Financial Management Assignment: Detailed Analysis, 2024

VerifiedAdded on 2022/08/28

|13

|1750

|69

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial management assignment. It addresses several key concepts including the time value of money, comparing ordinary annuities and annuities due. It provides detailed calculations for loan amortization, bond valuation, and dividend valuation. The assignment also explores investment appraisal techniques, including payback period, discounted payback period, net present value, present value index, and internal rate of return, with a focus on incremental cash flow analysis. The document concludes with a discussion of additional factors to consider when evaluating an investment project.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Answer to question 1:......................................................................................................................3

Answer to question 2:......................................................................................................................3

Answer to question 3:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................4

Answer to question 4:......................................................................................................................4

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................5

Answer to question 5:......................................................................................................................6

Part a:...........................................................................................................................................6

Part b:...........................................................................................................................................7

Part c:...........................................................................................................................................7

Answer to question 6:......................................................................................................................7

Part a:...........................................................................................................................................7

Part b:...........................................................................................................................................8

Answer to question 7:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................9

Part c:...........................................................................................................................................9

Table of Contents

Answer to question 1:......................................................................................................................3

Answer to question 2:......................................................................................................................3

Answer to question 3:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................4

Answer to question 4:......................................................................................................................4

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................5

Answer to question 5:......................................................................................................................6

Part a:...........................................................................................................................................6

Part b:...........................................................................................................................................7

Part c:...........................................................................................................................................7

Answer to question 6:......................................................................................................................7

Part a:...........................................................................................................................................7

Part b:...........................................................................................................................................8

Answer to question 7:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................9

Part c:...........................................................................................................................................9

2FINANCIAL MANAGEMENT

Part d:...........................................................................................................................................9

Part f:.........................................................................................................................................10

Part g:.........................................................................................................................................10

References and bibliography:........................................................................................................12

Part d:...........................................................................................................................................9

Part f:.........................................................................................................................................10

Part g:.........................................................................................................................................10

References and bibliography:........................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Answer to question 1:

Year 1 2 3

Income from the trust $ 40,000 $ 30,000 $ 60,000

Consumptions $ -32,000 $ -42,000 $ -

Balance (Income –

Consumption) $ 8,000 $ -12,000 $ 60,000

Compounding factor

@5% p.a. 1.1025 1.0500 1.0000

Compounded value

8000*1.1025 = $

8,820

-12000*1.0500 = $ -

12,600

60000*1.0000 = $

60,000

Consumption in two years = 8820+12600+60000 = $56,220

Answer to question 2:

In an ordinary annuity, the amount is paid at the end of the period whereas in an annuity

due, the amount is paid at the beginning of the period. As per the time value of money concept,

the amount is more preferable at present rather than a certain time period hence. Hence, it is

more beneficial to invest in an annuity due. Amount received from an annuity due at the

beginning of the period can be invested in another investment option. For example, if from an

annuity due, an amount of $10,000 is received at present it can be invested in market or in any

other investment option which can give a significant amount of earnings. If the same amount is

received at the end of the period then there would be a loss of interest earnings (Khan&

Jain2018).

Answer to question 3:

Part a:

Loan amount = $75,000

Interest rate per annum = 7.20%

Answer to question 1:

Year 1 2 3

Income from the trust $ 40,000 $ 30,000 $ 60,000

Consumptions $ -32,000 $ -42,000 $ -

Balance (Income –

Consumption) $ 8,000 $ -12,000 $ 60,000

Compounding factor

@5% p.a. 1.1025 1.0500 1.0000

Compounded value

8000*1.1025 = $

8,820

-12000*1.0500 = $ -

12,600

60000*1.0000 = $

60,000

Consumption in two years = 8820+12600+60000 = $56,220

Answer to question 2:

In an ordinary annuity, the amount is paid at the end of the period whereas in an annuity

due, the amount is paid at the beginning of the period. As per the time value of money concept,

the amount is more preferable at present rather than a certain time period hence. Hence, it is

more beneficial to invest in an annuity due. Amount received from an annuity due at the

beginning of the period can be invested in another investment option. For example, if from an

annuity due, an amount of $10,000 is received at present it can be invested in market or in any

other investment option which can give a significant amount of earnings. If the same amount is

received at the end of the period then there would be a loss of interest earnings (Khan&

Jain2018).

Answer to question 3:

Part a:

Loan amount = $75,000

Interest rate per annum = 7.20%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

Term of loan = 7Years

Number of payments in a year = 4 times

Therefore,

75000=

[ A

7.20 %

4

×

{1− 1

(1+7.20 %

4 )

7 × 4

}]

75000= [ A

0.018 ×0.3918 ]

A=75000 ×0.018

0.3918 = $3,434

A= Installment amount.

Part b:

If the installment amount is $3,867 then,

75000=

[ 3867

7.20 %

4

×

{1− 1

(1+7.20 %

4 )

n × 4

}]

n = Number of years

Solving the above equation, we get,

n = 6

Hence, if the installment amount is $3,867, then the loan could be repaid in 6 years.

Term of loan = 7Years

Number of payments in a year = 4 times

Therefore,

75000=

[ A

7.20 %

4

×

{1− 1

(1+7.20 %

4 )

7 × 4

}]

75000= [ A

0.018 ×0.3918 ]

A=75000 ×0.018

0.3918 = $3,434

A= Installment amount.

Part b:

If the installment amount is $3,867 then,

75000=

[ 3867

7.20 %

4

×

{1− 1

(1+7.20 %

4 )

n × 4

}]

n = Number of years

Solving the above equation, we get,

n = 6

Hence, if the installment amount is $3,867, then the loan could be repaid in 6 years.

5FINANCIAL MANAGEMENT

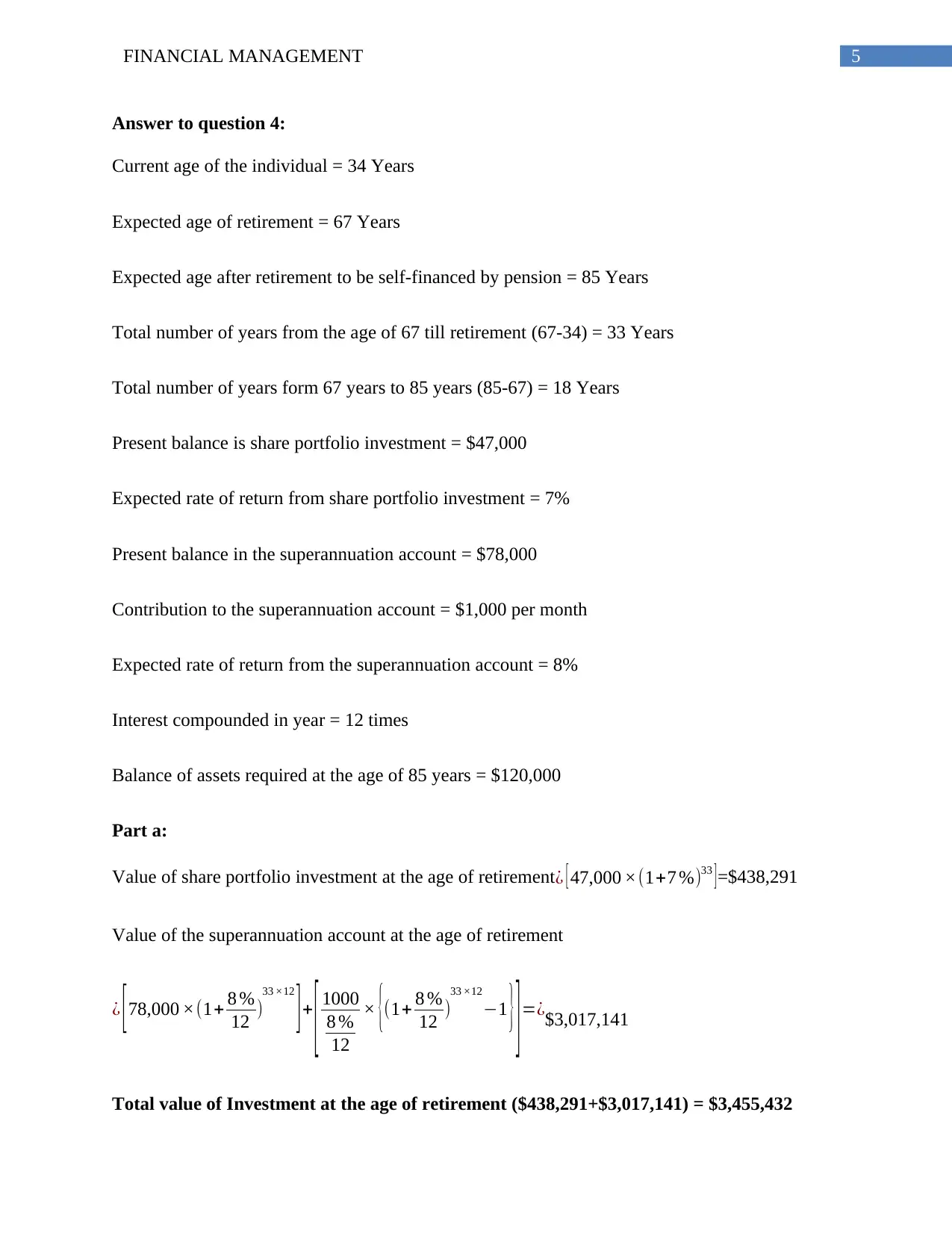

Answer to question 4:

Current age of the individual = 34 Years

Expected age of retirement = 67 Years

Expected age after retirement to be self-financed by pension = 85 Years

Total number of years from the age of 67 till retirement (67-34) = 33 Years

Total number of years form 67 years to 85 years (85-67) = 18 Years

Present balance is share portfolio investment = $47,000

Expected rate of return from share portfolio investment = 7%

Present balance in the superannuation account = $78,000

Contribution to the superannuation account = $1,000 per month

Expected rate of return from the superannuation account = 8%

Interest compounded in year = 12 times

Balance of assets required at the age of 85 years = $120,000

Part a:

Value of share portfolio investment at the age of retirement ¿ [ 47,000 ×(1+7 %)33 ]=$438,291

Value of the superannuation account at the age of retirement

¿ [78,000 ×(1+ 8 %

12 )

33 ×12

]+

[ 1000

8 %

12

× {(1+ 8 %

12 )

33 ×12

−1 }]=¿$3,017,141

Total value of Investment at the age of retirement ($438,291+$3,017,141) = $3,455,432

Answer to question 4:

Current age of the individual = 34 Years

Expected age of retirement = 67 Years

Expected age after retirement to be self-financed by pension = 85 Years

Total number of years from the age of 67 till retirement (67-34) = 33 Years

Total number of years form 67 years to 85 years (85-67) = 18 Years

Present balance is share portfolio investment = $47,000

Expected rate of return from share portfolio investment = 7%

Present balance in the superannuation account = $78,000

Contribution to the superannuation account = $1,000 per month

Expected rate of return from the superannuation account = 8%

Interest compounded in year = 12 times

Balance of assets required at the age of 85 years = $120,000

Part a:

Value of share portfolio investment at the age of retirement ¿ [ 47,000 ×(1+7 %)33 ]=$438,291

Value of the superannuation account at the age of retirement

¿ [78,000 ×(1+ 8 %

12 )

33 ×12

]+

[ 1000

8 %

12

× {(1+ 8 %

12 )

33 ×12

−1 }]=¿$3,017,141

Total value of Investment at the age of retirement ($438,291+$3,017,141) = $3,455,432

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Part b:

Expected rate of return from the investment in retirement scheme = 5%

Interest compounded in a year = 12 times

Monthly annuity (A):

$ 120,000=

[ A

8 %

12

× {(1+ 8 %

12 )

18 ×12

−1 }]

$ 120,000= [ A

0.00667 × {(1+0.00667)18× 12−1 } ]

$ 120,000= [ A

0.00667 ×12.891 ]

A=

[ 120,000× 0.00667

12.891 ]

A = $23,949.22

Answer to question 5:

Face value of bond = $1,000

Annual coupon rate of the bond = 10%

Annual coupon payment of the bond ($1,000*10%) = $100

Semiannual coupon payment ($100/2) = $50

Term of the bond = 8 Years

Market Yield rate = 11.28%

Part b:

Expected rate of return from the investment in retirement scheme = 5%

Interest compounded in a year = 12 times

Monthly annuity (A):

$ 120,000=

[ A

8 %

12

× {(1+ 8 %

12 )

18 ×12

−1 }]

$ 120,000= [ A

0.00667 × {(1+0.00667)18× 12−1 } ]

$ 120,000= [ A

0.00667 ×12.891 ]

A=

[ 120,000× 0.00667

12.891 ]

A = $23,949.22

Answer to question 5:

Face value of bond = $1,000

Annual coupon rate of the bond = 10%

Annual coupon payment of the bond ($1,000*10%) = $100

Semiannual coupon payment ($100/2) = $50

Term of the bond = 8 Years

Market Yield rate = 11.28%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Part a:

Price of each bond

¿

[1,000 × 1

(1+ 11.28 %

2 )

8 ×2

]+

[ 50

11.28 %

2

×

{1− 1

(1+ 11.28 %

2 )

8 × 2

}]

= $102.36

Part b:

Total capital requirement = $2,800,000

Number of bonds to be issued ($2,800,000/$102.36) = 27,355 bonds

Part c:

If the bonds are issued at the face value, then there is no capital yield, only return is the

interest yield. Hence, if the bonds in the given case needs to be issued at face value, then the

coupon rate should be the market yield rate of 11.28% (Shapiro &Hanouna 2019).

Answer to question 6:

Part a:

Current dividend = $0.55

Required rate of return = 12%

Constant growth rate = 4%

Year 2020 2021 2022 2023 2024

Growth rate 27% 22% 15% 4%

Dividend (Last year’s

return*(1+rowth rate) $ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 1.02

Value of share at January 2024* $ 13.25

Part a:

Price of each bond

¿

[1,000 × 1

(1+ 11.28 %

2 )

8 ×2

]+

[ 50

11.28 %

2

×

{1− 1

(1+ 11.28 %

2 )

8 × 2

}]

= $102.36

Part b:

Total capital requirement = $2,800,000

Number of bonds to be issued ($2,800,000/$102.36) = 27,355 bonds

Part c:

If the bonds are issued at the face value, then there is no capital yield, only return is the

interest yield. Hence, if the bonds in the given case needs to be issued at face value, then the

coupon rate should be the market yield rate of 11.28% (Shapiro &Hanouna 2019).

Answer to question 6:

Part a:

Current dividend = $0.55

Required rate of return = 12%

Constant growth rate = 4%

Year 2020 2021 2022 2023 2024

Growth rate 27% 22% 15% 4%

Dividend (Last year’s

return*(1+rowth rate) $ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 1.02

Value of share at January 2024* $ 13.25

8FINANCIAL MANAGEMENT

$ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 14.27

Discounting factor @ 12% p.a. 1.0000 0.8929 0.7972 0.7118 0.6355

Discounted value $ 0.55 $ 0.62 $ 0.68 $ 0.70 $ 9.07

* Value of share at January 2024 = 1.02×(1+4 %)

12 %−4 % = $13.25

Value of share = 0.55+0.62+0.68+0.70+9.07 = 11.62

Part b:

Cash Flow Timeline

Jan

2020

Jan

2021

Jan

2022

Jan

2023

Jan

2024

Jan

2024

$ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 1.02 $

13.25

Answer to question 7:

Part a:

Computation of incremental cash

flows:

Year 0 1 2 3 4

Increase in revenue $ - $ 2,50,000 $ 2,50,000 $

2,50,000 $ 2,50,000

Increase in variable costs $ - $ -60,000 $ -60,000 $ -60,000 $ -60,000

Annual depreciation $ - $ -1,12,500 $ -1,12,500 $ -1,12,500 $ -1,12,500

Interest expenses $ - $ -39,375 $ -39,375 $ -39,375 $ -39,375

Opportunity costs $ - $ -30,000 $ -30,000 $ -30,000 $ -30,000

Income tax $ - $ -2,438 $ -2,438 $ -2,438 $ -2,438

Subtotal $ - $ 5,688 $ 5,688 $

5,688 $ 5,688

Depreciation $ - $ 1,12,500 $ 1,12,500 $

1,12,500 $ 1,12,500

Lease compensation $ -33,000 $ - $ - $ - $ -

Additional working capital $ -35,000 $ - $ - $ - $ 35,000

$ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 14.27

Discounting factor @ 12% p.a. 1.0000 0.8929 0.7972 0.7118 0.6355

Discounted value $ 0.55 $ 0.62 $ 0.68 $ 0.70 $ 9.07

* Value of share at January 2024 = 1.02×(1+4 %)

12 %−4 % = $13.25

Value of share = 0.55+0.62+0.68+0.70+9.07 = 11.62

Part b:

Cash Flow Timeline

Jan

2020

Jan

2021

Jan

2022

Jan

2023

Jan

2024

Jan

2024

$ 0.55 $ 0.70 $ 0.85 $ 0.98 $ 1.02 $

13.25

Answer to question 7:

Part a:

Computation of incremental cash

flows:

Year 0 1 2 3 4

Increase in revenue $ - $ 2,50,000 $ 2,50,000 $

2,50,000 $ 2,50,000

Increase in variable costs $ - $ -60,000 $ -60,000 $ -60,000 $ -60,000

Annual depreciation $ - $ -1,12,500 $ -1,12,500 $ -1,12,500 $ -1,12,500

Interest expenses $ - $ -39,375 $ -39,375 $ -39,375 $ -39,375

Opportunity costs $ - $ -30,000 $ -30,000 $ -30,000 $ -30,000

Income tax $ - $ -2,438 $ -2,438 $ -2,438 $ -2,438

Subtotal $ - $ 5,688 $ 5,688 $

5,688 $ 5,688

Depreciation $ - $ 1,12,500 $ 1,12,500 $

1,12,500 $ 1,12,500

Lease compensation $ -33,000 $ - $ - $ - $ -

Additional working capital $ -35,000 $ - $ - $ - $ 35,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Investment $ -4,50,000 $ - $ - $ - $ 20,000

Incremental cash flows $ -5,18,000 $ 1,18,188 $ 1,18,188 $

1,18,188 $ 1,73,188

Internal calculations for payback period and discounted payback period:

Cumulative cash flow $ -5,18,000 $ -3,99,813 $ -2,81,625 $ -1,63,438 $ 9,750

Fraction in year 0.943702634

Discounting factor @ 10.25% 1.0000 0.9070 0.8227 0.7462 0.6768

Discounted cash flow

(Cash flow * Discounting factor) $ -5,18,000 $ 1,07,200 $ 97,233 $ 88,193 $ 1,17,220

Cumulative discounted cash flow $ -5,18,000 $ -4,10,800 $ -3,13,567 $ -2,25,374 $ -1,08,154

Fraction in year

Part b:

From the cumulative cash flow, it can be observed that, the cash flow converts into

positive in the year 4. Hence, it takes 3 years full and a part of the year 4 to recover back the

initial investment. Therefore, the payback period can be computed as follows.

Payback period = 3 + ($163,438/$173,118) = 3.94 Years.

Part c:

Net present value = Sum of discounted cash flows = (-518000+107200+97233+88193+117220)

= -$108,154

Part d:

Sum of discounted cash inflows = (107200+97233+88193+117220) = $409,846

Initial investment = $518,000

Present value index = Sum of discounted cash inflows/Initial investment

= 409846/518000 = 0.79

Investment $ -4,50,000 $ - $ - $ - $ 20,000

Incremental cash flows $ -5,18,000 $ 1,18,188 $ 1,18,188 $

1,18,188 $ 1,73,188

Internal calculations for payback period and discounted payback period:

Cumulative cash flow $ -5,18,000 $ -3,99,813 $ -2,81,625 $ -1,63,438 $ 9,750

Fraction in year 0.943702634

Discounting factor @ 10.25% 1.0000 0.9070 0.8227 0.7462 0.6768

Discounted cash flow

(Cash flow * Discounting factor) $ -5,18,000 $ 1,07,200 $ 97,233 $ 88,193 $ 1,17,220

Cumulative discounted cash flow $ -5,18,000 $ -4,10,800 $ -3,13,567 $ -2,25,374 $ -1,08,154

Fraction in year

Part b:

From the cumulative cash flow, it can be observed that, the cash flow converts into

positive in the year 4. Hence, it takes 3 years full and a part of the year 4 to recover back the

initial investment. Therefore, the payback period can be computed as follows.

Payback period = 3 + ($163,438/$173,118) = 3.94 Years.

Part c:

Net present value = Sum of discounted cash flows = (-518000+107200+97233+88193+117220)

= -$108,154

Part d:

Sum of discounted cash inflows = (107200+97233+88193+117220) = $409,846

Initial investment = $518,000

Present value index = Sum of discounted cash inflows/Initial investment

= 409846/518000 = 0.79

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

Part e:

From the internal calculation table above, it can be observed that, the cumulative

discounted cash flow is negative till the last year of the project. Hence, the discounted payback

period is beyond the project life.

Part f:

Discounting factor @1% 1.0000 0.9901 0.9803 0.9706 0.9610

Discounted cash flow $ -

5,18,000 $ 1,17,017 $ 1,15,859 $ 1,14,712 $ 1,66,430

Net present value = (-518000+117017+115859+114712+166430) = -3983

Discounting factor

@0.5% 1.0000 0.9950 0.9901 0.9851 0.9802

Discounted cash flow $ -

5,18,000

$

1,17,600

$

1,17,014

$

1,16,432

$

1,69,767

Net present value = (-518000+117600+117014+116432+169767) = 2813

At IRR the net present value is 0.

Hence, by applying simple interpolation technique,

1%-IRR/IRR-0.5% = -3983-0/0-2813

Solving the above equation we get, IRR = 0.71%

Part g:

There are various other factors which needs to be considered for the appraisal investment

in the proposed project. It can be observed that the land which will be used for the project is

giving a return of $30,000 per annum. The incremental cash flows are also not sufficient to give

Part e:

From the internal calculation table above, it can be observed that, the cumulative

discounted cash flow is negative till the last year of the project. Hence, the discounted payback

period is beyond the project life.

Part f:

Discounting factor @1% 1.0000 0.9901 0.9803 0.9706 0.9610

Discounted cash flow $ -

5,18,000 $ 1,17,017 $ 1,15,859 $ 1,14,712 $ 1,66,430

Net present value = (-518000+117017+115859+114712+166430) = -3983

Discounting factor

@0.5% 1.0000 0.9950 0.9901 0.9851 0.9802

Discounted cash flow $ -

5,18,000

$

1,17,600

$

1,17,014

$

1,16,432

$

1,69,767

Net present value = (-518000+117600+117014+116432+169767) = 2813

At IRR the net present value is 0.

Hence, by applying simple interpolation technique,

1%-IRR/IRR-0.5% = -3983-0/0-2813

Solving the above equation we get, IRR = 0.71%

Part g:

There are various other factors which needs to be considered for the appraisal investment

in the proposed project. It can be observed that the land which will be used for the project is

giving a return of $30,000 per annum. The incremental cash flows are also not sufficient to give

11FINANCIAL MANAGEMENT

a fair return to meet the return expectancy. On the other hand there might be any other social and

environmental perspective of the newly proposed project. All those perspective must be taken

care before deciding whether to go for the project or not (Shapiro& Hanouna2019).

a fair return to meet the return expectancy. On the other hand there might be any other social and

environmental perspective of the newly proposed project. All those perspective must be taken

care before deciding whether to go for the project or not (Shapiro& Hanouna2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.