Financial Management Analysis and Decision Making Report - HND

VerifiedAdded on 2023/01/16

|10

|1609

|36

Report

AI Summary

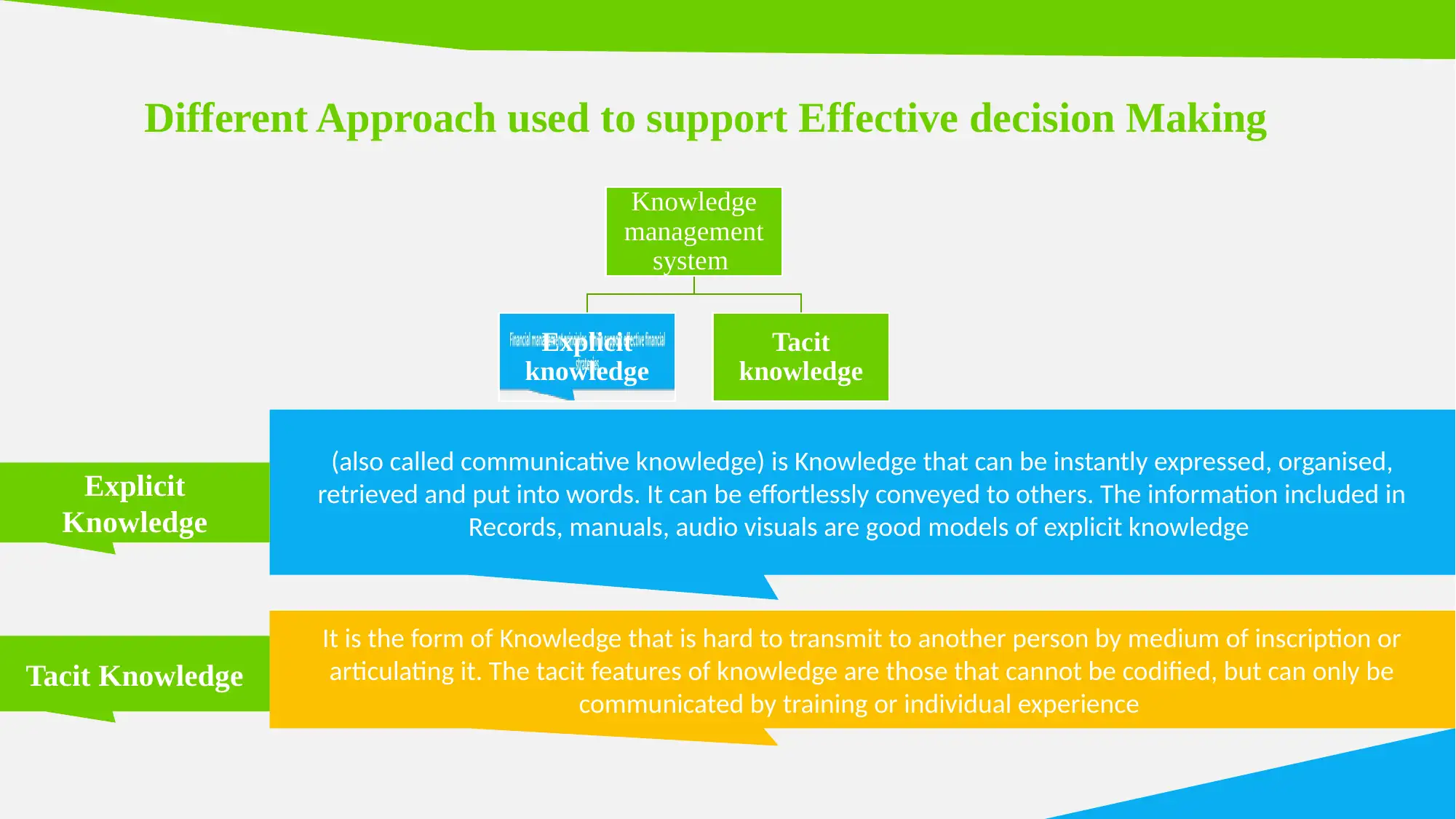

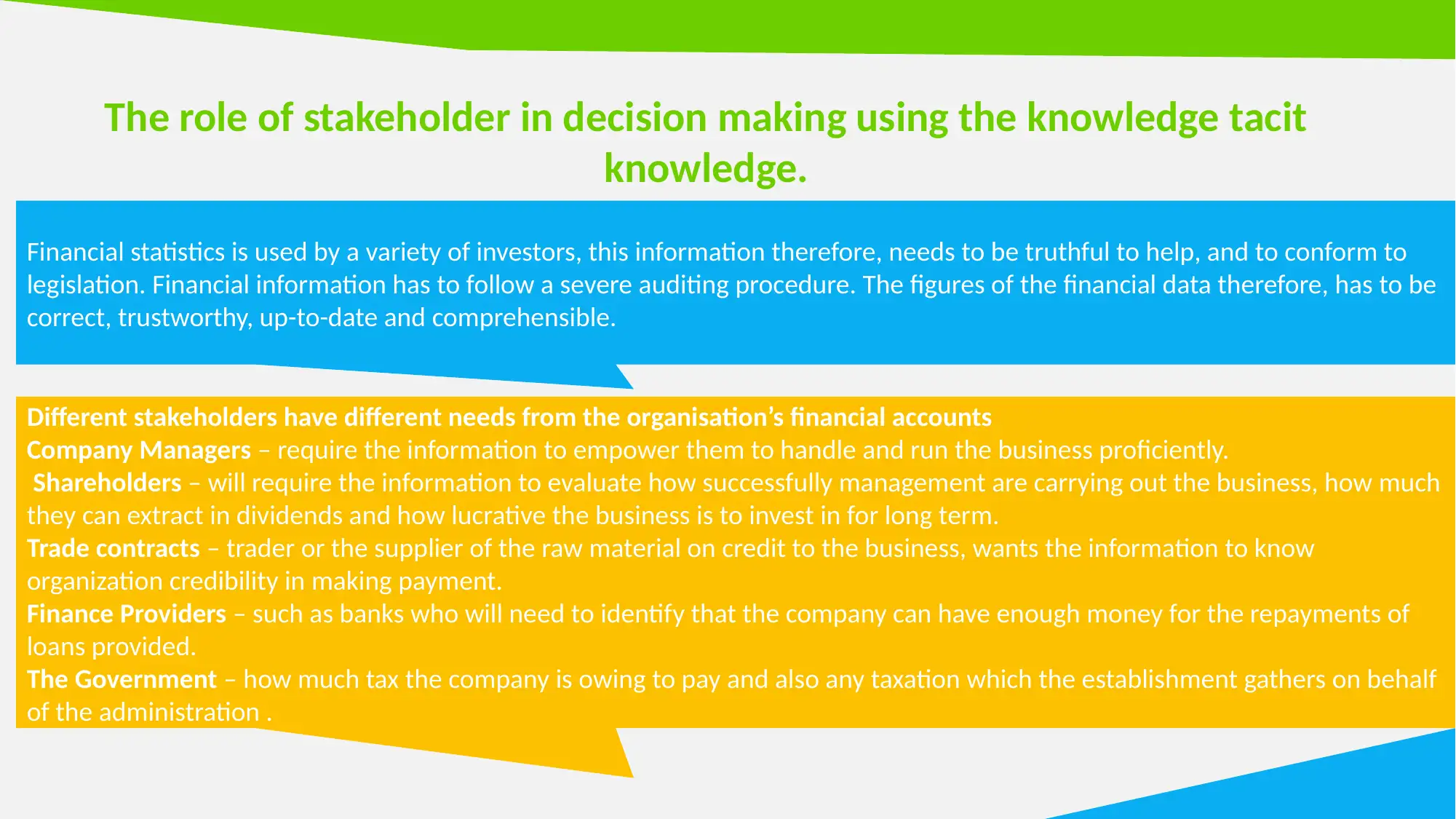

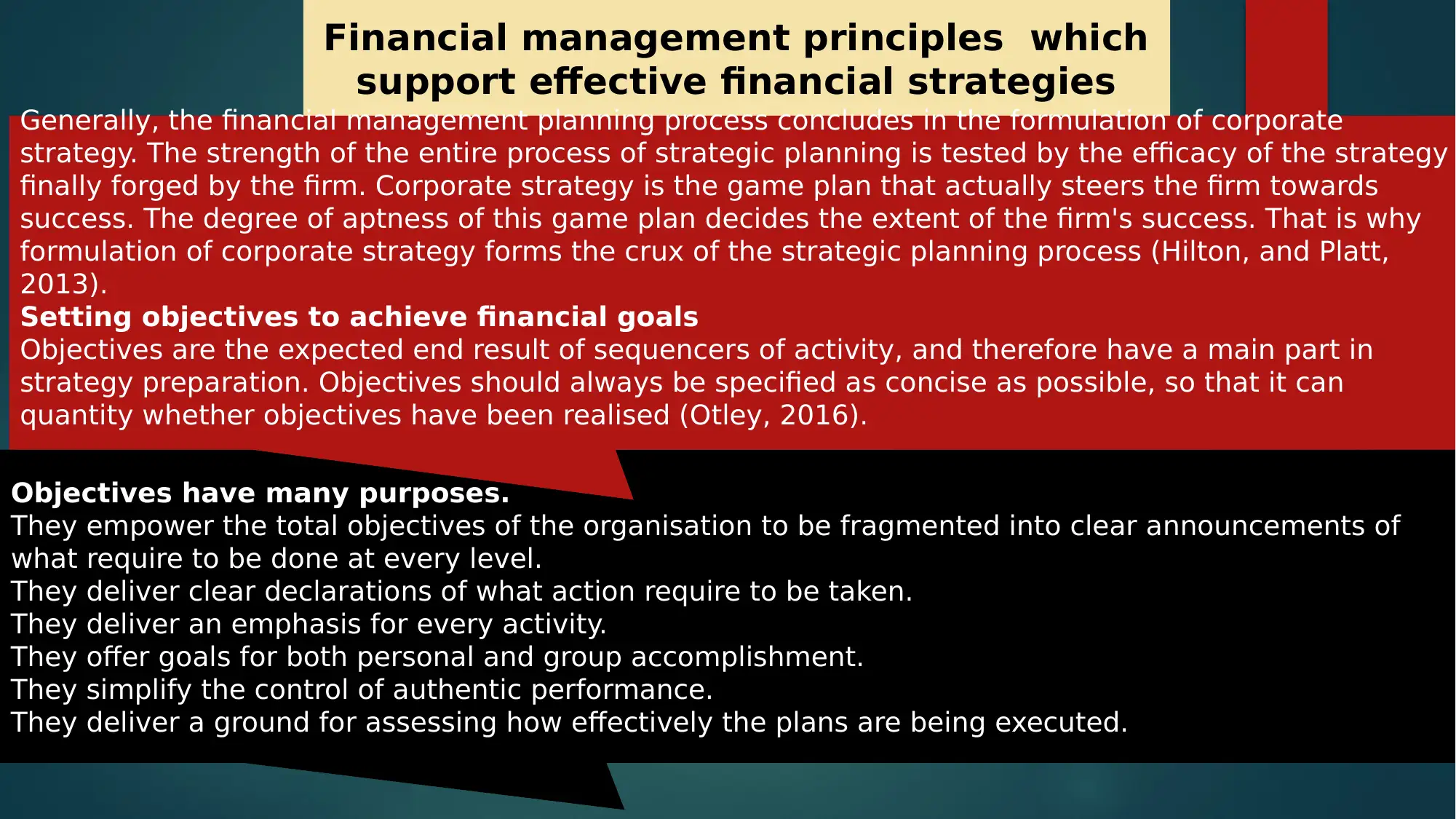

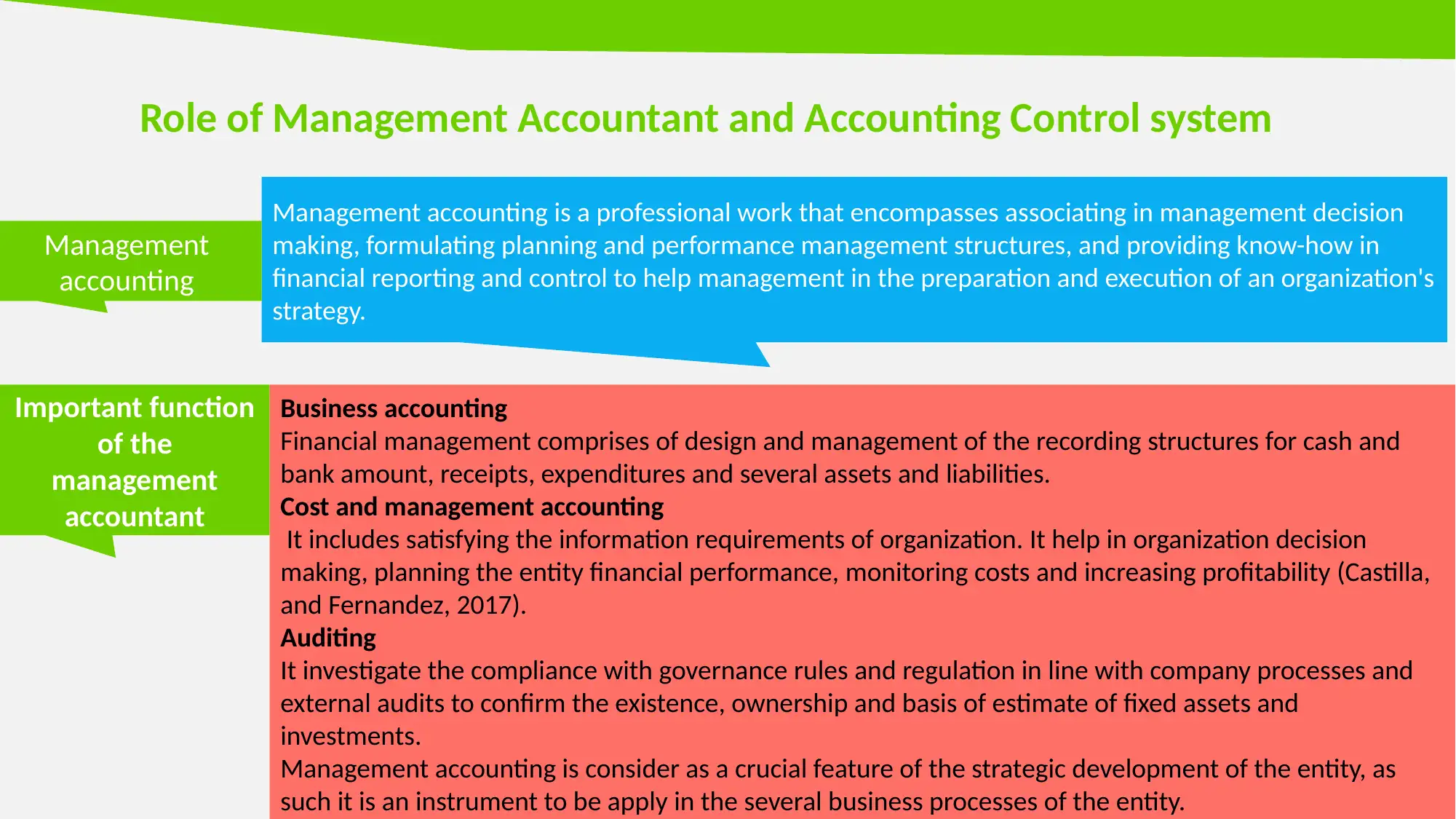

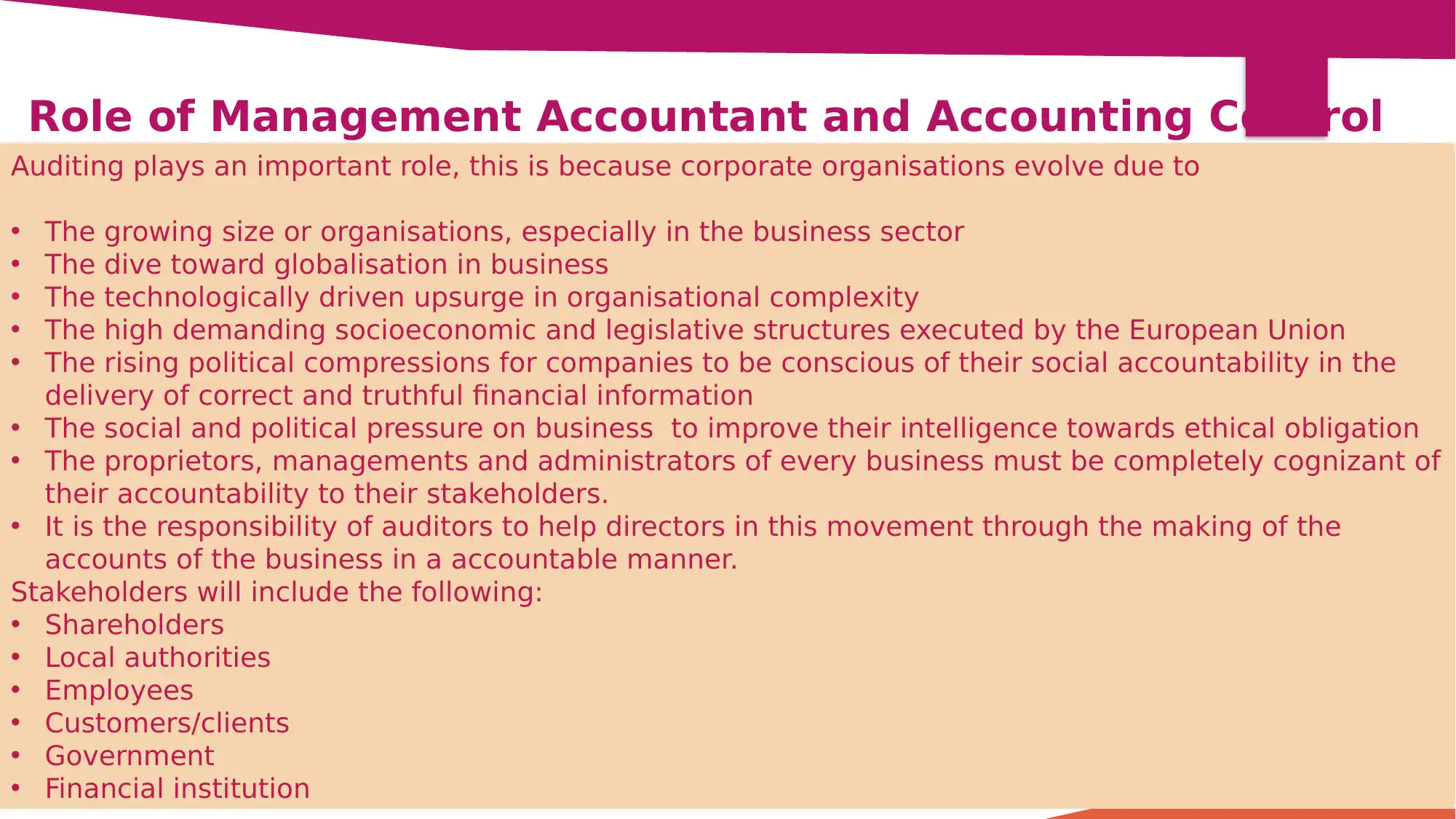

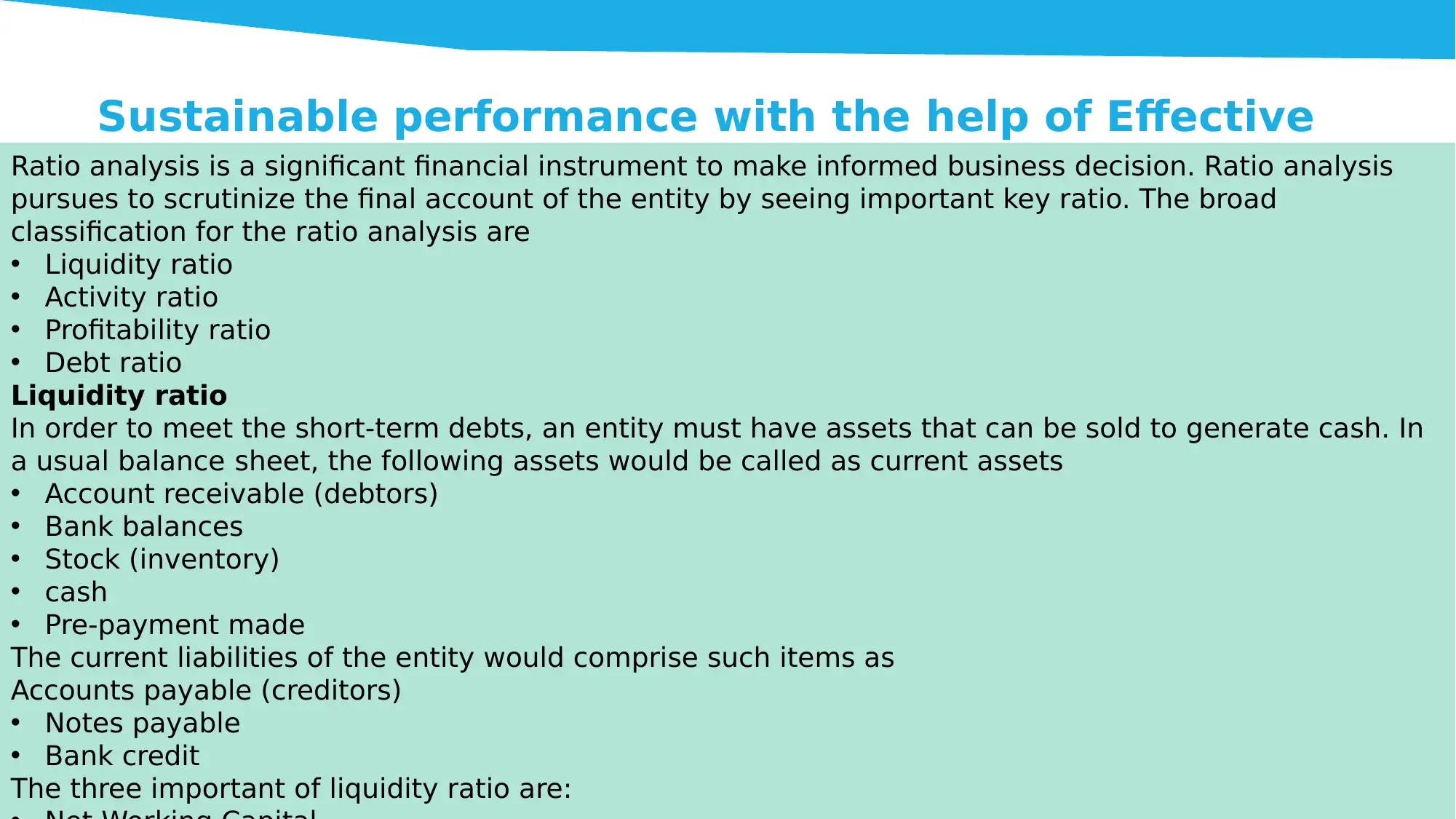

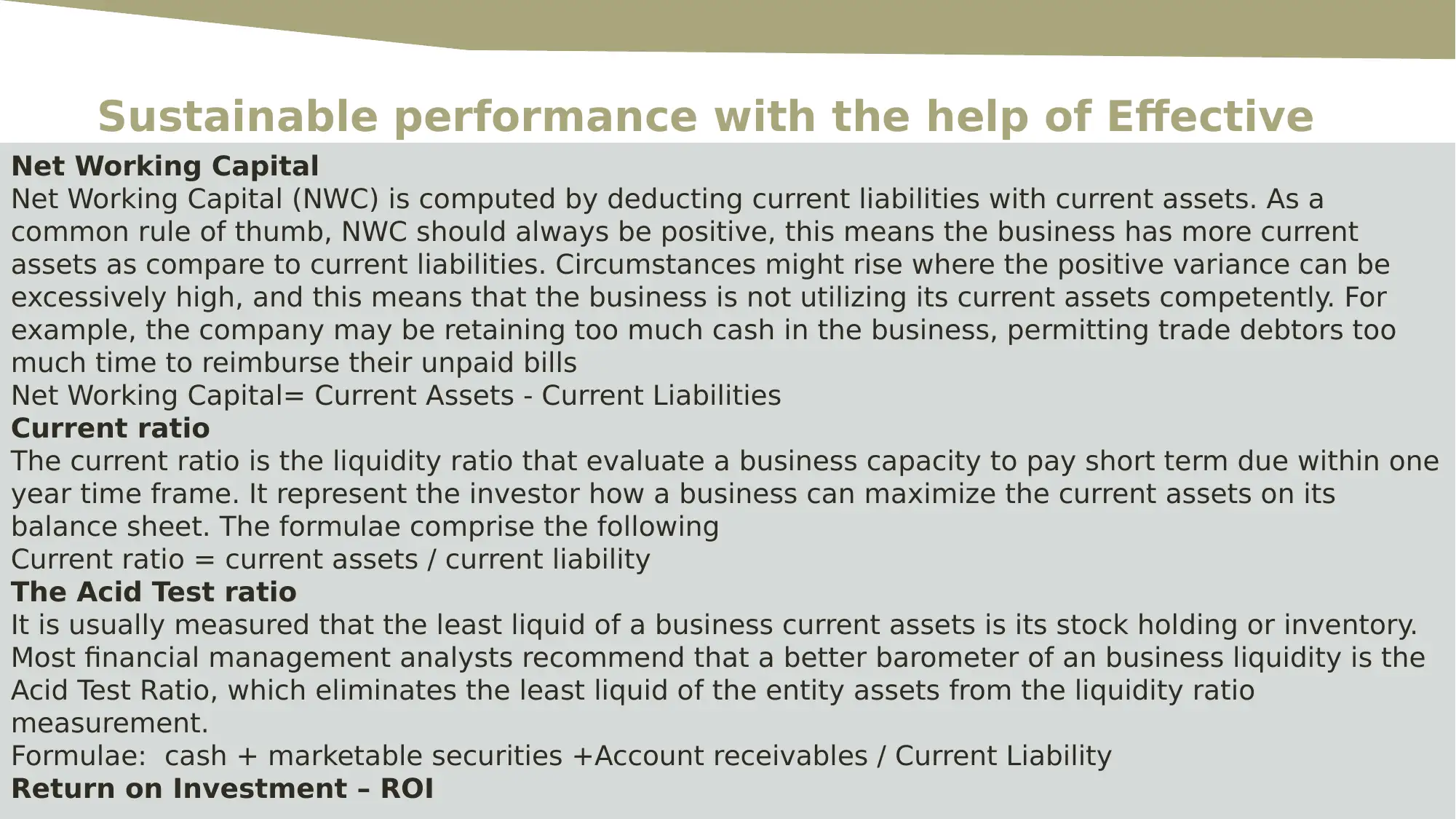

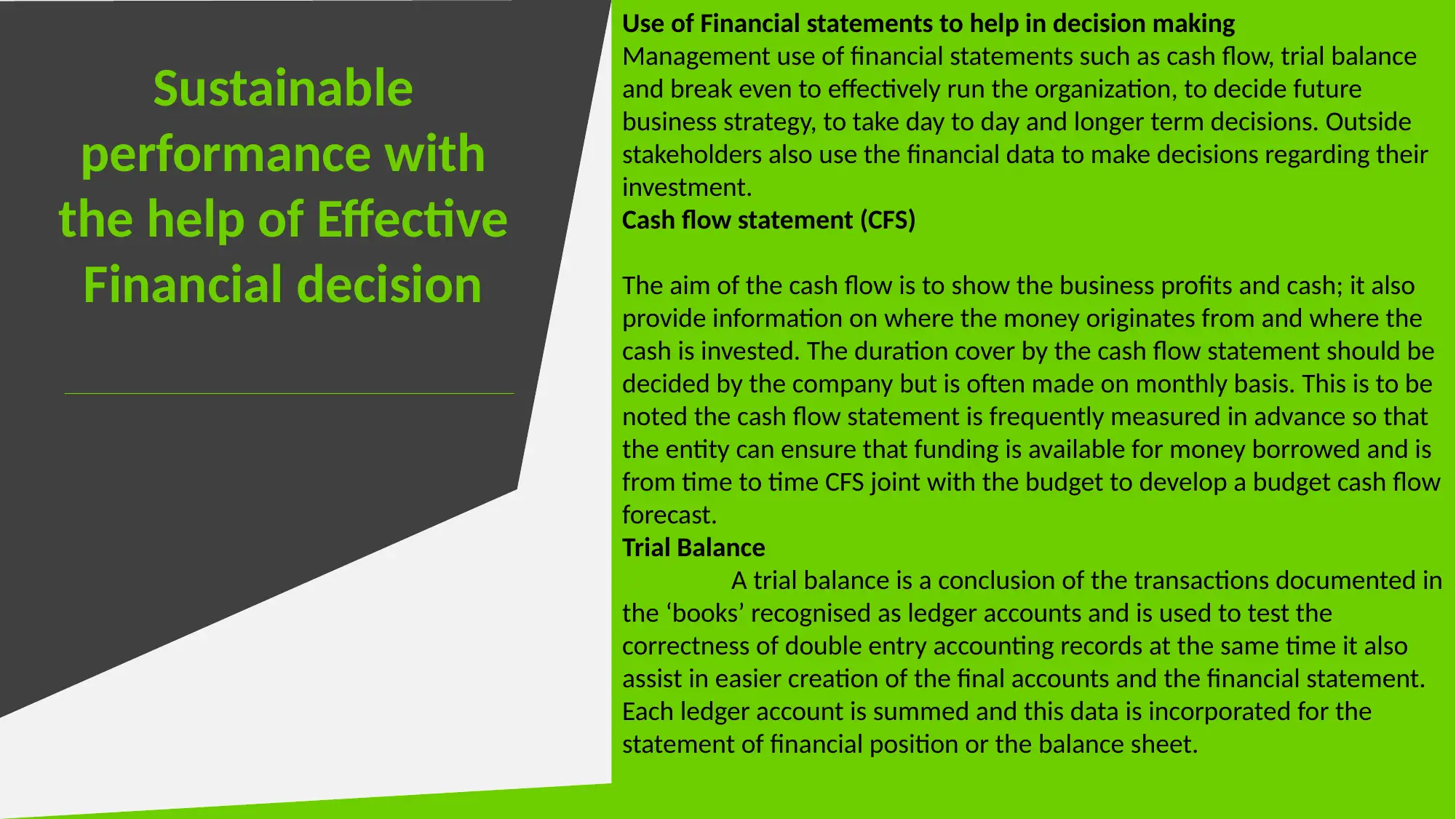

This report, submitted by a student, delves into the core principles of financial management, covering various approaches to support effective decision-making. It explores the application of knowledge management systems, including explicit and tacit knowledge, and examines the role of stakeholders in the decision-making process. The report further analyzes financial management principles that underpin effective financial strategies, such as setting objectives and the importance of corporate strategy. It also evaluates the role of management accountants and accounting control systems, highlighting the significance of auditing in ensuring compliance and accurate financial reporting. Additionally, the report discusses sustainable performance with the help of effective financial decision making, focusing on ratio analysis and the use of financial statements for informed decision-making. The report emphasizes the importance of financial statements for day-to-day and long-term decisions, benefiting both internal management and external stakeholders.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.