Financial Management Assignment: Equity & Investment Appraisal

VerifiedAdded on 2022/12/29

|16

|3921

|90

Homework Assignment

AI Summary

This assignment solution addresses key concepts in financial management, including long-term finance through equity finance and investment appraisal techniques. The solution begins by examining the issue of right shares for Lexbel PLC, calculating the number of shares to be issued, theoretical ex-rights price, and expected earnings per share under different rights issue prices. It then evaluates the benefits of scrip dividends for both shareholders and companies. The second part of the solution focuses on investment appraisal techniques, calculating the payback period, accounting rate of return, net present value, and internal rate of return for a given scenario. Detailed calculations and recommendations are provided to assist in making informed financial decisions. The assignment provides a thorough understanding of financial management principles and their practical applications.

Finance Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

QUESTION 3...................................................................................................................................5

(a) Calculations using the following Investment Appraisal techniques......................................5

(b) Benefits and limitations of each of differing investment appraisal techniques ....................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

QUESTION 3...................................................................................................................................5

(a) Calculations using the following Investment Appraisal techniques......................................5

(b) Benefits and limitations of each of differing investment appraisal techniques ....................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial management is defined as a procedure of effective preparation, arranging and

dominating of monetary resources. The term mainly consist of financial aspects and decisions in

regard of size of investments, sources and range of utilisation for capital to generate more

profitability in the business. For the maximization of profitability in the business requires to

focus on the financial resources that manage by management techniques (Al Ahbabi and

Nobanee, 2019). In the business finance manager apply different financial principal for the

financial assets and manage all the resources. The main aim of the report to understand the term

of financial management in context of business entity. This report based on the financial

management where different organisational are applying different types of financial techniques

to manage all the financial activities in effective manner. In this report consist of two questions,

first one is Long term finance: equity finance and second one is investment appraisal techniques.

QUESTION 1

(a) Long term finance: Equity finance

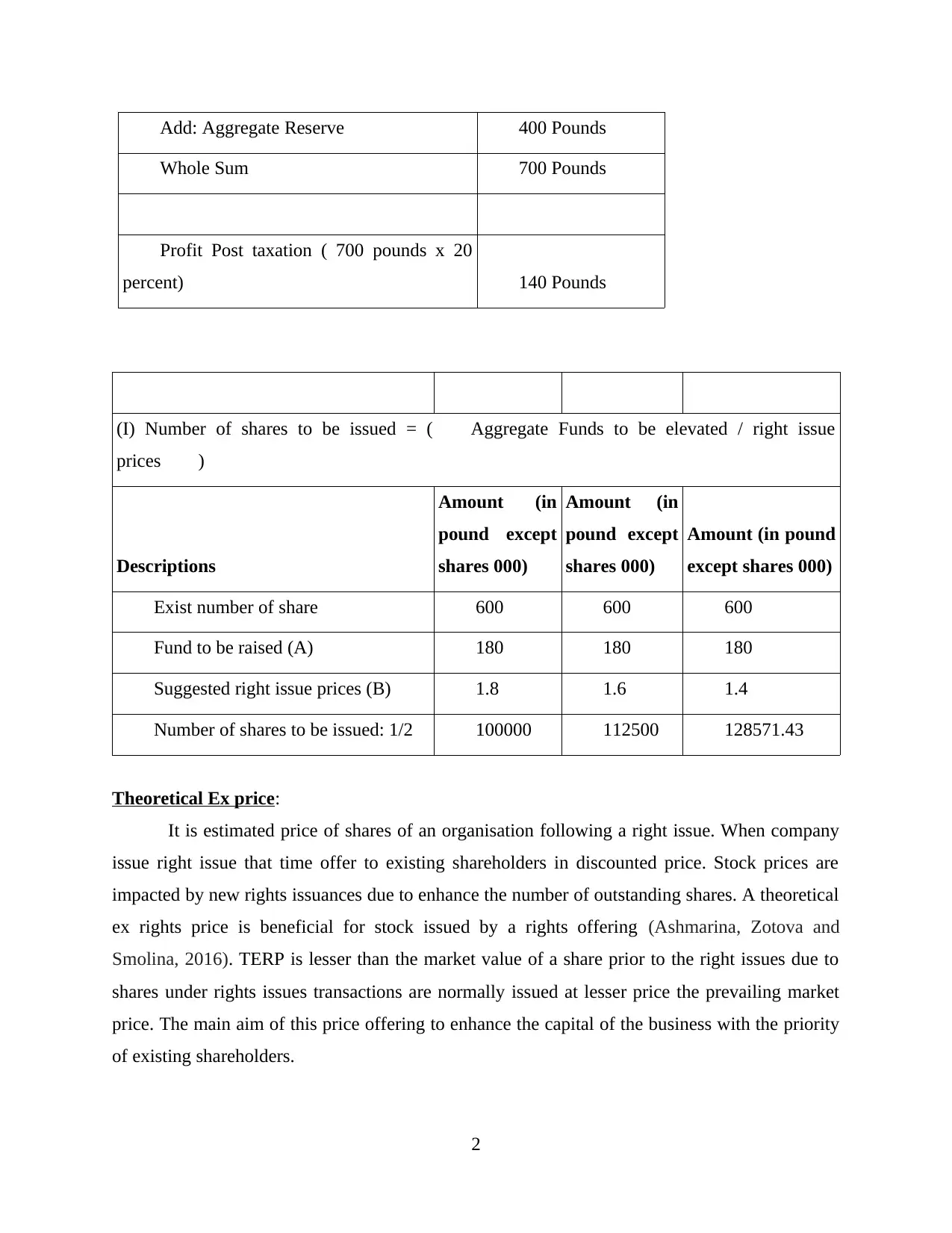

Issue of right share: It is a method for listed organisations to raise their capital. Right

issue is invitation for the presently shareholders to but new shares of organisation and it is gives

extra securities to exiting shareholders. Any organisation can issue right share whether public,

private and listed or unlisted company. These shares are offering to new customers when

existing customers are not ready to accept in the set time period of 15 days or more. In the

contest of Lexbel Plc want to issue right issue share to existing shareholders of completing

financial requirements (Antonopoulos and Hall, 2016). There are given the information of Issue

of right shares such as:

Lexbel plc wishes to rise: 180000 Pounds

Current ex-dividend market-price of Lexbel plc: 1.90 Pounds

3 assorted rights-issue prices recommended by corporation's finance director: GBP1.80, GBP

1.60 and GBP1.40

Right issue of Lexbel plc (In 000) (In 000)

…....Aggregate (no.)Ordinary shares (@ 50

for each) …....300 Pounds

1

Financial management is defined as a procedure of effective preparation, arranging and

dominating of monetary resources. The term mainly consist of financial aspects and decisions in

regard of size of investments, sources and range of utilisation for capital to generate more

profitability in the business. For the maximization of profitability in the business requires to

focus on the financial resources that manage by management techniques (Al Ahbabi and

Nobanee, 2019). In the business finance manager apply different financial principal for the

financial assets and manage all the resources. The main aim of the report to understand the term

of financial management in context of business entity. This report based on the financial

management where different organisational are applying different types of financial techniques

to manage all the financial activities in effective manner. In this report consist of two questions,

first one is Long term finance: equity finance and second one is investment appraisal techniques.

QUESTION 1

(a) Long term finance: Equity finance

Issue of right share: It is a method for listed organisations to raise their capital. Right

issue is invitation for the presently shareholders to but new shares of organisation and it is gives

extra securities to exiting shareholders. Any organisation can issue right share whether public,

private and listed or unlisted company. These shares are offering to new customers when

existing customers are not ready to accept in the set time period of 15 days or more. In the

contest of Lexbel Plc want to issue right issue share to existing shareholders of completing

financial requirements (Antonopoulos and Hall, 2016). There are given the information of Issue

of right shares such as:

Lexbel plc wishes to rise: 180000 Pounds

Current ex-dividend market-price of Lexbel plc: 1.90 Pounds

3 assorted rights-issue prices recommended by corporation's finance director: GBP1.80, GBP

1.60 and GBP1.40

Right issue of Lexbel plc (In 000) (In 000)

…....Aggregate (no.)Ordinary shares (@ 50

for each) …....300 Pounds

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

…....Add: Aggregate Reserve …....400 Pounds

…....Whole Sum …....700 Pounds

…....Profit Post taxation ( 700 pounds x 20

percent) …....140 Pounds

(I) Number of shares to be issued = (…....Aggregate Funds to be elevated / right issue

prices…....)

Descriptions

Amount (in

pound except

shares 000)

Amount (in

pound except

shares 000)

Amount (in pound

except shares 000)

…....Exist number of share …....600 …....600 …....600

…....Fund to be raised (A) …....180 …....180 …....180

…....Suggested right issue prices (B) …....1.8 …....1.6 …....1.4

…....Number of shares to be issued: 1/2 …....100000 …....112500 …....128571.43

Theoretical Ex price:

It is estimated price of shares of an organisation following a right issue. When company

issue right issue that time offer to existing shareholders in discounted price. Stock prices are

impacted by new rights issuances due to enhance the number of outstanding shares. A theoretical

ex rights price is beneficial for stock issued by a rights offering (Ashmarina, Zotova and

Smolina, 2016). TERP is lesser than the market value of a share prior to the right issues due to

shares under rights issues transactions are normally issued at lesser price the prevailing market

price. The main aim of this price offering to enhance the capital of the business with the priority

of existing shareholders.

2

…....Whole Sum …....700 Pounds

…....Profit Post taxation ( 700 pounds x 20

percent) …....140 Pounds

(I) Number of shares to be issued = (…....Aggregate Funds to be elevated / right issue

prices…....)

Descriptions

Amount (in

pound except

shares 000)

Amount (in

pound except

shares 000)

Amount (in pound

except shares 000)

…....Exist number of share …....600 …....600 …....600

…....Fund to be raised (A) …....180 …....180 …....180

…....Suggested right issue prices (B) …....1.8 …....1.6 …....1.4

…....Number of shares to be issued: 1/2 …....100000 …....112500 …....128571.43

Theoretical Ex price:

It is estimated price of shares of an organisation following a right issue. When company

issue right issue that time offer to existing shareholders in discounted price. Stock prices are

impacted by new rights issuances due to enhance the number of outstanding shares. A theoretical

ex rights price is beneficial for stock issued by a rights offering (Ashmarina, Zotova and

Smolina, 2016). TERP is lesser than the market value of a share prior to the right issues due to

shares under rights issues transactions are normally issued at lesser price the prevailing market

price. The main aim of this price offering to enhance the capital of the business with the priority

of existing shareholders.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

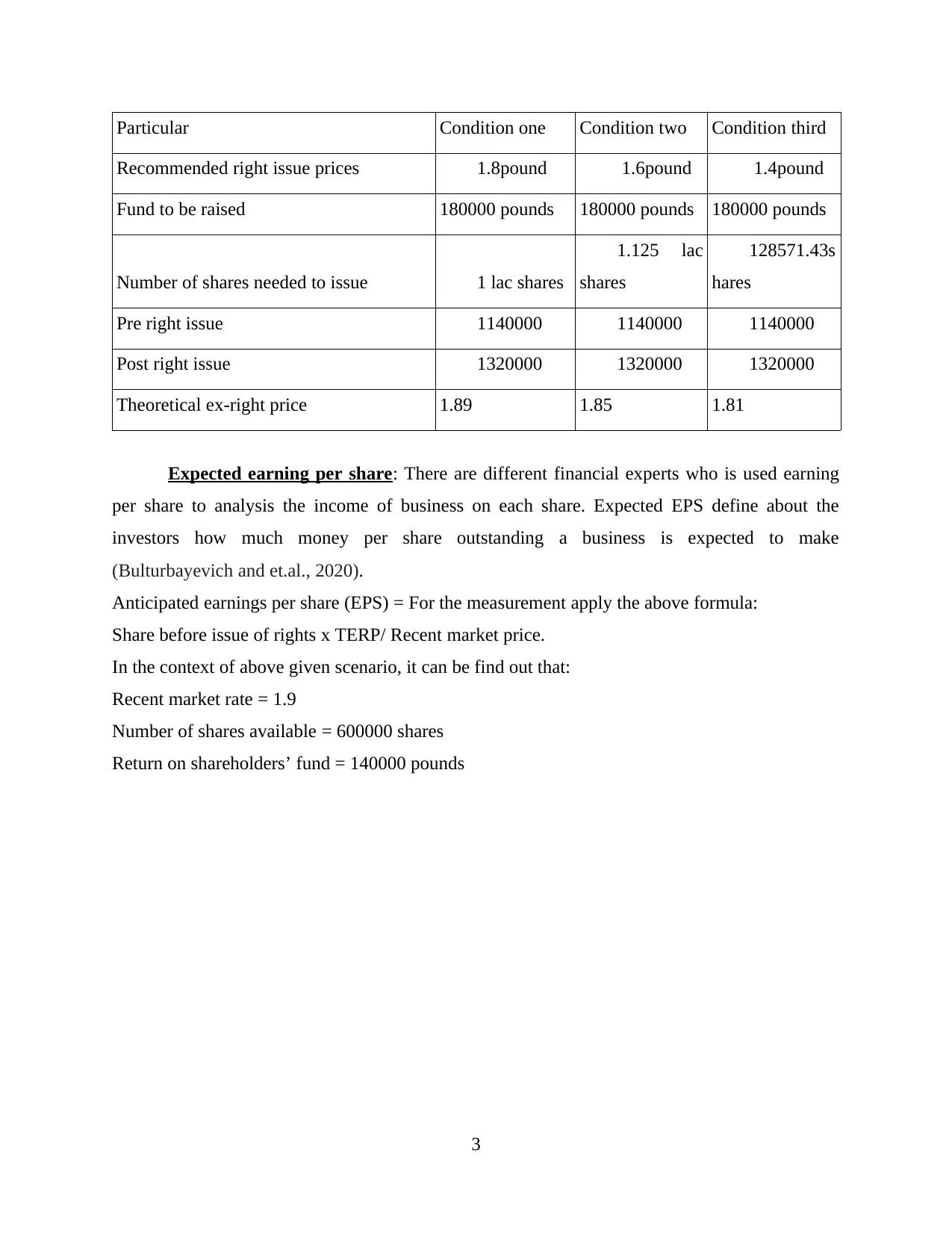

Particular Condition one Condition two Condition third

Recommended right issue prices …....1.8pound ….... 1.6pound …....1.4pound

Fund to be raised 180000 pounds 180000 pounds 180000 pounds

Number of shares needed to issue …....1 lac shares

…....1.125 lac

shares

…....128571.43s

hares

Pre right issue …....1140000 …....1140000 …....1140000

Post right issue …....1320000 …....1320000 …....1320000

Theoretical ex-right price 1.89 1.85 1.81

Expected earning per share: There are different financial experts who is used earning

per share to analysis the income of business on each share. Expected EPS define about the

investors how much money per share outstanding a business is expected to make

(Bulturbayevich and et.al., 2020).

Anticipated earnings per share (EPS) = For the measurement apply the above formula:

Share before issue of rights x TERP/ Recent market price.

In the context of above given scenario, it can be find out that:

Recent market rate = 1.9

Number of shares available = 600000 shares

Return on shareholders’ fund = 140000 pounds

3

Recommended right issue prices …....1.8pound ….... 1.6pound …....1.4pound

Fund to be raised 180000 pounds 180000 pounds 180000 pounds

Number of shares needed to issue …....1 lac shares

…....1.125 lac

shares

…....128571.43s

hares

Pre right issue …....1140000 …....1140000 …....1140000

Post right issue …....1320000 …....1320000 …....1320000

Theoretical ex-right price 1.89 1.85 1.81

Expected earning per share: There are different financial experts who is used earning

per share to analysis the income of business on each share. Expected EPS define about the

investors how much money per share outstanding a business is expected to make

(Bulturbayevich and et.al., 2020).

Anticipated earnings per share (EPS) = For the measurement apply the above formula:

Share before issue of rights x TERP/ Recent market price.

In the context of above given scenario, it can be find out that:

Recent market rate = 1.9

Number of shares available = 600000 shares

Return on shareholders’ fund = 140000 pounds

3

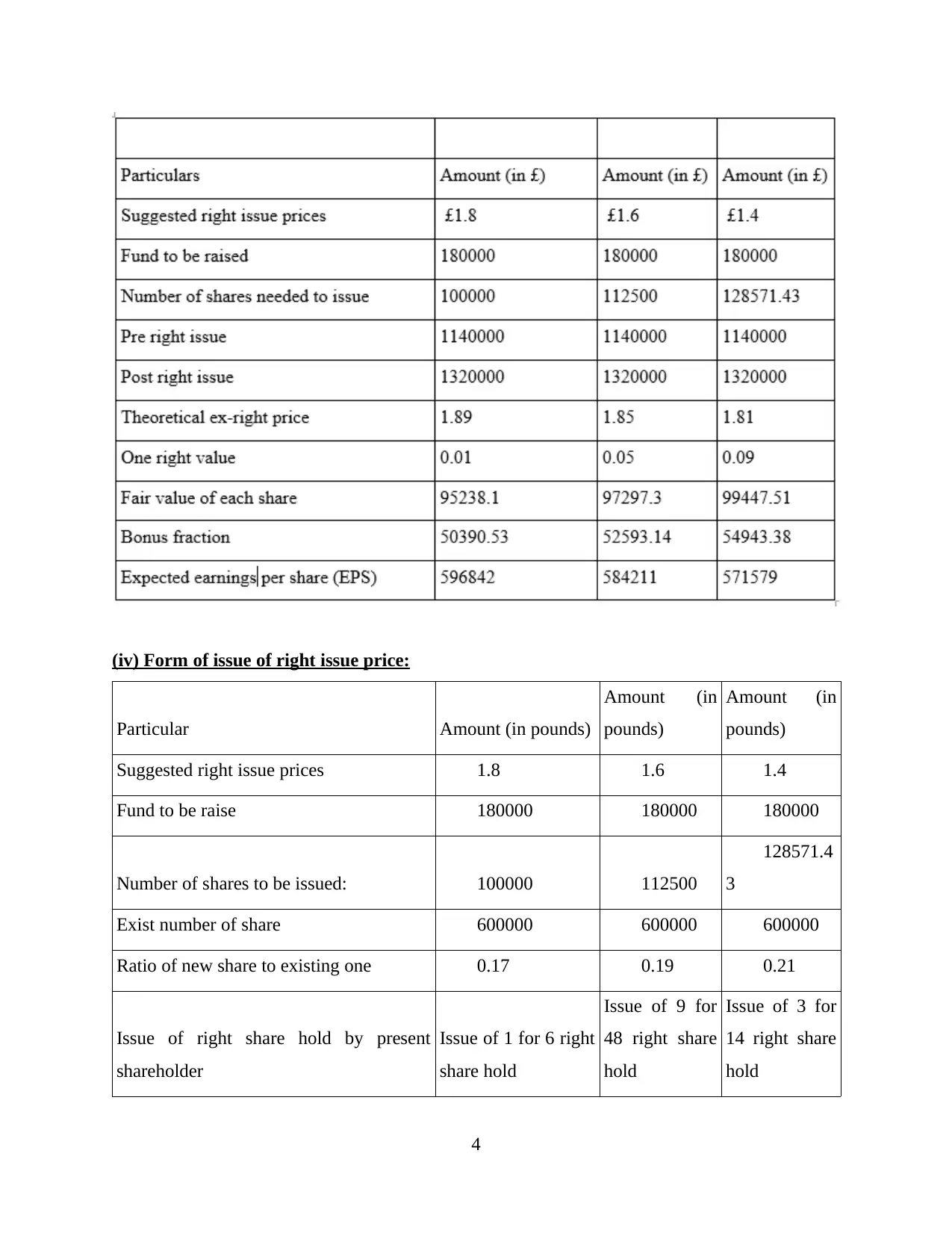

(iv) Form of issue of right issue price:

Particular Amount (in pounds)

Amount (in

pounds)

Amount (in

pounds)

Suggested right issue prices …....1.8 …....1.6 …....1.4

Fund to be raise …....180000 …....180000 …....180000

Number of shares to be issued: …....100000 …....112500

…....128571.4

3

Exist number of share …....600000 …....600000 …....600000

Ratio of new share to existing one …....0.17 …....0.19 …....0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

share hold

Issue of 9 for

48 right share

hold

Issue of 3 for

14 right share

hold

4

Particular Amount (in pounds)

Amount (in

pounds)

Amount (in

pounds)

Suggested right issue prices …....1.8 …....1.6 …....1.4

Fund to be raise …....180000 …....180000 …....180000

Number of shares to be issued: …....100000 …....112500

…....128571.4

3

Exist number of share …....600000 …....600000 …....600000

Ratio of new share to existing one …....0.17 …....0.19 …....0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

share hold

Issue of 9 for

48 right share

hold

Issue of 3 for

14 right share

hold

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the above calculation is has been determined that for the issue of shares, company

have three options that are following:

As per the first situation, the first option is 1.80 Pounds for each share and required to

issue 100,000 shares of each share. Thus, shareholders must classified pro-rata one share

that available 6 shares (Georgieva, 2018).

The option provide 1.60 Pounds per share are required to be issued of 112500 shares of

each share. Therefore, every stakeholders must provide their pro rata 9 shares that

available for 48 shares.

In the third option provide 1.40 Pounds for every share are estimated to be issued on the

128571.43 shares of every share. Thus, stakeholders must classified pro-rata 3 shares for

available 14 shares.

Critically evaluate the best option among the three right issues

There are providing three options for issue of right share and as per the analysis it is

advised that value of right share of 1.8 Pound of each share will be profitable for Lexbel

company. Therefore, value of expected earnings per share is greater in this alternatives as

compare to rest of two options.

(b) Benefits of scrip dividend in context of shareholders and companies

Scrip dividend: It is described as a new shares of an issuer's stock that are issued to

shareholders rather than of a dividend. It is mainly utilised by the company when they has less

cash for the issue of cash dividend but still want to pay their stakeholders in specified way. Scrip

dividend many be provide as an option to a cash dividend so dividend payments are

automatically rolled into more shares (Goryakin and et.al., 2017). It is a way where organisation

allows to its stakeholders to take their dividends in form of share instead of cash. Thus from the

overall analysis it is saying that script dividend is beneficial for those organisations who is not

able to pay cash dividends so they are giving option to shareholders to take shares. There are

mentioned the benefits of the scrip dividend for companies as well as for stakeholders such as:

For shareholders

The main advantage to shareholders of scrip dividend that painlessly enhance

shareholding in the business without having to pay broker's commission and stamp duty

on the rate of purchase share.

5

have three options that are following:

As per the first situation, the first option is 1.80 Pounds for each share and required to

issue 100,000 shares of each share. Thus, shareholders must classified pro-rata one share

that available 6 shares (Georgieva, 2018).

The option provide 1.60 Pounds per share are required to be issued of 112500 shares of

each share. Therefore, every stakeholders must provide their pro rata 9 shares that

available for 48 shares.

In the third option provide 1.40 Pounds for every share are estimated to be issued on the

128571.43 shares of every share. Thus, stakeholders must classified pro-rata 3 shares for

available 14 shares.

Critically evaluate the best option among the three right issues

There are providing three options for issue of right share and as per the analysis it is

advised that value of right share of 1.8 Pound of each share will be profitable for Lexbel

company. Therefore, value of expected earnings per share is greater in this alternatives as

compare to rest of two options.

(b) Benefits of scrip dividend in context of shareholders and companies

Scrip dividend: It is described as a new shares of an issuer's stock that are issued to

shareholders rather than of a dividend. It is mainly utilised by the company when they has less

cash for the issue of cash dividend but still want to pay their stakeholders in specified way. Scrip

dividend many be provide as an option to a cash dividend so dividend payments are

automatically rolled into more shares (Goryakin and et.al., 2017). It is a way where organisation

allows to its stakeholders to take their dividends in form of share instead of cash. Thus from the

overall analysis it is saying that script dividend is beneficial for those organisations who is not

able to pay cash dividends so they are giving option to shareholders to take shares. There are

mentioned the benefits of the scrip dividend for companies as well as for stakeholders such as:

For shareholders

The main advantage to shareholders of scrip dividend that painlessly enhance

shareholding in the business without having to pay broker's commission and stamp duty

on the rate of purchase share.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is beneficial for those stakeholders who wants to increase their shares in particular

organisation so it will help to decrease transactions cost in effective way.

It is another advantage that scrip dividend provide financial gain to shareholders due to

time travel of cash dividend.

Moreover, scrip dividend for investors provide equity shares in same company without

paying extra amount like purchasing fees, commission, mediator fees and many others.

For company

It is advantageous for organisation in case of have less cash liquidity so it will help to

provide option to investors to take issue of shares rather than of issuing cash dividends.

Moreover, issuing of scrip dividend increase the leverage and gearing circumstances

organisational entities. Thus, issuing of shares as a dividend as compare to cash help

them in increase effective leverage condition (Masharsky and et.al., 2018).

A business who have good brand position and goodwill can issue of shares easily when

company have not enough amount to pay dividend to its shareholders.

QUESTION 3

(a) Calculations using the following Investment Appraisal techniques

(a) Calculations-

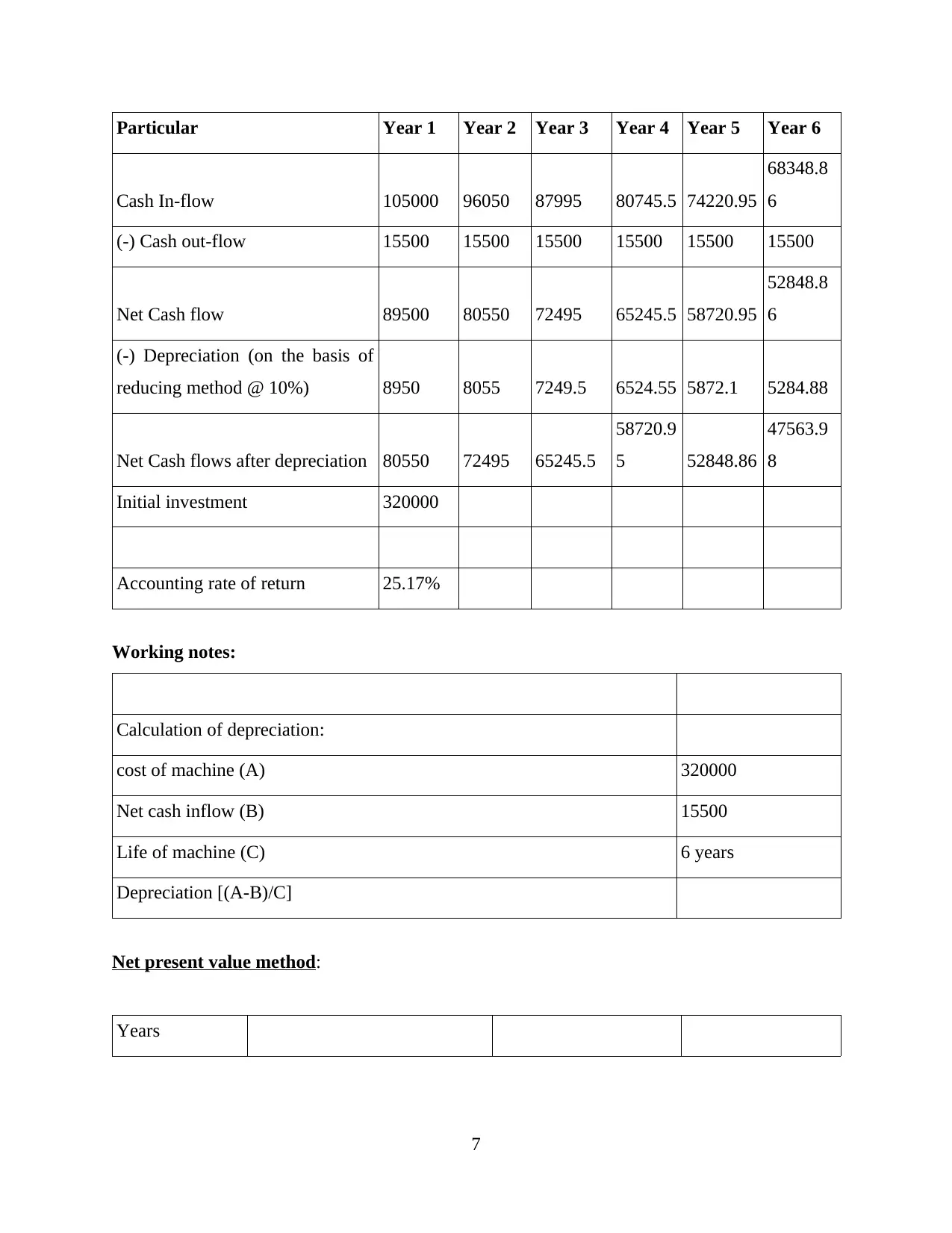

(I) Payback period method- Initial investment / cash flow (when there is equal cash flow)

Initial investment = 320,000 pounds

Cash flow = Expected annual cash inflow – cash outflow

= 105000 – 15500

= 89500 pounds

Hence, cash flow = 320000 / 89500

= 3.57 years

So cost of this project will be recovered within 3 years and few months.

(ii) Accounting rate of return- Cash flow after depreciation / Initial investment x 100

Initial investment = 320000 pounds

6

organisation so it will help to decrease transactions cost in effective way.

It is another advantage that scrip dividend provide financial gain to shareholders due to

time travel of cash dividend.

Moreover, scrip dividend for investors provide equity shares in same company without

paying extra amount like purchasing fees, commission, mediator fees and many others.

For company

It is advantageous for organisation in case of have less cash liquidity so it will help to

provide option to investors to take issue of shares rather than of issuing cash dividends.

Moreover, issuing of scrip dividend increase the leverage and gearing circumstances

organisational entities. Thus, issuing of shares as a dividend as compare to cash help

them in increase effective leverage condition (Masharsky and et.al., 2018).

A business who have good brand position and goodwill can issue of shares easily when

company have not enough amount to pay dividend to its shareholders.

QUESTION 3

(a) Calculations using the following Investment Appraisal techniques

(a) Calculations-

(I) Payback period method- Initial investment / cash flow (when there is equal cash flow)

Initial investment = 320,000 pounds

Cash flow = Expected annual cash inflow – cash outflow

= 105000 – 15500

= 89500 pounds

Hence, cash flow = 320000 / 89500

= 3.57 years

So cost of this project will be recovered within 3 years and few months.

(ii) Accounting rate of return- Cash flow after depreciation / Initial investment x 100

Initial investment = 320000 pounds

6

Particular Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash In-flow 105000 96050 87995 80745.5 74220.95

68348.8

6

(-) Cash out-flow 15500 15500 15500 15500 15500 15500

Net Cash flow 89500 80550 72495 65245.5 58720.95

52848.8

6

(-) Depreciation (on the basis of

reducing method @ 10%) 8950 8055 7249.5 6524.55 5872.1 5284.88

Net Cash flows after depreciation 80550 72495 65245.5

58720.9

5 52848.86

47563.9

8

Initial investment 320000

Accounting rate of return 25.17%

Working notes:

Calculation of depreciation:

cost of machine (A) 320000

Net cash inflow (B) 15500

Life of machine (C) 6 years

Depreciation [(A-B)/C]

Net present value method:

Years

7

Cash In-flow 105000 96050 87995 80745.5 74220.95

68348.8

6

(-) Cash out-flow 15500 15500 15500 15500 15500 15500

Net Cash flow 89500 80550 72495 65245.5 58720.95

52848.8

6

(-) Depreciation (on the basis of

reducing method @ 10%) 8950 8055 7249.5 6524.55 5872.1 5284.88

Net Cash flows after depreciation 80550 72495 65245.5

58720.9

5 52848.86

47563.9

8

Initial investment 320000

Accounting rate of return 25.17%

Working notes:

Calculation of depreciation:

cost of machine (A) 320000

Net cash inflow (B) 15500

Life of machine (C) 6 years

Depreciation [(A-B)/C]

Net present value method:

Years

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

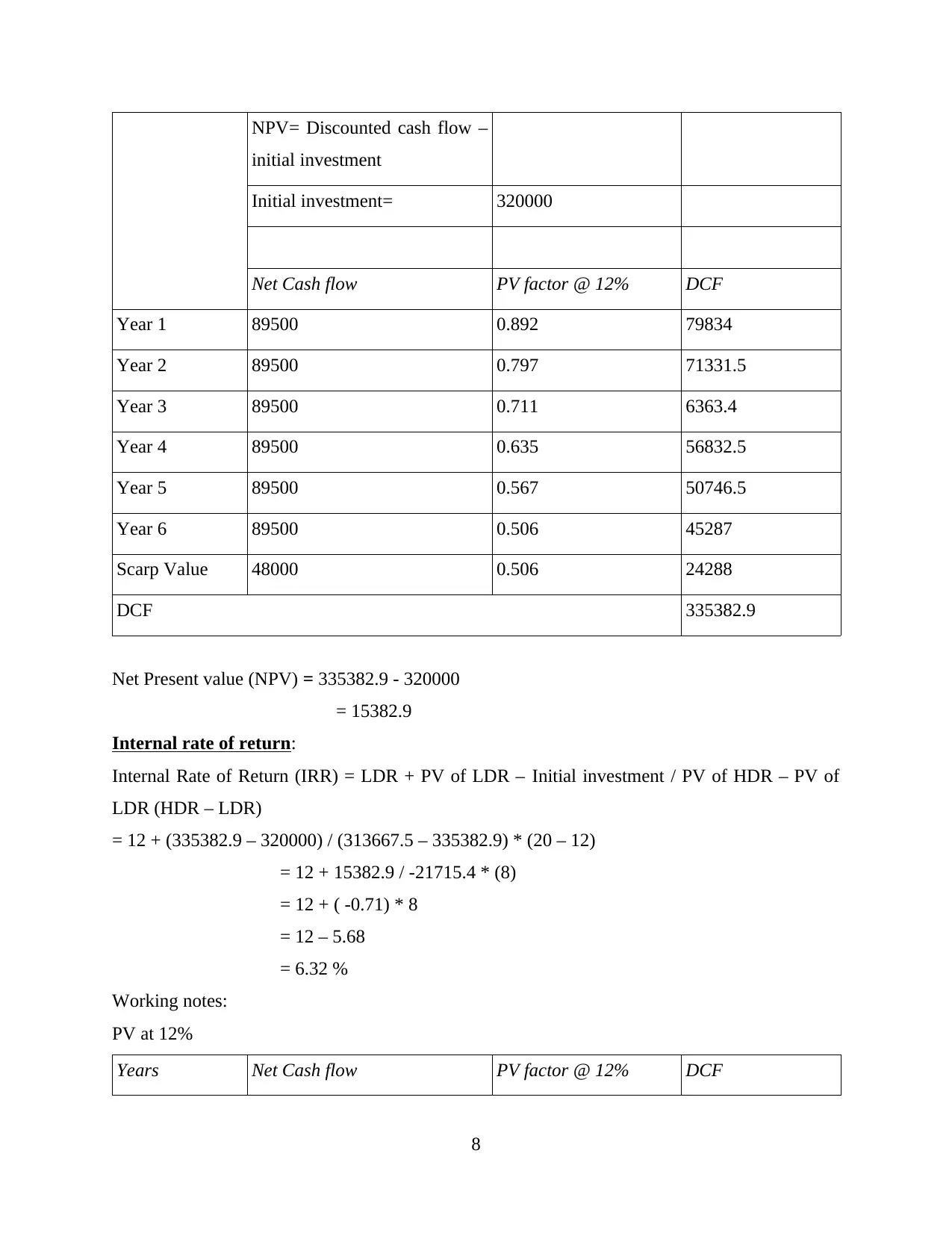

NPV= Discounted cash flow –

initial investment

Initial investment= 320000

Net Cash flow PV factor @ 12% DCF

Year 1 89500 0.892 79834

Year 2 89500 0.797 71331.5

Year 3 89500 0.711 6363.4

Year 4 89500 0.635 56832.5

Year 5 89500 0.567 50746.5

Year 6 89500 0.506 45287

Scarp Value 48000 0.506 24288

DCF 335382.9

Net Present value (NPV) = 335382.9 - 320000

= 15382.9

Internal rate of return:

Internal Rate of Return (IRR) = LDR + PV of LDR – Initial investment / PV of HDR – PV of

LDR (HDR – LDR)

= 12 + (335382.9 – 320000) / (313667.5 – 335382.9) * (20 – 12)

= 12 + 15382.9 / -21715.4 * (8)

= 12 + ( -0.71) * 8

= 12 – 5.68

= 6.32 %

Working notes:

PV at 12%

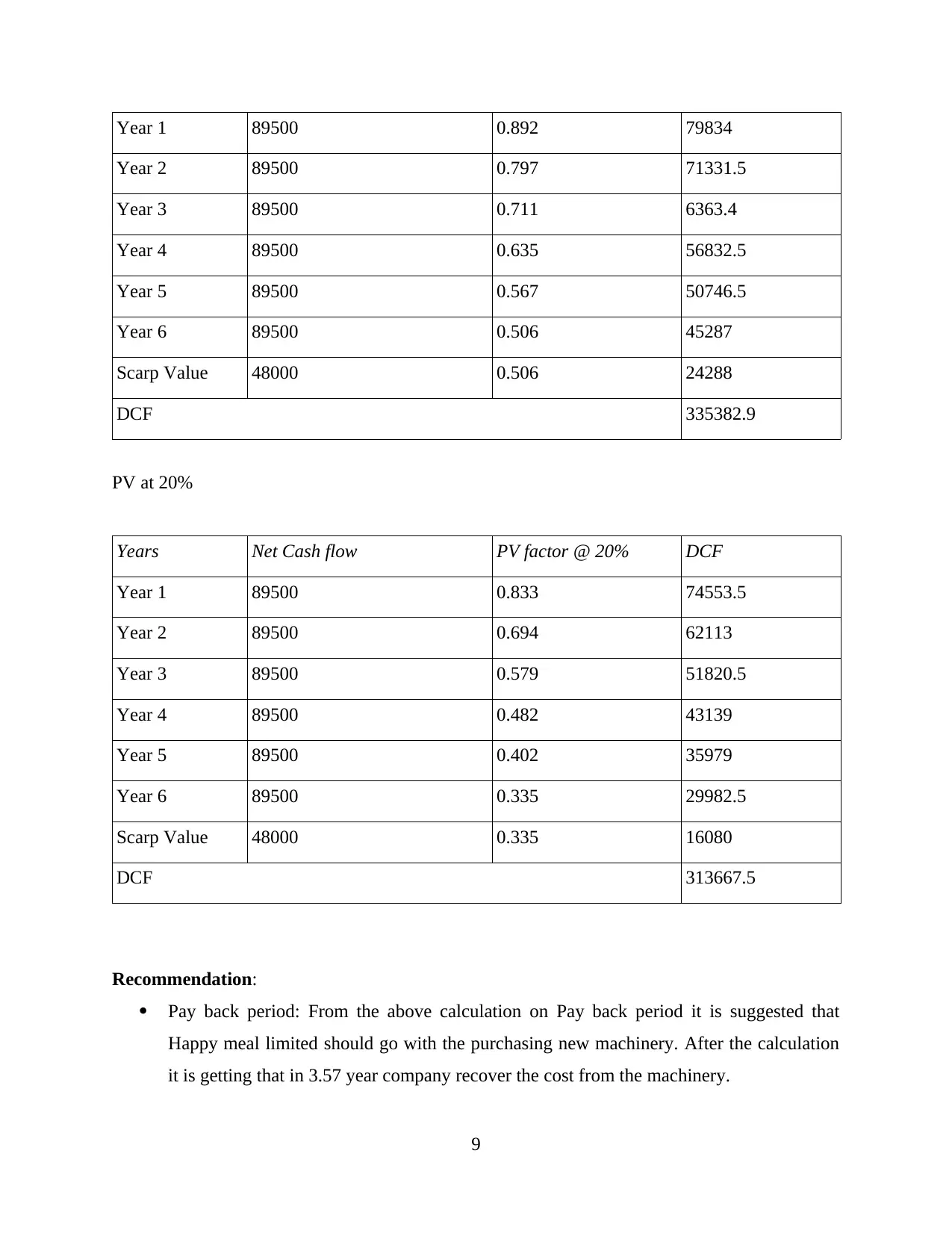

Years Net Cash flow PV factor @ 12% DCF

8

initial investment

Initial investment= 320000

Net Cash flow PV factor @ 12% DCF

Year 1 89500 0.892 79834

Year 2 89500 0.797 71331.5

Year 3 89500 0.711 6363.4

Year 4 89500 0.635 56832.5

Year 5 89500 0.567 50746.5

Year 6 89500 0.506 45287

Scarp Value 48000 0.506 24288

DCF 335382.9

Net Present value (NPV) = 335382.9 - 320000

= 15382.9

Internal rate of return:

Internal Rate of Return (IRR) = LDR + PV of LDR – Initial investment / PV of HDR – PV of

LDR (HDR – LDR)

= 12 + (335382.9 – 320000) / (313667.5 – 335382.9) * (20 – 12)

= 12 + 15382.9 / -21715.4 * (8)

= 12 + ( -0.71) * 8

= 12 – 5.68

= 6.32 %

Working notes:

PV at 12%

Years Net Cash flow PV factor @ 12% DCF

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 1 89500 0.892 79834

Year 2 89500 0.797 71331.5

Year 3 89500 0.711 6363.4

Year 4 89500 0.635 56832.5

Year 5 89500 0.567 50746.5

Year 6 89500 0.506 45287

Scarp Value 48000 0.506 24288

DCF 335382.9

PV at 20%

Years Net Cash flow PV factor @ 20% DCF

Year 1 89500 0.833 74553.5

Year 2 89500 0.694 62113

Year 3 89500 0.579 51820.5

Year 4 89500 0.482 43139

Year 5 89500 0.402 35979

Year 6 89500 0.335 29982.5

Scarp Value 48000 0.335 16080

DCF 313667.5

Recommendation:

Pay back period: From the above calculation on Pay back period it is suggested that

Happy meal limited should go with the purchasing new machinery. After the calculation

it is getting that in 3.57 year company recover the cost from the machinery.

9

Year 2 89500 0.797 71331.5

Year 3 89500 0.711 6363.4

Year 4 89500 0.635 56832.5

Year 5 89500 0.567 50746.5

Year 6 89500 0.506 45287

Scarp Value 48000 0.506 24288

DCF 335382.9

PV at 20%

Years Net Cash flow PV factor @ 20% DCF

Year 1 89500 0.833 74553.5

Year 2 89500 0.694 62113

Year 3 89500 0.579 51820.5

Year 4 89500 0.482 43139

Year 5 89500 0.402 35979

Year 6 89500 0.335 29982.5

Scarp Value 48000 0.335 16080

DCF 313667.5

Recommendation:

Pay back period: From the above calculation on Pay back period it is suggested that

Happy meal limited should go with the purchasing new machinery. After the calculation

it is getting that in 3.57 year company recover the cost from the machinery.

9

Accounting rate of return: As per the calculation the outcomes of ARR is 25.17% that is

greater and enough to recover cost of investment. Therefore, the Happy Meal limited

must purchase new machinery.

Net present value: As per the method when an organisation get results in position that

time must go with project otherwise not. In context of Happy Meal limited, new

machinery value as per net present value is 1582.9 Pounds. Thus, it is suggested that must

acquire the new machinery.

Internal rate of return: When company have higher internal rate of return so that time go

with the acquisition of new machinery. As per the calculation it is recommended that

company has 6.32% of recover cost of investment. Therefore, they must initiate to

purchase new machinery.

As per the above analysis it is suggested that Happy Meal limited must purchase new

machinery that will be beneficial in future.

(b) Benefits and limitations of each of differing investment appraisal techniques

Pay back period: It is capital budgeting techniques which is applied by the organisations

to calculate estimated period of time that occur in the procedure of recover cost of investment. It

is easy and simple method that can help to compute period of time in particular project. Such as,

Happy Meal limited wants to purchase new machine so for this apply this technique to calculate

the time period of recovery (Mitchell and Calabrese, 2019). There are mentioned benefits and

limitations of this technique such as:

Benefits

Simplicity: This technique is simple to use and easily understand all the calculations of

proposed projects. This method use by the manager with using of calculator and calculate

pay back period of a project.

Risk Focus: The analysis is concentrated on potential risk that arise in the future and

recover from investments. Therefore, the payback period utilised by the company to

compare different results by Payback period method.

Limitations

The payback method is not concentrating on value of money and ignores profitability of

the business entity.

10

greater and enough to recover cost of investment. Therefore, the Happy Meal limited

must purchase new machinery.

Net present value: As per the method when an organisation get results in position that

time must go with project otherwise not. In context of Happy Meal limited, new

machinery value as per net present value is 1582.9 Pounds. Thus, it is suggested that must

acquire the new machinery.

Internal rate of return: When company have higher internal rate of return so that time go

with the acquisition of new machinery. As per the calculation it is recommended that

company has 6.32% of recover cost of investment. Therefore, they must initiate to

purchase new machinery.

As per the above analysis it is suggested that Happy Meal limited must purchase new

machinery that will be beneficial in future.

(b) Benefits and limitations of each of differing investment appraisal techniques

Pay back period: It is capital budgeting techniques which is applied by the organisations

to calculate estimated period of time that occur in the procedure of recover cost of investment. It

is easy and simple method that can help to compute period of time in particular project. Such as,

Happy Meal limited wants to purchase new machine so for this apply this technique to calculate

the time period of recovery (Mitchell and Calabrese, 2019). There are mentioned benefits and

limitations of this technique such as:

Benefits

Simplicity: This technique is simple to use and easily understand all the calculations of

proposed projects. This method use by the manager with using of calculator and calculate

pay back period of a project.

Risk Focus: The analysis is concentrated on potential risk that arise in the future and

recover from investments. Therefore, the payback period utilised by the company to

compare different results by Payback period method.

Limitations

The payback method is not concentrating on value of money and ignores profitability of

the business entity.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.