Financial Management Report: Cost of Capital and Valuation

VerifiedAdded on 2021/01/01

|11

|2815

|486

Report

AI Summary

This report delves into financial management, focusing on cost of capital estimation and business valuation methods. It analyzes the financial statements of Vodafone Group PLC to calculate its cost of capital for equity investors and bondholders, including the 5.9% bond due in 2032. The report explores various valuation techniques, such as market value, asset-based, ROI-based, discounted cash flow (DCF), capitalization of earnings, and multi-stage dividend discount model (DDM). Furthermore, it evaluates the foreign exchange issues related to funds raised from bonds in different countries, addressing fluctuations and political risks. The report provides a comprehensive overview of financial management principles and their practical application, offering valuable insights for financial analysis and decision-making.

Financial

Management in

Organisation

Management in

Organisation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

(a) Methods of Estimating Cost of Capital.............................................................................1

(b) Possible methods of business valuation............................................................................3

(c) Evaluation of foreign exchange issues related to funds raised from bonds in different

countries.................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

(a) Methods of Estimating Cost of Capital.............................................................................1

(b) Possible methods of business valuation............................................................................3

(c) Evaluation of foreign exchange issues related to funds raised from bonds in different

countries.................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial management is considered as an important aspect in any organisation. As it is

very important for any company to be financially strong in order to gain success, stability and

growth. Finance is the most essential element, it is required by every organisation to run it

business successfully or to start the new start-up. It includes various financial statements and

proper analysis in order to formulate new strategies to increase its stability and growth (Banerjee,

2012). This report contains analysis of financial statements of Vodafone Group PLC to calculate

its cost of capital for their equity investor and for the investors of 5.9% bond which is due by

year 2032. This report also talks about various business valuation methods used to compute the

value of any company.

REPORT

(a) Methods of Estimating Cost of Capital

Cost of Capital: Cost of capital is required as a necessary return which is required by

companies to create a capital budgeting project. It is the weighted average of a company's cost of

equity and cost of debt. This metric is used internally to judge that the capital project which

company wants to acquire is worthy of expenditure which will be incurred. To estimate cost of

capital following methods are used:

COST BY SPECIFIC SOURCE OF FINANCE

Cost of Debt: Cost of debt means the interest which the company has to pay to its

debenture holders (Parker, 2012). The debentures can be issued at premium or at par or at

discount or redeemable debentures, to calculate the cost of debentures issued will be

calculate by using the following formula

At Par

Kdb = I/P

where I is interest payable and P is principal

At Discount or Premium

Kdb = I/NP

where I is interest payable and NP is Net Proceeds (principal + premium – discount )

After Tax

Kdb = I/NP (1-t)

1

Financial management is considered as an important aspect in any organisation. As it is

very important for any company to be financially strong in order to gain success, stability and

growth. Finance is the most essential element, it is required by every organisation to run it

business successfully or to start the new start-up. It includes various financial statements and

proper analysis in order to formulate new strategies to increase its stability and growth (Banerjee,

2012). This report contains analysis of financial statements of Vodafone Group PLC to calculate

its cost of capital for their equity investor and for the investors of 5.9% bond which is due by

year 2032. This report also talks about various business valuation methods used to compute the

value of any company.

REPORT

(a) Methods of Estimating Cost of Capital

Cost of Capital: Cost of capital is required as a necessary return which is required by

companies to create a capital budgeting project. It is the weighted average of a company's cost of

equity and cost of debt. This metric is used internally to judge that the capital project which

company wants to acquire is worthy of expenditure which will be incurred. To estimate cost of

capital following methods are used:

COST BY SPECIFIC SOURCE OF FINANCE

Cost of Debt: Cost of debt means the interest which the company has to pay to its

debenture holders (Parker, 2012). The debentures can be issued at premium or at par or at

discount or redeemable debentures, to calculate the cost of debentures issued will be

calculate by using the following formula

At Par

Kdb = I/P

where I is interest payable and P is principal

At Discount or Premium

Kdb = I/NP

where I is interest payable and NP is Net Proceeds (principal + premium – discount )

After Tax

Kdb = I/NP (1-t)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

where I is interest payable, NP is Net Proceeds and t is tax rate

Redeemable Debentures

Kdb = I + 1 / n (RV – NP) / 1 / 2 (RV-NP)

where I is interest payable, NP is Net Proceeds, n is number of years and RV is Redeemable

Value

Cost of Preference Share Capital: Cost of preference share capital is the is the fixed

rate of dividend which is payable to preference shareholders. If company defaults in the

payment of this dividend it affects the company's capacity to raise fund.

At Par

Kp =D/P

where D is Dividend payable and P is principal

At Discount or Premium

Kp = D/NP

where D is Dividend payable and NP is Net Proceeds (principal + premium – discount)

Redeemable Preference Share

Kp = D + 1 / n (MV – NP) / 1 / 2 (MV-NP)

where D is Dividend payable, NP is Net Proceeds, n is number of years and MV is Minimum

Value

Cost of Equity Share Capital: Dividend in the case of equity share capital is not fixed.

Equity shareholders get dividend at fluctuating rate and even some time they are not even

paid. In this case the return may be of different form.

Dividend Per Share

Ke = D/P

Where D is Dividend Paid and P is Principal

Dividend Per Share plus Growth

Ke = D/P + g

Where D is Dividend Paid, P is Principal and g is the growth

Earning Per Share

Ke = EPS/NP

Where EPS is the earning per share and NP is the Net profit.

2

Redeemable Debentures

Kdb = I + 1 / n (RV – NP) / 1 / 2 (RV-NP)

where I is interest payable, NP is Net Proceeds, n is number of years and RV is Redeemable

Value

Cost of Preference Share Capital: Cost of preference share capital is the is the fixed

rate of dividend which is payable to preference shareholders. If company defaults in the

payment of this dividend it affects the company's capacity to raise fund.

At Par

Kp =D/P

where D is Dividend payable and P is principal

At Discount or Premium

Kp = D/NP

where D is Dividend payable and NP is Net Proceeds (principal + premium – discount)

Redeemable Preference Share

Kp = D + 1 / n (MV – NP) / 1 / 2 (MV-NP)

where D is Dividend payable, NP is Net Proceeds, n is number of years and MV is Minimum

Value

Cost of Equity Share Capital: Dividend in the case of equity share capital is not fixed.

Equity shareholders get dividend at fluctuating rate and even some time they are not even

paid. In this case the return may be of different form.

Dividend Per Share

Ke = D/P

Where D is Dividend Paid and P is Principal

Dividend Per Share plus Growth

Ke = D/P + g

Where D is Dividend Paid, P is Principal and g is the growth

Earning Per Share

Ke = EPS/NP

Where EPS is the earning per share and NP is the Net profit.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of Retained Earning: Cost of retained earning is considered as a opportunity cost

of dividend which is foregone by the equity shareholders.

Kr = D/NP + g

where D is Dividend Payable, NP is Net Profit and g is Growth.

WEIGHTED AVERAGE COST OF CAPITAL

Weighted average cost of capital is also known as overall cost of capital. It adds all the

sources through which a company can increase its capital. To calculate the weighted average cost

weights are allotted to various specific cost of capital (Garengo and Biazzo, 2013). These weight

can be either book value or market value. While calculating market value is preferred over the

book value as it shows the actual value of the capital.

I) Calculation of cost of capital for Vodafone Equity providers

Cost of equity of Vodafone is calculated using the following formula:

Ke = D / P

Ke = 3920 / 4238

= 0.924

the above calculation shows the cost of equity as 0.924.

II) Calculation of cost of bond:

Cost of bond= £450 million * 5.9% = £ 26.55 million

(b) Possible methods of business valuation

Business Valuation: A process of estimating an economic value of any firm is known as

business valuation. It is used to determine the fair value of a business which includes the value of

assets and liabilities of the company, it is done for many reasons which include the sale value,

for taxation, for merger or acquisition. Following are the methods which are used for business

valuation:

Market Value Business Valuation Method: This method is considered as the most

subjective approach of valuing a business net worth. In this type of method the value of

business is taken by comparing it with similar business which is sold. This report is

considered to be the challenging report the sole proprietors, as it is difficult to find

comparative data in this case. This method only works for those businesses which have

an access to the sufficient market data of their competitors.

3

of dividend which is foregone by the equity shareholders.

Kr = D/NP + g

where D is Dividend Payable, NP is Net Profit and g is Growth.

WEIGHTED AVERAGE COST OF CAPITAL

Weighted average cost of capital is also known as overall cost of capital. It adds all the

sources through which a company can increase its capital. To calculate the weighted average cost

weights are allotted to various specific cost of capital (Garengo and Biazzo, 2013). These weight

can be either book value or market value. While calculating market value is preferred over the

book value as it shows the actual value of the capital.

I) Calculation of cost of capital for Vodafone Equity providers

Cost of equity of Vodafone is calculated using the following formula:

Ke = D / P

Ke = 3920 / 4238

= 0.924

the above calculation shows the cost of equity as 0.924.

II) Calculation of cost of bond:

Cost of bond= £450 million * 5.9% = £ 26.55 million

(b) Possible methods of business valuation

Business Valuation: A process of estimating an economic value of any firm is known as

business valuation. It is used to determine the fair value of a business which includes the value of

assets and liabilities of the company, it is done for many reasons which include the sale value,

for taxation, for merger or acquisition. Following are the methods which are used for business

valuation:

Market Value Business Valuation Method: This method is considered as the most

subjective approach of valuing a business net worth. In this type of method the value of

business is taken by comparing it with similar business which is sold. This report is

considered to be the challenging report the sole proprietors, as it is difficult to find

comparative data in this case. This method only works for those businesses which have

an access to the sufficient market data of their competitors.

3

Assets Based Business Valuation Methods: in this method of valuation, company's net

assets and net liabilities from the balance are taken into consideration for the valuation of

its business value. To calculate value of business with the help of assets based business

valuation method it uses the net asset value minus net liabilities as given in the balance

sheet.

ROI Based Business Valuation Method: ROI is return on invest which means that in

this method of valuation of business return on investment is taken n to consideration.

Before investing in any thing business always try to find out the return which it will get

from that particular investment. Same in the valuation process of business return is

calculated (Jacque, 2014).

Discounted Cash Flow (DCF) Method: Discounted cash flow method is a method

which uses future projected cash flow to estimate value of company, which is discounted

to its current value. This method is also known as income method as it values business on

a basis of its inflows and outflows of cash from organisation. The main purpose of

Discounted Cash Flow analysis to find out value of investment which investor will get for

his investment. It can be calculated by using following formula:

Capitalization of Earnings Method: For calculation of business value with the help of

this method a company requires its annual ROI, Cash flow and its expected value. This

method of calculation of business value is best preferred for those businesses which are

stable. Capitalization of Earning methods is used to calculate estimate value of business

by using net present value (NPV) of cash flows or profits which is expected in near

future. To determine the value of business using this method it takes the future earnings

of the organisation and divide it with capitalization rate (Sparrow, Farndale and Scullion,

2013).

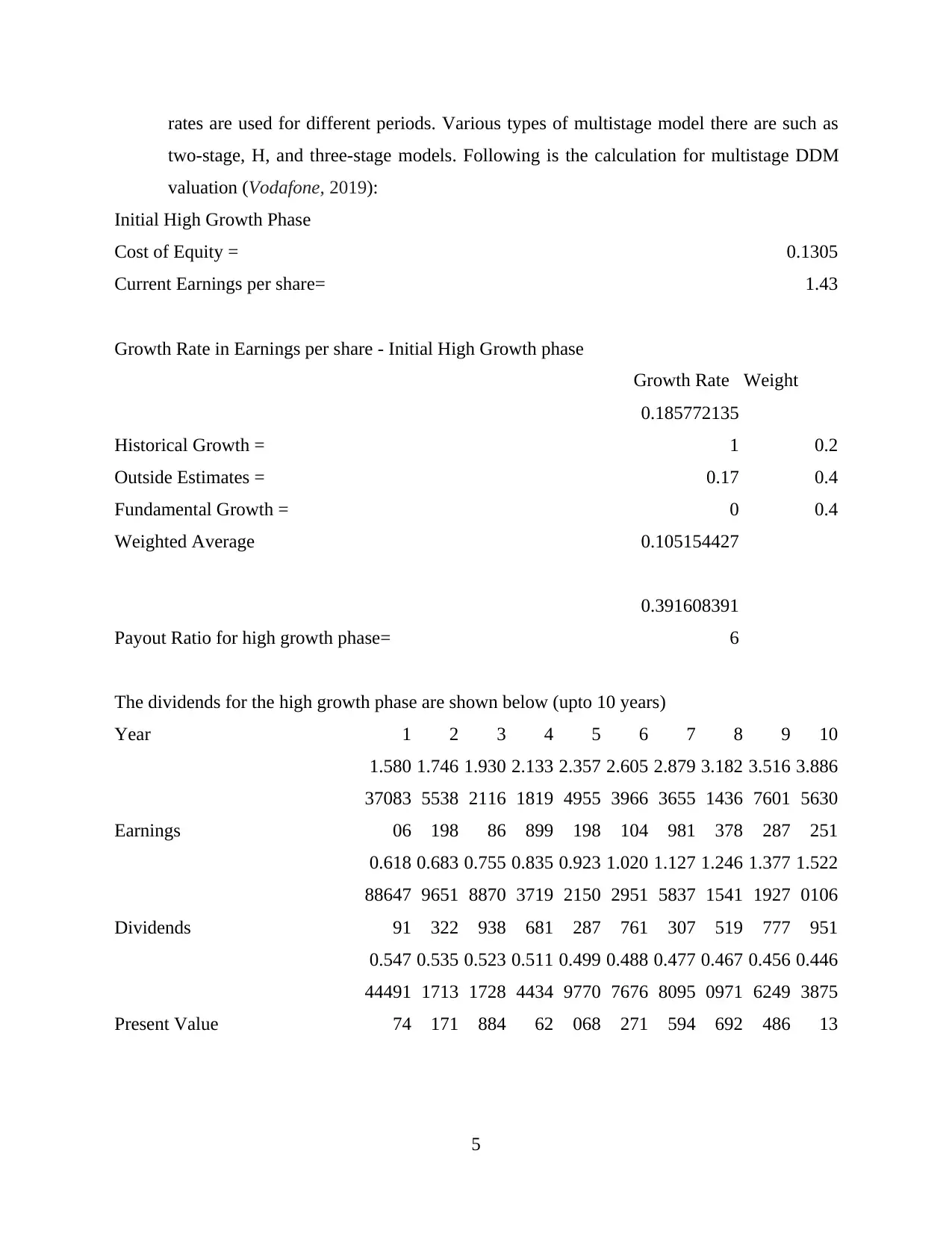

Multiples Stage DDM Method: The multistage dividend discount model is kind of

equity valuation method that developed and based on the Gordon growth model by using

fluctuating growth rates in order to do calculation. Under this model, dynamic growth

4

assets and net liabilities from the balance are taken into consideration for the valuation of

its business value. To calculate value of business with the help of assets based business

valuation method it uses the net asset value minus net liabilities as given in the balance

sheet.

ROI Based Business Valuation Method: ROI is return on invest which means that in

this method of valuation of business return on investment is taken n to consideration.

Before investing in any thing business always try to find out the return which it will get

from that particular investment. Same in the valuation process of business return is

calculated (Jacque, 2014).

Discounted Cash Flow (DCF) Method: Discounted cash flow method is a method

which uses future projected cash flow to estimate value of company, which is discounted

to its current value. This method is also known as income method as it values business on

a basis of its inflows and outflows of cash from organisation. The main purpose of

Discounted Cash Flow analysis to find out value of investment which investor will get for

his investment. It can be calculated by using following formula:

Capitalization of Earnings Method: For calculation of business value with the help of

this method a company requires its annual ROI, Cash flow and its expected value. This

method of calculation of business value is best preferred for those businesses which are

stable. Capitalization of Earning methods is used to calculate estimate value of business

by using net present value (NPV) of cash flows or profits which is expected in near

future. To determine the value of business using this method it takes the future earnings

of the organisation and divide it with capitalization rate (Sparrow, Farndale and Scullion,

2013).

Multiples Stage DDM Method: The multistage dividend discount model is kind of

equity valuation method that developed and based on the Gordon growth model by using

fluctuating growth rates in order to do calculation. Under this model, dynamic growth

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

rates are used for different periods. Various types of multistage model there are such as

two-stage, H, and three-stage models. Following is the calculation for multistage DDM

valuation (Vodafone, 2019):

Initial High Growth Phase

Cost of Equity = 0.1305

Current Earnings per share= 1.43

Growth Rate in Earnings per share - Initial High Growth phase

Growth Rate Weight

Historical Growth =

0.185772135

1 0.2

Outside Estimates = 0.17 0.4

Fundamental Growth = 0 0.4

Weighted Average 0.105154427

Payout Ratio for high growth phase=

0.391608391

6

The dividends for the high growth phase are shown below (upto 10 years)

Year 1 2 3 4 5 6 7 8 9 10

Earnings

1.580

37083

06

1.746

5538

198

1.930

2116

86

2.133

1819

899

2.357

4955

198

2.605

3966

104

2.879

3655

981

3.182

1436

378

3.516

7601

287

3.886

5630

251

Dividends

0.618

88647

91

0.683

9651

322

0.755

8870

938

0.835

3719

681

0.923

2150

287

1.020

2951

761

1.127

5837

307

1.246

1541

519

1.377

1927

777

1.522

0106

951

Present Value

0.547

44491

74

0.535

1713

171

0.523

1728

884

0.511

4434

62

0.499

9770

068

0.488

7676

271

0.477

8095

594

0.467

0971

692

0.456

6249

486

0.446

3875

13

5

two-stage, H, and three-stage models. Following is the calculation for multistage DDM

valuation (Vodafone, 2019):

Initial High Growth Phase

Cost of Equity = 0.1305

Current Earnings per share= 1.43

Growth Rate in Earnings per share - Initial High Growth phase

Growth Rate Weight

Historical Growth =

0.185772135

1 0.2

Outside Estimates = 0.17 0.4

Fundamental Growth = 0 0.4

Weighted Average 0.105154427

Payout Ratio for high growth phase=

0.391608391

6

The dividends for the high growth phase are shown below (upto 10 years)

Year 1 2 3 4 5 6 7 8 9 10

Earnings

1.580

37083

06

1.746

5538

198

1.930

2116

86

2.133

1819

899

2.357

4955

198

2.605

3966

104

2.879

3655

981

3.182

1436

378

3.516

7601

287

3.886

5630

251

Dividends

0.618

88647

91

0.683

9651

322

0.755

8870

938

0.835

3719

681

0.923

2150

287

1.020

2951

761

1.127

5837

307

1.246

1541

519

1.377

1927

777

1.522

0106

951

Present Value

0.547

44491

74

0.535

1713

171

0.523

1728

884

0.511

4434

62

0.499

9770

068

0.488

7676

271

0.477

8095

594

0.467

0971

692

0.456

6249

486

0.446

3875

13

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

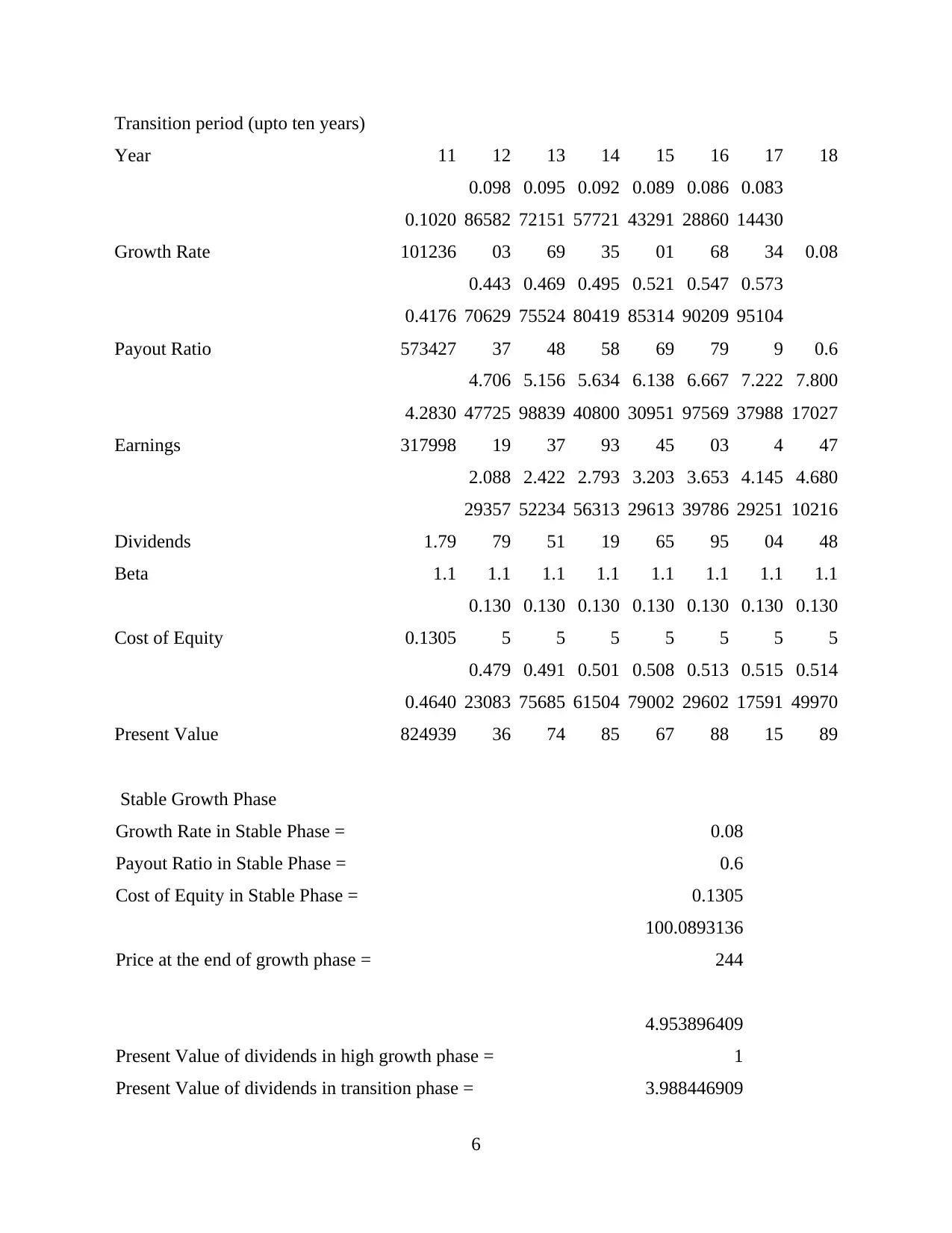

Transition period (upto ten years)

Year 11 12 13 14 15 16 17 18

Growth Rate

0.1020

101236

0.098

86582

03

0.095

72151

69

0.092

57721

35

0.089

43291

01

0.086

28860

68

0.083

14430

34 0.08

Payout Ratio

0.4176

573427

0.443

70629

37

0.469

75524

48

0.495

80419

58

0.521

85314

69

0.547

90209

79

0.573

95104

9 0.6

Earnings

4.2830

317998

4.706

47725

19

5.156

98839

37

5.634

40800

93

6.138

30951

45

6.667

97569

03

7.222

37988

4

7.800

17027

47

Dividends 1.79

2.088

29357

79

2.422

52234

51

2.793

56313

19

3.203

29613

65

3.653

39786

95

4.145

29251

04

4.680

10216

48

Beta 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1

Cost of Equity 0.1305

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

Present Value

0.4640

824939

0.479

23083

36

0.491

75685

74

0.501

61504

85

0.508

79002

67

0.513

29602

88

0.515

17591

15

0.514

49970

89

Stable Growth Phase

Growth Rate in Stable Phase = 0.08

Payout Ratio in Stable Phase = 0.6

Cost of Equity in Stable Phase = 0.1305

Price at the end of growth phase =

100.0893136

244

Present Value of dividends in high growth phase =

4.953896409

1

Present Value of dividends in transition phase = 3.988446909

6

Year 11 12 13 14 15 16 17 18

Growth Rate

0.1020

101236

0.098

86582

03

0.095

72151

69

0.092

57721

35

0.089

43291

01

0.086

28860

68

0.083

14430

34 0.08

Payout Ratio

0.4176

573427

0.443

70629

37

0.469

75524

48

0.495

80419

58

0.521

85314

69

0.547

90209

79

0.573

95104

9 0.6

Earnings

4.2830

317998

4.706

47725

19

5.156

98839

37

5.634

40800

93

6.138

30951

45

6.667

97569

03

7.222

37988

4

7.800

17027

47

Dividends 1.79

2.088

29357

79

2.422

52234

51

2.793

56313

19

3.203

29613

65

3.653

39786

95

4.145

29251

04

4.680

10216

48

Beta 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1

Cost of Equity 0.1305

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

0.130

5

Present Value

0.4640

824939

0.479

23083

36

0.491

75685

74

0.501

61504

85

0.508

79002

67

0.513

29602

88

0.515

17591

15

0.514

49970

89

Stable Growth Phase

Growth Rate in Stable Phase = 0.08

Payout Ratio in Stable Phase = 0.6

Cost of Equity in Stable Phase = 0.1305

Price at the end of growth phase =

100.0893136

244

Present Value of dividends in high growth phase =

4.953896409

1

Present Value of dividends in transition phase = 3.988446909

6

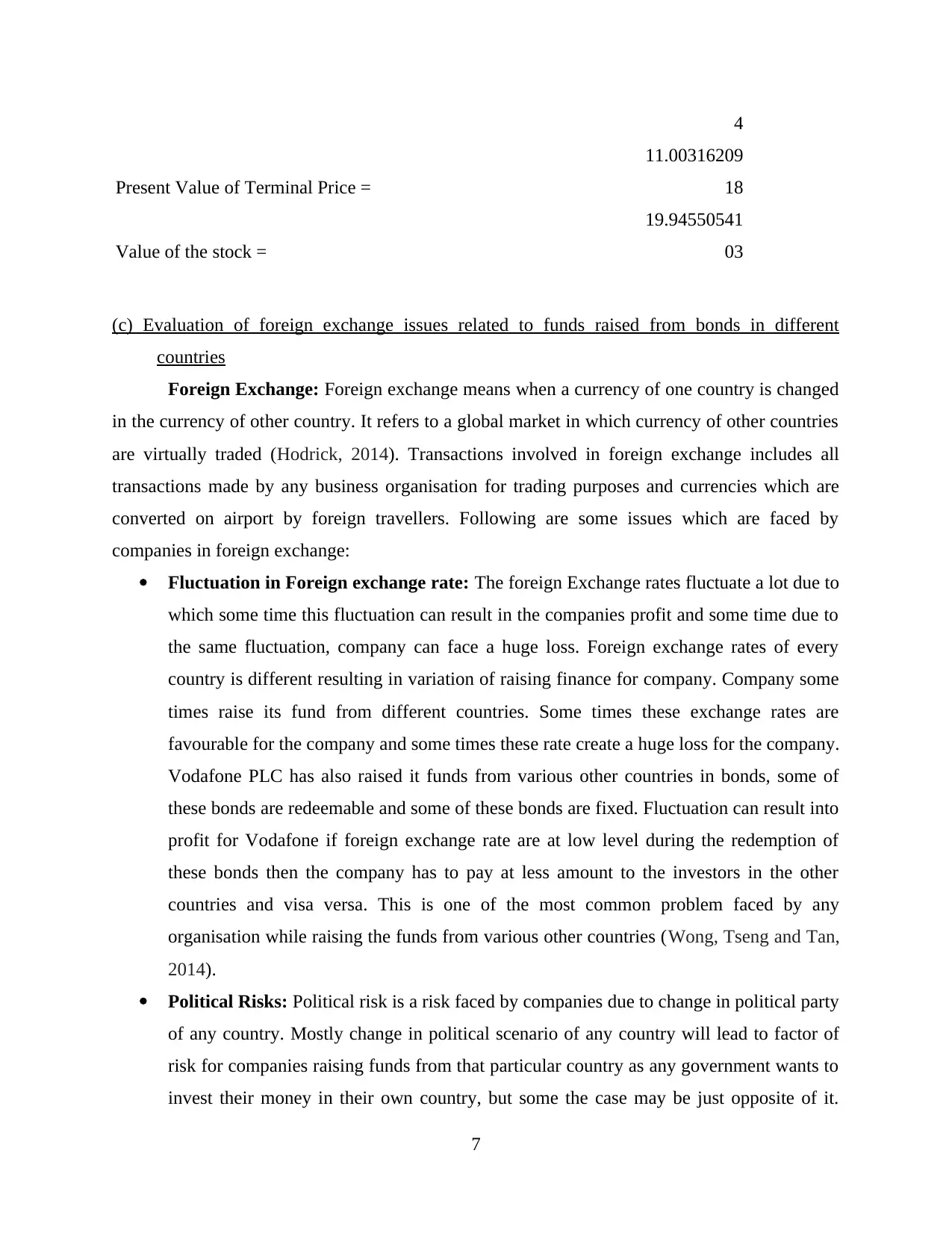

4

Present Value of Terminal Price =

11.00316209

18

Value of the stock =

19.94550541

03

(c) Evaluation of foreign exchange issues related to funds raised from bonds in different

countries

Foreign Exchange: Foreign exchange means when a currency of one country is changed

in the currency of other country. It refers to a global market in which currency of other countries

are virtually traded (Hodrick, 2014). Transactions involved in foreign exchange includes all

transactions made by any business organisation for trading purposes and currencies which are

converted on airport by foreign travellers. Following are some issues which are faced by

companies in foreign exchange:

Fluctuation in Foreign exchange rate: The foreign Exchange rates fluctuate a lot due to

which some time this fluctuation can result in the companies profit and some time due to

the same fluctuation, company can face a huge loss. Foreign exchange rates of every

country is different resulting in variation of raising finance for company. Company some

times raise its fund from different countries. Some times these exchange rates are

favourable for the company and some times these rate create a huge loss for the company.

Vodafone PLC has also raised it funds from various other countries in bonds, some of

these bonds are redeemable and some of these bonds are fixed. Fluctuation can result into

profit for Vodafone if foreign exchange rate are at low level during the redemption of

these bonds then the company has to pay at less amount to the investors in the other

countries and visa versa. This is one of the most common problem faced by any

organisation while raising the funds from various other countries (Wong, Tseng and Tan,

2014).

Political Risks: Political risk is a risk faced by companies due to change in political party

of any country. Mostly change in political scenario of any country will lead to factor of

risk for companies raising funds from that particular country as any government wants to

invest their money in their own country, but some the case may be just opposite of it.

7

Present Value of Terminal Price =

11.00316209

18

Value of the stock =

19.94550541

03

(c) Evaluation of foreign exchange issues related to funds raised from bonds in different

countries

Foreign Exchange: Foreign exchange means when a currency of one country is changed

in the currency of other country. It refers to a global market in which currency of other countries

are virtually traded (Hodrick, 2014). Transactions involved in foreign exchange includes all

transactions made by any business organisation for trading purposes and currencies which are

converted on airport by foreign travellers. Following are some issues which are faced by

companies in foreign exchange:

Fluctuation in Foreign exchange rate: The foreign Exchange rates fluctuate a lot due to

which some time this fluctuation can result in the companies profit and some time due to

the same fluctuation, company can face a huge loss. Foreign exchange rates of every

country is different resulting in variation of raising finance for company. Company some

times raise its fund from different countries. Some times these exchange rates are

favourable for the company and some times these rate create a huge loss for the company.

Vodafone PLC has also raised it funds from various other countries in bonds, some of

these bonds are redeemable and some of these bonds are fixed. Fluctuation can result into

profit for Vodafone if foreign exchange rate are at low level during the redemption of

these bonds then the company has to pay at less amount to the investors in the other

countries and visa versa. This is one of the most common problem faced by any

organisation while raising the funds from various other countries (Wong, Tseng and Tan,

2014).

Political Risks: Political risk is a risk faced by companies due to change in political party

of any country. Mostly change in political scenario of any country will lead to factor of

risk for companies raising funds from that particular country as any government wants to

invest their money in their own country, but some the case may be just opposite of it.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Political changes create a risk for company that whether the political party in power will

support it or create some strict rules. As for the case of Vodafone PLC changes in the

political party of some countries has lead to risk for investors in other countries creating a

problem for company (Ülkü and Demirci, 2012).

Credit Risk: Credit risk is a risk which is involved in the companies while trading

internationally with other countries. This is a type of risk faced by companies when other

party in some other country fails to execute its parts of obligation to complete that

contract. This risk involves fluctuation of exchange rates due to which party facing loss

does not plays his part in obligation of contract. Investor who have invested in company

and some amount of bond or equity is left to be called upon and foreign exchange rate

increases then those investors does not pay remaining amount.

Interest Rate Risk: Interest rate risk is a risk where interest rate for an investment

changes due to change in rate of foreign exchange. This type of risk is usually involved in

those countries whose currency is not so strong as compared to other countries. Countries

where the foreign exchange rate change frequently every time, some time changes in

exchange rate can benefit the company. Due to the change in the rate of exchange of

foreign currency the interest payable to investors increase when converted in to the

currencies of those countries whose currencies is weak as compared to other countries. In

a case of Vodafone PLC it has raised it capital in form of debts at 5.9% of interest of total

of 450 million. Company has various other debts including the above debts (Kim, 2013).

CONCLUSION

From the above report it can be concluded that financial accounting is an important part

for every organisation. As talked above in the report benefits of financial accounting it helps the

organisation to control its cost. The above report also states methods of calculation of value of

the firm. In this report the value of Vodafone PLC is established and all the issues related to

raising funds from other countries are highlighted.

8

support it or create some strict rules. As for the case of Vodafone PLC changes in the

political party of some countries has lead to risk for investors in other countries creating a

problem for company (Ülkü and Demirci, 2012).

Credit Risk: Credit risk is a risk which is involved in the companies while trading

internationally with other countries. This is a type of risk faced by companies when other

party in some other country fails to execute its parts of obligation to complete that

contract. This risk involves fluctuation of exchange rates due to which party facing loss

does not plays his part in obligation of contract. Investor who have invested in company

and some amount of bond or equity is left to be called upon and foreign exchange rate

increases then those investors does not pay remaining amount.

Interest Rate Risk: Interest rate risk is a risk where interest rate for an investment

changes due to change in rate of foreign exchange. This type of risk is usually involved in

those countries whose currency is not so strong as compared to other countries. Countries

where the foreign exchange rate change frequently every time, some time changes in

exchange rate can benefit the company. Due to the change in the rate of exchange of

foreign currency the interest payable to investors increase when converted in to the

currencies of those countries whose currencies is weak as compared to other countries. In

a case of Vodafone PLC it has raised it capital in form of debts at 5.9% of interest of total

of 450 million. Company has various other debts including the above debts (Kim, 2013).

CONCLUSION

From the above report it can be concluded that financial accounting is an important part

for every organisation. As talked above in the report benefits of financial accounting it helps the

organisation to control its cost. The above report also states methods of calculation of value of

the firm. In this report the value of Vodafone PLC is established and all the issues related to

raising funds from other countries are highlighted.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Banerjee, B., 2012. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Parker, L. D., 2012. From privatised to hybrid corporatised higher education: A global financial

management discourse. Financial Accountability & Management. 28(3) pp.247-268.

Garengo, P. and Biazzo, S., 2013. From ISO quality standards to an integrated management

system: An implementation process in SME. Total Quality Management & Business

Excellence. 24(3-4). pp.310-335.

Jacque, L. L., 2014. Management of foreign exchange risk. International Accounting and

Transnational Decisions. p.361.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign

exchange markets. Routledge.

Ülkü, N. and Demirci, E., 2012. Joint dynamics of foreign exchange and stock markets in

emerging Europe. Journal of International Financial Markets, Institutions and

Money. 22(1). pp.55-86.

Kim, S. K., 2013. General framework for management of technology evolution. The Journal of

High Technology Management Research. 24(2). pp.130-137.

Wong, W. P., Tseng, M. L. and Tan, K. H., 2014. A business process management capabilities

perspective on organisation performance. Total Quality Management & Business

Excellence. 25(5-6). pp.602-617.

Sparrow, P., Farndale, E. and Scullion, H., 2013. An empirical study of the role of the corporate

HR function in global talent management in professional and financial service firms in

the global financial crisis. The International Journal of Human Resource

Management, 24(9), pp.1777-1798.

Online

Vodafone. 2019. [Online]. Available through:

<https://www.vodafone.co.uk/>

9

Books and journals

Banerjee, B., 2012. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Parker, L. D., 2012. From privatised to hybrid corporatised higher education: A global financial

management discourse. Financial Accountability & Management. 28(3) pp.247-268.

Garengo, P. and Biazzo, S., 2013. From ISO quality standards to an integrated management

system: An implementation process in SME. Total Quality Management & Business

Excellence. 24(3-4). pp.310-335.

Jacque, L. L., 2014. Management of foreign exchange risk. International Accounting and

Transnational Decisions. p.361.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign

exchange markets. Routledge.

Ülkü, N. and Demirci, E., 2012. Joint dynamics of foreign exchange and stock markets in

emerging Europe. Journal of International Financial Markets, Institutions and

Money. 22(1). pp.55-86.

Kim, S. K., 2013. General framework for management of technology evolution. The Journal of

High Technology Management Research. 24(2). pp.130-137.

Wong, W. P., Tseng, M. L. and Tan, K. H., 2014. A business process management capabilities

perspective on organisation performance. Total Quality Management & Business

Excellence. 25(5-6). pp.602-617.

Sparrow, P., Farndale, E. and Scullion, H., 2013. An empirical study of the role of the corporate

HR function in global talent management in professional and financial service firms in

the global financial crisis. The International Journal of Human Resource

Management, 24(9), pp.1777-1798.

Online

Vodafone. 2019. [Online]. Available through:

<https://www.vodafone.co.uk/>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.