MBA 606: Application of Time Value of Money and Risk Analysis

VerifiedAdded on 2023/04/25

|13

|2864

|67

Report

AI Summary

This report provides a detailed analysis of the time value of money and its application in financial decision-making. It covers key concepts such as present value, future value, annuity, and perpetuity, and their importance in valuing loans, bonds, and other financial instruments. The report also evaluates standalone and portfolio risk, including the contribution of individual securities to overall portfolio risk. Practical examples and calculations are provided to illustrate these concepts, along with a loan amortization table. The report emphasizes the role of diversification in managing portfolio risk and concludes with a summary of the key findings. Desklib offers a wealth of similar solved assignments and resources for students.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Analysis of Cash Flow.................................................................................................................2

Valuing Loans..........................................................................................................................2

Time Value of Money..............................................................................................................2

Loan Classification..................................................................................................................2

Valuing Bonds.........................................................................................................................3

Present Value of Annuity.............................................................................................................5

Future Value of Annuity..............................................................................................................5

Perpetuity.....................................................................................................................................6

Portfolio Risk of Various Cash Flows and Securities.................................................................6

Contribution of Security in Portfolio Risk...................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Analysis of Cash Flow.................................................................................................................2

Valuing Loans..........................................................................................................................2

Time Value of Money..............................................................................................................2

Loan Classification..................................................................................................................2

Valuing Bonds.........................................................................................................................3

Present Value of Annuity.............................................................................................................5

Future Value of Annuity..............................................................................................................5

Perpetuity.....................................................................................................................................6

Portfolio Risk of Various Cash Flows and Securities.................................................................6

Contribution of Security in Portfolio Risk...................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2FINANCIAL MANAGEMENT

Introduction

Time value of money is an important consideration taken into account for the valuation of

the cash flows of the company. The time value of the money is taken into account for

discounting the cash flows received from an investment project or an asset. Inflation, risk factors,

potential investment return are some of the factors that affect the decision making in a company.

The various aspects and factors such as future value, present value, annuity and perpetuity was

taken into consideration for discussing the same (Muda & Hasibuan 2018).

Analysis of Cash Flow

Valuing Loans

The valuation of Loan is done for analysing the decisions, regarding performance, sub-

performing and non-performing loans. Present Value calculation, includes the analysis of the

risks and TVM when assets related decisions are made. Valuation of loan is done for analysing

the cash flows and assessing the true value of the amount that will be received (Johari et al.

2018).

Time Value of Money

The concept of time value of money shows the worth of money available today is worth

more than the same amount in the future date because of the earnings potential of the money

(Chan and Rate 2018).

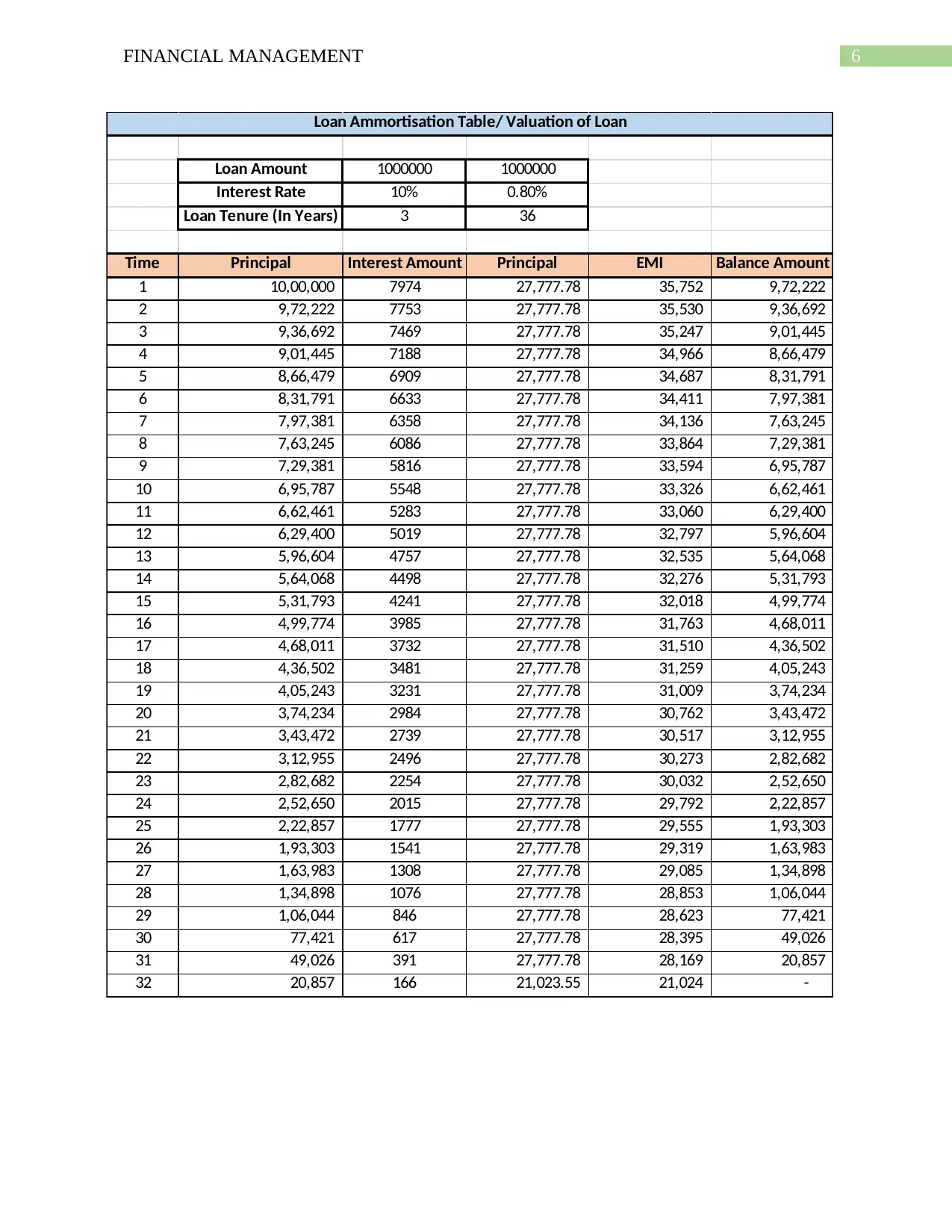

Loan Classification

The valuation of the loan depends on the type and structure of the loan. The loan

valuation that was taken into consideration for the purpose of valuation was a three year monthly

payable loan carrying an interest rate of about 10% p.a. (Alikar et al. 2017). A loan amortisation

Introduction

Time value of money is an important consideration taken into account for the valuation of

the cash flows of the company. The time value of the money is taken into account for

discounting the cash flows received from an investment project or an asset. Inflation, risk factors,

potential investment return are some of the factors that affect the decision making in a company.

The various aspects and factors such as future value, present value, annuity and perpetuity was

taken into consideration for discussing the same (Muda & Hasibuan 2018).

Analysis of Cash Flow

Valuing Loans

The valuation of Loan is done for analysing the decisions, regarding performance, sub-

performing and non-performing loans. Present Value calculation, includes the analysis of the

risks and TVM when assets related decisions are made. Valuation of loan is done for analysing

the cash flows and assessing the true value of the amount that will be received (Johari et al.

2018).

Time Value of Money

The concept of time value of money shows the worth of money available today is worth

more than the same amount in the future date because of the earnings potential of the money

(Chan and Rate 2018).

Loan Classification

The valuation of the loan depends on the type and structure of the loan. The loan

valuation that was taken into consideration for the purpose of valuation was a three year monthly

payable loan carrying an interest rate of about 10% p.a. (Alikar et al. 2017). A loan amortisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

table was prepared for the purpose of valuation of the loan and the monthly amount payable by

the borrower. The monthly EMI which would be paid by the borrower would be comprised of

payment of paying of the principal and interest component and the same time. The borrower

would be paying the loan amount in total of 36 months where the EMI would be in the form of

decreasing trend line (Cardin and Hu 2016). Now breaking down the component of EMI the

monthly instalment payment would be recovering a fixed amount of the principal amount of

27,777 and the interest would be charged on the opening balance amount at the rate of 10%. The

application of discounting plays an important role and the concepts of time value of money for

making the loan amortisation table (Jaggi, Khanna and Nidhi 2016).

Valuing Bonds

The valuation of bonds is done by the taking the amount of cash flows that would be

received from the bond in the due course of the time of the bond. The key factors which plays a

crucial role in the valuation of bond is the cash flows of the bonds and the interest rate applicable

in discounting the cash flows of the bond. The cash flows are discounted at the relevant discount

rate for determining the discounted cash flows from the bond. An hypothetical example was

taken into account for describing the valuation of bonds. The future value of the bond was taken

at 1000, the relevant coupon rate for the bond was taken at 6% payable annually and the market

interest rate for the bond was taken at 8% payable annually. The present value of the bond was

determined by discounting the cash flows that will be received from the bond to get the real

worth or the present value of the bond. The present value of the bond was calculated to be

around -948.46 and the same has been discounting the cash flows for a sum of three years of

period (Ries, Glock and Schwindl 2016).

table was prepared for the purpose of valuation of the loan and the monthly amount payable by

the borrower. The monthly EMI which would be paid by the borrower would be comprised of

payment of paying of the principal and interest component and the same time. The borrower

would be paying the loan amount in total of 36 months where the EMI would be in the form of

decreasing trend line (Cardin and Hu 2016). Now breaking down the component of EMI the

monthly instalment payment would be recovering a fixed amount of the principal amount of

27,777 and the interest would be charged on the opening balance amount at the rate of 10%. The

application of discounting plays an important role and the concepts of time value of money for

making the loan amortisation table (Jaggi, Khanna and Nidhi 2016).

Valuing Bonds

The valuation of bonds is done by the taking the amount of cash flows that would be

received from the bond in the due course of the time of the bond. The key factors which plays a

crucial role in the valuation of bond is the cash flows of the bonds and the interest rate applicable

in discounting the cash flows of the bond. The cash flows are discounted at the relevant discount

rate for determining the discounted cash flows from the bond. An hypothetical example was

taken into account for describing the valuation of bonds. The future value of the bond was taken

at 1000, the relevant coupon rate for the bond was taken at 6% payable annually and the market

interest rate for the bond was taken at 8% payable annually. The present value of the bond was

determined by discounting the cash flows that will be received from the bond to get the real

worth or the present value of the bond. The present value of the bond was calculated to be

around -948.46 and the same has been discounting the cash flows for a sum of three years of

period (Ries, Glock and Schwindl 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

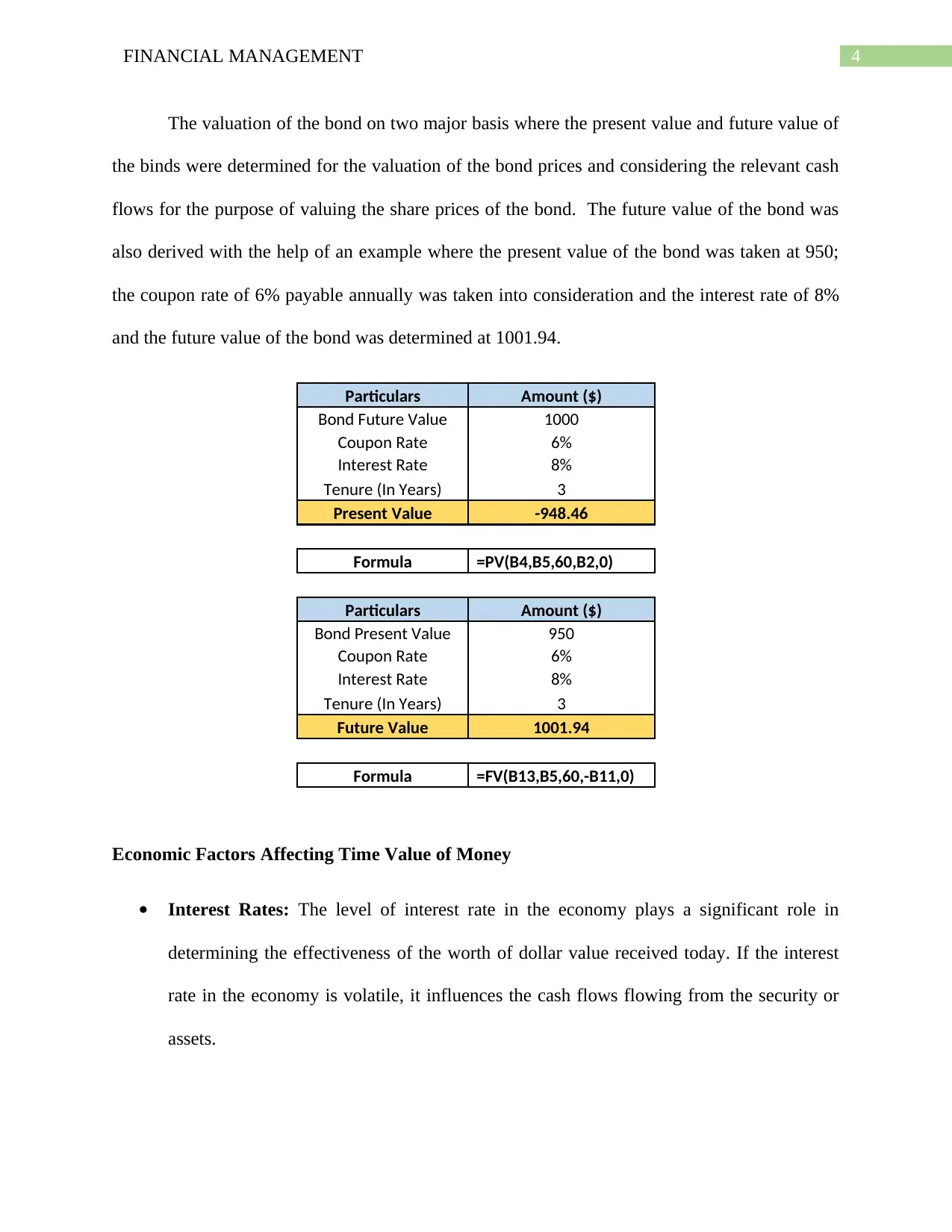

The valuation of the bond on two major basis where the present value and future value of

the binds were determined for the valuation of the bond prices and considering the relevant cash

flows for the purpose of valuing the share prices of the bond. The future value of the bond was

also derived with the help of an example where the present value of the bond was taken at 950;

the coupon rate of 6% payable annually was taken into consideration and the interest rate of 8%

and the future value of the bond was determined at 1001.94.

Particulars Amount ($)

Bond Future Value 1000

Coupon Rate 6%

Interest Rate 8%

Tenure (In Years) 3

Present Value -948.46

Formula =PV(B4,B5,60,B2,0)

Particulars Amount ($)

Bond Present Value 950

Coupon Rate 6%

Interest Rate 8%

Tenure (In Years) 3

Future Value 1001.94

Formula =FV(B13,B5,60,-B11,0)

Economic Factors Affecting Time Value of Money

Interest Rates: The level of interest rate in the economy plays a significant role in

determining the effectiveness of the worth of dollar value received today. If the interest

rate in the economy is volatile, it influences the cash flows flowing from the security or

assets.

The valuation of the bond on two major basis where the present value and future value of

the binds were determined for the valuation of the bond prices and considering the relevant cash

flows for the purpose of valuing the share prices of the bond. The future value of the bond was

also derived with the help of an example where the present value of the bond was taken at 950;

the coupon rate of 6% payable annually was taken into consideration and the interest rate of 8%

and the future value of the bond was determined at 1001.94.

Particulars Amount ($)

Bond Future Value 1000

Coupon Rate 6%

Interest Rate 8%

Tenure (In Years) 3

Present Value -948.46

Formula =PV(B4,B5,60,B2,0)

Particulars Amount ($)

Bond Present Value 950

Coupon Rate 6%

Interest Rate 8%

Tenure (In Years) 3

Future Value 1001.94

Formula =FV(B13,B5,60,-B11,0)

Economic Factors Affecting Time Value of Money

Interest Rates: The level of interest rate in the economy plays a significant role in

determining the effectiveness of the worth of dollar value received today. If the interest

rate in the economy is volatile, it influences the cash flows flowing from the security or

assets.

5FINANCIAL MANAGEMENT

Inflation Rate: The higher the inflation rate the higher is the money required from the

investor from the investments done in the form of higher interest rate or required return

from an assets.

Mortgage Cash Flow Obligations

A Mortgage cash flow obligation could be regarded to a debt security which has a

specific period and payments flowing to the bond holders in the form of interest payment and

principal payments. A mortgage cash flow obligation pays principal and interest at a

predetermined specific period of time as similar to a bond. The monthly payment from a pool of

underlying mortgages are bundled together and the same will be used for making the principal

and interest payment.

The MBS can be the best example of this scenario where the underlying security is the

portfolio of various loans given by a bank against which the bonds have been issued from the

bondholders of the company. The payment to the bondholders will be in the form of interest and

principal repayment of loans.

Inflation Rate: The higher the inflation rate the higher is the money required from the

investor from the investments done in the form of higher interest rate or required return

from an assets.

Mortgage Cash Flow Obligations

A Mortgage cash flow obligation could be regarded to a debt security which has a

specific period and payments flowing to the bond holders in the form of interest payment and

principal payments. A mortgage cash flow obligation pays principal and interest at a

predetermined specific period of time as similar to a bond. The monthly payment from a pool of

underlying mortgages are bundled together and the same will be used for making the principal

and interest payment.

The MBS can be the best example of this scenario where the underlying security is the

portfolio of various loans given by a bank against which the bonds have been issued from the

bondholders of the company. The payment to the bondholders will be in the form of interest and

principal repayment of loans.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Loan Amount 1000000 1000000

Interest Rate 10% 0.80%

Loan Tenure (In Years) 3 36

Time Principal Interest Amount Principal EMI Balance Amount

1 10,00,000 7974 27,777.78 35,752 9,72,222

2 9,72,222 7753 27,777.78 35,530 9,36,692

3 9,36,692 7469 27,777.78 35,247 9,01,445

4 9,01,445 7188 27,777.78 34,966 8,66,479

5 8,66,479 6909 27,777.78 34,687 8,31,791

6 8,31,791 6633 27,777.78 34,411 7,97,381

7 7,97,381 6358 27,777.78 34,136 7,63,245

8 7,63,245 6086 27,777.78 33,864 7,29,381

9 7,29,381 5816 27,777.78 33,594 6,95,787

10 6,95,787 5548 27,777.78 33,326 6,62,461

11 6,62,461 5283 27,777.78 33,060 6,29,400

12 6,29,400 5019 27,777.78 32,797 5,96,604

13 5,96,604 4757 27,777.78 32,535 5,64,068

14 5,64,068 4498 27,777.78 32,276 5,31,793

15 5,31,793 4241 27,777.78 32,018 4,99,774

16 4,99,774 3985 27,777.78 31,763 4,68,011

17 4,68,011 3732 27,777.78 31,510 4,36,502

18 4,36,502 3481 27,777.78 31,259 4,05,243

19 4,05,243 3231 27,777.78 31,009 3,74,234

20 3,74,234 2984 27,777.78 30,762 3,43,472

21 3,43,472 2739 27,777.78 30,517 3,12,955

22 3,12,955 2496 27,777.78 30,273 2,82,682

23 2,82,682 2254 27,777.78 30,032 2,52,650

24 2,52,650 2015 27,777.78 29,792 2,22,857

25 2,22,857 1777 27,777.78 29,555 1,93,303

26 1,93,303 1541 27,777.78 29,319 1,63,983

27 1,63,983 1308 27,777.78 29,085 1,34,898

28 1,34,898 1076 27,777.78 28,853 1,06,044

29 1,06,044 846 27,777.78 28,623 77,421

30 77,421 617 27,777.78 28,395 49,026

31 49,026 391 27,777.78 28,169 20,857

32 20,857 166 21,023.55 21,024 -

Loan Ammortisation Table/ Valuation of Loan

Loan Amount 1000000 1000000

Interest Rate 10% 0.80%

Loan Tenure (In Years) 3 36

Time Principal Interest Amount Principal EMI Balance Amount

1 10,00,000 7974 27,777.78 35,752 9,72,222

2 9,72,222 7753 27,777.78 35,530 9,36,692

3 9,36,692 7469 27,777.78 35,247 9,01,445

4 9,01,445 7188 27,777.78 34,966 8,66,479

5 8,66,479 6909 27,777.78 34,687 8,31,791

6 8,31,791 6633 27,777.78 34,411 7,97,381

7 7,97,381 6358 27,777.78 34,136 7,63,245

8 7,63,245 6086 27,777.78 33,864 7,29,381

9 7,29,381 5816 27,777.78 33,594 6,95,787

10 6,95,787 5548 27,777.78 33,326 6,62,461

11 6,62,461 5283 27,777.78 33,060 6,29,400

12 6,29,400 5019 27,777.78 32,797 5,96,604

13 5,96,604 4757 27,777.78 32,535 5,64,068

14 5,64,068 4498 27,777.78 32,276 5,31,793

15 5,31,793 4241 27,777.78 32,018 4,99,774

16 4,99,774 3985 27,777.78 31,763 4,68,011

17 4,68,011 3732 27,777.78 31,510 4,36,502

18 4,36,502 3481 27,777.78 31,259 4,05,243

19 4,05,243 3231 27,777.78 31,009 3,74,234

20 3,74,234 2984 27,777.78 30,762 3,43,472

21 3,43,472 2739 27,777.78 30,517 3,12,955

22 3,12,955 2496 27,777.78 30,273 2,82,682

23 2,82,682 2254 27,777.78 30,032 2,52,650

24 2,52,650 2015 27,777.78 29,792 2,22,857

25 2,22,857 1777 27,777.78 29,555 1,93,303

26 1,93,303 1541 27,777.78 29,319 1,63,983

27 1,63,983 1308 27,777.78 29,085 1,34,898

28 1,34,898 1076 27,777.78 28,853 1,06,044

29 1,06,044 846 27,777.78 28,623 77,421

30 77,421 617 27,777.78 28,395 49,026

31 49,026 391 27,777.78 28,169 20,857

32 20,857 166 21,023.55 21,024 -

Loan Ammortisation Table/ Valuation of Loan

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

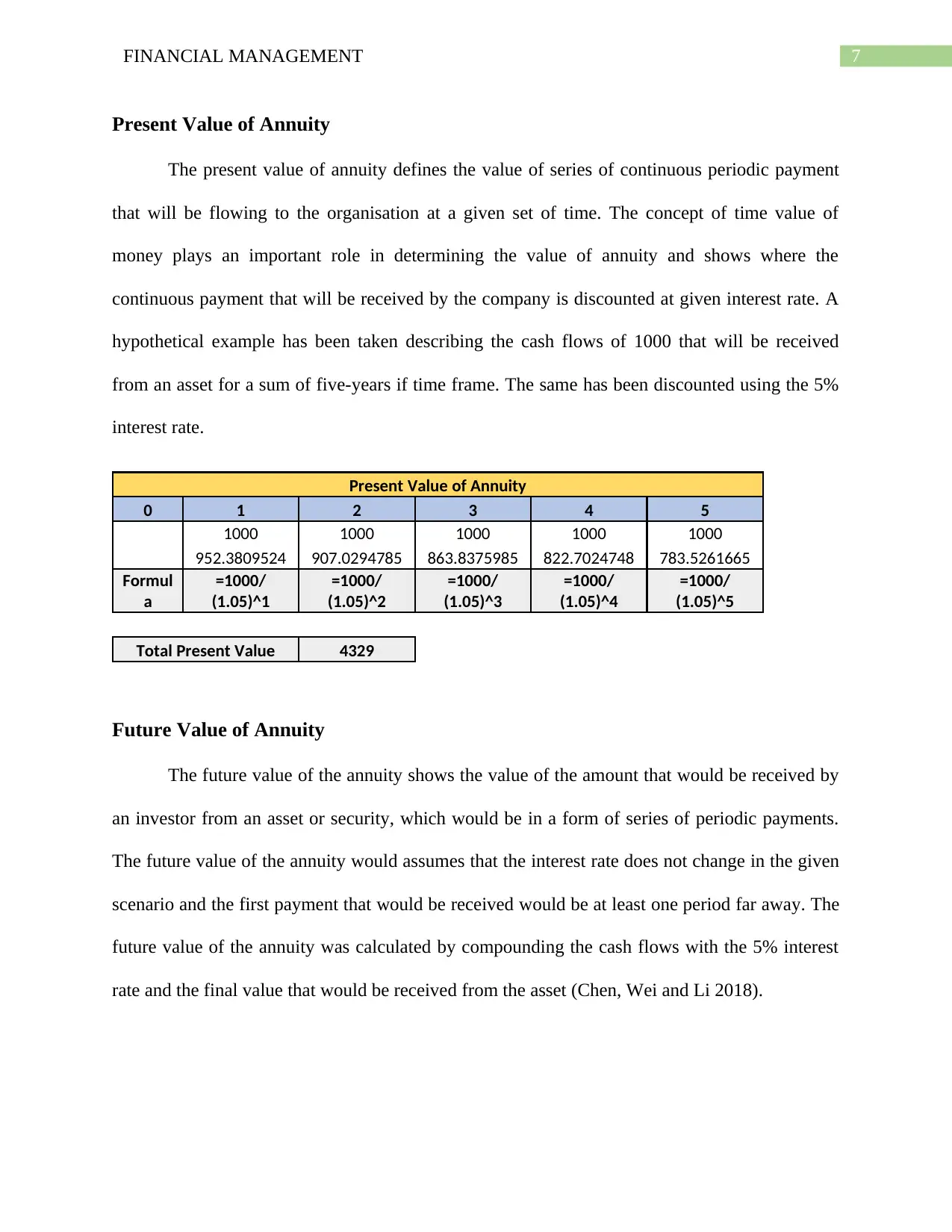

Present Value of Annuity

The present value of annuity defines the value of series of continuous periodic payment

that will be flowing to the organisation at a given set of time. The concept of time value of

money plays an important role in determining the value of annuity and shows where the

continuous payment that will be received by the company is discounted at given interest rate. A

hypothetical example has been taken describing the cash flows of 1000 that will be received

from an asset for a sum of five-years if time frame. The same has been discounted using the 5%

interest rate.

Present Value of Annuity

0 1 2 3 4 5

1000 1000 1000 1000 1000

952.3809524 907.0294785 863.8375985 822.7024748 783.5261665

Formul

a

=1000/

(1.05)^1

=1000/

(1.05)^2

=1000/

(1.05)^3

=1000/

(1.05)^4

=1000/

(1.05)^5

Total Present Value 4329

Future Value of Annuity

The future value of the annuity shows the value of the amount that would be received by

an investor from an asset or security, which would be in a form of series of periodic payments.

The future value of the annuity would assumes that the interest rate does not change in the given

scenario and the first payment that would be received would be at least one period far away. The

future value of the annuity was calculated by compounding the cash flows with the 5% interest

rate and the final value that would be received from the asset (Chen, Wei and Li 2018).

Present Value of Annuity

The present value of annuity defines the value of series of continuous periodic payment

that will be flowing to the organisation at a given set of time. The concept of time value of

money plays an important role in determining the value of annuity and shows where the

continuous payment that will be received by the company is discounted at given interest rate. A

hypothetical example has been taken describing the cash flows of 1000 that will be received

from an asset for a sum of five-years if time frame. The same has been discounted using the 5%

interest rate.

Present Value of Annuity

0 1 2 3 4 5

1000 1000 1000 1000 1000

952.3809524 907.0294785 863.8375985 822.7024748 783.5261665

Formul

a

=1000/

(1.05)^1

=1000/

(1.05)^2

=1000/

(1.05)^3

=1000/

(1.05)^4

=1000/

(1.05)^5

Total Present Value 4329

Future Value of Annuity

The future value of the annuity shows the value of the amount that would be received by

an investor from an asset or security, which would be in a form of series of periodic payments.

The future value of the annuity would assumes that the interest rate does not change in the given

scenario and the first payment that would be received would be at least one period far away. The

future value of the annuity was calculated by compounding the cash flows with the 5% interest

rate and the final value that would be received from the asset (Chen, Wei and Li 2018).

8FINANCIAL MANAGEMENT

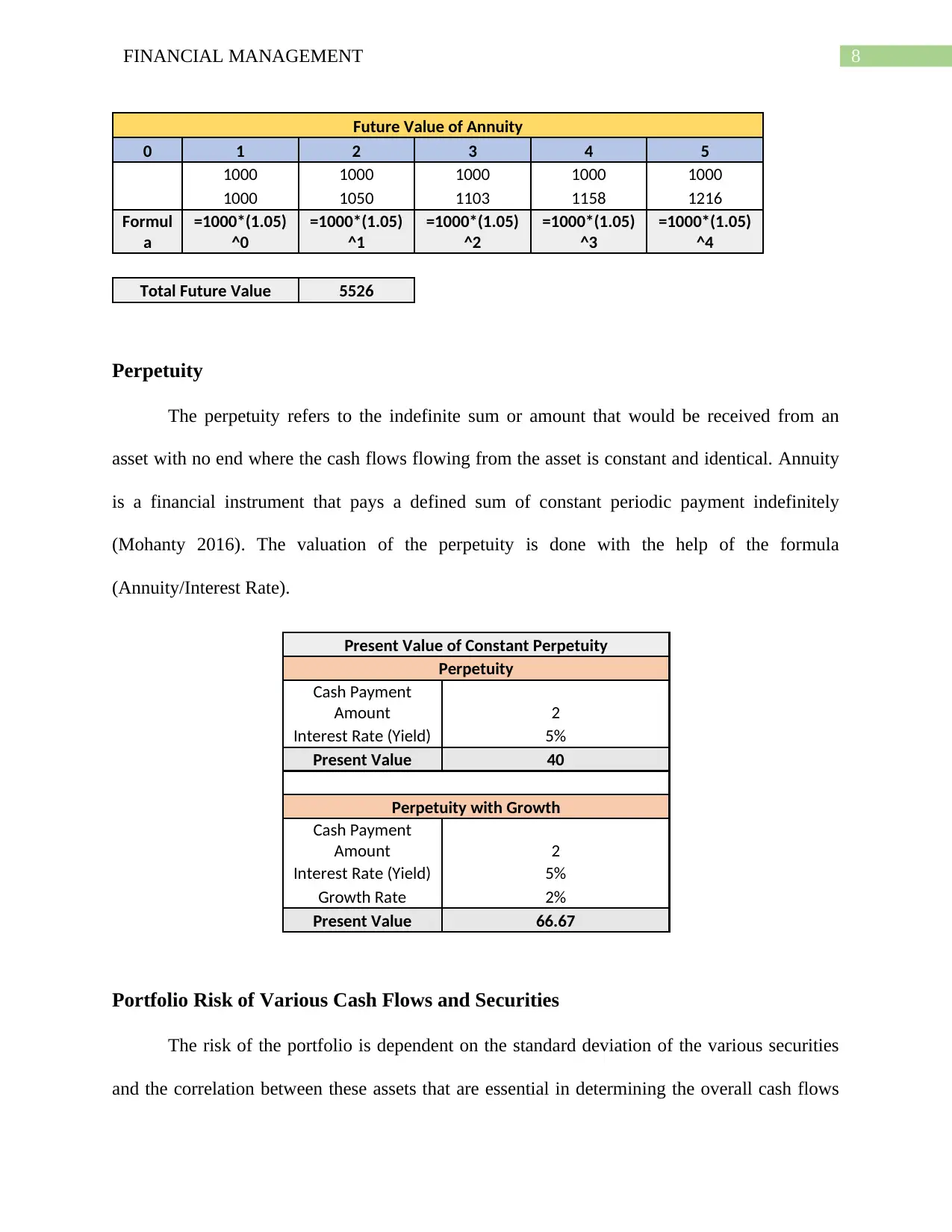

Future Value of Annuity

0 1 2 3 4 5

1000 1000 1000 1000 1000

1000 1050 1103 1158 1216

Formul

a

=1000*(1.05)

^0

=1000*(1.05)

^1

=1000*(1.05)

^2

=1000*(1.05)

^3

=1000*(1.05)

^4

Total Future Value 5526

Perpetuity

The perpetuity refers to the indefinite sum or amount that would be received from an

asset with no end where the cash flows flowing from the asset is constant and identical. Annuity

is a financial instrument that pays a defined sum of constant periodic payment indefinitely

(Mohanty 2016). The valuation of the perpetuity is done with the help of the formula

(Annuity/Interest Rate).

Present Value of Constant Perpetuity

Perpetuity

Cash Payment

Amount 2

Interest Rate (Yield) 5%

Present Value 40

Perpetuity with Growth

Cash Payment

Amount 2

Interest Rate (Yield) 5%

Growth Rate 2%

Present Value 66.67

Portfolio Risk of Various Cash Flows and Securities

The risk of the portfolio is dependent on the standard deviation of the various securities

and the correlation between these assets that are essential in determining the overall cash flows

Future Value of Annuity

0 1 2 3 4 5

1000 1000 1000 1000 1000

1000 1050 1103 1158 1216

Formul

a

=1000*(1.05)

^0

=1000*(1.05)

^1

=1000*(1.05)

^2

=1000*(1.05)

^3

=1000*(1.05)

^4

Total Future Value 5526

Perpetuity

The perpetuity refers to the indefinite sum or amount that would be received from an

asset with no end where the cash flows flowing from the asset is constant and identical. Annuity

is a financial instrument that pays a defined sum of constant periodic payment indefinitely

(Mohanty 2016). The valuation of the perpetuity is done with the help of the formula

(Annuity/Interest Rate).

Present Value of Constant Perpetuity

Perpetuity

Cash Payment

Amount 2

Interest Rate (Yield) 5%

Present Value 40

Perpetuity with Growth

Cash Payment

Amount 2

Interest Rate (Yield) 5%

Growth Rate 2%

Present Value 66.67

Portfolio Risk of Various Cash Flows and Securities

The risk of the portfolio is dependent on the standard deviation of the various securities

and the correlation between these assets that are essential in determining the overall cash flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

from the same. The contribution of the securities in the risk return of the portfolio is of great

importance where the risk and return of the portfolio is calculate with the help of the weight of

each security and there contribution in the overall risk and return of the portfolio (Monga and

Zor 2018).

Diversification plays a crucial risk in the portfolio where adding more and more security

reduces the overall risk of the portfolio and modifies the risk of the portfolio. Adding more

securities, which are less correlated, will be helping the company in reducing the risk of portfolio

and making the portfolio to be more efficient.

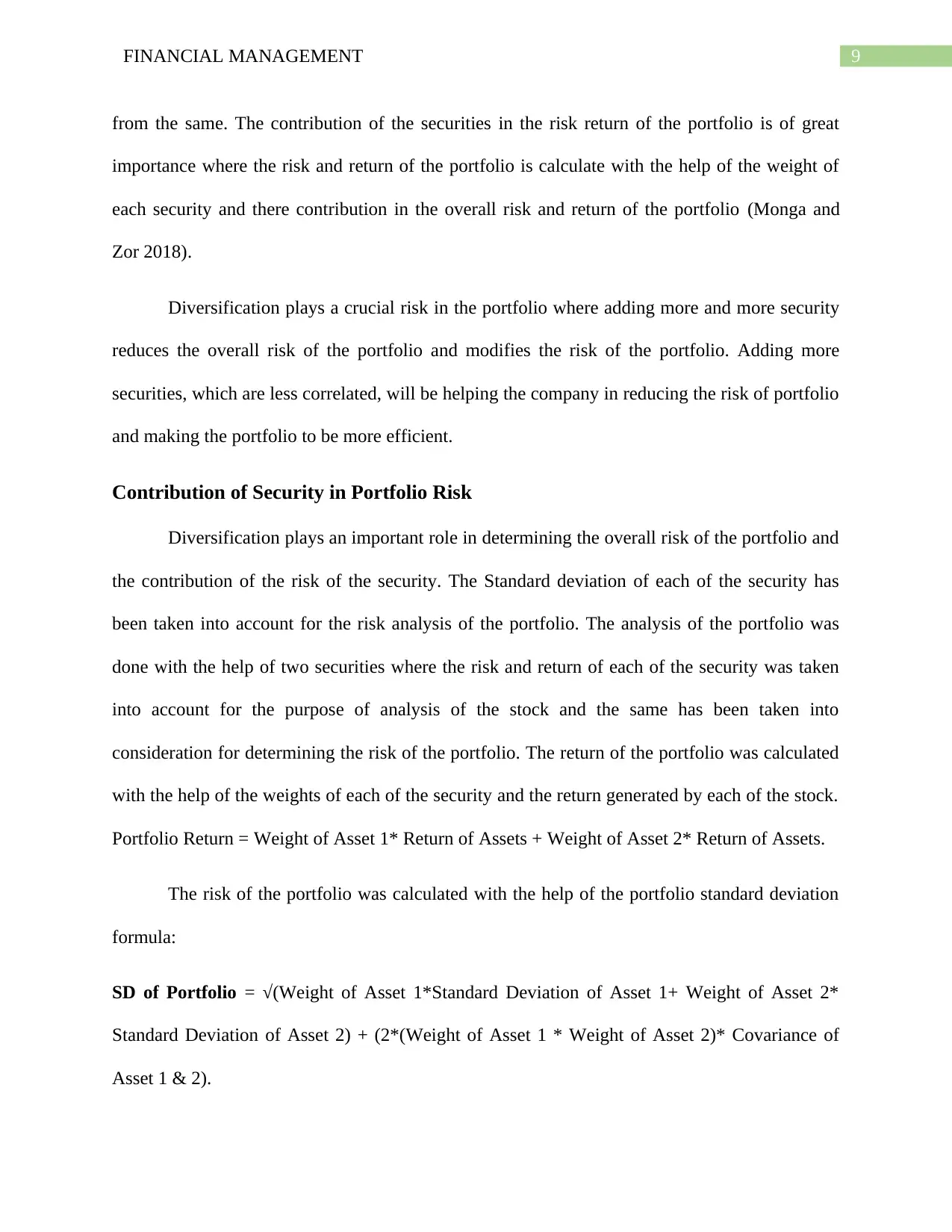

Contribution of Security in Portfolio Risk

Diversification plays an important role in determining the overall risk of the portfolio and

the contribution of the risk of the security. The Standard deviation of each of the security has

been taken into account for the risk analysis of the portfolio. The analysis of the portfolio was

done with the help of two securities where the risk and return of each of the security was taken

into account for the purpose of analysis of the stock and the same has been taken into

consideration for determining the risk of the portfolio. The return of the portfolio was calculated

with the help of the weights of each of the security and the return generated by each of the stock.

Portfolio Return = Weight of Asset 1* Return of Assets + Weight of Asset 2* Return of Assets.

The risk of the portfolio was calculated with the help of the portfolio standard deviation

formula:

SD of Portfolio = √(Weight of Asset 1*Standard Deviation of Asset 1+ Weight of Asset 2*

Standard Deviation of Asset 2) + (2*(Weight of Asset 1 * Weight of Asset 2)* Covariance of

Asset 1 & 2).

from the same. The contribution of the securities in the risk return of the portfolio is of great

importance where the risk and return of the portfolio is calculate with the help of the weight of

each security and there contribution in the overall risk and return of the portfolio (Monga and

Zor 2018).

Diversification plays a crucial risk in the portfolio where adding more and more security

reduces the overall risk of the portfolio and modifies the risk of the portfolio. Adding more

securities, which are less correlated, will be helping the company in reducing the risk of portfolio

and making the portfolio to be more efficient.

Contribution of Security in Portfolio Risk

Diversification plays an important role in determining the overall risk of the portfolio and

the contribution of the risk of the security. The Standard deviation of each of the security has

been taken into account for the risk analysis of the portfolio. The analysis of the portfolio was

done with the help of two securities where the risk and return of each of the security was taken

into account for the purpose of analysis of the stock and the same has been taken into

consideration for determining the risk of the portfolio. The return of the portfolio was calculated

with the help of the weights of each of the security and the return generated by each of the stock.

Portfolio Return = Weight of Asset 1* Return of Assets + Weight of Asset 2* Return of Assets.

The risk of the portfolio was calculated with the help of the portfolio standard deviation

formula:

SD of Portfolio = √(Weight of Asset 1*Standard Deviation of Asset 1+ Weight of Asset 2*

Standard Deviation of Asset 2) + (2*(Weight of Asset 1 * Weight of Asset 2)* Covariance of

Asset 1 & 2).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

The standard deviation of the portfolio was calculated to be around 12% where the risk of

the portfolio got modified and the return of the portfolio on the overall basis was modified.

Particulars

Investment

Amount Return Weight Standard Deviation

Asset 1 60,000 20% 60% 10%

Asset 2 40,000 12% 40% 16%

Correlation 1

Portfolio Return = Weight of Asset 1* Return of Asset + Weight of Asset 2* Return of Asset

Return of Portfolio 0.6*20%+0.4*12%

Portfolio Return 16.80%

Portfolio Risk

SD of Portfolio = √(Weight of Asset 1*S.D of Asset 1+ Weight of Asset 2* S.D of Asset 2) + (2*(Weight

of Asset 1 * Weight of Asset 2)* Covariance of Asset 1 & 2)

SD of Portfolio = sqrt(0.6^2*10^2 + 0.4^2*16^2 + 2*0.6*0.4*1*0.10*0.16)

SD of Portfolio 12.29%

Conclusion

The application of the time value of money was taken into account for the purpose of the

discussion of the various concept associated with the time value of money. There were various

examples and scenarios taken into consideration for the purpose of discussing the various factors

of time value of money. Annuity, Perpetuity were some of the crucial factors, which were

discussed in the report, and the importance of same in valuing the cash flows of the same.

The standard deviation of the portfolio was calculated to be around 12% where the risk of

the portfolio got modified and the return of the portfolio on the overall basis was modified.

Particulars

Investment

Amount Return Weight Standard Deviation

Asset 1 60,000 20% 60% 10%

Asset 2 40,000 12% 40% 16%

Correlation 1

Portfolio Return = Weight of Asset 1* Return of Asset + Weight of Asset 2* Return of Asset

Return of Portfolio 0.6*20%+0.4*12%

Portfolio Return 16.80%

Portfolio Risk

SD of Portfolio = √(Weight of Asset 1*S.D of Asset 1+ Weight of Asset 2* S.D of Asset 2) + (2*(Weight

of Asset 1 * Weight of Asset 2)* Covariance of Asset 1 & 2)

SD of Portfolio = sqrt(0.6^2*10^2 + 0.4^2*16^2 + 2*0.6*0.4*1*0.10*0.16)

SD of Portfolio 12.29%

Conclusion

The application of the time value of money was taken into account for the purpose of the

discussion of the various concept associated with the time value of money. There were various

examples and scenarios taken into consideration for the purpose of discussing the various factors

of time value of money. Annuity, Perpetuity were some of the crucial factors, which were

discussed in the report, and the importance of same in valuing the cash flows of the same.

11FINANCIAL MANAGEMENT

References

Alikar, N., Mousavi, S.M., Ghazilla, R.A.R., Tavana, M. and Olugu, E.U., 2017. A bi-objective

multi-period series-parallel inventory-redundancy allocation problem with time value of money

and inflation considerations. Computers & Industrial Engineering, 104, pp.51-67.

Cardin, M.A. and Hu, J., 2016. Analyzing the tradeoffs between economies of scale, time-value

of money, and flexibility in design under uncertainty: Study of centralized versus decentralized

waste-to-energy systems. Journal of Mechanical Design, 138(1), p.011401.

Chan, K. and Rate, E.A.I., 2018. & 6 The Time Value of Money. Financial Management.

Chen, W., Wei, L. and Li, Y., 2018. Fuzzy multicycle manufacturing/remanufacturing

production decisions considering inflation and the time value of money. Journal of Cleaner

Production, 198, pp.1494-1502.

Jaggi, C., Khanna, A. and Nidhi, N., 2016. Effects of inflation and time value of money on an

inventory system with deteriorating items and partially backlogged shortages. International

Journal of Industrial Engineering Computations, 7(2), pp.267-282.

Johari, M., Hosseini-Motlagh, S.M., Nematollahi, M., Goh, M. and Ignatius, J., 2018. Bi-level

credit period coordination for periodic review inventory system with price-credit dependent

demand under time value of money. Transportation Research Part E: Logistics and

Transportation Review, 114, pp.270-291.

Mohanty, B., 2016. NOC: Time Value of Money: Concepts and Calculations.

Monga, A. and Zor, O., 2018. Time versus Money. Current opinion in psychology.

References

Alikar, N., Mousavi, S.M., Ghazilla, R.A.R., Tavana, M. and Olugu, E.U., 2017. A bi-objective

multi-period series-parallel inventory-redundancy allocation problem with time value of money

and inflation considerations. Computers & Industrial Engineering, 104, pp.51-67.

Cardin, M.A. and Hu, J., 2016. Analyzing the tradeoffs between economies of scale, time-value

of money, and flexibility in design under uncertainty: Study of centralized versus decentralized

waste-to-energy systems. Journal of Mechanical Design, 138(1), p.011401.

Chan, K. and Rate, E.A.I., 2018. & 6 The Time Value of Money. Financial Management.

Chen, W., Wei, L. and Li, Y., 2018. Fuzzy multicycle manufacturing/remanufacturing

production decisions considering inflation and the time value of money. Journal of Cleaner

Production, 198, pp.1494-1502.

Jaggi, C., Khanna, A. and Nidhi, N., 2016. Effects of inflation and time value of money on an

inventory system with deteriorating items and partially backlogged shortages. International

Journal of Industrial Engineering Computations, 7(2), pp.267-282.

Johari, M., Hosseini-Motlagh, S.M., Nematollahi, M., Goh, M. and Ignatius, J., 2018. Bi-level

credit period coordination for periodic review inventory system with price-credit dependent

demand under time value of money. Transportation Research Part E: Logistics and

Transportation Review, 114, pp.270-291.

Mohanty, B., 2016. NOC: Time Value of Money: Concepts and Calculations.

Monga, A. and Zor, O., 2018. Time versus Money. Current opinion in psychology.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.