Financial Management: Valuation Techniques, Problems, and Appraisal

VerifiedAdded on 2023/01/11

|15

|3763

|50

Report

AI Summary

This report delves into financial management, exploring various valuation techniques and investment appraisal methods. It begins by explaining the price-earnings ratio, dividend valuation method, and discounted cash flow method, providing calculations and examples for each. The report also addresses the problems associated with these valuation techniques, offering a critical analysis of their limitations. Furthermore, it examines investment appraisal techniques, including the payback period, accounting rate of return, net present value, and internal rate of return, with detailed computations and interpretations. The benefits and limitations of these investment appraisal tools are evaluated, providing a comprehensive understanding of their application in financial decision-making.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 2...................................................................................................................................1

a) Price Earning Ratio..................................................................................................................1

b) Dividend Valuation Method....................................................................................................1

c) Discounted cash flow method..................................................................................................2

d) Problems associated with the valuation techniques.................................................................3

QUESTION 3...................................................................................................................................7

1. Application of various investment appraisal techniques.........................................................7

2. Evaluating benefits and limitation of investment appraisal tool ............................................9

REFERENCES..............................................................................................................................13

QUESTION 2...................................................................................................................................1

a) Price Earning Ratio..................................................................................................................1

b) Dividend Valuation Method....................................................................................................1

c) Discounted cash flow method..................................................................................................2

d) Problems associated with the valuation techniques.................................................................3

QUESTION 3...................................................................................................................................7

1. Application of various investment appraisal techniques.........................................................7

2. Evaluating benefits and limitation of investment appraisal tool ............................................9

REFERENCES..............................................................................................................................13

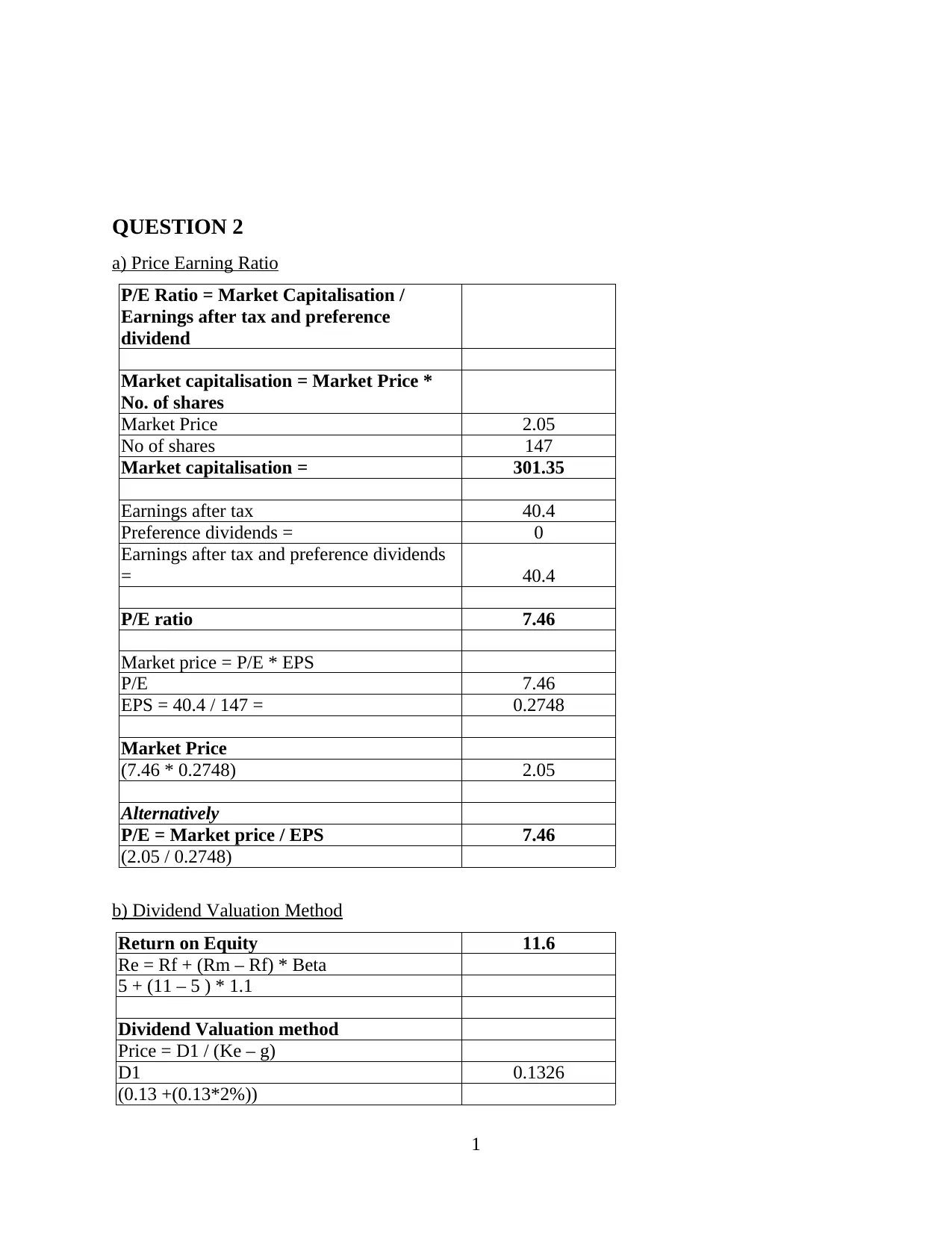

QUESTION 2

a) Price Earning Ratio

P/E Ratio = Market Capitalisation /

Earnings after tax and preference

dividend

Market capitalisation = Market Price *

No. of shares

Market Price 2.05

No of shares 147

Market capitalisation = 301.35

Earnings after tax 40.4

Preference dividends = 0

Earnings after tax and preference dividends

= 40.4

P/E ratio 7.46

Market price = P/E * EPS

P/E 7.46

EPS = 40.4 / 147 = 0.2748

Market Price

(7.46 * 0.2748) 2.05

Alternatively

P/E = Market price / EPS 7.46

(2.05 / 0.2748)

b) Dividend Valuation Method

Return on Equity 11.6

Re = Rf + (Rm – Rf) * Beta

5 + (11 – 5 ) * 1.1

Dividend Valuation method

Price = D1 / (Ke – g)

D1 0.1326

(0.13 +(0.13*2%))

1

a) Price Earning Ratio

P/E Ratio = Market Capitalisation /

Earnings after tax and preference

dividend

Market capitalisation = Market Price *

No. of shares

Market Price 2.05

No of shares 147

Market capitalisation = 301.35

Earnings after tax 40.4

Preference dividends = 0

Earnings after tax and preference dividends

= 40.4

P/E ratio 7.46

Market price = P/E * EPS

P/E 7.46

EPS = 40.4 / 147 = 0.2748

Market Price

(7.46 * 0.2748) 2.05

Alternatively

P/E = Market price / EPS 7.46

(2.05 / 0.2748)

b) Dividend Valuation Method

Return on Equity 11.6

Re = Rf + (Rm – Rf) * Beta

5 + (11 – 5 ) * 1.1

Dividend Valuation method

Price = D1 / (Ke – g)

D1 0.1326

(0.13 +(0.13*2%))

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ke 11.60%

g 2.00%

Price = D1 / (Ke – g) 1.38

(0.1326 / (0.116 – 0.02)

c) Discounted cash flow method

Discounted cash flow method

WACC

Cost of equity 11.60%

Cost of debt 5.60%

(7% * (1-tax rate)

Weights

Equity 0.67

(147 / 219)

Debt 0.33

(72 / 219)

WACC 9.63%

(11.60% * 0.67)+(5.60% * 0.33)

Year

Cash flow

@g=2%

Discount @

9.63%

Present

value

1 40.4 0.912 36.86

2 41.2 0.832 34.31

3 42.0 0.760 31.93

4 42.9 0.693 29.71

5 43.7 0.632 27.65

6 44.6 0.577 25.73

Discounted cash flow = FCFF / (Kc – g)

FCFF 5 27.65

Present value of FCFF 6 25.73

44.6 / (1.096)^6

Kc 9.63%

g 2.00%

Value of the firm 338.5

Alternatively

2

g 2.00%

Price = D1 / (Ke – g) 1.38

(0.1326 / (0.116 – 0.02)

c) Discounted cash flow method

Discounted cash flow method

WACC

Cost of equity 11.60%

Cost of debt 5.60%

(7% * (1-tax rate)

Weights

Equity 0.67

(147 / 219)

Debt 0.33

(72 / 219)

WACC 9.63%

(11.60% * 0.67)+(5.60% * 0.33)

Year

Cash flow

@g=2%

Discount @

9.63%

Present

value

1 40.4 0.912 36.86

2 41.2 0.832 34.31

3 42.0 0.760 31.93

4 42.9 0.693 29.71

5 43.7 0.632 27.65

6 44.6 0.577 25.73

Discounted cash flow = FCFF / (Kc – g)

FCFF 5 27.65

Present value of FCFF 6 25.73

44.6 / (1.096)^6

Kc 9.63%

g 2.00%

Value of the firm 338.5

Alternatively

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

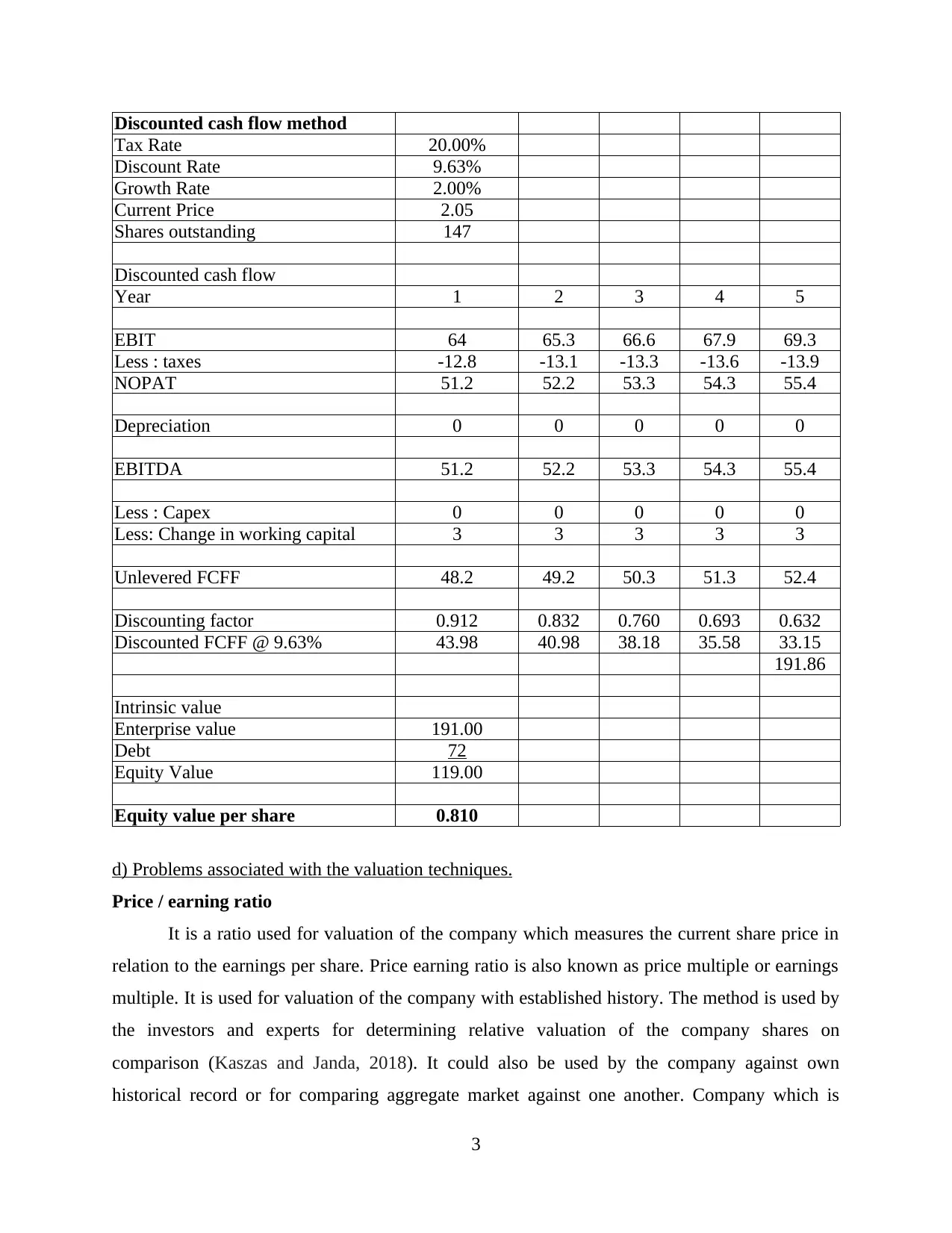

Discounted cash flow method

Tax Rate 20.00%

Discount Rate 9.63%

Growth Rate 2.00%

Current Price 2.05

Shares outstanding 147

Discounted cash flow

Year 1 2 3 4 5

EBIT 64 65.3 66.6 67.9 69.3

Less : taxes -12.8 -13.1 -13.3 -13.6 -13.9

NOPAT 51.2 52.2 53.3 54.3 55.4

Depreciation 0 0 0 0 0

EBITDA 51.2 52.2 53.3 54.3 55.4

Less : Capex 0 0 0 0 0

Less: Change in working capital 3 3 3 3 3

Unlevered FCFF 48.2 49.2 50.3 51.3 52.4

Discounting factor 0.912 0.832 0.760 0.693 0.632

Discounted FCFF @ 9.63% 43.98 40.98 38.18 35.58 33.15

191.86

Intrinsic value

Enterprise value 191.00

Debt 72

Equity Value 119.00

Equity value per share 0.810

d) Problems associated with the valuation techniques.

Price / earning ratio

It is a ratio used for valuation of the company which measures the current share price in

relation to the earnings per share. Price earning ratio is also known as price multiple or earnings

multiple. It is used for valuation of the company with established history. The method is used by

the investors and experts for determining relative valuation of the company shares on

comparison (Kaszas and Janda, 2018). It could also be used by the company against own

historical record or for comparing aggregate market against one another. Company which is

3

Tax Rate 20.00%

Discount Rate 9.63%

Growth Rate 2.00%

Current Price 2.05

Shares outstanding 147

Discounted cash flow

Year 1 2 3 4 5

EBIT 64 65.3 66.6 67.9 69.3

Less : taxes -12.8 -13.1 -13.3 -13.6 -13.9

NOPAT 51.2 52.2 53.3 54.3 55.4

Depreciation 0 0 0 0 0

EBITDA 51.2 52.2 53.3 54.3 55.4

Less : Capex 0 0 0 0 0

Less: Change in working capital 3 3 3 3 3

Unlevered FCFF 48.2 49.2 50.3 51.3 52.4

Discounting factor 0.912 0.832 0.760 0.693 0.632

Discounted FCFF @ 9.63% 43.98 40.98 38.18 35.58 33.15

191.86

Intrinsic value

Enterprise value 191.00

Debt 72

Equity Value 119.00

Equity value per share 0.810

d) Problems associated with the valuation techniques.

Price / earning ratio

It is a ratio used for valuation of the company which measures the current share price in

relation to the earnings per share. Price earning ratio is also known as price multiple or earnings

multiple. It is used for valuation of the company with established history. The method is used by

the investors and experts for determining relative valuation of the company shares on

comparison (Kaszas and Janda, 2018). It could also be used by the company against own

historical record or for comparing aggregate market against one another. Company which is

3

having higher ratio shows that the share prices are over valued or the investors of company are

expecting higher growth rates. Price earning ratio is determined by dividing the market price of

share with the earnings per share.

There are limitations of the above approach. True value of the shares could not be

determined using earnings of current year. Value depends over the expected value of future cash

flows and the earnings of company. It is used as good starting but does not always give the true

value of the shares. It is a simple tool for assessing the value of company. It is used by many of

the investors due to the growth rate. Earnings of the enterprise are affected from various factors

which obstructs true nature of earnings metric. The earnings could be manipulated by the

management of company for meeting the earning expectations of shareholders (Dutta, Saha and

Das, 2018). Investors are required to be aware about the manner in which companies are arriving

at the reported EPS. Adjustments are required to be done for obtaining more accurate for

earnings than one reported in income statement. Market price of the company is directly

available in the market but it is difficult to obtain the right earnings per share as actual shares are

difficult to obtain. Higher Price earning represents the stocks as overvalued. The process is used

by the Alzec for valuing the Price earning of Trojan plc for its valuation.

Dividend valuation method

Dividend discount model is used for estimating price of shares of company. Model is

based over theory that present value of stock is equivalent to present value of the future

dividends after discounting them back. In situations where present value is higher under DDM as

compared with current price it means stock is overvalued and it will be beneficial for the

investors to buy the securities. It is the formula used for determining overall value of the stock.

After the value is determined it is used for comparing current market prices of the stocks. It

enables the investors to identify whether the shares of company are undervalues or overvalued. It

is also known as dividend discount model (Khatik and Patil, 2018). The model uses future

dividends for making predictions over the share values. This is based over the idea that

investments are being made for earning dividends.

It is a conservative model used for valuation of the stocks. It does not requires

assumptions for growth for creating the value. Growth rate of the dividends could not be higher

than return rate. The method is easy to understand as it could be used for any stock which is

offering dividend. It gives more control on the investment options as the actual value of the

4

expecting higher growth rates. Price earning ratio is determined by dividing the market price of

share with the earnings per share.

There are limitations of the above approach. True value of the shares could not be

determined using earnings of current year. Value depends over the expected value of future cash

flows and the earnings of company. It is used as good starting but does not always give the true

value of the shares. It is a simple tool for assessing the value of company. It is used by many of

the investors due to the growth rate. Earnings of the enterprise are affected from various factors

which obstructs true nature of earnings metric. The earnings could be manipulated by the

management of company for meeting the earning expectations of shareholders (Dutta, Saha and

Das, 2018). Investors are required to be aware about the manner in which companies are arriving

at the reported EPS. Adjustments are required to be done for obtaining more accurate for

earnings than one reported in income statement. Market price of the company is directly

available in the market but it is difficult to obtain the right earnings per share as actual shares are

difficult to obtain. Higher Price earning represents the stocks as overvalued. The process is used

by the Alzec for valuing the Price earning of Trojan plc for its valuation.

Dividend valuation method

Dividend discount model is used for estimating price of shares of company. Model is

based over theory that present value of stock is equivalent to present value of the future

dividends after discounting them back. In situations where present value is higher under DDM as

compared with current price it means stock is overvalued and it will be beneficial for the

investors to buy the securities. It is the formula used for determining overall value of the stock.

After the value is determined it is used for comparing current market prices of the stocks. It

enables the investors to identify whether the shares of company are undervalues or overvalued. It

is also known as dividend discount model (Khatik and Patil, 2018). The model uses future

dividends for making predictions over the share values. This is based over the idea that

investments are being made for earning dividends.

It is a conservative model used for valuation of the stocks. It does not requires

assumptions for growth for creating the value. Growth rate of the dividends could not be higher

than return rate. The method is easy to understand as it could be used for any stock which is

offering dividend. It gives more control on the investment options as the actual value of the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shares is easily identified. It gives the time to investors for comparing the stock which are

overpriced. Investors use the model for growing value of the portfolio. The model provides the

base to decide about the investment plan when investors decide to make investments over several

stocks.

There are also some drawbacks associated with the method. In the real market value of

dividend do not grow at specific rate till end of the period. Some firm may increase where some

may decrease the dividends which makes the comparison irrelevant. The method is applicable

only on the companies that pay dividends which makes the comparison between small cap and

large companies vague. Dividend discount model does not consider the non dividend factor in

the calculations such as brand loyalty, customer retention and ownership of the intangible assets.

It means valuation model will not be producing desired results even it is calculated correctly. The

method values dividends as the return over investment (Prohaska, Uroda and Peša, 2017).

Discounted cash flow method

It is a valuation technique which is used by the company for projecting the future cah

flows and using net present value method for valuing the cash flows. In this analysis cash flows

of the company are projected using various assumptions like business will be performing in

future and forecasting how the business performance is translated into cash flows which are

generated by business. It is used in various situations as measures value created by the business

directly. It is most theoretically right valuation method. Value of firm is determined from

inherent value of the future cash flows. It is broadly used technique of valuation because of the

theoretical underpinning and ability of using all the scenarios. It is used by corporate finance,

investment bankers and professional of business developments. Valuation which is obtained is

sensitive to various assumptions and forecasts that could vary over wide range. One wrong

assumptions could lead the valuation to go over completely different direction. DCF involve

prediction of the future event over most reliable estimates. The method do not consider market

related information for the valuation like valuation of the comparable firms. The method is

suggested to be done along with other method that consider market forces in the valuation.

It is extremely useful tool when growth rate assumed for series of the period is justifiable

by operating performance of company (Wu and et.al., 2016). It is difficult to estimate growth

rate accurately and correctly. Calculation of the WACC may not be applicable over the real

world. It requires also the projections to be made for capital expenditures in the coming years. In

5

overpriced. Investors use the model for growing value of the portfolio. The model provides the

base to decide about the investment plan when investors decide to make investments over several

stocks.

There are also some drawbacks associated with the method. In the real market value of

dividend do not grow at specific rate till end of the period. Some firm may increase where some

may decrease the dividends which makes the comparison irrelevant. The method is applicable

only on the companies that pay dividends which makes the comparison between small cap and

large companies vague. Dividend discount model does not consider the non dividend factor in

the calculations such as brand loyalty, customer retention and ownership of the intangible assets.

It means valuation model will not be producing desired results even it is calculated correctly. The

method values dividends as the return over investment (Prohaska, Uroda and Peša, 2017).

Discounted cash flow method

It is a valuation technique which is used by the company for projecting the future cah

flows and using net present value method for valuing the cash flows. In this analysis cash flows

of the company are projected using various assumptions like business will be performing in

future and forecasting how the business performance is translated into cash flows which are

generated by business. It is used in various situations as measures value created by the business

directly. It is most theoretically right valuation method. Value of firm is determined from

inherent value of the future cash flows. It is broadly used technique of valuation because of the

theoretical underpinning and ability of using all the scenarios. It is used by corporate finance,

investment bankers and professional of business developments. Valuation which is obtained is

sensitive to various assumptions and forecasts that could vary over wide range. One wrong

assumptions could lead the valuation to go over completely different direction. DCF involve

prediction of the future event over most reliable estimates. The method do not consider market

related information for the valuation like valuation of the comparable firms. The method is

suggested to be done along with other method that consider market forces in the valuation.

It is extremely useful tool when growth rate assumed for series of the period is justifiable

by operating performance of company (Wu and et.al., 2016). It is difficult to estimate growth

rate accurately and correctly. Calculation of the WACC may not be applicable over the real

world. It requires also the projections to be made for capital expenditures in the coming years. In

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

real world it may not prove to be true. The technique is time intensive in relation with other

techniques used for valuation by the companies.

The board of Aztec should adopt for price earning ratio for valuing the shares of

company. The valuation technique is more reliable and accurate as compared with other

techniques. The technique considers earnings of the company and market price which could be

more reliably derived as compared with other components in other techniques. The technique

considers both the earnings of company and market factors that is price of shares prevailing in

market. Therefore the boars should choose price earning method for valuation.

6

techniques used for valuation by the companies.

The board of Aztec should adopt for price earning ratio for valuing the shares of

company. The valuation technique is more reliable and accurate as compared with other

techniques. The technique considers earnings of the company and market price which could be

more reliably derived as compared with other components in other techniques. The technique

considers both the earnings of company and market factors that is price of shares prevailing in

market. Therefore the boars should choose price earning method for valuation.

6

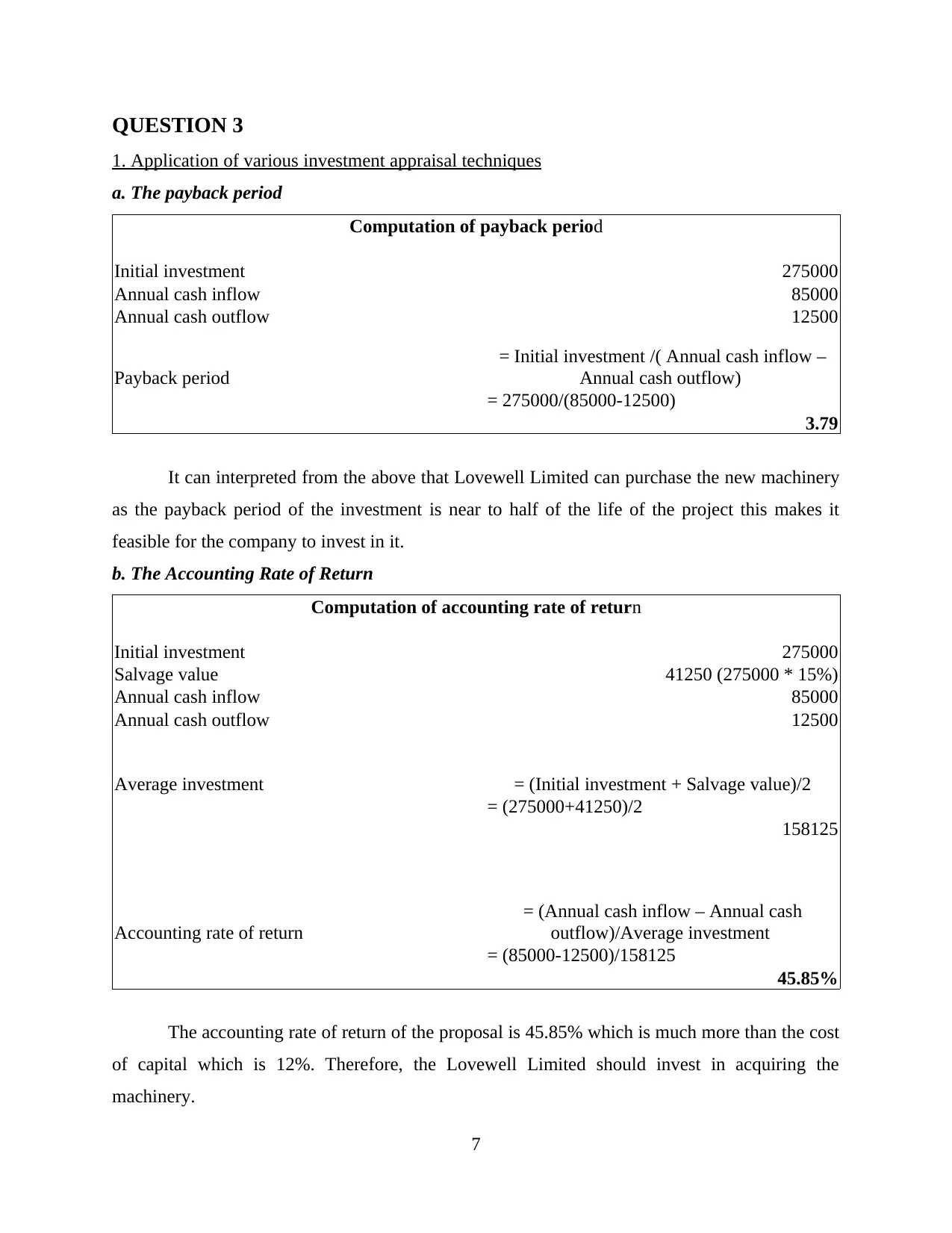

QUESTION 3

1. Application of various investment appraisal techniques

a. The payback period

Computation of payback period

Initial investment 275000

Annual cash inflow 85000

Annual cash outflow 12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79

It can interpreted from the above that Lovewell Limited can purchase the new machinery

as the payback period of the investment is near to half of the life of the project this makes it

feasible for the company to invest in it.

b. The Accounting Rate of Return

Computation of accounting rate of return

Initial investment 275000

Salvage value 41250 (275000 * 15%)

Annual cash inflow 85000

Annual cash outflow 12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

158125

Accounting rate of return

= (Annual cash inflow – Annual cash

outflow)/Average investment

= (85000-12500)/158125

45.85%

The accounting rate of return of the proposal is 45.85% which is much more than the cost

of capital which is 12%. Therefore, the Lovewell Limited should invest in acquiring the

machinery.

7

1. Application of various investment appraisal techniques

a. The payback period

Computation of payback period

Initial investment 275000

Annual cash inflow 85000

Annual cash outflow 12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79

It can interpreted from the above that Lovewell Limited can purchase the new machinery

as the payback period of the investment is near to half of the life of the project this makes it

feasible for the company to invest in it.

b. The Accounting Rate of Return

Computation of accounting rate of return

Initial investment 275000

Salvage value 41250 (275000 * 15%)

Annual cash inflow 85000

Annual cash outflow 12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

158125

Accounting rate of return

= (Annual cash inflow – Annual cash

outflow)/Average investment

= (85000-12500)/158125

45.85%

The accounting rate of return of the proposal is 45.85% which is much more than the cost

of capital which is 12%. Therefore, the Lovewell Limited should invest in acquiring the

machinery.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

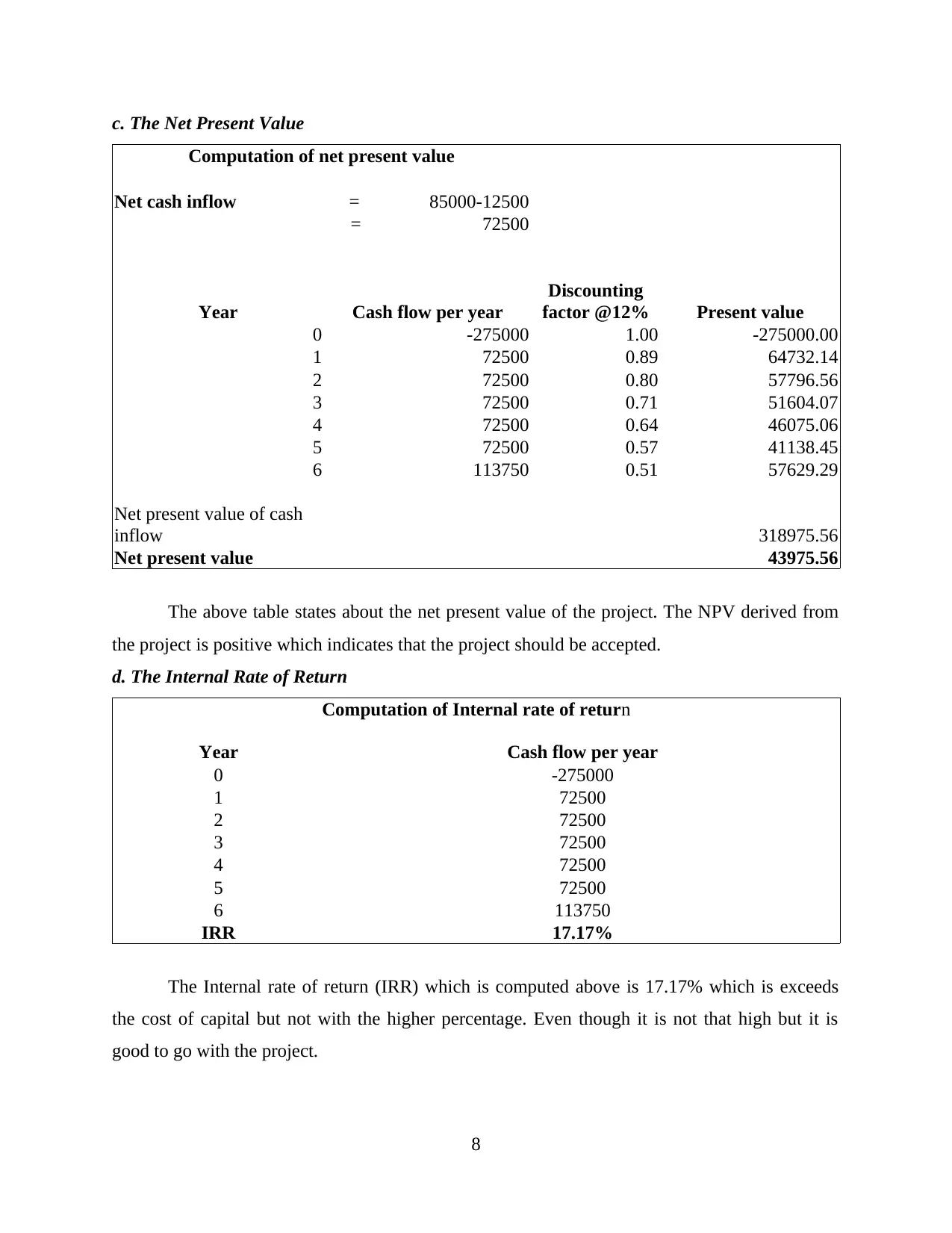

c. The Net Present Value

Computation of net present value

Net cash inflow = 85000-12500

= 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

5 72500 0.57 41138.45

6 113750 0.51 57629.29

Net present value of cash

inflow 318975.56

Net present value 43975.56

The above table states about the net present value of the project. The NPV derived from

the project is positive which indicates that the project should be accepted.

d. The Internal Rate of Return

Computation of Internal rate of return

Year Cash flow per year

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

IRR 17.17%

The Internal rate of return (IRR) which is computed above is 17.17% which is exceeds

the cost of capital but not with the higher percentage. Even though it is not that high but it is

good to go with the project.

8

Computation of net present value

Net cash inflow = 85000-12500

= 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

5 72500 0.57 41138.45

6 113750 0.51 57629.29

Net present value of cash

inflow 318975.56

Net present value 43975.56

The above table states about the net present value of the project. The NPV derived from

the project is positive which indicates that the project should be accepted.

d. The Internal Rate of Return

Computation of Internal rate of return

Year Cash flow per year

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

IRR 17.17%

The Internal rate of return (IRR) which is computed above is 17.17% which is exceeds

the cost of capital but not with the higher percentage. Even though it is not that high but it is

good to go with the project.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thus, based on the above evaluation, it can be said that it is profitable and feasible for

Lovewell Limited to acquire the new machinery as it is turned out be positive under each

investment appraisal technique.

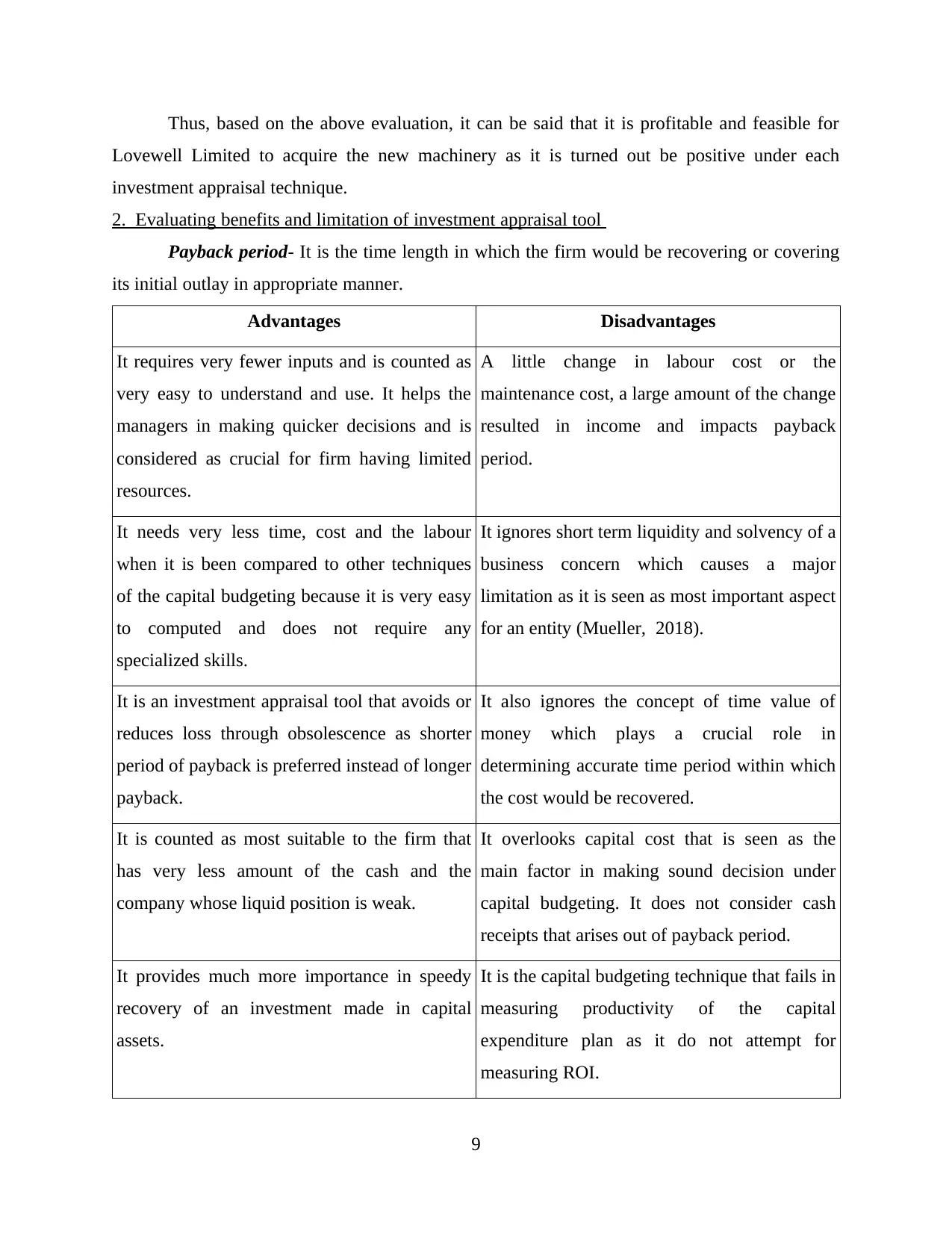

2. Evaluating benefits and limitation of investment appraisal tool

Payback period- It is the time length in which the firm would be recovering or covering

its initial outlay in appropriate manner.

Advantages Disadvantages

It requires very fewer inputs and is counted as

very easy to understand and use. It helps the

managers in making quicker decisions and is

considered as crucial for firm having limited

resources.

A little change in labour cost or the

maintenance cost, a large amount of the change

resulted in income and impacts payback

period.

It needs very less time, cost and the labour

when it is been compared to other techniques

of the capital budgeting because it is very easy

to computed and does not require any

specialized skills.

It ignores short term liquidity and solvency of a

business concern which causes a major

limitation as it is seen as most important aspect

for an entity (Mueller, 2018).

It is an investment appraisal tool that avoids or

reduces loss through obsolescence as shorter

period of payback is preferred instead of longer

payback.

It also ignores the concept of time value of

money which plays a crucial role in

determining accurate time period within which

the cost would be recovered.

It is counted as most suitable to the firm that

has very less amount of the cash and the

company whose liquid position is weak.

It overlooks capital cost that is seen as the

main factor in making sound decision under

capital budgeting. It does not consider cash

receipts that arises out of payback period.

It provides much more importance in speedy

recovery of an investment made in capital

assets.

It is the capital budgeting technique that fails in

measuring productivity of the capital

expenditure plan as it do not attempt for

measuring ROI.

9

Lovewell Limited to acquire the new machinery as it is turned out be positive under each

investment appraisal technique.

2. Evaluating benefits and limitation of investment appraisal tool

Payback period- It is the time length in which the firm would be recovering or covering

its initial outlay in appropriate manner.

Advantages Disadvantages

It requires very fewer inputs and is counted as

very easy to understand and use. It helps the

managers in making quicker decisions and is

considered as crucial for firm having limited

resources.

A little change in labour cost or the

maintenance cost, a large amount of the change

resulted in income and impacts payback

period.

It needs very less time, cost and the labour

when it is been compared to other techniques

of the capital budgeting because it is very easy

to computed and does not require any

specialized skills.

It ignores short term liquidity and solvency of a

business concern which causes a major

limitation as it is seen as most important aspect

for an entity (Mueller, 2018).

It is an investment appraisal tool that avoids or

reduces loss through obsolescence as shorter

period of payback is preferred instead of longer

payback.

It also ignores the concept of time value of

money which plays a crucial role in

determining accurate time period within which

the cost would be recovered.

It is counted as most suitable to the firm that

has very less amount of the cash and the

company whose liquid position is weak.

It overlooks capital cost that is seen as the

main factor in making sound decision under

capital budgeting. It does not consider cash

receipts that arises out of payback period.

It provides much more importance in speedy

recovery of an investment made in capital

assets.

It is the capital budgeting technique that fails in

measuring productivity of the capital

expenditure plan as it do not attempt for

measuring ROI.

9

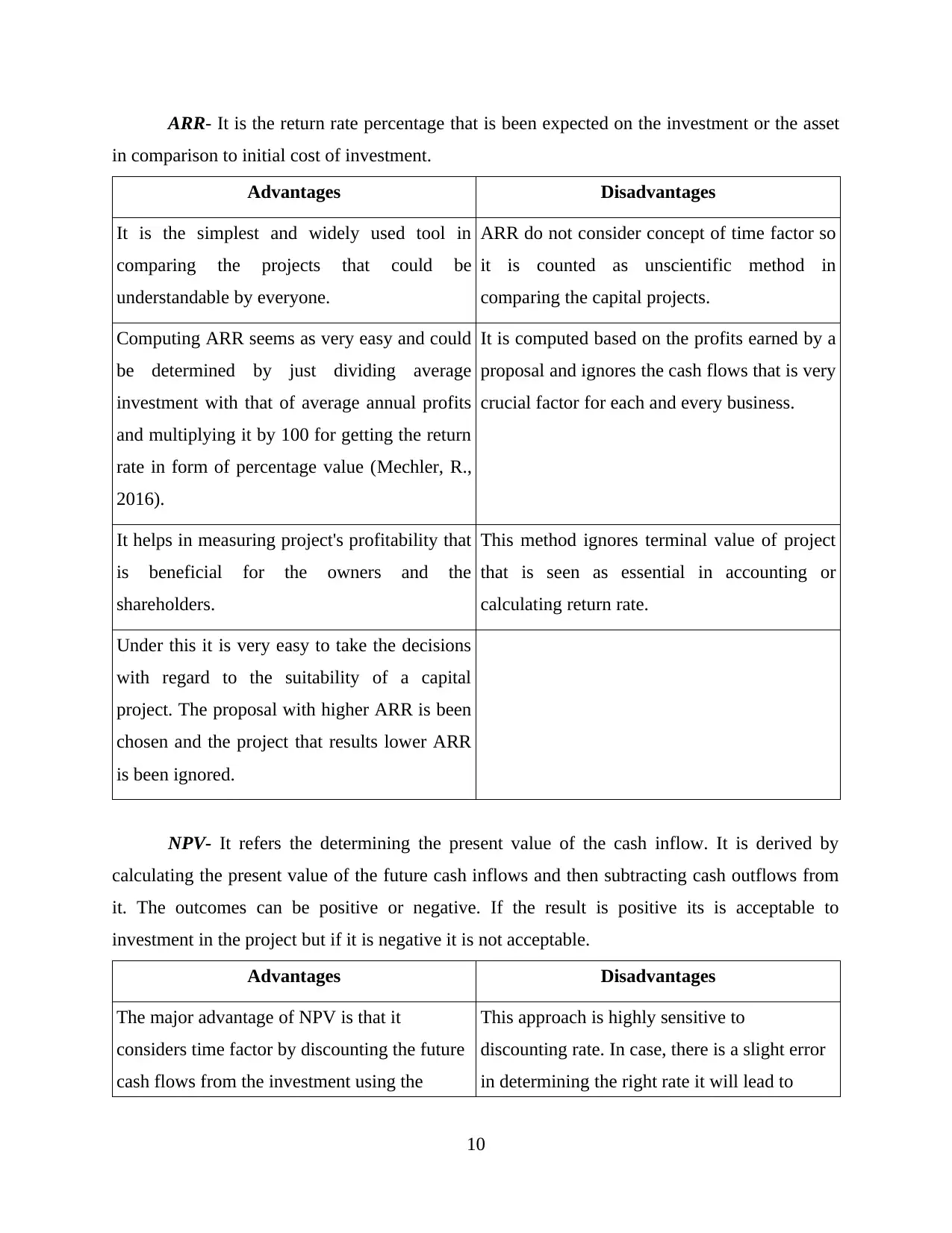

ARR- It is the return rate percentage that is been expected on the investment or the asset

in comparison to initial cost of investment.

Advantages Disadvantages

It is the simplest and widely used tool in

comparing the projects that could be

understandable by everyone.

ARR do not consider concept of time factor so

it is counted as unscientific method in

comparing the capital projects.

Computing ARR seems as very easy and could

be determined by just dividing average

investment with that of average annual profits

and multiplying it by 100 for getting the return

rate in form of percentage value (Mechler, R.,

2016).

It is computed based on the profits earned by a

proposal and ignores the cash flows that is very

crucial factor for each and every business.

It helps in measuring project's profitability that

is beneficial for the owners and the

shareholders.

This method ignores terminal value of project

that is seen as essential in accounting or

calculating return rate.

Under this it is very easy to take the decisions

with regard to the suitability of a capital

project. The proposal with higher ARR is been

chosen and the project that results lower ARR

is been ignored.

NPV- It refers the determining the present value of the cash inflow. It is derived by

calculating the present value of the future cash inflows and then subtracting cash outflows from

it. The outcomes can be positive or negative. If the result is positive its is acceptable to

investment in the project but if it is negative it is not acceptable.

Advantages Disadvantages

The major advantage of NPV is that it

considers time factor by discounting the future

cash flows from the investment using the

This approach is highly sensitive to

discounting rate. In case, there is a slight error

in determining the right rate it will lead to

10

in comparison to initial cost of investment.

Advantages Disadvantages

It is the simplest and widely used tool in

comparing the projects that could be

understandable by everyone.

ARR do not consider concept of time factor so

it is counted as unscientific method in

comparing the capital projects.

Computing ARR seems as very easy and could

be determined by just dividing average

investment with that of average annual profits

and multiplying it by 100 for getting the return

rate in form of percentage value (Mechler, R.,

2016).

It is computed based on the profits earned by a

proposal and ignores the cash flows that is very

crucial factor for each and every business.

It helps in measuring project's profitability that

is beneficial for the owners and the

shareholders.

This method ignores terminal value of project

that is seen as essential in accounting or

calculating return rate.

Under this it is very easy to take the decisions

with regard to the suitability of a capital

project. The proposal with higher ARR is been

chosen and the project that results lower ARR

is been ignored.

NPV- It refers the determining the present value of the cash inflow. It is derived by

calculating the present value of the future cash inflows and then subtracting cash outflows from

it. The outcomes can be positive or negative. If the result is positive its is acceptable to

investment in the project but if it is negative it is not acceptable.

Advantages Disadvantages

The major advantage of NPV is that it

considers time factor by discounting the future

cash flows from the investment using the

This approach is highly sensitive to

discounting rate. In case, there is a slight error

in determining the right rate it will lead to

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.