Financial Management Report: Kadlex plc and Happy Meal Ltd Analysis

VerifiedAdded on 2021/02/19

|15

|3932

|96

Report

AI Summary

This financial management report delves into key concepts and techniques essential for effective financial decision-making. The report begins by defining financial management and its significance, then explores the cost of capital and capital structure, including calculations of Weighted Average Cost of Capital (WACC) using both book and market values for Kadlex plc. It then examines the implications of integrating new capital and the effects of short-termism on bankruptcy and agency problems. The report further analyzes investment appraisal techniques such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR) using the case of Happy Meal Limited. Detailed calculations and recommendations for each technique are provided, offering a comprehensive overview of financial management strategies and their practical application.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1: Cost of capital and Capital structure........................................................................3

Question 3 Investment Appraisal Techniques.............................................................................7

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1: Cost of capital and Capital structure........................................................................3

Question 3 Investment Appraisal Techniques.............................................................................7

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

The term financial management can be defined as an activity of controlling and managing

available financial resources of business entities (Finkler, Smith and Calabrese, 2018).

Basically, it is important for companies to manage their financial activities in an effective

manner because finance is key of success. There are various kind of methods and functions to

manage the financial resources of companies. The project report covers about different aspects

such as cost of capital and structure, investment appraisal techniques like payback period, net

present value, internal rate of return method and many more. Apart from it, various calculation is

done as per the given data.

MAIN BODY

Question 1: Cost of capital and Capital structure.

(a) Calculation of book value and market value cost of capital (WACC)

Concept of cost of capital -

The term cost of capital can be defined as cost which occurs in process of making any

investment. In other words, the cost of capital is expected rate of return which could have been

earned by investing equal amount of money in various investments with risk (Renz and Herman,

2016). This can be measured by market and presents a degree of risk by investors. The cost of

capital is calculated in a situation in which there are two investments with equal risk then

investors compute the cost of capital and select one alternative whose return is higher. Like in

the Kadlex plc, their finance director calculates the cost of capital in order to take important

decisions.

Capital structure -

The term capital structure may be defined as the way in which a business entity finances

their assets by combination of equity, debt or any other securities (Pandey, 2015). Basically, this

is helpful for companies in assessing which type of funding the company is applying to finance

their entire activities and operations. In addition, it presents the proportion between debt and

equity in funding.

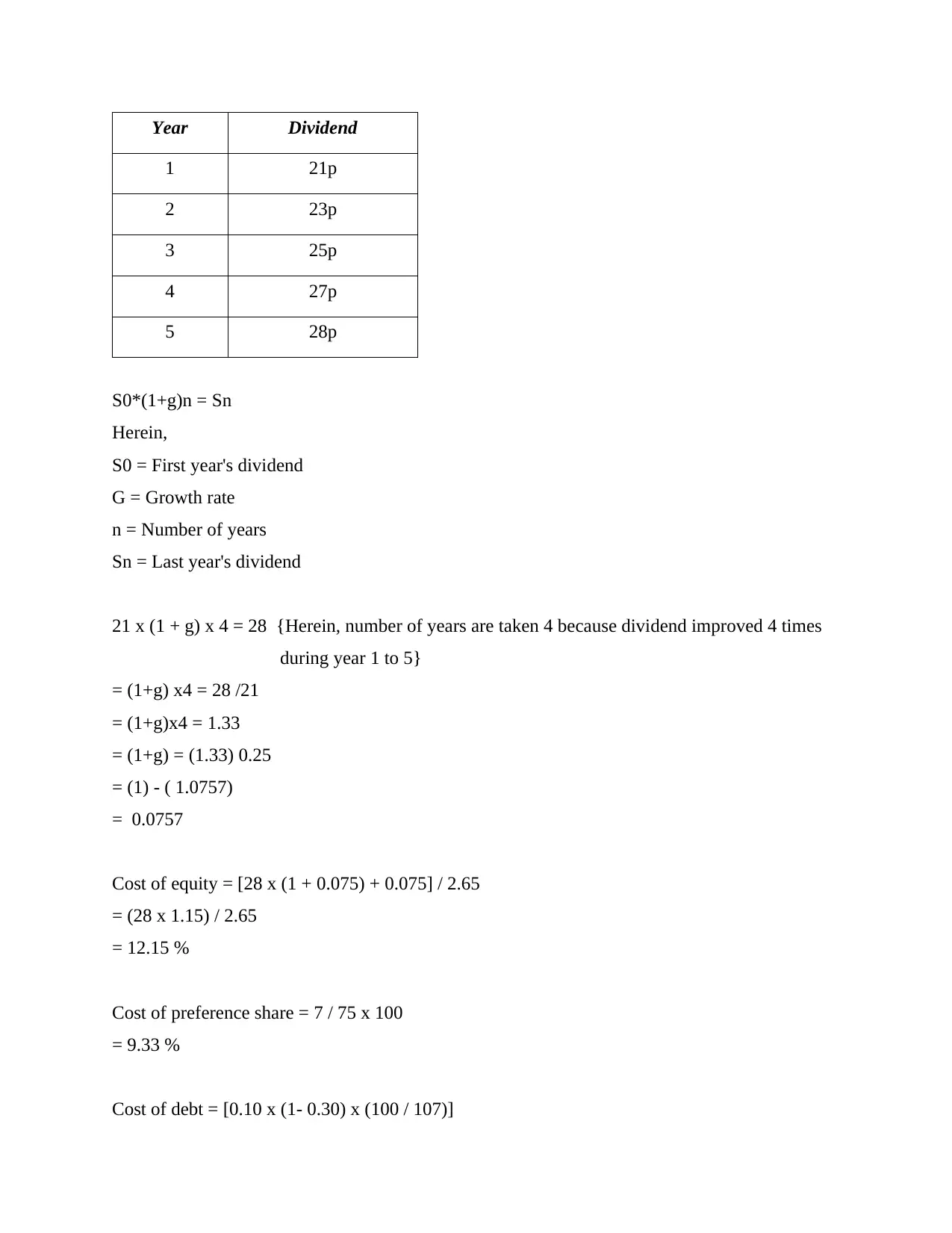

In the aspect of Kadlex plc their last five years dividend payment are as follows :

The term financial management can be defined as an activity of controlling and managing

available financial resources of business entities (Finkler, Smith and Calabrese, 2018).

Basically, it is important for companies to manage their financial activities in an effective

manner because finance is key of success. There are various kind of methods and functions to

manage the financial resources of companies. The project report covers about different aspects

such as cost of capital and structure, investment appraisal techniques like payback period, net

present value, internal rate of return method and many more. Apart from it, various calculation is

done as per the given data.

MAIN BODY

Question 1: Cost of capital and Capital structure.

(a) Calculation of book value and market value cost of capital (WACC)

Concept of cost of capital -

The term cost of capital can be defined as cost which occurs in process of making any

investment. In other words, the cost of capital is expected rate of return which could have been

earned by investing equal amount of money in various investments with risk (Renz and Herman,

2016). This can be measured by market and presents a degree of risk by investors. The cost of

capital is calculated in a situation in which there are two investments with equal risk then

investors compute the cost of capital and select one alternative whose return is higher. Like in

the Kadlex plc, their finance director calculates the cost of capital in order to take important

decisions.

Capital structure -

The term capital structure may be defined as the way in which a business entity finances

their assets by combination of equity, debt or any other securities (Pandey, 2015). Basically, this

is helpful for companies in assessing which type of funding the company is applying to finance

their entire activities and operations. In addition, it presents the proportion between debt and

equity in funding.

In the aspect of Kadlex plc their last five years dividend payment are as follows :

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year Dividend

1 21p

2 23p

3 25p

4 27p

5 28p

S0*(1+g)n = Sn

Herein,

S0 = First year's dividend

G = Growth rate

n = Number of years

Sn = Last year's dividend

21 x (1 + g) x 4 = 28 {Herein, number of years are taken 4 because dividend improved 4 times

during year 1 to 5}

= (1+g) x4 = 28 /21

= (1+g)x4 = 1.33

= (1+g) = (1.33) 0.25

= (1) - ( 1.0757)

= 0.0757

Cost of equity = [28 x (1 + 0.075) + 0.075] / 2.65

= (28 x 1.15) / 2.65

= 12.15 %

Cost of preference share = 7 / 75 x 100

= 9.33 %

Cost of debt = [0.10 x (1- 0.30) x (100 / 107)]

1 21p

2 23p

3 25p

4 27p

5 28p

S0*(1+g)n = Sn

Herein,

S0 = First year's dividend

G = Growth rate

n = Number of years

Sn = Last year's dividend

21 x (1 + g) x 4 = 28 {Herein, number of years are taken 4 because dividend improved 4 times

during year 1 to 5}

= (1+g) x4 = 28 /21

= (1+g)x4 = 1.33

= (1+g) = (1.33) 0.25

= (1) - ( 1.0757)

= 0.0757

Cost of equity = [28 x (1 + 0.075) + 0.075] / 2.65

= (28 x 1.15) / 2.65

= 12.15 %

Cost of preference share = 7 / 75 x 100

= 9.33 %

Cost of debt = [0.10 x (1- 0.30) x (100 / 107)]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 0.0654 x 100

= 6.54 %

Calculation of book and market value :

Particulars Book Value

(in £'000)

Market Value (in £'000) Proposed Value (in £'000)

Number

of share

(A)

Market

Price

(B)

Value

(A*B)

Number of

share (C)

Price

(D)

Value

(C*D)

Equity share

along with

reserve

25000 20000 2.65 53000 20000 2.85 57000

Preference

Share

10000 10000 0.75 7500 10000 0.68 6800

Irredeemable

Bond

15000 15000 1.07 16050 15000 1.07 16050

Total Capital 50000 - - 76550 - - -

New Bond - - - - 15000 1.05 15750

Total - - - - - - 95600

So, the book value is of £50000 and market value is of £76550. In addition, proposed value is of

£95600.

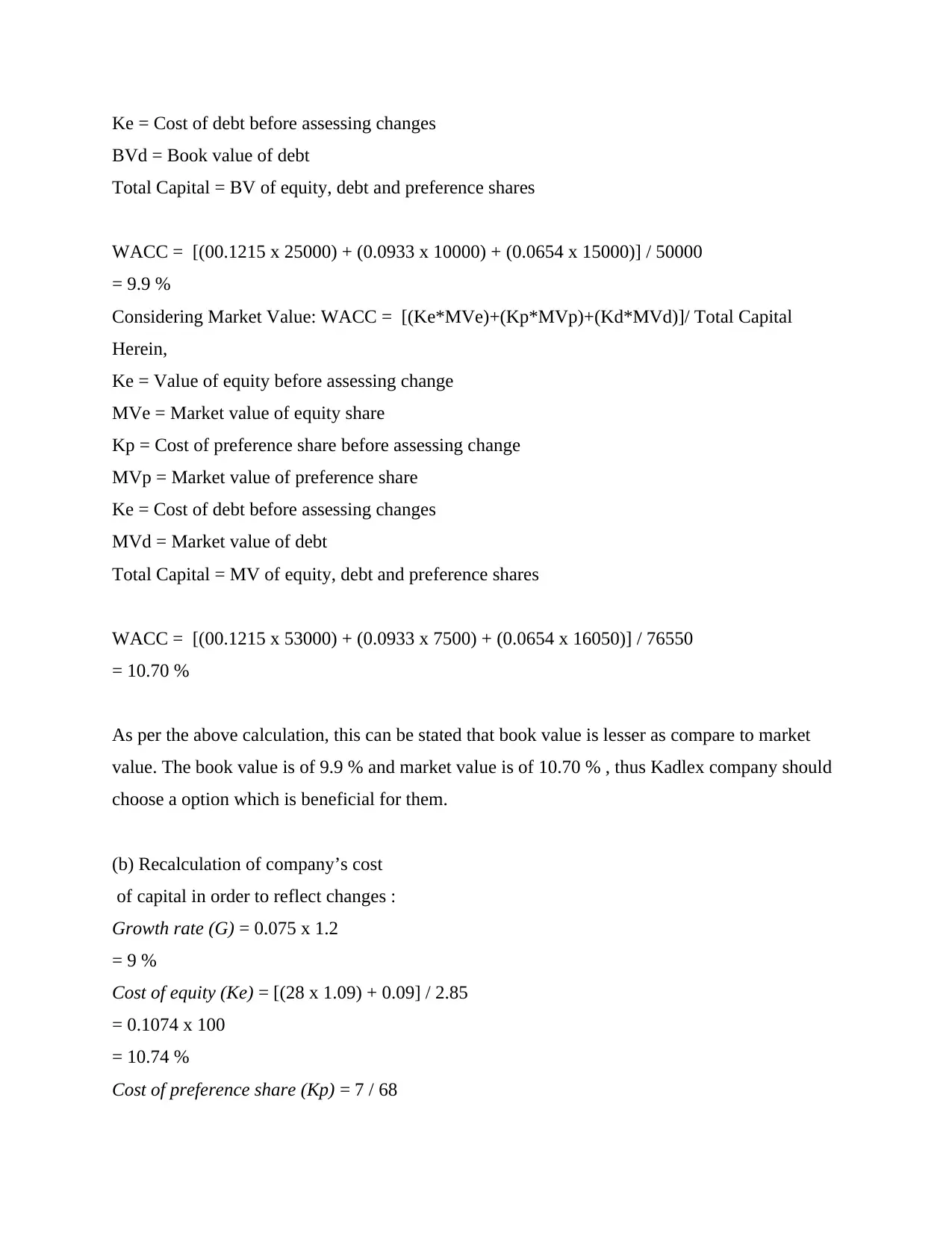

Considering Book Value: WACC = [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/ Total Capital

Herein,

Ke = Value of equity before assessing change

BVe = Book value of equity share

Kp = Cost of preference share before assessing change

BVp = Book value of preference share

= 6.54 %

Calculation of book and market value :

Particulars Book Value

(in £'000)

Market Value (in £'000) Proposed Value (in £'000)

Number

of share

(A)

Market

Price

(B)

Value

(A*B)

Number of

share (C)

Price

(D)

Value

(C*D)

Equity share

along with

reserve

25000 20000 2.65 53000 20000 2.85 57000

Preference

Share

10000 10000 0.75 7500 10000 0.68 6800

Irredeemable

Bond

15000 15000 1.07 16050 15000 1.07 16050

Total Capital 50000 - - 76550 - - -

New Bond - - - - 15000 1.05 15750

Total - - - - - - 95600

So, the book value is of £50000 and market value is of £76550. In addition, proposed value is of

£95600.

Considering Book Value: WACC = [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/ Total Capital

Herein,

Ke = Value of equity before assessing change

BVe = Book value of equity share

Kp = Cost of preference share before assessing change

BVp = Book value of preference share

Ke = Cost of debt before assessing changes

BVd = Book value of debt

Total Capital = BV of equity, debt and preference shares

WACC = [(00.1215 x 25000) + (0.0933 x 10000) + (0.0654 x 15000)] / 50000

= 9.9 %

Considering Market Value: WACC = [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/ Total Capital

Herein,

Ke = Value of equity before assessing change

MVe = Market value of equity share

Kp = Cost of preference share before assessing change

MVp = Market value of preference share

Ke = Cost of debt before assessing changes

MVd = Market value of debt

Total Capital = MV of equity, debt and preference shares

WACC = [(00.1215 x 53000) + (0.0933 x 7500) + (0.0654 x 16050)] / 76550

= 10.70 %

As per the above calculation, this can be stated that book value is lesser as compare to market

value. The book value is of 9.9 % and market value is of 10.70 % , thus Kadlex company should

choose a option which is beneficial for them.

(b) Recalculation of company’s cost

of capital in order to reflect changes :

Growth rate (G) = 0.075 x 1.2

= 9 %

Cost of equity (Ke) = [(28 x 1.09) + 0.09] / 2.85

= 0.1074 x 100

= 10.74 %

Cost of preference share (Kp) = 7 / 68

BVd = Book value of debt

Total Capital = BV of equity, debt and preference shares

WACC = [(00.1215 x 25000) + (0.0933 x 10000) + (0.0654 x 15000)] / 50000

= 9.9 %

Considering Market Value: WACC = [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/ Total Capital

Herein,

Ke = Value of equity before assessing change

MVe = Market value of equity share

Kp = Cost of preference share before assessing change

MVp = Market value of preference share

Ke = Cost of debt before assessing changes

MVd = Market value of debt

Total Capital = MV of equity, debt and preference shares

WACC = [(00.1215 x 53000) + (0.0933 x 7500) + (0.0654 x 16050)] / 76550

= 10.70 %

As per the above calculation, this can be stated that book value is lesser as compare to market

value. The book value is of 9.9 % and market value is of 10.70 % , thus Kadlex company should

choose a option which is beneficial for them.

(b) Recalculation of company’s cost

of capital in order to reflect changes :

Growth rate (G) = 0.075 x 1.2

= 9 %

Cost of equity (Ke) = [(28 x 1.09) + 0.09] / 2.85

= 0.1074 x 100

= 10.74 %

Cost of preference share (Kp) = 7 / 68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 0.1029 x 100

= 10.29 %

Cost of irredeemable bond (Kd) = [10 (1-0.30)] x 100 / 107

= 0.0654 x 100

= 6.54 %

Cost of new bonds (Kd) = [0.11 (1-0.30)] x 100 / 105

= 0.0733 x 100

= 7.33 %

Hence, Proposed WACC = [(0.09 x 57000) + (0.1074 x 6800) + (0.0654 x 165050) + (0.0733 x

15750)]

= 0.0844 x 100

= 8.44 %

(c) Critical analysis of integrating new capital

The proposed weighted average cost of capital is 8.44 % while WACC considering

market value is of 10.70 %. Herein, difference between cost of capital is of 2.26 %. It indicates

that if above Kadlex company will convert their capital structure into proposed WACC then they

will be able to reduce their cost of capital by 2.26 %.

(d) Effects of short-termism on bankruptcy and the agency problem in

companies.

Short termism – It can be defined as a condition in which investors focus on short-term results at

risk of long term interest (Mitchell, 2017). This can impact on bankruptcy and agency problem in

companies. It is so because if business entities will focus on short term outcomes then they will

not be able to solve agency problems.

Question 3 Investment Appraisal Techniques.

There are different kind of appraisal techniques which are used by companies in order to

assess different investment alternatives (Tang and Baker, 2016). Herein, the case of Happy meal

= 10.29 %

Cost of irredeemable bond (Kd) = [10 (1-0.30)] x 100 / 107

= 0.0654 x 100

= 6.54 %

Cost of new bonds (Kd) = [0.11 (1-0.30)] x 100 / 105

= 0.0733 x 100

= 7.33 %

Hence, Proposed WACC = [(0.09 x 57000) + (0.1074 x 6800) + (0.0654 x 165050) + (0.0733 x

15750)]

= 0.0844 x 100

= 8.44 %

(c) Critical analysis of integrating new capital

The proposed weighted average cost of capital is 8.44 % while WACC considering

market value is of 10.70 %. Herein, difference between cost of capital is of 2.26 %. It indicates

that if above Kadlex company will convert their capital structure into proposed WACC then they

will be able to reduce their cost of capital by 2.26 %.

(d) Effects of short-termism on bankruptcy and the agency problem in

companies.

Short termism – It can be defined as a condition in which investors focus on short-term results at

risk of long term interest (Mitchell, 2017). This can impact on bankruptcy and agency problem in

companies. It is so because if business entities will focus on short term outcomes then they will

not be able to solve agency problems.

Question 3 Investment Appraisal Techniques.

There are different kind of appraisal techniques which are used by companies in order to

assess different investment alternatives (Tang and Baker, 2016). Herein, the case of Happy meal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

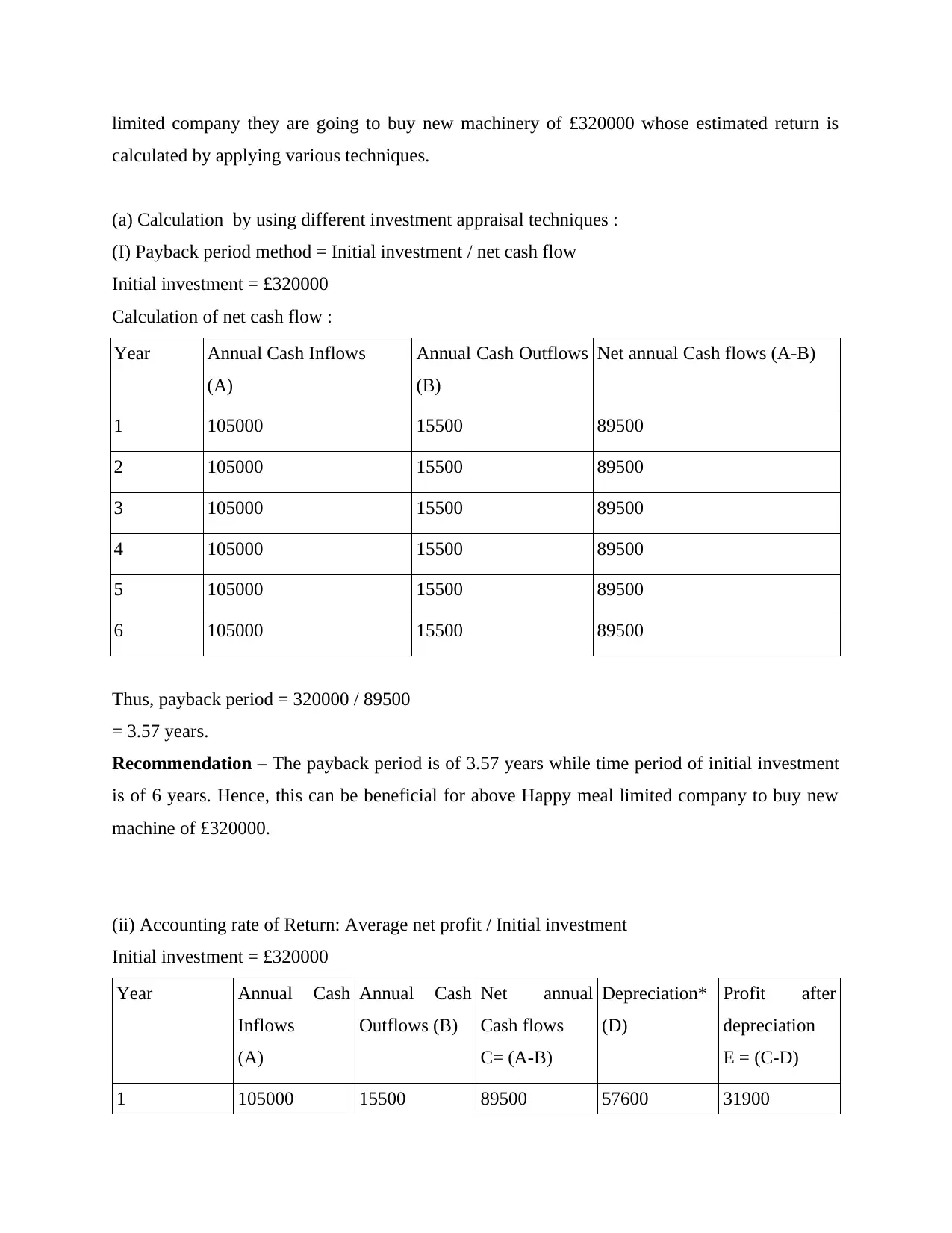

limited company they are going to buy new machinery of £320000 whose estimated return is

calculated by applying various techniques.

(a) Calculation by using different investment appraisal techniques :

(I) Payback period method = Initial investment / net cash flow

Initial investment = £320000

Calculation of net cash flow :

Year Annual Cash Inflows

(A)

Annual Cash Outflows

(B)

Net annual Cash flows (A-B)

1 105000 15500 89500

2 105000 15500 89500

3 105000 15500 89500

4 105000 15500 89500

5 105000 15500 89500

6 105000 15500 89500

Thus, payback period = 320000 / 89500

= 3.57 years.

Recommendation – The payback period is of 3.57 years while time period of initial investment

is of 6 years. Hence, this can be beneficial for above Happy meal limited company to buy new

machine of £320000.

(ii) Accounting rate of Return: Average net profit / Initial investment

Initial investment = £320000

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual

Cash flows

C= (A-B)

Depreciation*

(D)

Profit after

depreciation

E = (C-D)

1 105000 15500 89500 57600 31900

calculated by applying various techniques.

(a) Calculation by using different investment appraisal techniques :

(I) Payback period method = Initial investment / net cash flow

Initial investment = £320000

Calculation of net cash flow :

Year Annual Cash Inflows

(A)

Annual Cash Outflows

(B)

Net annual Cash flows (A-B)

1 105000 15500 89500

2 105000 15500 89500

3 105000 15500 89500

4 105000 15500 89500

5 105000 15500 89500

6 105000 15500 89500

Thus, payback period = 320000 / 89500

= 3.57 years.

Recommendation – The payback period is of 3.57 years while time period of initial investment

is of 6 years. Hence, this can be beneficial for above Happy meal limited company to buy new

machine of £320000.

(ii) Accounting rate of Return: Average net profit / Initial investment

Initial investment = £320000

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual

Cash flows

C= (A-B)

Depreciation*

(D)

Profit after

depreciation

E = (C-D)

1 105000 15500 89500 57600 31900

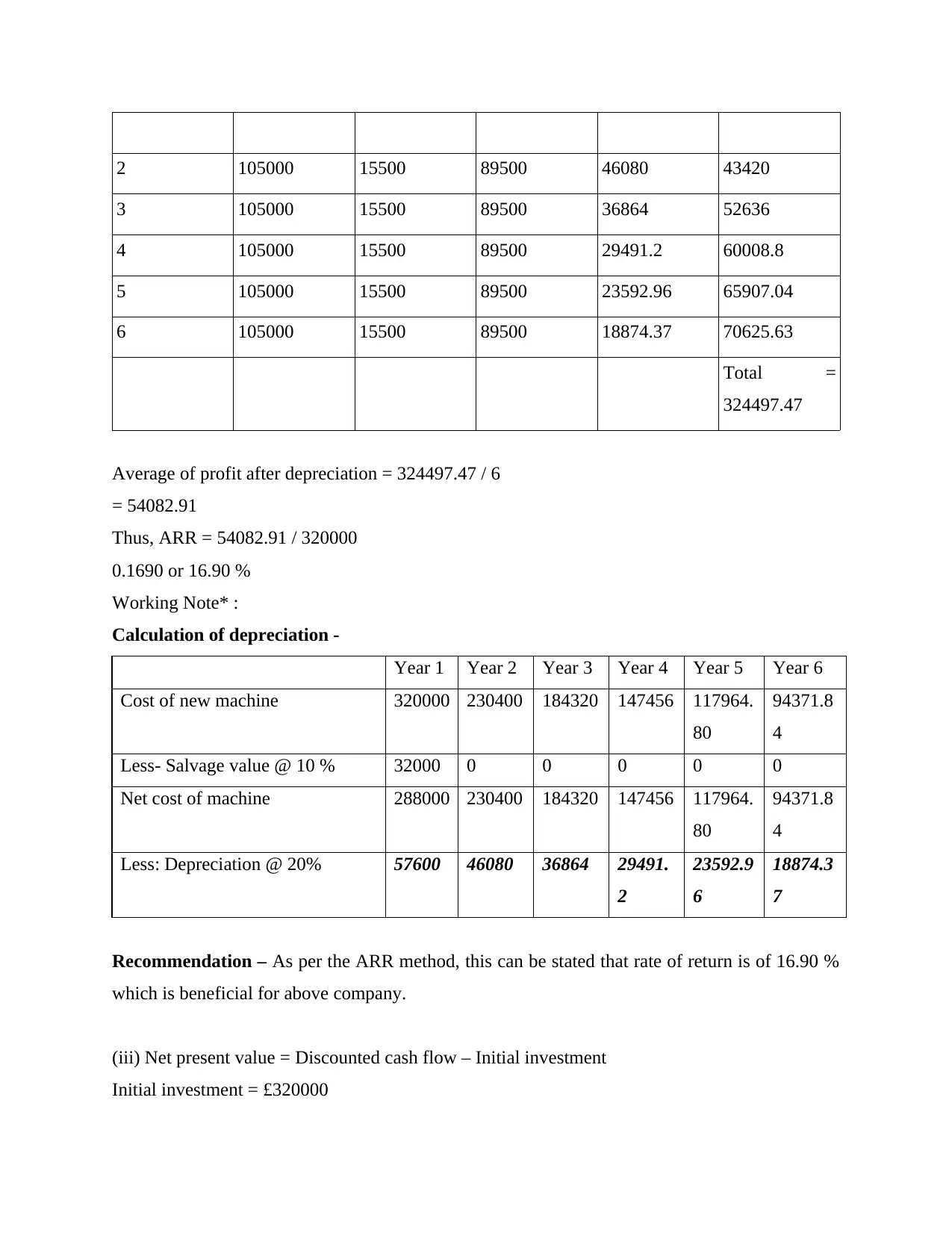

2 105000 15500 89500 46080 43420

3 105000 15500 89500 36864 52636

4 105000 15500 89500 29491.2 60008.8

5 105000 15500 89500 23592.96 65907.04

6 105000 15500 89500 18874.37 70625.63

Total =

324497.47

Average of profit after depreciation = 324497.47 / 6

= 54082.91

Thus, ARR = 54082.91 / 320000

0.1690 or 16.90 %

Working Note* :

Calculation of depreciation -

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cost of new machine 320000 230400 184320 147456 117964.

80

94371.8

4

Less- Salvage value @ 10 % 32000 0 0 0 0 0

Net cost of machine 288000 230400 184320 147456 117964.

80

94371.8

4

Less: Depreciation @ 20% 57600 46080 36864 29491.

2

23592.9

6

18874.3

7

Recommendation – As per the ARR method, this can be stated that rate of return is of 16.90 %

which is beneficial for above company.

(iii) Net present value = Discounted cash flow – Initial investment

Initial investment = £320000

3 105000 15500 89500 36864 52636

4 105000 15500 89500 29491.2 60008.8

5 105000 15500 89500 23592.96 65907.04

6 105000 15500 89500 18874.37 70625.63

Total =

324497.47

Average of profit after depreciation = 324497.47 / 6

= 54082.91

Thus, ARR = 54082.91 / 320000

0.1690 or 16.90 %

Working Note* :

Calculation of depreciation -

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cost of new machine 320000 230400 184320 147456 117964.

80

94371.8

4

Less- Salvage value @ 10 % 32000 0 0 0 0 0

Net cost of machine 288000 230400 184320 147456 117964.

80

94371.8

4

Less: Depreciation @ 20% 57600 46080 36864 29491.

2

23592.9

6

18874.3

7

Recommendation – As per the ARR method, this can be stated that rate of return is of 16.90 %

which is beneficial for above company.

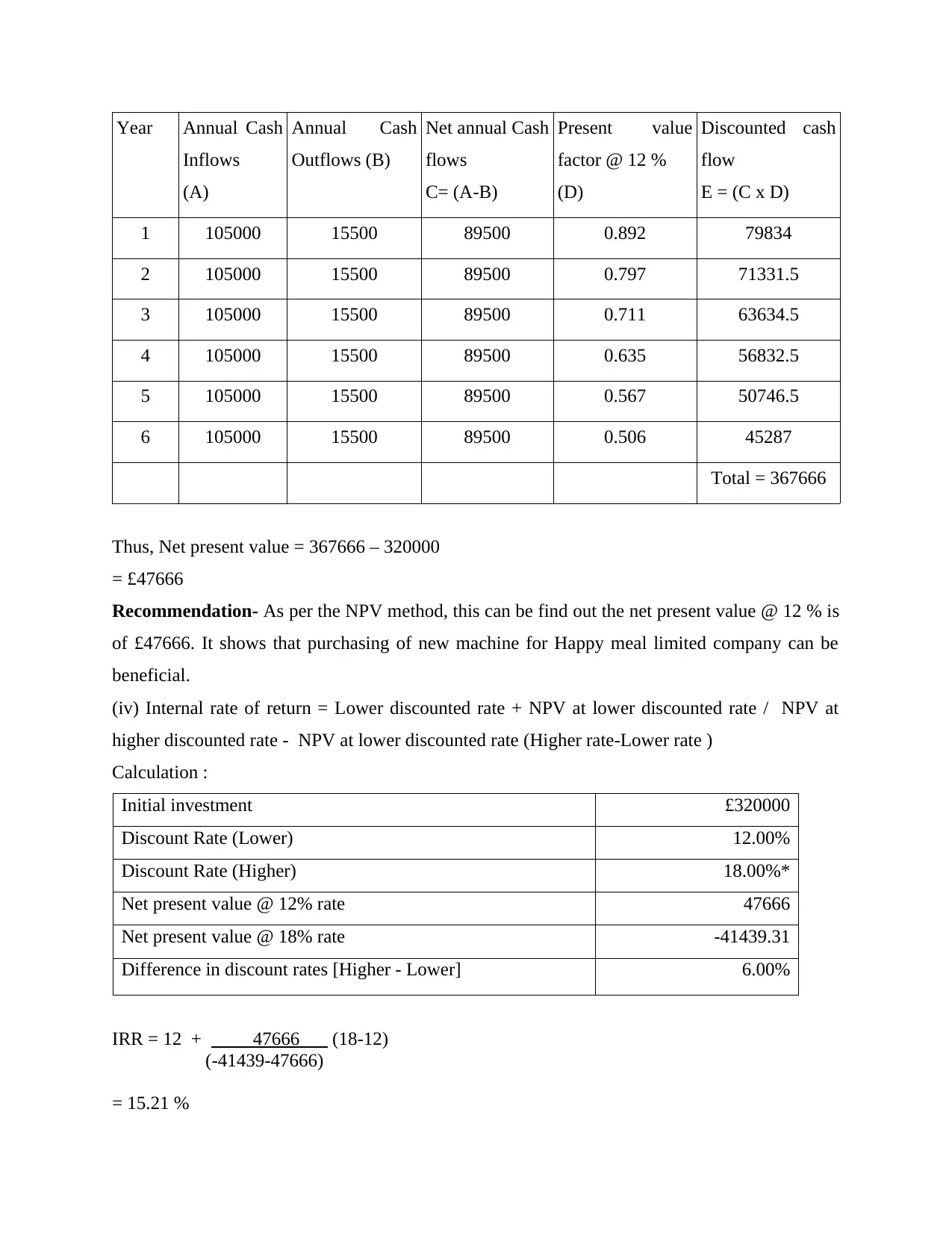

(iii) Net present value = Discounted cash flow – Initial investment

Initial investment = £320000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 12 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.892 79834

2 105000 15500 89500 0.797 71331.5

3 105000 15500 89500 0.711 63634.5

4 105000 15500 89500 0.635 56832.5

5 105000 15500 89500 0.567 50746.5

6 105000 15500 89500 0.506 45287

Total = 367666

Thus, Net present value = 367666 – 320000

= £47666

Recommendation- As per the NPV method, this can be find out the net present value @ 12 % is

of £47666. It shows that purchasing of new machine for Happy meal limited company can be

beneficial.

(iv) Internal rate of return = Lower discounted rate + NPV at lower discounted rate / NPV at

higher discounted rate - NPV at lower discounted rate (Higher rate-Lower rate )

Calculation :

Initial investment £320000

Discount Rate (Lower) 12.00%

Discount Rate (Higher) 18.00%*

Net present value @ 12% rate 47666

Net present value @ 18% rate -41439.31

Difference in discount rates [Higher - Lower] 6.00%

IRR = 12 + 47666 (18-12)

(-41439-47666)

= 15.21 %

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 12 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.892 79834

2 105000 15500 89500 0.797 71331.5

3 105000 15500 89500 0.711 63634.5

4 105000 15500 89500 0.635 56832.5

5 105000 15500 89500 0.567 50746.5

6 105000 15500 89500 0.506 45287

Total = 367666

Thus, Net present value = 367666 – 320000

= £47666

Recommendation- As per the NPV method, this can be find out the net present value @ 12 % is

of £47666. It shows that purchasing of new machine for Happy meal limited company can be

beneficial.

(iv) Internal rate of return = Lower discounted rate + NPV at lower discounted rate / NPV at

higher discounted rate - NPV at lower discounted rate (Higher rate-Lower rate )

Calculation :

Initial investment £320000

Discount Rate (Lower) 12.00%

Discount Rate (Higher) 18.00%*

Net present value @ 12% rate 47666

Net present value @ 18% rate -41439.31

Difference in discount rates [Higher - Lower] 6.00%

IRR = 12 + 47666 (18-12)

(-41439-47666)

= 15.21 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

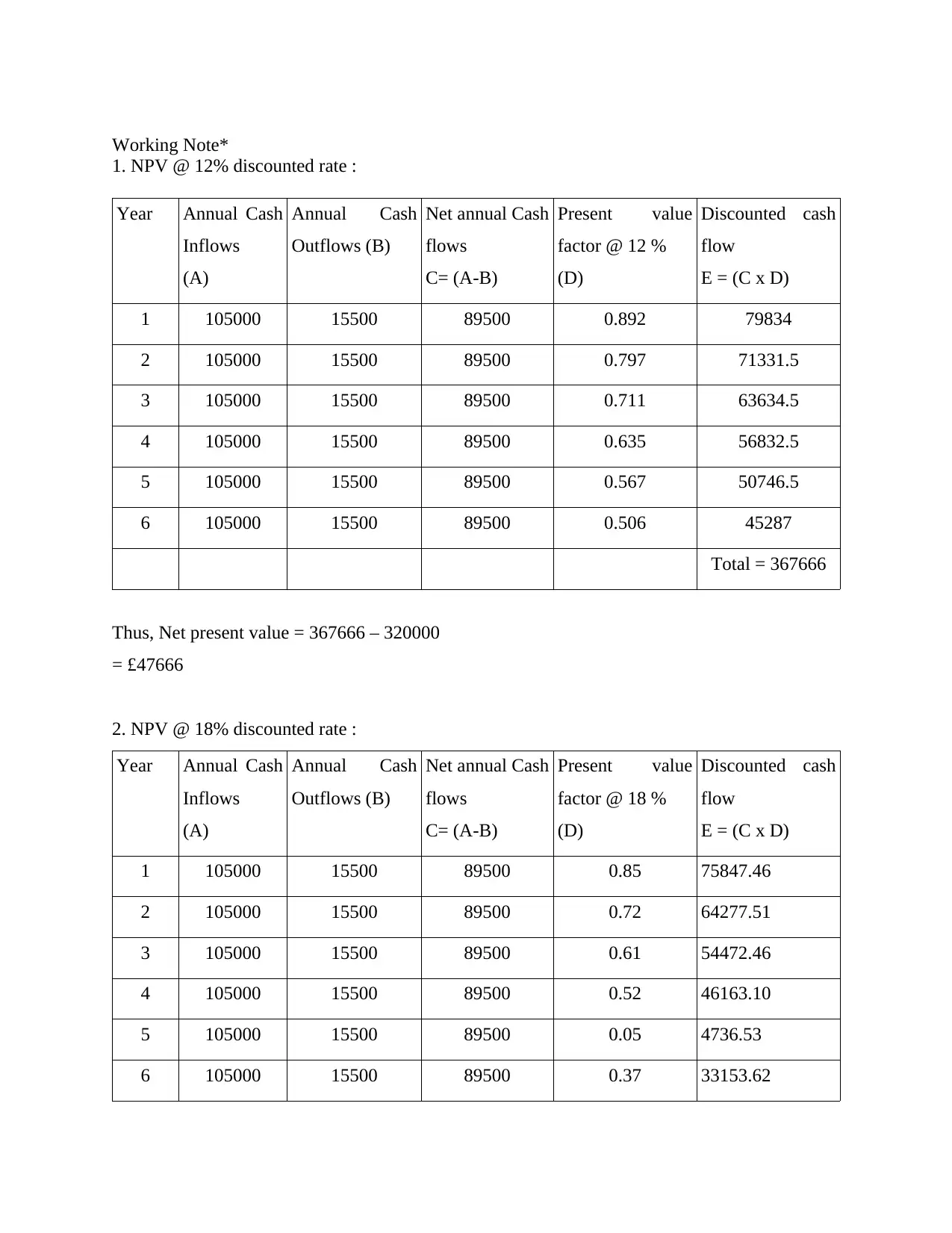

Working Note*

1. NPV @ 12% discounted rate :

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 12 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.892 79834

2 105000 15500 89500 0.797 71331.5

3 105000 15500 89500 0.711 63634.5

4 105000 15500 89500 0.635 56832.5

5 105000 15500 89500 0.567 50746.5

6 105000 15500 89500 0.506 45287

Total = 367666

Thus, Net present value = 367666 – 320000

= £47666

2. NPV @ 18% discounted rate :

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 18 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.85 75847.46

2 105000 15500 89500 0.72 64277.51

3 105000 15500 89500 0.61 54472.46

4 105000 15500 89500 0.52 46163.10

5 105000 15500 89500 0.05 4736.53

6 105000 15500 89500 0.37 33153.62

1. NPV @ 12% discounted rate :

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 12 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.892 79834

2 105000 15500 89500 0.797 71331.5

3 105000 15500 89500 0.711 63634.5

4 105000 15500 89500 0.635 56832.5

5 105000 15500 89500 0.567 50746.5

6 105000 15500 89500 0.506 45287

Total = 367666

Thus, Net present value = 367666 – 320000

= £47666

2. NPV @ 18% discounted rate :

Year Annual Cash

Inflows

(A)

Annual Cash

Outflows (B)

Net annual Cash

flows

C= (A-B)

Present value

factor @ 18 %

(D)

Discounted cash

flow

E = (C x D)

1 105000 15500 89500 0.85 75847.46

2 105000 15500 89500 0.72 64277.51

3 105000 15500 89500 0.61 54472.46

4 105000 15500 89500 0.52 46163.10

5 105000 15500 89500 0.05 4736.53

6 105000 15500 89500 0.37 33153.62

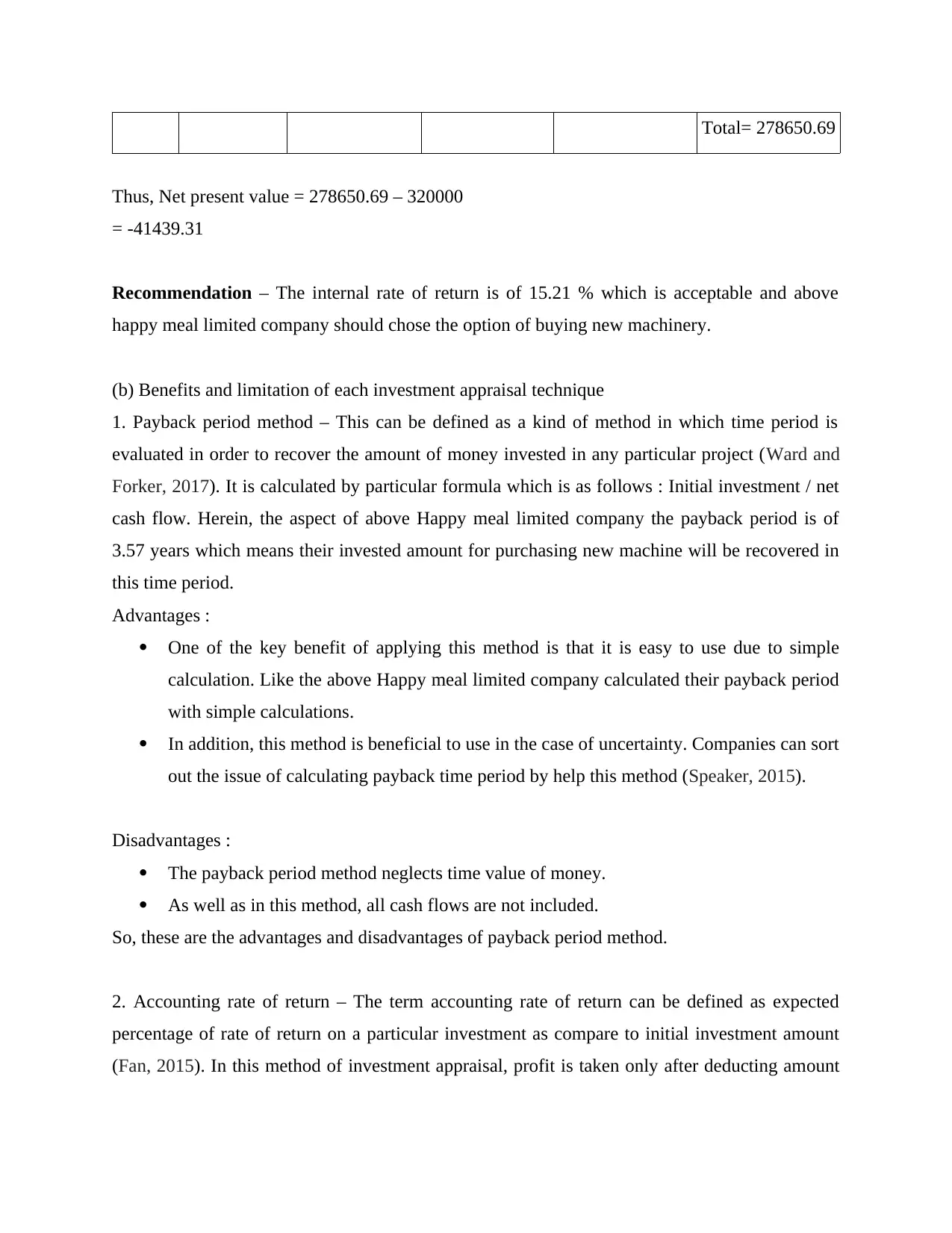

Total= 278650.69

Thus, Net present value = 278650.69 – 320000

= -41439.31

Recommendation – The internal rate of return is of 15.21 % which is acceptable and above

happy meal limited company should chose the option of buying new machinery.

(b) Benefits and limitation of each investment appraisal technique

1. Payback period method – This can be defined as a kind of method in which time period is

evaluated in order to recover the amount of money invested in any particular project (Ward and

Forker, 2017). It is calculated by particular formula which is as follows : Initial investment / net

cash flow. Herein, the aspect of above Happy meal limited company the payback period is of

3.57 years which means their invested amount for purchasing new machine will be recovered in

this time period.

Advantages :

One of the key benefit of applying this method is that it is easy to use due to simple

calculation. Like the above Happy meal limited company calculated their payback period

with simple calculations.

In addition, this method is beneficial to use in the case of uncertainty. Companies can sort

out the issue of calculating payback time period by help this method (Speaker, 2015).

Disadvantages :

The payback period method neglects time value of money.

As well as in this method, all cash flows are not included.

So, these are the advantages and disadvantages of payback period method.

2. Accounting rate of return – The term accounting rate of return can be defined as expected

percentage of rate of return on a particular investment as compare to initial investment amount

(Fan, 2015). In this method of investment appraisal, profit is taken only after deducting amount

Thus, Net present value = 278650.69 – 320000

= -41439.31

Recommendation – The internal rate of return is of 15.21 % which is acceptable and above

happy meal limited company should chose the option of buying new machinery.

(b) Benefits and limitation of each investment appraisal technique

1. Payback period method – This can be defined as a kind of method in which time period is

evaluated in order to recover the amount of money invested in any particular project (Ward and

Forker, 2017). It is calculated by particular formula which is as follows : Initial investment / net

cash flow. Herein, the aspect of above Happy meal limited company the payback period is of

3.57 years which means their invested amount for purchasing new machine will be recovered in

this time period.

Advantages :

One of the key benefit of applying this method is that it is easy to use due to simple

calculation. Like the above Happy meal limited company calculated their payback period

with simple calculations.

In addition, this method is beneficial to use in the case of uncertainty. Companies can sort

out the issue of calculating payback time period by help this method (Speaker, 2015).

Disadvantages :

The payback period method neglects time value of money.

As well as in this method, all cash flows are not included.

So, these are the advantages and disadvantages of payback period method.

2. Accounting rate of return – The term accounting rate of return can be defined as expected

percentage of rate of return on a particular investment as compare to initial investment amount

(Fan, 2015). In this method of investment appraisal, profit is taken only after deducting amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.