Financial Management: Ratio Analysis and Decision-Making Process

VerifiedAdded on 2023/01/10

|21

|5508

|99

Report

AI Summary

This report provides an analysis of financial management, covering decision-making approaches, stakeholder management, and the value of management accounting techniques in controlling costs and maximizing shareholder value. It includes a financial ratio analysis of J Sainsbury PLC for the years 2018, 2019, and 2020, examining investment appraisal techniques and recommendations for improving financial sustainability. The report also discusses fraud detection and prevention techniques, ethical decision-making approaches, and the role of financial decision-making in long-term sustainability. The overall aim is to provide insights into effective financial resource management and strategic decision-making within a business context, aligning with the principles of financial management for optimal resource utilization.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Scenario A........................................................................................................................................3

1.Approaches, techniques and factors contributing in effective decision making. ...............3

2. Stakeholder management & managing conflicting objectives of the different group of

stakeholders............................................................................................................................5

3. Value of the MA techniques in controlling cost and in maximizing the shareholders value .6

4.Techniques for fraud detection and prevention and approaches for ethical decision making.

................................................................................................................................................7

5. Reflection...........................................................................................................................8

Scenario B........................................................................................................................................9

1. Financial ratios analysis of J Sainsbury PLC for the year 2020, 2019 & 2018..................9

2. Analysing investment appraisal techniques utilized in taking actions to maximize ROI 17

Recommendations to improve financial sustainability.........................................................18

3. Value of techniques..........................................................................................................18

4. Financial decision making in long term sustainability ....................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUCTION...........................................................................................................................3

Scenario A........................................................................................................................................3

1.Approaches, techniques and factors contributing in effective decision making. ...............3

2. Stakeholder management & managing conflicting objectives of the different group of

stakeholders............................................................................................................................5

3. Value of the MA techniques in controlling cost and in maximizing the shareholders value .6

4.Techniques for fraud detection and prevention and approaches for ethical decision making.

................................................................................................................................................7

5. Reflection...........................................................................................................................8

Scenario B........................................................................................................................................9

1. Financial ratios analysis of J Sainsbury PLC for the year 2020, 2019 & 2018..................9

2. Analysing investment appraisal techniques utilized in taking actions to maximize ROI 17

Recommendations to improve financial sustainability.........................................................18

3. Value of techniques..........................................................................................................18

4. Financial decision making in long term sustainability ....................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

INTRODUCTION

Financial management is focused on the managing the financial resources of the business

organization with the objective of optimum utilizing it. It involves implementation of financial

management principles and techniques for effective utilization of resources. This report states

about the various techniques and factors which leads to improved decision and effective

management of the stakeholders in attaining the desired goals. It also covers the financial ratio

analysis of the Sainsbury PLC to gain an insight about the financial performance and position of

the business.

Scenario A

1.Approaches, techniques and factors contributing in effective decision making.

Different approaches for decision making

Knowledge Based Approac

Knowledge based approach uses a pre- determined criteria for measuring and ensuring

optimal outcome for the specific topic. This approach is highly useful in strategic and effective

decision making establishing reasoning and thought process behind every decision taken by the

management. Managers before taking any critical decisions are required to gather all the relevant

information and essential details for getting better understanding of the decision area and making

decisions that will give best outcome. This approach promotes open communication between

leaders and the employees. This approach is highly used in the organisation for making decisions

that have significant impact over the operations of business. The decisions are not taken simply

on beliefs or thoughts regarding particular topic but by making thorough analysis of all the

factors associated with the decisions.

Formal Approach

This is critical to the success of the organisation. This approach ensure that the decision

makers are having right information for making the decisions. Managers should be familiar with

the organisational strategies implemented. They should knowledge about the reasons due to

which projects are falling short. This approach follows a set structure for making decisions for

the business. It makes the company to make effective decisions analysing the decision areas

more adequately (Lusardiand Mitchell, 2017). In this approach decision are taken by the top

level executives and management team without involving lower level subordinates or staff. They

are required to follow the set instruction for achieving the goals of organisation.

Financial management is focused on the managing the financial resources of the business

organization with the objective of optimum utilizing it. It involves implementation of financial

management principles and techniques for effective utilization of resources. This report states

about the various techniques and factors which leads to improved decision and effective

management of the stakeholders in attaining the desired goals. It also covers the financial ratio

analysis of the Sainsbury PLC to gain an insight about the financial performance and position of

the business.

Scenario A

1.Approaches, techniques and factors contributing in effective decision making.

Different approaches for decision making

Knowledge Based Approac

Knowledge based approach uses a pre- determined criteria for measuring and ensuring

optimal outcome for the specific topic. This approach is highly useful in strategic and effective

decision making establishing reasoning and thought process behind every decision taken by the

management. Managers before taking any critical decisions are required to gather all the relevant

information and essential details for getting better understanding of the decision area and making

decisions that will give best outcome. This approach promotes open communication between

leaders and the employees. This approach is highly used in the organisation for making decisions

that have significant impact over the operations of business. The decisions are not taken simply

on beliefs or thoughts regarding particular topic but by making thorough analysis of all the

factors associated with the decisions.

Formal Approach

This is critical to the success of the organisation. This approach ensure that the decision

makers are having right information for making the decisions. Managers should be familiar with

the organisational strategies implemented. They should knowledge about the reasons due to

which projects are falling short. This approach follows a set structure for making decisions for

the business. It makes the company to make effective decisions analysing the decision areas

more adequately (Lusardiand Mitchell, 2017). In this approach decision are taken by the top

level executives and management team without involving lower level subordinates or staff. They

are required to follow the set instruction for achieving the goals of organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Informal Approach

This approach uses the intuitive reasoning and is also subject to the cognitive biases. It is

the decision approach that do not uses and set structure for making decisions. This involves

making decisions on instant basis. This approach is followed in the organisation generally for

making the decisions which are required to be taken immediately in any of the situation. This

approach does not gives time to managers on deciding about various factors influencing the

decisions. Informal decisions are taken by the enterprise by involving employees and team

members for making more accurate decisions. Employees are involves as they are the people

who have more correct knowledge as deal with the operations more closely.

Make or Buy decisions

Make or buy decisions refers to act to make strategic choices between internal,

production of the items or to buy from external sources. Buy side decisions are known as

outsourcing. These decisions arise generally when the firm has developed part or product or is

significantly modified the product or part and is having issues with the current suppliers or

changing demand (Carvalho, Meier and Wang, 2016). These decisions are conducted over the

operational and strategic decisions. At strategic level includes analysis of future and current

environment. In these decisions it takes the decision which proves to be most beneficial for the

entity. These decisions are taken by analysing all the factors associated with the buying or

making the products or item.

Limiting Factor Analysis

There are different constraints that could affect the growth and sales maximisation

Along with taking decision management is also required to consider the factors that could affect

growth of the business and affects the maximisation of sales. These includes government

regulations which are required to be considered before taking any decisions as it has to comply

with all the rules and regulations. It has to analyse the market conditions regarding the products

its demand and supply (Taylor and Parsons, IP Reservoir LLC, 2018). Management has to

undertake competitor analysis of the decisions regarding the products or services.

This approach uses the intuitive reasoning and is also subject to the cognitive biases. It is

the decision approach that do not uses and set structure for making decisions. This involves

making decisions on instant basis. This approach is followed in the organisation generally for

making the decisions which are required to be taken immediately in any of the situation. This

approach does not gives time to managers on deciding about various factors influencing the

decisions. Informal decisions are taken by the enterprise by involving employees and team

members for making more accurate decisions. Employees are involves as they are the people

who have more correct knowledge as deal with the operations more closely.

Make or Buy decisions

Make or buy decisions refers to act to make strategic choices between internal,

production of the items or to buy from external sources. Buy side decisions are known as

outsourcing. These decisions arise generally when the firm has developed part or product or is

significantly modified the product or part and is having issues with the current suppliers or

changing demand (Carvalho, Meier and Wang, 2016). These decisions are conducted over the

operational and strategic decisions. At strategic level includes analysis of future and current

environment. In these decisions it takes the decision which proves to be most beneficial for the

entity. These decisions are taken by analysing all the factors associated with the buying or

making the products or item.

Limiting Factor Analysis

There are different constraints that could affect the growth and sales maximisation

Along with taking decision management is also required to consider the factors that could affect

growth of the business and affects the maximisation of sales. These includes government

regulations which are required to be considered before taking any decisions as it has to comply

with all the rules and regulations. It has to analyse the market conditions regarding the products

its demand and supply (Taylor and Parsons, IP Reservoir LLC, 2018). Management has to

undertake competitor analysis of the decisions regarding the products or services.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Stakeholder management & managing conflicting objectives of the different group of

stakeholders.

Managing the stakeholders refers to the process through which an individual could

monitor, organize and improves the relationships with that of the stakeholders. It includes

systematically determining the stakeholders, assessing their expectations and needs, planning and

executing several tasks for engaging them in the management of the company. The conflict of

the objective among the different stakeholders could be managed through several ways that are

as follows-

Setting objectives for achieving the financial goals- It means as setting the different

goals as per the term in order to achieve the finance related goals in effective manner. Setting up

short, long and the medium term goals is counted as an important task towards becoming as

financially secure (Armour and et.al., 2016). Making an annual financial plan provides an entity

with new opportunities in formally reviewing the goals, reviewing progress and updating it in

timely manner. In case the company never set the goals prior to developing plan, the period of

planning provides an opportunity in formulating it so that the firm could perform within the set

target or financial footing. Adequate financial & the retirement planning begins with the setting

goals with an inclusion of short, long and medium term objectives. The main short period goal

involves setting the budget and starting with an emergency fund. The medium term objectives

involves key insurances, however long run goals require emphasizing on the retirement.

Ethical FM- It is essential for the financial managers in handling the large sum of an

organization's money. It is important to have the code of ethics in the finance for living up with

those principles each day. The role of an ethics in FM is to protect, balance and preserves the

interest of stakeholders. The standards that are found in the ethical code involves acting with

integrity & honesty, avoiding the conflict of an interest in the professional relationships and

avoiding appearance of such type of conflicts (Holynskyy, 2017). Facilitating the people with

objective, understandable and accurate information also acts as the ethical FM. Disclosing all

appropriate information whether it is negative or positive in complying with all the rules and the

regulation by governing the position of company provides an accurate picture to the users.

Wealth maximization- It means as the concept with regard to increasing value of the

business for the purpose of increasing value of shares that is held by their stockholders. This

stakeholders.

Managing the stakeholders refers to the process through which an individual could

monitor, organize and improves the relationships with that of the stakeholders. It includes

systematically determining the stakeholders, assessing their expectations and needs, planning and

executing several tasks for engaging them in the management of the company. The conflict of

the objective among the different stakeholders could be managed through several ways that are

as follows-

Setting objectives for achieving the financial goals- It means as setting the different

goals as per the term in order to achieve the finance related goals in effective manner. Setting up

short, long and the medium term goals is counted as an important task towards becoming as

financially secure (Armour and et.al., 2016). Making an annual financial plan provides an entity

with new opportunities in formally reviewing the goals, reviewing progress and updating it in

timely manner. In case the company never set the goals prior to developing plan, the period of

planning provides an opportunity in formulating it so that the firm could perform within the set

target or financial footing. Adequate financial & the retirement planning begins with the setting

goals with an inclusion of short, long and medium term objectives. The main short period goal

involves setting the budget and starting with an emergency fund. The medium term objectives

involves key insurances, however long run goals require emphasizing on the retirement.

Ethical FM- It is essential for the financial managers in handling the large sum of an

organization's money. It is important to have the code of ethics in the finance for living up with

those principles each day. The role of an ethics in FM is to protect, balance and preserves the

interest of stakeholders. The standards that are found in the ethical code involves acting with

integrity & honesty, avoiding the conflict of an interest in the professional relationships and

avoiding appearance of such type of conflicts (Holynskyy, 2017). Facilitating the people with

objective, understandable and accurate information also acts as the ethical FM. Disclosing all

appropriate information whether it is negative or positive in complying with all the rules and the

regulation by governing the position of company provides an accurate picture to the users.

Wealth maximization- It means as the concept with regard to increasing value of the

business for the purpose of increasing value of shares that is held by their stockholders. This

concept need management team of an enterprise in consistently searching for highest or

maximum returns on the funds that are invested in business, however mitigating any kind of

attached risk relating to loss. This called for detailed assessment of cash flows in association with

of the prospective investment and constant attention towards strategic direction of an entity.

Delivering long term sustainable growth- It is crucial for the companies to embrace

expectations of the society as the part of their business strategies is rising. Increasing the reliance

on the sustainable issues by the business is seen as critical towards growing interconnectedness

& future business value (Finkler, Smith and Calabrese, 2018). Financial management helps the

company in promoting sustainable type of development and the business practices. Allocating

the capital budget for the sustainable issues enhance the competitive edge of business.

3. Value of the MA techniques in controlling cost and in maximizing the shareholders value

MA plays a vital role in facilitating the information about the management in relation to

the affairs of an entity and to stakeholders. It relates to provision of using relevant information

for the decision-making, cost control, planning and evaluation of performance. It is counted as

primary role of MA to advise and inform the management regarding the latest position of an

enterprise (Ghasemi and et.al., 2016). MA are been assigned with managing the cost elements of

product among the responsibilities and aligns the cost with efficiency so that goals can be

accomplished effectively.

Marginal costing- This technique is been for fixing the selling price, selecting the best

sales related mix, optimum use of the scarce resources, in taking buy or make decisions, rejection

or acceptance of the bulk order. This is mainly based on fixed, variable, contribution and the

cost.

Budgetary control- This tool helps in future financial requirement are arranged &

estimated in accordance to orderly basis. It is been used for controlling financial performances of

the business enterprise. The business activities are been directed in the desired direction and

provides a guideline based on which the task would be performed along with ensuring full

control over the cost so that large amount of profits can be gained.

Cost Accounting- It is the technique of MA that provides an information relating to the

cost data as per product, department, process and branch wise. Such cost data are been compared

with the pre-determined one which in turn helps in deciding reasons responsible for difference

resulted between different types of costs.

maximum returns on the funds that are invested in business, however mitigating any kind of

attached risk relating to loss. This called for detailed assessment of cash flows in association with

of the prospective investment and constant attention towards strategic direction of an entity.

Delivering long term sustainable growth- It is crucial for the companies to embrace

expectations of the society as the part of their business strategies is rising. Increasing the reliance

on the sustainable issues by the business is seen as critical towards growing interconnectedness

& future business value (Finkler, Smith and Calabrese, 2018). Financial management helps the

company in promoting sustainable type of development and the business practices. Allocating

the capital budget for the sustainable issues enhance the competitive edge of business.

3. Value of the MA techniques in controlling cost and in maximizing the shareholders value

MA plays a vital role in facilitating the information about the management in relation to

the affairs of an entity and to stakeholders. It relates to provision of using relevant information

for the decision-making, cost control, planning and evaluation of performance. It is counted as

primary role of MA to advise and inform the management regarding the latest position of an

enterprise (Ghasemi and et.al., 2016). MA are been assigned with managing the cost elements of

product among the responsibilities and aligns the cost with efficiency so that goals can be

accomplished effectively.

Marginal costing- This technique is been for fixing the selling price, selecting the best

sales related mix, optimum use of the scarce resources, in taking buy or make decisions, rejection

or acceptance of the bulk order. This is mainly based on fixed, variable, contribution and the

cost.

Budgetary control- This tool helps in future financial requirement are arranged &

estimated in accordance to orderly basis. It is been used for controlling financial performances of

the business enterprise. The business activities are been directed in the desired direction and

provides a guideline based on which the task would be performed along with ensuring full

control over the cost so that large amount of profits can be gained.

Cost Accounting- It is the technique of MA that provides an information relating to the

cost data as per product, department, process and branch wise. Such cost data are been compared

with the pre-determined one which in turn helps in deciding reasons responsible for difference

resulted between different types of costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial planning- The main purpose of business entity is to maximize the profits. This

purpose is been attained by making sound and proper financial planning. Hence, the financial

planning is counted as the best tool for attaining the objectives of business.

Cost volume profit analysis- It is been used for determining the manner in which changes

in the volume and cost impacts operating income of the firm (Taylor and Scapens, 2016). It

requires that all cost of an entity involving manufacturing, administrative and the selling cost is

been determined as fixed or a variable cost. It looks at effects of the differing activity levels on

financial results of business so that adequate decisions could be made for increasing profits and

making decisions.

Financial statement assessment- P&L account and the balance sheet are considered as

financial statements. Such reports are been assessed for the different period that helps the

management in knowing growth rate of business entity. This assessment is been done through

the comparative final reports, ratio analysis and the common size statements.

These tools helps the company in controlling the cost and leads to increase in the value of

stakeholders which leads to achieving higher success and growth.

4.Techniques for fraud detection and prevention and approaches for ethical decision making.

Though the focus of the company is towards maximising the profits and reducing costs it

has to be active regarding the internal activities. Often well performing companies lose their

focus over the internal activities and operations will taking the decisions regarding growth

prospects. Companies are required to ensure that the processes are being followed are free from

frauds and errors. There are various tools and techniques for fraud detection and prevention

which are used by the organisation.

Internal Controls

These are the rules, procedures, mechanism implemented by the company for ensuring

integrity of the financial & accounting information, promoting accountability and for preventing

frauds. Internal controls are used by the enterprises at the various level for ensuring that the

processes followed by the organisation are accurate and are flowing in the set direction. The

controls are set by the management over areas that are most prone to the errors or frauds. These

internal controls ensure that the employees are working efficiently and achieving the set target

within the defined time frames (Lichtenberg, 2016). The controls of the business helps in

identifying the frauds if any taking place in the business by employee or management.

purpose is been attained by making sound and proper financial planning. Hence, the financial

planning is counted as the best tool for attaining the objectives of business.

Cost volume profit analysis- It is been used for determining the manner in which changes

in the volume and cost impacts operating income of the firm (Taylor and Scapens, 2016). It

requires that all cost of an entity involving manufacturing, administrative and the selling cost is

been determined as fixed or a variable cost. It looks at effects of the differing activity levels on

financial results of business so that adequate decisions could be made for increasing profits and

making decisions.

Financial statement assessment- P&L account and the balance sheet are considered as

financial statements. Such reports are been assessed for the different period that helps the

management in knowing growth rate of business entity. This assessment is been done through

the comparative final reports, ratio analysis and the common size statements.

These tools helps the company in controlling the cost and leads to increase in the value of

stakeholders which leads to achieving higher success and growth.

4.Techniques for fraud detection and prevention and approaches for ethical decision making.

Though the focus of the company is towards maximising the profits and reducing costs it

has to be active regarding the internal activities. Often well performing companies lose their

focus over the internal activities and operations will taking the decisions regarding growth

prospects. Companies are required to ensure that the processes are being followed are free from

frauds and errors. There are various tools and techniques for fraud detection and prevention

which are used by the organisation.

Internal Controls

These are the rules, procedures, mechanism implemented by the company for ensuring

integrity of the financial & accounting information, promoting accountability and for preventing

frauds. Internal controls are used by the enterprises at the various level for ensuring that the

processes followed by the organisation are accurate and are flowing in the set direction. The

controls are set by the management over areas that are most prone to the errors or frauds. These

internal controls ensure that the employees are working efficiently and achieving the set target

within the defined time frames (Lichtenberg, 2016). The controls of the business helps in

identifying the frauds if any taking place in the business by employee or management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

Auditing refers to the process of inspecting and examining the financial record of the

entity for ensuring that financial statements give true and fair view of the financial position.

Audit is carried out by auditing professionals for ensuring that the financial records are in

accordance with the set accounting standards and reporting frameworks. Audit is to be carried

out by every enterprise whose turnover goes beyond the threshold limit. Auditors inspect the

financial records of the firm to identify that all the transactions carried out by the organisation

are properly recorded and their effect is reflected in the financial statements. They also identify

any errors or omission taking place in the financial records to identify the frauds. Auditors have

the main responsibility to ensure that the financial records are free from omissions and

misstatements. They identify the fraud if any carried out within organisation by auditing and

reporting to the management and statutory authorities. Auditing helps in detecting as well as

preventing the frauds in an organisation.

Ethical Consideration in decision making

Number of stakeholders are associated with the financial statements published by the

enterprise. Business should follow ethical code of conduct in its operation. Ethical code should

be followed from top to bottom. Management should establish ethical codes to be followed by

the organisation. They should protect the rights of the employees and ensure that organisational

goals are achieved also aligning the employee goals (Finke, Hower and Huston, 2017). Financial

decisions are required to be taken by the management for growth ensuring that the interest of any

particular stakeholder group is not affected or deprived. In preparing the financial statement

management should ensure that the financial statements are free from errors and misstatement

and reflects the actual performance and position of the company. It should not be manipulated

for reflecting false position for gaining advantage.

5. Reflection

I am having deep interest in the financial sector and so with the management of finance.

This research has helped in learning about the various approaches of decision making such as

function and non functional. These approaches should be used by the organisation as per the

circumstances. Management for making various critical decisions use decision tree and other

tools for analysing the pros and cons of various options and choosing the best for entity. I have

learned that stakeholders are important parties interested in the success or failure of the entity.

Auditing refers to the process of inspecting and examining the financial record of the

entity for ensuring that financial statements give true and fair view of the financial position.

Audit is carried out by auditing professionals for ensuring that the financial records are in

accordance with the set accounting standards and reporting frameworks. Audit is to be carried

out by every enterprise whose turnover goes beyond the threshold limit. Auditors inspect the

financial records of the firm to identify that all the transactions carried out by the organisation

are properly recorded and their effect is reflected in the financial statements. They also identify

any errors or omission taking place in the financial records to identify the frauds. Auditors have

the main responsibility to ensure that the financial records are free from omissions and

misstatements. They identify the fraud if any carried out within organisation by auditing and

reporting to the management and statutory authorities. Auditing helps in detecting as well as

preventing the frauds in an organisation.

Ethical Consideration in decision making

Number of stakeholders are associated with the financial statements published by the

enterprise. Business should follow ethical code of conduct in its operation. Ethical code should

be followed from top to bottom. Management should establish ethical codes to be followed by

the organisation. They should protect the rights of the employees and ensure that organisational

goals are achieved also aligning the employee goals (Finke, Hower and Huston, 2017). Financial

decisions are required to be taken by the management for growth ensuring that the interest of any

particular stakeholder group is not affected or deprived. In preparing the financial statement

management should ensure that the financial statements are free from errors and misstatement

and reflects the actual performance and position of the company. It should not be manipulated

for reflecting false position for gaining advantage.

5. Reflection

I am having deep interest in the financial sector and so with the management of finance.

This research has helped in learning about the various approaches of decision making such as

function and non functional. These approaches should be used by the organisation as per the

circumstances. Management for making various critical decisions use decision tree and other

tools for analysing the pros and cons of various options and choosing the best for entity. I have

learned that stakeholders are important parties interested in the success or failure of the entity.

Decisions taken by the management have impact over the stakeholders of company and therefore

required to ensure that decisions are taken considering the stakeholder interest. They have to

reduce the conflicts between stakeholders interests by appropriate planning and strategies.

Management accounting provides different tools and techniques for controlling the costs and

expenses of the business. It provides the management with the most effective techniques for

reducing the cost of the organisation and ensuring that the business is making most effective

utilisation of the resources for generating maximum benefits. Company along with doing

business is also required to have control over the internal functions for identifying and

preventing the frauds or omissions as they could hardly hit the financial standing of the

company.

Scenario B

1. Financial ratios analysis of J Sainsbury PLC for the year 2020, 2019 & 2018

Ratio analysis: It is a quantitative approach for the purpose of gain idea about the

performance and positioning of the company's liquidity, efficiency, profitability and other

factors.

J Sainsbury PLC

Particulars Formulas 2020 2019 2018

Liquidity ratio

Current assets 7582 7550 7866

Current liabilities 12047 11849 10302

Inventory 1732 1929 1810

Current ratio

Current Asset/ Current

liabilities 0.63 0.64 0.76

Quick ratio

Quick Assets/ Current

liabilities 0.49 0.47 0.59

Profitability ratio

Capital employed 16119 16431 11744

Operating profit 1057 606 547

Shareholders Equity 7525 7534 6902

Net profit after tax 129 168 291

Sales 28993 29007 28459

required to ensure that decisions are taken considering the stakeholder interest. They have to

reduce the conflicts between stakeholders interests by appropriate planning and strategies.

Management accounting provides different tools and techniques for controlling the costs and

expenses of the business. It provides the management with the most effective techniques for

reducing the cost of the organisation and ensuring that the business is making most effective

utilisation of the resources for generating maximum benefits. Company along with doing

business is also required to have control over the internal functions for identifying and

preventing the frauds or omissions as they could hardly hit the financial standing of the

company.

Scenario B

1. Financial ratios analysis of J Sainsbury PLC for the year 2020, 2019 & 2018

Ratio analysis: It is a quantitative approach for the purpose of gain idea about the

performance and positioning of the company's liquidity, efficiency, profitability and other

factors.

J Sainsbury PLC

Particulars Formulas 2020 2019 2018

Liquidity ratio

Current assets 7582 7550 7866

Current liabilities 12047 11849 10302

Inventory 1732 1929 1810

Current ratio

Current Asset/ Current

liabilities 0.63 0.64 0.76

Quick ratio

Quick Assets/ Current

liabilities 0.49 0.47 0.59

Profitability ratio

Capital employed 16119 16431 11744

Operating profit 1057 606 547

Shareholders Equity 7525 7534 6902

Net profit after tax 129 168 291

Sales 28993 29007 28459

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on capital employed

Operating

profit/capital

employed 6.6% 3.7% 4.7%

Return on equity

Net income/

Shareholder's equity 1.7% 2.2% 4.2%

Net profit margin Net profit/ sales 0.4% 0.6% 1.0%

Efficiency ratio

Net sales 28993 29007 28459

Total assets 28166 28280 22046

Inventory 1732 1929 1810

Cost of sales 26799 26807 26593

Accounts receivables 4672 4268 4104

Asset turnover ratio Net sales/total assets 1.03 1.03 1.29

Inventory turnover ratio

Cost of

sales/inventory 15.47 13.90 14.69

Accounts receivable turnover

ratio

Net sales/accounts

receivables 6.21 6.80 6.93

Solvency ratio

Total debt 20641 20746 15144

Total Equity 7525 7534 6902

Debt equity ratio

Total debt/ total

equity 2.74 2.75 2.19

Analysis and interpretation:

Liquidity ratio

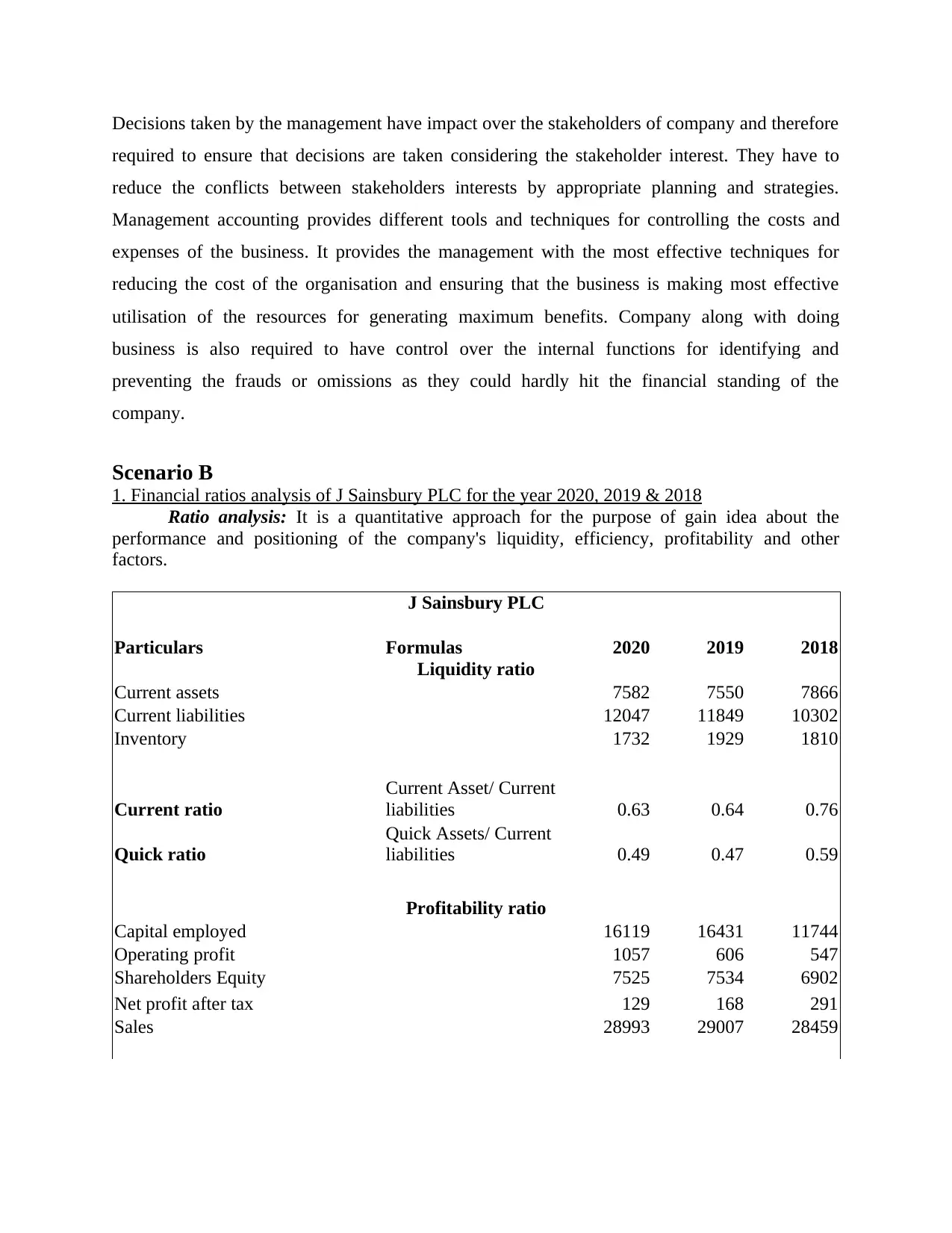

The below graph shows the liquidity position of the company. The current ratio of the

company is very low and is also declining as it has reduced from 0.76 times to 0.63 times. This

reflects that the company is not effectively managing its current assets and there is large amount

of current liabilities (Bragg, 2018). Therefore, company is required to take steps like increasing

its current assets or reducing its short term liabilities for improving its position.

Operating

profit/capital

employed 6.6% 3.7% 4.7%

Return on equity

Net income/

Shareholder's equity 1.7% 2.2% 4.2%

Net profit margin Net profit/ sales 0.4% 0.6% 1.0%

Efficiency ratio

Net sales 28993 29007 28459

Total assets 28166 28280 22046

Inventory 1732 1929 1810

Cost of sales 26799 26807 26593

Accounts receivables 4672 4268 4104

Asset turnover ratio Net sales/total assets 1.03 1.03 1.29

Inventory turnover ratio

Cost of

sales/inventory 15.47 13.90 14.69

Accounts receivable turnover

ratio

Net sales/accounts

receivables 6.21 6.80 6.93

Solvency ratio

Total debt 20641 20746 15144

Total Equity 7525 7534 6902

Debt equity ratio

Total debt/ total

equity 2.74 2.75 2.19

Analysis and interpretation:

Liquidity ratio

The below graph shows the liquidity position of the company. The current ratio of the

company is very low and is also declining as it has reduced from 0.76 times to 0.63 times. This

reflects that the company is not effectively managing its current assets and there is large amount

of current liabilities (Bragg, 2018). Therefore, company is required to take steps like increasing

its current assets or reducing its short term liabilities for improving its position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 2019 2020

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Current ratio

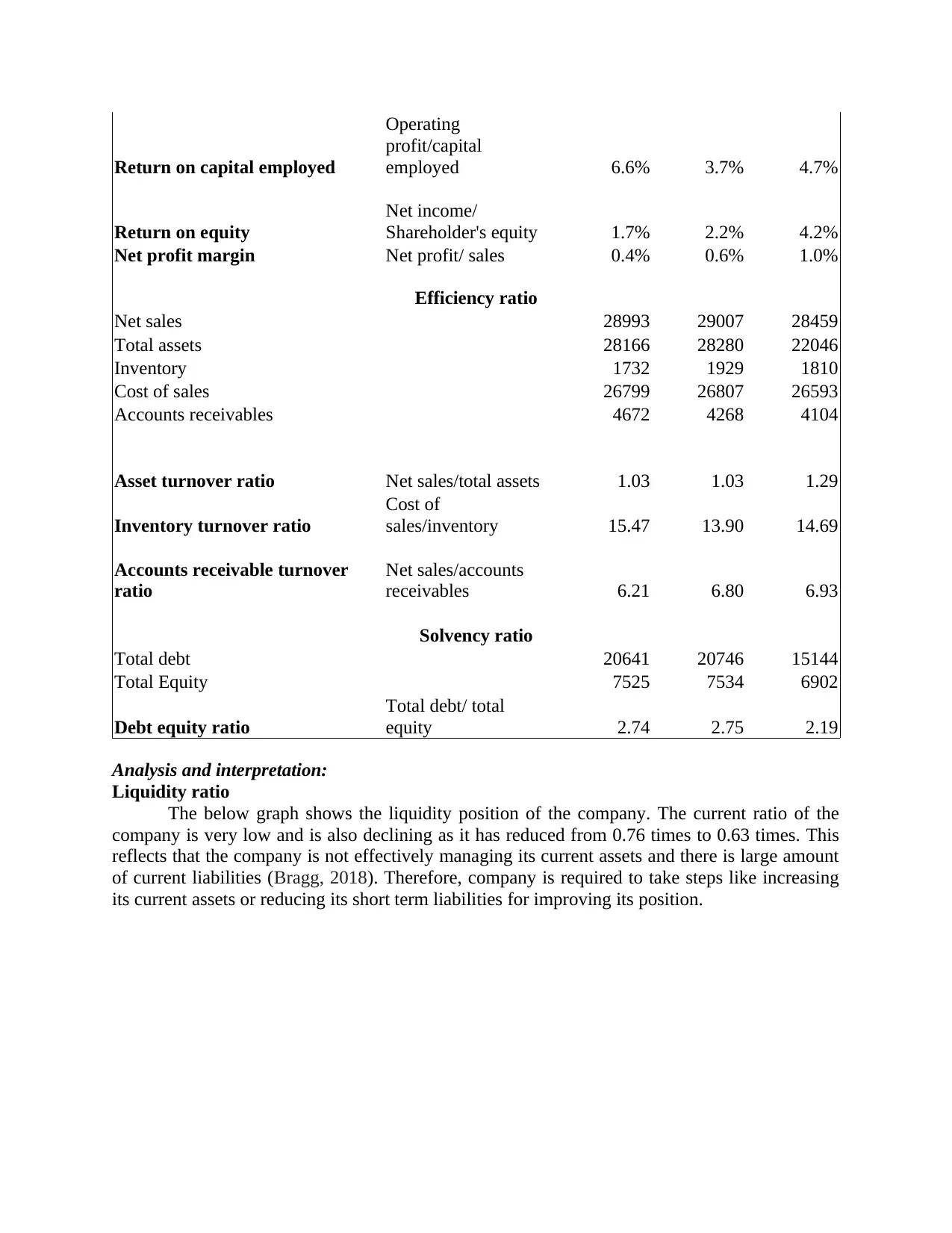

The graph below illustrates the quick ratio of Sainsbury which is extremely low which

indicates that the company has invested more in its inventory rather than other assets. Thus, it is

the risky situation for the company. So, the company is required to work on increasing its current

assets.

2018 2019 2020

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio

Profitability ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Current ratio

The graph below illustrates the quick ratio of Sainsbury which is extremely low which

indicates that the company has invested more in its inventory rather than other assets. Thus, it is

the risky situation for the company. So, the company is required to work on increasing its current

assets.

2018 2019 2020

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio

Profitability ratio

2018 2019 2020

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

Return on capital employed

2018 2019 2020

0

0.01

0.01

0.02

0.02

0.03

0.03

0.04

0.04

0.05

Return on equity

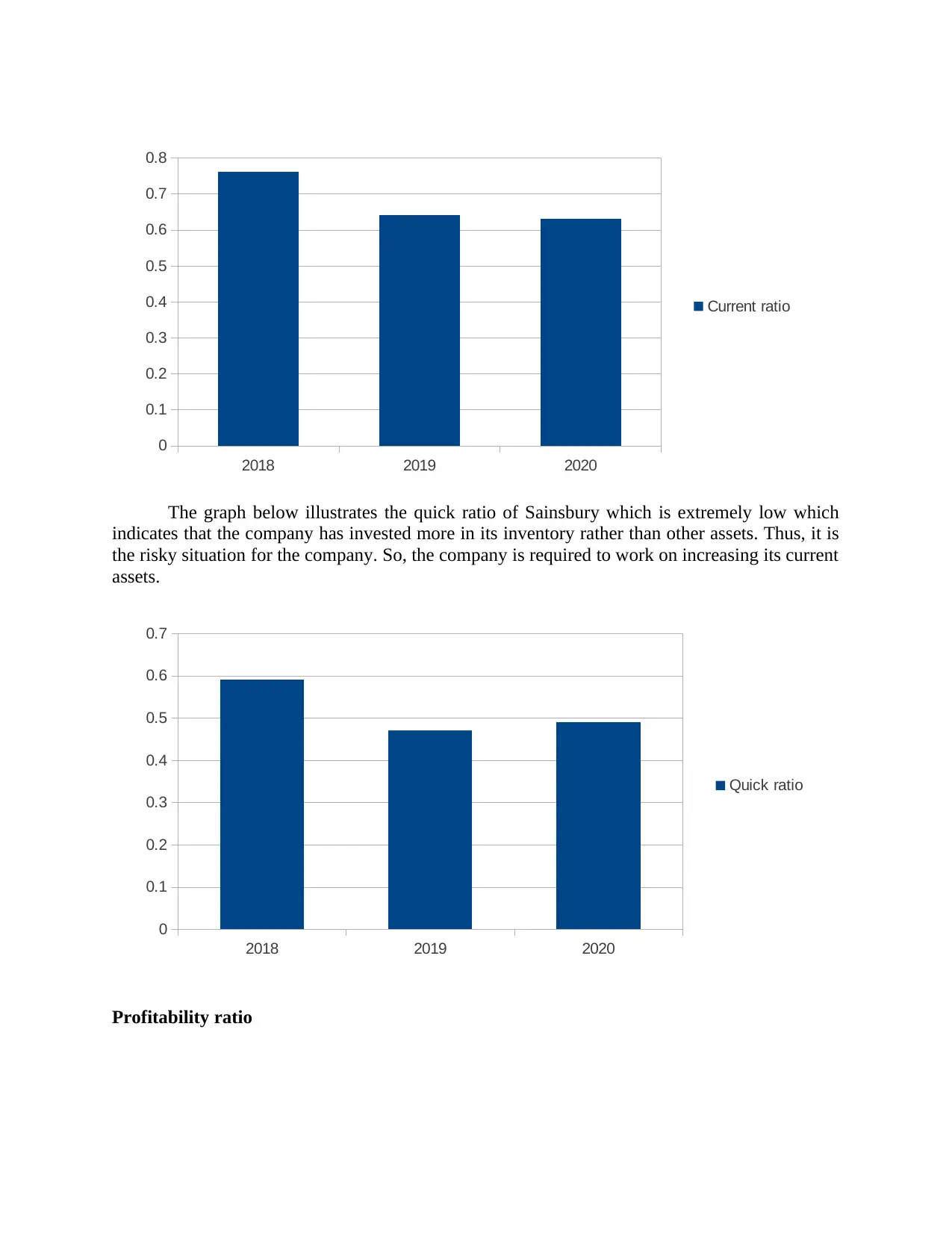

The return on capital employed of the company has increased over the three years from

4.7% to 6.6% in 2020 (Grimm and Blazovich, 2016). Also, the return on equity has reduced to

1.7% in the year 2020. This means that the organization is effectively utilizing its capital

employed but it is not effective in using its shareholders fund.

The below graph is about the net profit margin of the company which has shown a

decreased from 1% to 0.4% which is a point of concern for the organization. Thus, company

should make efforts to decrease its cost or increase its revenue.

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

Return on capital employed

2018 2019 2020

0

0.01

0.01

0.02

0.02

0.03

0.03

0.04

0.04

0.05

Return on equity

The return on capital employed of the company has increased over the three years from

4.7% to 6.6% in 2020 (Grimm and Blazovich, 2016). Also, the return on equity has reduced to

1.7% in the year 2020. This means that the organization is effectively utilizing its capital

employed but it is not effective in using its shareholders fund.

The below graph is about the net profit margin of the company which has shown a

decreased from 1% to 0.4% which is a point of concern for the organization. Thus, company

should make efforts to decrease its cost or increase its revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.