Accounting and Financial Management: Zurich Plc Performance Report

VerifiedAdded on 2024/05/20

|15

|4271

|420

Report

AI Summary

This report evaluates the financial performance of Zurich Plc using ratio analysis, covering profitability, liquidity, gearing, asset utilization, and investor potential for the years 2015 and 2016. It calculates and interprets key financial ratios, highlighting trends and potential issues such as increasing liabilities. The report also critically evaluates the limitations of ratio analysis for decision-making, considering factors like historical data, inflation, and differing cost bases. Furthermore, the report assesses the economic feasibility of acquiring a machine using investment appraisal techniques, discussing the benefits and limitations of each method, and evaluates possible sources of finance for the investment. The analysis aims to provide a comprehensive overview of Zurich Plc's financial health and inform strategic decision-making.

Accounting and Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Prepare a report for the Board of Zurich Plc. that evaluates the performance of the company in

relation to profitability, liquidity, gearing, asset utilization, and investor potential. Your report

must be supported by the calculation of relevant ratios in the five evaluation areas mentioned

above................................................................................................................................................4

2. The directors of Zurich Plc want to use the information provided in your report for decision

making and believe ratios provide perfect information for this purpose. Therefore, critically

evaluate the limitations of ratio analysis for decision-making purposes as an additional section

within the report...............................................................................................................................8

All calculations should be clearly shown including all appropriate workings, and should be made

to the nearest £000 or two decimal places where required..............................................................8

Task 2..............................................................................................................................................9

1. Calculate using the following investment appraisal techniques, and provide recommendations

as to the economic feasibility of acquiring the machine:................................................................9

2. Critically evaluate the key benefits and limitations of each of the differing investment

appraisal techniques, supporting the response with relevant academic research as to whether each

of the differing techniques is applied in practice within a real-life business context....................12

3. You are also required to critical evaluate the possible sources of finance to fund this

investment......................................................................................................................................14

Reference.......................................................................................................................................16

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................4

Prepare a report for the Board of Zurich Plc. that evaluates the performance of the company in

relation to profitability, liquidity, gearing, asset utilization, and investor potential. Your report

must be supported by the calculation of relevant ratios in the five evaluation areas mentioned

above................................................................................................................................................4

2. The directors of Zurich Plc want to use the information provided in your report for decision

making and believe ratios provide perfect information for this purpose. Therefore, critically

evaluate the limitations of ratio analysis for decision-making purposes as an additional section

within the report...............................................................................................................................8

All calculations should be clearly shown including all appropriate workings, and should be made

to the nearest £000 or two decimal places where required..............................................................8

Task 2..............................................................................................................................................9

1. Calculate using the following investment appraisal techniques, and provide recommendations

as to the economic feasibility of acquiring the machine:................................................................9

2. Critically evaluate the key benefits and limitations of each of the differing investment

appraisal techniques, supporting the response with relevant academic research as to whether each

of the differing techniques is applied in practice within a real-life business context....................12

3. You are also required to critical evaluate the possible sources of finance to fund this

investment......................................................................................................................................14

Reference.......................................................................................................................................16

2

Introduction

Accounting is the dimension, dispensation and communiqué of the financial information of the

business entities and the corporations. It reveals the profit and loss for a given period and the

worth and the nature of the company’s assets. It is the statement of accounts that provide the

depiction regarding the company’s performance. The financial statements are the final reports

that are provided by the company at the end of the accounting year. It contains the trial balance,

profit and loss account and the balance sheet which predicts the financial report of the company.

3

Accounting is the dimension, dispensation and communiqué of the financial information of the

business entities and the corporations. It reveals the profit and loss for a given period and the

worth and the nature of the company’s assets. It is the statement of accounts that provide the

depiction regarding the company’s performance. The financial statements are the final reports

that are provided by the company at the end of the accounting year. It contains the trial balance,

profit and loss account and the balance sheet which predicts the financial report of the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Prepare a report for the Board of Zurich Plc. that evaluates the performance of the

company in relation to profitability, liquidity, gearing, asset utilization, and investor

potential. Your report must be supported by the calculation of relevant ratios in the five

evaluation areas mentioned above

Financial analyst is the financial head in an organization. The role of financial analyst is to

analyze the financial results of the organization( Finkler, 2016). The financial analyzer is to

check the reports of the organization in a systematic manner. Financial analyst has the ability to

interface between internal customers along with the programming and the technical staff. The

role of the financial analyst is to understand the regulations and laws regarding the financial

sections. As a financial analyst in the Board of Zurich PLC the function will be to overview the

past records of the organization along with the present prospects of the organization and provide

a blue print of the future prospects of the organization in a significant manner. The audit report

along with the minute records of the organization should be provided to the financial analyst in a

systematic manner and here the role of the financial analyst should be to analyze the same and

formulate a policy that would be beneficial and effective for the organization in the future

context (Scott and Davis, 2015). The performance of the organization can be evaluated by the

techniques which are profitability ratio, liquidity ratio, gearing ratio, asset utilization and

investor potential of the organization.

The role of the financial analyst is to operate as per the guidelines provided by the Governing

body of the organization, Board of Directors of the organization along with the internal

management of the organization (Finkler, et al., 2016). Financial analyzer is to perform the

operations of the management is to generate and monitor key performance of the organization.

Financial analyst is to aid in the quarterly, half yearly and annually the annual report of the

organization. The calculations for the compensation section are to be formulated by the financial

analyst. Cash inflow and outflow are to be checked by the financial analyst. Periodically analyze

the balance sheet of the organization is the role of the financial analyzer. The financial analyst is

4

Prepare a report for the Board of Zurich Plc. that evaluates the performance of the

company in relation to profitability, liquidity, gearing, asset utilization, and investor

potential. Your report must be supported by the calculation of relevant ratios in the five

evaluation areas mentioned above

Financial analyst is the financial head in an organization. The role of financial analyst is to

analyze the financial results of the organization( Finkler, 2016). The financial analyzer is to

check the reports of the organization in a systematic manner. Financial analyst has the ability to

interface between internal customers along with the programming and the technical staff. The

role of the financial analyst is to understand the regulations and laws regarding the financial

sections. As a financial analyst in the Board of Zurich PLC the function will be to overview the

past records of the organization along with the present prospects of the organization and provide

a blue print of the future prospects of the organization in a significant manner. The audit report

along with the minute records of the organization should be provided to the financial analyst in a

systematic manner and here the role of the financial analyst should be to analyze the same and

formulate a policy that would be beneficial and effective for the organization in the future

context (Scott and Davis, 2015). The performance of the organization can be evaluated by the

techniques which are profitability ratio, liquidity ratio, gearing ratio, asset utilization and

investor potential of the organization.

The role of the financial analyst is to operate as per the guidelines provided by the Governing

body of the organization, Board of Directors of the organization along with the internal

management of the organization (Finkler, et al., 2016). Financial analyzer is to perform the

operations of the management is to generate and monitor key performance of the organization.

Financial analyst is to aid in the quarterly, half yearly and annually the annual report of the

organization. The calculations for the compensation section are to be formulated by the financial

analyst. Cash inflow and outflow are to be checked by the financial analyst. Periodically analyze

the balance sheet of the organization is the role of the financial analyzer. The financial analyst is

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

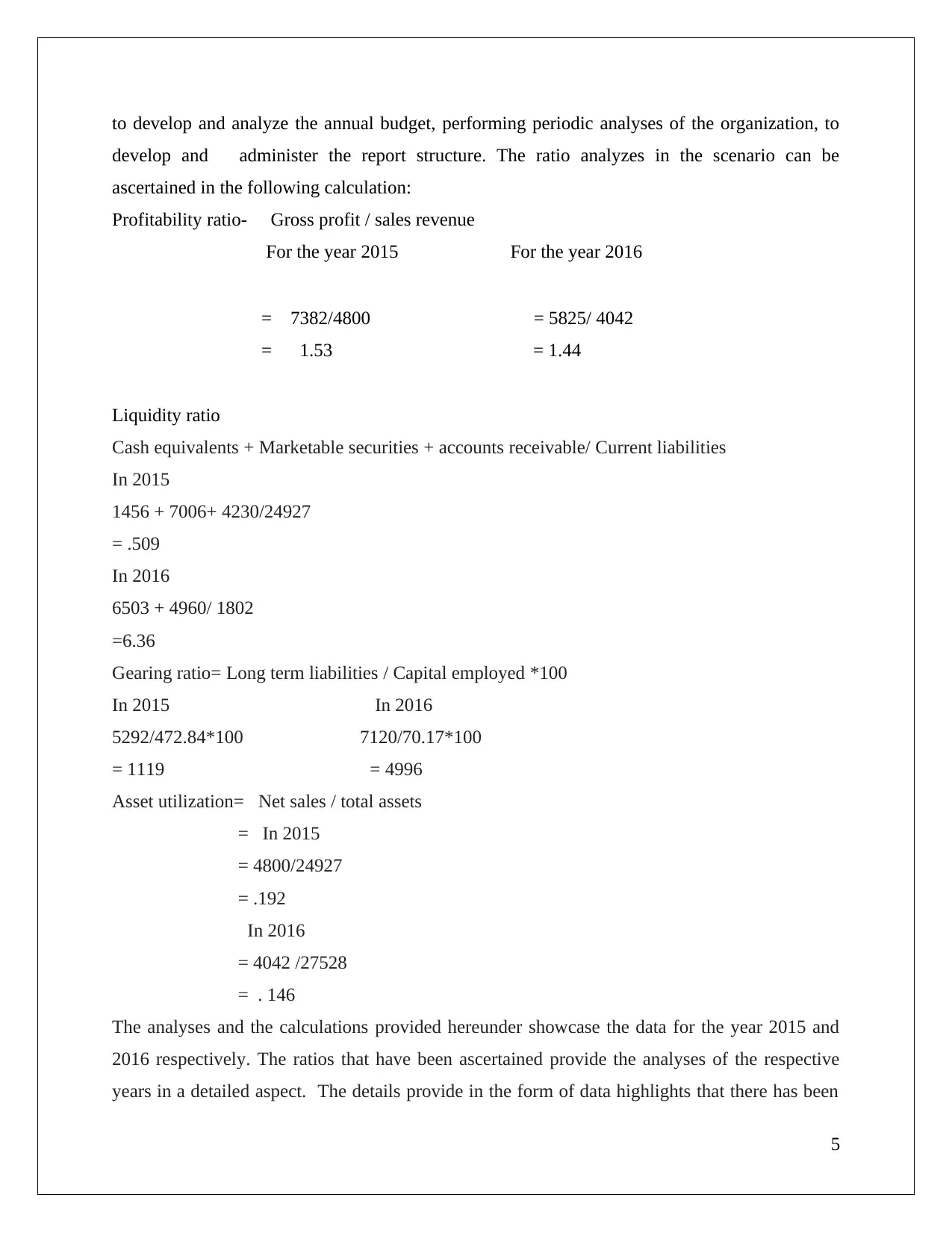

to develop and analyze the annual budget, performing periodic analyses of the organization, to

develop and administer the report structure. The ratio analyzes in the scenario can be

ascertained in the following calculation:

Profitability ratio- Gross profit / sales revenue

For the year 2015 For the year 2016

= 7382/4800 = 5825/ 4042

= 1.53 = 1.44

Liquidity ratio

Cash equivalents + Marketable securities + accounts receivable/ Current liabilities

In 2015

1456 + 7006+ 4230/24927

= .509

In 2016

6503 + 4960/ 1802

=6.36

Gearing ratio= Long term liabilities / Capital employed *100

In 2015 In 2016

5292/472.84*100 7120/70.17*100

= 1119 = 4996

Asset utilization= Net sales / total assets

= In 2015

= 4800/24927

= .192

In 2016

= 4042 /27528

= . 146

The analyses and the calculations provided hereunder showcase the data for the year 2015 and

2016 respectively. The ratios that have been ascertained provide the analyses of the respective

years in a detailed aspect. The details provide in the form of data highlights that there has been

5

develop and administer the report structure. The ratio analyzes in the scenario can be

ascertained in the following calculation:

Profitability ratio- Gross profit / sales revenue

For the year 2015 For the year 2016

= 7382/4800 = 5825/ 4042

= 1.53 = 1.44

Liquidity ratio

Cash equivalents + Marketable securities + accounts receivable/ Current liabilities

In 2015

1456 + 7006+ 4230/24927

= .509

In 2016

6503 + 4960/ 1802

=6.36

Gearing ratio= Long term liabilities / Capital employed *100

In 2015 In 2016

5292/472.84*100 7120/70.17*100

= 1119 = 4996

Asset utilization= Net sales / total assets

= In 2015

= 4800/24927

= .192

In 2016

= 4042 /27528

= . 146

The analyses and the calculations provided hereunder showcase the data for the year 2015 and

2016 respectively. The ratios that have been ascertained provide the analyses of the respective

years in a detailed aspect. The details provide in the form of data highlights that there has been

5

transition in the respective ratios in the significant years. The ratios ascertained helps to

formulate the policies for the next accounting year and the drawbacks entertained are to be

reviewed and the necessary changes in the formulation of the policies are to be ascertained. The

role in this scenario vests with the financial analyst to check the pros and cons of the policies

simultaneously. The role here vests with the financial analyses of the data ascertained.

Profitability ratio determines the sales revenue along with the income generated in the significant

year (Robinson, 2015). The analyses provide the scenario that the value ascertained in the

significant year tends to provide the overall value for the significant year. It is the determining

factor in the escalation of the profit in the succeeding year. The revenue generated helps to

ascertain the faults prevailing in the respective part and helps to ascertain the policies in the

significant manner. The policy ascertained gives a thought process as to the projection of the

ratio value. It acts as the transition ratio in the formulation of the policies.

Liquidity ratio determines the market securities along with the cash equivalent along with

accounts receivable differentiated by the current liabilities( May, 2017). The value ascertained

helps in the configuration of the revenue generated along with the liabilities configured. It is the

ascertainment of the current scenario regarding the revenue generated and helps to ascertain the

revenue shortfall and the increase in the liability. The future scenario would help in the

configuration of the past and the present records and helps in the elimination of the faults

prevailing and configuring the data in an effective manner.

Gearing ratio formulates the data for the long term liabilities along with the capital employed for

the years 2015 and 2016. The data generated helps to configure that the liabilities in the

respective years tend to increase which led to the decrease in the revenue in the following years.

Increase in the liabilities tends to disfigure the ratio analyses in an effective manner. In order to

curtail the discrepancy the liability ascertained should be provided to the creditors along with the

financial institutions. The allocation of the dues to the respective divisions helps to curtail the

liability to a considerable extent which can retain the creditors market along with the financial

markets. The reduction in the liability would tend to escalate in the field of the revenue

generation which can provide goodwill for the organization simultaneously. The increase in the

revenue acts in the escalation of the goodwill for the organization.

6

formulate the policies for the next accounting year and the drawbacks entertained are to be

reviewed and the necessary changes in the formulation of the policies are to be ascertained. The

role in this scenario vests with the financial analyst to check the pros and cons of the policies

simultaneously. The role here vests with the financial analyses of the data ascertained.

Profitability ratio determines the sales revenue along with the income generated in the significant

year (Robinson, 2015). The analyses provide the scenario that the value ascertained in the

significant year tends to provide the overall value for the significant year. It is the determining

factor in the escalation of the profit in the succeeding year. The revenue generated helps to

ascertain the faults prevailing in the respective part and helps to ascertain the policies in the

significant manner. The policy ascertained gives a thought process as to the projection of the

ratio value. It acts as the transition ratio in the formulation of the policies.

Liquidity ratio determines the market securities along with the cash equivalent along with

accounts receivable differentiated by the current liabilities( May, 2017). The value ascertained

helps in the configuration of the revenue generated along with the liabilities configured. It is the

ascertainment of the current scenario regarding the revenue generated and helps to ascertain the

revenue shortfall and the increase in the liability. The future scenario would help in the

configuration of the past and the present records and helps in the elimination of the faults

prevailing and configuring the data in an effective manner.

Gearing ratio formulates the data for the long term liabilities along with the capital employed for

the years 2015 and 2016. The data generated helps to configure that the liabilities in the

respective years tend to increase which led to the decrease in the revenue in the following years.

Increase in the liabilities tends to disfigure the ratio analyses in an effective manner. In order to

curtail the discrepancy the liability ascertained should be provided to the creditors along with the

financial institutions. The allocation of the dues to the respective divisions helps to curtail the

liability to a considerable extent which can retain the creditors market along with the financial

markets. The reduction in the liability would tend to escalate in the field of the revenue

generation which can provide goodwill for the organization simultaneously. The increase in the

revenue acts in the escalation of the goodwill for the organization.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Asset utilization is the ratio analyses where the net sales along with the total assets are

configured. It helps in the determination of the asset evaluation in the respective fields and in the

proper allocation of assets in the respective fields. This acts as the review index in the calculation

of the asset execution. The asset execution acts as the game changer in the future fields. The

execution of the asset helps in the design of formulating the future prospects in the organization.

This is one of the key aspects in escalating the think tank along with the work force in the

implementation of the policies and improvising the policies in the upliftment of the

organizational prospects. The prospects ascertained after the review of the same helps in

formulating the policies in a systematic manner and helps in the cost effective measures in

implementing the policies along with the development in the same sphere concurrently.

The ratio policies chartered in the above analyses helps in the arrangement of proper and

effective management which acts as the trend setter in the effective management of the same.

The effective execution of the policies encountered helps in the promoting the organization

simultaneously. The managerial prospects in the above provided scenario has a effective role to

implement which is towards effective accountability in the organization significantly. This would

help in eliminating the issues and adequately promote the organization in the global platform.

The effective implementation in the trade would generate a scenario where the prospects of the

organization can be towards the development in the future eliminating the pros and cons

prevailing there under in the specific field prior to the review. This would help in the promotion

of the respective organization with chances of progress and innovation appreciably.

7

configured. It helps in the determination of the asset evaluation in the respective fields and in the

proper allocation of assets in the respective fields. This acts as the review index in the calculation

of the asset execution. The asset execution acts as the game changer in the future fields. The

execution of the asset helps in the design of formulating the future prospects in the organization.

This is one of the key aspects in escalating the think tank along with the work force in the

implementation of the policies and improvising the policies in the upliftment of the

organizational prospects. The prospects ascertained after the review of the same helps in

formulating the policies in a systematic manner and helps in the cost effective measures in

implementing the policies along with the development in the same sphere concurrently.

The ratio policies chartered in the above analyses helps in the arrangement of proper and

effective management which acts as the trend setter in the effective management of the same.

The effective execution of the policies encountered helps in the promoting the organization

simultaneously. The managerial prospects in the above provided scenario has a effective role to

implement which is towards effective accountability in the organization significantly. This would

help in eliminating the issues and adequately promote the organization in the global platform.

The effective implementation in the trade would generate a scenario where the prospects of the

organization can be towards the development in the future eliminating the pros and cons

prevailing there under in the specific field prior to the review. This would help in the promotion

of the respective organization with chances of progress and innovation appreciably.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. The directors of Zurich Plc want to use the information provided in your report for

decision making and believe ratios provide perfect information for this purpose. Therefore,

critically evaluate the limitations of ratio analysis for decision-making purposes as an

additional section within the report.

The calculations that have been explained in the aforesaid question highlights the ratios in the

respective years 2015 and 2016. The ratios as explained provides the detailed analyses of the

financial prospects of the organization concurrently. The ratios act as the determining factor as

regard to the future prospect of the organization in the larger prospects. It is one of the guiding

force which forecasts the trends as regard to the management policies and execution of the

changes in the organization briskly. The ratios that have been explained acts in the decisive zone

in the organization. It is one of the most effective measures in the calculation of the future trends

of the organization.

From the analyses the directors of Zurich PLC can ascertain the drawbacks prevailing and to

justify on the respective grounds. The most important aspect in the analyses is the increase in the

liabilities in the respective field which can create a unanimity in the functioning of the

organization. The statistics ascertained from the liability tends to create the difference in the field

of the ascertainment of the balance sheet and the financial scenario in all the above scenario tend

to increase the liability in the organization. The aspects regarding the ratio analyses can be

configured from the fact that increase in the liability tends to increase the task in the organization

with regard to the payment to the creditors and eliminating the dues retrospectively. Asset should

be in the escalation rather than liability.

It is the effective tool for emphasizing the growth in the organization. However, there are certain

pitfalls in ratio analyses. The pitfalls are summarized hereunder:

1. Historical- The results ascertained in the ratio analyses are resultant from the

chronological data. This does not ascertain that the same statistics may showcase in the

near future. However ratio analyses can be used on pro forma information and compare

it with the past results for reliability.

2. Historical cost and current cost- The data generated in the income statement may be at

current cost and the data generated in the balance sheet may be at historical cost. This

8

decision making and believe ratios provide perfect information for this purpose. Therefore,

critically evaluate the limitations of ratio analysis for decision-making purposes as an

additional section within the report.

The calculations that have been explained in the aforesaid question highlights the ratios in the

respective years 2015 and 2016. The ratios as explained provides the detailed analyses of the

financial prospects of the organization concurrently. The ratios act as the determining factor as

regard to the future prospect of the organization in the larger prospects. It is one of the guiding

force which forecasts the trends as regard to the management policies and execution of the

changes in the organization briskly. The ratios that have been explained acts in the decisive zone

in the organization. It is one of the most effective measures in the calculation of the future trends

of the organization.

From the analyses the directors of Zurich PLC can ascertain the drawbacks prevailing and to

justify on the respective grounds. The most important aspect in the analyses is the increase in the

liabilities in the respective field which can create a unanimity in the functioning of the

organization. The statistics ascertained from the liability tends to create the difference in the field

of the ascertainment of the balance sheet and the financial scenario in all the above scenario tend

to increase the liability in the organization. The aspects regarding the ratio analyses can be

configured from the fact that increase in the liability tends to increase the task in the organization

with regard to the payment to the creditors and eliminating the dues retrospectively. Asset should

be in the escalation rather than liability.

It is the effective tool for emphasizing the growth in the organization. However, there are certain

pitfalls in ratio analyses. The pitfalls are summarized hereunder:

1. Historical- The results ascertained in the ratio analyses are resultant from the

chronological data. This does not ascertain that the same statistics may showcase in the

near future. However ratio analyses can be used on pro forma information and compare

it with the past results for reliability.

2. Historical cost and current cost- The data generated in the income statement may be at

current cost and the data generated in the balance sheet may be at historical cost. This

8

provides difference in the tally regarding both the data generated. This creates adverse

results.

3. Inflation- It is one of the prime factors in the ratio analyses. Escalation in the inflation

would change the ratio analyses all together. This would ascertain that the value

ascertained may not be analogous across period.

4. Accounting policies- The accounting policies may be different in different periods. No

company policies can tally. So comparison with the companies in the respective field

may not be effective.

Task 2

1. Calculate using the following investment appraisal techniques, and provide

recommendations as to the economic feasibility of acquiring the machine:

a. The Payback Period.

b. The Discounted Payback Period.

c. The Accounting Rate of Return.

d. The Net Present Value.

e. The Internal Rate of Return (to two decimal places) (15%)

The analyses in the above scenario are regarding the cash flow during a particular point of time.

The analyses in the above can be ascertained from the configuration of the following scenarios as

depicted.

Payback period- cost of investment / net cash flow

= 2000000/1220000

= 1.639

Discounted Payback Period= Initial investment / Periodical cash flow

= 2000000/350000

= 5.714

Accounting rate of return= Average net profit/ Net investment

= 500000 /2000000

= .25

Net Present Value = Present value of cash outflow/ present value of cash inflow

9

results.

3. Inflation- It is one of the prime factors in the ratio analyses. Escalation in the inflation

would change the ratio analyses all together. This would ascertain that the value

ascertained may not be analogous across period.

4. Accounting policies- The accounting policies may be different in different periods. No

company policies can tally. So comparison with the companies in the respective field

may not be effective.

Task 2

1. Calculate using the following investment appraisal techniques, and provide

recommendations as to the economic feasibility of acquiring the machine:

a. The Payback Period.

b. The Discounted Payback Period.

c. The Accounting Rate of Return.

d. The Net Present Value.

e. The Internal Rate of Return (to two decimal places) (15%)

The analyses in the above scenario are regarding the cash flow during a particular point of time.

The analyses in the above can be ascertained from the configuration of the following scenarios as

depicted.

Payback period- cost of investment / net cash flow

= 2000000/1220000

= 1.639

Discounted Payback Period= Initial investment / Periodical cash flow

= 2000000/350000

= 5.714

Accounting rate of return= Average net profit/ Net investment

= 500000 /2000000

= .25

Net Present Value = Present value of cash outflow/ present value of cash inflow

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 350000/1220000

= .286

Internal rate of return= It is the discounted rate of the net cash inflow along with the investment

ascertained (Robinson, 2015). The maximum the internal rate of return the maximum is the

turnover over the success ding years and vice versa. Internal rate of return is the expected

amount which tend to show case the company’s progress in the respective field.

Net present value is the ascertainment of the present inflow of cash along with the present out

flow of cash during a particular period of time (Jayasekera, 2017). It is the graph which sets the

tone as to the faults that are yet to be delivered. The showcase as regard to the development to

the financial return would tend to provide the outcome adequately.

The Accounting rate of return in the specific field tend to provide the average net profit along

with the net investment incurred during the particular of time (Altonji and Zimmerman, 2017). It

ascertains the turnover during the period of time which helps in the progression in the same

simultaneously. The development in the same can be provided by the accounting rate of return

during the particular point of time. The value ascertained helps in the configuration of the

organization simultaneously. It acts as the trend setter in the configuration of the organization

progress. The development escalation in the respective sphere acts as the minute in the respective

field.

10

= .286

Internal rate of return= It is the discounted rate of the net cash inflow along with the investment

ascertained (Robinson, 2015). The maximum the internal rate of return the maximum is the

turnover over the success ding years and vice versa. Internal rate of return is the expected

amount which tend to show case the company’s progress in the respective field.

Net present value is the ascertainment of the present inflow of cash along with the present out

flow of cash during a particular period of time (Jayasekera, 2017). It is the graph which sets the

tone as to the faults that are yet to be delivered. The showcase as regard to the development to

the financial return would tend to provide the outcome adequately.

The Accounting rate of return in the specific field tend to provide the average net profit along

with the net investment incurred during the particular of time (Altonji and Zimmerman, 2017). It

ascertains the turnover during the period of time which helps in the progression in the same

simultaneously. The development in the same can be provided by the accounting rate of return

during the particular point of time. The value ascertained helps in the configuration of the

organization simultaneously. It acts as the trend setter in the configuration of the organization

progress. The development escalation in the respective sphere acts as the minute in the respective

field.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Critically evaluate the key benefits and limitations of each of the differing investment

appraisal techniques, supporting the response with relevant academic research as to

whether each of the differing techniques is applied in practice within a real-life business

context.

Investment appraisal is group of techniques which is used to define many ways of attraction of

investments (Cummins and Harrington, 2013). The main purpose is to assess the possibility of

purchasing the machine, the worth it can generate. The chief objective is to earn profit so that the

costs are justified. By using the techniques the sunk costs are ignored. There are techniques that

can be used are as follows:

Accounting rate of return(ARR)

Payback period

Discounted cash flow

Risk on investment and sensitivity analysis

Accounting rate of return (ARR)

Accounting rate of return compares the profits that Johnson Ltd can expect from the machine to

the amount needed to be invested (Thomsett, 2017). It is calculated on the expected average

profit on the investment comparing with £2,000,000 that has been invested.

Advantages of ARR method:

It is very easy and simple to calculate and understand.

The method uses the theory of net earnings i.e. earnings after tax. It is an important factor

in the proposal.

It gives a clear method about the profit the machine can provide.

The method is used to understand the current performance of Johnson Ltd.

Disadvantages of ARR method:

The method ignores time factor.

A reasonable rate of return cannot determine on ARR.

It does not consider cash inflows which is more significant than profits.

It does not consider external factors which affects the profits (Cummins et al., 2013).

11

appraisal techniques, supporting the response with relevant academic research as to

whether each of the differing techniques is applied in practice within a real-life business

context.

Investment appraisal is group of techniques which is used to define many ways of attraction of

investments (Cummins and Harrington, 2013). The main purpose is to assess the possibility of

purchasing the machine, the worth it can generate. The chief objective is to earn profit so that the

costs are justified. By using the techniques the sunk costs are ignored. There are techniques that

can be used are as follows:

Accounting rate of return(ARR)

Payback period

Discounted cash flow

Risk on investment and sensitivity analysis

Accounting rate of return (ARR)

Accounting rate of return compares the profits that Johnson Ltd can expect from the machine to

the amount needed to be invested (Thomsett, 2017). It is calculated on the expected average

profit on the investment comparing with £2,000,000 that has been invested.

Advantages of ARR method:

It is very easy and simple to calculate and understand.

The method uses the theory of net earnings i.e. earnings after tax. It is an important factor

in the proposal.

It gives a clear method about the profit the machine can provide.

The method is used to understand the current performance of Johnson Ltd.

Disadvantages of ARR method:

The method ignores time factor.

A reasonable rate of return cannot determine on ARR.

It does not consider cash inflows which is more significant than profits.

It does not consider external factors which affects the profits (Cummins et al., 2013).

11

Payback period

It is a technique for evaluating £2,000,000 by length of time it takes to refund it. It can be the

default technique for Johnson Ltd. It focuses on cashflow over profit.

Advantages of payback period:

It is very easy and simple to calculate and understand.

It needs less cost, labour and time comparing to other methods.

It gives importance on speedy recovery of investment.

It is suitable for company if it has fewer amounts of cash and the position is very weak.

Disadvantages of payback period:

A small change in the labour cost makes a huge change in the earnings.

It ignores short term liquidity of the company.

It can mislead in decisions made on capital budgeting.

It treats each asset individually, but practically it is not feasible(Hang et al., 2012).

Discounted cash flow:

It applies discount rate to work out the present corresponding of future cashflow (Hang et al.,

2012). There are two kinds of methods- the net present value method and internal rate of return.

Advantages of discounted cash flow:

It is used for valuing the company as a whole.

It is easy to understand and can be revised to deal with complex situations.

It can be used by both equity shareholders and debt holders to take decisions about

Johnson Ltd.

Disadvantages of discounted cash flow:

It is dependent highly on inputs, if that is altered slightly there will be a large change in

valuation.

It is dependent on cash flow, so the achievement of the method is connected whether the

company can predict future cash flows precisely.

12

It is a technique for evaluating £2,000,000 by length of time it takes to refund it. It can be the

default technique for Johnson Ltd. It focuses on cashflow over profit.

Advantages of payback period:

It is very easy and simple to calculate and understand.

It needs less cost, labour and time comparing to other methods.

It gives importance on speedy recovery of investment.

It is suitable for company if it has fewer amounts of cash and the position is very weak.

Disadvantages of payback period:

A small change in the labour cost makes a huge change in the earnings.

It ignores short term liquidity of the company.

It can mislead in decisions made on capital budgeting.

It treats each asset individually, but practically it is not feasible(Hang et al., 2012).

Discounted cash flow:

It applies discount rate to work out the present corresponding of future cashflow (Hang et al.,

2012). There are two kinds of methods- the net present value method and internal rate of return.

Advantages of discounted cash flow:

It is used for valuing the company as a whole.

It is easy to understand and can be revised to deal with complex situations.

It can be used by both equity shareholders and debt holders to take decisions about

Johnson Ltd.

Disadvantages of discounted cash flow:

It is dependent highly on inputs, if that is altered slightly there will be a large change in

valuation.

It is dependent on cash flow, so the achievement of the method is connected whether the

company can predict future cash flows precisely.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.