Financial Management and Analysis Report: Unilever Case Study

VerifiedAdded on 2022/12/26

|13

|3660

|67

Report

AI Summary

This report provides a comprehensive financial analysis of Unilever, a company listed on the London Stock Exchange. The analysis begins with an examination of Unilever's financial performance and health over the past two years, utilizing various financial ratios to assess liquidity, profitability, efficiency, capital structure, and stock market performance. The report then discusses the limitations of ratio analysis and suggests improvements. Subsequent tasks delve into investment decision-making, including payback period, Net Present Value (NPV), and Internal Rate of Return (IRR) calculations for different investment choices. Further, the report evaluates the valuation of right issues, assesses market capitalization, and explores the net asset value of the company. It also uses the Price-to-Earnings (P/E) ratio method to value the company and analyzes historical dividend growth rates. The report concludes with a discussion of systematic and unsystematic risks associated with the stock market.

FINANCIAL

MANAGEMENT AND

ANALYSIS

MANAGEMENT AND

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...............................................................................................................................3

MAIN BODY.......................................................................................................................................3

Task 1................................................................................................................................................3

1) Critical analysis of Unilever’s financial performance and health based on past two years

performance and position..................................................................................................................3

Task 2................................................................................................................................................4

Task 3................................................................................................................................................6

Task 4................................................................................................................................................7

Task 5................................................................................................................................................9

CONCLUSION..................................................................................................................................11

REFERENCES..................................................................................................................................12

INTRODUCTION...............................................................................................................................3

MAIN BODY.......................................................................................................................................3

Task 1................................................................................................................................................3

1) Critical analysis of Unilever’s financial performance and health based on past two years

performance and position..................................................................................................................3

Task 2................................................................................................................................................4

Task 3................................................................................................................................................6

Task 4................................................................................................................................................7

Task 5................................................................................................................................................9

CONCLUSION..................................................................................................................................11

REFERENCES..................................................................................................................................12

INTRODUCTION

Financial management can be defined as the strategic planning, organisation, direction

and controlling of the financial assets of the organization in order to operate with great level

of efficiency and ensure smooth functioning of the business. It can be defined also as the

application of general principles of management on the financial resources of the business

with the basic aim of maximising profits and minimising costs of the business (Brigham and

Houston, 2021). Financial management generally has three elements which includes

investment decision, financing decision and dividend decision. In this report, there will be

five different tasks where the first task includes the financial analysis of any company listed

on London stock exchange which will be taken here as Unilever. The second task will be

related to investment decision making and third one is related to valuing right issues. The

fourth task will be related to the valuation of the company in different circumstances and in

the fifth task various factors associated with the stock market will be discussed.

MAIN BODY

Task 1

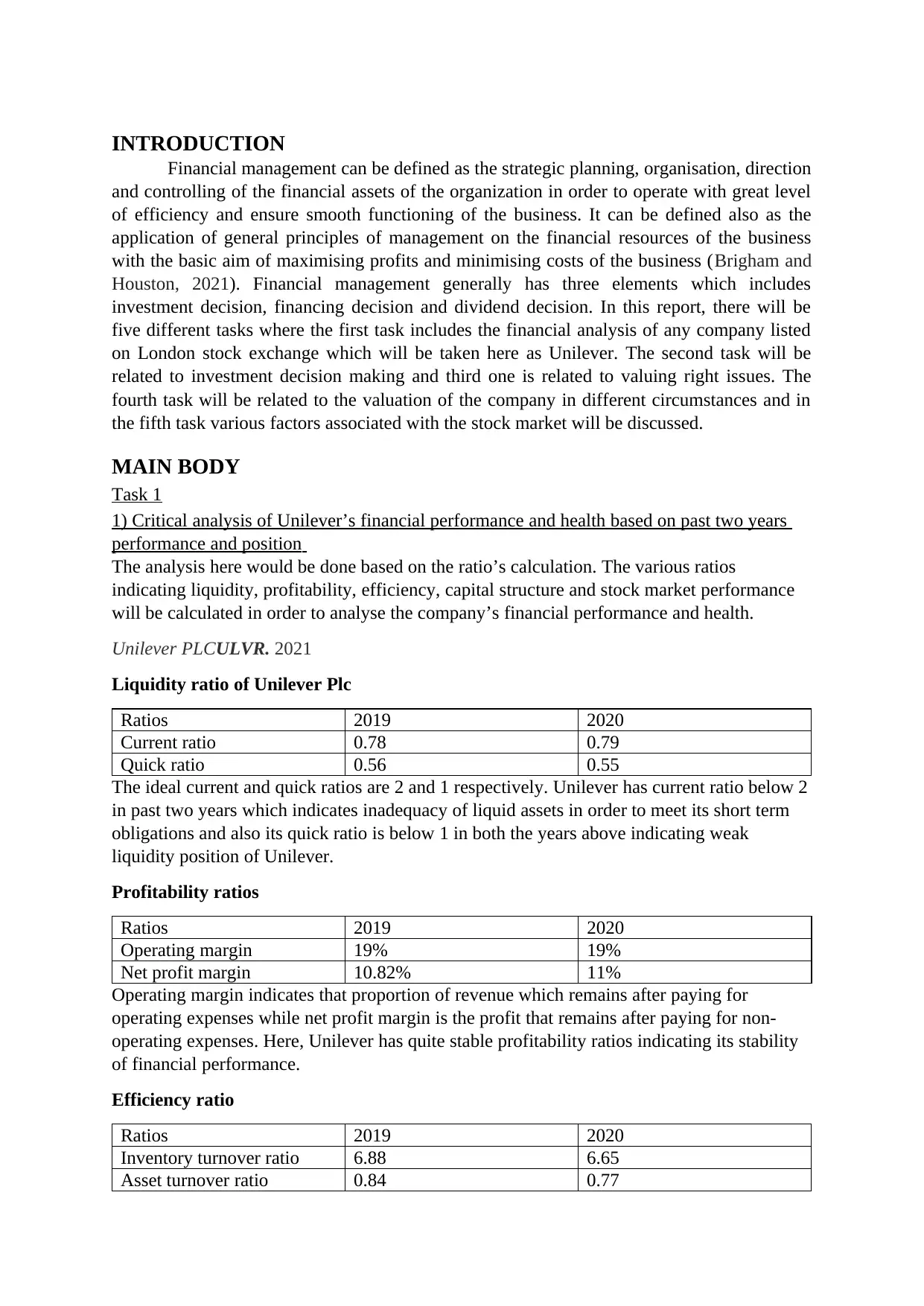

1) Critical analysis of Unilever’s financial performance and health based on past two years

performance and position

The analysis here would be done based on the ratio’s calculation. The various ratios

indicating liquidity, profitability, efficiency, capital structure and stock market performance

will be calculated in order to analyse the company’s financial performance and health.

Unilever PLCULVR. 2021

Liquidity ratio of Unilever Plc

Ratios 2019 2020

Current ratio 0.78 0.79

Quick ratio 0.56 0.55

The ideal current and quick ratios are 2 and 1 respectively. Unilever has current ratio below 2

in past two years which indicates inadequacy of liquid assets in order to meet its short term

obligations and also its quick ratio is below 1 in both the years above indicating weak

liquidity position of Unilever.

Profitability ratios

Ratios 2019 2020

Operating margin 19% 19%

Net profit margin 10.82% 11%

Operating margin indicates that proportion of revenue which remains after paying for

operating expenses while net profit margin is the profit that remains after paying for non-

operating expenses. Here, Unilever has quite stable profitability ratios indicating its stability

of financial performance.

Efficiency ratio

Ratios 2019 2020

Inventory turnover ratio 6.88 6.65

Asset turnover ratio 0.84 0.77

Financial management can be defined as the strategic planning, organisation, direction

and controlling of the financial assets of the organization in order to operate with great level

of efficiency and ensure smooth functioning of the business. It can be defined also as the

application of general principles of management on the financial resources of the business

with the basic aim of maximising profits and minimising costs of the business (Brigham and

Houston, 2021). Financial management generally has three elements which includes

investment decision, financing decision and dividend decision. In this report, there will be

five different tasks where the first task includes the financial analysis of any company listed

on London stock exchange which will be taken here as Unilever. The second task will be

related to investment decision making and third one is related to valuing right issues. The

fourth task will be related to the valuation of the company in different circumstances and in

the fifth task various factors associated with the stock market will be discussed.

MAIN BODY

Task 1

1) Critical analysis of Unilever’s financial performance and health based on past two years

performance and position

The analysis here would be done based on the ratio’s calculation. The various ratios

indicating liquidity, profitability, efficiency, capital structure and stock market performance

will be calculated in order to analyse the company’s financial performance and health.

Unilever PLCULVR. 2021

Liquidity ratio of Unilever Plc

Ratios 2019 2020

Current ratio 0.78 0.79

Quick ratio 0.56 0.55

The ideal current and quick ratios are 2 and 1 respectively. Unilever has current ratio below 2

in past two years which indicates inadequacy of liquid assets in order to meet its short term

obligations and also its quick ratio is below 1 in both the years above indicating weak

liquidity position of Unilever.

Profitability ratios

Ratios 2019 2020

Operating margin 19% 19%

Net profit margin 10.82% 11%

Operating margin indicates that proportion of revenue which remains after paying for

operating expenses while net profit margin is the profit that remains after paying for non-

operating expenses. Here, Unilever has quite stable profitability ratios indicating its stability

of financial performance.

Efficiency ratio

Ratios 2019 2020

Inventory turnover ratio 6.88 6.65

Asset turnover ratio 0.84 0.77

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency ratio indicates the efficiency of company in managing its and liabilities in the short

run to generate revenue for the business. The inventory turnover ratio indicates how

efficiently a concern can liquidate its inventory to generate revenue. So, Unilever has

experiences reduction in its efficiency in generating revenue which can be seen from its

reduced efficiency ratios.

Capital structure

Ratios 2019 2020

Debt to equity ratio 1.96 1.63

Debt to equity ratio indicates the proportion of debt capital and equity component in the total

capital of the company. Here, it can be interpreted from the above stated ratio that the

company is reducing its debt and moving towards equity financing which can be beneficial

for a business to reduce its financial costs and risks.

Stock market performance

Ratios 2019 2020

Price / earnings ratio 14.51 21.63

The increasing price / earning ratio indicates that due to growth potential in the company, the

investors are willing to pay more for buying company’s share. A higher ratio means higher

market price over the earning on each share.

2) Problems or limitations of ratio analysis

The problem with the ratio analysis is that it does not indicate or guarantee any future

perspective about the concern as it is built on historic data (Brigham and Houston,

2021).

The external environmental factors are not considered while deriving the performance

of the concern and even many internal factors such as human resource quality of the

company is not taken into consideration.

3) Recommendations for the improvements

The above analysis can be improved through including soft factors such as the

considerable impact of economic and political factors on the financial performance of

the company.

Also, by avoiding window dressing act while preparing financial statements can be

helpful in enhancing the reliability and relevancy of the financial ratio analysis

(Illmeyer and et.al., 2017).

Task 2

The investment manager in order to decide upon which choice should be adopted by

analysing each based on various techniques of investment decisions as follows:

(a) Calculation of payback period for three choices

run to generate revenue for the business. The inventory turnover ratio indicates how

efficiently a concern can liquidate its inventory to generate revenue. So, Unilever has

experiences reduction in its efficiency in generating revenue which can be seen from its

reduced efficiency ratios.

Capital structure

Ratios 2019 2020

Debt to equity ratio 1.96 1.63

Debt to equity ratio indicates the proportion of debt capital and equity component in the total

capital of the company. Here, it can be interpreted from the above stated ratio that the

company is reducing its debt and moving towards equity financing which can be beneficial

for a business to reduce its financial costs and risks.

Stock market performance

Ratios 2019 2020

Price / earnings ratio 14.51 21.63

The increasing price / earning ratio indicates that due to growth potential in the company, the

investors are willing to pay more for buying company’s share. A higher ratio means higher

market price over the earning on each share.

2) Problems or limitations of ratio analysis

The problem with the ratio analysis is that it does not indicate or guarantee any future

perspective about the concern as it is built on historic data (Brigham and Houston,

2021).

The external environmental factors are not considered while deriving the performance

of the concern and even many internal factors such as human resource quality of the

company is not taken into consideration.

3) Recommendations for the improvements

The above analysis can be improved through including soft factors such as the

considerable impact of economic and political factors on the financial performance of

the company.

Also, by avoiding window dressing act while preparing financial statements can be

helpful in enhancing the reliability and relevancy of the financial ratio analysis

(Illmeyer and et.al., 2017).

Task 2

The investment manager in order to decide upon which choice should be adopted by

analysing each based on various techniques of investment decisions as follows:

(a) Calculation of payback period for three choices

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

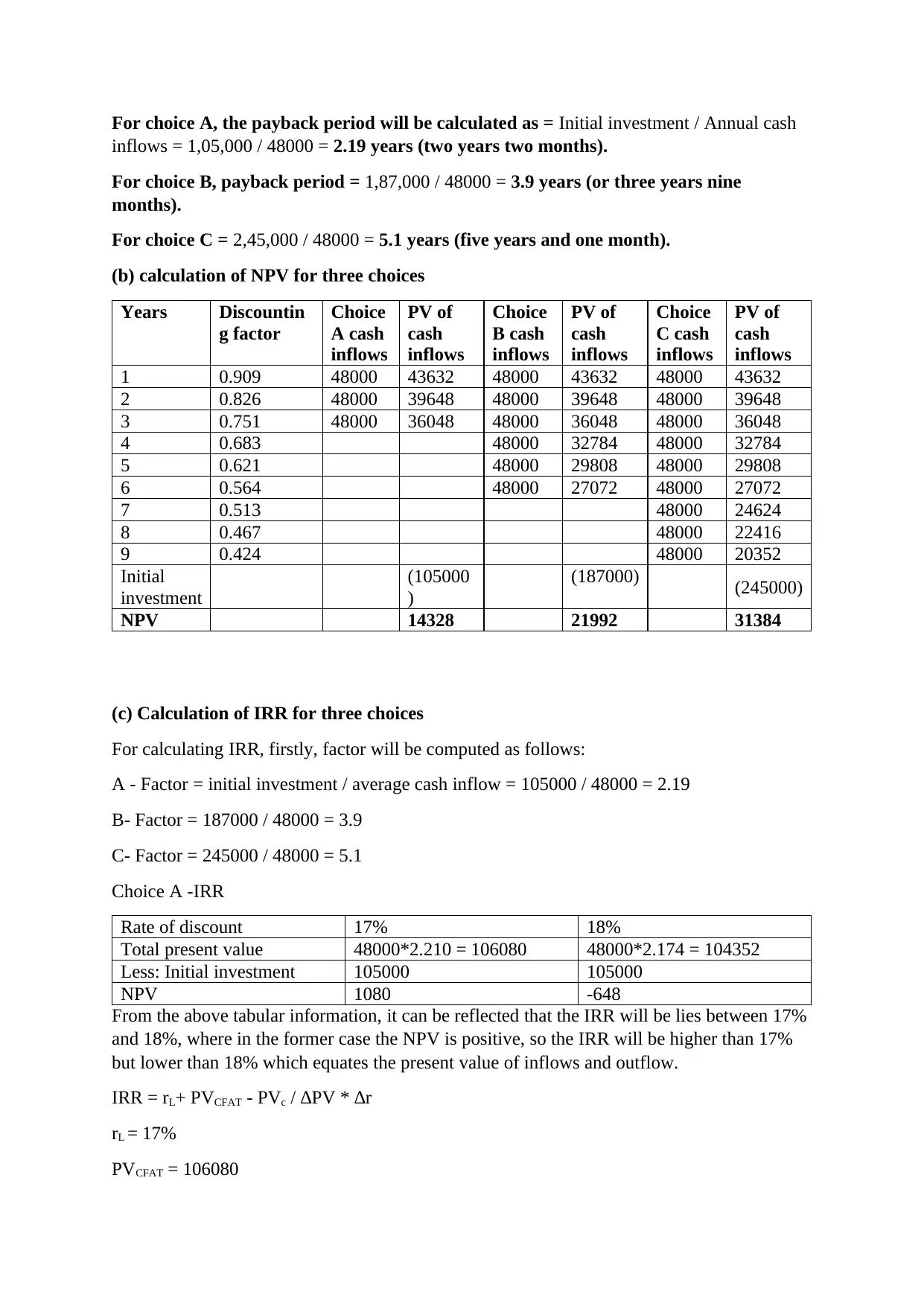

For choice A, the payback period will be calculated as = Initial investment / Annual cash

inflows = 1,05,000 / 48000 = 2.19 years (two years two months).

For choice B, payback period = 1,87,000 / 48000 = 3.9 years (or three years nine

months).

For choice C = 2,45,000 / 48000 = 5.1 years (five years and one month).

(b) calculation of NPV for three choices

Years Discountin

g factor

Choice

A cash

inflows

PV of

cash

inflows

Choice

B cash

inflows

PV of

cash

inflows

Choice

C cash

inflows

PV of

cash

inflows

1 0.909 48000 43632 48000 43632 48000 43632

2 0.826 48000 39648 48000 39648 48000 39648

3 0.751 48000 36048 48000 36048 48000 36048

4 0.683 48000 32784 48000 32784

5 0.621 48000 29808 48000 29808

6 0.564 48000 27072 48000 27072

7 0.513 48000 24624

8 0.467 48000 22416

9 0.424 48000 20352

Initial

investment

(105000

)

(187000) (245000)

NPV 14328 21992 31384

(c) Calculation of IRR for three choices

For calculating IRR, firstly, factor will be computed as follows:

A - Factor = initial investment / average cash inflow = 105000 / 48000 = 2.19

B- Factor = 187000 / 48000 = 3.9

C- Factor = 245000 / 48000 = 5.1

Choice A -IRR

Rate of discount 17% 18%

Total present value 48000*2.210 = 106080 48000*2.174 = 104352

Less: Initial investment 105000 105000

NPV 1080 -648

From the above tabular information, it can be reflected that the IRR will be lies between 17%

and 18%, where in the former case the NPV is positive, so the IRR will be higher than 17%

but lower than 18% which equates the present value of inflows and outflow.

IRR = rL+ PVCFAT - PVc / ∆PV * ∆r

rL = 17%

PVCFAT = 106080

inflows = 1,05,000 / 48000 = 2.19 years (two years two months).

For choice B, payback period = 1,87,000 / 48000 = 3.9 years (or three years nine

months).

For choice C = 2,45,000 / 48000 = 5.1 years (five years and one month).

(b) calculation of NPV for three choices

Years Discountin

g factor

Choice

A cash

inflows

PV of

cash

inflows

Choice

B cash

inflows

PV of

cash

inflows

Choice

C cash

inflows

PV of

cash

inflows

1 0.909 48000 43632 48000 43632 48000 43632

2 0.826 48000 39648 48000 39648 48000 39648

3 0.751 48000 36048 48000 36048 48000 36048

4 0.683 48000 32784 48000 32784

5 0.621 48000 29808 48000 29808

6 0.564 48000 27072 48000 27072

7 0.513 48000 24624

8 0.467 48000 22416

9 0.424 48000 20352

Initial

investment

(105000

)

(187000) (245000)

NPV 14328 21992 31384

(c) Calculation of IRR for three choices

For calculating IRR, firstly, factor will be computed as follows:

A - Factor = initial investment / average cash inflow = 105000 / 48000 = 2.19

B- Factor = 187000 / 48000 = 3.9

C- Factor = 245000 / 48000 = 5.1

Choice A -IRR

Rate of discount 17% 18%

Total present value 48000*2.210 = 106080 48000*2.174 = 104352

Less: Initial investment 105000 105000

NPV 1080 -648

From the above tabular information, it can be reflected that the IRR will be lies between 17%

and 18%, where in the former case the NPV is positive, so the IRR will be higher than 17%

but lower than 18% which equates the present value of inflows and outflow.

IRR = rL+ PVCFAT - PVc / ∆PV * ∆r

rL = 17%

PVCFAT = 106080

PVc = 105000

∆PV = 1728

∆r = 1

IRR = 17% + 106080 – 105000 / 1728 * 1 = 17+ 0.625 = 17.625%

Choice B

Rate of discount 13% 14%

Total present value 48000*3.998 = 191904 48000*3.889 = 186672

Less: Initial investment 187000 187000

NPV 4904 -328

IRR will be higher than 13% and lower than 14%.

IRR = 13% + 191904 – 187000 / 5232*1 = 17+ 0.937 = 13.937%

Choice C

Rate of discount 13% 14%

Total present value 48000*5.132= 246336 48000*4.946= 237408

Less: Initial

investment

245000 245000

NPV 1336 -7592

IRR will be higher than 13% and lower than 14%.

IRR = 13% + 246336 – 245000 / 8928 *1 = 13+0.15 = 13.15%.

(D) If any one choice needs to be selected from available three choices then the advisable

choice would be as follows:

If decision would be made on the basis of payback period due to the manager’s

desires for recovering its initial cost as early as possible then the choice A would be

chosen as it is having least payback period among three alternatives (Dwiastanti,

2017).

If decision will be taken on the basis of NPV technique, then the choice C would be

selected as it is having highest NPV among three choices.

At, last there is no priority for any one choice in case IRR technique, as all three

choices will give higher rate of return against the cost of capital, but the choice A

would be advisable as it is having greater IRR than the other two choices (Haydarov,

2020).

Task 3

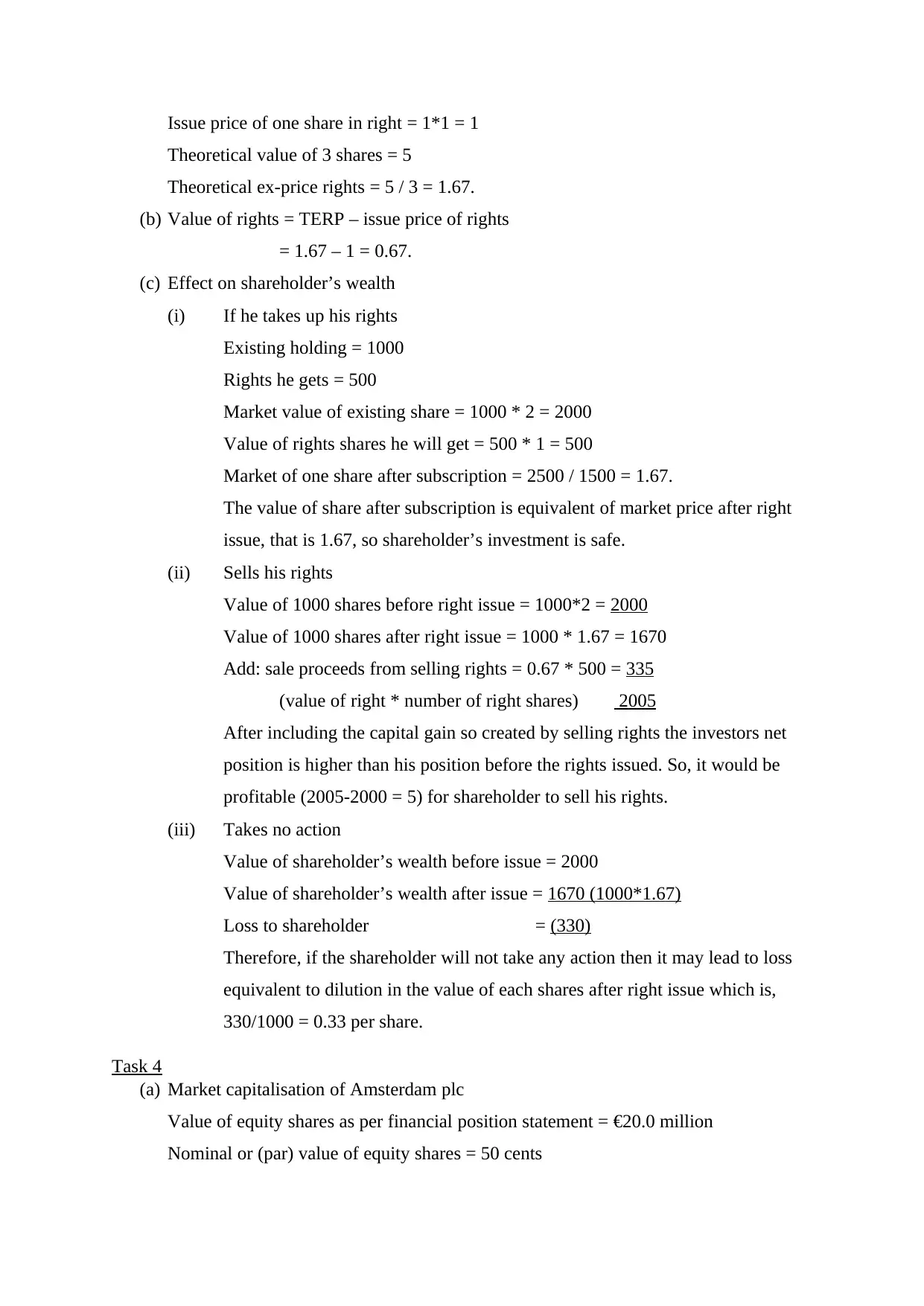

(a) Calculation of TERP

Market value of two existing shares = 2*2 = 4

∆PV = 1728

∆r = 1

IRR = 17% + 106080 – 105000 / 1728 * 1 = 17+ 0.625 = 17.625%

Choice B

Rate of discount 13% 14%

Total present value 48000*3.998 = 191904 48000*3.889 = 186672

Less: Initial investment 187000 187000

NPV 4904 -328

IRR will be higher than 13% and lower than 14%.

IRR = 13% + 191904 – 187000 / 5232*1 = 17+ 0.937 = 13.937%

Choice C

Rate of discount 13% 14%

Total present value 48000*5.132= 246336 48000*4.946= 237408

Less: Initial

investment

245000 245000

NPV 1336 -7592

IRR will be higher than 13% and lower than 14%.

IRR = 13% + 246336 – 245000 / 8928 *1 = 13+0.15 = 13.15%.

(D) If any one choice needs to be selected from available three choices then the advisable

choice would be as follows:

If decision would be made on the basis of payback period due to the manager’s

desires for recovering its initial cost as early as possible then the choice A would be

chosen as it is having least payback period among three alternatives (Dwiastanti,

2017).

If decision will be taken on the basis of NPV technique, then the choice C would be

selected as it is having highest NPV among three choices.

At, last there is no priority for any one choice in case IRR technique, as all three

choices will give higher rate of return against the cost of capital, but the choice A

would be advisable as it is having greater IRR than the other two choices (Haydarov,

2020).

Task 3

(a) Calculation of TERP

Market value of two existing shares = 2*2 = 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Issue price of one share in right = 1*1 = 1

Theoretical value of 3 shares = 5

Theoretical ex-price rights = 5 / 3 = 1.67.

(b) Value of rights = TERP – issue price of rights

= 1.67 – 1 = 0.67.

(c) Effect on shareholder’s wealth

(i) If he takes up his rights

Existing holding = 1000

Rights he gets = 500

Market value of existing share = 1000 * 2 = 2000

Value of rights shares he will get = 500 * 1 = 500

Market of one share after subscription = 2500 / 1500 = 1.67.

The value of share after subscription is equivalent of market price after right

issue, that is 1.67, so shareholder’s investment is safe.

(ii) Sells his rights

Value of 1000 shares before right issue = 1000*2 = 2000

Value of 1000 shares after right issue = 1000 * 1.67 = 1670

Add: sale proceeds from selling rights = 0.67 * 500 = 335

(value of right * number of right shares) 2005

After including the capital gain so created by selling rights the investors net

position is higher than his position before the rights issued. So, it would be

profitable (2005-2000 = 5) for shareholder to sell his rights.

(iii) Takes no action

Value of shareholder’s wealth before issue = 2000

Value of shareholder’s wealth after issue = 1670 (1000*1.67)

Loss to shareholder = (330)

Therefore, if the shareholder will not take any action then it may lead to loss

equivalent to dilution in the value of each shares after right issue which is,

330/1000 = 0.33 per share.

Task 4

(a) Market capitalisation of Amsterdam plc

Value of equity shares as per financial position statement = €20.0 million

Nominal or (par) value of equity shares = 50 cents

Theoretical value of 3 shares = 5

Theoretical ex-price rights = 5 / 3 = 1.67.

(b) Value of rights = TERP – issue price of rights

= 1.67 – 1 = 0.67.

(c) Effect on shareholder’s wealth

(i) If he takes up his rights

Existing holding = 1000

Rights he gets = 500

Market value of existing share = 1000 * 2 = 2000

Value of rights shares he will get = 500 * 1 = 500

Market of one share after subscription = 2500 / 1500 = 1.67.

The value of share after subscription is equivalent of market price after right

issue, that is 1.67, so shareholder’s investment is safe.

(ii) Sells his rights

Value of 1000 shares before right issue = 1000*2 = 2000

Value of 1000 shares after right issue = 1000 * 1.67 = 1670

Add: sale proceeds from selling rights = 0.67 * 500 = 335

(value of right * number of right shares) 2005

After including the capital gain so created by selling rights the investors net

position is higher than his position before the rights issued. So, it would be

profitable (2005-2000 = 5) for shareholder to sell his rights.

(iii) Takes no action

Value of shareholder’s wealth before issue = 2000

Value of shareholder’s wealth after issue = 1670 (1000*1.67)

Loss to shareholder = (330)

Therefore, if the shareholder will not take any action then it may lead to loss

equivalent to dilution in the value of each shares after right issue which is,

330/1000 = 0.33 per share.

Task 4

(a) Market capitalisation of Amsterdam plc

Value of equity shares as per financial position statement = €20.0 million

Nominal or (par) value of equity shares = 50 cents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

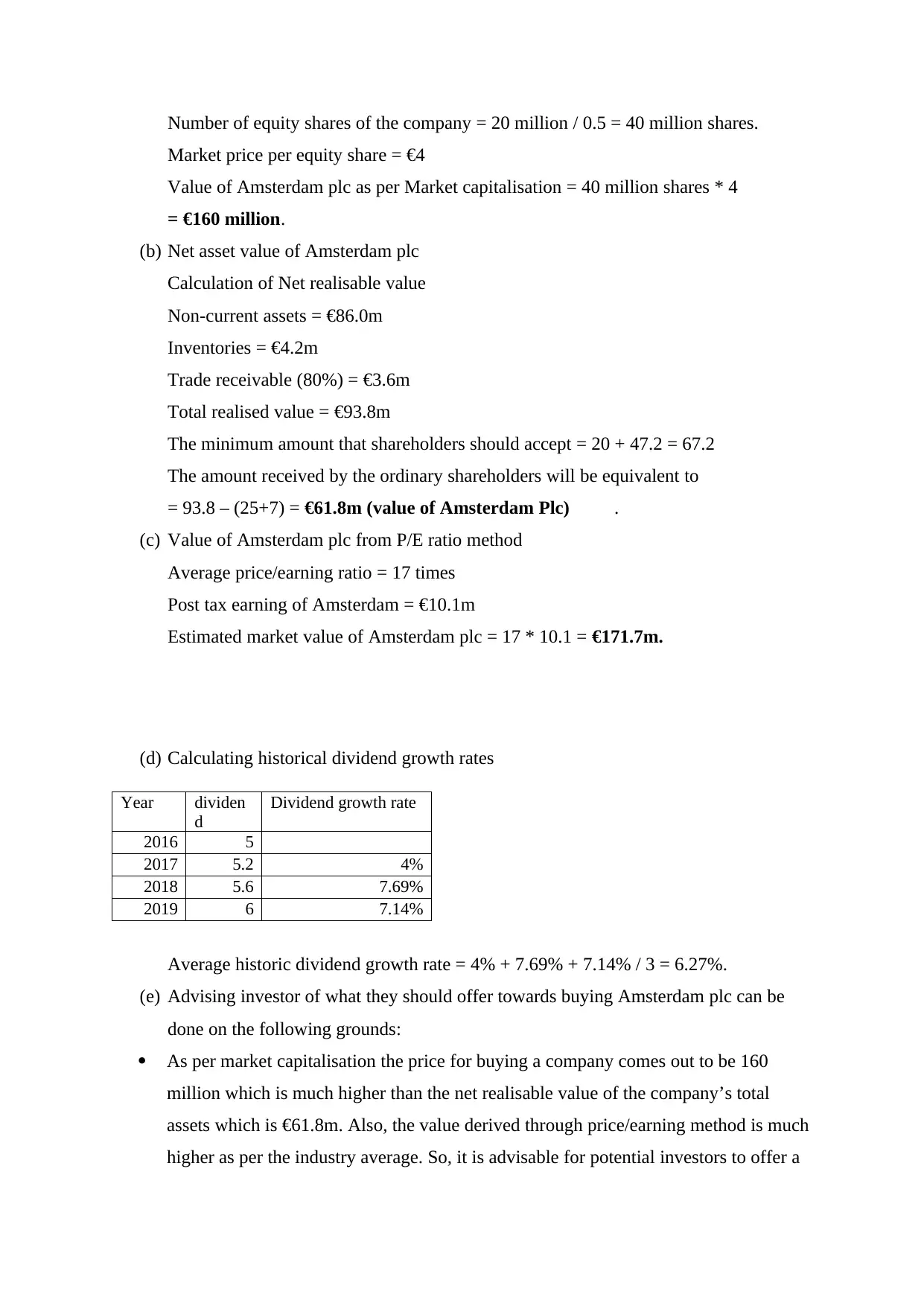

Number of equity shares of the company = 20 million / 0.5 = 40 million shares.

Market price per equity share = €4

Value of Amsterdam plc as per Market capitalisation = 40 million shares * 4

= €160 million.

(b) Net asset value of Amsterdam plc

Calculation of Net realisable value

Non-current assets = €86.0m

Inventories = €4.2m

Trade receivable (80%) = €3.6m

Total realised value = €93.8m

The minimum amount that shareholders should accept = 20 + 47.2 = 67.2

The amount received by the ordinary shareholders will be equivalent to

= 93.8 – (25+7) = €61.8m (value of Amsterdam Plc) .

(c) Value of Amsterdam plc from P/E ratio method

Average price/earning ratio = 17 times

Post tax earning of Amsterdam = €10.1m

Estimated market value of Amsterdam plc = 17 * 10.1 = €171.7m.

(d) Calculating historical dividend growth rates

Year dividen

d

Dividend growth rate

2016 5

2017 5.2 4%

2018 5.6 7.69%

2019 6 7.14%

Average historic dividend growth rate = 4% + 7.69% + 7.14% / 3 = 6.27%.

(e) Advising investor of what they should offer towards buying Amsterdam plc can be

done on the following grounds:

As per market capitalisation the price for buying a company comes out to be 160

million which is much higher than the net realisable value of the company’s total

assets which is €61.8m. Also, the value derived through price/earning method is much

higher as per the industry average. So, it is advisable for potential investors to offer a

Market price per equity share = €4

Value of Amsterdam plc as per Market capitalisation = 40 million shares * 4

= €160 million.

(b) Net asset value of Amsterdam plc

Calculation of Net realisable value

Non-current assets = €86.0m

Inventories = €4.2m

Trade receivable (80%) = €3.6m

Total realised value = €93.8m

The minimum amount that shareholders should accept = 20 + 47.2 = 67.2

The amount received by the ordinary shareholders will be equivalent to

= 93.8 – (25+7) = €61.8m (value of Amsterdam Plc) .

(c) Value of Amsterdam plc from P/E ratio method

Average price/earning ratio = 17 times

Post tax earning of Amsterdam = €10.1m

Estimated market value of Amsterdam plc = 17 * 10.1 = €171.7m.

(d) Calculating historical dividend growth rates

Year dividen

d

Dividend growth rate

2016 5

2017 5.2 4%

2018 5.6 7.69%

2019 6 7.14%

Average historic dividend growth rate = 4% + 7.69% + 7.14% / 3 = 6.27%.

(e) Advising investor of what they should offer towards buying Amsterdam plc can be

done on the following grounds:

As per market capitalisation the price for buying a company comes out to be 160

million which is much higher than the net realisable value of the company’s total

assets which is €61.8m. Also, the value derived through price/earning method is much

higher as per the industry average. So, it is advisable for potential investors to offer a

good deal of premium price in order to acquire Amsterdam plc as the target seems to

be earning potential.

Task 5

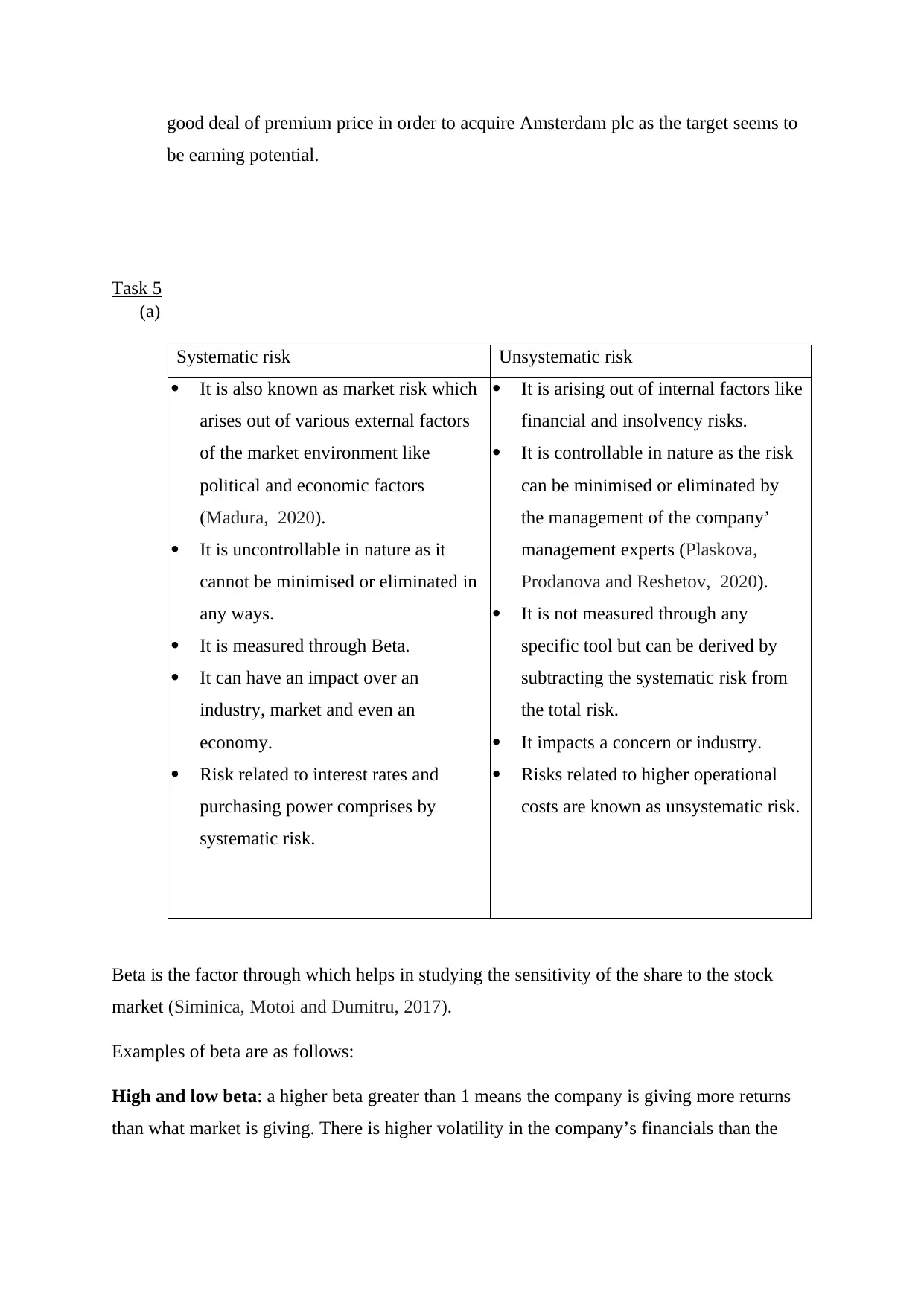

(a)

Systematic risk Unsystematic risk

It is also known as market risk which

arises out of various external factors

of the market environment like

political and economic factors

(Madura, 2020).

It is uncontrollable in nature as it

cannot be minimised or eliminated in

any ways.

It is measured through Beta.

It can have an impact over an

industry, market and even an

economy.

Risk related to interest rates and

purchasing power comprises by

systematic risk.

It is arising out of internal factors like

financial and insolvency risks.

It is controllable in nature as the risk

can be minimised or eliminated by

the management of the company’

management experts (Plaskova,

Prodanova and Reshetov, 2020).

It is not measured through any

specific tool but can be derived by

subtracting the systematic risk from

the total risk.

It impacts a concern or industry.

Risks related to higher operational

costs are known as unsystematic risk.

Beta is the factor through which helps in studying the sensitivity of the share to the stock

market (Siminica, Motoi and Dumitru, 2017).

Examples of beta are as follows:

High and low beta: a higher beta greater than 1 means the company is giving more returns

than what market is giving. There is higher volatility in the company’s financials than the

be earning potential.

Task 5

(a)

Systematic risk Unsystematic risk

It is also known as market risk which

arises out of various external factors

of the market environment like

political and economic factors

(Madura, 2020).

It is uncontrollable in nature as it

cannot be minimised or eliminated in

any ways.

It is measured through Beta.

It can have an impact over an

industry, market and even an

economy.

Risk related to interest rates and

purchasing power comprises by

systematic risk.

It is arising out of internal factors like

financial and insolvency risks.

It is controllable in nature as the risk

can be minimised or eliminated by

the management of the company’

management experts (Plaskova,

Prodanova and Reshetov, 2020).

It is not measured through any

specific tool but can be derived by

subtracting the systematic risk from

the total risk.

It impacts a concern or industry.

Risks related to higher operational

costs are known as unsystematic risk.

Beta is the factor through which helps in studying the sensitivity of the share to the stock

market (Siminica, Motoi and Dumitru, 2017).

Examples of beta are as follows:

High and low beta: a higher beta greater than 1 means the company is giving more returns

than what market is giving. There is higher volatility in the company’s financials than the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market. Like a company with 1.5 beta means it is giving 150% of the market return and vice

versa.

Negative beta: a negative beta lower than one means that the company is negatively

correlated with the market return. So, if there is 10% rise in market return and then there

would be reduction by 10% from company’s return.

(b) The basic or main difference between money market and capital market is that in the

former market short term securities with the validity of less than one year are traded

and lending and borrowing is done for a very short period not more than a year

(Shapiro and Hanouna, 2019). In the latter market long term securities are traded

which is having expiry period more than a year and the securities are used for

financing long term operations of the company.

Interest bearing instruments are those which pays a fixed rate of interests either at

regular intervals or even it can be on maturity. On the other hand, discount

instruments are those which is issued in the market at the discounted value which is

less than the face value of the instruments and on maturity, the redemption has been

done on the face value it possesses.

Examples of capital market instruments

Ordinary Stocks: It can be either equity or preference shares. It is issued to the

company’s shareholders in order to procure finance for the business. It pays variable

dividend to the shareholders.

Bonds: bonds are highly secured debt instruments, which pays fixed interest and

repaid the principle on maturity. It provides companies with the growth capital.

Preference stocks: It is a quite like ordinary stocks but here the shareholders are given

preference while paying dividend over ordinary shareholders (Yap, Komalasari and

Hadiansah, 2018).

Examples of money market instruments

Treasury bills: short term instrument issued by the central bank of the country on

behalf of the government having maturity of less than a year, and issued at a

discounted rate and repayment is done on face value, where the difference between

the two is the return earned by the investors.

Commercial papers: a kind of promissory noted issued by large corporations in order

to meet their short-term fund requirement. It is issued against the company’s

credibility as a security and are generally considered as an unsecured instrument.

versa.

Negative beta: a negative beta lower than one means that the company is negatively

correlated with the market return. So, if there is 10% rise in market return and then there

would be reduction by 10% from company’s return.

(b) The basic or main difference between money market and capital market is that in the

former market short term securities with the validity of less than one year are traded

and lending and borrowing is done for a very short period not more than a year

(Shapiro and Hanouna, 2019). In the latter market long term securities are traded

which is having expiry period more than a year and the securities are used for

financing long term operations of the company.

Interest bearing instruments are those which pays a fixed rate of interests either at

regular intervals or even it can be on maturity. On the other hand, discount

instruments are those which is issued in the market at the discounted value which is

less than the face value of the instruments and on maturity, the redemption has been

done on the face value it possesses.

Examples of capital market instruments

Ordinary Stocks: It can be either equity or preference shares. It is issued to the

company’s shareholders in order to procure finance for the business. It pays variable

dividend to the shareholders.

Bonds: bonds are highly secured debt instruments, which pays fixed interest and

repaid the principle on maturity. It provides companies with the growth capital.

Preference stocks: It is a quite like ordinary stocks but here the shareholders are given

preference while paying dividend over ordinary shareholders (Yap, Komalasari and

Hadiansah, 2018).

Examples of money market instruments

Treasury bills: short term instrument issued by the central bank of the country on

behalf of the government having maturity of less than a year, and issued at a

discounted rate and repayment is done on face value, where the difference between

the two is the return earned by the investors.

Commercial papers: a kind of promissory noted issued by large corporations in order

to meet their short-term fund requirement. It is issued against the company’s

credibility as a security and are generally considered as an unsecured instrument.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Certificate of deposits: an instrument issued by financial institutions and banks

known as a financial asset and gives the investors fixed return on the amount so

invested. It has a maturity ranging from a week to a year (Brigham and Houston,

2021).

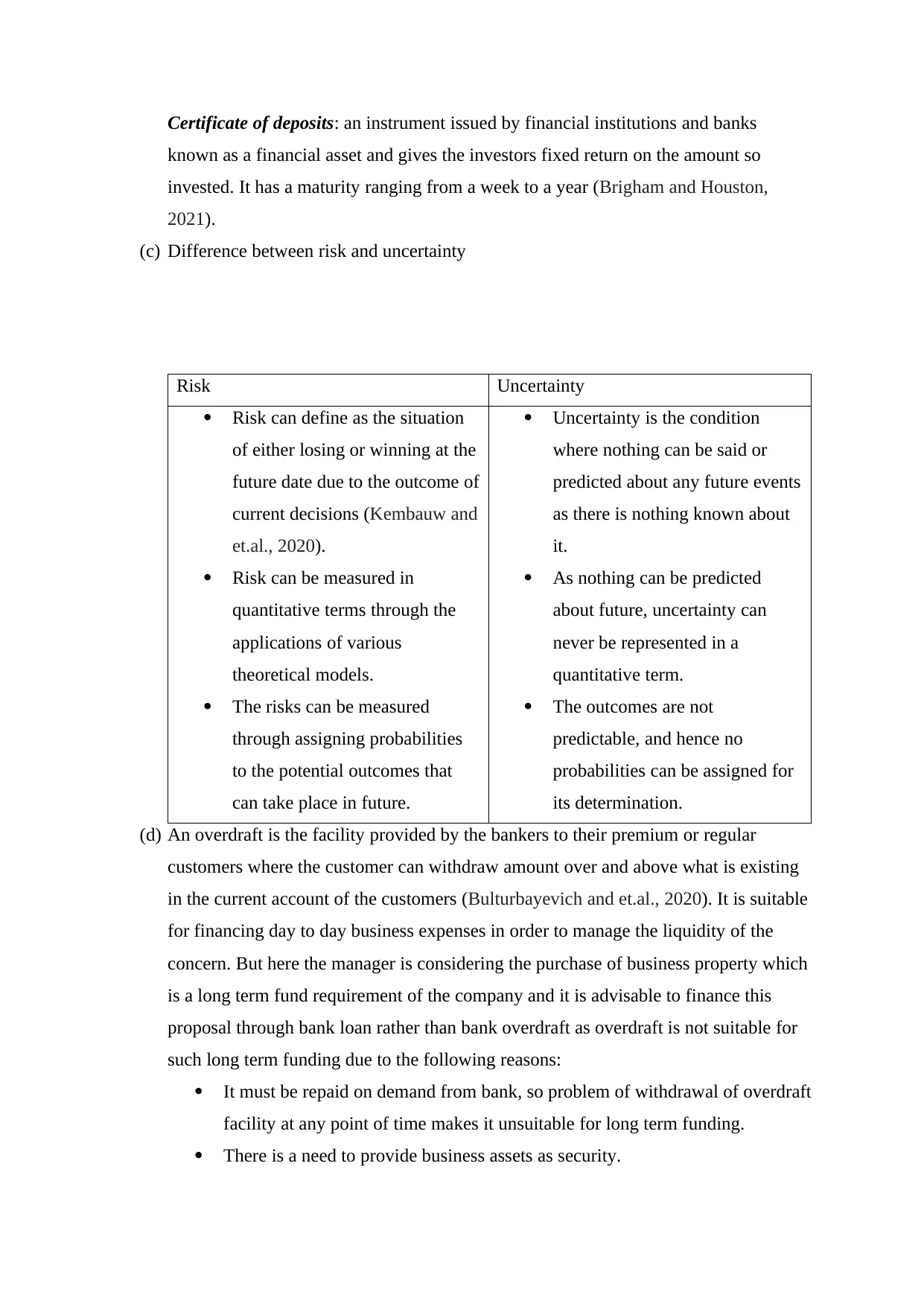

(c) Difference between risk and uncertainty

Risk Uncertainty

Risk can define as the situation

of either losing or winning at the

future date due to the outcome of

current decisions (Kembauw and

et.al., 2020).

Risk can be measured in

quantitative terms through the

applications of various

theoretical models.

The risks can be measured

through assigning probabilities

to the potential outcomes that

can take place in future.

Uncertainty is the condition

where nothing can be said or

predicted about any future events

as there is nothing known about

it.

As nothing can be predicted

about future, uncertainty can

never be represented in a

quantitative term.

The outcomes are not

predictable, and hence no

probabilities can be assigned for

its determination.

(d) An overdraft is the facility provided by the bankers to their premium or regular

customers where the customer can withdraw amount over and above what is existing

in the current account of the customers (Bulturbayevich and et.al., 2020). It is suitable

for financing day to day business expenses in order to manage the liquidity of the

concern. But here the manager is considering the purchase of business property which

is a long term fund requirement of the company and it is advisable to finance this

proposal through bank loan rather than bank overdraft as overdraft is not suitable for

such long term funding due to the following reasons:

It must be repaid on demand from bank, so problem of withdrawal of overdraft

facility at any point of time makes it unsuitable for long term funding.

There is a need to provide business assets as security.

known as a financial asset and gives the investors fixed return on the amount so

invested. It has a maturity ranging from a week to a year (Brigham and Houston,

2021).

(c) Difference between risk and uncertainty

Risk Uncertainty

Risk can define as the situation

of either losing or winning at the

future date due to the outcome of

current decisions (Kembauw and

et.al., 2020).

Risk can be measured in

quantitative terms through the

applications of various

theoretical models.

The risks can be measured

through assigning probabilities

to the potential outcomes that

can take place in future.

Uncertainty is the condition

where nothing can be said or

predicted about any future events

as there is nothing known about

it.

As nothing can be predicted

about future, uncertainty can

never be represented in a

quantitative term.

The outcomes are not

predictable, and hence no

probabilities can be assigned for

its determination.

(d) An overdraft is the facility provided by the bankers to their premium or regular

customers where the customer can withdraw amount over and above what is existing

in the current account of the customers (Bulturbayevich and et.al., 2020). It is suitable

for financing day to day business expenses in order to manage the liquidity of the

concern. But here the manager is considering the purchase of business property which

is a long term fund requirement of the company and it is advisable to finance this

proposal through bank loan rather than bank overdraft as overdraft is not suitable for

such long term funding due to the following reasons:

It must be repaid on demand from bank, so problem of withdrawal of overdraft

facility at any point of time makes it unsuitable for long term funding.

There is a need to provide business assets as security.

The cost derived from interest rates are much higher in case of overdraft

facility if it is used for long term aspect.

CONCLUSION

From the above report it has been concluded that management of every company must

give enough considerations towards the financial management aspects of the business. The

minor mistakes in financial decision making can bring huge losses to the business and even

leads to the failure of the concern.

REFERENCES

Bulturbayevich, M. B., and et.al., 2020. Modern features of financial management in small

businesses. International Engineering Journal For Research & Development, 5(4),

pp.5-5.

Kembauw, E., and et.al., 2020. Strategies of Financial Management Quality Control in

Busines

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Yap, R. J. C., Komalasari, F. and Hadiansah, I., 2018. The effect of financial literacy and

attitude on financial management behavior and satisfaction. BISNIS & BIROKRASI:

Jurnal Ilmu Administrasi dan Organisasi, 23(3).

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley &

Sons.

Siminica, M., Motoi, A. G. and Dumitru, A., 2017. Financial management as component of

tactical management. Polish Journal of Management Studies, 15.

Madura, J., 2020. International financial management. Cengage Learning.

Plaskova, N. S., Prodanova, N. A. and Reshetov, K. Y., 2020. Dealing Operations as a Means

of Improving the Efficiency of the Financial Management of a Production Company.

In Complex Systems: Innovation and Sustainability in the Digital Age (pp. 61-70).

Springer, Cham.

Haydarov, U., 2020. Financial management system, tools, sources of investment activities

and factors. Архив научных исследований, 35.

Dwiastanti, A., 2017. Analysis of financial knowledge and financial attitude on locus of

control and financial management behavior. MBR (Management and Business

Review), 1(1), pp.1-8.

Illmeyer, M., and et.al., 2017. The impact of financial management on

innovation. Entrepreneurship and Sustainability Issues, 5(1), pp.58-71.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management: Concise.

Cengage Learning.

facility if it is used for long term aspect.

CONCLUSION

From the above report it has been concluded that management of every company must

give enough considerations towards the financial management aspects of the business. The

minor mistakes in financial decision making can bring huge losses to the business and even

leads to the failure of the concern.

REFERENCES

Bulturbayevich, M. B., and et.al., 2020. Modern features of financial management in small

businesses. International Engineering Journal For Research & Development, 5(4),

pp.5-5.

Kembauw, E., and et.al., 2020. Strategies of Financial Management Quality Control in

Busines

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Yap, R. J. C., Komalasari, F. and Hadiansah, I., 2018. The effect of financial literacy and

attitude on financial management behavior and satisfaction. BISNIS & BIROKRASI:

Jurnal Ilmu Administrasi dan Organisasi, 23(3).

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley &

Sons.

Siminica, M., Motoi, A. G. and Dumitru, A., 2017. Financial management as component of

tactical management. Polish Journal of Management Studies, 15.

Madura, J., 2020. International financial management. Cengage Learning.

Plaskova, N. S., Prodanova, N. A. and Reshetov, K. Y., 2020. Dealing Operations as a Means

of Improving the Efficiency of the Financial Management of a Production Company.

In Complex Systems: Innovation and Sustainability in the Digital Age (pp. 61-70).

Springer, Cham.

Haydarov, U., 2020. Financial management system, tools, sources of investment activities

and factors. Архив научных исследований, 35.

Dwiastanti, A., 2017. Analysis of financial knowledge and financial attitude on locus of

control and financial management behavior. MBR (Management and Business

Review), 1(1), pp.1-8.

Illmeyer, M., and et.al., 2017. The impact of financial management on

innovation. Entrepreneurship and Sustainability Issues, 5(1), pp.58-71.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management: Concise.

Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.