APC308 Financial Management Assignment: Equity and Investment

VerifiedAdded on 2023/01/16

|17

|4292

|82

Homework Assignment

AI Summary

This financial management assignment solution provides a comprehensive analysis of key financial concepts. It begins with an introduction to financial management and its importance in the current business environment, emphasizing strategic planning and resource allocation. The main body addresses two key questions. Question 2(a) delves into long-term finance, specifically equity finance, analyzing the issuance of right shares and evaluating different right issue prices. The solution calculates the number of shares to be issued, the theoretical ex-rights price, and the anticipated earnings per share (EPS) under various scenarios. It then evaluates the best right issue option based on the analysis. Question 2(c) evaluates the benefits of scrip dividends for both shareholders and companies, discussing advantages like maintaining cash positions and tax benefits. Question 3 focuses on investment appraisal techniques, including the payback period and accounting rate of return (ARR). The solution provides formulas and calculations for both, illustrating their application in evaluating investment viability. The assignment concludes with a summary of the key findings and insights.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 2...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

(c) Evaluate the benefits of scrip divided in context of shareholders or companies...................4

QUESTION 3...................................................................................................................................5

a. Investment appraisal technique...............................................................................................5

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 2...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

(c) Evaluate the benefits of scrip divided in context of shareholders or companies...................4

QUESTION 3...................................................................................................................................5

a. Investment appraisal technique...............................................................................................5

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the current business atmosphere, it is recognized as financial management to handle

and monitor each financial event over a specified period of time. There's a necessity to monitor

and allocate fiscal resources across every form of enterprise in attempt to perform out the

intended operation in most efficient way to enhance the overall profits. This is categorized as a

sort of tactics best linked to financial practices, planning, leadership and strategic planning. It

emphasizes simply on percentage growth and obligations as it makes it possible to efficiently

manage the strategic plan. Furthermore, all forms of businesses require this to manage the

funding and financial resources (Shapiro and Hanouna, 2019).

Key strategic decisions are being made in this study to render critically important

decisions, crucial comprehension of specific analytical skills are discussed to make decisions at

international scale. Furthermore, constraints of the present state regarding financial theories are

developed which make much better business decisions.

MAIN BODY

QUESTION 2

(a) Long term finance: Equity finance.

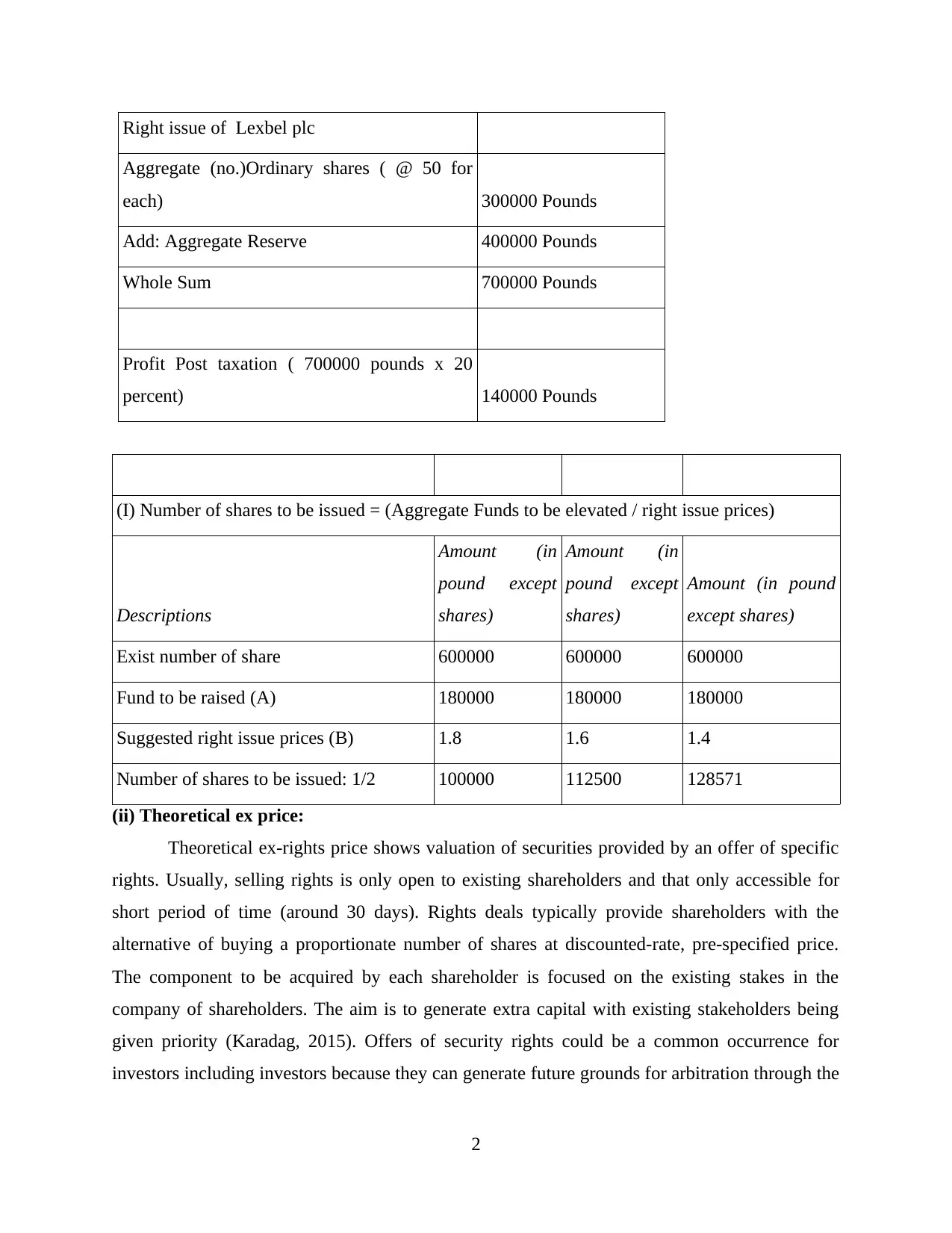

(A) Issue of Right share: Rights issue implies to offering of rights to company's current

shareholders which allows them to purchase added securities directly from corporation at a

discounted rate instead of buy shares on secondary market. The total of extra securities to be

purchased relies on the shareholders ' existing holdings. Rights issue offers present shareholders

preferential attention where they have the legal ability like right (not the ethical responsibility) to

buy shares at cheaper price before or on a specific date (Brigham and Houston, 2012). Here in

this context Lexbel plc wants to issue right shares among existing shareholders with aim to fulfil

their funding requirements. In this context following are calculations to assess the number of

right share that company can issue based on their existing profits and capital structure, as

follows:

Lexbel plc wishes to rise: 180000GBP

Current ex-dividend market-price of Lexbel plc: 1.90GBP

3 assorted rights-issue prices recommended by corporation's finance director: GBP1.80,

GBP1.60 and GBP1.40

1

In the current business atmosphere, it is recognized as financial management to handle

and monitor each financial event over a specified period of time. There's a necessity to monitor

and allocate fiscal resources across every form of enterprise in attempt to perform out the

intended operation in most efficient way to enhance the overall profits. This is categorized as a

sort of tactics best linked to financial practices, planning, leadership and strategic planning. It

emphasizes simply on percentage growth and obligations as it makes it possible to efficiently

manage the strategic plan. Furthermore, all forms of businesses require this to manage the

funding and financial resources (Shapiro and Hanouna, 2019).

Key strategic decisions are being made in this study to render critically important

decisions, crucial comprehension of specific analytical skills are discussed to make decisions at

international scale. Furthermore, constraints of the present state regarding financial theories are

developed which make much better business decisions.

MAIN BODY

QUESTION 2

(a) Long term finance: Equity finance.

(A) Issue of Right share: Rights issue implies to offering of rights to company's current

shareholders which allows them to purchase added securities directly from corporation at a

discounted rate instead of buy shares on secondary market. The total of extra securities to be

purchased relies on the shareholders ' existing holdings. Rights issue offers present shareholders

preferential attention where they have the legal ability like right (not the ethical responsibility) to

buy shares at cheaper price before or on a specific date (Brigham and Houston, 2012). Here in

this context Lexbel plc wants to issue right shares among existing shareholders with aim to fulfil

their funding requirements. In this context following are calculations to assess the number of

right share that company can issue based on their existing profits and capital structure, as

follows:

Lexbel plc wishes to rise: 180000GBP

Current ex-dividend market-price of Lexbel plc: 1.90GBP

3 assorted rights-issue prices recommended by corporation's finance director: GBP1.80,

GBP1.60 and GBP1.40

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Right issue of Lexbel plc

Aggregate (no.)Ordinary shares ( @ 50 for

each) 300000 Pounds

Add: Aggregate Reserve 400000 Pounds

Whole Sum 700000 Pounds

Profit Post taxation ( 700000 pounds x 20

percent) 140000 Pounds

(I) Number of shares to be issued = (Aggregate Funds to be elevated / right issue prices)

Descriptions

Amount (in

pound except

shares)

Amount (in

pound except

shares)

Amount (in pound

except shares)

Exist number of share 600000 600000 600000

Fund to be raised (A) 180000 180000 180000

Suggested right issue prices (B) 1.8 1.6 1.4

Number of shares to be issued: 1/2 100000 112500 128571

(ii) Theoretical ex price:

Theoretical ex-rights price shows valuation of securities provided by an offer of specific

rights. Usually, selling rights is only open to existing shareholders and that only accessible for

short period of time (around 30 days). Rights deals typically provide shareholders with the

alternative of buying a proportionate number of shares at discounted-rate, pre-specified price.

The component to be acquired by each shareholder is focused on the existing stakes in the

company of shareholders. The aim is to generate extra capital with existing stakeholders being

given priority (Karadag, 2015). Offers of security rights could be a common occurrence for

investors including investors because they can generate future grounds for arbitration through the

2

Aggregate (no.)Ordinary shares ( @ 50 for

each) 300000 Pounds

Add: Aggregate Reserve 400000 Pounds

Whole Sum 700000 Pounds

Profit Post taxation ( 700000 pounds x 20

percent) 140000 Pounds

(I) Number of shares to be issued = (Aggregate Funds to be elevated / right issue prices)

Descriptions

Amount (in

pound except

shares)

Amount (in

pound except

shares)

Amount (in pound

except shares)

Exist number of share 600000 600000 600000

Fund to be raised (A) 180000 180000 180000

Suggested right issue prices (B) 1.8 1.6 1.4

Number of shares to be issued: 1/2 100000 112500 128571

(ii) Theoretical ex price:

Theoretical ex-rights price shows valuation of securities provided by an offer of specific

rights. Usually, selling rights is only open to existing shareholders and that only accessible for

short period of time (around 30 days). Rights deals typically provide shareholders with the

alternative of buying a proportionate number of shares at discounted-rate, pre-specified price.

The component to be acquired by each shareholder is focused on the existing stakes in the

company of shareholders. The aim is to generate extra capital with existing stakeholders being

given priority (Karadag, 2015). Offers of security rights could be a common occurrence for

investors including investors because they can generate future grounds for arbitration through the

2

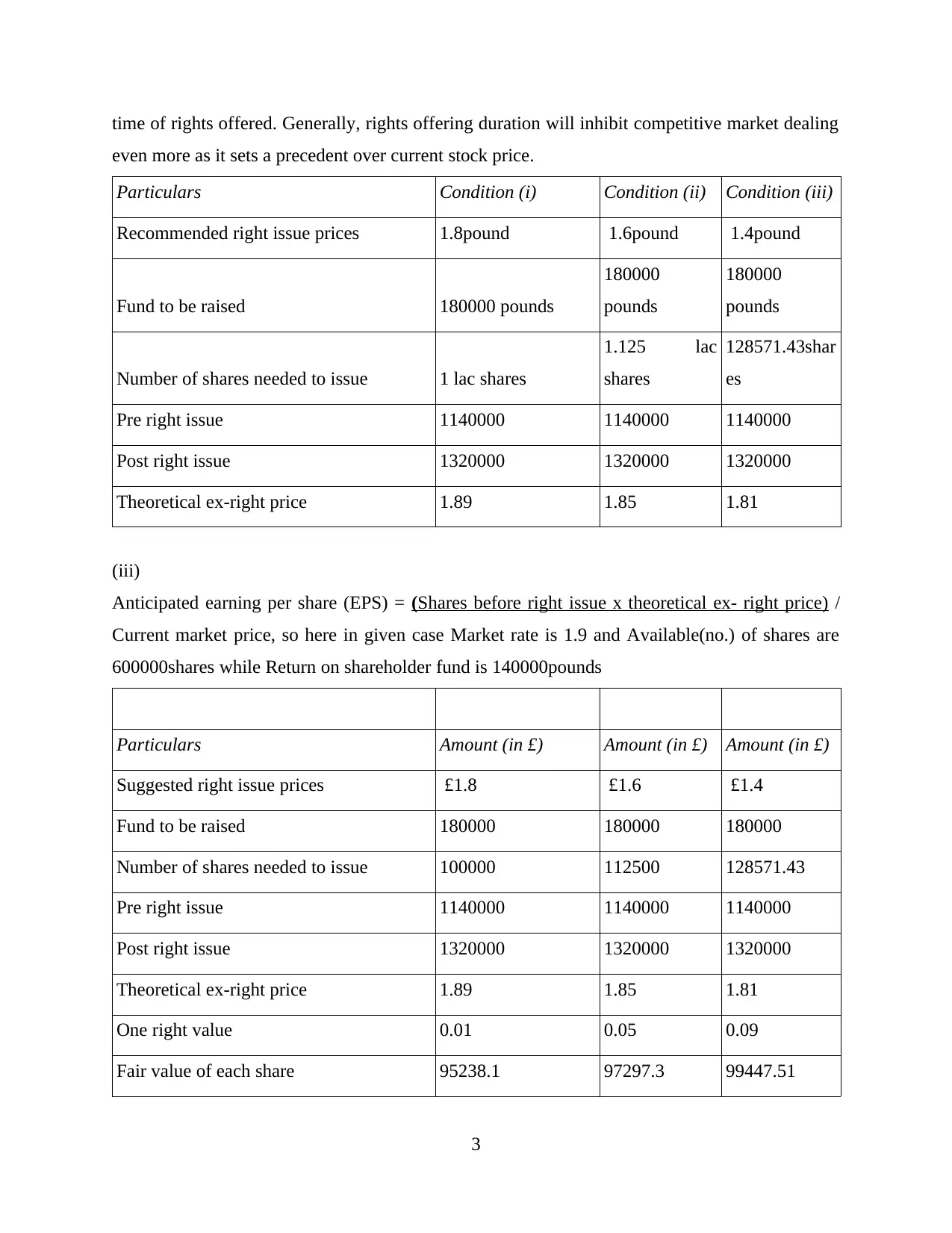

time of rights offered. Generally, rights offering duration will inhibit competitive market dealing

even more as it sets a precedent over current stock price.

Particulars Condition (i) Condition (ii) Condition (iii)

Recommended right issue prices 1.8pound 1.6pound 1.4pound

Fund to be raised 180000 pounds

180000

pounds

180000

pounds

Number of shares needed to issue 1 lac shares

1.125 lac

shares

128571.43shar

es

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex-right price 1.89 1.85 1.81

(iii)

Anticipated earning per share (EPS) = (Shares before right issue x theoretical ex- right price) /

Current market price, so here in given case Market rate is 1.9 and Available(no.) of shares are

600000shares while Return on shareholder fund is 140000pounds

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue prices £1.8 £1.6 £1.4

Fund to be raised 180000 180000 180000

Number of shares needed to issue 100000 112500 128571.43

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex-right price 1.89 1.85 1.81

One right value 0.01 0.05 0.09

Fair value of each share 95238.1 97297.3 99447.51

3

even more as it sets a precedent over current stock price.

Particulars Condition (i) Condition (ii) Condition (iii)

Recommended right issue prices 1.8pound 1.6pound 1.4pound

Fund to be raised 180000 pounds

180000

pounds

180000

pounds

Number of shares needed to issue 1 lac shares

1.125 lac

shares

128571.43shar

es

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex-right price 1.89 1.85 1.81

(iii)

Anticipated earning per share (EPS) = (Shares before right issue x theoretical ex- right price) /

Current market price, so here in given case Market rate is 1.9 and Available(no.) of shares are

600000shares while Return on shareholder fund is 140000pounds

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue prices £1.8 £1.6 £1.4

Fund to be raised 180000 180000 180000

Number of shares needed to issue 100000 112500 128571.43

Pre right issue 1140000 1140000 1140000

Post right issue 1320000 1320000 1320000

Theoretical ex-right price 1.89 1.85 1.81

One right value 0.01 0.05 0.09

Fair value of each share 95238.1 97297.3 99447.51

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

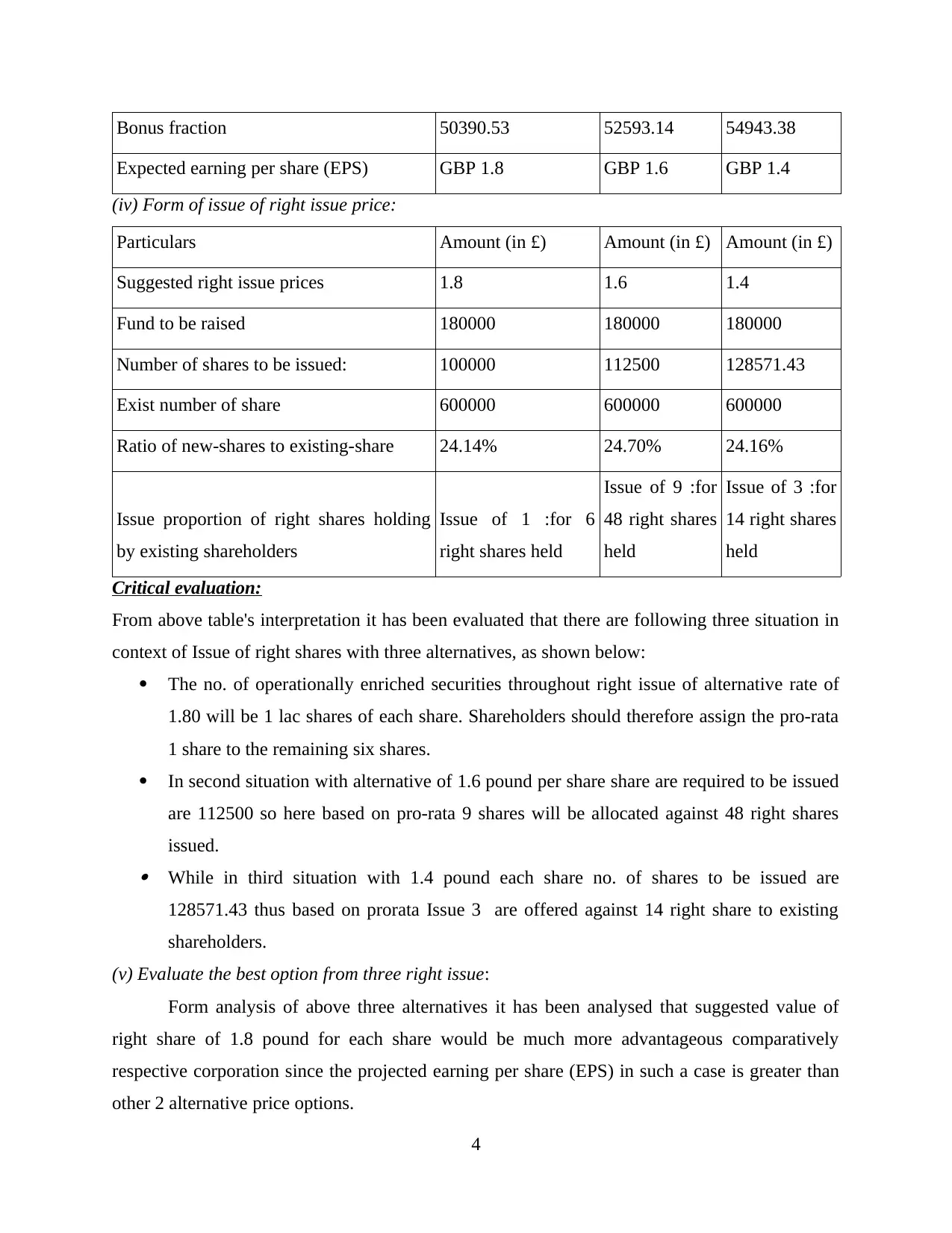

Bonus fraction 50390.53 52593.14 54943.38

Expected earning per share (EPS) GBP 1.8 GBP 1.6 GBP 1.4

(iv) Form of issue of right issue price:

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue prices 1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares to be issued: 100000 112500 128571.43

Exist number of share 600000 600000 600000

Ratio of new-shares to existing-share 24.14% 24.70% 24.16%

Issue proportion of right shares holding

by existing shareholders

Issue of 1 :for 6

right shares held

Issue of 9 :for

48 right shares

held

Issue of 3 :for

14 right shares

held

Critical evaluation:

From above table's interpretation it has been evaluated that there are following three situation in

context of Issue of right shares with three alternatives, as shown below:

The no. of operationally enriched securities throughout right issue of alternative rate of

1.80 will be 1 lac shares of each share. Shareholders should therefore assign the pro-rata

1 share to the remaining six shares.

In second situation with alternative of 1.6 pound per share share are required to be issued

are 112500 so here based on pro-rata 9 shares will be allocated against 48 right shares

issued. While in third situation with 1.4 pound each share no. of shares to be issued are

128571.43 thus based on prorata Issue 3 are offered against 14 right share to existing

shareholders.

(v) Evaluate the best option from three right issue:

Form analysis of above three alternatives it has been analysed that suggested value of

right share of 1.8 pound for each share would be much more advantageous comparatively

respective corporation since the projected earning per share (EPS) in such a case is greater than

other 2 alternative price options.

4

Expected earning per share (EPS) GBP 1.8 GBP 1.6 GBP 1.4

(iv) Form of issue of right issue price:

Particulars Amount (in £) Amount (in £) Amount (in £)

Suggested right issue prices 1.8 1.6 1.4

Fund to be raised 180000 180000 180000

Number of shares to be issued: 100000 112500 128571.43

Exist number of share 600000 600000 600000

Ratio of new-shares to existing-share 24.14% 24.70% 24.16%

Issue proportion of right shares holding

by existing shareholders

Issue of 1 :for 6

right shares held

Issue of 9 :for

48 right shares

held

Issue of 3 :for

14 right shares

held

Critical evaluation:

From above table's interpretation it has been evaluated that there are following three situation in

context of Issue of right shares with three alternatives, as shown below:

The no. of operationally enriched securities throughout right issue of alternative rate of

1.80 will be 1 lac shares of each share. Shareholders should therefore assign the pro-rata

1 share to the remaining six shares.

In second situation with alternative of 1.6 pound per share share are required to be issued

are 112500 so here based on pro-rata 9 shares will be allocated against 48 right shares

issued. While in third situation with 1.4 pound each share no. of shares to be issued are

128571.43 thus based on prorata Issue 3 are offered against 14 right share to existing

shareholders.

(v) Evaluate the best option from three right issue:

Form analysis of above three alternatives it has been analysed that suggested value of

right share of 1.8 pound for each share would be much more advantageous comparatively

respective corporation since the projected earning per share (EPS) in such a case is greater than

other 2 alternative price options.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(c) Evaluate the benefits of scrip divided in context of shareholders or companies

Scrip dividend: Scrip dividend defined as new stock for a corporation issued to

stockholders rather than a normal dividend. As company who issue have much little cash

accessible to issue cash dividend, a scrip dividends could be used, but they still need to charge

their stakeholders somehow. Shareholders might also be given scrip dividends as just an option

to monetary dividend in order to gradually carry out their dividend payouts into even more

shares. The downside for stakeholders is that if they acquire new securities, they don't have to

bear any transaction costs, like commission. It is also a substantial way of saving money by not

having to pay cash dividend payments for stock issuer. Scrip dividends linked to common shares

help the distributing entity to maintain and encourage shareholders to raise their investment in

the corporation. not only does this reduce costs of purchasing stock options, but it could also

offer a tax deduction for the shareholder. For instance, rather than earnings, the shareholder

realizes capital gain. The capital gain can be taxed at reduced percentage than regular dividends.

The company utilise this strategy when it has to pay-out their inventors, since they don't have

enough funds for it. This refers primarily to the freshly generated securities compared to existing

securities (Burtonshaw-Gunn, 2017). In many situations, it'll be viewed as a category of debt that

has certain advantages as well as pitfalls in both the company and the investors. Additional

assessment discussed below:

Benefits of Scrip dividend:

In context of company:

This aid in maintaining corporation's cash-funds position as here in this kind of dividend

mostly shareholders go with the option of shares. Due to this company's cash funds as

well as equity increase.

Due to issuance of shares under option of scrip dividend, company's leveraging and

gearing position may improve which leads to enhancement in overall borrowing capacity

of corporation.

A corporation with higher brand value and good market position, can issue this type of

dividend even with limited cash funds if company ensure that most of the go with share

alternative.

5

Scrip dividend: Scrip dividend defined as new stock for a corporation issued to

stockholders rather than a normal dividend. As company who issue have much little cash

accessible to issue cash dividend, a scrip dividends could be used, but they still need to charge

their stakeholders somehow. Shareholders might also be given scrip dividends as just an option

to monetary dividend in order to gradually carry out their dividend payouts into even more

shares. The downside for stakeholders is that if they acquire new securities, they don't have to

bear any transaction costs, like commission. It is also a substantial way of saving money by not

having to pay cash dividend payments for stock issuer. Scrip dividends linked to common shares

help the distributing entity to maintain and encourage shareholders to raise their investment in

the corporation. not only does this reduce costs of purchasing stock options, but it could also

offer a tax deduction for the shareholder. For instance, rather than earnings, the shareholder

realizes capital gain. The capital gain can be taxed at reduced percentage than regular dividends.

The company utilise this strategy when it has to pay-out their inventors, since they don't have

enough funds for it. This refers primarily to the freshly generated securities compared to existing

securities (Burtonshaw-Gunn, 2017). In many situations, it'll be viewed as a category of debt that

has certain advantages as well as pitfalls in both the company and the investors. Additional

assessment discussed below:

Benefits of Scrip dividend:

In context of company:

This aid in maintaining corporation's cash-funds position as here in this kind of dividend

mostly shareholders go with the option of shares. Due to this company's cash funds as

well as equity increase.

Due to issuance of shares under option of scrip dividend, company's leveraging and

gearing position may improve which leads to enhancement in overall borrowing capacity

of corporation.

A corporation with higher brand value and good market position, can issue this type of

dividend even with limited cash funds if company ensure that most of the go with share

alternative.

5

Another advantageous thing here is that smaller scrip dividend issuance generally not

dilutes company's share price majorly. Although where company is not offering cash as

an alternate, experiential grounds proposes that shares' price will be fall. It also a significant source of finance and funding due to option of shares against

dividend.

In context of shareholders:

Most prime advantage for shareholders, of a scrip dividend is that they can get tax

advantages by adopting the option/alternative of shares.

Shareholder who have desire to make an increase in their shareholding in company this

dividend is beneficial as they can enhance shareholding without any additional

transaction costs.

Share option in scrip dividend may provide a greater monetary benefits as compare to

cash dividend so mostly shareholders wants to get scrip dividend.

QUESTION 3

a. Investment appraisal technique

(I) Payback Period:

This is a capital budgeting technique that is meant to assess the new

investment's viability and to support the individual decision of selection of most appropriate

investment alternative. Payback period defined as specific duration over which the company will

reimburse the amount of money invested. Minimal payback duration is advantageous to the

organization as it allows to retrieve initial investment and commence to generate yields on it. It

allows managers to assess whether investment made on any option is capable to return back

within a reasonable period. Payback period is mandated to recuperate negative

project/venture cash from the purchase and/or initial years for positive project/venture cash flow.

Payback may be measured either from beginning of a proposal or from beginning of production

process. Payback periods are usually measured on the basis of undiscounted cash-flows, but it

may even be estimated at minimum return rate(%) for Discounted Cash Flows (Arnold, 2012).

The insight that investor wants to retrieve the spent capital at the earliest opportunity is driving

payback measures. Below is specific formula for computation of payback period, as follows:

Formula: Payback Period = Initial investment / cash inflow

6

dilutes company's share price majorly. Although where company is not offering cash as

an alternate, experiential grounds proposes that shares' price will be fall. It also a significant source of finance and funding due to option of shares against

dividend.

In context of shareholders:

Most prime advantage for shareholders, of a scrip dividend is that they can get tax

advantages by adopting the option/alternative of shares.

Shareholder who have desire to make an increase in their shareholding in company this

dividend is beneficial as they can enhance shareholding without any additional

transaction costs.

Share option in scrip dividend may provide a greater monetary benefits as compare to

cash dividend so mostly shareholders wants to get scrip dividend.

QUESTION 3

a. Investment appraisal technique

(I) Payback Period:

This is a capital budgeting technique that is meant to assess the new

investment's viability and to support the individual decision of selection of most appropriate

investment alternative. Payback period defined as specific duration over which the company will

reimburse the amount of money invested. Minimal payback duration is advantageous to the

organization as it allows to retrieve initial investment and commence to generate yields on it. It

allows managers to assess whether investment made on any option is capable to return back

within a reasonable period. Payback period is mandated to recuperate negative

project/venture cash from the purchase and/or initial years for positive project/venture cash flow.

Payback may be measured either from beginning of a proposal or from beginning of production

process. Payback periods are usually measured on the basis of undiscounted cash-flows, but it

may even be estimated at minimum return rate(%) for Discounted Cash Flows (Arnold, 2012).

The insight that investor wants to retrieve the spent capital at the earliest opportunity is driving

payback measures. Below is specific formula for computation of payback period, as follows:

Formula: Payback Period = Initial investment / cash inflow

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

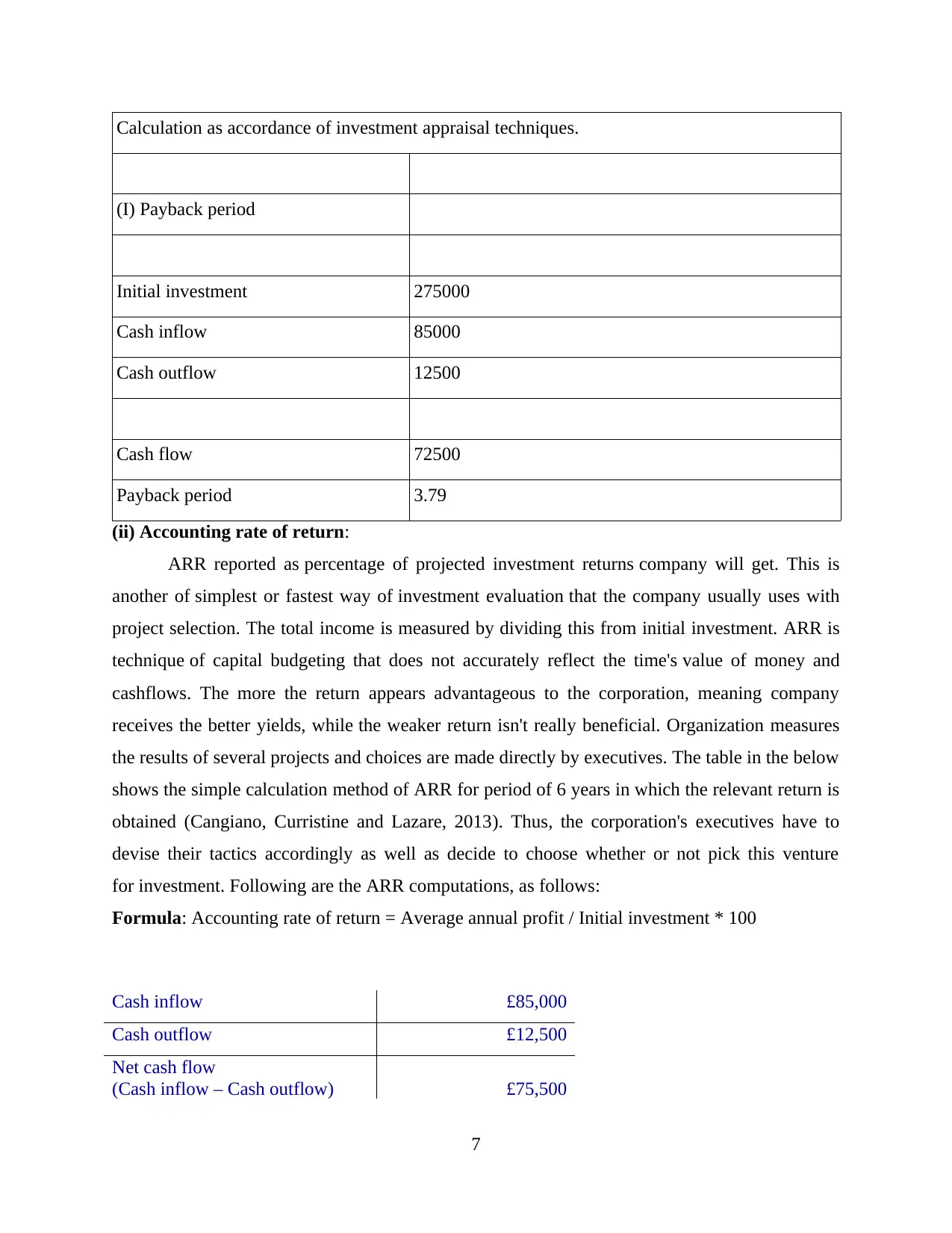

Calculation as accordance of investment appraisal techniques.

(I) Payback period

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Cash flow 72500

Payback period 3.79

(ii) Accounting rate of return:

ARR reported as percentage of projected investment returns company will get. This is

another of simplest or fastest way of investment evaluation that the company usually uses with

project selection. The total income is measured by dividing this from initial investment. ARR is

technique of capital budgeting that does not accurately reflect the time's value of money and

cashflows. The more the return appears advantageous to the corporation, meaning company

receives the better yields, while the weaker return isn't really beneficial. Organization measures

the results of several projects and choices are made directly by executives. The table in the below

shows the simple calculation method of ARR for period of 6 years in which the relevant return is

obtained (Cangiano, Curristine and Lazare, 2013). Thus, the corporation's executives have to

devise their tactics accordingly as well as decide to choose whether or not pick this venture

for investment. Following are the ARR computations, as follows:

Formula: Accounting rate of return = Average annual profit / Initial investment * 100

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

7

(I) Payback period

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Cash flow 72500

Payback period 3.79

(ii) Accounting rate of return:

ARR reported as percentage of projected investment returns company will get. This is

another of simplest or fastest way of investment evaluation that the company usually uses with

project selection. The total income is measured by dividing this from initial investment. ARR is

technique of capital budgeting that does not accurately reflect the time's value of money and

cashflows. The more the return appears advantageous to the corporation, meaning company

receives the better yields, while the weaker return isn't really beneficial. Organization measures

the results of several projects and choices are made directly by executives. The table in the below

shows the simple calculation method of ARR for period of 6 years in which the relevant return is

obtained (Cangiano, Curristine and Lazare, 2013). Thus, the corporation's executives have to

devise their tactics accordingly as well as decide to choose whether or not pick this venture

for investment. Following are the ARR computations, as follows:

Formula: Accounting rate of return = Average annual profit / Initial investment * 100

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

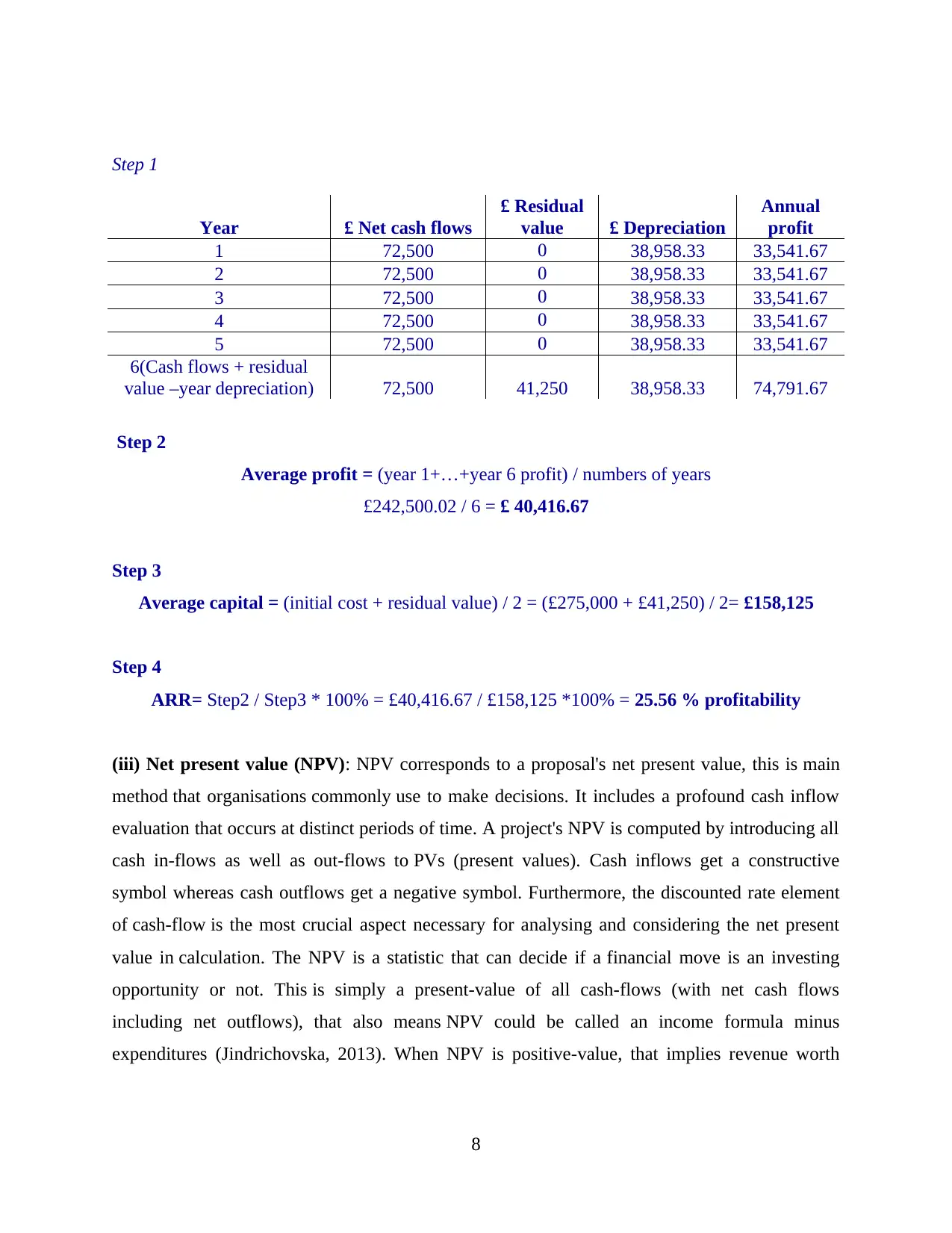

Step 1

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

Average capital = (initial cost + residual value) / 2 = (£275,000 + £41,250) / 2= £158,125

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

(iii) Net present value (NPV): NPV corresponds to a proposal's net present value, this is main

method that organisations commonly use to make decisions. It includes a profound cash inflow

evaluation that occurs at distinct periods of time. A project's NPV is computed by introducing all

cash in-flows as well as out-flows to PVs (present values). Cash inflows get a constructive

symbol whereas cash outflows get a negative symbol. Furthermore, the discounted rate element

of cash-flow is the most crucial aspect necessary for analysing and considering the net present

value in calculation. The NPV is a statistic that can decide if a financial move is an investing

opportunity or not. This is simply a present-value of all cash-flows (with net cash flows

including net outflows), that also means NPV could be called an income formula minus

expenditures (Jindrichovska, 2013). When NPV is positive-value, that implies revenue worth

8

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

Average capital = (initial cost + residual value) / 2 = (£275,000 + £41,250) / 2= £158,125

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

(iii) Net present value (NPV): NPV corresponds to a proposal's net present value, this is main

method that organisations commonly use to make decisions. It includes a profound cash inflow

evaluation that occurs at distinct periods of time. A project's NPV is computed by introducing all

cash in-flows as well as out-flows to PVs (present values). Cash inflows get a constructive

symbol whereas cash outflows get a negative symbol. Furthermore, the discounted rate element

of cash-flow is the most crucial aspect necessary for analysing and considering the net present

value in calculation. The NPV is a statistic that can decide if a financial move is an investing

opportunity or not. This is simply a present-value of all cash-flows (with net cash flows

including net outflows), that also means NPV could be called an income formula minus

expenditures (Jindrichovska, 2013). When NPV is positive-value, that implies revenue worth

8

(cash in flows) is higher than costs (cash-outflows). The investor generates a return when the

profits are higher than the expenses. Here is computation of NPV, as follows:

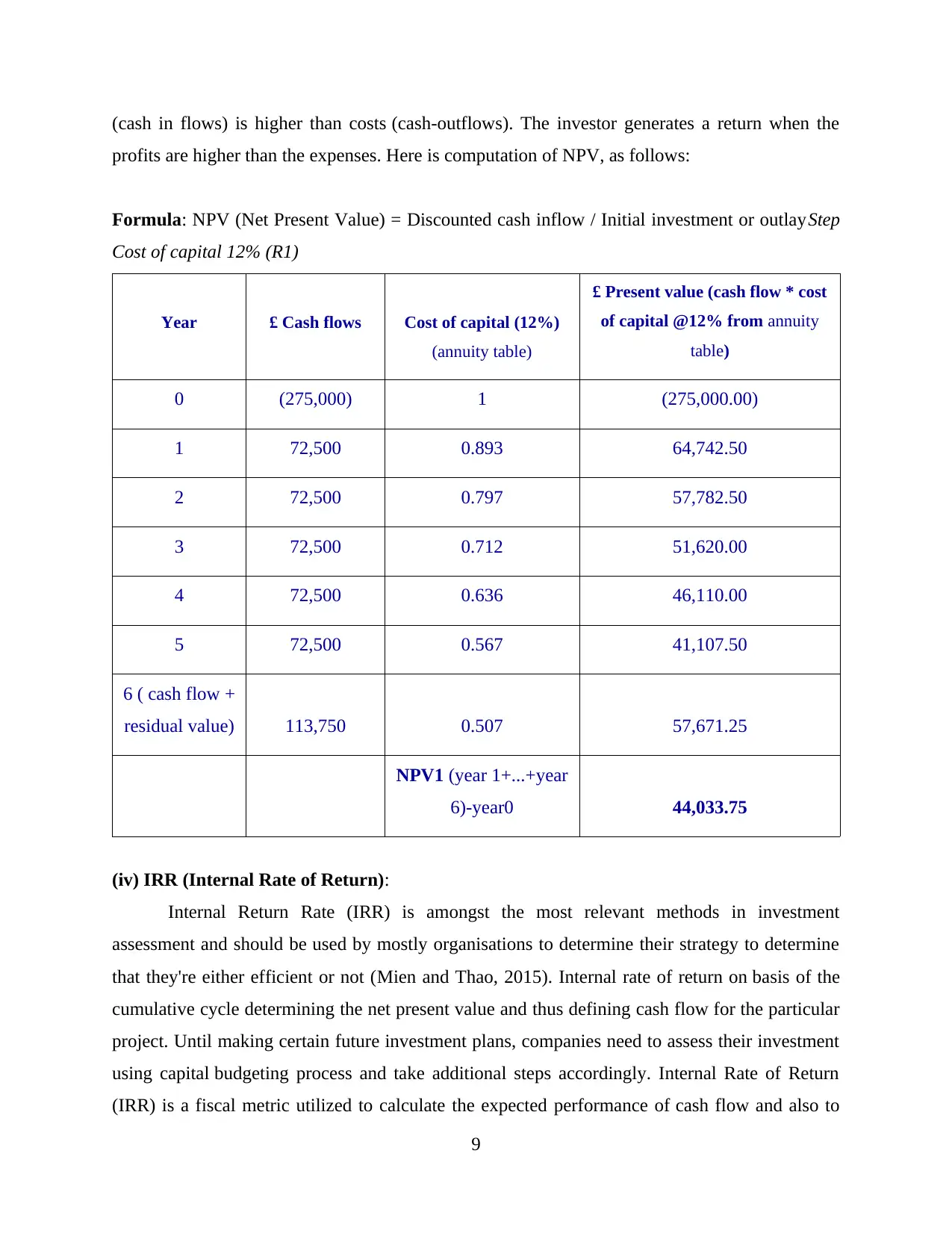

Formula: NPV (Net Present Value) = Discounted cash inflow / Initial investment or outlayStep

Cost of capital 12% (R1)

Year £ Cash flows Cost of capital (12%)

(annuity table)

£ Present value (cash flow * cost

of capital @12% from annuity

table)

0 (275,000) 1 (275,000.00)

1 72,500 0.893 64,742.50

2 72,500 0.797 57,782.50

3 72,500 0.712 51,620.00

4 72,500 0.636 46,110.00

5 72,500 0.567 41,107.50

6 ( cash flow +

residual value) 113,750 0.507 57,671.25

NPV1 (year 1+...+year

6)-year0 44,033.75

(iv) IRR (Internal Rate of Return):

Internal Return Rate (IRR) is amongst the most relevant methods in investment

assessment and should be used by mostly organisations to determine their strategy to determine

that they're either efficient or not (Mien and Thao, 2015). Internal rate of return on basis of the

cumulative cycle determining the net present value and thus defining cash flow for the particular

project. Until making certain future investment plans, companies need to assess their investment

using capital budgeting process and take additional steps accordingly. Internal Rate of Return

(IRR) is a fiscal metric utilized to calculate the expected performance of cash flow and also to

9

profits are higher than the expenses. Here is computation of NPV, as follows:

Formula: NPV (Net Present Value) = Discounted cash inflow / Initial investment or outlayStep

Cost of capital 12% (R1)

Year £ Cash flows Cost of capital (12%)

(annuity table)

£ Present value (cash flow * cost

of capital @12% from annuity

table)

0 (275,000) 1 (275,000.00)

1 72,500 0.893 64,742.50

2 72,500 0.797 57,782.50

3 72,500 0.712 51,620.00

4 72,500 0.636 46,110.00

5 72,500 0.567 41,107.50

6 ( cash flow +

residual value) 113,750 0.507 57,671.25

NPV1 (year 1+...+year

6)-year0 44,033.75

(iv) IRR (Internal Rate of Return):

Internal Return Rate (IRR) is amongst the most relevant methods in investment

assessment and should be used by mostly organisations to determine their strategy to determine

that they're either efficient or not (Mien and Thao, 2015). Internal rate of return on basis of the

cumulative cycle determining the net present value and thus defining cash flow for the particular

project. Until making certain future investment plans, companies need to assess their investment

using capital budgeting process and take additional steps accordingly. Internal Rate of Return

(IRR) is a fiscal metric utilized to calculate the expected performance of cash flow and also to

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.