Report on Managing Financial Resources and Decisions at XYZ Ltd

VerifiedAdded on 2020/06/06

|13

|3992

|50

Report

AI Summary

This report examines the management of financial resources and decision-making strategies within XYZ Ltd. It explores various sources of finance, including owner's capital, loans, and retained earnings, while also addressing the implications of legal and financial aspects. The report delves into financial planning, emphasizing its importance for business success, and provides a cash flow forecast for a business project. Cost analysis, including the cost-plus and unit cost methods, is conducted to determine margin and price structure. Furthermore, the report analyzes investment options, evaluating projects based on NPV, payback period, IRR, and ARR. The report also covers the types of information needed by decision-makers and explains the impact of finance on financial statements, including income statements and balance sheets. Finally, it calculates accounting ratios to assess the financial performance of the business, providing a comprehensive overview of financial management practices at XYZ Ltd.

MANGING FINANCIAL

RESOURCES AND DECISION

RESOURCES AND DECISION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Range of sources of finance available to build and expand XYZ Ltd..................................1

1.2 Implications of legal, financial and dilution of control with in the organisation..................1

1.3 Benefits of finance for the expansion project.......................................................................2

2.1 Evaluation of the cost of chosen sources of finance for the expansion project....................2

TASK 2............................................................................................................................................2

2.2 importance of financial planning in success of business......................................................2

3.1 Cash flow forecast for the business project...........................................................................3

TASK 3............................................................................................................................................4

3.2 cost analysis to determine margin and price structure..........................................................4

TASK 4............................................................................................................................................5

3.3 Analysis of Investment option..............................................................................................5

TASK 5............................................................................................................................................7

2.3 Type of information needs for each decision maker in organisational context....................7

2.4 Explain the impact of finance (bank loan and investments) on the financial statements......7

4.1 & 4.2 Purpose of income statements and the balance sheet with comparison between

different formats of financial statements.....................................................................................8

4.3 Calculation of accounting ratios to determine the financial performance of business..........8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Range of sources of finance available to build and expand XYZ Ltd..................................1

1.2 Implications of legal, financial and dilution of control with in the organisation..................1

1.3 Benefits of finance for the expansion project.......................................................................2

2.1 Evaluation of the cost of chosen sources of finance for the expansion project....................2

TASK 2............................................................................................................................................2

2.2 importance of financial planning in success of business......................................................2

3.1 Cash flow forecast for the business project...........................................................................3

TASK 3............................................................................................................................................4

3.2 cost analysis to determine margin and price structure..........................................................4

TASK 4............................................................................................................................................5

3.3 Analysis of Investment option..............................................................................................5

TASK 5............................................................................................................................................7

2.3 Type of information needs for each decision maker in organisational context....................7

2.4 Explain the impact of finance (bank loan and investments) on the financial statements......7

4.1 & 4.2 Purpose of income statements and the balance sheet with comparison between

different formats of financial statements.....................................................................................8

4.3 Calculation of accounting ratios to determine the financial performance of business..........8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management of Financial resources is the key functional area in managerial terms. This is

one of the important and crucial aspect in terms of managing financial resources with effective

decision making strategies (Zapata and Hall, 2012). In this report, opportunities to develop

techniques to create and present useful information for make effective business decisions are

defined explained. Availability of resources in terms of generating funds for finance defined in

this context. Type of financial information which are used to make strategies and plans are

defined in this context. Planing and budgeting process illustrated by practical overview of

business equations. How effective financial decision assist organisational structure to sustainable

growth and development elaborated in this context.

TASK 1

1.1 Range of sources of finance available to build and expand XYZ Ltd

There are type of financial resources are found in respect of generating financial

requirement with in the organisation. Main financial resources subject to generating finance are

defined as follows:

Owner's capital: owners of organisation contributes funds by their own. This is one of

the cost effective source of funding with in the organisation. Business need not to pay any further

cost to external parties. Owner's keep significant share in profit in exchange of their contribution.

Loans: this is one of the external source of funding which fulfil the short term and long

term requirement of finance with in the organisation. Company has to pay interest on the loan

amount for a specific rate of interest. Short term loans contains high rate of interest and long

terms loans contains low rate of interest (Yang and Wong, 2012).

Retain earnings: this source of fund is considered as internal source of funding subject

to fulfil the financial requirement with in the organisation.

1.2 Implications of legal, financial and dilution of control with in the organisation

Legal financial terms are used to analyse the sustainability of projects and investment.

Financial sources are required to set of implications. Which are required to analyse the aspect in

terms of analysing the comparability of projects and investment. Debt financing and loans are

the sources of funding which contains lots of legal terms and procedures. Organisation has to

face lots of legal formalities and aspects in terms of repayment and payback of loans and interest.

1

Management of Financial resources is the key functional area in managerial terms. This is

one of the important and crucial aspect in terms of managing financial resources with effective

decision making strategies (Zapata and Hall, 2012). In this report, opportunities to develop

techniques to create and present useful information for make effective business decisions are

defined explained. Availability of resources in terms of generating funds for finance defined in

this context. Type of financial information which are used to make strategies and plans are

defined in this context. Planing and budgeting process illustrated by practical overview of

business equations. How effective financial decision assist organisational structure to sustainable

growth and development elaborated in this context.

TASK 1

1.1 Range of sources of finance available to build and expand XYZ Ltd

There are type of financial resources are found in respect of generating financial

requirement with in the organisation. Main financial resources subject to generating finance are

defined as follows:

Owner's capital: owners of organisation contributes funds by their own. This is one of

the cost effective source of funding with in the organisation. Business need not to pay any further

cost to external parties. Owner's keep significant share in profit in exchange of their contribution.

Loans: this is one of the external source of funding which fulfil the short term and long

term requirement of finance with in the organisation. Company has to pay interest on the loan

amount for a specific rate of interest. Short term loans contains high rate of interest and long

terms loans contains low rate of interest (Yang and Wong, 2012).

Retain earnings: this source of fund is considered as internal source of funding subject

to fulfil the financial requirement with in the organisation.

1.2 Implications of legal, financial and dilution of control with in the organisation

Legal financial terms are used to analyse the sustainability of projects and investment.

Financial sources are required to set of implications. Which are required to analyse the aspect in

terms of analysing the comparability of projects and investment. Debt financing and loans are

the sources of funding which contains lots of legal terms and procedures. Organisation has to

face lots of legal formalities and aspects in terms of repayment and payback of loans and interest.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All the legal terms and formats are required to analysed before adopting the finance

source form market. It is required to read all the related documents and papers related to loans

and bonds. Thirty party investments also bound the organisation subject to repayment of loans

and debts. So it is required that organisation need to understand legal dimensions subject to

repayment of loans.

1.3 Benefits of finance for the expansion project

As per analysis of financial resources subject to expansion plan in respect of XYZ Ltd, it

is suggested that loan is considered as options for investment. There are some benefits of loans

and short terms debts are defined below.

Advantages of long term loans: long term loans and debts fulfil long term financial

requirement of organisation. This is one of the beneficial financial resource because interest rates

remain low on long term loans and advances (Witt, Brooke and Buckley, 2013).

Advantages of short term loans: these are the type of financial resources which fulfil

the sort term financial requirement of organisation. Duration of short term loans do not more

than three years.

2.1 Evaluation of the cost of chosen sources of finance for the expansion project

It is seen that the cost of different source of finance remain associated with cost of

expansion plan and project;

Cost of debts and loans: organisation has to pay an specific amount of interest upon

loans and advances. It is required to analyse the cost of operations and advances subject to

determine the cost of long term debts and loans. There is an annual rate of interest is mentioned

upon loans and advances which is considered as cost of financial resources.

Opportunity cost: the cost of losing the existing investment option to choose better

alternative is called as opportunity cost. In other words if an organisation opts a better investment

plans with its existing one, than the difference between the amount of new plan and existing plan

is called as opportunity cost (Spenceleym, 2012).

TASK 2

2.2 importance of financial planning in success of business

REPORT

To Finance manager

2

source form market. It is required to read all the related documents and papers related to loans

and bonds. Thirty party investments also bound the organisation subject to repayment of loans

and debts. So it is required that organisation need to understand legal dimensions subject to

repayment of loans.

1.3 Benefits of finance for the expansion project

As per analysis of financial resources subject to expansion plan in respect of XYZ Ltd, it

is suggested that loan is considered as options for investment. There are some benefits of loans

and short terms debts are defined below.

Advantages of long term loans: long term loans and debts fulfil long term financial

requirement of organisation. This is one of the beneficial financial resource because interest rates

remain low on long term loans and advances (Witt, Brooke and Buckley, 2013).

Advantages of short term loans: these are the type of financial resources which fulfil

the sort term financial requirement of organisation. Duration of short term loans do not more

than three years.

2.1 Evaluation of the cost of chosen sources of finance for the expansion project

It is seen that the cost of different source of finance remain associated with cost of

expansion plan and project;

Cost of debts and loans: organisation has to pay an specific amount of interest upon

loans and advances. It is required to analyse the cost of operations and advances subject to

determine the cost of long term debts and loans. There is an annual rate of interest is mentioned

upon loans and advances which is considered as cost of financial resources.

Opportunity cost: the cost of losing the existing investment option to choose better

alternative is called as opportunity cost. In other words if an organisation opts a better investment

plans with its existing one, than the difference between the amount of new plan and existing plan

is called as opportunity cost (Spenceleym, 2012).

TASK 2

2.2 importance of financial planning in success of business

REPORT

To Finance manager

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

XYZ Ltd.

Subject: Importance of financial planing

Financial planing is becoming most crucial and important aspect in terms of evaluating

financial plans and investment option. Financial forecast and estimation helps to analyse the

sustainability and transparency of investment plans and options. With the help of financial

planing income and expenditures can be managed in effective manner. Cash flow projection

also made with the help of analysing further requirement of cash inflows for operating functions

of business. This basically helps to analyse the capital requirement at initial level which remain

associated with analysing the capital requirement for new projects. Financial planing is a

process which basically helps to sort out the plans and reduce the complexities of financial

decisions.

Financial plan assist the managers to make appropriate strategies and plans as well as align the

departments and functions of organisation in single format. Evaluating capital requirements and

evaluating capital structure are key criteria which are considered in financial planing. This

process defines that how much capital is required to pursue and assist the structure of

organisation. More over finance plans helps to sort out plans and analysing the sustainability of

projects.

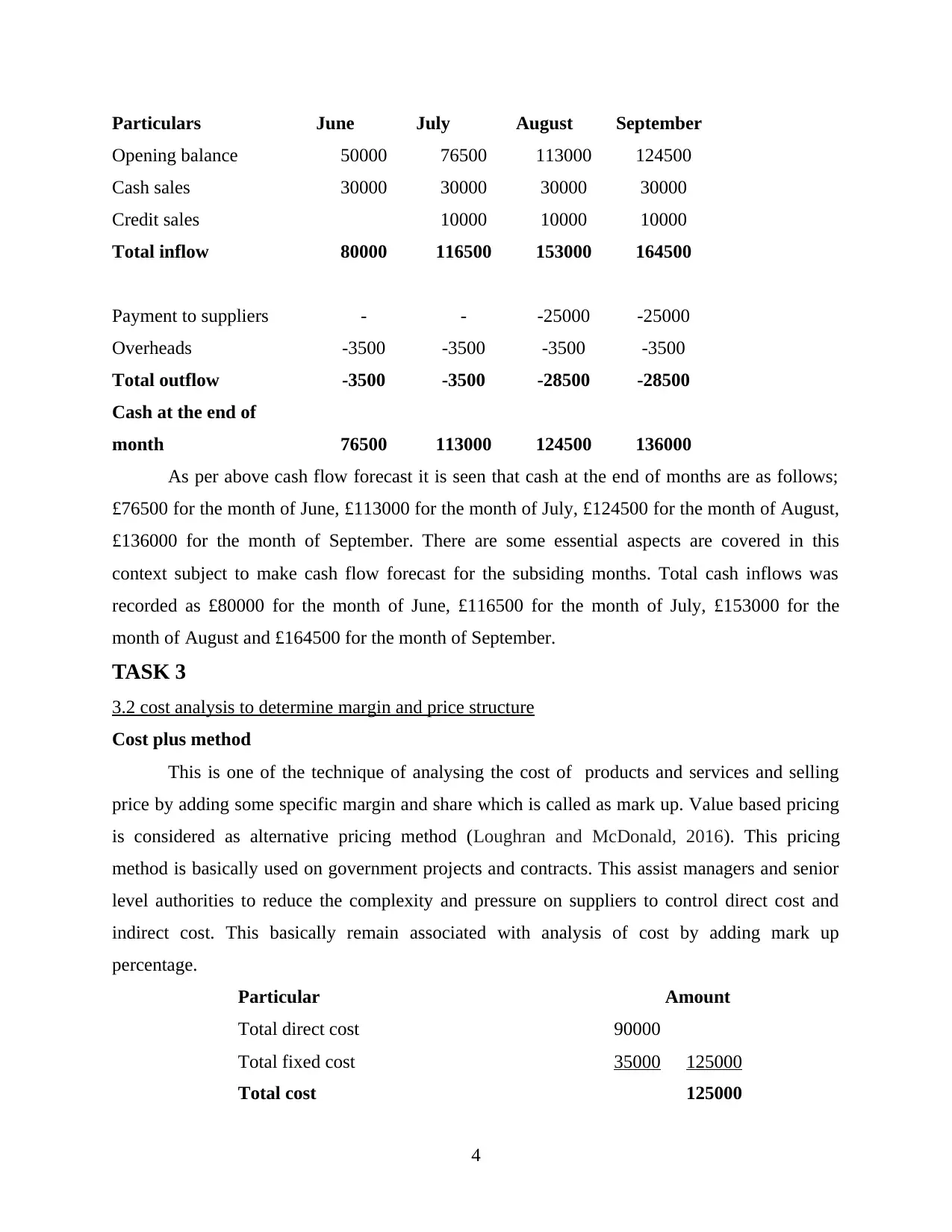

3.1 Cash flow forecast for the business project

Cash flow forecast: this is considered as an estimation in respect of analysing the further

cash requirement in terms of analysing the further cash requirement and needs. With the help of

cash forecast managers and accountants be able to identify the cash requirement and analyse the

requirement of cash for future events and transactions (Rodríguez,Williams and Hall, 2014). It

usually covers the the duration of maximum of 12 months. Cash flow projection provides a vast

overview and aspects in terms of analysing the sustainability and project life cycle for upcoming

events.

There is a cash flow forecast is prepared in respect of XYZ Ltd. There is an allocation of

£50,000 for a new project which is need to start in June 2017. the fund is proposed for

introducing direct usage. Cost of raw material was calculated as £65000 which was not paid till

July, 2017. there are estimated cash flows are given below in respect of June, July, August and

September.

3

Subject: Importance of financial planing

Financial planing is becoming most crucial and important aspect in terms of evaluating

financial plans and investment option. Financial forecast and estimation helps to analyse the

sustainability and transparency of investment plans and options. With the help of financial

planing income and expenditures can be managed in effective manner. Cash flow projection

also made with the help of analysing further requirement of cash inflows for operating functions

of business. This basically helps to analyse the capital requirement at initial level which remain

associated with analysing the capital requirement for new projects. Financial planing is a

process which basically helps to sort out the plans and reduce the complexities of financial

decisions.

Financial plan assist the managers to make appropriate strategies and plans as well as align the

departments and functions of organisation in single format. Evaluating capital requirements and

evaluating capital structure are key criteria which are considered in financial planing. This

process defines that how much capital is required to pursue and assist the structure of

organisation. More over finance plans helps to sort out plans and analysing the sustainability of

projects.

3.1 Cash flow forecast for the business project

Cash flow forecast: this is considered as an estimation in respect of analysing the further

cash requirement in terms of analysing the further cash requirement and needs. With the help of

cash forecast managers and accountants be able to identify the cash requirement and analyse the

requirement of cash for future events and transactions (Rodríguez,Williams and Hall, 2014). It

usually covers the the duration of maximum of 12 months. Cash flow projection provides a vast

overview and aspects in terms of analysing the sustainability and project life cycle for upcoming

events.

There is a cash flow forecast is prepared in respect of XYZ Ltd. There is an allocation of

£50,000 for a new project which is need to start in June 2017. the fund is proposed for

introducing direct usage. Cost of raw material was calculated as £65000 which was not paid till

July, 2017. there are estimated cash flows are given below in respect of June, July, August and

September.

3

Particulars June July August September

Opening balance 50000 76500 113000 124500

Cash sales 30000 30000 30000 30000

Credit sales 10000 10000 10000

Total inflow 80000 116500 153000 164500

Payment to suppliers - - -25000 -25000

Overheads -3500 -3500 -3500 -3500

Total outflow -3500 -3500 -28500 -28500

Cash at the end of

month 76500 113000 124500 136000

As per above cash flow forecast it is seen that cash at the end of months are as follows;

£76500 for the month of June, £113000 for the month of July, £124500 for the month of August,

£136000 for the month of September. There are some essential aspects are covered in this

context subject to make cash flow forecast for the subsiding months. Total cash inflows was

recorded as £80000 for the month of June, £116500 for the month of July, £153000 for the

month of August and £164500 for the month of September.

TASK 3

3.2 cost analysis to determine margin and price structure

Cost plus method

This is one of the technique of analysing the cost of products and services and selling

price by adding some specific margin and share which is called as mark up. Value based pricing

is considered as alternative pricing method (Loughran and McDonald, 2016). This pricing

method is basically used on government projects and contracts. This assist managers and senior

level authorities to reduce the complexity and pressure on suppliers to control direct cost and

indirect cost. This basically remain associated with analysis of cost by adding mark up

percentage.

Particular Amount

Total direct cost 90000

Total fixed cost 35000 125000

Total cost 125000

4

Opening balance 50000 76500 113000 124500

Cash sales 30000 30000 30000 30000

Credit sales 10000 10000 10000

Total inflow 80000 116500 153000 164500

Payment to suppliers - - -25000 -25000

Overheads -3500 -3500 -3500 -3500

Total outflow -3500 -3500 -28500 -28500

Cash at the end of

month 76500 113000 124500 136000

As per above cash flow forecast it is seen that cash at the end of months are as follows;

£76500 for the month of June, £113000 for the month of July, £124500 for the month of August,

£136000 for the month of September. There are some essential aspects are covered in this

context subject to make cash flow forecast for the subsiding months. Total cash inflows was

recorded as £80000 for the month of June, £116500 for the month of July, £153000 for the

month of August and £164500 for the month of September.

TASK 3

3.2 cost analysis to determine margin and price structure

Cost plus method

This is one of the technique of analysing the cost of products and services and selling

price by adding some specific margin and share which is called as mark up. Value based pricing

is considered as alternative pricing method (Loughran and McDonald, 2016). This pricing

method is basically used on government projects and contracts. This assist managers and senior

level authorities to reduce the complexity and pressure on suppliers to control direct cost and

indirect cost. This basically remain associated with analysis of cost by adding mark up

percentage.

Particular Amount

Total direct cost 90000

Total fixed cost 35000 125000

Total cost 125000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

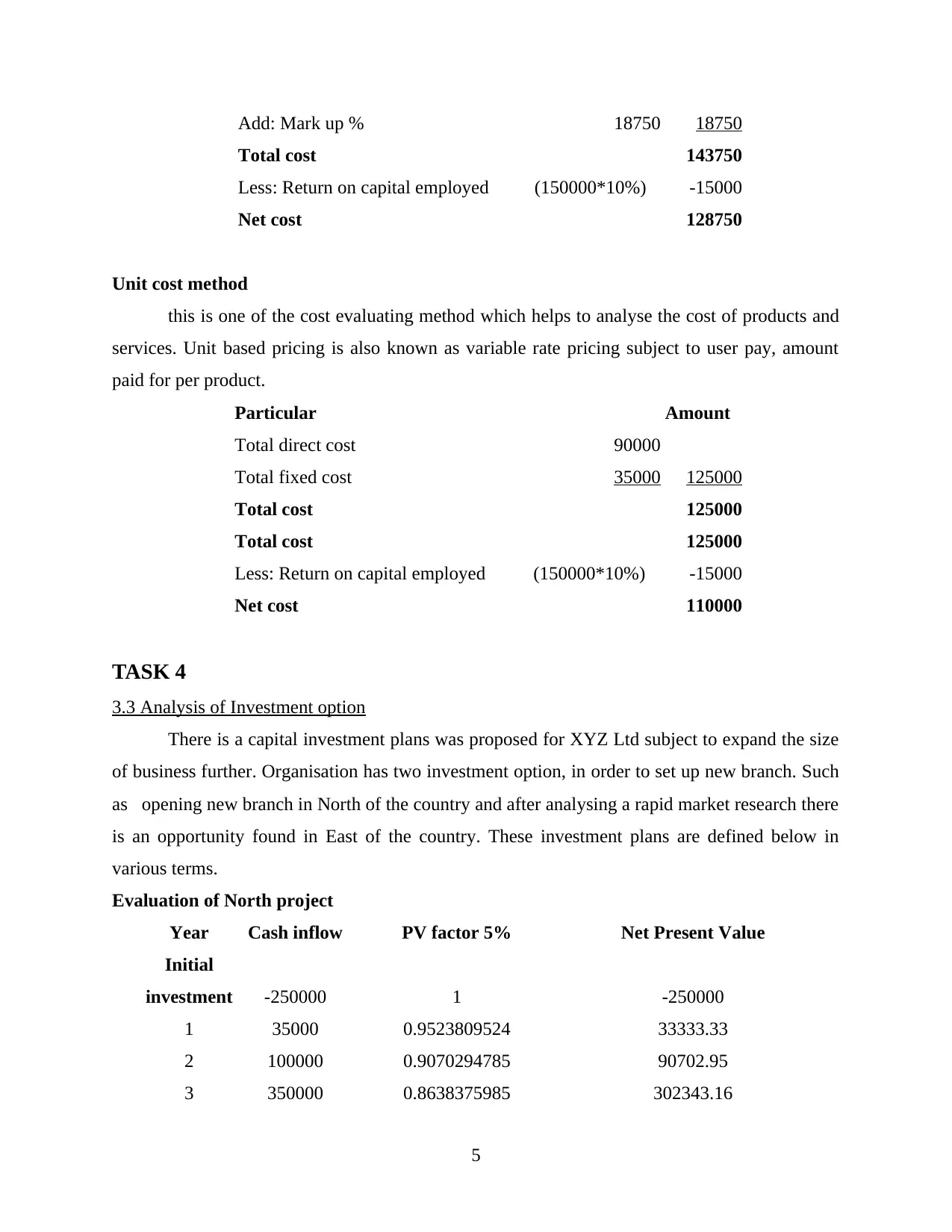

Add: Mark up % 18750 18750

Total cost 143750

Less: Return on capital employed (150000*10%) -15000

Net cost 128750

Unit cost method

this is one of the cost evaluating method which helps to analyse the cost of products and

services. Unit based pricing is also known as variable rate pricing subject to user pay, amount

paid for per product.

Particular Amount

Total direct cost 90000

Total fixed cost 35000 125000

Total cost 125000

Total cost 125000

Less: Return on capital employed (150000*10%) -15000

Net cost 110000

TASK 4

3.3 Analysis of Investment option

There is a capital investment plans was proposed for XYZ Ltd subject to expand the size

of business further. Organisation has two investment option, in order to set up new branch. Such

as opening new branch in North of the country and after analysing a rapid market research there

is an opportunity found in East of the country. These investment plans are defined below in

various terms.

Evaluation of North project

Year Cash inflow PV factor 5% Net Present Value

Initial

investment -250000 1 -250000

1 35000 0.9523809524 33333.33

2 100000 0.9070294785 90702.95

3 350000 0.8638375985 302343.16

5

Total cost 143750

Less: Return on capital employed (150000*10%) -15000

Net cost 128750

Unit cost method

this is one of the cost evaluating method which helps to analyse the cost of products and

services. Unit based pricing is also known as variable rate pricing subject to user pay, amount

paid for per product.

Particular Amount

Total direct cost 90000

Total fixed cost 35000 125000

Total cost 125000

Total cost 125000

Less: Return on capital employed (150000*10%) -15000

Net cost 110000

TASK 4

3.3 Analysis of Investment option

There is a capital investment plans was proposed for XYZ Ltd subject to expand the size

of business further. Organisation has two investment option, in order to set up new branch. Such

as opening new branch in North of the country and after analysing a rapid market research there

is an opportunity found in East of the country. These investment plans are defined below in

various terms.

Evaluation of North project

Year Cash inflow PV factor 5% Net Present Value

Initial

investment -250000 1 -250000

1 35000 0.9523809524 33333.33

2 100000 0.9070294785 90702.95

3 350000 0.8638375985 302343.16

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

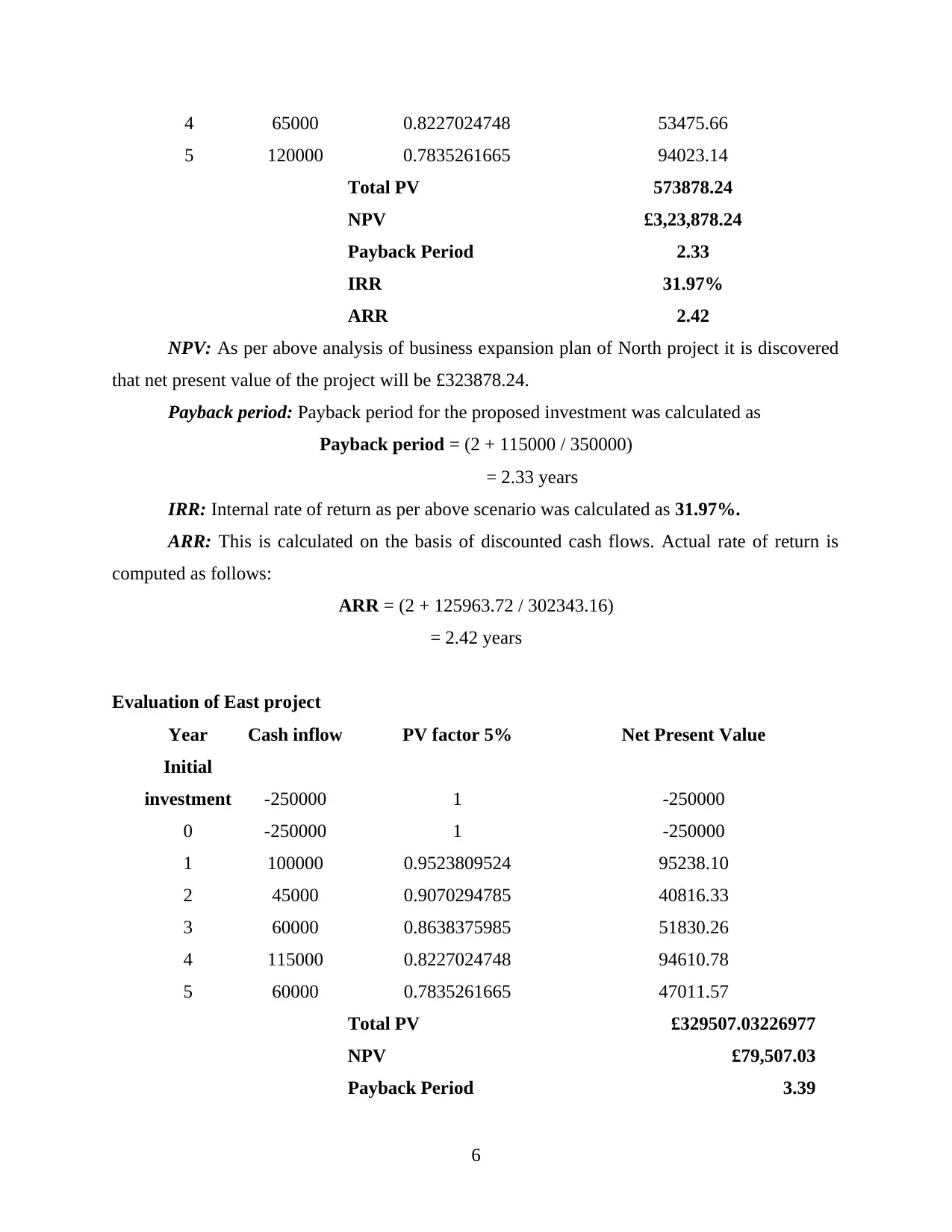

4 65000 0.8227024748 53475.66

5 120000 0.7835261665 94023.14

Total PV 573878.24

NPV £3,23,878.24

Payback Period 2.33

IRR 31.97%

ARR 2.42

NPV: As per above analysis of business expansion plan of North project it is discovered

that net present value of the project will be £323878.24.

Payback period: Payback period for the proposed investment was calculated as

Payback period = (2 + 115000 / 350000)

= 2.33 years

IRR: Internal rate of return as per above scenario was calculated as 31.97%.

ARR: This is calculated on the basis of discounted cash flows. Actual rate of return is

computed as follows:

ARR = (2 + 125963.72 / 302343.16)

= 2.42 years

Evaluation of East project

Year Cash inflow PV factor 5% Net Present Value

Initial

investment -250000 1 -250000

0 -250000 1 -250000

1 100000 0.9523809524 95238.10

2 45000 0.9070294785 40816.33

3 60000 0.8638375985 51830.26

4 115000 0.8227024748 94610.78

5 60000 0.7835261665 47011.57

Total PV £329507.03226977

NPV £79,507.03

Payback Period 3.39

6

5 120000 0.7835261665 94023.14

Total PV 573878.24

NPV £3,23,878.24

Payback Period 2.33

IRR 31.97%

ARR 2.42

NPV: As per above analysis of business expansion plan of North project it is discovered

that net present value of the project will be £323878.24.

Payback period: Payback period for the proposed investment was calculated as

Payback period = (2 + 115000 / 350000)

= 2.33 years

IRR: Internal rate of return as per above scenario was calculated as 31.97%.

ARR: This is calculated on the basis of discounted cash flows. Actual rate of return is

computed as follows:

ARR = (2 + 125963.72 / 302343.16)

= 2.42 years

Evaluation of East project

Year Cash inflow PV factor 5% Net Present Value

Initial

investment -250000 1 -250000

0 -250000 1 -250000

1 100000 0.9523809524 95238.10

2 45000 0.9070294785 40816.33

3 60000 0.8638375985 51830.26

4 115000 0.8227024748 94610.78

5 60000 0.7835261665 47011.57

Total PV £329507.03226977

NPV £79,507.03

Payback Period 3.39

6

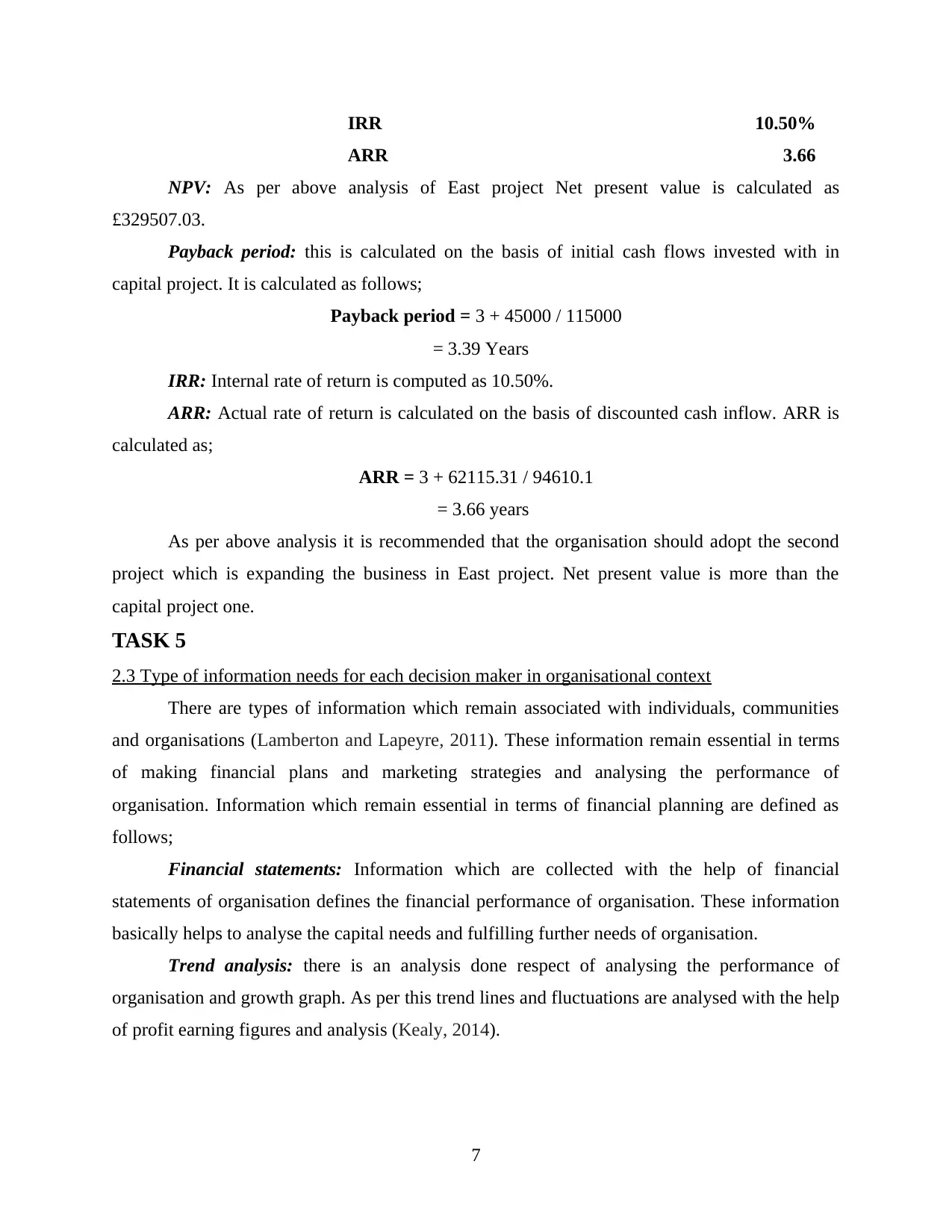

IRR 10.50%

ARR 3.66

NPV: As per above analysis of East project Net present value is calculated as

£329507.03.

Payback period: this is calculated on the basis of initial cash flows invested with in

capital project. It is calculated as follows;

Payback period = 3 + 45000 / 115000

= 3.39 Years

IRR: Internal rate of return is computed as 10.50%.

ARR: Actual rate of return is calculated on the basis of discounted cash inflow. ARR is

calculated as;

ARR = 3 + 62115.31 / 94610.1

= 3.66 years

As per above analysis it is recommended that the organisation should adopt the second

project which is expanding the business in East project. Net present value is more than the

capital project one.

TASK 5

2.3 Type of information needs for each decision maker in organisational context

There are types of information which remain associated with individuals, communities

and organisations (Lamberton and Lapeyre, 2011). These information remain essential in terms

of making financial plans and marketing strategies and analysing the performance of

organisation. Information which remain essential in terms of financial planning are defined as

follows;

Financial statements: Information which are collected with the help of financial

statements of organisation defines the financial performance of organisation. These information

basically helps to analyse the capital needs and fulfilling further needs of organisation.

Trend analysis: there is an analysis done respect of analysing the performance of

organisation and growth graph. As per this trend lines and fluctuations are analysed with the help

of profit earning figures and analysis (Kealy, 2014).

7

ARR 3.66

NPV: As per above analysis of East project Net present value is calculated as

£329507.03.

Payback period: this is calculated on the basis of initial cash flows invested with in

capital project. It is calculated as follows;

Payback period = 3 + 45000 / 115000

= 3.39 Years

IRR: Internal rate of return is computed as 10.50%.

ARR: Actual rate of return is calculated on the basis of discounted cash inflow. ARR is

calculated as;

ARR = 3 + 62115.31 / 94610.1

= 3.66 years

As per above analysis it is recommended that the organisation should adopt the second

project which is expanding the business in East project. Net present value is more than the

capital project one.

TASK 5

2.3 Type of information needs for each decision maker in organisational context

There are types of information which remain associated with individuals, communities

and organisations (Lamberton and Lapeyre, 2011). These information remain essential in terms

of making financial plans and marketing strategies and analysing the performance of

organisation. Information which remain essential in terms of financial planning are defined as

follows;

Financial statements: Information which are collected with the help of financial

statements of organisation defines the financial performance of organisation. These information

basically helps to analyse the capital needs and fulfilling further needs of organisation.

Trend analysis: there is an analysis done respect of analysing the performance of

organisation and growth graph. As per this trend lines and fluctuations are analysed with the help

of profit earning figures and analysis (Kealy, 2014).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government rates and policies: There are some information remain related to tax rates,

charges and information subject to policies. These information helps to reduce the complexity

form decision making process.

Managers be able to sort out the financial plans and complex business situations while

making market strategies.

2.4 Explain the impact of finance (bank loan and investments) on the financial statements

Bank loans and investment are two separate aspects which remain essential in terms of

improving the structure of business. These aspects are defined as follows;

Investments

Investments are considered as assets for the organisation. There is a significant amount is

introduced in to get retain in terms of profit. Investment basically helps to analyse the

sustainability of plans and enhance the income (Greenwood and Scharfstein, 2013). These are

presented in assets side of balance sheer. Return from investments are collected in the form of

interest. There are two types of basic investments are found in organisational context such as

capital investment and revenue investment. Capital investments basically helps to analyse the

long term sustainability of organisation and improve the income graph of organisation.

Loans

These are considered as an liability which is need to pay by the organisation after a

particular period of time. There are two types of loans are found in organisational context such as

short term loans and long term loans. Duration of short term loans not more than one year. This

basically fulfil short term finance requirement for the organisation. Long term loans fulfil the

long term financial requirement of organisation. Rate of interest on short term loans remain high

in comparison to long term loans. These are shown in the liability side of balance sheet.

Organisation has to pay interest on loans. Interest is debited in profit and loss account.

4.1 & 4.2 Purpose of income statements and the balance sheet with comparison between different

formats of financial statements

Purpose of income statement and balance sheet

In accordance with the financial analysis, it has been determine that income statement is

consider as one of the most important part of the company. The main objective is to provide

financial earning performance of an organisation over a particular period of time. This will guide

8

charges and information subject to policies. These information helps to reduce the complexity

form decision making process.

Managers be able to sort out the financial plans and complex business situations while

making market strategies.

2.4 Explain the impact of finance (bank loan and investments) on the financial statements

Bank loans and investment are two separate aspects which remain essential in terms of

improving the structure of business. These aspects are defined as follows;

Investments

Investments are considered as assets for the organisation. There is a significant amount is

introduced in to get retain in terms of profit. Investment basically helps to analyse the

sustainability of plans and enhance the income (Greenwood and Scharfstein, 2013). These are

presented in assets side of balance sheer. Return from investments are collected in the form of

interest. There are two types of basic investments are found in organisational context such as

capital investment and revenue investment. Capital investments basically helps to analyse the

long term sustainability of organisation and improve the income graph of organisation.

Loans

These are considered as an liability which is need to pay by the organisation after a

particular period of time. There are two types of loans are found in organisational context such as

short term loans and long term loans. Duration of short term loans not more than one year. This

basically fulfil short term finance requirement for the organisation. Long term loans fulfil the

long term financial requirement of organisation. Rate of interest on short term loans remain high

in comparison to long term loans. These are shown in the liability side of balance sheet.

Organisation has to pay interest on loans. Interest is debited in profit and loss account.

4.1 & 4.2 Purpose of income statements and the balance sheet with comparison between different

formats of financial statements

Purpose of income statement and balance sheet

In accordance with the financial analysis, it has been determine that income statement is

consider as one of the most important part of the company. The main objective is to provide

financial earning performance of an organisation over a particular period of time. This will guide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managers certain aspects which is related with total gain and loss a company is getting during the

period of time (Baxter and et. al., 2014).

Balance sheet importance:

The overall performance is being analyse by using balance sheet of an organisation. It is used to

reveal the financial position of a business for a particular period of time. By the help of this total

flow of assets and liabilities a company kept in their business in an accounting period.

Financial statements use by sole proprietors:

under this particular organisation, statements of balance sheet and profit an loss statements which

can be formed during the time.

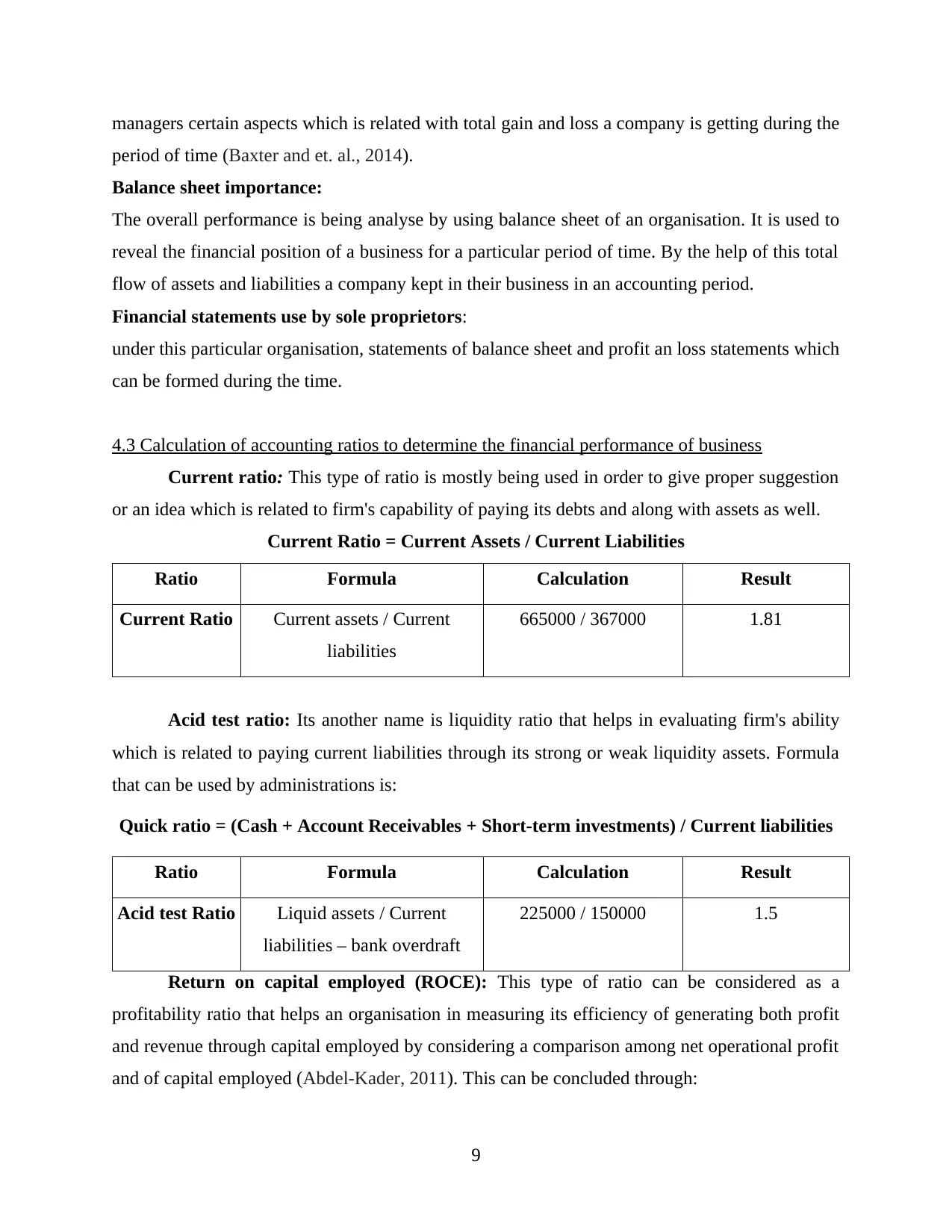

4.3 Calculation of accounting ratios to determine the financial performance of business

Current ratio: This type of ratio is mostly being used in order to give proper suggestion

or an idea which is related to firm's capability of paying its debts and along with assets as well.

Current Ratio = Current Assets / Current Liabilities

Ratio Formula Calculation Result

Current Ratio Current assets / Current

liabilities

665000 / 367000 1.81

Acid test ratio: Its another name is liquidity ratio that helps in evaluating firm's ability

which is related to paying current liabilities through its strong or weak liquidity assets. Formula

that can be used by administrations is:

Quick ratio = (Cash + Account Receivables + Short-term investments) / Current liabilities

Ratio Formula Calculation Result

Acid test Ratio Liquid assets / Current

liabilities – bank overdraft

225000 / 150000 1.5

Return on capital employed (ROCE): This type of ratio can be considered as a

profitability ratio that helps an organisation in measuring its efficiency of generating both profit

and revenue through capital employed by considering a comparison among net operational profit

and of capital employed (Abdel-Kader, 2011). This can be concluded through:

9

period of time (Baxter and et. al., 2014).

Balance sheet importance:

The overall performance is being analyse by using balance sheet of an organisation. It is used to

reveal the financial position of a business for a particular period of time. By the help of this total

flow of assets and liabilities a company kept in their business in an accounting period.

Financial statements use by sole proprietors:

under this particular organisation, statements of balance sheet and profit an loss statements which

can be formed during the time.

4.3 Calculation of accounting ratios to determine the financial performance of business

Current ratio: This type of ratio is mostly being used in order to give proper suggestion

or an idea which is related to firm's capability of paying its debts and along with assets as well.

Current Ratio = Current Assets / Current Liabilities

Ratio Formula Calculation Result

Current Ratio Current assets / Current

liabilities

665000 / 367000 1.81

Acid test ratio: Its another name is liquidity ratio that helps in evaluating firm's ability

which is related to paying current liabilities through its strong or weak liquidity assets. Formula

that can be used by administrations is:

Quick ratio = (Cash + Account Receivables + Short-term investments) / Current liabilities

Ratio Formula Calculation Result

Acid test Ratio Liquid assets / Current

liabilities – bank overdraft

225000 / 150000 1.5

Return on capital employed (ROCE): This type of ratio can be considered as a

profitability ratio that helps an organisation in measuring its efficiency of generating both profit

and revenue through capital employed by considering a comparison among net operational profit

and of capital employed (Abdel-Kader, 2011). This can be concluded through:

9

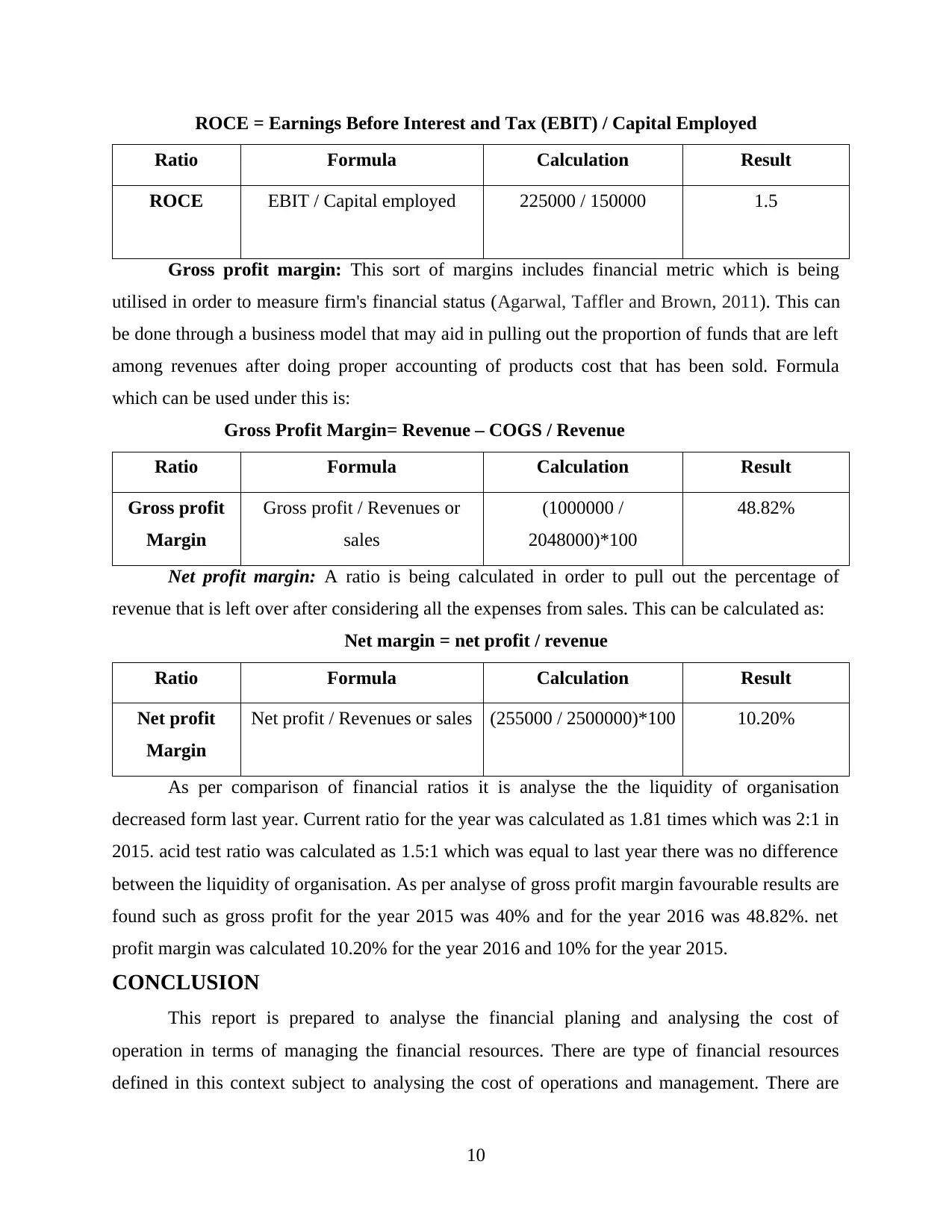

ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed

Ratio Formula Calculation Result

ROCE EBIT / Capital employed 225000 / 150000 1.5

Gross profit margin: This sort of margins includes financial metric which is being

utilised in order to measure firm's financial status (Agarwal, Taffler and Brown, 2011). This can

be done through a business model that may aid in pulling out the proportion of funds that are left

among revenues after doing proper accounting of products cost that has been sold. Formula

which can be used under this is:

Gross Profit Margin= Revenue – COGS / Revenue

Ratio Formula Calculation Result

Gross profit

Margin

Gross profit / Revenues or

sales

(1000000 /

2048000)*100

48.82%

Net profit margin: A ratio is being calculated in order to pull out the percentage of

revenue that is left over after considering all the expenses from sales. This can be calculated as:

Net margin = net profit / revenue

Ratio Formula Calculation Result

Net profit

Margin

Net profit / Revenues or sales (255000 / 2500000)*100 10.20%

As per comparison of financial ratios it is analyse the the liquidity of organisation

decreased form last year. Current ratio for the year was calculated as 1.81 times which was 2:1 in

2015. acid test ratio was calculated as 1.5:1 which was equal to last year there was no difference

between the liquidity of organisation. As per analyse of gross profit margin favourable results are

found such as gross profit for the year 2015 was 40% and for the year 2016 was 48.82%. net

profit margin was calculated 10.20% for the year 2016 and 10% for the year 2015.

CONCLUSION

This report is prepared to analyse the financial planing and analysing the cost of

operation in terms of managing the financial resources. There are type of financial resources

defined in this context subject to analysing the cost of operations and management. There are

10

Ratio Formula Calculation Result

ROCE EBIT / Capital employed 225000 / 150000 1.5

Gross profit margin: This sort of margins includes financial metric which is being

utilised in order to measure firm's financial status (Agarwal, Taffler and Brown, 2011). This can

be done through a business model that may aid in pulling out the proportion of funds that are left

among revenues after doing proper accounting of products cost that has been sold. Formula

which can be used under this is:

Gross Profit Margin= Revenue – COGS / Revenue

Ratio Formula Calculation Result

Gross profit

Margin

Gross profit / Revenues or

sales

(1000000 /

2048000)*100

48.82%

Net profit margin: A ratio is being calculated in order to pull out the percentage of

revenue that is left over after considering all the expenses from sales. This can be calculated as:

Net margin = net profit / revenue

Ratio Formula Calculation Result

Net profit

Margin

Net profit / Revenues or sales (255000 / 2500000)*100 10.20%

As per comparison of financial ratios it is analyse the the liquidity of organisation

decreased form last year. Current ratio for the year was calculated as 1.81 times which was 2:1 in

2015. acid test ratio was calculated as 1.5:1 which was equal to last year there was no difference

between the liquidity of organisation. As per analyse of gross profit margin favourable results are

found such as gross profit for the year 2015 was 40% and for the year 2016 was 48.82%. net

profit margin was calculated 10.20% for the year 2016 and 10% for the year 2015.

CONCLUSION

This report is prepared to analyse the financial planing and analysing the cost of

operation in terms of managing the financial resources. There are type of financial resources

defined in this context subject to analysing the cost of operations and management. There are

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.