Financial Management Accounting Exam Solution, LD Training, 2020/21

VerifiedAdded on 2022/12/09

|8

|1482

|401

Homework Assignment

AI Summary

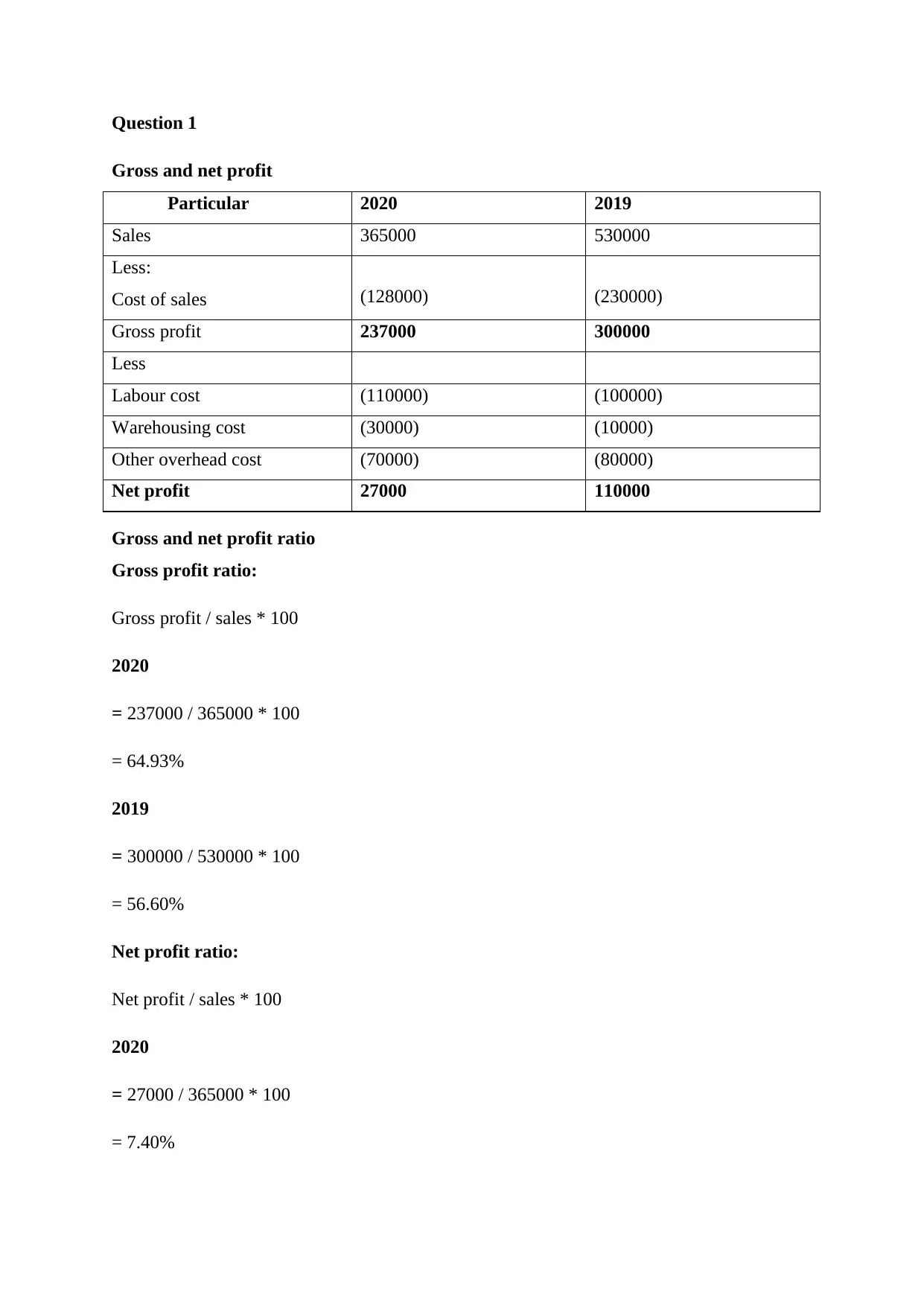

This document presents a comprehensive solution to a financial management accounting exam, addressing three case study questions. Question 1 analyzes Happyday Caterers Ltd., calculating gross and net profit, providing ratio analysis, and offering strategic recommendations to address declining profits and cash flow issues. Question 2 focuses on break-even point calculations, setting profitable sales targets, and evaluating the switch to activity-based costing. Question 3 involves calculating variances (sales, direct material, and direct labor), identifying their causes and consequences, and suggesting strategies for elimination or correlation. The solution also explores the advantages and disadvantages of switching from incremental-based budgeting to zero-based budgeting. The document includes detailed calculations, explanations, and references to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.