Financial Management Exam: Costing, Variances, and Budgeting

VerifiedAdded on 2022/12/29

|11

|2512

|94

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Financial Management online exam. The solution begins by calculating the cost and profit per unit using both labor hour-based and Activity-Based Costing (ABC) approaches, followed by a critical evaluation of the two methods. The analysis includes detailed calculations and comparisons of the results. The solution then delves into variance analysis, calculating material usage, mix, and yield variances, and discusses the limitations of the current variance reporting system. The final section critically examines Zero-Based Budgeting (ZBB) and Incremental Budgeting (IB), evaluating their roles in planning, coordination, and control, and explaining why neither provides a perfect solution. The document provides detailed calculations and analysis for each question, offering a thorough understanding of the concepts covered in the exam.

Financial

Management

(online exam)

Management

(online exam)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

A) Calculate the cost (and hence the profit) per unit, absorbing all the overheads on the basis

of labour hours.............................................................................................................................1

B) Calculate the cost (and hence profit) per unit, absorbing the overheads using an Activity

Based Costing approach. .............................................................................................................1

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.................................................................................................3

d) Discuss how sensitivity analysis help managers to cope with uncertainties...........................4

QUESTION 2...................................................................................................................................4

A) Calculate the following variances for the last month:............................................................4

II) The total material Mix variance..............................................................................................5

III) The total material yield variance...........................................................................................5

B) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager................................................................5

QUESTION 3...................................................................................................................................6

Critically discussed why neither ZBB nor the IB provides the perfect toll for planning

coordination and control..............................................................................................................6

QUESTION 1...................................................................................................................................1

A) Calculate the cost (and hence the profit) per unit, absorbing all the overheads on the basis

of labour hours.............................................................................................................................1

B) Calculate the cost (and hence profit) per unit, absorbing the overheads using an Activity

Based Costing approach. .............................................................................................................1

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.................................................................................................3

d) Discuss how sensitivity analysis help managers to cope with uncertainties...........................4

QUESTION 2...................................................................................................................................4

A) Calculate the following variances for the last month:............................................................4

II) The total material Mix variance..............................................................................................5

III) The total material yield variance...........................................................................................5

B) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager................................................................5

QUESTION 3...................................................................................................................................6

Critically discussed why neither ZBB nor the IB provides the perfect toll for planning

coordination and control..............................................................................................................6

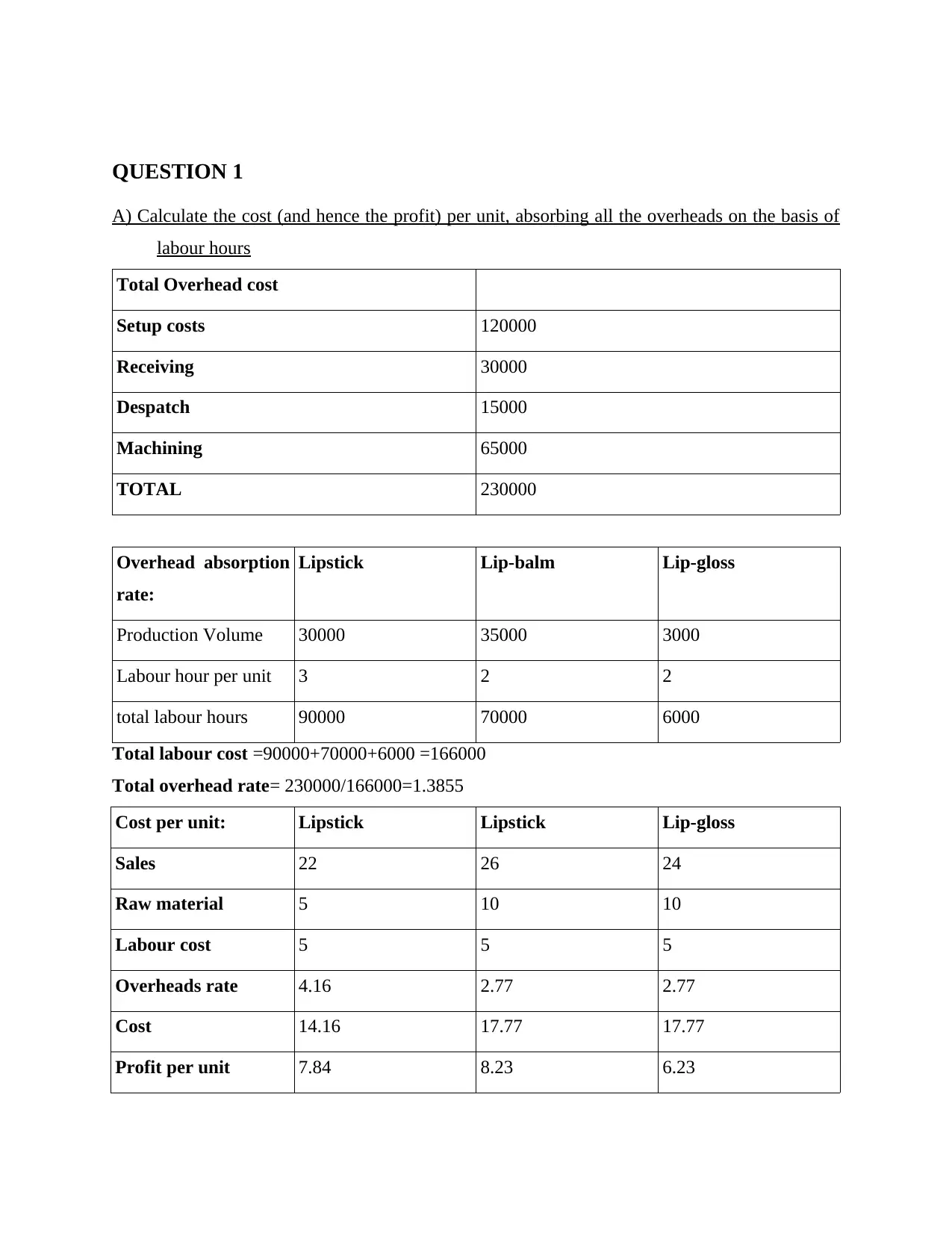

QUESTION 1

A) Calculate the cost (and hence the profit) per unit, absorbing all the overheads on the basis of

labour hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

TOTAL 230000

Overhead absorption

rate:

Lipstick Lip-balm Lip-gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

Total labour cost =90000+70000+6000 =166000

Total overhead rate= 230000/166000=1.3855

Cost per unit: Lipstick Lipstick Lip-gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

A) Calculate the cost (and hence the profit) per unit, absorbing all the overheads on the basis of

labour hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

TOTAL 230000

Overhead absorption

rate:

Lipstick Lip-balm Lip-gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

Total labour cost =90000+70000+6000 =166000

Total overhead rate= 230000/166000=1.3855

Cost per unit: Lipstick Lipstick Lip-gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

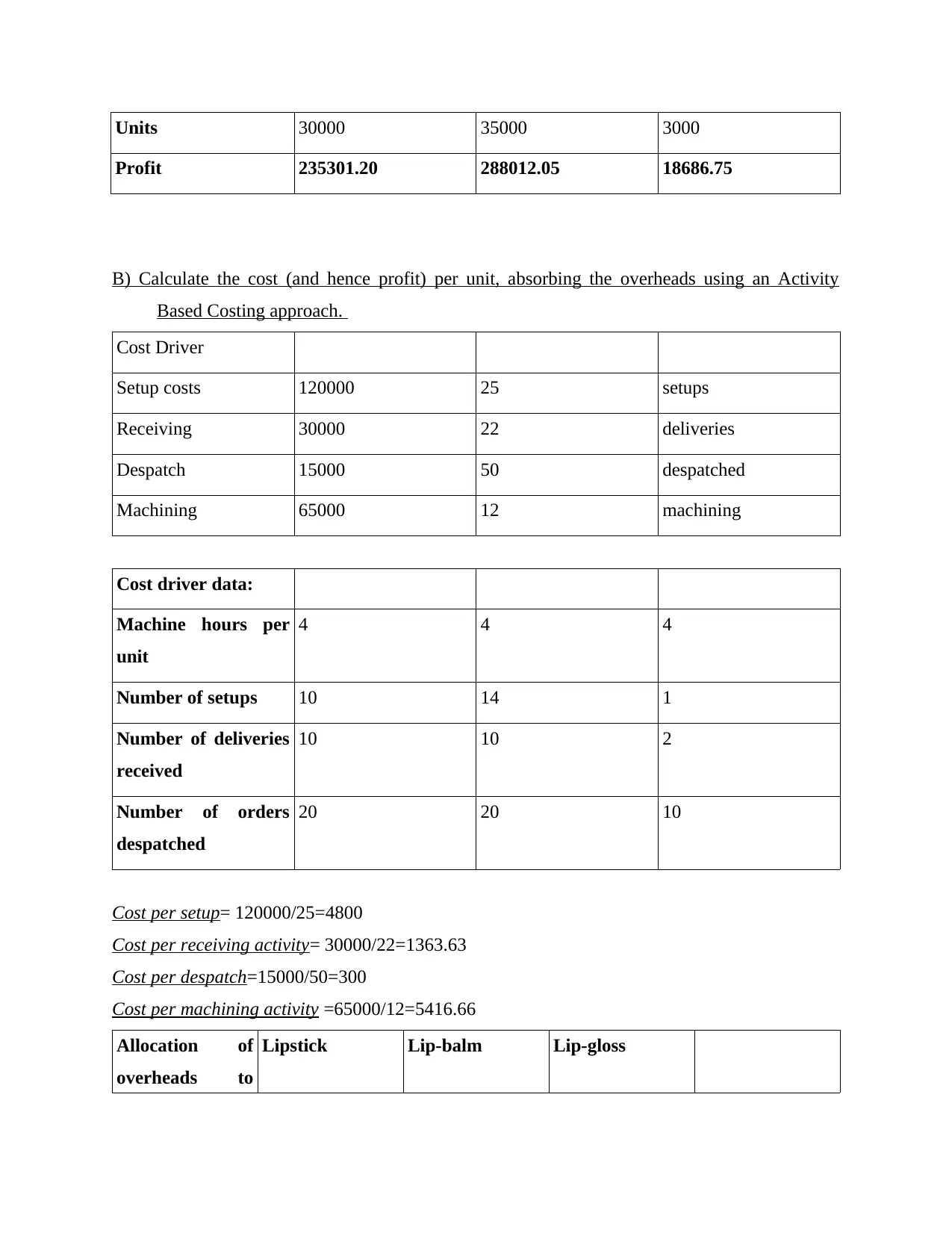

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

B) Calculate the cost (and hence profit) per unit, absorbing the overheads using an Activity

Based Costing approach.

Cost Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per

unit

4 4 4

Number of setups 10 14 1

Number of deliveries

received

10 10 2

Number of orders

despatched

20 20 10

Cost per setup= 120000/25=4800

Cost per receiving activity= 30000/22=1363.63

Cost per despatch=15000/50=300

Cost per machining activity =65000/12=5416.66

Allocation of

overheads to

Lipstick Lip-balm Lip-gloss

Profit 235301.20 288012.05 18686.75

B) Calculate the cost (and hence profit) per unit, absorbing the overheads using an Activity

Based Costing approach.

Cost Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per

unit

4 4 4

Number of setups 10 14 1

Number of deliveries

received

10 10 2

Number of orders

despatched

20 20 10

Cost per setup= 120000/25=4800

Cost per receiving activity= 30000/22=1363.63

Cost per despatch=15000/50=300

Cost per machining activity =65000/12=5416.66

Allocation of

overheads to

Lipstick Lip-balm Lip-gloss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

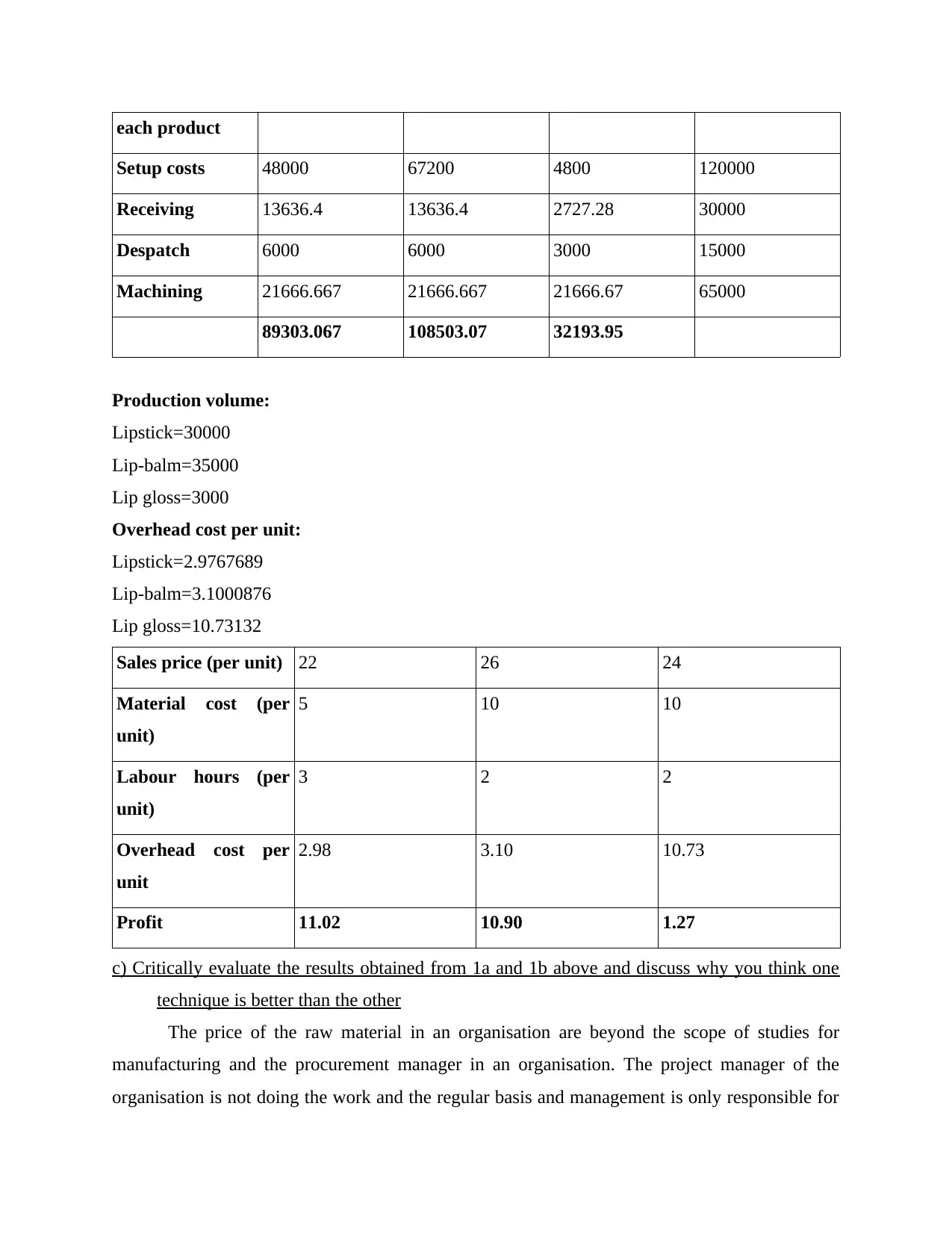

each product

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production volume:

Lipstick=30000

Lip-balm=35000

Lip gloss=3000

Overhead cost per unit:

Lipstick=2.9767689

Lip-balm=3.1000876

Lip gloss=10.73132

Sales price (per unit) 22 26 24

Material cost (per

unit)

5 10 10

Labour hours (per

unit)

3 2 2

Overhead cost per

unit

2.98 3.10 10.73

Profit 11.02 10.90 1.27

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other

The price of the raw material in an organisation are beyond the scope of studies for

manufacturing and the procurement manager in an organisation. The project manager of the

organisation is not doing the work and the regular basis and management is only responsible for

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production volume:

Lipstick=30000

Lip-balm=35000

Lip gloss=3000

Overhead cost per unit:

Lipstick=2.9767689

Lip-balm=3.1000876

Lip gloss=10.73132

Sales price (per unit) 22 26 24

Material cost (per

unit)

5 10 10

Labour hours (per

unit)

3 2 2

Overhead cost per

unit

2.98 3.10 10.73

Profit 11.02 10.90 1.27

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other

The price of the raw material in an organisation are beyond the scope of studies for

manufacturing and the procurement manager in an organisation. The project manager of the

organisation is not doing the work and the regular basis and management is only responsible for

the situation. The efficiency and the prices of the 3 materials are cannot be predict easily in an

organisation and helps in yielding the differences. The mixture of the substance is not improved

in the last five years. These two methods includes the specific approach and cost per units. The

difference rises is because of the absorption costs (Chandra, 2020). By observing all labour head

cost on the labour hours are the 7.84, 8.23, 6.23 and ABC profits are 11.02, 10.90, 1.27. The

considerations taken into the absorption cost are the fixed and the warehouse cost and the cost of

utility in factory. The basic cost cover is the direct material, direct labour and other expenses.

Absorption costing has the fixed production and the decisions are to be taken in an proper

manner. Weak valuation of the actual cost of an item is given by the absorption costing so the

decision-making are not taken properly. ABC costing helps in proper distribution of the overhead

so the decisions are to be taken in the proper manner. Once the cost get allocated it is used in

doing the operations. It also helps in minimizing the overhead cost in an organisation. In the

complicated situation Activity based costing performs well and the situation will be handled in

an proper manner. Various useful information are to be provided by the activity based costing.

The details would be accessible properly if there is proper collection of details in the each

decision-making. The structure is divided and the cost benefit study helps in providing the

benefit for the information so the decisions are to be taken in proper manner. From the above it

has been analysed that the ABC costing is useful for the comprehensive analysis.

d) Discuss how sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis helps in determining the the independent values and there impacts on

the dependent variables under the specific assumptions is called an sensitivity analysis. It helps

in response of the outcomes of model so that they can shift up into the input details so the

decisions are to be taken in proper manner and will not affect the organisation. Cash flows are

depend on the future predictions and if there is any mistake in the calculation the prediction will

get affected. If these are detected than it is the matter of concern for an organisation. These

measurement can be done easily by having the spreadsheet kits (Madura, 2020). It also helps in

determining how the independent variables an individual factors in the specific conditions. It

helps in targeting the parameters which are affected by the external changes are called the input

considerations. Testing variable and the qualitative parameters are to be evaluated in an proper

manner and the sensitivity test can be measured. It helps in determining the future values of the

assets so the decisions are to be taken in proper manner. It also shift the interest rates of the

organisation and helps in yielding the differences. The mixture of the substance is not improved

in the last five years. These two methods includes the specific approach and cost per units. The

difference rises is because of the absorption costs (Chandra, 2020). By observing all labour head

cost on the labour hours are the 7.84, 8.23, 6.23 and ABC profits are 11.02, 10.90, 1.27. The

considerations taken into the absorption cost are the fixed and the warehouse cost and the cost of

utility in factory. The basic cost cover is the direct material, direct labour and other expenses.

Absorption costing has the fixed production and the decisions are to be taken in an proper

manner. Weak valuation of the actual cost of an item is given by the absorption costing so the

decision-making are not taken properly. ABC costing helps in proper distribution of the overhead

so the decisions are to be taken in the proper manner. Once the cost get allocated it is used in

doing the operations. It also helps in minimizing the overhead cost in an organisation. In the

complicated situation Activity based costing performs well and the situation will be handled in

an proper manner. Various useful information are to be provided by the activity based costing.

The details would be accessible properly if there is proper collection of details in the each

decision-making. The structure is divided and the cost benefit study helps in providing the

benefit for the information so the decisions are to be taken in proper manner. From the above it

has been analysed that the ABC costing is useful for the comprehensive analysis.

d) Discuss how sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis helps in determining the the independent values and there impacts on

the dependent variables under the specific assumptions is called an sensitivity analysis. It helps

in response of the outcomes of model so that they can shift up into the input details so the

decisions are to be taken in proper manner and will not affect the organisation. Cash flows are

depend on the future predictions and if there is any mistake in the calculation the prediction will

get affected. If these are detected than it is the matter of concern for an organisation. These

measurement can be done easily by having the spreadsheet kits (Madura, 2020). It also helps in

determining how the independent variables an individual factors in the specific conditions. It

helps in targeting the parameters which are affected by the external changes are called the input

considerations. Testing variable and the qualitative parameters are to be evaluated in an proper

manner and the sensitivity test can be measured. It helps in determining the future values of the

assets so the decisions are to be taken in proper manner. It also shift the interest rates of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

bonds. Interest rates are independent and the value of the bonds are dependent. The reason of the

lower profit will be determined and has its impact on the net profit. Sensitivity will be easily

analysed so that the risk can be measured properly. It monitors the risky profile and help in

determining the proper output from the given input.

QUESTION 2

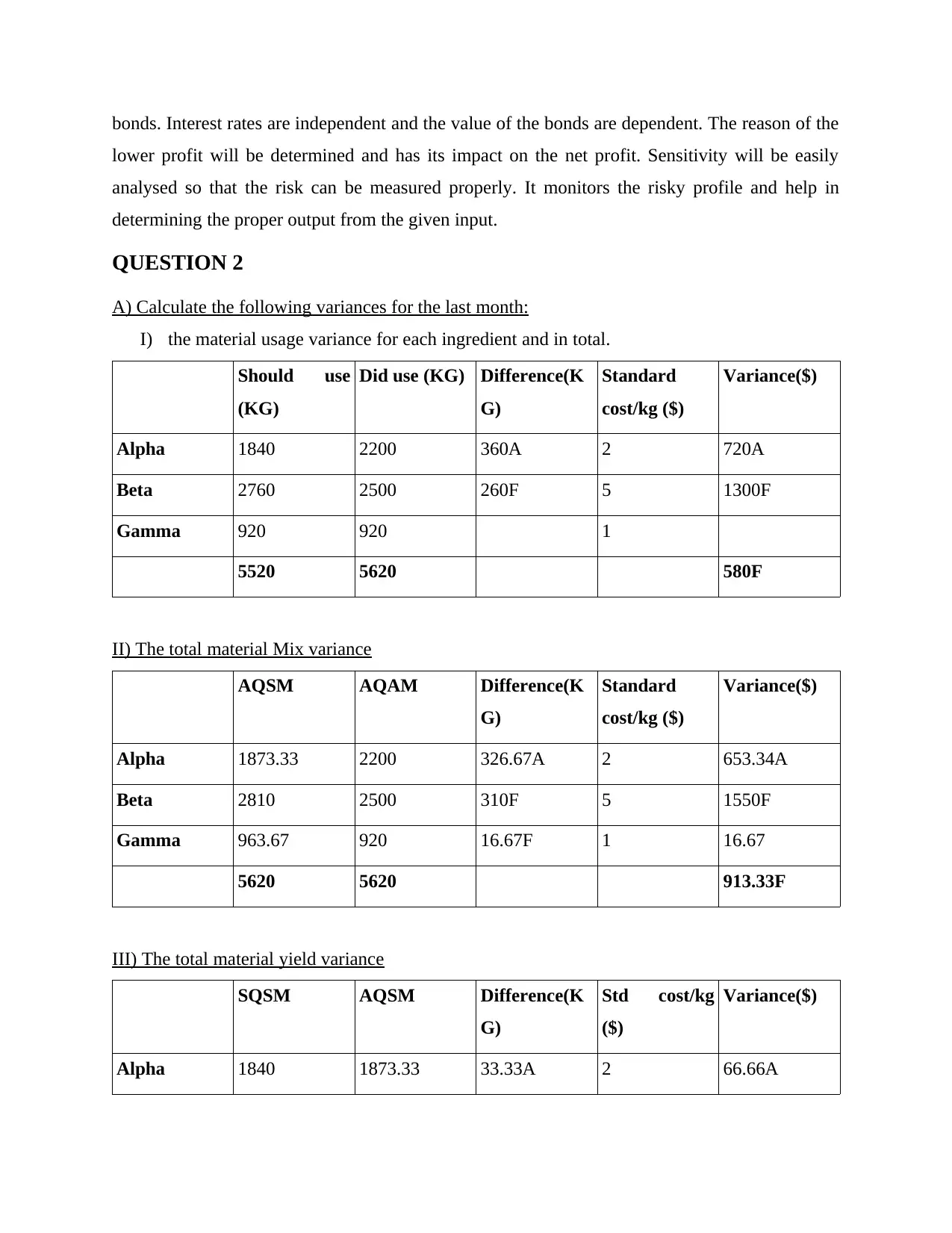

A) Calculate the following variances for the last month:

I) the material usage variance for each ingredient and in total.

Should use

(KG)

Did use (KG) Difference(K

G)

Standard

cost/kg ($)

Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

II) The total material Mix variance

AQSM AQAM Difference(K

G)

Standard

cost/kg ($)

Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

III) The total material yield variance

SQSM AQSM Difference(K

G)

Std cost/kg

($)

Variance($)

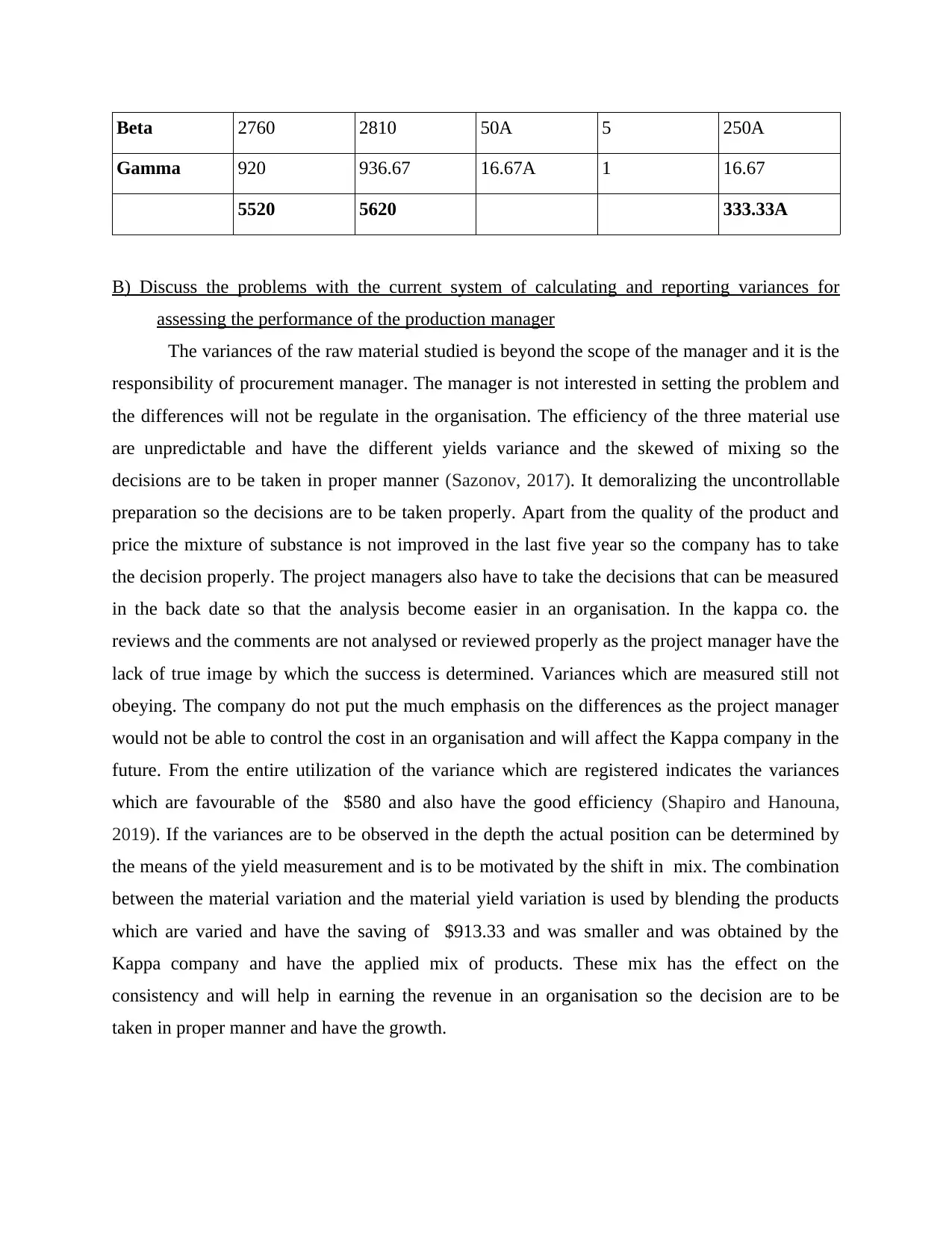

Alpha 1840 1873.33 33.33A 2 66.66A

lower profit will be determined and has its impact on the net profit. Sensitivity will be easily

analysed so that the risk can be measured properly. It monitors the risky profile and help in

determining the proper output from the given input.

QUESTION 2

A) Calculate the following variances for the last month:

I) the material usage variance for each ingredient and in total.

Should use

(KG)

Did use (KG) Difference(K

G)

Standard

cost/kg ($)

Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

II) The total material Mix variance

AQSM AQAM Difference(K

G)

Standard

cost/kg ($)

Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

III) The total material yield variance

SQSM AQSM Difference(K

G)

Std cost/kg

($)

Variance($)

Alpha 1840 1873.33 33.33A 2 66.66A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

B) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager

The variances of the raw material studied is beyond the scope of the manager and it is the

responsibility of procurement manager. The manager is not interested in setting the problem and

the differences will not be regulate in the organisation. The efficiency of the three material use

are unpredictable and have the different yields variance and the skewed of mixing so the

decisions are to be taken in proper manner (Sazonov, 2017). It demoralizing the uncontrollable

preparation so the decisions are to be taken properly. Apart from the quality of the product and

price the mixture of substance is not improved in the last five year so the company has to take

the decision properly. The project managers also have to take the decisions that can be measured

in the back date so that the analysis become easier in an organisation. In the kappa co. the

reviews and the comments are not analysed or reviewed properly as the project manager have the

lack of true image by which the success is determined. Variances which are measured still not

obeying. The company do not put the much emphasis on the differences as the project manager

would not be able to control the cost in an organisation and will affect the Kappa company in the

future. From the entire utilization of the variance which are registered indicates the variances

which are favourable of the $580 and also have the good efficiency (Shapiro and Hanouna,

2019). If the variances are to be observed in the depth the actual position can be determined by

the means of the yield measurement and is to be motivated by the shift in mix. The combination

between the material variation and the material yield variation is used by blending the products

which are varied and have the saving of $913.33 and was smaller and was obtained by the

Kappa company and have the applied mix of products. These mix has the effect on the

consistency and will help in earning the revenue in an organisation so the decision are to be

taken in proper manner and have the growth.

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

B) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager

The variances of the raw material studied is beyond the scope of the manager and it is the

responsibility of procurement manager. The manager is not interested in setting the problem and

the differences will not be regulate in the organisation. The efficiency of the three material use

are unpredictable and have the different yields variance and the skewed of mixing so the

decisions are to be taken in proper manner (Sazonov, 2017). It demoralizing the uncontrollable

preparation so the decisions are to be taken properly. Apart from the quality of the product and

price the mixture of substance is not improved in the last five year so the company has to take

the decision properly. The project managers also have to take the decisions that can be measured

in the back date so that the analysis become easier in an organisation. In the kappa co. the

reviews and the comments are not analysed or reviewed properly as the project manager have the

lack of true image by which the success is determined. Variances which are measured still not

obeying. The company do not put the much emphasis on the differences as the project manager

would not be able to control the cost in an organisation and will affect the Kappa company in the

future. From the entire utilization of the variance which are registered indicates the variances

which are favourable of the $580 and also have the good efficiency (Shapiro and Hanouna,

2019). If the variances are to be observed in the depth the actual position can be determined by

the means of the yield measurement and is to be motivated by the shift in mix. The combination

between the material variation and the material yield variation is used by blending the products

which are varied and have the saving of $913.33 and was smaller and was obtained by the

Kappa company and have the applied mix of products. These mix has the effect on the

consistency and will help in earning the revenue in an organisation so the decision are to be

taken in proper manner and have the growth.

QUESTION 3

Critically discussed why neither ZBB nor the IB provides the perfect toll for planning

coordination and control.

Zero-based budgeting method is used to make a budget from the start or from the zero

stage so the decisions are to be taken in proper manner. These are not dependent on the budgets

which are prepared earlier in an organisation. The cost will be explained properly before apply

the Zero-based budgeting methods for the financial planning so the decision is to be taken in

proper manner. The main aim of the zero-based budgeting method is that the expenditure get

minimised and cutting down of the cost where it is possible. It helps in spending the budget

which needs the priority as the distribution are made according to that only. This budgeting

method is used by the various organisation to start the budget from the zero so that the actual

position can be analysed regarding the expenses and the revenue and the person can start saving

if the profit rises.

Role of Zero-based budgeting in planning and coordination:

The top level priorities of the strategic are to be incorporated in the phase of the

budgeting which is mostly encouraged by the Zero based budgeting. These are connected to the

firms functional regions when the expenditure are grouped and helps ion analysing the past

performance of the company in an proper manner. IT helps in motivating the employees and

engage them in decision making so that the results can be analysed in an organisation. During the

planning the possible adjustment are also taken into account so that the decisions are to be taken

properly. If the mistake will not analysed of the past budget than it will have the impact on the

future budgets also and will affect the organisation so the efficiency is to be measured on the

regular basis. These types of errors are easily solved in the ZBB method.

Incremental budgeting is a budget which focused on the minor adjustments of the budget

that is existing and the deal can be created in proper manner. The actual budget is used for the

budgetary control so that the adjustments that occurred can be applied or get deducted so that the

new budgets can be performed from the base amounts (Siminica, Motoi and Dumitru, 2017).

This type of budgeting is the restrictive strategy of the financial planning. The best is the gradual

budgeting which helps in analysing the plan properly for the present period so the future plan can

be estimated properly in an organisation. It is flexible and helps in saving the time in the

Critically discussed why neither ZBB nor the IB provides the perfect toll for planning

coordination and control.

Zero-based budgeting method is used to make a budget from the start or from the zero

stage so the decisions are to be taken in proper manner. These are not dependent on the budgets

which are prepared earlier in an organisation. The cost will be explained properly before apply

the Zero-based budgeting methods for the financial planning so the decision is to be taken in

proper manner. The main aim of the zero-based budgeting method is that the expenditure get

minimised and cutting down of the cost where it is possible. It helps in spending the budget

which needs the priority as the distribution are made according to that only. This budgeting

method is used by the various organisation to start the budget from the zero so that the actual

position can be analysed regarding the expenses and the revenue and the person can start saving

if the profit rises.

Role of Zero-based budgeting in planning and coordination:

The top level priorities of the strategic are to be incorporated in the phase of the

budgeting which is mostly encouraged by the Zero based budgeting. These are connected to the

firms functional regions when the expenditure are grouped and helps ion analysing the past

performance of the company in an proper manner. IT helps in motivating the employees and

engage them in decision making so that the results can be analysed in an organisation. During the

planning the possible adjustment are also taken into account so that the decisions are to be taken

properly. If the mistake will not analysed of the past budget than it will have the impact on the

future budgets also and will affect the organisation so the efficiency is to be measured on the

regular basis. These types of errors are easily solved in the ZBB method.

Incremental budgeting is a budget which focused on the minor adjustments of the budget

that is existing and the deal can be created in proper manner. The actual budget is used for the

budgetary control so that the adjustments that occurred can be applied or get deducted so that the

new budgets can be performed from the base amounts (Siminica, Motoi and Dumitru, 2017).

This type of budgeting is the restrictive strategy of the financial planning. The best is the gradual

budgeting which helps in analysing the plan properly for the present period so the future plan can

be estimated properly in an organisation. It is flexible and helps in saving the time in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budgetary control and the decision are to be taken properly so that the efficiency can be

measured.

Role of Incremental budgeting in planning and coordination:

It is a budgetary method which helps in demonstrating the budgetary plan in an proper

manner so that the plan can be implemented, evaluated and monitored in an proper manner so

that the outcomes can be achieved properly in an organisation. The sudden crises of the company

will also stop. IT is an idea which is used to prepare the new budget by having the minor

adjustments in the existing budget. Incremental sums are used to meet the latest budgets. The

strategy used in the cumulative budgeting which helps the premise to accumulate the cost from

the starting only (Yuniningsih, Pertiwi and Purwanto, 2019). The positives and the negatives

helps in understanding the notion in the proper manner. The framework of the present budget is

used for spending this allocation for the next year. The analyst preparing the budget will spend it

on the regular basis but if the amount left then it will be spend in the next year and the decision

becomes easier.

measured.

Role of Incremental budgeting in planning and coordination:

It is a budgetary method which helps in demonstrating the budgetary plan in an proper

manner so that the plan can be implemented, evaluated and monitored in an proper manner so

that the outcomes can be achieved properly in an organisation. The sudden crises of the company

will also stop. IT is an idea which is used to prepare the new budget by having the minor

adjustments in the existing budget. Incremental sums are used to meet the latest budgets. The

strategy used in the cumulative budgeting which helps the premise to accumulate the cost from

the starting only (Yuniningsih, Pertiwi and Purwanto, 2019). The positives and the negatives

helps in understanding the notion in the proper manner. The framework of the present budget is

used for spending this allocation for the next year. The analyst preparing the budget will spend it

on the regular basis but if the amount left then it will be spend in the next year and the decision

becomes easier.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Chandra, P., 2020. Fundamentals of Financial Management. McGraw-Hill Education.

Madura, J., 2020. International financial management. Cengage Learning.

Sazonov, S. and et. al., 2017. Theory and methodology of the financial management of the

regional supporting university. J. Advanced Res. L. & Econ. 8. p.211.

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley & Sons.

Siminica, M., Motoi, A. G. and Dumitru, A., 2017. Financial management as component of

tactical management. Polish Journal of Management Studies. 15.

Yuniningsih, Y., Pertiwi, T. and Purwanto, E., 2019. Fundamental factor of financial

management in determining company values. Management Science Letters. 9(2).

pp.205-216

Books & Journals

Chandra, P., 2020. Fundamentals of Financial Management. McGraw-Hill Education.

Madura, J., 2020. International financial management. Cengage Learning.

Sazonov, S. and et. al., 2017. Theory and methodology of the financial management of the

regional supporting university. J. Advanced Res. L. & Econ. 8. p.211.

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley & Sons.

Siminica, M., Motoi, A. G. and Dumitru, A., 2017. Financial management as component of

tactical management. Polish Journal of Management Studies. 15.

Yuniningsih, Y., Pertiwi, T. and Purwanto, E., 2019. Fundamental factor of financial

management in determining company values. Management Science Letters. 9(2).

pp.205-216

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.