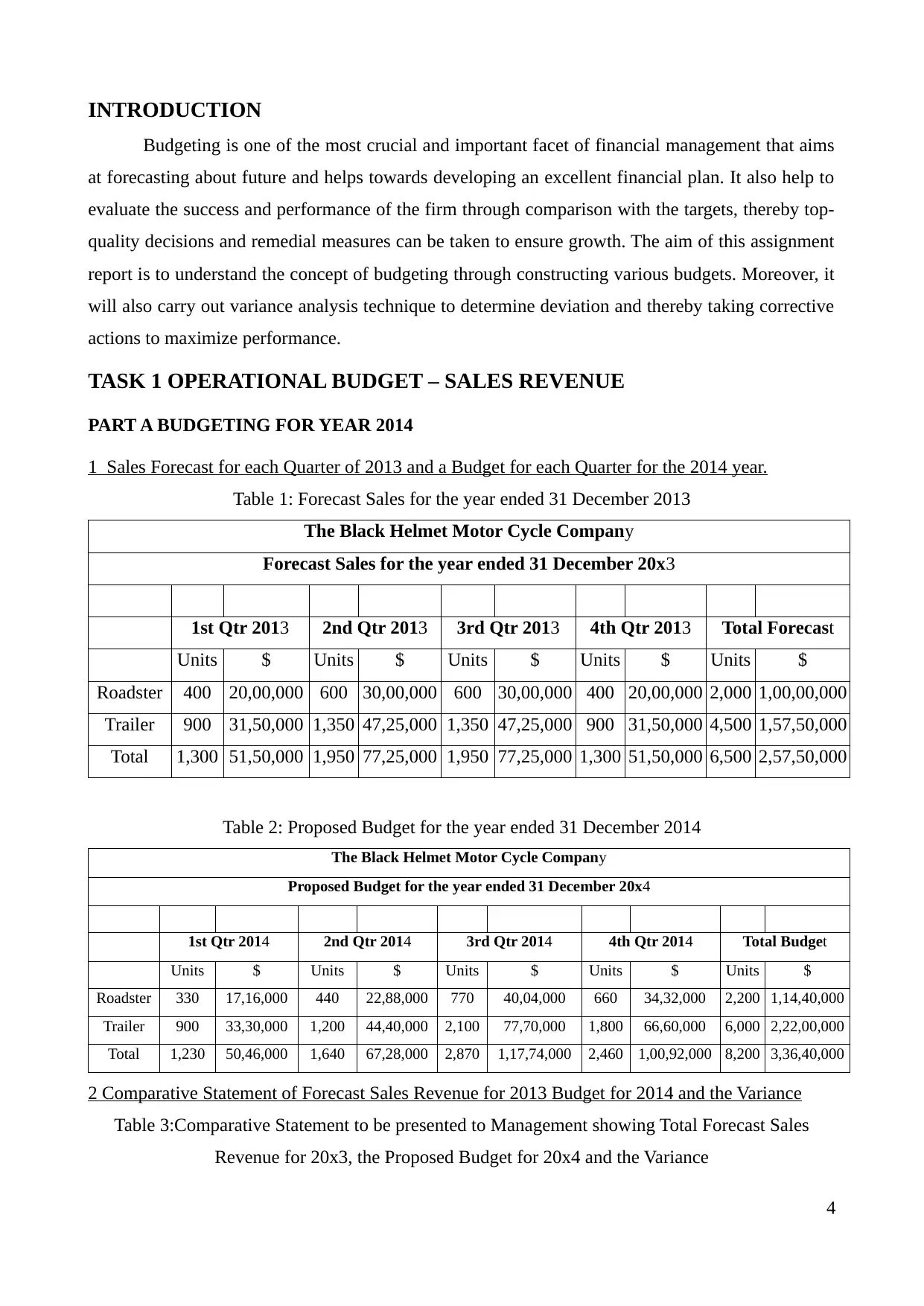

INTRODUCTION

Budgeting is one of the most crucial and important facet of financial management that aims

at forecasting about future and helps towards developing an excellent financial plan. It also help to

evaluate the success and performance of the firm through comparison with the targets, thereby top-

quality decisions and remedial measures can be taken to ensure growth. The aim of this assignment

report is to understand the concept of budgeting through constructing various budgets. Moreover, it

will also carry out variance analysis technique to determine deviation and thereby taking corrective

actions to maximize performance.

TASK 1 OPERATIONAL BUDGET – SALES REVENUE

PART A BUDGETING FOR YEAR 2014

1 Sales Forecast for each Quarter of 2013 and a Budget for each Quarter for the 2014 year.

Table 1: Forecast Sales for the year ended 31 December 2013

The Black Helmet Motor Cycle Company

Forecast Sales for the year ended 31 December 20x3

1st Qtr 2013 2nd Qtr 2013 3rd Qtr 2013 4th Qtr 2013 Total Forecast

Units $ Units $ Units $ Units $ Units $

Roadster 400 20,00,000 600 30,00,000 600 30,00,000 400 20,00,000 2,000 1,00,00,000

Trailer 900 31,50,000 1,350 47,25,000 1,350 47,25,000 900 31,50,000 4,500 1,57,50,000

Total 1,300 51,50,000 1,950 77,25,000 1,950 77,25,000 1,300 51,50,000 6,500 2,57,50,000

Table 2: Proposed Budget for the year ended 31 December 2014

The Black Helmet Motor Cycle Company

Proposed Budget for the year ended 31 December 20x4

1st Qtr 2014 2nd Qtr 2014 3rd Qtr 2014 4th Qtr 2014 Total Budget

Units $ Units $ Units $ Units $ Units $

Roadster 330 17,16,000 440 22,88,000 770 40,04,000 660 34,32,000 2,200 1,14,40,000

Trailer 900 33,30,000 1,200 44,40,000 2,100 77,70,000 1,800 66,60,000 6,000 2,22,00,000

Total 1,230 50,46,000 1,640 67,28,000 2,870 1,17,74,000 2,460 1,00,92,000 8,200 3,36,40,000

2 Comparative Statement of Forecast Sales Revenue for 2013 Budget for 2014 and the Variance

Table 3:Comparative Statement to be presented to Management showing Total Forecast Sales

Revenue for 20x3, the Proposed Budget for 20x4 and the Variance

4

Budgeting is one of the most crucial and important facet of financial management that aims

at forecasting about future and helps towards developing an excellent financial plan. It also help to

evaluate the success and performance of the firm through comparison with the targets, thereby top-

quality decisions and remedial measures can be taken to ensure growth. The aim of this assignment

report is to understand the concept of budgeting through constructing various budgets. Moreover, it

will also carry out variance analysis technique to determine deviation and thereby taking corrective

actions to maximize performance.

TASK 1 OPERATIONAL BUDGET – SALES REVENUE

PART A BUDGETING FOR YEAR 2014

1 Sales Forecast for each Quarter of 2013 and a Budget for each Quarter for the 2014 year.

Table 1: Forecast Sales for the year ended 31 December 2013

The Black Helmet Motor Cycle Company

Forecast Sales for the year ended 31 December 20x3

1st Qtr 2013 2nd Qtr 2013 3rd Qtr 2013 4th Qtr 2013 Total Forecast

Units $ Units $ Units $ Units $ Units $

Roadster 400 20,00,000 600 30,00,000 600 30,00,000 400 20,00,000 2,000 1,00,00,000

Trailer 900 31,50,000 1,350 47,25,000 1,350 47,25,000 900 31,50,000 4,500 1,57,50,000

Total 1,300 51,50,000 1,950 77,25,000 1,950 77,25,000 1,300 51,50,000 6,500 2,57,50,000

Table 2: Proposed Budget for the year ended 31 December 2014

The Black Helmet Motor Cycle Company

Proposed Budget for the year ended 31 December 20x4

1st Qtr 2014 2nd Qtr 2014 3rd Qtr 2014 4th Qtr 2014 Total Budget

Units $ Units $ Units $ Units $ Units $

Roadster 330 17,16,000 440 22,88,000 770 40,04,000 660 34,32,000 2,200 1,14,40,000

Trailer 900 33,30,000 1,200 44,40,000 2,100 77,70,000 1,800 66,60,000 6,000 2,22,00,000

Total 1,230 50,46,000 1,640 67,28,000 2,870 1,17,74,000 2,460 1,00,92,000 8,200 3,36,40,000

2 Comparative Statement of Forecast Sales Revenue for 2013 Budget for 2014 and the Variance

Table 3:Comparative Statement to be presented to Management showing Total Forecast Sales

Revenue for 20x3, the Proposed Budget for 20x4 and the Variance

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

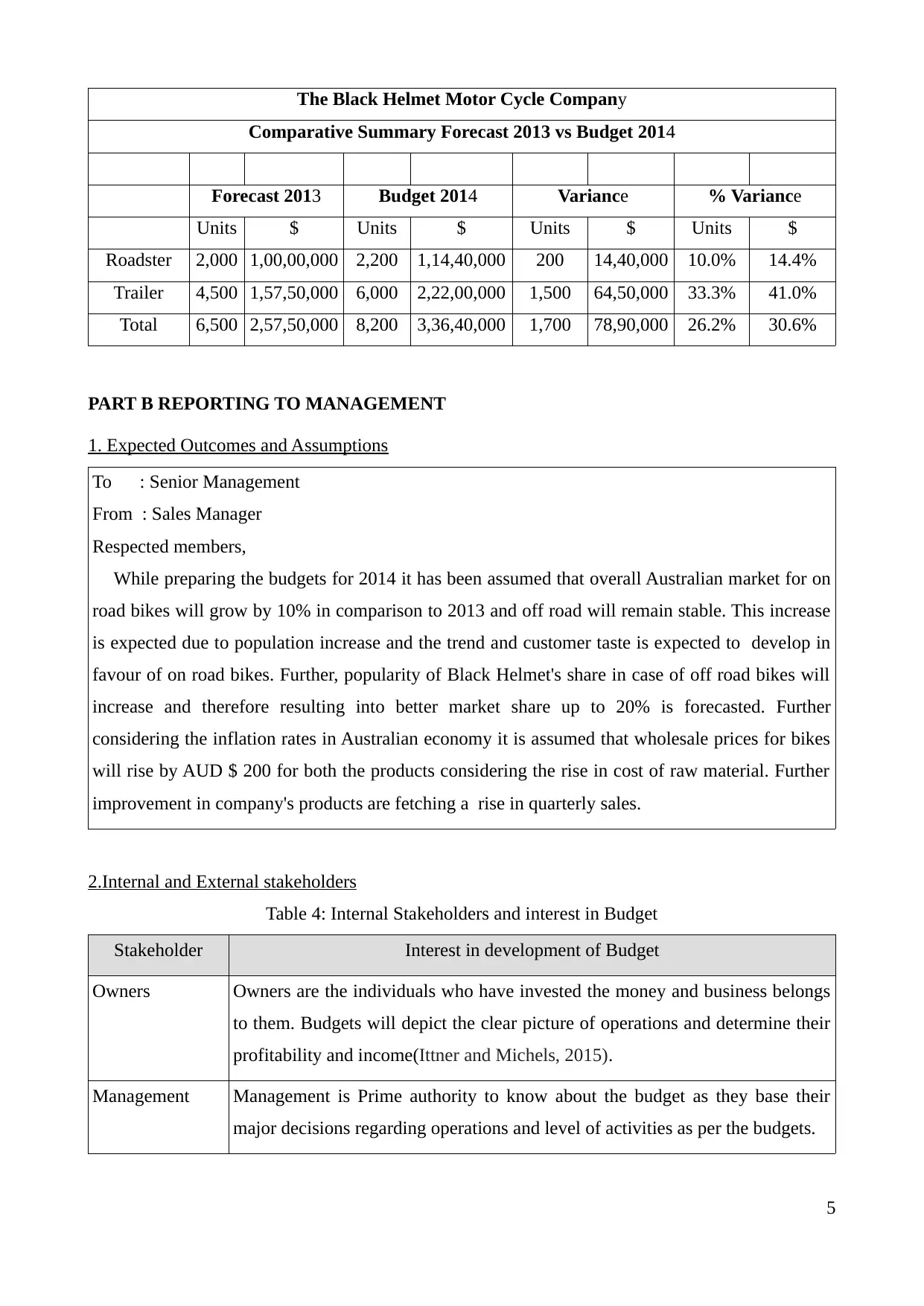

The Black Helmet Motor Cycle Company

Comparative Summary Forecast 2013 vs Budget 2014

Forecast 2013 Budget 2014 Variance % Variance

Units $ Units $ Units $ Units $

Roadster 2,000 1,00,00,000 2,200 1,14,40,000 200 14,40,000 10.0% 14.4%

Trailer 4,500 1,57,50,000 6,000 2,22,00,000 1,500 64,50,000 33.3% 41.0%

Total 6,500 2,57,50,000 8,200 3,36,40,000 1,700 78,90,000 26.2% 30.6%

PART B REPORTING TO MANAGEMENT

1. Expected Outcomes and Assumptions

To : Senior Management

From : Sales Manager

Respected members,

While preparing the budgets for 2014 it has been assumed that overall Australian market for on

road bikes will grow by 10% in comparison to 2013 and off road will remain stable. This increase

is expected due to population increase and the trend and customer taste is expected to develop in

favour of on road bikes. Further, popularity of Black Helmet's share in case of off road bikes will

increase and therefore resulting into better market share up to 20% is forecasted. Further

considering the inflation rates in Australian economy it is assumed that wholesale prices for bikes

will rise by AUD $ 200 for both the products considering the rise in cost of raw material. Further

improvement in company's products are fetching a rise in quarterly sales.

2.Internal and External stakeholders

Table 4: Internal Stakeholders and interest in Budget

Stakeholder Interest in development of Budget

Owners Owners are the individuals who have invested the money and business belongs

to them. Budgets will depict the clear picture of operations and determine their

profitability and income(Ittner and Michels, 2015).

Management Management is Prime authority to know about the budget as they base their

major decisions regarding operations and level of activities as per the budgets.

5

Comparative Summary Forecast 2013 vs Budget 2014

Forecast 2013 Budget 2014 Variance % Variance

Units $ Units $ Units $ Units $

Roadster 2,000 1,00,00,000 2,200 1,14,40,000 200 14,40,000 10.0% 14.4%

Trailer 4,500 1,57,50,000 6,000 2,22,00,000 1,500 64,50,000 33.3% 41.0%

Total 6,500 2,57,50,000 8,200 3,36,40,000 1,700 78,90,000 26.2% 30.6%

PART B REPORTING TO MANAGEMENT

1. Expected Outcomes and Assumptions

To : Senior Management

From : Sales Manager

Respected members,

While preparing the budgets for 2014 it has been assumed that overall Australian market for on

road bikes will grow by 10% in comparison to 2013 and off road will remain stable. This increase

is expected due to population increase and the trend and customer taste is expected to develop in

favour of on road bikes. Further, popularity of Black Helmet's share in case of off road bikes will

increase and therefore resulting into better market share up to 20% is forecasted. Further

considering the inflation rates in Australian economy it is assumed that wholesale prices for bikes

will rise by AUD $ 200 for both the products considering the rise in cost of raw material. Further

improvement in company's products are fetching a rise in quarterly sales.

2.Internal and External stakeholders

Table 4: Internal Stakeholders and interest in Budget

Stakeholder Interest in development of Budget

Owners Owners are the individuals who have invested the money and business belongs

to them. Budgets will depict the clear picture of operations and determine their

profitability and income(Ittner and Michels, 2015).

Management Management is Prime authority to know about the budget as they base their

major decisions regarding operations and level of activities as per the budgets.

5

Employees Employees have interest in Budgets to know the expectation of organisation

from them and knowing the expected production and estimations regarding

their income, perks and bonuses.

Investors Investors are the persons who are willing to invest into Business. By knowing

the expected sales and budgeted profits and operational level they will base

their decision to buy, sell or hold the investment in the company.

Table 5: External Stakeholders and interest in Budget

Stakeholder Interest in development of Budget

Creditors Creditors are the persons who own the business and interested in budget to

know whether the company has sufficient earnings in future to pay off their debt

and financial cost.

Clients Clients are the customers or dealers who are selling and trading in the bikes of

the company therefore want to know how much production is expected and

probability of growing sales.

Government Government is the supreme authority to collect taxes. Through budget it can

have an overview about the tax implications of the company and then compare

the unexpected variances if any(Lowe and Tinker, 2015).

Intermediaries Intermediaries are the agents who arrange for the credit or set up to sale the

bikes and making them available in the market. They are keen to know the level

of operation to ascertain their commission from the company.

3.Approaches and Factors for preparing the Budgets

Budgeting activity is a function of various processes and type of work force and training

imparted to them for completing the budget (Kelly, 2015). Operating budgets should be discussed

with management, stakeholders and all the department heads for effective coordination and decision

making. Although there are various approaches for budgeting but line- item should be followed by

Black Helmet Motorcycle Company. Under this approach all the expensed are bifurcated or divided

into respective functional heads of the company such as Finance, Administration, production etc..

TASK 2 – OPERATIONAL BUDGETS

PART A INVENTORY AND COST OF GOODS SOLD

Table 6: Inventory Budget for 2014

6

from them and knowing the expected production and estimations regarding

their income, perks and bonuses.

Investors Investors are the persons who are willing to invest into Business. By knowing

the expected sales and budgeted profits and operational level they will base

their decision to buy, sell or hold the investment in the company.

Table 5: External Stakeholders and interest in Budget

Stakeholder Interest in development of Budget

Creditors Creditors are the persons who own the business and interested in budget to

know whether the company has sufficient earnings in future to pay off their debt

and financial cost.

Clients Clients are the customers or dealers who are selling and trading in the bikes of

the company therefore want to know how much production is expected and

probability of growing sales.

Government Government is the supreme authority to collect taxes. Through budget it can

have an overview about the tax implications of the company and then compare

the unexpected variances if any(Lowe and Tinker, 2015).

Intermediaries Intermediaries are the agents who arrange for the credit or set up to sale the

bikes and making them available in the market. They are keen to know the level

of operation to ascertain their commission from the company.

3.Approaches and Factors for preparing the Budgets

Budgeting activity is a function of various processes and type of work force and training

imparted to them for completing the budget (Kelly, 2015). Operating budgets should be discussed

with management, stakeholders and all the department heads for effective coordination and decision

making. Although there are various approaches for budgeting but line- item should be followed by

Black Helmet Motorcycle Company. Under this approach all the expensed are bifurcated or divided

into respective functional heads of the company such as Finance, Administration, production etc..

TASK 2 – OPERATIONAL BUDGETS

PART A INVENTORY AND COST OF GOODS SOLD

Table 6: Inventory Budget for 2014

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

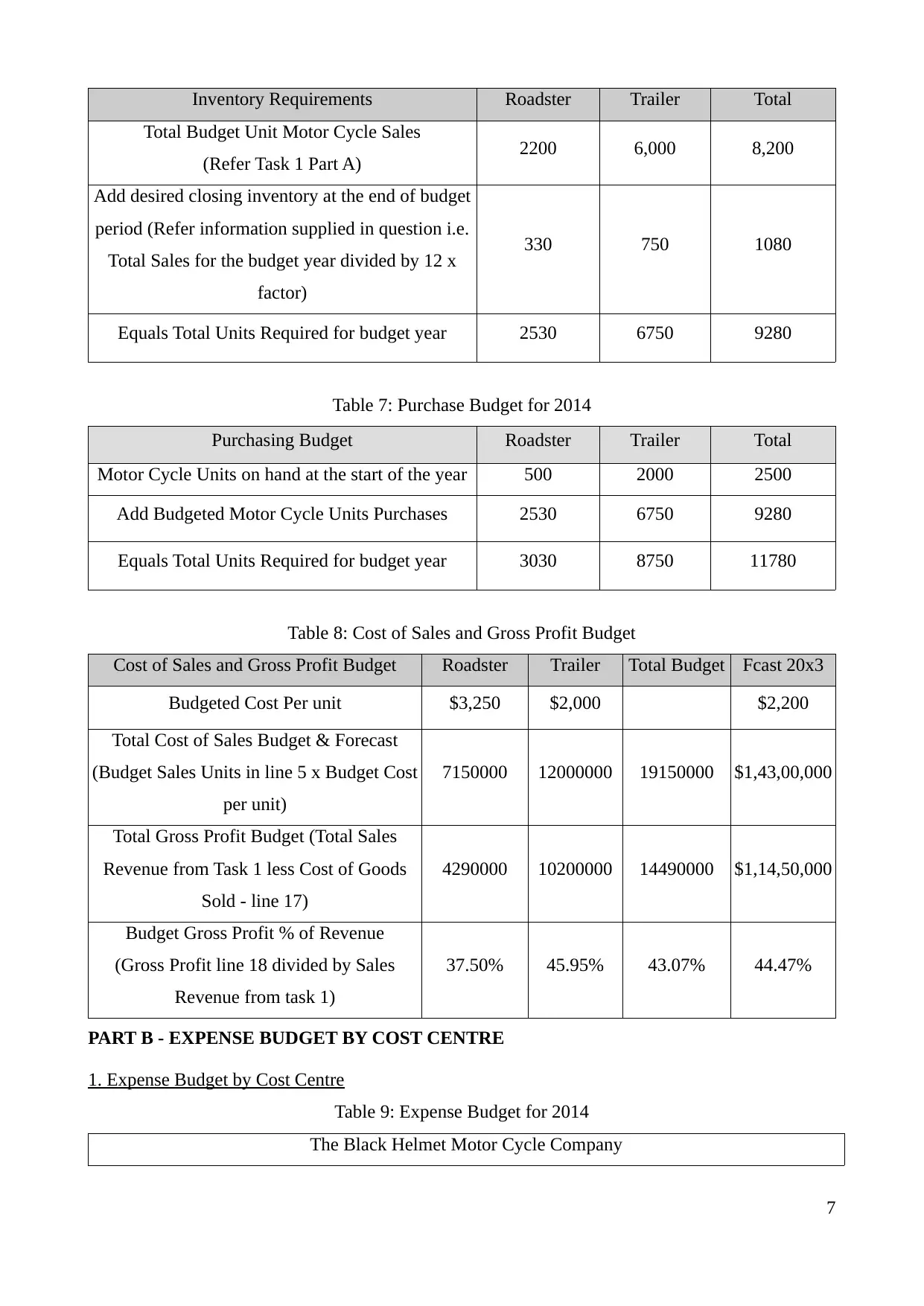

Inventory Requirements Roadster Trailer Total

Total Budget Unit Motor Cycle Sales

(Refer Task 1 Part A) 2200 6,000 8,200

Add desired closing inventory at the end of budget

period (Refer information supplied in question i.e.

Total Sales for the budget year divided by 12 x

factor)

330 750 1080

Equals Total Units Required for budget year 2530 6750 9280

Table 7: Purchase Budget for 2014

Purchasing Budget Roadster Trailer Total

Motor Cycle Units on hand at the start of the year 500 2000 2500

Add Budgeted Motor Cycle Units Purchases 2530 6750 9280

Equals Total Units Required for budget year 3030 8750 11780

Table 8: Cost of Sales and Gross Profit Budget

Cost of Sales and Gross Profit Budget Roadster Trailer Total Budget Fcast 20x3

Budgeted Cost Per unit $3,250 $2,000 $2,200

Total Cost of Sales Budget & Forecast

(Budget Sales Units in line 5 x Budget Cost

per unit)

7150000 12000000 19150000 $1,43,00,000

Total Gross Profit Budget (Total Sales

Revenue from Task 1 less Cost of Goods

Sold - line 17)

4290000 10200000 14490000 $1,14,50,000

Budget Gross Profit % of Revenue

(Gross Profit line 18 divided by Sales

Revenue from task 1)

37.50% 45.95% 43.07% 44.47%

PART B - EXPENSE BUDGET BY COST CENTRE

1. Expense Budget by Cost Centre

Table 9: Expense Budget for 2014

The Black Helmet Motor Cycle Company

7

Total Budget Unit Motor Cycle Sales

(Refer Task 1 Part A) 2200 6,000 8,200

Add desired closing inventory at the end of budget

period (Refer information supplied in question i.e.

Total Sales for the budget year divided by 12 x

factor)

330 750 1080

Equals Total Units Required for budget year 2530 6750 9280

Table 7: Purchase Budget for 2014

Purchasing Budget Roadster Trailer Total

Motor Cycle Units on hand at the start of the year 500 2000 2500

Add Budgeted Motor Cycle Units Purchases 2530 6750 9280

Equals Total Units Required for budget year 3030 8750 11780

Table 8: Cost of Sales and Gross Profit Budget

Cost of Sales and Gross Profit Budget Roadster Trailer Total Budget Fcast 20x3

Budgeted Cost Per unit $3,250 $2,000 $2,200

Total Cost of Sales Budget & Forecast

(Budget Sales Units in line 5 x Budget Cost

per unit)

7150000 12000000 19150000 $1,43,00,000

Total Gross Profit Budget (Total Sales

Revenue from Task 1 less Cost of Goods

Sold - line 17)

4290000 10200000 14490000 $1,14,50,000

Budget Gross Profit % of Revenue

(Gross Profit line 18 divided by Sales

Revenue from task 1)

37.50% 45.95% 43.07% 44.47%

PART B - EXPENSE BUDGET BY COST CENTRE

1. Expense Budget by Cost Centre

Table 9: Expense Budget for 2014

The Black Helmet Motor Cycle Company

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

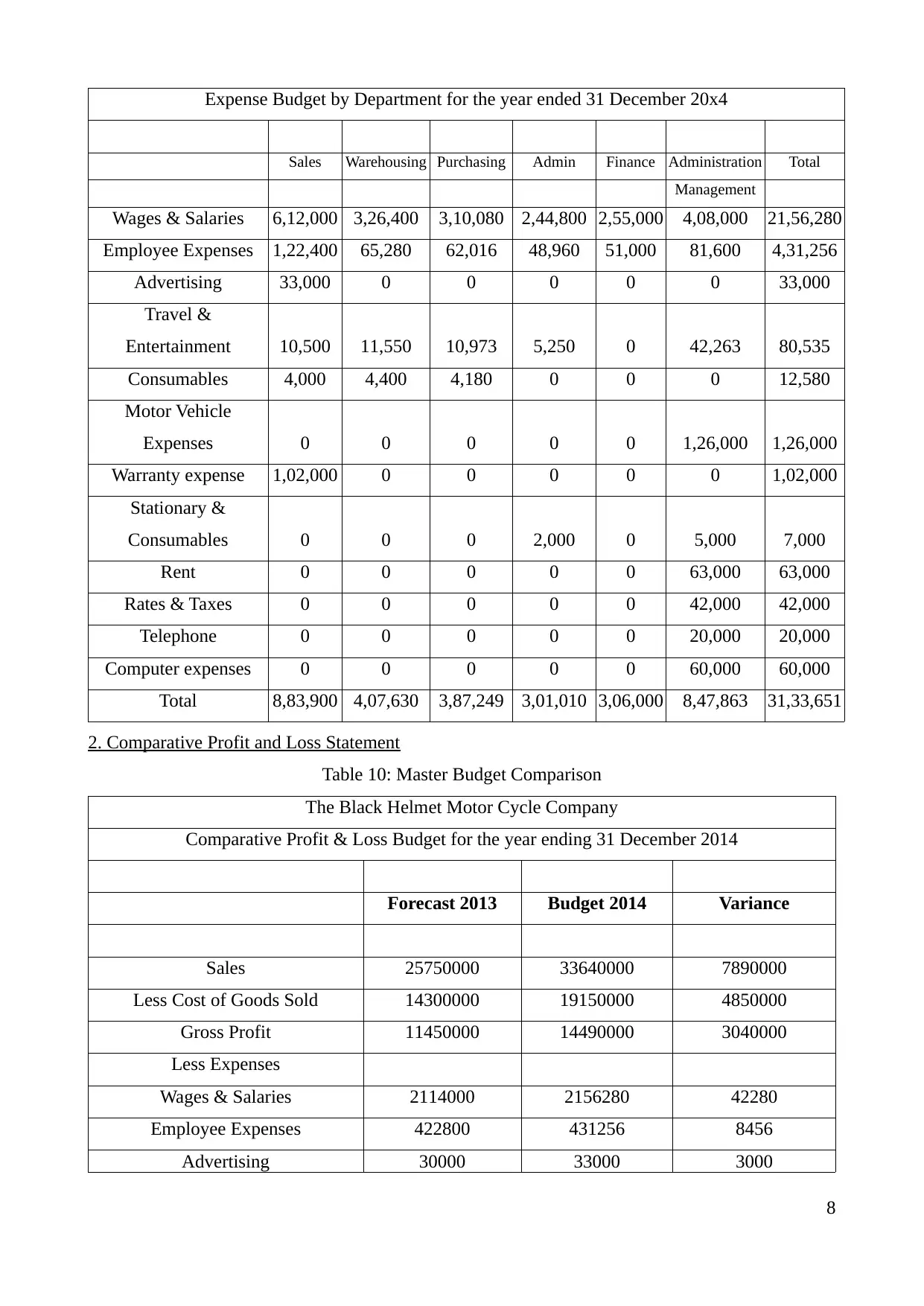

Expense Budget by Department for the year ended 31 December 20x4

Sales Warehousing Purchasing Admin Finance Administration Total

Management

Wages & Salaries 6,12,000 3,26,400 3,10,080 2,44,800 2,55,000 4,08,000 21,56,280

Employee Expenses 1,22,400 65,280 62,016 48,960 51,000 81,600 4,31,256

Advertising 33,000 0 0 0 0 0 33,000

Travel &

Entertainment 10,500 11,550 10,973 5,250 0 42,263 80,535

Consumables 4,000 4,400 4,180 0 0 0 12,580

Motor Vehicle

Expenses 0 0 0 0 0 1,26,000 1,26,000

Warranty expense 1,02,000 0 0 0 0 0 1,02,000

Stationary &

Consumables 0 0 0 2,000 0 5,000 7,000

Rent 0 0 0 0 0 63,000 63,000

Rates & Taxes 0 0 0 0 0 42,000 42,000

Telephone 0 0 0 0 0 20,000 20,000

Computer expenses 0 0 0 0 0 60,000 60,000

Total 8,83,900 4,07,630 3,87,249 3,01,010 3,06,000 8,47,863 31,33,651

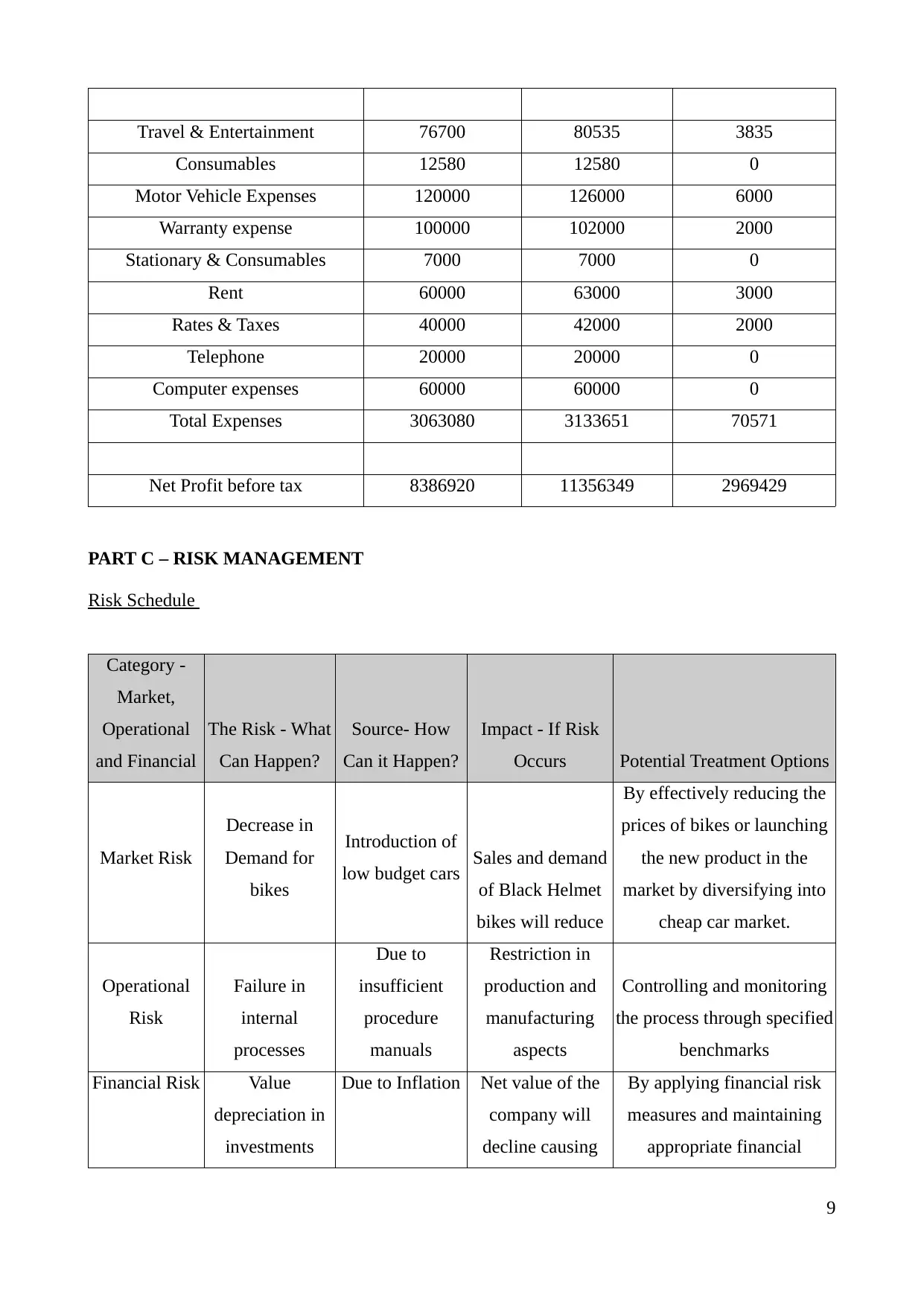

2. Comparative Profit and Loss Statement

Table 10: Master Budget Comparison

The Black Helmet Motor Cycle Company

Comparative Profit & Loss Budget for the year ending 31 December 2014

Forecast 2013 Budget 2014 Variance

Sales 25750000 33640000 7890000

Less Cost of Goods Sold 14300000 19150000 4850000

Gross Profit 11450000 14490000 3040000

Less Expenses

Wages & Salaries 2114000 2156280 42280

Employee Expenses 422800 431256 8456

Advertising 30000 33000 3000

8

Sales Warehousing Purchasing Admin Finance Administration Total

Management

Wages & Salaries 6,12,000 3,26,400 3,10,080 2,44,800 2,55,000 4,08,000 21,56,280

Employee Expenses 1,22,400 65,280 62,016 48,960 51,000 81,600 4,31,256

Advertising 33,000 0 0 0 0 0 33,000

Travel &

Entertainment 10,500 11,550 10,973 5,250 0 42,263 80,535

Consumables 4,000 4,400 4,180 0 0 0 12,580

Motor Vehicle

Expenses 0 0 0 0 0 1,26,000 1,26,000

Warranty expense 1,02,000 0 0 0 0 0 1,02,000

Stationary &

Consumables 0 0 0 2,000 0 5,000 7,000

Rent 0 0 0 0 0 63,000 63,000

Rates & Taxes 0 0 0 0 0 42,000 42,000

Telephone 0 0 0 0 0 20,000 20,000

Computer expenses 0 0 0 0 0 60,000 60,000

Total 8,83,900 4,07,630 3,87,249 3,01,010 3,06,000 8,47,863 31,33,651

2. Comparative Profit and Loss Statement

Table 10: Master Budget Comparison

The Black Helmet Motor Cycle Company

Comparative Profit & Loss Budget for the year ending 31 December 2014

Forecast 2013 Budget 2014 Variance

Sales 25750000 33640000 7890000

Less Cost of Goods Sold 14300000 19150000 4850000

Gross Profit 11450000 14490000 3040000

Less Expenses

Wages & Salaries 2114000 2156280 42280

Employee Expenses 422800 431256 8456

Advertising 30000 33000 3000

8

Travel & Entertainment 76700 80535 3835

Consumables 12580 12580 0

Motor Vehicle Expenses 120000 126000 6000

Warranty expense 100000 102000 2000

Stationary & Consumables 7000 7000 0

Rent 60000 63000 3000

Rates & Taxes 40000 42000 2000

Telephone 20000 20000 0

Computer expenses 60000 60000 0

Total Expenses 3063080 3133651 70571

Net Profit before tax 8386920 11356349 2969429

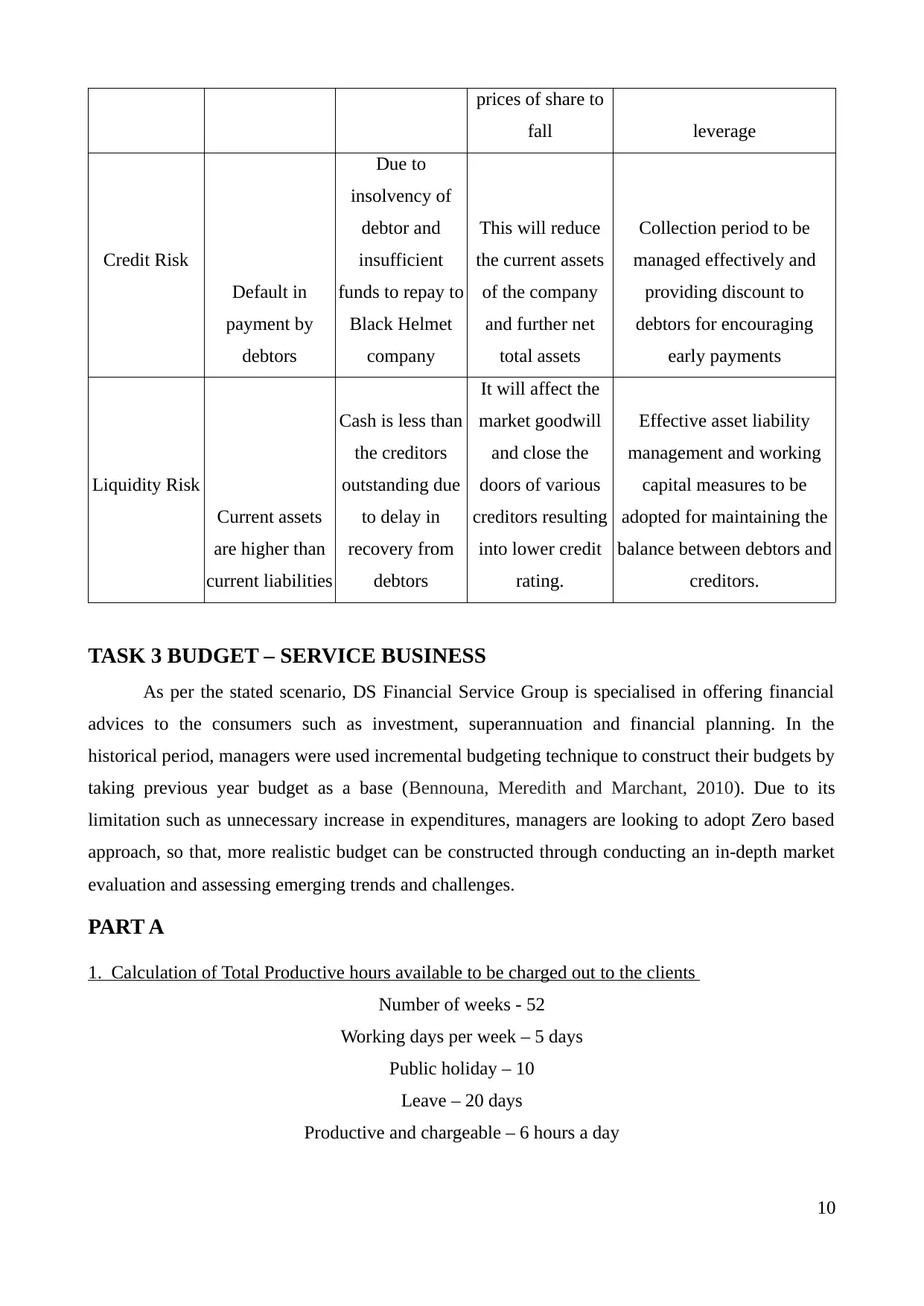

PART C – RISK MANAGEMENT

Risk Schedule

Category -

Market,

Operational

and Financial

The Risk - What

Can Happen?

Source- How

Can it Happen?

Impact - If Risk

Occurs Potential Treatment Options

Market Risk

Decrease in

Demand for

bikes

Introduction of

low budget cars Sales and demand

of Black Helmet

bikes will reduce

By effectively reducing the

prices of bikes or launching

the new product in the

market by diversifying into

cheap car market.

Operational

Risk

Failure in

internal

processes

Due to

insufficient

procedure

manuals

Restriction in

production and

manufacturing

aspects

Controlling and monitoring

the process through specified

benchmarks

Financial Risk Value

depreciation in

investments

Due to Inflation Net value of the

company will

decline causing

By applying financial risk

measures and maintaining

appropriate financial

9

Consumables 12580 12580 0

Motor Vehicle Expenses 120000 126000 6000

Warranty expense 100000 102000 2000

Stationary & Consumables 7000 7000 0

Rent 60000 63000 3000

Rates & Taxes 40000 42000 2000

Telephone 20000 20000 0

Computer expenses 60000 60000 0

Total Expenses 3063080 3133651 70571

Net Profit before tax 8386920 11356349 2969429

PART C – RISK MANAGEMENT

Risk Schedule

Category -

Market,

Operational

and Financial

The Risk - What

Can Happen?

Source- How

Can it Happen?

Impact - If Risk

Occurs Potential Treatment Options

Market Risk

Decrease in

Demand for

bikes

Introduction of

low budget cars Sales and demand

of Black Helmet

bikes will reduce

By effectively reducing the

prices of bikes or launching

the new product in the

market by diversifying into

cheap car market.

Operational

Risk

Failure in

internal

processes

Due to

insufficient

procedure

manuals

Restriction in

production and

manufacturing

aspects

Controlling and monitoring

the process through specified

benchmarks

Financial Risk Value

depreciation in

investments

Due to Inflation Net value of the

company will

decline causing

By applying financial risk

measures and maintaining

appropriate financial

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prices of share to

fall leverage

Credit Risk

Default in

payment by

debtors

Due to

insolvency of

debtor and

insufficient

funds to repay to

Black Helmet

company

This will reduce

the current assets

of the company

and further net

total assets

Collection period to be

managed effectively and

providing discount to

debtors for encouraging

early payments

Liquidity Risk

Current assets

are higher than

current liabilities

Cash is less than

the creditors

outstanding due

to delay in

recovery from

debtors

It will affect the

market goodwill

and close the

doors of various

creditors resulting

into lower credit

rating.

Effective asset liability

management and working

capital measures to be

adopted for maintaining the

balance between debtors and

creditors.

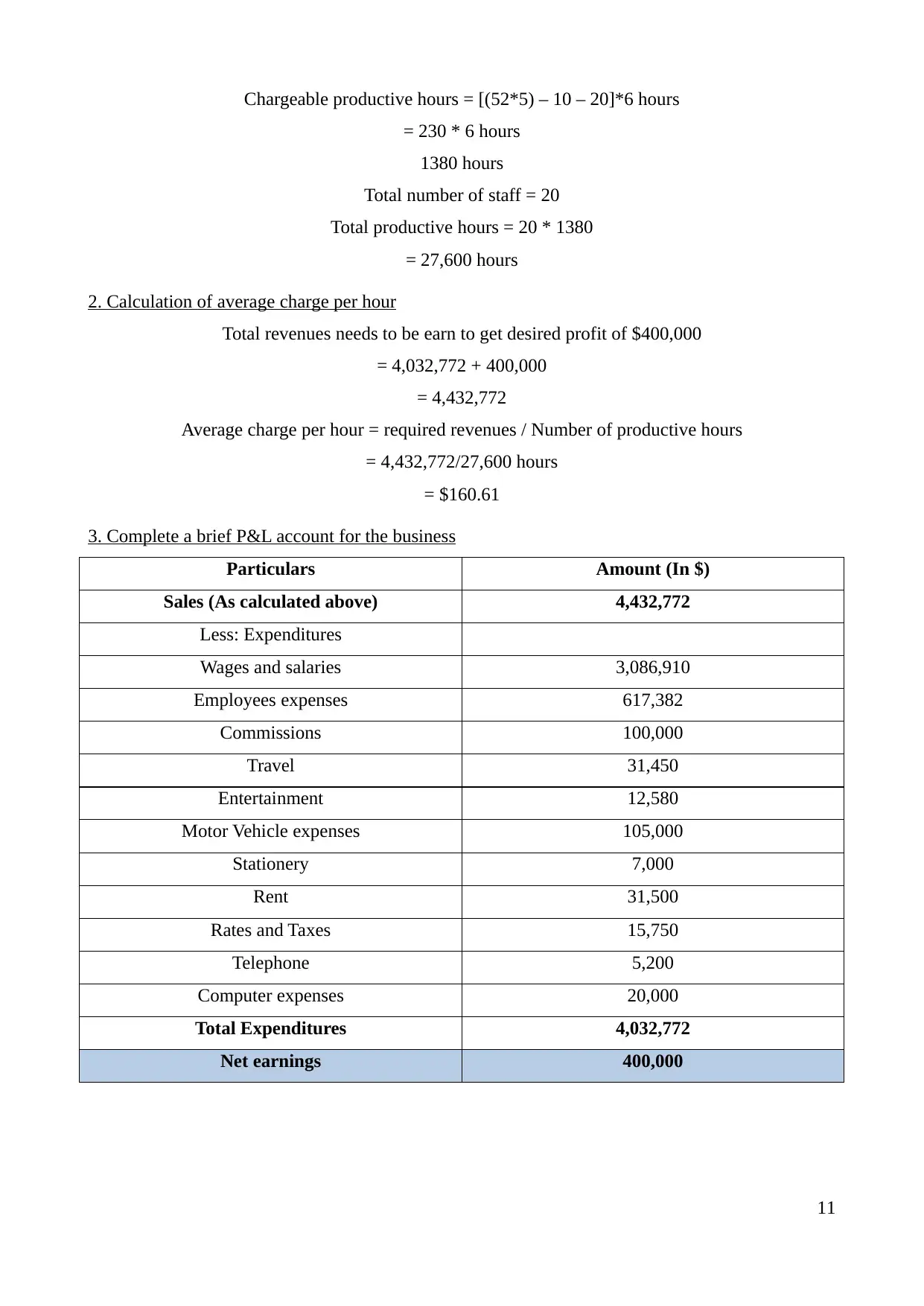

TASK 3 BUDGET – SERVICE BUSINESS

As per the stated scenario, DS Financial Service Group is specialised in offering financial

advices to the consumers such as investment, superannuation and financial planning. In the

historical period, managers were used incremental budgeting technique to construct their budgets by

taking previous year budget as a base (Bennouna, Meredith and Marchant, 2010). Due to its

limitation such as unnecessary increase in expenditures, managers are looking to adopt Zero based

approach, so that, more realistic budget can be constructed through conducting an in-depth market

evaluation and assessing emerging trends and challenges.

PART A

1. Calculation of Total Productive hours available to be charged out to the clients

Number of weeks - 52

Working days per week – 5 days

Public holiday – 10

Leave – 20 days

Productive and chargeable – 6 hours a day

10

fall leverage

Credit Risk

Default in

payment by

debtors

Due to

insolvency of

debtor and

insufficient

funds to repay to

Black Helmet

company

This will reduce

the current assets

of the company

and further net

total assets

Collection period to be

managed effectively and

providing discount to

debtors for encouraging

early payments

Liquidity Risk

Current assets

are higher than

current liabilities

Cash is less than

the creditors

outstanding due

to delay in

recovery from

debtors

It will affect the

market goodwill

and close the

doors of various

creditors resulting

into lower credit

rating.

Effective asset liability

management and working

capital measures to be

adopted for maintaining the

balance between debtors and

creditors.

TASK 3 BUDGET – SERVICE BUSINESS

As per the stated scenario, DS Financial Service Group is specialised in offering financial

advices to the consumers such as investment, superannuation and financial planning. In the

historical period, managers were used incremental budgeting technique to construct their budgets by

taking previous year budget as a base (Bennouna, Meredith and Marchant, 2010). Due to its

limitation such as unnecessary increase in expenditures, managers are looking to adopt Zero based

approach, so that, more realistic budget can be constructed through conducting an in-depth market

evaluation and assessing emerging trends and challenges.

PART A

1. Calculation of Total Productive hours available to be charged out to the clients

Number of weeks - 52

Working days per week – 5 days

Public holiday – 10

Leave – 20 days

Productive and chargeable – 6 hours a day

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chargeable productive hours = [(52*5) – 10 – 20]*6 hours

= 230 * 6 hours

1380 hours

Total number of staff = 20

Total productive hours = 20 * 1380

= 27,600 hours

2. Calculation of average charge per hour

Total revenues needs to be earn to get desired profit of $400,000

= 4,032,772 + 400,000

= 4,432,772

Average charge per hour = required revenues / Number of productive hours

= 4,432,772/27,600 hours

= $160.61

3. Complete a brief P&L account for the business

Particulars Amount (In $)

Sales (As calculated above) 4,432,772

Less: Expenditures

Wages and salaries 3,086,910

Employees expenses 617,382

Commissions 100,000

Travel 31,450

Entertainment 12,580

Motor Vehicle expenses 105,000

Stationery 7,000

Rent 31,500

Rates and Taxes 15,750

Telephone 5,200

Computer expenses 20,000

Total Expenditures 4,032,772

Net earnings 400,000

11

= 230 * 6 hours

1380 hours

Total number of staff = 20

Total productive hours = 20 * 1380

= 27,600 hours

2. Calculation of average charge per hour

Total revenues needs to be earn to get desired profit of $400,000

= 4,032,772 + 400,000

= 4,432,772

Average charge per hour = required revenues / Number of productive hours

= 4,432,772/27,600 hours

= $160.61

3. Complete a brief P&L account for the business

Particulars Amount (In $)

Sales (As calculated above) 4,432,772

Less: Expenditures

Wages and salaries 3,086,910

Employees expenses 617,382

Commissions 100,000

Travel 31,450

Entertainment 12,580

Motor Vehicle expenses 105,000

Stationery 7,000

Rent 31,500

Rates and Taxes 15,750

Telephone 5,200

Computer expenses 20,000

Total Expenditures 4,032,772

Net earnings 400,000

11

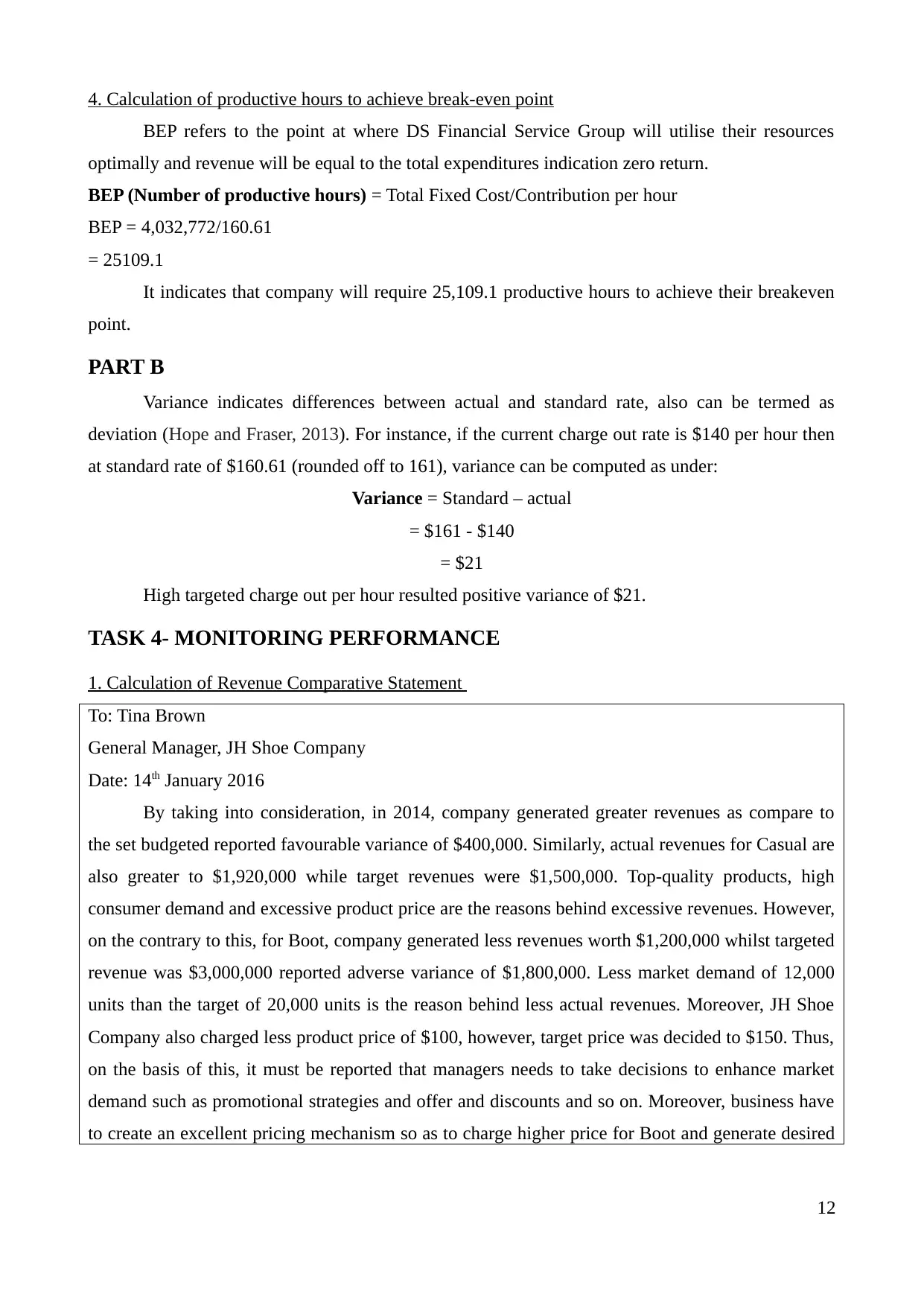

4. Calculation of productive hours to achieve break-even point

BEP refers to the point at where DS Financial Service Group will utilise their resources

optimally and revenue will be equal to the total expenditures indication zero return.

BEP (Number of productive hours) = Total Fixed Cost/Contribution per hour

BEP = 4,032,772/160.61

= 25109.1

It indicates that company will require 25,109.1 productive hours to achieve their breakeven

point.

PART B

Variance indicates differences between actual and standard rate, also can be termed as

deviation (Hope and Fraser, 2013). For instance, if the current charge out rate is $140 per hour then

at standard rate of $160.61 (rounded off to 161), variance can be computed as under:

Variance = Standard – actual

= $161 - $140

= $21

High targeted charge out per hour resulted positive variance of $21.

TASK 4- MONITORING PERFORMANCE

1. Calculation of Revenue Comparative Statement

To: Tina Brown

General Manager, JH Shoe Company

Date: 14th January 2016

By taking into consideration, in 2014, company generated greater revenues as compare to

the set budgeted reported favourable variance of $400,000. Similarly, actual revenues for Casual are

also greater to $1,920,000 while target revenues were $1,500,000. Top-quality products, high

consumer demand and excessive product price are the reasons behind excessive revenues. However,

on the contrary to this, for Boot, company generated less revenues worth $1,200,000 whilst targeted

revenue was $3,000,000 reported adverse variance of $1,800,000. Less market demand of 12,000

units than the target of 20,000 units is the reason behind less actual revenues. Moreover, JH Shoe

Company also charged less product price of $100, however, target price was decided to $150. Thus,

on the basis of this, it must be reported that managers needs to take decisions to enhance market

demand such as promotional strategies and offer and discounts and so on. Moreover, business have

to create an excellent pricing mechanism so as to charge higher price for Boot and generate desired

12

BEP refers to the point at where DS Financial Service Group will utilise their resources

optimally and revenue will be equal to the total expenditures indication zero return.

BEP (Number of productive hours) = Total Fixed Cost/Contribution per hour

BEP = 4,032,772/160.61

= 25109.1

It indicates that company will require 25,109.1 productive hours to achieve their breakeven

point.

PART B

Variance indicates differences between actual and standard rate, also can be termed as

deviation (Hope and Fraser, 2013). For instance, if the current charge out rate is $140 per hour then

at standard rate of $160.61 (rounded off to 161), variance can be computed as under:

Variance = Standard – actual

= $161 - $140

= $21

High targeted charge out per hour resulted positive variance of $21.

TASK 4- MONITORING PERFORMANCE

1. Calculation of Revenue Comparative Statement

To: Tina Brown

General Manager, JH Shoe Company

Date: 14th January 2016

By taking into consideration, in 2014, company generated greater revenues as compare to

the set budgeted reported favourable variance of $400,000. Similarly, actual revenues for Casual are

also greater to $1,920,000 while target revenues were $1,500,000. Top-quality products, high

consumer demand and excessive product price are the reasons behind excessive revenues. However,

on the contrary to this, for Boot, company generated less revenues worth $1,200,000 whilst targeted

revenue was $3,000,000 reported adverse variance of $1,800,000. Less market demand of 12,000

units than the target of 20,000 units is the reason behind less actual revenues. Moreover, JH Shoe

Company also charged less product price of $100, however, target price was decided to $150. Thus,

on the basis of this, it must be reported that managers needs to take decisions to enhance market

demand such as promotional strategies and offer and discounts and so on. Moreover, business have

to create an excellent pricing mechanism so as to charge higher price for Boot and generate desired

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.