Business Valuation of Vodafone Group Plc: Financial Management Report

VerifiedAdded on 2023/04/07

|16

|2968

|252

Report

AI Summary

This report presents a comprehensive business valuation of Vodafone Group Plc, evaluating its financial performance and market position. It begins with an introduction to business valuation, emphasizing its significance in investment decisions. The report delves into the methods of estimating the cost of capital, including the cost of debt, equity, and preference shares, with illustrative examples. It then applies these concepts to Vodafone, determining the cost of equity providers. The core of the report focuses on business valuation methods such as discounted cash flow (DCF), internal rate of return (IRR), and asset-based valuation, providing detailed calculations and analysis for Vodafone. The report also addresses foreign exchange issues related to the finance raised from bonds in different currencies. The analysis provides a practical application of financial management principles to assess Vodafone's value and investment potential, including its present value, internal rate of return, and net asset value, making it a valuable resource for students studying financial analysis and business valuation. The conclusion summarizes the findings and the report includes a detailed reference list.

Business Valuation

Vodafone Group Plc

User

Vodafone Group Plc

User

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Table of Contents

Introduction......................................................................................................................................2

Methods of Estimating Cost of Capital...........................................................................................2

Cost of Debt Capital....................................................................................................................3

Cost of Equity Share Capital.......................................................................................................4

Cost of Preference Share Capital.................................................................................................5

The Cost of Vodafone Equity Providers..................................................................................6

Business Valuation Methods...........................................................................................................7

Discounted Cash Flow Method...............................................................................................7

Internal Rate of Return............................................................................................................9

Asset Based Business Valuation Method................................................................................9

Foreign Exchange Issues Related to the Finance Raised From Bonds in Different Currencies....11

Conclusion.....................................................................................................................................11

Reference List................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................2

Methods of Estimating Cost of Capital...........................................................................................2

Cost of Debt Capital....................................................................................................................3

Cost of Equity Share Capital.......................................................................................................4

Cost of Preference Share Capital.................................................................................................5

The Cost of Vodafone Equity Providers..................................................................................6

Business Valuation Methods...........................................................................................................7

Discounted Cash Flow Method...............................................................................................7

Internal Rate of Return............................................................................................................9

Asset Based Business Valuation Method................................................................................9

Foreign Exchange Issues Related to the Finance Raised From Bonds in Different Currencies....11

Conclusion.....................................................................................................................................11

Reference List................................................................................................................................13

2

Introduction

Valuation of business has been considered as the most significant decisions which are influenced

by a number of factors such as the market forces, competitive forces, and the nature of the

business enterprise as well as the economic factors (Fernández, 2007). Therefore, it becomes

essential for the business and the potential investors to compute the value of the business at the

present date so as to base their decision with regard to making future investment (Fernández et

al, 2002). There are a number of methodologies that have been adopted by organization and the

academics in the researcher with regard to the company valuation that is commonly used.

This report provides as complete analyses of the method of cot of capital such as the cost of

equity, cost of debt capital, and cost of preference shares with examples along with the cost of

equity of a telecommunication company Vodafone Group plc. The company operates in the

global market with its origin in London. The company is listed on the London Stock Exchange

and thus, the data and information with regard to the market rates and value have been taken

from London Stock Exchange and the annual report of the company.

Methods of Estimating Cost of Capital

Cost of capital, one of the most crucial topics in financial management has gained momentum in

the world market due to its adoption by various multinational organizations for the purpose of

business valuation (Gebhardt et al, 2001). The cost of capital, when defined from organizational

point of view, it is the rate at which capital is raised from the market for the purpose of further

investment in any proposed project (Botosan and Plumlee, 2002). In addition to this, when

defined from investor’s point of view, it is the rate of return from the capital that is invested in

Introduction

Valuation of business has been considered as the most significant decisions which are influenced

by a number of factors such as the market forces, competitive forces, and the nature of the

business enterprise as well as the economic factors (Fernández, 2007). Therefore, it becomes

essential for the business and the potential investors to compute the value of the business at the

present date so as to base their decision with regard to making future investment (Fernández et

al, 2002). There are a number of methodologies that have been adopted by organization and the

academics in the researcher with regard to the company valuation that is commonly used.

This report provides as complete analyses of the method of cot of capital such as the cost of

equity, cost of debt capital, and cost of preference shares with examples along with the cost of

equity of a telecommunication company Vodafone Group plc. The company operates in the

global market with its origin in London. The company is listed on the London Stock Exchange

and thus, the data and information with regard to the market rates and value have been taken

from London Stock Exchange and the annual report of the company.

Methods of Estimating Cost of Capital

Cost of capital, one of the most crucial topics in financial management has gained momentum in

the world market due to its adoption by various multinational organizations for the purpose of

business valuation (Gebhardt et al, 2001). The cost of capital, when defined from organizational

point of view, it is the rate at which capital is raised from the market for the purpose of further

investment in any proposed project (Botosan and Plumlee, 2002). In addition to this, when

defined from investor’s point of view, it is the rate of return from the capital that is invested in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

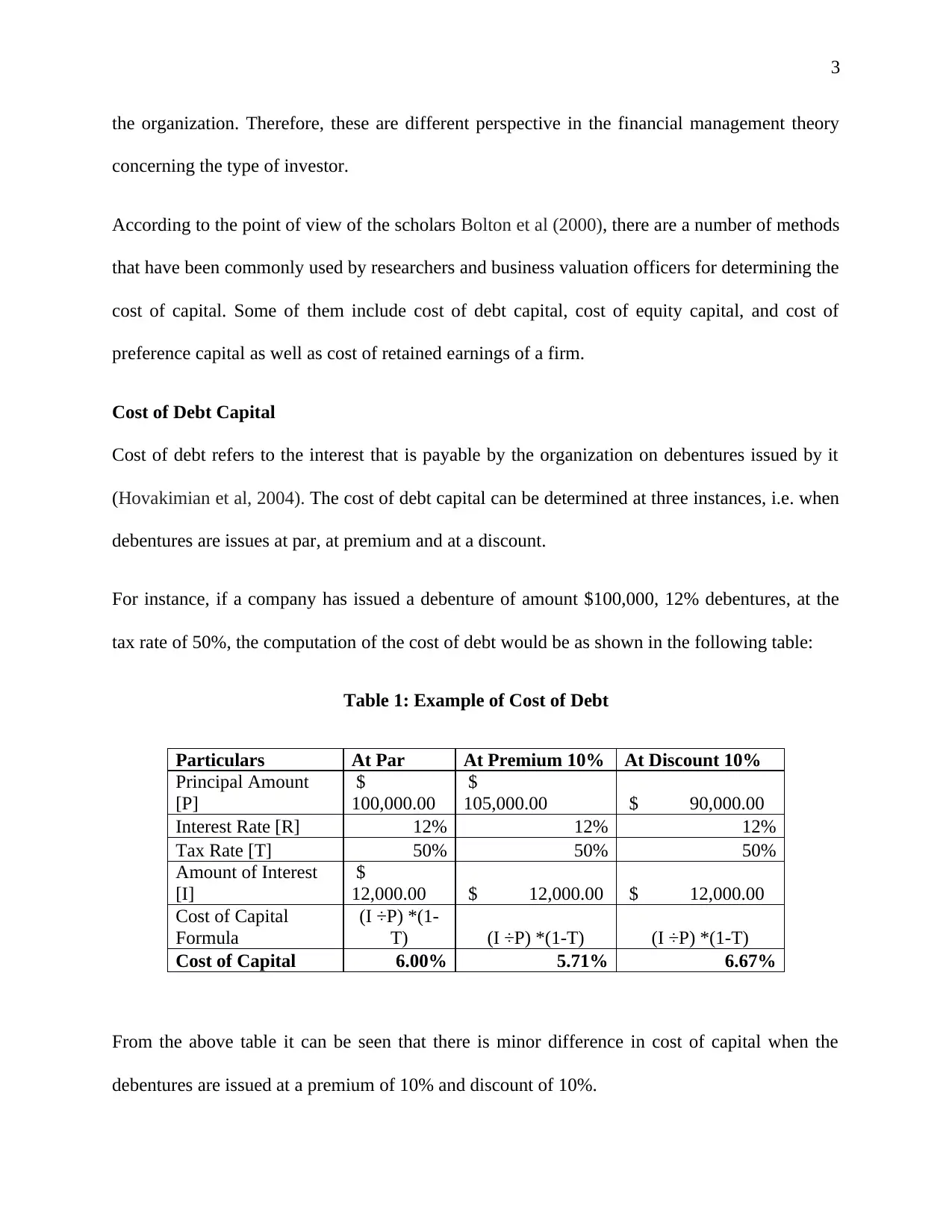

the organization. Therefore, these are different perspective in the financial management theory

concerning the type of investor.

According to the point of view of the scholars Bolton et al (2000), there are a number of methods

that have been commonly used by researchers and business valuation officers for determining the

cost of capital. Some of them include cost of debt capital, cost of equity capital, and cost of

preference capital as well as cost of retained earnings of a firm.

Cost of Debt Capital

Cost of debt refers to the interest that is payable by the organization on debentures issued by it

(Hovakimian et al, 2004). The cost of debt capital can be determined at three instances, i.e. when

debentures are issues at par, at premium and at a discount.

For instance, if a company has issued a debenture of amount $100,000, 12% debentures, at the

tax rate of 50%, the computation of the cost of debt would be as shown in the following table:

Table 1: Example of Cost of Debt

Particulars At Par At Premium 10% At Discount 10%

Principal Amount

[P]

$

100,000.00

$

105,000.00 $ 90,000.00

Interest Rate [R] 12% 12% 12%

Tax Rate [T] 50% 50% 50%

Amount of Interest

[I]

$

12,000.00 $ 12,000.00 $ 12,000.00

Cost of Capital

Formula

(I ÷P) *(1-

T) (I ÷P) *(1-T) (I ÷P) *(1-T)

Cost of Capital 6.00% 5.71% 6.67%

From the above table it can be seen that there is minor difference in cost of capital when the

debentures are issued at a premium of 10% and discount of 10%.

the organization. Therefore, these are different perspective in the financial management theory

concerning the type of investor.

According to the point of view of the scholars Bolton et al (2000), there are a number of methods

that have been commonly used by researchers and business valuation officers for determining the

cost of capital. Some of them include cost of debt capital, cost of equity capital, and cost of

preference capital as well as cost of retained earnings of a firm.

Cost of Debt Capital

Cost of debt refers to the interest that is payable by the organization on debentures issued by it

(Hovakimian et al, 2004). The cost of debt capital can be determined at three instances, i.e. when

debentures are issues at par, at premium and at a discount.

For instance, if a company has issued a debenture of amount $100,000, 12% debentures, at the

tax rate of 50%, the computation of the cost of debt would be as shown in the following table:

Table 1: Example of Cost of Debt

Particulars At Par At Premium 10% At Discount 10%

Principal Amount

[P]

$

100,000.00

$

105,000.00 $ 90,000.00

Interest Rate [R] 12% 12% 12%

Tax Rate [T] 50% 50% 50%

Amount of Interest

[I]

$

12,000.00 $ 12,000.00 $ 12,000.00

Cost of Capital

Formula

(I ÷P) *(1-

T) (I ÷P) *(1-T) (I ÷P) *(1-T)

Cost of Capital 6.00% 5.71% 6.67%

From the above table it can be seen that there is minor difference in cost of capital when the

debentures are issued at a premium of 10% and discount of 10%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Cost of Equity Share Capital

Equity shares are issued by companies to raise capital from the market (Hovakimian et al, 2004).

The investors invest money in an organization by purchasing the equity shares issued by the firm

(Margaritis and Psillaki, 2010). The cost of equity shares can be computed under various

methods for instance, the dividend price approach, earnings price approach, capital asset pricing

model and many others. The below table reflects the cost of equity capital under different

models.

Table 2: Cost of Equity under Different Models

Cost of Equity Capital (Dividend Price

Approach) Cost of Equity Capital (CAPM Method)

Dividend per

share $10

Expected rate of return

on asset (Rm) 15%

Market price per

share $400 Beta coefficient (B) 0.7

Cost of Equity

Formula

(Dividend per

share/Market price

per share) * 100

Risk free rate of return

(Rf) 10%

Cost of Equity 2.50% CAPM Formula Rf+[B*(Rm-Rf)]

Cost of Capital 13.50%

Cost of Equity Capital (Price Earnings

Approach)

Earnings per share $40

Market price per

share $600

Cost of Equity

Formula

(Earnings per

share/Market price

per share) * 100

Cost of Equity 6.67%

Cost of Equity Share Capital

Equity shares are issued by companies to raise capital from the market (Hovakimian et al, 2004).

The investors invest money in an organization by purchasing the equity shares issued by the firm

(Margaritis and Psillaki, 2010). The cost of equity shares can be computed under various

methods for instance, the dividend price approach, earnings price approach, capital asset pricing

model and many others. The below table reflects the cost of equity capital under different

models.

Table 2: Cost of Equity under Different Models

Cost of Equity Capital (Dividend Price

Approach) Cost of Equity Capital (CAPM Method)

Dividend per

share $10

Expected rate of return

on asset (Rm) 15%

Market price per

share $400 Beta coefficient (B) 0.7

Cost of Equity

Formula

(Dividend per

share/Market price

per share) * 100

Risk free rate of return

(Rf) 10%

Cost of Equity 2.50% CAPM Formula Rf+[B*(Rm-Rf)]

Cost of Capital 13.50%

Cost of Equity Capital (Price Earnings

Approach)

Earnings per share $40

Market price per

share $600

Cost of Equity

Formula

(Earnings per

share/Market price

per share) * 100

Cost of Equity 6.67%

5

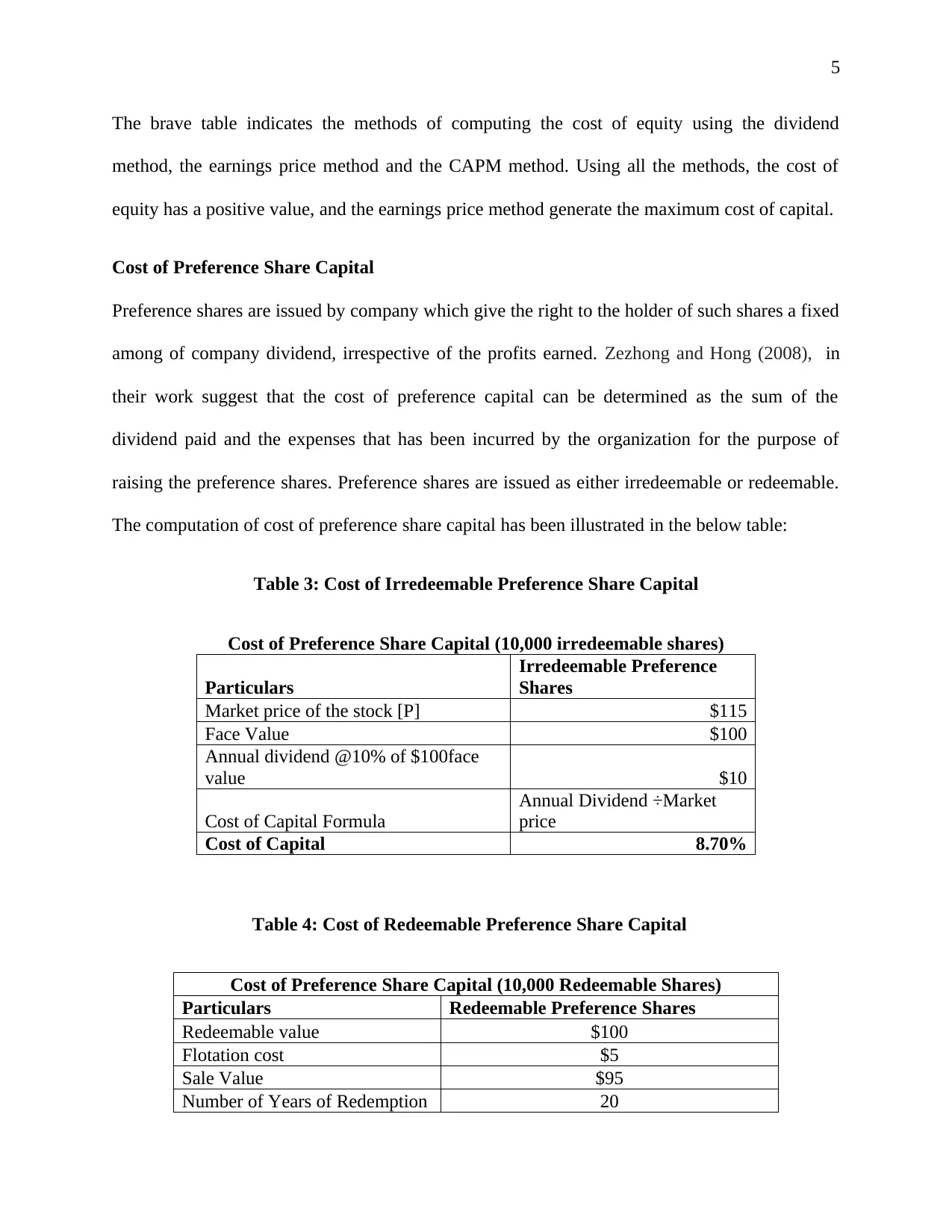

The brave table indicates the methods of computing the cost of equity using the dividend

method, the earnings price method and the CAPM method. Using all the methods, the cost of

equity has a positive value, and the earnings price method generate the maximum cost of capital.

Cost of Preference Share Capital

Preference shares are issued by company which give the right to the holder of such shares a fixed

among of company dividend, irrespective of the profits earned. Zezhong and Hong (2008), in

their work suggest that the cost of preference capital can be determined as the sum of the

dividend paid and the expenses that has been incurred by the organization for the purpose of

raising the preference shares. Preference shares are issued as either irredeemable or redeemable.

The computation of cost of preference share capital has been illustrated in the below table:

Table 3: Cost of Irredeemable Preference Share Capital

Cost of Preference Share Capital (10,000 irredeemable shares)

Particulars

Irredeemable Preference

Shares

Market price of the stock [P] $115

Face Value $100

Annual dividend @10% of $100face

value $10

Cost of Capital Formula

Annual Dividend ÷Market

price

Cost of Capital 8.70%

Table 4: Cost of Redeemable Preference Share Capital

Cost of Preference Share Capital (10,000 Redeemable Shares)

Particulars Redeemable Preference Shares

Redeemable value $100

Flotation cost $5

Sale Value $95

Number of Years of Redemption 20

The brave table indicates the methods of computing the cost of equity using the dividend

method, the earnings price method and the CAPM method. Using all the methods, the cost of

equity has a positive value, and the earnings price method generate the maximum cost of capital.

Cost of Preference Share Capital

Preference shares are issued by company which give the right to the holder of such shares a fixed

among of company dividend, irrespective of the profits earned. Zezhong and Hong (2008), in

their work suggest that the cost of preference capital can be determined as the sum of the

dividend paid and the expenses that has been incurred by the organization for the purpose of

raising the preference shares. Preference shares are issued as either irredeemable or redeemable.

The computation of cost of preference share capital has been illustrated in the below table:

Table 3: Cost of Irredeemable Preference Share Capital

Cost of Preference Share Capital (10,000 irredeemable shares)

Particulars

Irredeemable Preference

Shares

Market price of the stock [P] $115

Face Value $100

Annual dividend @10% of $100face

value $10

Cost of Capital Formula

Annual Dividend ÷Market

price

Cost of Capital 8.70%

Table 4: Cost of Redeemable Preference Share Capital

Cost of Preference Share Capital (10,000 Redeemable Shares)

Particulars Redeemable Preference Shares

Redeemable value $100

Flotation cost $5

Sale Value $95

Number of Years of Redemption 20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

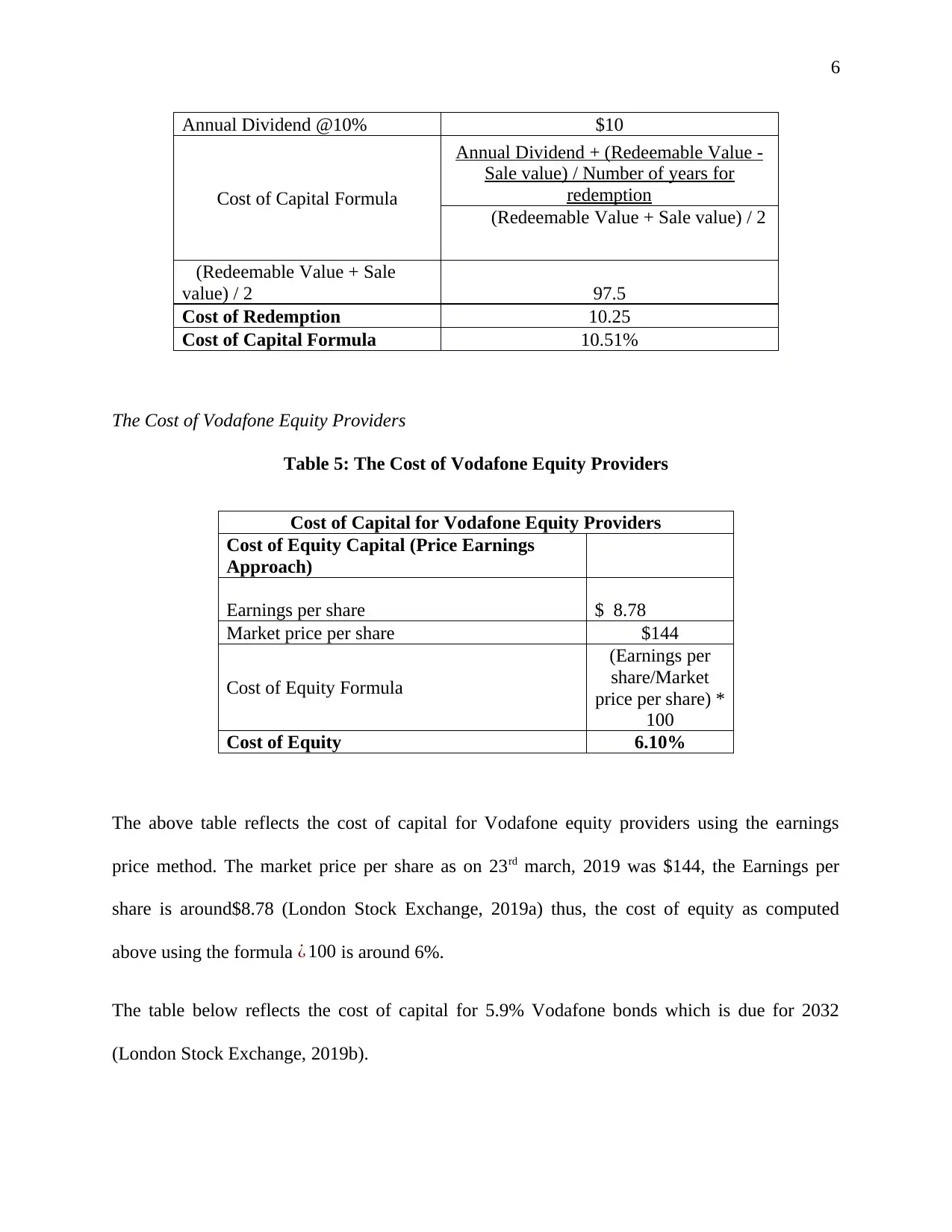

Annual Dividend @10% $10

Cost of Capital Formula

Annual Dividend + (Redeemable Value -

Sale value) / Number of years for

redemption

(Redeemable Value + Sale value) / 2

(Redeemable Value + Sale

value) / 2 97.5

Cost of Redemption 10.25

Cost of Capital Formula 10.51%

The Cost of Vodafone Equity Providers

Table 5: The Cost of Vodafone Equity Providers

Cost of Capital for Vodafone Equity Providers

Cost of Equity Capital (Price Earnings

Approach)

Earnings per share $ 8.78

Market price per share $144

Cost of Equity Formula

(Earnings per

share/Market

price per share) *

100

Cost of Equity 6.10%

The above table reflects the cost of capital for Vodafone equity providers using the earnings

price method. The market price per share as on 23rd march, 2019 was $144, the Earnings per

share is around$8.78 (London Stock Exchange, 2019a) thus, the cost of equity as computed

above using the formula ¿ 100 is around 6%.

The table below reflects the cost of capital for 5.9% Vodafone bonds which is due for 2032

(London Stock Exchange, 2019b).

Annual Dividend @10% $10

Cost of Capital Formula

Annual Dividend + (Redeemable Value -

Sale value) / Number of years for

redemption

(Redeemable Value + Sale value) / 2

(Redeemable Value + Sale

value) / 2 97.5

Cost of Redemption 10.25

Cost of Capital Formula 10.51%

The Cost of Vodafone Equity Providers

Table 5: The Cost of Vodafone Equity Providers

Cost of Capital for Vodafone Equity Providers

Cost of Equity Capital (Price Earnings

Approach)

Earnings per share $ 8.78

Market price per share $144

Cost of Equity Formula

(Earnings per

share/Market

price per share) *

100

Cost of Equity 6.10%

The above table reflects the cost of capital for Vodafone equity providers using the earnings

price method. The market price per share as on 23rd march, 2019 was $144, the Earnings per

share is around$8.78 (London Stock Exchange, 2019a) thus, the cost of equity as computed

above using the formula ¿ 100 is around 6%.

The table below reflects the cost of capital for 5.9% Vodafone bonds which is due for 2032

(London Stock Exchange, 2019b).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

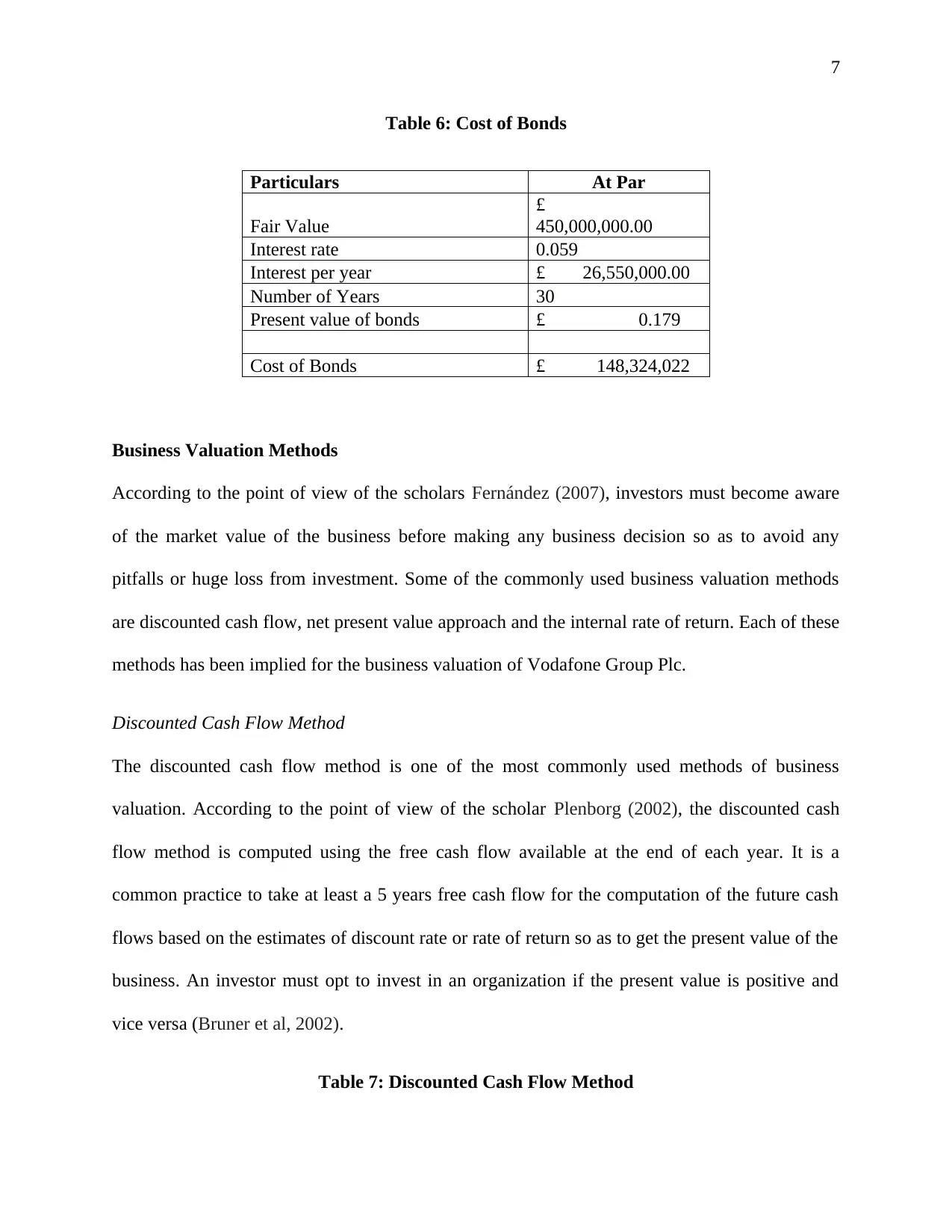

Table 6: Cost of Bonds

Particulars At Par

Fair Value

£

450,000,000.00

Interest rate 0.059

Interest per year £ 26,550,000.00

Number of Years 30

Present value of bonds £ 0.179

Cost of Bonds £ 148,324,022

Business Valuation Methods

According to the point of view of the scholars Fernández (2007), investors must become aware

of the market value of the business before making any business decision so as to avoid any

pitfalls or huge loss from investment. Some of the commonly used business valuation methods

are discounted cash flow, net present value approach and the internal rate of return. Each of these

methods has been implied for the business valuation of Vodafone Group Plc.

Discounted Cash Flow Method

The discounted cash flow method is one of the most commonly used methods of business

valuation. According to the point of view of the scholar Plenborg (2002), the discounted cash

flow method is computed using the free cash flow available at the end of each year. It is a

common practice to take at least a 5 years free cash flow for the computation of the future cash

flows based on the estimates of discount rate or rate of return so as to get the present value of the

business. An investor must opt to invest in an organization if the present value is positive and

vice versa (Bruner et al, 2002).

Table 7: Discounted Cash Flow Method

Table 6: Cost of Bonds

Particulars At Par

Fair Value

£

450,000,000.00

Interest rate 0.059

Interest per year £ 26,550,000.00

Number of Years 30

Present value of bonds £ 0.179

Cost of Bonds £ 148,324,022

Business Valuation Methods

According to the point of view of the scholars Fernández (2007), investors must become aware

of the market value of the business before making any business decision so as to avoid any

pitfalls or huge loss from investment. Some of the commonly used business valuation methods

are discounted cash flow, net present value approach and the internal rate of return. Each of these

methods has been implied for the business valuation of Vodafone Group Plc.

Discounted Cash Flow Method

The discounted cash flow method is one of the most commonly used methods of business

valuation. According to the point of view of the scholar Plenborg (2002), the discounted cash

flow method is computed using the free cash flow available at the end of each year. It is a

common practice to take at least a 5 years free cash flow for the computation of the future cash

flows based on the estimates of discount rate or rate of return so as to get the present value of the

business. An investor must opt to invest in an organization if the present value is positive and

vice versa (Bruner et al, 2002).

Table 7: Discounted Cash Flow Method

8

Discounted Cash Flow Method

Particulars 2014 2015 2016 2017 2018

Operating cash

flow £ 7,536.00

£

13,284.00

£

13,290.00

£

14,223.00

£

13,600.00

Capital

Expenditure -£ 8,137.00 -£

12,147.00

-£

15,031.00

-£

8,861.00

-£

8,163.00

Free Cash Flow -£ 601.00

£

1,137.00

-£

1,741.00

£

5,362.00

£

5,437.00

Rate of discount assumed 10%

Year NPER

Free Cash

Flow

Future

Value

1 4 -£ 601.00

£

879.92

2 3 £ 1,137.00

-£

1,513.35

3 2 -£ 1,741.00

£

2,106.61

4 1 £ 5,362.00

-£

5,898.20

5 0 £ 5,437.00

-£

5,437.00

Total Present

Value £ 9,594.00

(Source: Vodafone Group Plc, 2018)

From the above table it can be seen that the present value of the company is around £9594

million which is a positive figure and this indicates that it is one of the best option for

investment.

Internal Rate of Return

Internal rate of return is another option which is commonly used for business valuation purpose.

According to the point of view of the scholars Talavera et al (2010), the internal rate of return is

used for the purpose of anticipating the rate of return on the investments made. The proposed

Discounted Cash Flow Method

Particulars 2014 2015 2016 2017 2018

Operating cash

flow £ 7,536.00

£

13,284.00

£

13,290.00

£

14,223.00

£

13,600.00

Capital

Expenditure -£ 8,137.00 -£

12,147.00

-£

15,031.00

-£

8,861.00

-£

8,163.00

Free Cash Flow -£ 601.00

£

1,137.00

-£

1,741.00

£

5,362.00

£

5,437.00

Rate of discount assumed 10%

Year NPER

Free Cash

Flow

Future

Value

1 4 -£ 601.00

£

879.92

2 3 £ 1,137.00

-£

1,513.35

3 2 -£ 1,741.00

£

2,106.61

4 1 £ 5,362.00

-£

5,898.20

5 0 £ 5,437.00

-£

5,437.00

Total Present

Value £ 9,594.00

(Source: Vodafone Group Plc, 2018)

From the above table it can be seen that the present value of the company is around £9594

million which is a positive figure and this indicates that it is one of the best option for

investment.

Internal Rate of Return

Internal rate of return is another option which is commonly used for business valuation purpose.

According to the point of view of the scholars Talavera et al (2010), the internal rate of return is

used for the purpose of anticipating the rate of return on the investments made. The proposed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

investment decisions are made on the positive outcome, i.e. the positive internal rate of return

and those projects must be rejected that have a negative internal rate of return.

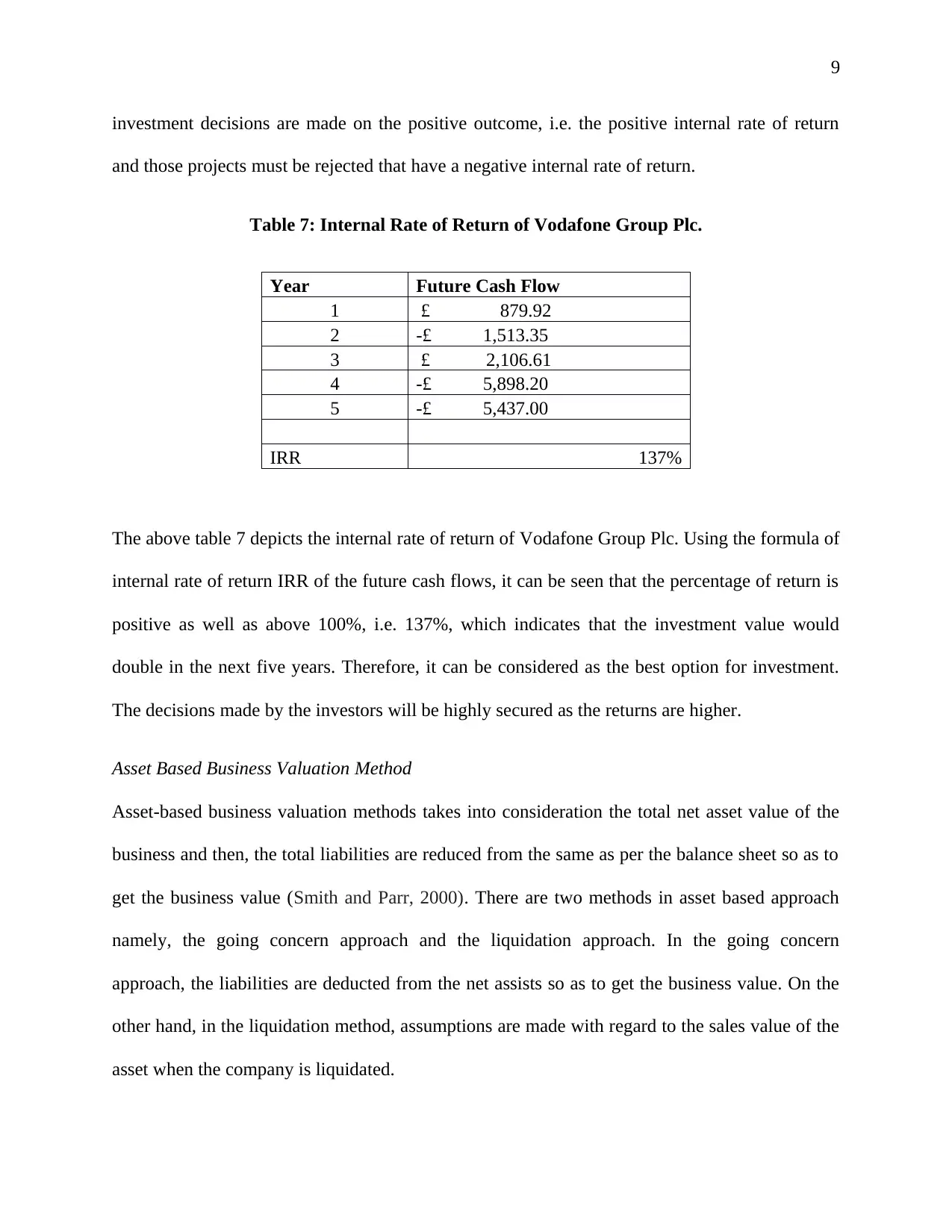

Table 7: Internal Rate of Return of Vodafone Group Plc.

Year Future Cash Flow

1 £ 879.92

2 -£ 1,513.35

3 £ 2,106.61

4 -£ 5,898.20

5 -£ 5,437.00

IRR 137%

The above table 7 depicts the internal rate of return of Vodafone Group Plc. Using the formula of

internal rate of return IRR of the future cash flows, it can be seen that the percentage of return is

positive as well as above 100%, i.e. 137%, which indicates that the investment value would

double in the next five years. Therefore, it can be considered as the best option for investment.

The decisions made by the investors will be highly secured as the returns are higher.

Asset Based Business Valuation Method

Asset-based business valuation methods takes into consideration the total net asset value of the

business and then, the total liabilities are reduced from the same as per the balance sheet so as to

get the business value (Smith and Parr, 2000). There are two methods in asset based approach

namely, the going concern approach and the liquidation approach. In the going concern

approach, the liabilities are deducted from the net assists so as to get the business value. On the

other hand, in the liquidation method, assumptions are made with regard to the sales value of the

asset when the company is liquidated.

investment decisions are made on the positive outcome, i.e. the positive internal rate of return

and those projects must be rejected that have a negative internal rate of return.

Table 7: Internal Rate of Return of Vodafone Group Plc.

Year Future Cash Flow

1 £ 879.92

2 -£ 1,513.35

3 £ 2,106.61

4 -£ 5,898.20

5 -£ 5,437.00

IRR 137%

The above table 7 depicts the internal rate of return of Vodafone Group Plc. Using the formula of

internal rate of return IRR of the future cash flows, it can be seen that the percentage of return is

positive as well as above 100%, i.e. 137%, which indicates that the investment value would

double in the next five years. Therefore, it can be considered as the best option for investment.

The decisions made by the investors will be highly secured as the returns are higher.

Asset Based Business Valuation Method

Asset-based business valuation methods takes into consideration the total net asset value of the

business and then, the total liabilities are reduced from the same as per the balance sheet so as to

get the business value (Smith and Parr, 2000). There are two methods in asset based approach

namely, the going concern approach and the liquidation approach. In the going concern

approach, the liabilities are deducted from the net assists so as to get the business value. On the

other hand, in the liquidation method, assumptions are made with regard to the sales value of the

asset when the company is liquidated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

In the present case, as the Vodafone Group Plc. is a going concern company, therefore the first

method would be applicable.

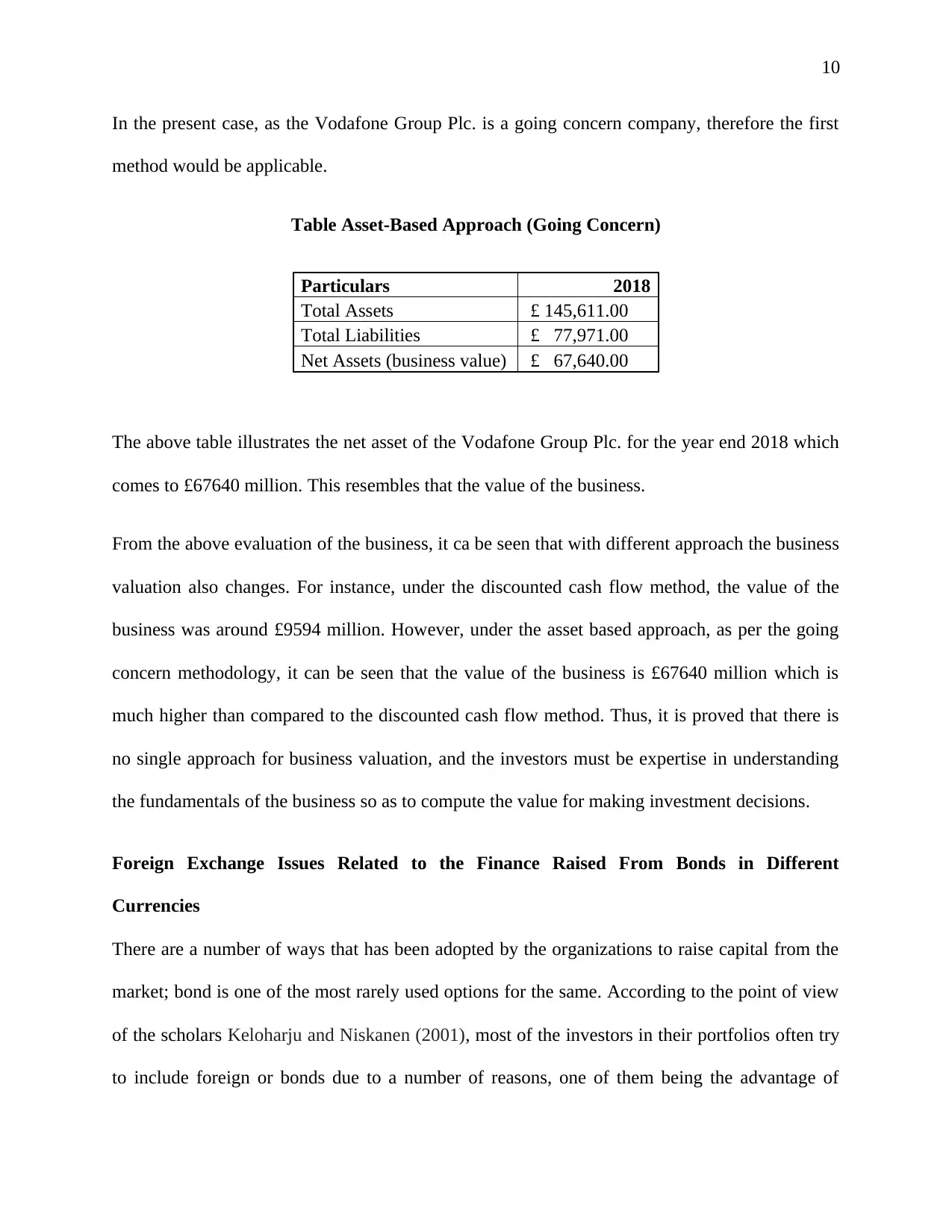

Table Asset-Based Approach (Going Concern)

Particulars 2018

Total Assets £ 145,611.00

Total Liabilities £ 77,971.00

Net Assets (business value) £ 67,640.00

The above table illustrates the net asset of the Vodafone Group Plc. for the year end 2018 which

comes to £67640 million. This resembles that the value of the business.

From the above evaluation of the business, it ca be seen that with different approach the business

valuation also changes. For instance, under the discounted cash flow method, the value of the

business was around £9594 million. However, under the asset based approach, as per the going

concern methodology, it can be seen that the value of the business is £67640 million which is

much higher than compared to the discounted cash flow method. Thus, it is proved that there is

no single approach for business valuation, and the investors must be expertise in understanding

the fundamentals of the business so as to compute the value for making investment decisions.

Foreign Exchange Issues Related to the Finance Raised From Bonds in Different

Currencies

There are a number of ways that has been adopted by the organizations to raise capital from the

market; bond is one of the most rarely used options for the same. According to the point of view

of the scholars Keloharju and Niskanen (2001), most of the investors in their portfolios often try

to include foreign or bonds due to a number of reasons, one of them being the advantage of

In the present case, as the Vodafone Group Plc. is a going concern company, therefore the first

method would be applicable.

Table Asset-Based Approach (Going Concern)

Particulars 2018

Total Assets £ 145,611.00

Total Liabilities £ 77,971.00

Net Assets (business value) £ 67,640.00

The above table illustrates the net asset of the Vodafone Group Plc. for the year end 2018 which

comes to £67640 million. This resembles that the value of the business.

From the above evaluation of the business, it ca be seen that with different approach the business

valuation also changes. For instance, under the discounted cash flow method, the value of the

business was around £9594 million. However, under the asset based approach, as per the going

concern methodology, it can be seen that the value of the business is £67640 million which is

much higher than compared to the discounted cash flow method. Thus, it is proved that there is

no single approach for business valuation, and the investors must be expertise in understanding

the fundamentals of the business so as to compute the value for making investment decisions.

Foreign Exchange Issues Related to the Finance Raised From Bonds in Different

Currencies

There are a number of ways that has been adopted by the organizations to raise capital from the

market; bond is one of the most rarely used options for the same. According to the point of view

of the scholars Keloharju and Niskanen (2001), most of the investors in their portfolios often try

to include foreign or bonds due to a number of reasons, one of them being the advantage of

11

higher interest rates as well as for the purpose of diversifications of their holdings. However,

Henderson et al (2006) in their work have emphasized that the higher rate of return that is often

anticipated by the investors by investing in foreign bonds is generally complemented by the

increased risk that arises from adverse foreign currency fluctuation. In addition to this,

Eichengreen and Mathieson (2000) have argued that owing to the comparatively minor level of

absolute return from bond in comparison to the equities, it can be said that the currency volatility

have a significant effect on the rate of return of bonds. Therefore, the potential investors must be

aware and conscious of the exchange risk from foreign bonds, as well as they should implement

strategies so as to lessen or diminish the currency risk.

Currency risk arises from the currency of bond denomination as well as the location of the

investors, and therefore, there is not concern with the domicile of issuers. When bonds are issued

in different currencies, the issues faces a number of difficulties when there is fluctuation in the

rate of exchange at which the bonds are issued. In addition to this, the fall in the price of the

market rate of bonds would indicate a loss to the business as the company has raised capital

through the bond at the market price.

Conclusion

Business valuation, as the name suggests, is the most essential technique that is used by company

and the potential investors for the purpose of acknowledging the correct market value of the

business and whether it is fit for investment purpose. The organizations use valuation method so

as to understand the strengths and weakness in the financials of the firm as well as the net worth

in the market. In addition to this, the potential investors must take up initiatives towards the

valuation methods and use the same for valuing the business.

higher interest rates as well as for the purpose of diversifications of their holdings. However,

Henderson et al (2006) in their work have emphasized that the higher rate of return that is often

anticipated by the investors by investing in foreign bonds is generally complemented by the

increased risk that arises from adverse foreign currency fluctuation. In addition to this,

Eichengreen and Mathieson (2000) have argued that owing to the comparatively minor level of

absolute return from bond in comparison to the equities, it can be said that the currency volatility

have a significant effect on the rate of return of bonds. Therefore, the potential investors must be

aware and conscious of the exchange risk from foreign bonds, as well as they should implement

strategies so as to lessen or diminish the currency risk.

Currency risk arises from the currency of bond denomination as well as the location of the

investors, and therefore, there is not concern with the domicile of issuers. When bonds are issued

in different currencies, the issues faces a number of difficulties when there is fluctuation in the

rate of exchange at which the bonds are issued. In addition to this, the fall in the price of the

market rate of bonds would indicate a loss to the business as the company has raised capital

through the bond at the market price.

Conclusion

Business valuation, as the name suggests, is the most essential technique that is used by company

and the potential investors for the purpose of acknowledging the correct market value of the

business and whether it is fit for investment purpose. The organizations use valuation method so

as to understand the strengths and weakness in the financials of the firm as well as the net worth

in the market. In addition to this, the potential investors must take up initiatives towards the

valuation methods and use the same for valuing the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.