Financial Management Report: Sainsbury's PLC Analysis and Appraisal

VerifiedAdded on 2019/12/03

|24

|5045

|246

Report

AI Summary

This report provides a financial analysis of Sainsbury's PLC, a company listed on the London Stock Exchange. The analysis is divided into two main parts. Part 1 focuses on the calculation and interpretation of various financial ratios, including liquidity, efficiency/turnover, profitability, and performance ratios, using data from 2010 to 2012. The report provides a detailed examination of each ratio, comparing Sainsbury's performance against industry standards and highlighting trends. Part 2 covers investment appraisal techniques, specifically Net Present Value (NPV) and Payback Period methods, applied to hypothetical projects. The report calculates and compares the financial viability of two projects, discussing the advantages and disadvantages of each method. The conclusion summarizes the key findings and offers insights into Sainsbury's financial health and investment potential.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

Part 1................................................................................................................................................4

1.1: Calculation of Ratios............................................................................................................4

1.2: Ratio Analysis.......................................................................................................................7

1.3: Summarized Report..............................................................................................................9

Part 2: Investment Appraisal for PLC plc......................................................................................10

2.1: Project Appraisal...............................................................................................................10

2.2: Payback Period Method......................................................................................................14

2.3: Advantages and disadvantages of the investment appraisal methods................................15

2.4: Summarized Report............................................................................................................16

CONCLUSION..............................................................................................................................17

Reference.......................................................................................................................................18

Appendix........................................................................................................................................19

Introduction......................................................................................................................................4

Part 1................................................................................................................................................4

1.1: Calculation of Ratios............................................................................................................4

1.2: Ratio Analysis.......................................................................................................................7

1.3: Summarized Report..............................................................................................................9

Part 2: Investment Appraisal for PLC plc......................................................................................10

2.1: Project Appraisal...............................................................................................................10

2.2: Payback Period Method......................................................................................................14

2.3: Advantages and disadvantages of the investment appraisal methods................................15

2.4: Summarized Report............................................................................................................16

CONCLUSION..............................................................................................................................17

Reference.......................................................................................................................................18

Appendix........................................................................................................................................19

List of Tables

Table 1: Ratio Analysis of Sainsbury..............................................................................................7

Table 2 : Summarized Report..........................................................................................................9

Table 3 : Cash Flow for Two Projects...........................................................................................10

Table 4 : NPV at 10%....................................................................................................................11

Table 5 : NPV of Project 1............................................................................................................12

Table 6 : NPV of Project 2............................................................................................................12

Table 7 : Payback Period of Project 1...........................................................................................14

Table 8 : Payback Period of Project 2...........................................................................................14

Table 1: Ratio Analysis of Sainsbury..............................................................................................7

Table 2 : Summarized Report..........................................................................................................9

Table 3 : Cash Flow for Two Projects...........................................................................................10

Table 4 : NPV at 10%....................................................................................................................11

Table 5 : NPV of Project 1............................................................................................................12

Table 6 : NPV of Project 2............................................................................................................12

Table 7 : Payback Period of Project 1...........................................................................................14

Table 8 : Payback Period of Project 2...........................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Financial analysis of a company indicates its position in the market. This can be done in 2

ways either through fundamental analysis or through technical analysis. Both these analysis

depicts companies’ financial information with a difference that former does in tabular form and

latter in chart forms. In modern world, analysts prefer to do technical analysis of the company.

Fundamental tool consists of various analysis of the company like that of ratio analysis, balance

sheet, income statement etc. It also helps in determining the suitability for investment of

company (Arnold, 2005).

Part 1

1.1: Calculation of Ratios

Sainsbury’s plc shares are traded on London Stock Exchange (LSE) and it is a part of FTSE-100

Index.

Ratio analysis – is the systematic use of available accounting information required to evaluate

the financial statements of the company. It also reveals the financial and operating performance

of the firm. Ratio analysis includes judgment for a valuable evaluation of the financial

statements. Sainsbury’s performance ratios include liquidity ratio, profitability margin, and

efficiency / turnover ratio (Atrill, and McLaney, 2008).

Liquidity Ratio –computes the current status of the firm whether it can pay its current liabilities

in short term or not. This ratio depicts financial solvency of a firm in short term. Every business

firm is aware that it should not suffer from lack of liquidity. If a firm is not capable to meet its

short term obligation that means it has a bad credit image. On the other hand, firm with high

liquidity is also not attractive as it implies that firm has funds, cash in hand which are not used to

earn anything. So, it is essential to balance between liquidity and lack of the same. Liquidity

ratio can be further classified as –

Current Ratio –is the connection between current assets and liabilities. It computes the

short term solvency of a company and can be calculated by dividing current assets with

current liabilities.

Current Ratio = Current Asset / Current Liabilities

In this, current assets includes bank balance and cash in hand, debtors and inventory,

marketable securities excluding provision for doubtful debtors and bad debts, prepaid

expenses and bills receivables. Current liabilities entail bills payable, sundry creditors,

Financial analysis of a company indicates its position in the market. This can be done in 2

ways either through fundamental analysis or through technical analysis. Both these analysis

depicts companies’ financial information with a difference that former does in tabular form and

latter in chart forms. In modern world, analysts prefer to do technical analysis of the company.

Fundamental tool consists of various analysis of the company like that of ratio analysis, balance

sheet, income statement etc. It also helps in determining the suitability for investment of

company (Arnold, 2005).

Part 1

1.1: Calculation of Ratios

Sainsbury’s plc shares are traded on London Stock Exchange (LSE) and it is a part of FTSE-100

Index.

Ratio analysis – is the systematic use of available accounting information required to evaluate

the financial statements of the company. It also reveals the financial and operating performance

of the firm. Ratio analysis includes judgment for a valuable evaluation of the financial

statements. Sainsbury’s performance ratios include liquidity ratio, profitability margin, and

efficiency / turnover ratio (Atrill, and McLaney, 2008).

Liquidity Ratio –computes the current status of the firm whether it can pay its current liabilities

in short term or not. This ratio depicts financial solvency of a firm in short term. Every business

firm is aware that it should not suffer from lack of liquidity. If a firm is not capable to meet its

short term obligation that means it has a bad credit image. On the other hand, firm with high

liquidity is also not attractive as it implies that firm has funds, cash in hand which are not used to

earn anything. So, it is essential to balance between liquidity and lack of the same. Liquidity

ratio can be further classified as –

Current Ratio –is the connection between current assets and liabilities. It computes the

short term solvency of a company and can be calculated by dividing current assets with

current liabilities.

Current Ratio = Current Asset / Current Liabilities

In this, current assets includes bank balance and cash in hand, debtors and inventory,

marketable securities excluding provision for doubtful debtors and bad debts, prepaid

expenses and bills receivables. Current liabilities entail bills payable, sundry creditors,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income – tax liability, short term loans and dividends payable and accrued expenses

(Atrill, 2009). Acid Test Ratio –is used to calculate the liquidity of the firm and is a corresponding ratio

to the current ratio.

Acid Test Ratio = Quick Assets / Current liabilities

In the above formula, quick assets are known as those assets which are immediately

converted in cash form without loss of its value. They include bank balance, cash in hand,

bill’s receivables, sundry debtors and marketable securities.

Cash Ratio – it calculates relationship between super quick current assets and liabilities.

In this, ratio assets are described as bank balance, cash in hand and quick marketable

securities. It is calculated by dividing absolute liquid assets from current liabilities.

Cash Ratio = Absolute Liquid Assets / Current Liabilities

Efficiency / Turnover Ratio – by the use of this ratio a firm manage its current assets. There are

following ratios which help in judging efficiency of assets (Bennouna, Meredith, and Marchant,

2010).

Inventory Turnover Ratio – inventory is the most important part of any business firm.

This ratio indicates that how many times a firm has converted its inventory into sales.

Inventory turnover ratio = Cost of goods sold / Average Inventory

Where average inventory = opening balance + closing balance / 2

But in some circumstances opening balance of the inventory is not given, and then the

closing balance is treated as average inventory.

Creditor Turnover Ratio – it means how many times in a year firm is paying money to its

sundry creditors. It judges the requirements of paying cash to its sundry creditors.

Creditor Turnover Ratio = Net Credit Purchase / Average Trade Creditor

Where net credit purchase = gross credit purchase – purchase return

But when information about opening and closing balance, credit purchases of trade

creditors is not given then the ratio is calculated as:

Creditor Turnover Ratio = Total Purchase / Total Trade Creditors

Debtor Turnover Ratio – this indicates that how much times debtors had paid or they are

converted into cash in a period. It is calculated as follows:

Debtor Turnover Ratio = Net Credit Sales / Average Trade Debtors

(Atrill, 2009). Acid Test Ratio –is used to calculate the liquidity of the firm and is a corresponding ratio

to the current ratio.

Acid Test Ratio = Quick Assets / Current liabilities

In the above formula, quick assets are known as those assets which are immediately

converted in cash form without loss of its value. They include bank balance, cash in hand,

bill’s receivables, sundry debtors and marketable securities.

Cash Ratio – it calculates relationship between super quick current assets and liabilities.

In this, ratio assets are described as bank balance, cash in hand and quick marketable

securities. It is calculated by dividing absolute liquid assets from current liabilities.

Cash Ratio = Absolute Liquid Assets / Current Liabilities

Efficiency / Turnover Ratio – by the use of this ratio a firm manage its current assets. There are

following ratios which help in judging efficiency of assets (Bennouna, Meredith, and Marchant,

2010).

Inventory Turnover Ratio – inventory is the most important part of any business firm.

This ratio indicates that how many times a firm has converted its inventory into sales.

Inventory turnover ratio = Cost of goods sold / Average Inventory

Where average inventory = opening balance + closing balance / 2

But in some circumstances opening balance of the inventory is not given, and then the

closing balance is treated as average inventory.

Creditor Turnover Ratio – it means how many times in a year firm is paying money to its

sundry creditors. It judges the requirements of paying cash to its sundry creditors.

Creditor Turnover Ratio = Net Credit Purchase / Average Trade Creditor

Where net credit purchase = gross credit purchase – purchase return

But when information about opening and closing balance, credit purchases of trade

creditors is not given then the ratio is calculated as:

Creditor Turnover Ratio = Total Purchase / Total Trade Creditors

Debtor Turnover Ratio – this indicates that how much times debtors had paid or they are

converted into cash in a period. It is calculated as follows:

Debtor Turnover Ratio = Net Credit Sales / Average Trade Debtors

Where net credit sales = gross credit sale – sales return

&

Average trade debtors = opening + closing balance / 2

But when information of trade debtors is not available then it is calculated by following

method:

Debtor Turnover Ratio = Total Sales / Trade Debtors

Assets Turnover Ratio –shows the relationship between assets and sales. It is computed

by following formula:

Assets Turnover Ratio = Cost of goods sold / Average Total Assets

Profitability Raito – it measures the firms’ profitability. In the context of profitability, it

measures the operating efficiency of a firm and its ability to ensure adequate return in terms of

profits. Profitability ratio includes gross profit margin and net profit margin (Collier, 2012).

Gross Profit Margin - it measures the relationship between gross profit and sales. It is

calculated by following formula:

Gross Profit Margin = (Gross profit / Net sales) * 100

It is the difference between sales and cost of goods sold.

Net Profit Margin - it is a relationship between net profits and sales of a firm. Further, it

depicts the efficiency of firm’s management in administrating, manufacturing and selling

the products. It is calculated by the following formula:

Net Profit Margin = (Earnings after Tax / Net Sales) * 100

Performance Ratio – It provides relationship between returns of the firm and its total

investments. It is further divided in major four parts which are as follows (Dauber, 2012).

Return on Assets - it provides a relationship between net profits and net assets. To

calculate this ratio net profits and assets can be determined in various ways.

Return on Assets = (Net Profit after Tax / Average total assets) * 100

Return on Capital Employed – it provides relationship between capital employed and net

profit of the firm. Capital employed means funds are supplied by the owners and lenders.

Further it can be calculated as follows:

Return on Capital Employed = (Net Profit after Tax / Total capital Employed) * 100

&

Average trade debtors = opening + closing balance / 2

But when information of trade debtors is not available then it is calculated by following

method:

Debtor Turnover Ratio = Total Sales / Trade Debtors

Assets Turnover Ratio –shows the relationship between assets and sales. It is computed

by following formula:

Assets Turnover Ratio = Cost of goods sold / Average Total Assets

Profitability Raito – it measures the firms’ profitability. In the context of profitability, it

measures the operating efficiency of a firm and its ability to ensure adequate return in terms of

profits. Profitability ratio includes gross profit margin and net profit margin (Collier, 2012).

Gross Profit Margin - it measures the relationship between gross profit and sales. It is

calculated by following formula:

Gross Profit Margin = (Gross profit / Net sales) * 100

It is the difference between sales and cost of goods sold.

Net Profit Margin - it is a relationship between net profits and sales of a firm. Further, it

depicts the efficiency of firm’s management in administrating, manufacturing and selling

the products. It is calculated by the following formula:

Net Profit Margin = (Earnings after Tax / Net Sales) * 100

Performance Ratio – It provides relationship between returns of the firm and its total

investments. It is further divided in major four parts which are as follows (Dauber, 2012).

Return on Assets - it provides a relationship between net profits and net assets. To

calculate this ratio net profits and assets can be determined in various ways.

Return on Assets = (Net Profit after Tax / Average total assets) * 100

Return on Capital Employed – it provides relationship between capital employed and net

profit of the firm. Capital employed means funds are supplied by the owners and lenders.

Further it can be calculated as follows:

Return on Capital Employed = (Net Profit after Tax / Total capital Employed) * 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on Equity – it renders relationship between return to the sources of funds or

relationship between net profits and equity shareholders funds of the firm. It is calculated

as following:

Return on Equity = Net Profit after Tax / Total Shareholder's Equity

Earnings per Share – it measures the profit available for the shareholders on per share. It

is calculated as follows:

Earnings per Share = Net Profit Available to Equity Holders / Number of shares

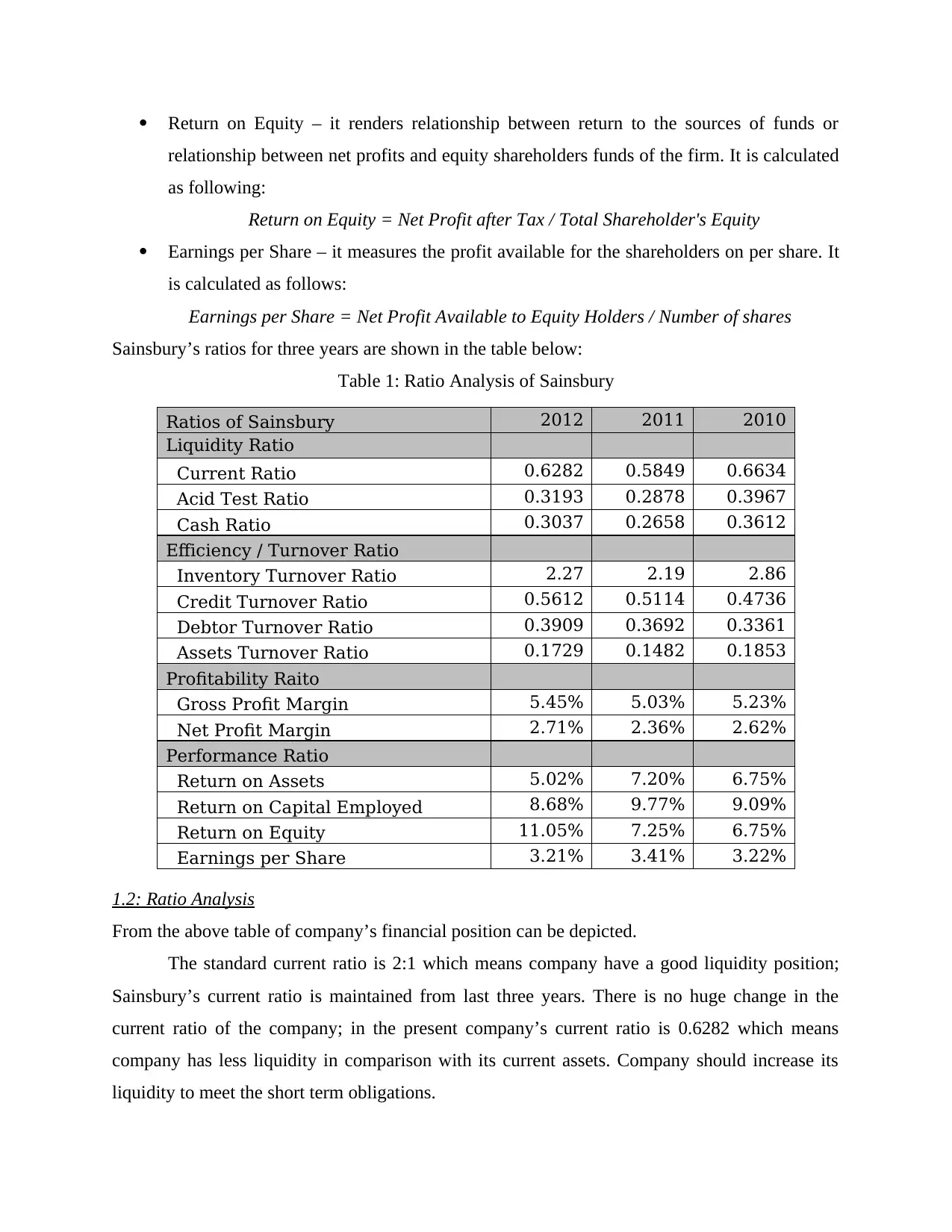

Sainsbury’s ratios for three years are shown in the table below:

Table 1: Ratio Analysis of Sainsbury

Ratios of Sainsbury 2012 2011 2010

Liquidity Ratio

Current Ratio 0.6282 0.5849 0.6634

Acid Test Ratio 0.3193 0.2878 0.3967

Cash Ratio 0.3037 0.2658 0.3612

Efficiency / Turnover Ratio

Inventory Turnover Ratio 2.27 2.19 2.86

Credit Turnover Ratio 0.5612 0.5114 0.4736

Debtor Turnover Ratio 0.3909 0.3692 0.3361

Assets Turnover Ratio 0.1729 0.1482 0.1853

Profitability Raito

Gross Profit Margin 5.45% 5.03% 5.23%

Net Profit Margin 2.71% 2.36% 2.62%

Performance Ratio

Return on Assets 5.02% 7.20% 6.75%

Return on Capital Employed 8.68% 9.77% 9.09%

Return on Equity 11.05% 7.25% 6.75%

Earnings per Share 3.21% 3.41% 3.22%

1.2: Ratio Analysis

From the above table of company’s financial position can be depicted.

The standard current ratio is 2:1 which means company have a good liquidity position;

Sainsbury’s current ratio is maintained from last three years. There is no huge change in the

current ratio of the company; in the present company’s current ratio is 0.6282 which means

company has less liquidity in comparison with its current assets. Company should increase its

liquidity to meet the short term obligations.

relationship between net profits and equity shareholders funds of the firm. It is calculated

as following:

Return on Equity = Net Profit after Tax / Total Shareholder's Equity

Earnings per Share – it measures the profit available for the shareholders on per share. It

is calculated as follows:

Earnings per Share = Net Profit Available to Equity Holders / Number of shares

Sainsbury’s ratios for three years are shown in the table below:

Table 1: Ratio Analysis of Sainsbury

Ratios of Sainsbury 2012 2011 2010

Liquidity Ratio

Current Ratio 0.6282 0.5849 0.6634

Acid Test Ratio 0.3193 0.2878 0.3967

Cash Ratio 0.3037 0.2658 0.3612

Efficiency / Turnover Ratio

Inventory Turnover Ratio 2.27 2.19 2.86

Credit Turnover Ratio 0.5612 0.5114 0.4736

Debtor Turnover Ratio 0.3909 0.3692 0.3361

Assets Turnover Ratio 0.1729 0.1482 0.1853

Profitability Raito

Gross Profit Margin 5.45% 5.03% 5.23%

Net Profit Margin 2.71% 2.36% 2.62%

Performance Ratio

Return on Assets 5.02% 7.20% 6.75%

Return on Capital Employed 8.68% 9.77% 9.09%

Return on Equity 11.05% 7.25% 6.75%

Earnings per Share 3.21% 3.41% 3.22%

1.2: Ratio Analysis

From the above table of company’s financial position can be depicted.

The standard current ratio is 2:1 which means company have a good liquidity position;

Sainsbury’s current ratio is maintained from last three years. There is no huge change in the

current ratio of the company; in the present company’s current ratio is 0.6282 which means

company has less liquidity in comparison with its current assets. Company should increase its

liquidity to meet the short term obligations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A satisfactory acid test ratio is 1:1 which means a firm having equal liquidity to its

current assets. Sainsbury’s acid test ratio is approximately same for the last three years. But

when it is compared to standard it did not seems quite well. Company should decrease its current

liabilities because the current assets are the in a good position (Drury, 2008).

Cash ratios of Sainsbury depicts that company did not have much cash in hand or cast at

bank. But they are capable enough to meet their day to day expenses. Company should

concentrate on sale which can increase its profits and liquidity.

A turnover ratio of the company depicts the good position of its turnover.

In the last year company had inventory turnover ratio at 2.27, which means company in turning

its goods into sales more than two times in year. Conversion of goods into sales will results it in

maintaining cash and liquidity. From the last two years the ratio is decreasing which is quite

thoughtful for its managers.

Credit turnover ratio of the company is increasing from the last two years which means

company is able to make payments to its creditors. In the current situation company is paying

more than three times in a year, which means company had a good liaising with its creditor and

suppliers.

Debtor turnover ratio of the company is increasing from the last two years which means

company’s debtors are paying them at time. The debtor turnover ratio in the FY 2012 is at

0.3909 which means company is able to collect money 4 times in a year.

Assets turnover ratio of the company is good in the current situation; it means company is

capable to generate money, in the comparison with its current assets. In the FY year 2012 the

asset turnover ratio of company is 0.1729, which means company can meet any kind of short

term obligations (Mclaney, 2006).

Profitability Ratio depicts the current position of the company, whether it can sustain in

long run or not. Profitability there is two types of profitability ratio is calculated for the

company.

Gross Profit Margin or Ratio of the company is 5.45% for the FY 2012. It is increasing

from last year. Gross profit margin is calculated after deducting tax, dividend and interest.

Sainsbury’s net operating income is high but there net income is very low which means company

is paying good dividend to its stake holders.

current assets. Sainsbury’s acid test ratio is approximately same for the last three years. But

when it is compared to standard it did not seems quite well. Company should decrease its current

liabilities because the current assets are the in a good position (Drury, 2008).

Cash ratios of Sainsbury depicts that company did not have much cash in hand or cast at

bank. But they are capable enough to meet their day to day expenses. Company should

concentrate on sale which can increase its profits and liquidity.

A turnover ratio of the company depicts the good position of its turnover.

In the last year company had inventory turnover ratio at 2.27, which means company in turning

its goods into sales more than two times in year. Conversion of goods into sales will results it in

maintaining cash and liquidity. From the last two years the ratio is decreasing which is quite

thoughtful for its managers.

Credit turnover ratio of the company is increasing from the last two years which means

company is able to make payments to its creditors. In the current situation company is paying

more than three times in a year, which means company had a good liaising with its creditor and

suppliers.

Debtor turnover ratio of the company is increasing from the last two years which means

company’s debtors are paying them at time. The debtor turnover ratio in the FY 2012 is at

0.3909 which means company is able to collect money 4 times in a year.

Assets turnover ratio of the company is good in the current situation; it means company is

capable to generate money, in the comparison with its current assets. In the FY year 2012 the

asset turnover ratio of company is 0.1729, which means company can meet any kind of short

term obligations (Mclaney, 2006).

Profitability Ratio depicts the current position of the company, whether it can sustain in

long run or not. Profitability there is two types of profitability ratio is calculated for the

company.

Gross Profit Margin or Ratio of the company is 5.45% for the FY 2012. It is increasing

from last year. Gross profit margin is calculated after deducting tax, dividend and interest.

Sainsbury’s net operating income is high but there net income is very low which means company

is paying good dividend to its stake holders.

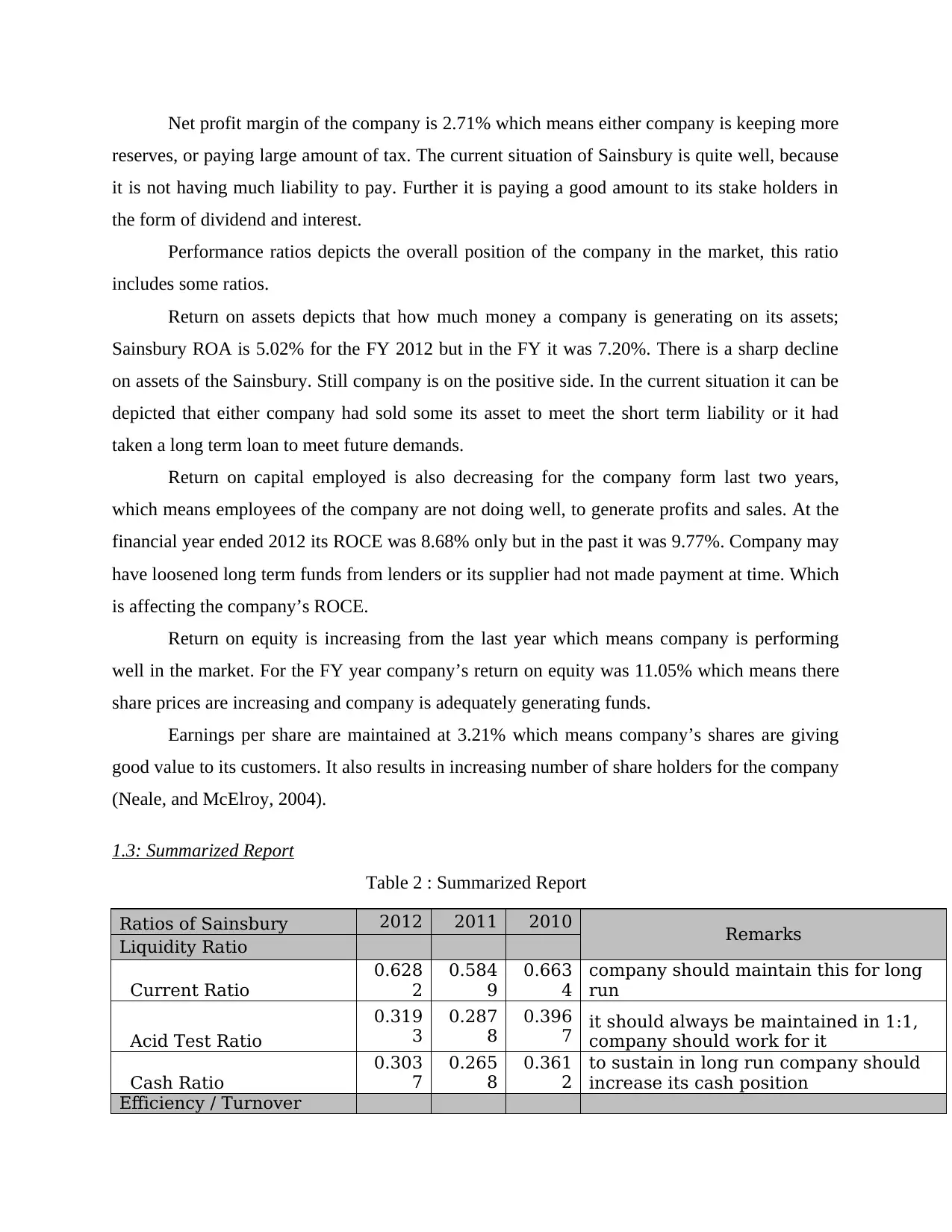

Net profit margin of the company is 2.71% which means either company is keeping more

reserves, or paying large amount of tax. The current situation of Sainsbury is quite well, because

it is not having much liability to pay. Further it is paying a good amount to its stake holders in

the form of dividend and interest.

Performance ratios depicts the overall position of the company in the market, this ratio

includes some ratios.

Return on assets depicts that how much money a company is generating on its assets;

Sainsbury ROA is 5.02% for the FY 2012 but in the FY it was 7.20%. There is a sharp decline

on assets of the Sainsbury. Still company is on the positive side. In the current situation it can be

depicted that either company had sold some its asset to meet the short term liability or it had

taken a long term loan to meet future demands.

Return on capital employed is also decreasing for the company form last two years,

which means employees of the company are not doing well, to generate profits and sales. At the

financial year ended 2012 its ROCE was 8.68% only but in the past it was 9.77%. Company may

have loosened long term funds from lenders or its supplier had not made payment at time. Which

is affecting the company’s ROCE.

Return on equity is increasing from the last year which means company is performing

well in the market. For the FY year company’s return on equity was 11.05% which means there

share prices are increasing and company is adequately generating funds.

Earnings per share are maintained at 3.21% which means company’s shares are giving

good value to its customers. It also results in increasing number of share holders for the company

(Neale, and McElroy, 2004).

1.3: Summarized Report

Table 2 : Summarized Report

Ratios of Sainsbury 2012 2011 2010 Remarks

Liquidity Ratio

Current Ratio

0.628

2

0.584

9

0.663

4

company should maintain this for long

run

Acid Test Ratio

0.319

3

0.287

8

0.396

7 it should always be maintained in 1:1,

company should work for it

Cash Ratio

0.303

7

0.265

8

0.361

2

to sustain in long run company should

increase its cash position

Efficiency / Turnover

reserves, or paying large amount of tax. The current situation of Sainsbury is quite well, because

it is not having much liability to pay. Further it is paying a good amount to its stake holders in

the form of dividend and interest.

Performance ratios depicts the overall position of the company in the market, this ratio

includes some ratios.

Return on assets depicts that how much money a company is generating on its assets;

Sainsbury ROA is 5.02% for the FY 2012 but in the FY it was 7.20%. There is a sharp decline

on assets of the Sainsbury. Still company is on the positive side. In the current situation it can be

depicted that either company had sold some its asset to meet the short term liability or it had

taken a long term loan to meet future demands.

Return on capital employed is also decreasing for the company form last two years,

which means employees of the company are not doing well, to generate profits and sales. At the

financial year ended 2012 its ROCE was 8.68% only but in the past it was 9.77%. Company may

have loosened long term funds from lenders or its supplier had not made payment at time. Which

is affecting the company’s ROCE.

Return on equity is increasing from the last year which means company is performing

well in the market. For the FY year company’s return on equity was 11.05% which means there

share prices are increasing and company is adequately generating funds.

Earnings per share are maintained at 3.21% which means company’s shares are giving

good value to its customers. It also results in increasing number of share holders for the company

(Neale, and McElroy, 2004).

1.3: Summarized Report

Table 2 : Summarized Report

Ratios of Sainsbury 2012 2011 2010 Remarks

Liquidity Ratio

Current Ratio

0.628

2

0.584

9

0.663

4

company should maintain this for long

run

Acid Test Ratio

0.319

3

0.287

8

0.396

7 it should always be maintained in 1:1,

company should work for it

Cash Ratio

0.303

7

0.265

8

0.361

2

to sustain in long run company should

increase its cash position

Efficiency / Turnover

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ratio

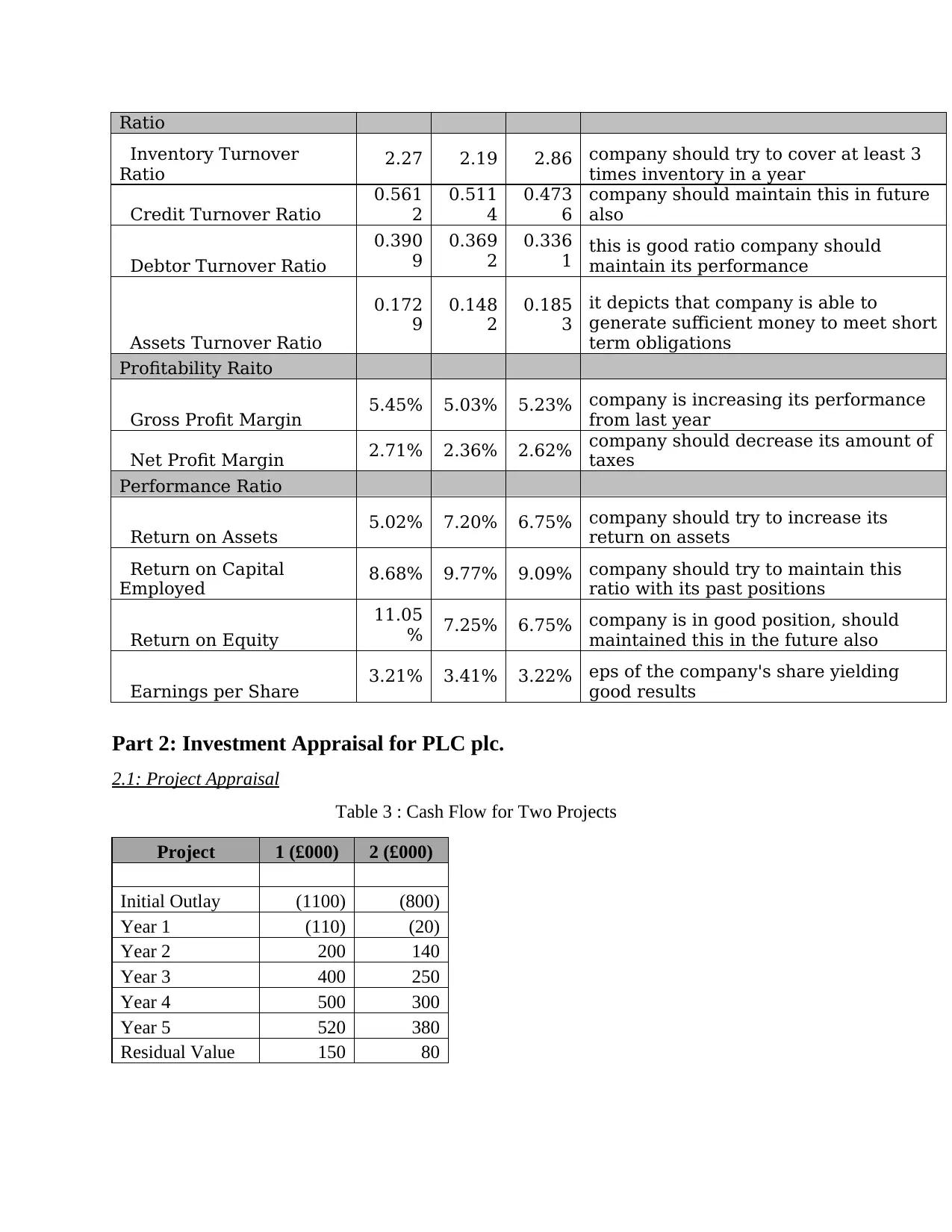

Inventory Turnover

Ratio 2.27 2.19 2.86 company should try to cover at least 3

times inventory in a year

Credit Turnover Ratio

0.561

2

0.511

4

0.473

6

company should maintain this in future

also

Debtor Turnover Ratio

0.390

9

0.369

2

0.336

1 this is good ratio company should

maintain its performance

Assets Turnover Ratio

0.172

9

0.148

2

0.185

3

it depicts that company is able to

generate sufficient money to meet short

term obligations

Profitability Raito

Gross Profit Margin 5.45% 5.03% 5.23% company is increasing its performance

from last year

Net Profit Margin 2.71% 2.36% 2.62% company should decrease its amount of

taxes

Performance Ratio

Return on Assets 5.02% 7.20% 6.75% company should try to increase its

return on assets

Return on Capital

Employed 8.68% 9.77% 9.09% company should try to maintain this

ratio with its past positions

Return on Equity

11.05

% 7.25% 6.75% company is in good position, should

maintained this in the future also

Earnings per Share 3.21% 3.41% 3.22% eps of the company's share yielding

good results

Part 2: Investment Appraisal for PLC plc.

2.1: Project Appraisal

Table 3 : Cash Flow for Two Projects

Project 1 (£000) 2 (£000)

Initial Outlay (1100) (800)

Year 1 (110) (20)

Year 2 200 140

Year 3 400 250

Year 4 500 300

Year 5 520 380

Residual Value 150 80

Inventory Turnover

Ratio 2.27 2.19 2.86 company should try to cover at least 3

times inventory in a year

Credit Turnover Ratio

0.561

2

0.511

4

0.473

6

company should maintain this in future

also

Debtor Turnover Ratio

0.390

9

0.369

2

0.336

1 this is good ratio company should

maintain its performance

Assets Turnover Ratio

0.172

9

0.148

2

0.185

3

it depicts that company is able to

generate sufficient money to meet short

term obligations

Profitability Raito

Gross Profit Margin 5.45% 5.03% 5.23% company is increasing its performance

from last year

Net Profit Margin 2.71% 2.36% 2.62% company should decrease its amount of

taxes

Performance Ratio

Return on Assets 5.02% 7.20% 6.75% company should try to increase its

return on assets

Return on Capital

Employed 8.68% 9.77% 9.09% company should try to maintain this

ratio with its past positions

Return on Equity

11.05

% 7.25% 6.75% company is in good position, should

maintained this in the future also

Earnings per Share 3.21% 3.41% 3.22% eps of the company's share yielding

good results

Part 2: Investment Appraisal for PLC plc.

2.1: Project Appraisal

Table 3 : Cash Flow for Two Projects

Project 1 (£000) 2 (£000)

Initial Outlay (1100) (800)

Year 1 (110) (20)

Year 2 200 140

Year 3 400 250

Year 4 500 300

Year 5 520 380

Residual Value 150 80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

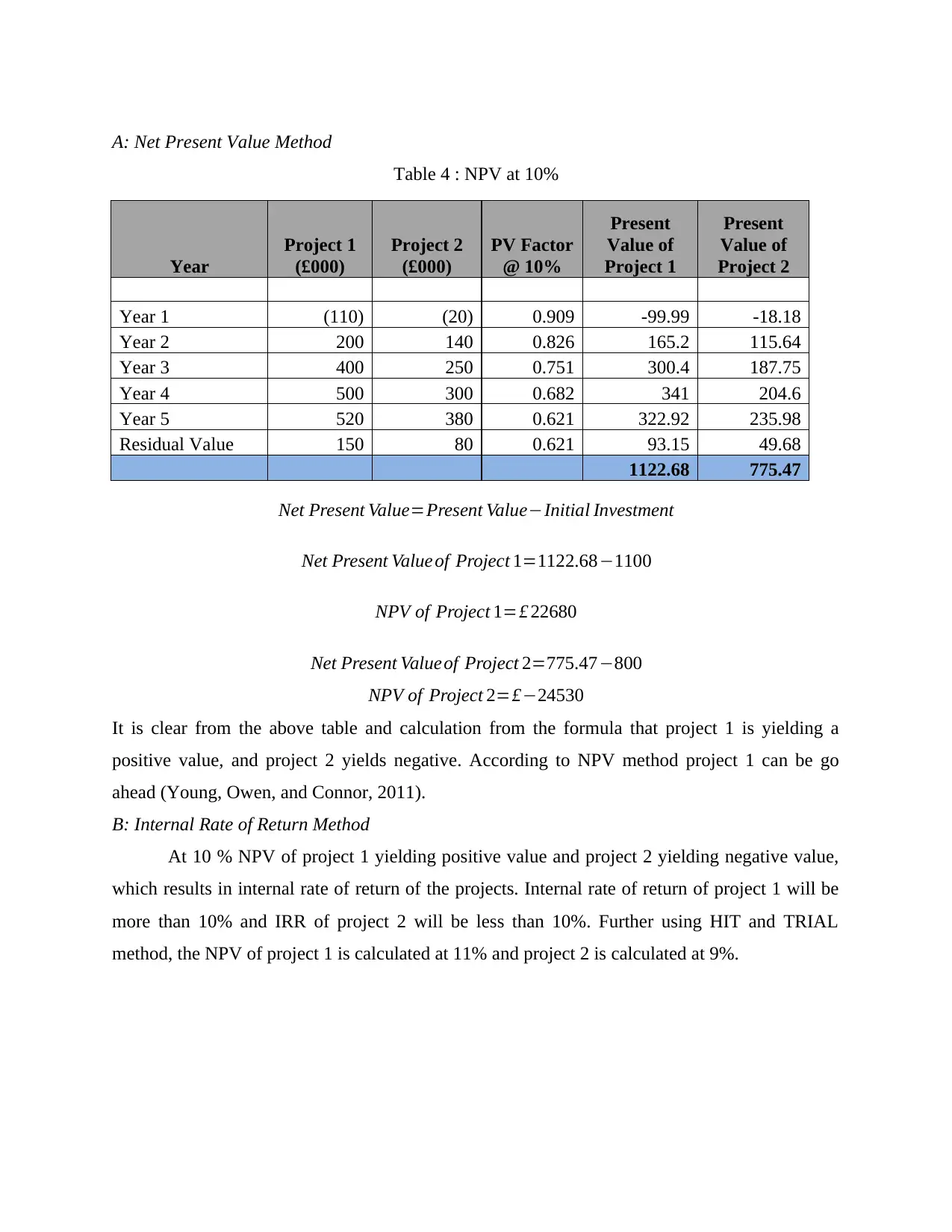

A: Net Present Value Method

Table 4 : NPV at 10%

Year

Project 1

(£000)

Project 2

(£000)

PV Factor

@ 10%

Present

Value of

Project 1

Present

Value of

Project 2

Year 1 (110) (20) 0.909 -99.99 -18.18

Year 2 200 140 0.826 165.2 115.64

Year 3 400 250 0.751 300.4 187.75

Year 4 500 300 0.682 341 204.6

Year 5 520 380 0.621 322.92 235.98

Residual Value 150 80 0.621 93.15 49.68

1122.68 775.47

Net Present Value=Present Value−Initial Investment

Net Present Value of Project 1=1122.68−1100

NPV of Project 1=£ 22680

Net Present Valueof Project 2=775.47−800

NPV of Project 2=£−24530

It is clear from the above table and calculation from the formula that project 1 is yielding a

positive value, and project 2 yields negative. According to NPV method project 1 can be go

ahead (Young, Owen, and Connor, 2011).

B: Internal Rate of Return Method

At 10 % NPV of project 1 yielding positive value and project 2 yielding negative value,

which results in internal rate of return of the projects. Internal rate of return of project 1 will be

more than 10% and IRR of project 2 will be less than 10%. Further using HIT and TRIAL

method, the NPV of project 1 is calculated at 11% and project 2 is calculated at 9%.

Table 4 : NPV at 10%

Year

Project 1

(£000)

Project 2

(£000)

PV Factor

@ 10%

Present

Value of

Project 1

Present

Value of

Project 2

Year 1 (110) (20) 0.909 -99.99 -18.18

Year 2 200 140 0.826 165.2 115.64

Year 3 400 250 0.751 300.4 187.75

Year 4 500 300 0.682 341 204.6

Year 5 520 380 0.621 322.92 235.98

Residual Value 150 80 0.621 93.15 49.68

1122.68 775.47

Net Present Value=Present Value−Initial Investment

Net Present Value of Project 1=1122.68−1100

NPV of Project 1=£ 22680

Net Present Valueof Project 2=775.47−800

NPV of Project 2=£−24530

It is clear from the above table and calculation from the formula that project 1 is yielding a

positive value, and project 2 yields negative. According to NPV method project 1 can be go

ahead (Young, Owen, and Connor, 2011).

B: Internal Rate of Return Method

At 10 % NPV of project 1 yielding positive value and project 2 yielding negative value,

which results in internal rate of return of the projects. Internal rate of return of project 1 will be

more than 10% and IRR of project 2 will be less than 10%. Further using HIT and TRIAL

method, the NPV of project 1 is calculated at 11% and project 2 is calculated at 9%.

Table 5 : NPV of Project 1

Year

Project 1

(£000)

PV Factor @

11%

Present Value

of project 1

Year 1 -110 0.901 -99.11

Year 2 200 0.812 162.4

Year 3 400 0.731 292.4

Year 4 500 0.659 329.5

Year 5 520 0.593 308.36

Residual Value 150 0.593 88.95

1082.5

NPV of Project 1=1082.5−1100

NPV of project 1=£−17500

Table 6 : NPV of Project 2

Year

Project 2

(£000)

PV Factor @

9%

Present

Value of

Project 2

Year 1 -20 0.917 -18.34

Year 2 140 0.842 117.88

Year 3 250 0.772 193

Year 4 300 0.708 212.4

Year 5 380 0.65 247

Residual Value 80 0.65 52

803.94

NPV of Project 2=803.94−800

NPV of Project 2=£ 3940

From the table 5 and table 6 the Internal Rate of Return of both project is been shown. IRR of

project will be in between 10% to 11% and IRR of project 2 will be in between 9% - 10%.

IRR of project 1:

IRR=10+ 1122.68−1100

1122.68−1082.5∗1

Year

Project 1

(£000)

PV Factor @

11%

Present Value

of project 1

Year 1 -110 0.901 -99.11

Year 2 200 0.812 162.4

Year 3 400 0.731 292.4

Year 4 500 0.659 329.5

Year 5 520 0.593 308.36

Residual Value 150 0.593 88.95

1082.5

NPV of Project 1=1082.5−1100

NPV of project 1=£−17500

Table 6 : NPV of Project 2

Year

Project 2

(£000)

PV Factor @

9%

Present

Value of

Project 2

Year 1 -20 0.917 -18.34

Year 2 140 0.842 117.88

Year 3 250 0.772 193

Year 4 300 0.708 212.4

Year 5 380 0.65 247

Residual Value 80 0.65 52

803.94

NPV of Project 2=803.94−800

NPV of Project 2=£ 3940

From the table 5 and table 6 the Internal Rate of Return of both project is been shown. IRR of

project will be in between 10% to 11% and IRR of project 2 will be in between 9% - 10%.

IRR of project 1:

IRR=10+ 1122.68−1100

1122.68−1082.5∗1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.