A Report on Managing Financial Resources and Decisions at Sainsbury's

VerifiedAdded on 2020/01/23

|20

|4580

|70

Report

AI Summary

This report provides a comprehensive analysis of Sainsbury's financial resource management and decision-making processes. It explores various sources of funds, including proprietor's funds, bank loans, hire purchase agreements, and retained earnings, evaluating their legal and financial implications. The report delves into financial planning, budgeting, and pricing techniques, examining the roles and interests of stakeholders such as shareholders, employees, creditors, and lenders. It analyzes the impact of financial decisions on the balance sheet and presents a cash flow forecast, identifying potential shortfalls and strategies for improvement. Furthermore, the report includes cost analysis, break-even point calculations, and a discussion of fixed and variable costs, providing a detailed overview of Sainsbury's financial strategies and performance.

Managing Financial Resource and Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.........................................................................................................................................4

TASK 1..........................................................................................................................................................4

1.1...............................................................................................................................................................4

1.2...............................................................................................................................................................5

1.3...............................................................................................................................................................6

TASK 2..........................................................................................................................................................7

2.1...............................................................................................................................................................7

2.2...............................................................................................................................................................7

2.3...............................................................................................................................................................8

2.4...............................................................................................................................................................8

TASK 3..........................................................................................................................................................9

3.1...............................................................................................................................................................9

3.2.............................................................................................................................................................10

3.3.............................................................................................................................................................11

TASK 4........................................................................................................................................................13

4.1.............................................................................................................................................................13

4.2.............................................................................................................................................................14

4.3.............................................................................................................................................................14

CONCLUSION............................................................................................................................................16

REFERENCES............................................................................................................................................17

INTRODUCTION.........................................................................................................................................4

TASK 1..........................................................................................................................................................4

1.1...............................................................................................................................................................4

1.2...............................................................................................................................................................5

1.3...............................................................................................................................................................6

TASK 2..........................................................................................................................................................7

2.1...............................................................................................................................................................7

2.2...............................................................................................................................................................7

2.3...............................................................................................................................................................8

2.4...............................................................................................................................................................8

TASK 3..........................................................................................................................................................9

3.1...............................................................................................................................................................9

3.2.............................................................................................................................................................10

3.3.............................................................................................................................................................11

TASK 4........................................................................................................................................................13

4.1.............................................................................................................................................................13

4.2.............................................................................................................................................................14

4.3.............................................................................................................................................................14

CONCLUSION............................................................................................................................................16

REFERENCES............................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

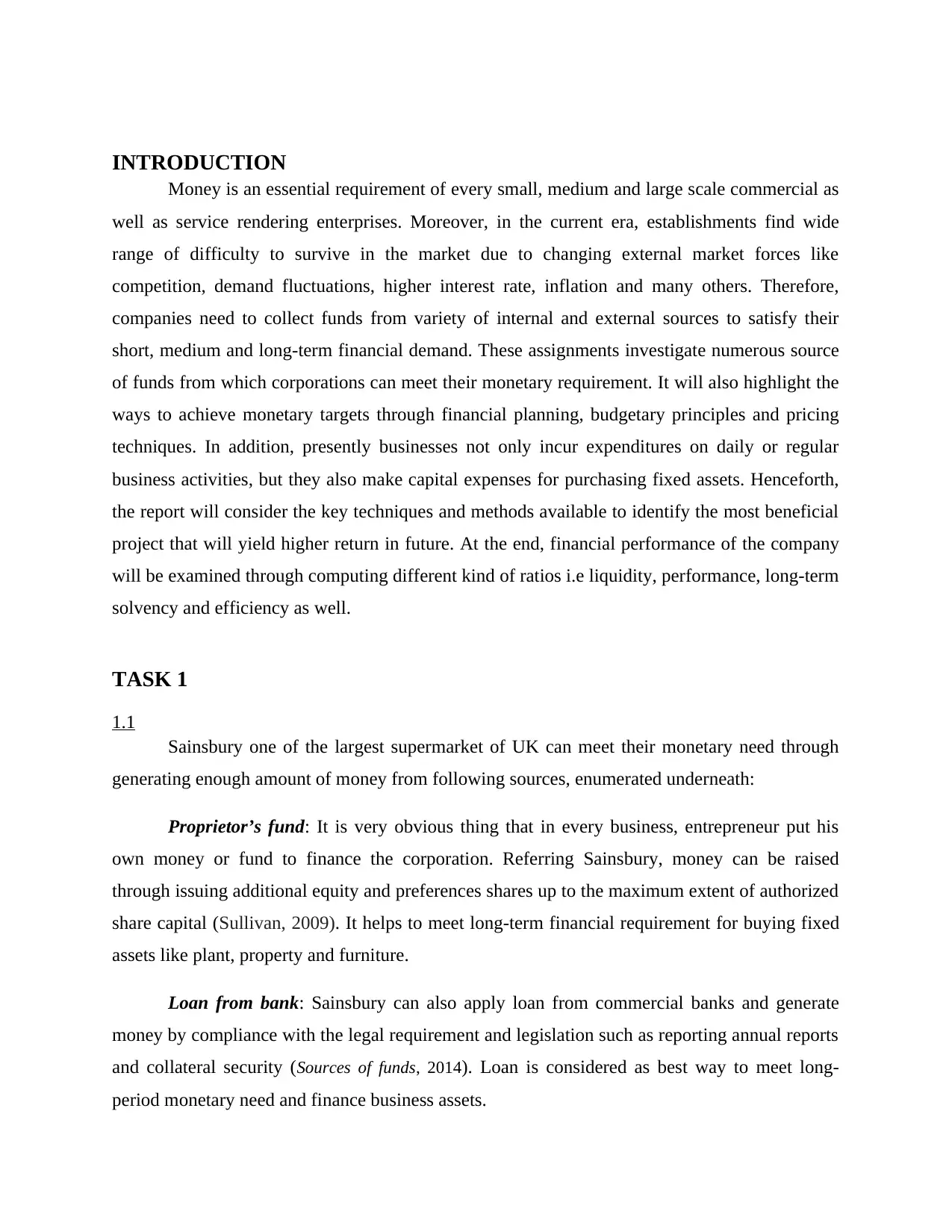

INTRODUCTION

Money is an essential requirement of every small, medium and large scale commercial as

well as service rendering enterprises. Moreover, in the current era, establishments find wide

range of difficulty to survive in the market due to changing external market forces like

competition, demand fluctuations, higher interest rate, inflation and many others. Therefore,

companies need to collect funds from variety of internal and external sources to satisfy their

short, medium and long-term financial demand. These assignments investigate numerous source

of funds from which corporations can meet their monetary requirement. It will also highlight the

ways to achieve monetary targets through financial planning, budgetary principles and pricing

techniques. In addition, presently businesses not only incur expenditures on daily or regular

business activities, but they also make capital expenses for purchasing fixed assets. Henceforth,

the report will consider the key techniques and methods available to identify the most beneficial

project that will yield higher return in future. At the end, financial performance of the company

will be examined through computing different kind of ratios i.e liquidity, performance, long-term

solvency and efficiency as well.

TASK 1

1.1

Sainsbury one of the largest supermarket of UK can meet their monetary need through

generating enough amount of money from following sources, enumerated underneath:

Proprietor’s fund: It is very obvious thing that in every business, entrepreneur put his

own money or fund to finance the corporation. Referring Sainsbury, money can be raised

through issuing additional equity and preferences shares up to the maximum extent of authorized

share capital (Sullivan, 2009). It helps to meet long-term financial requirement for buying fixed

assets like plant, property and furniture.

Loan from bank: Sainsbury can also apply loan from commercial banks and generate

money by compliance with the legal requirement and legislation such as reporting annual reports

and collateral security (Sources of funds, 2014). Loan is considered as best way to meet long-

period monetary need and finance business assets.

Money is an essential requirement of every small, medium and large scale commercial as

well as service rendering enterprises. Moreover, in the current era, establishments find wide

range of difficulty to survive in the market due to changing external market forces like

competition, demand fluctuations, higher interest rate, inflation and many others. Therefore,

companies need to collect funds from variety of internal and external sources to satisfy their

short, medium and long-term financial demand. These assignments investigate numerous source

of funds from which corporations can meet their monetary requirement. It will also highlight the

ways to achieve monetary targets through financial planning, budgetary principles and pricing

techniques. In addition, presently businesses not only incur expenditures on daily or regular

business activities, but they also make capital expenses for purchasing fixed assets. Henceforth,

the report will consider the key techniques and methods available to identify the most beneficial

project that will yield higher return in future. At the end, financial performance of the company

will be examined through computing different kind of ratios i.e liquidity, performance, long-term

solvency and efficiency as well.

TASK 1

1.1

Sainsbury one of the largest supermarket of UK can meet their monetary need through

generating enough amount of money from following sources, enumerated underneath:

Proprietor’s fund: It is very obvious thing that in every business, entrepreneur put his

own money or fund to finance the corporation. Referring Sainsbury, money can be raised

through issuing additional equity and preferences shares up to the maximum extent of authorized

share capital (Sullivan, 2009). It helps to meet long-term financial requirement for buying fixed

assets like plant, property and furniture.

Loan from bank: Sainsbury can also apply loan from commercial banks and generate

money by compliance with the legal requirement and legislation such as reporting annual reports

and collateral security (Sources of funds, 2014). Loan is considered as best way to meet long-

period monetary need and finance business assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hire purchase: It is a contract or agreement undertaken between assets vendor and buyer,

in which, owner provide right to the purchaser to utilize assets by making regular installment

payments with interest charges (Broadbent and Cullen, 2012). However, legally property right

will be transferred at the time of payment of final installment.

Retained earnings: The residual proportion of Sainsbury’s net earnings after paying

dividend to the shareholders is called retained earnings or profit (De Wit,2016). Company can

invest back their residual return or yield in the business and thereby fulfill their monetary

requirement.

1.2

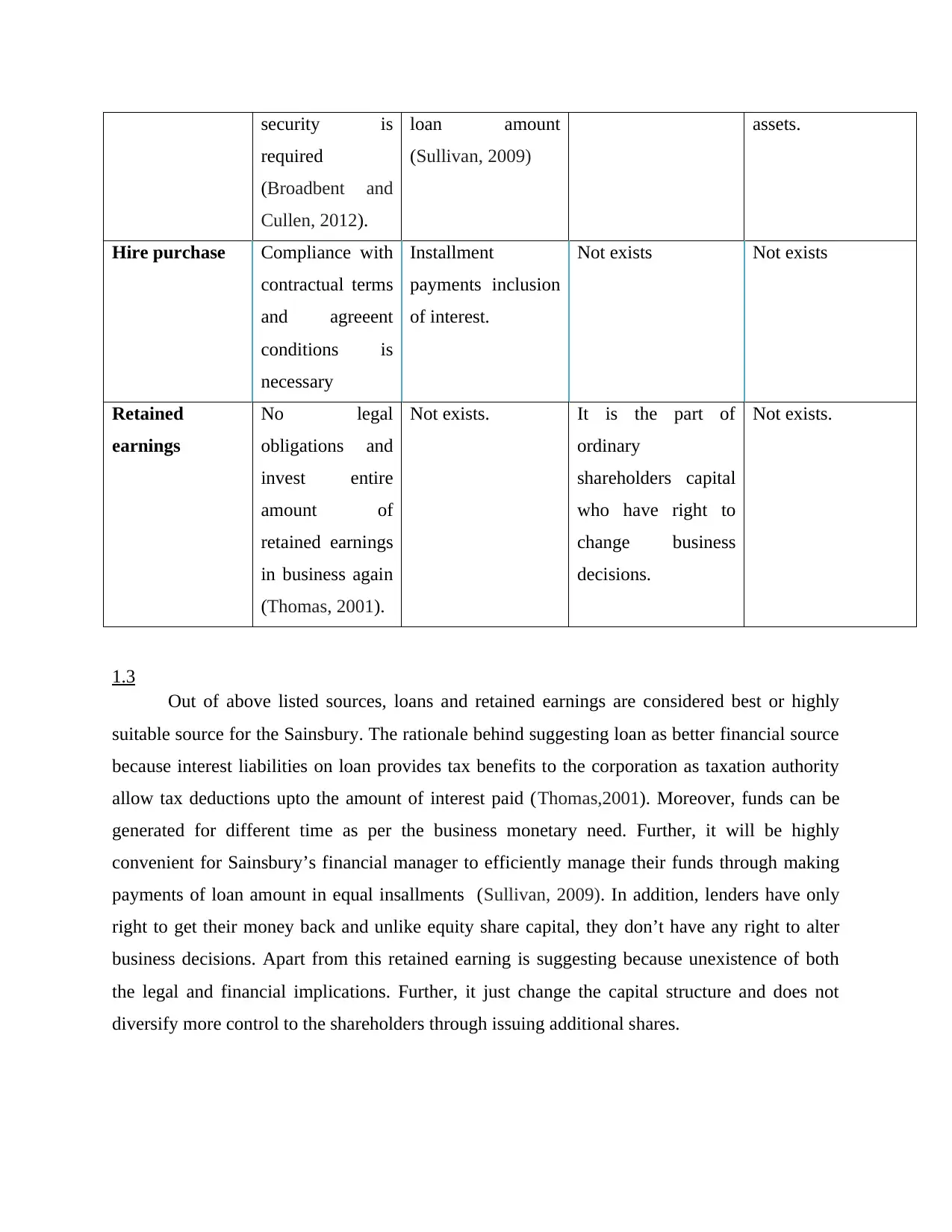

Source of funds Legal Financial Control dilution Bankruptcy

Properietr or’s

fund

Shares can be

issued to the

maximum extent

of authorized

share capital

(Thomas, 2001).

Moreover,

adherence and

compliance with

the rules and

regulations of

Security

Exchange

Commission

(SEC) is

required.

On prefernce share

capital, Sainsbury

is liable to pay

fixed rate of

dividend whereas

on equity share

capital, it need to

pay a proposed rate

of dividend from

the net earnings

(De Wit,2016).

Equity share holders

have power to vote,

henceforth, they

have right to control

operations and make

decisions, wherease

preference

shareholders are not

entitled to make

business decisions

(Thomas, 2001).

Not exist but still

preference

shareholders will be

repaied earlier

before repayment of

capital to ordinary

share holders.

Bank loan Adherence to the

legal rules and

regulations like

collateral

Interest needs to be

paid either on

principle amount or

residual or balanced

Not exist. Loan will be repaid

even at the time of

insolvency by

disposal of business

in which, owner provide right to the purchaser to utilize assets by making regular installment

payments with interest charges (Broadbent and Cullen, 2012). However, legally property right

will be transferred at the time of payment of final installment.

Retained earnings: The residual proportion of Sainsbury’s net earnings after paying

dividend to the shareholders is called retained earnings or profit (De Wit,2016). Company can

invest back their residual return or yield in the business and thereby fulfill their monetary

requirement.

1.2

Source of funds Legal Financial Control dilution Bankruptcy

Properietr or’s

fund

Shares can be

issued to the

maximum extent

of authorized

share capital

(Thomas, 2001).

Moreover,

adherence and

compliance with

the rules and

regulations of

Security

Exchange

Commission

(SEC) is

required.

On prefernce share

capital, Sainsbury

is liable to pay

fixed rate of

dividend whereas

on equity share

capital, it need to

pay a proposed rate

of dividend from

the net earnings

(De Wit,2016).

Equity share holders

have power to vote,

henceforth, they

have right to control

operations and make

decisions, wherease

preference

shareholders are not

entitled to make

business decisions

(Thomas, 2001).

Not exist but still

preference

shareholders will be

repaied earlier

before repayment of

capital to ordinary

share holders.

Bank loan Adherence to the

legal rules and

regulations like

collateral

Interest needs to be

paid either on

principle amount or

residual or balanced

Not exist. Loan will be repaid

even at the time of

insolvency by

disposal of business

security is

required

(Broadbent and

Cullen, 2012).

loan amount

(Sullivan, 2009)

assets.

Hire purchase Compliance with

contractual terms

and agreeent

conditions is

necessary

Installment

payments inclusion

of interest.

Not exists Not exists

Retained

earnings

No legal

obligations and

invest entire

amount of

retained earnings

in business again

(Thomas, 2001).

Not exists. It is the part of

ordinary

shareholders capital

who have right to

change business

decisions.

Not exists.

1.3

Out of above listed sources, loans and retained earnings are considered best or highly

suitable source for the Sainsbury. The rationale behind suggesting loan as better financial source

because interest liabilities on loan provides tax benefits to the corporation as taxation authority

allow tax deductions upto the amount of interest paid (Thomas,2001). Moreover, funds can be

generated for different time as per the business monetary need. Further, it will be highly

convenient for Sainsbury’s financial manager to efficiently manage their funds through making

payments of loan amount in equal insallments (Sullivan, 2009). In addition, lenders have only

right to get their money back and unlike equity share capital, they don’t have any right to alter

business decisions. Apart from this retained earning is suggesting because unexistence of both

the legal and financial implications. Further, it just change the capital structure and does not

diversify more control to the shareholders through issuing additional shares.

required

(Broadbent and

Cullen, 2012).

loan amount

(Sullivan, 2009)

assets.

Hire purchase Compliance with

contractual terms

and agreeent

conditions is

necessary

Installment

payments inclusion

of interest.

Not exists Not exists

Retained

earnings

No legal

obligations and

invest entire

amount of

retained earnings

in business again

(Thomas, 2001).

Not exists. It is the part of

ordinary

shareholders capital

who have right to

change business

decisions.

Not exists.

1.3

Out of above listed sources, loans and retained earnings are considered best or highly

suitable source for the Sainsbury. The rationale behind suggesting loan as better financial source

because interest liabilities on loan provides tax benefits to the corporation as taxation authority

allow tax deductions upto the amount of interest paid (Thomas,2001). Moreover, funds can be

generated for different time as per the business monetary need. Further, it will be highly

convenient for Sainsbury’s financial manager to efficiently manage their funds through making

payments of loan amount in equal insallments (Sullivan, 2009). In addition, lenders have only

right to get their money back and unlike equity share capital, they don’t have any right to alter

business decisions. Apart from this retained earning is suggesting because unexistence of both

the legal and financial implications. Further, it just change the capital structure and does not

diversify more control to the shareholders through issuing additional shares.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2.1

Interest cost: As discussed earlier, that there is a financial implication exists on loan

regards to interest payment. Henceforth, it is the cost of bank loan, higher the interest rate rises

the burden of debt on business enterprise or vice-versa (Malik, Field and Gorwood, 2016).

Moreover, vendor of the assets also charge a fixed rate of interest in hire purchase agreement, but

still, both the interest obligation provides tax benefit to the business.

Dividend: If Sainsbury will raise monetary resources through issuance of either equity or

preference share capital, then it will need to pay dividend to the shareholders (De Wit,2016). In

such respect, rate of dividend on preference share capital is fixed whereas on equity share

capital, Sainsbury is not liable to pay fixed rate of dividend annually.

2.2

Sainsbury’s financial manager is responsible to gather sufficient quantum of money,

procurement and its efffective utilization in business activities through making effective and

strong financial plan (Sabri and et.al., 2015).

Significance of monetary planning:

Gathering enough amount of monetary resources from variety of financial sources such

as share capital, debt, lease, hire purchase, retained earnings etc.

Maximum and optimum utilization of funds in the business operations.

Maintain surplus of cash through creating better balance between sources of cash and its

disposal (Bir, 2016).

Overcoming shortcomings and shortfall of funds through generating higher turnover and

other revenues.

Combat threats due to external market volatility and fluctuations such as sudden increase

in price, reduction in consumer demand, introduction of new product in market by rival

firms and others (Revell, 2016).

Ensure growth and development by running a successful business without any financial

difficulties and problems.

2.1

Interest cost: As discussed earlier, that there is a financial implication exists on loan

regards to interest payment. Henceforth, it is the cost of bank loan, higher the interest rate rises

the burden of debt on business enterprise or vice-versa (Malik, Field and Gorwood, 2016).

Moreover, vendor of the assets also charge a fixed rate of interest in hire purchase agreement, but

still, both the interest obligation provides tax benefit to the business.

Dividend: If Sainsbury will raise monetary resources through issuance of either equity or

preference share capital, then it will need to pay dividend to the shareholders (De Wit,2016). In

such respect, rate of dividend on preference share capital is fixed whereas on equity share

capital, Sainsbury is not liable to pay fixed rate of dividend annually.

2.2

Sainsbury’s financial manager is responsible to gather sufficient quantum of money,

procurement and its efffective utilization in business activities through making effective and

strong financial plan (Sabri and et.al., 2015).

Significance of monetary planning:

Gathering enough amount of monetary resources from variety of financial sources such

as share capital, debt, lease, hire purchase, retained earnings etc.

Maximum and optimum utilization of funds in the business operations.

Maintain surplus of cash through creating better balance between sources of cash and its

disposal (Bir, 2016).

Overcoming shortcomings and shortfall of funds through generating higher turnover and

other revenues.

Combat threats due to external market volatility and fluctuations such as sudden increase

in price, reduction in consumer demand, introduction of new product in market by rival

firms and others (Revell, 2016).

Ensure growth and development by running a successful business without any financial

difficulties and problems.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3

Shareholders: They are interested in business growth, progress and improved

performance. Before investing their own money, investors examine Sainsbury’s profitability,

dividend payment, movement in share’s market price and financial risk as well.

Employees: Sainsbury’s personnel are responsible for giving their best contribution to

deliver quality goods and services as per their need. They expect better working condition, good

salary, rewards and staff welfare activities in return for their valuable and exceptional efforts to

meet business goals (Malik, Field and Gorwood, 2016).

Creditors: They supply material and other resources to Sainsbury for a fixed credit

period. In order to get payment timely, they inquire about company’s liquidity position, net

profitability, cash flow generating capacity and sufficiency of nearby resources to pay short-term

liability (Speybroeck and et.al., 2015).

Government: They are interested in getting timely tax receipts on Sainsbury’s net

operating profit after interest payment. Moreover, they assure that all the establishments are

conducting operations ethically or legally and in consumer interest (Bir, 2016). Further,

compliance and adherence to legislations and governmental rules is also necessary for the

company,

Lender: They need collateral security and examine Sainsbury’s annual accounting

reports to assess profitability, net cash position, debt-service coverage ratio, interest bearing

ability and financial burden (Sabri and et.al., 2015).. They provide long-term fund if they are

confident that about their fund security.

2.4

Balance sheet represents both the preference and ordinary share capital in the liability

side of balance sheet. Collection of fund through share capital increase Sainsbury’s cash or bank

balance. However, cost that is dividend is deducted from net profit after interest and taxes to

determined retained or residual earnings, at the same time, cash balance will be reduced to the

extent of dividend payment (Huang, Ritter and Zhang, 2016). Contrary to this, loan amount is

reported under the non-current liability head and also improve total cash position. However, on

the other side, interest payment is considered as operational spending hence results in less net

Shareholders: They are interested in business growth, progress and improved

performance. Before investing their own money, investors examine Sainsbury’s profitability,

dividend payment, movement in share’s market price and financial risk as well.

Employees: Sainsbury’s personnel are responsible for giving their best contribution to

deliver quality goods and services as per their need. They expect better working condition, good

salary, rewards and staff welfare activities in return for their valuable and exceptional efforts to

meet business goals (Malik, Field and Gorwood, 2016).

Creditors: They supply material and other resources to Sainsbury for a fixed credit

period. In order to get payment timely, they inquire about company’s liquidity position, net

profitability, cash flow generating capacity and sufficiency of nearby resources to pay short-term

liability (Speybroeck and et.al., 2015).

Government: They are interested in getting timely tax receipts on Sainsbury’s net

operating profit after interest payment. Moreover, they assure that all the establishments are

conducting operations ethically or legally and in consumer interest (Bir, 2016). Further,

compliance and adherence to legislations and governmental rules is also necessary for the

company,

Lender: They need collateral security and examine Sainsbury’s annual accounting

reports to assess profitability, net cash position, debt-service coverage ratio, interest bearing

ability and financial burden (Sabri and et.al., 2015).. They provide long-term fund if they are

confident that about their fund security.

2.4

Balance sheet represents both the preference and ordinary share capital in the liability

side of balance sheet. Collection of fund through share capital increase Sainsbury’s cash or bank

balance. However, cost that is dividend is deducted from net profit after interest and taxes to

determined retained or residual earnings, at the same time, cash balance will be reduced to the

extent of dividend payment (Huang, Ritter and Zhang, 2016). Contrary to this, loan amount is

reported under the non-current liability head and also improve total cash position. However, on

the other side, interest payment is considered as operational spending hence results in less net

return and cash position. On the other, investment in fixed assets is reported under the head long-

terrm assets of balance sheet. However, equal periodical instalments paid to assets vendor is

reported as expenditures and decline net yield (Shibata and Nishihara, 2015).

TASK 3

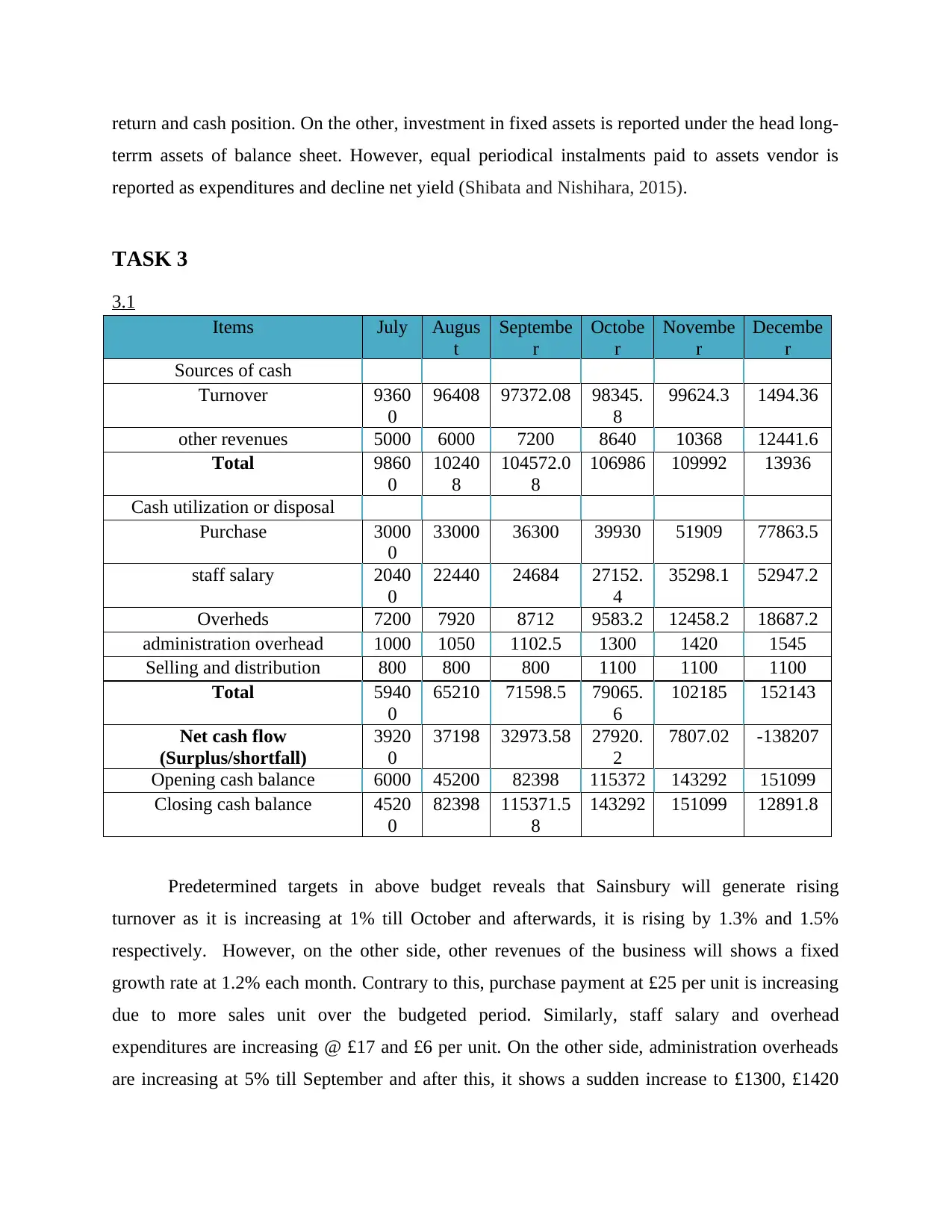

3.1

Items July Augus

t

Septembe

r

Octobe

r

Novembe

r

Decembe

r

Sources of cash

Turnover 9360

0

96408 97372.08 98345.

8

99624.3 1494.36

other revenues 5000 6000 7200 8640 10368 12441.6

Total 9860

0

10240

8

104572.0

8

106986 109992 13936

Cash utilization or disposal

Purchase 3000

0

33000 36300 39930 51909 77863.5

staff salary 2040

0

22440 24684 27152.

4

35298.1 52947.2

Overheds 7200 7920 8712 9583.2 12458.2 18687.2

administration overhead 1000 1050 1102.5 1300 1420 1545

Selling and distribution 800 800 800 1100 1100 1100

Total 5940

0

65210 71598.5 79065.

6

102185 152143

Net cash flow

(Surplus/shortfall)

3920

0

37198 32973.58 27920.

2

7807.02 -138207

Opening cash balance 6000 45200 82398 115372 143292 151099

Closing cash balance 4520

0

82398 115371.5

8

143292 151099 12891.8

Predetermined targets in above budget reveals that Sainsbury will generate rising

turnover as it is increasing at 1% till October and afterwards, it is rising by 1.3% and 1.5%

respectively. However, on the other side, other revenues of the business will shows a fixed

growth rate at 1.2% each month. Contrary to this, purchase payment at £25 per unit is increasing

due to more sales unit over the budgeted period. Similarly, staff salary and overhead

expenditures are increasing @ £17 and £6 per unit. On the other side, administration overheads

are increasing at 5% till September and after this, it shows a sudden increase to £1300, £1420

terrm assets of balance sheet. However, equal periodical instalments paid to assets vendor is

reported as expenditures and decline net yield (Shibata and Nishihara, 2015).

TASK 3

3.1

Items July Augus

t

Septembe

r

Octobe

r

Novembe

r

Decembe

r

Sources of cash

Turnover 9360

0

96408 97372.08 98345.

8

99624.3 1494.36

other revenues 5000 6000 7200 8640 10368 12441.6

Total 9860

0

10240

8

104572.0

8

106986 109992 13936

Cash utilization or disposal

Purchase 3000

0

33000 36300 39930 51909 77863.5

staff salary 2040

0

22440 24684 27152.

4

35298.1 52947.2

Overheds 7200 7920 8712 9583.2 12458.2 18687.2

administration overhead 1000 1050 1102.5 1300 1420 1545

Selling and distribution 800 800 800 1100 1100 1100

Total 5940

0

65210 71598.5 79065.

6

102185 152143

Net cash flow

(Surplus/shortfall)

3920

0

37198 32973.58 27920.

2

7807.02 -138207

Opening cash balance 6000 45200 82398 115372 143292 151099

Closing cash balance 4520

0

82398 115371.5

8

143292 151099 12891.8

Predetermined targets in above budget reveals that Sainsbury will generate rising

turnover as it is increasing at 1% till October and afterwards, it is rising by 1.3% and 1.5%

respectively. However, on the other side, other revenues of the business will shows a fixed

growth rate at 1.2% each month. Contrary to this, purchase payment at £25 per unit is increasing

due to more sales unit over the budgeted period. Similarly, staff salary and overhead

expenditures are increasing @ £17 and £6 per unit. On the other side, administration overheads

are increasing at 5% till September and after this, it shows a sudden increase to £1300, £1420

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and £1545 whilst S&D expenditures remains constant till September to 800 and afterwards rose

to £1100 per month. Due to lower increase in revenues than cash outflow, surplus balance shows

a decreasing trend and in end, indicates cash shortfall.

Ways to remove shortfall and maximize surplus

- Investing surplus money in other profitable purpose rather than keeping it in account

where Sainsbury can generate yield or return (Lowe and Tinker, 2015).

- Controlling administration expenditures through better monitoring and controlling.

- Buying quality material at reasonable prices and recruiting skilled labor at an affordable

wages rate.

3.2

Fixed cost comprises all the business spending that have no relation with total output and

production and remains constant throughout the period such as depreciation and insurance

(Kaplan and Atkinson, 2015).

Variable cost consists of expenditures that have direct relationship with total

manufacturing as at high production volume, it moves upwards or vice-versa such as material,

labor and direct overheads (Haynes, 2015).

Total cost = Total Fixed cost (TFC) + Total Variable cost (TVC)

Unit cost/per unit cost = Total production cost/Quantity of goods produced

Items Per unit cost Cost

Material 25 125000

Labor 17 85000

Overheads 6 30000

TVC 28 240000

TFC 60000

TC 300000

Quantity of goods produced = 5000

= £300,000/5000 units

= £60

to £1100 per month. Due to lower increase in revenues than cash outflow, surplus balance shows

a decreasing trend and in end, indicates cash shortfall.

Ways to remove shortfall and maximize surplus

- Investing surplus money in other profitable purpose rather than keeping it in account

where Sainsbury can generate yield or return (Lowe and Tinker, 2015).

- Controlling administration expenditures through better monitoring and controlling.

- Buying quality material at reasonable prices and recruiting skilled labor at an affordable

wages rate.

3.2

Fixed cost comprises all the business spending that have no relation with total output and

production and remains constant throughout the period such as depreciation and insurance

(Kaplan and Atkinson, 2015).

Variable cost consists of expenditures that have direct relationship with total

manufacturing as at high production volume, it moves upwards or vice-versa such as material,

labor and direct overheads (Haynes, 2015).

Total cost = Total Fixed cost (TFC) + Total Variable cost (TVC)

Unit cost/per unit cost = Total production cost/Quantity of goods produced

Items Per unit cost Cost

Material 25 125000

Labor 17 85000

Overheads 6 30000

TVC 28 240000

TFC 60000

TC 300000

Quantity of goods produced = 5000

= £300,000/5000 units

= £60

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling price as per Cost-oriented method = Cost per unit + Mark-up on cost

= £60 + (£60*30%)

= £60 + £18

= £78

BEP (Units) = TFC/Contribution each unit

Contribution per unit = selling price – TVC

= £60,000/(£78-£28)

= £60,000/£50

= 1200

Derived results reveal that at selling price of £78 per unit, Sainsbury needs to sell 1200

units so as to recover both the fixed and variable costs. After this break-even point, every

additional selling unit will drive profit into the business as BEP represents maximum utilization

of business resources. While, if company became unable to achieve this point than it will

definitely bear loss.

3.3

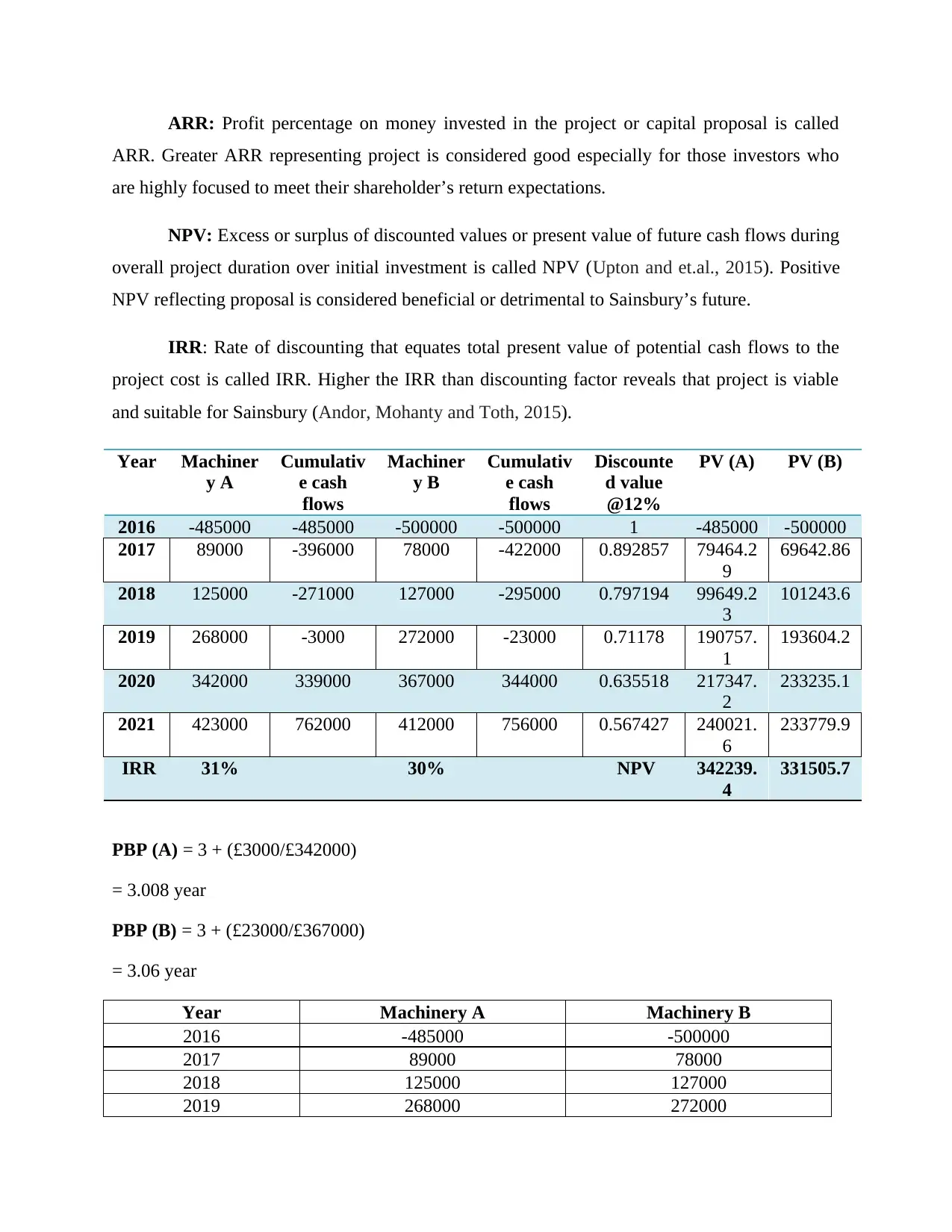

Sainsbury can use capital budgeting techniques to examine and evaluate relative

attractiveness of different projects and identify the most worthy project (Investment appraisal

techniques, 2016). Payback period (PBP) and Accounting rate of return (ARR) are non-

discounting methods of project evaluation whereas net present value (NPV) and internal rate of

return (IRR) are discounted techniques which consider time value of relevant cash flows.

PBP: The time lag or length in which, cumulative cash flows of the projects comes just

equal to the initial cash outlay is called PBP (Götze, Northcott and Schuster, 2015). Lower PBP

is always considered superior or attracts those investors who are highly interested to generate

back earlier their initial investment.

= £60 + (£60*30%)

= £60 + £18

= £78

BEP (Units) = TFC/Contribution each unit

Contribution per unit = selling price – TVC

= £60,000/(£78-£28)

= £60,000/£50

= 1200

Derived results reveal that at selling price of £78 per unit, Sainsbury needs to sell 1200

units so as to recover both the fixed and variable costs. After this break-even point, every

additional selling unit will drive profit into the business as BEP represents maximum utilization

of business resources. While, if company became unable to achieve this point than it will

definitely bear loss.

3.3

Sainsbury can use capital budgeting techniques to examine and evaluate relative

attractiveness of different projects and identify the most worthy project (Investment appraisal

techniques, 2016). Payback period (PBP) and Accounting rate of return (ARR) are non-

discounting methods of project evaluation whereas net present value (NPV) and internal rate of

return (IRR) are discounted techniques which consider time value of relevant cash flows.

PBP: The time lag or length in which, cumulative cash flows of the projects comes just

equal to the initial cash outlay is called PBP (Götze, Northcott and Schuster, 2015). Lower PBP

is always considered superior or attracts those investors who are highly interested to generate

back earlier their initial investment.

ARR: Profit percentage on money invested in the project or capital proposal is called

ARR. Greater ARR representing project is considered good especially for those investors who

are highly focused to meet their shareholder’s return expectations.

NPV: Excess or surplus of discounted values or present value of future cash flows during

overall project duration over initial investment is called NPV (Upton and et.al., 2015). Positive

NPV reflecting proposal is considered beneficial or detrimental to Sainsbury’s future.

IRR: Rate of discounting that equates total present value of potential cash flows to the

project cost is called IRR. Higher the IRR than discounting factor reveals that project is viable

and suitable for Sainsbury (Andor, Mohanty and Toth, 2015).

Year Machiner

y A

Cumulativ

e cash

flows

Machiner

y B

Cumulativ

e cash

flows

Discounte

d value

@12%

PV (A) PV (B)

2016 -485000 -485000 -500000 -500000 1 -485000 -500000

2017 89000 -396000 78000 -422000 0.892857 79464.2

9

69642.86

2018 125000 -271000 127000 -295000 0.797194 99649.2

3

101243.6

2019 268000 -3000 272000 -23000 0.71178 190757.

1

193604.2

2020 342000 339000 367000 344000 0.635518 217347.

2

233235.1

2021 423000 762000 412000 756000 0.567427 240021.

6

233779.9

IRR 31% 30% NPV 342239.

4

331505.7

PBP (A) = 3 + (£3000/£342000)

= 3.008 year

PBP (B) = 3 + (£23000/£367000)

= 3.06 year

Year Machinery A Machinery B

2016 -485000 -500000

2017 89000 78000

2018 125000 127000

2019 268000 272000

ARR. Greater ARR representing project is considered good especially for those investors who

are highly focused to meet their shareholder’s return expectations.

NPV: Excess or surplus of discounted values or present value of future cash flows during

overall project duration over initial investment is called NPV (Upton and et.al., 2015). Positive

NPV reflecting proposal is considered beneficial or detrimental to Sainsbury’s future.

IRR: Rate of discounting that equates total present value of potential cash flows to the

project cost is called IRR. Higher the IRR than discounting factor reveals that project is viable

and suitable for Sainsbury (Andor, Mohanty and Toth, 2015).

Year Machiner

y A

Cumulativ

e cash

flows

Machiner

y B

Cumulativ

e cash

flows

Discounte

d value

@12%

PV (A) PV (B)

2016 -485000 -485000 -500000 -500000 1 -485000 -500000

2017 89000 -396000 78000 -422000 0.892857 79464.2

9

69642.86

2018 125000 -271000 127000 -295000 0.797194 99649.2

3

101243.6

2019 268000 -3000 272000 -23000 0.71178 190757.

1

193604.2

2020 342000 339000 367000 344000 0.635518 217347.

2

233235.1

2021 423000 762000 412000 756000 0.567427 240021.

6

233779.9

IRR 31% 30% NPV 342239.

4

331505.7

PBP (A) = 3 + (£3000/£342000)

= 3.008 year

PBP (B) = 3 + (£23000/£367000)

= 3.06 year

Year Machinery A Machinery B

2016 -485000 -500000

2017 89000 78000

2018 125000 127000

2019 268000 272000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.