Financial and Managerial Accounting (ACC202) Tutor-Marked Assignment

VerifiedAdded on 2022/08/20

|11

|1659

|7

Homework Assignment

AI Summary

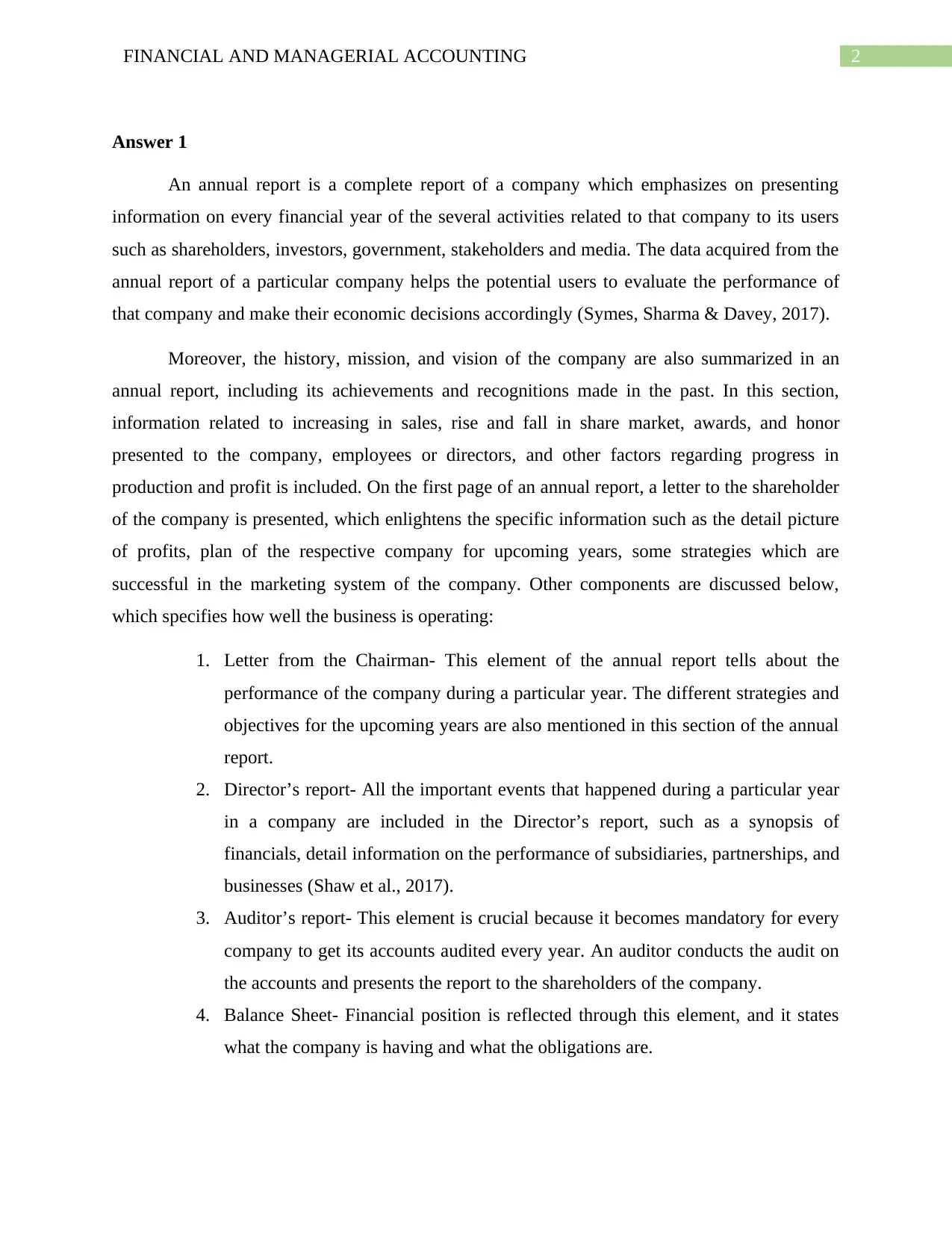

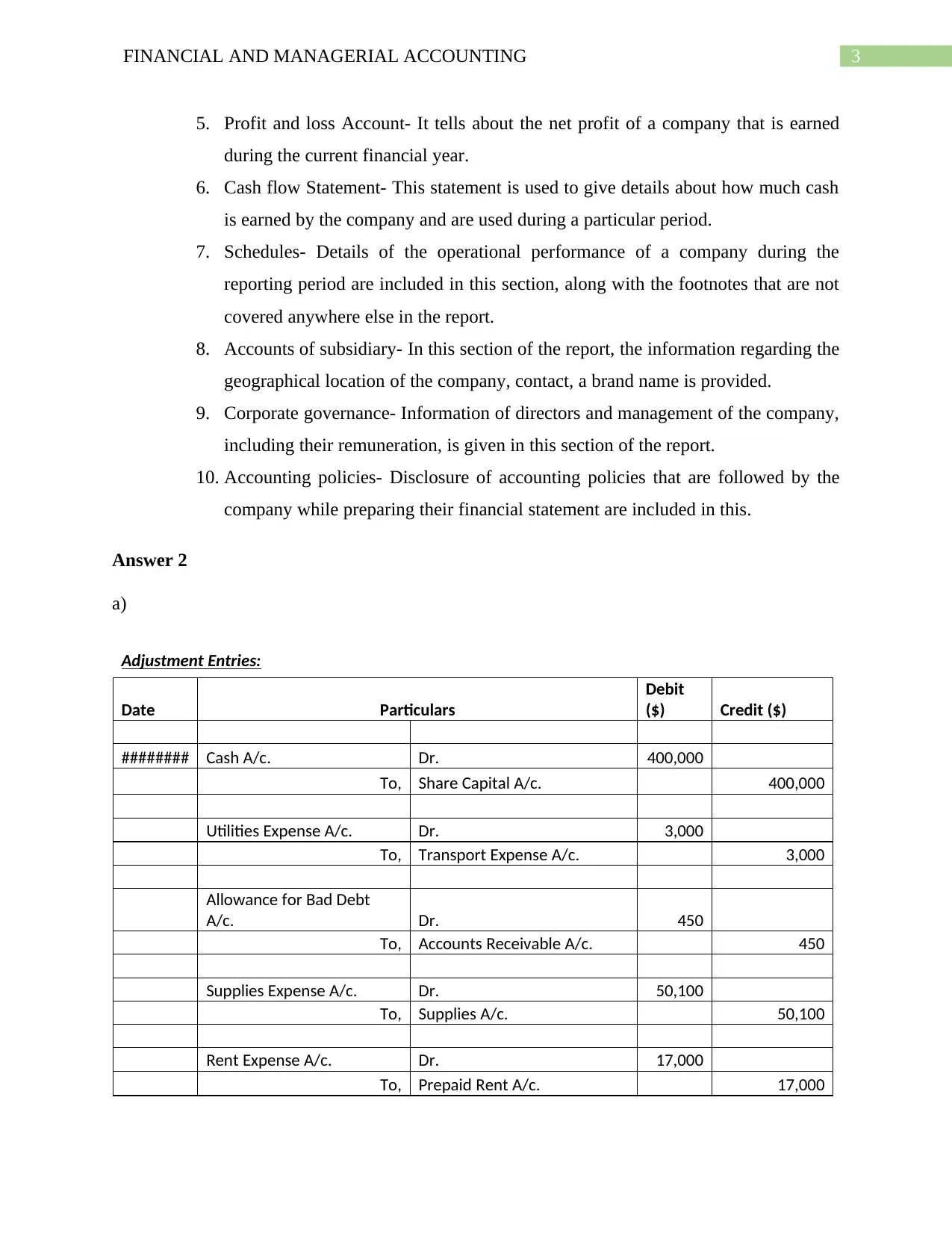

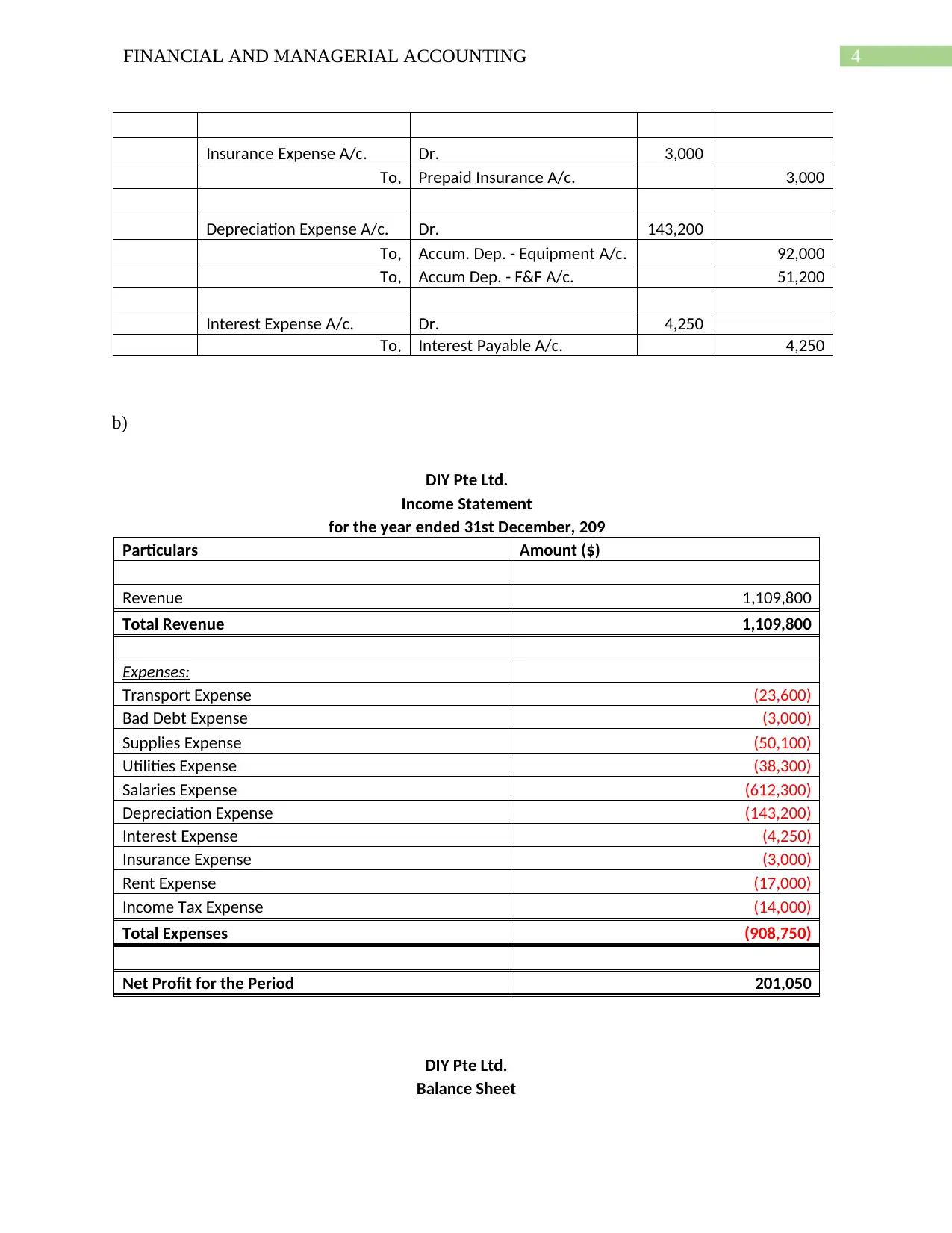

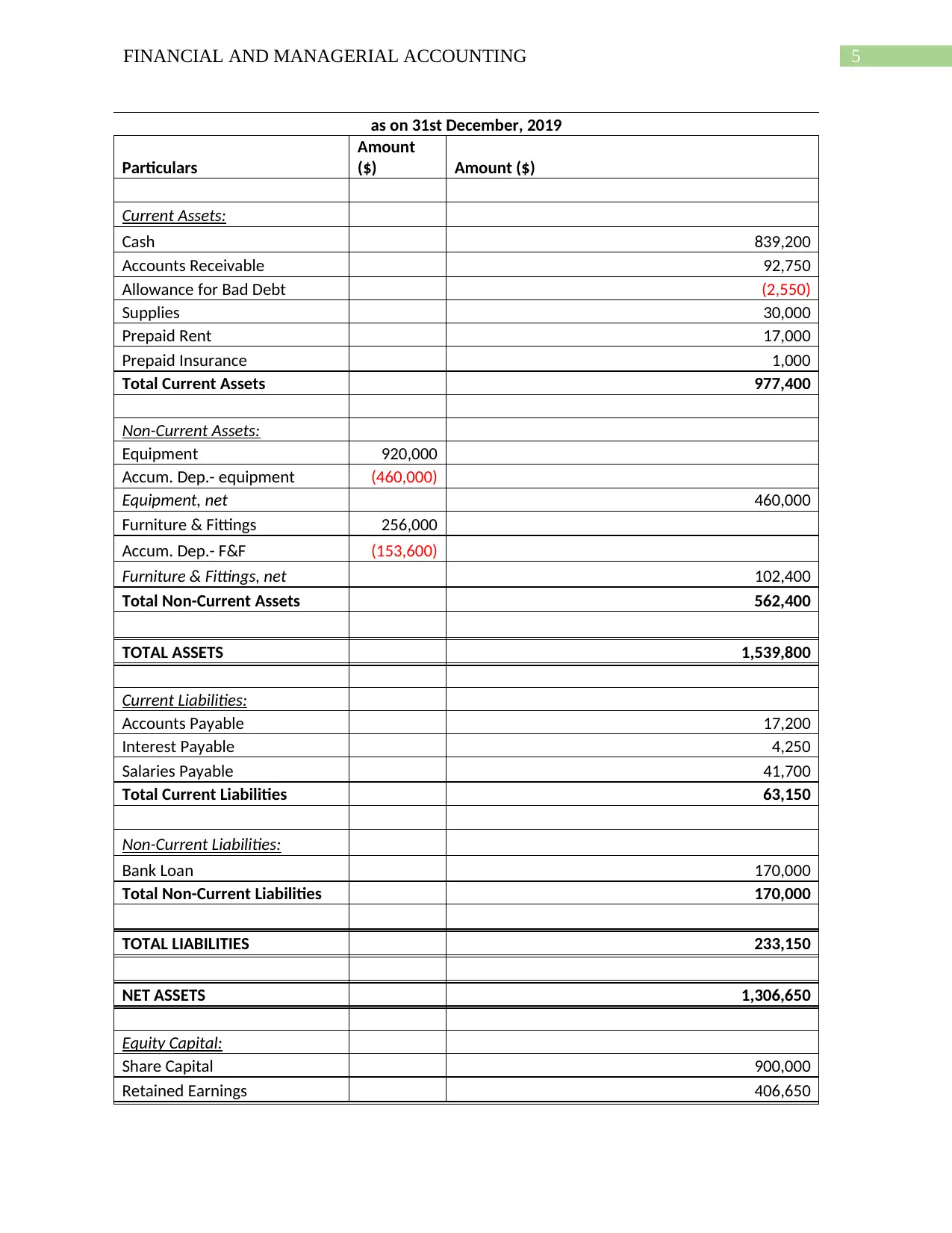

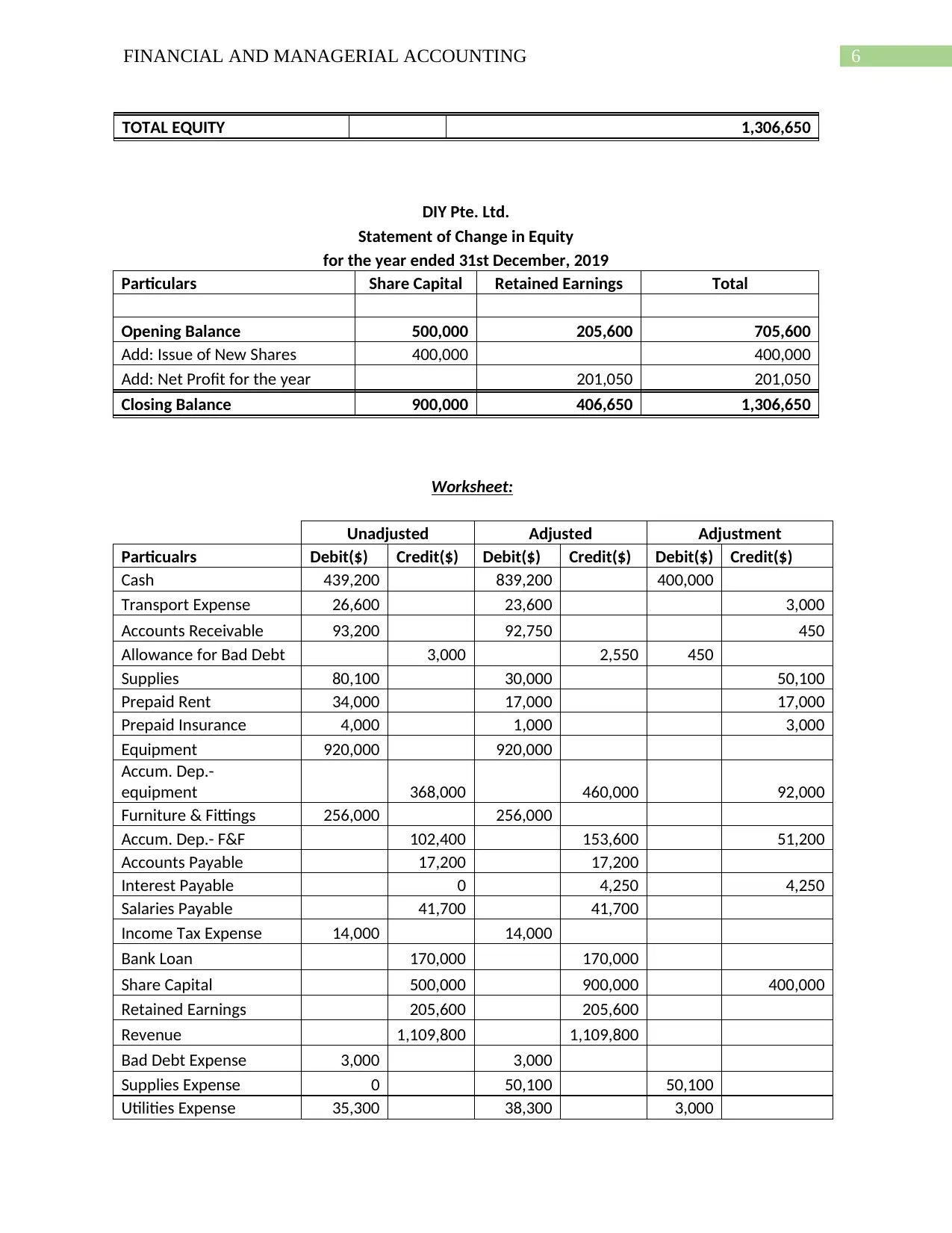

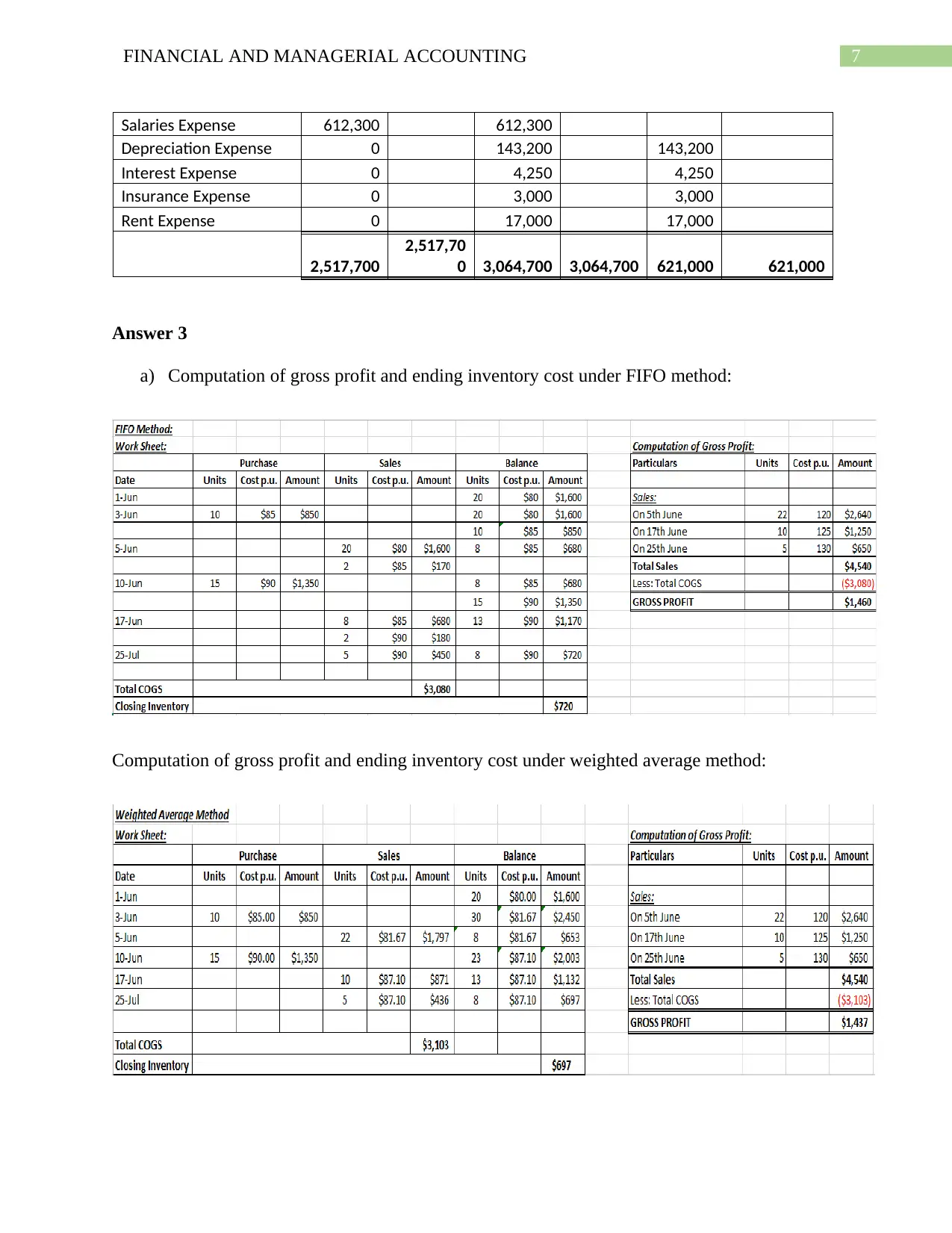

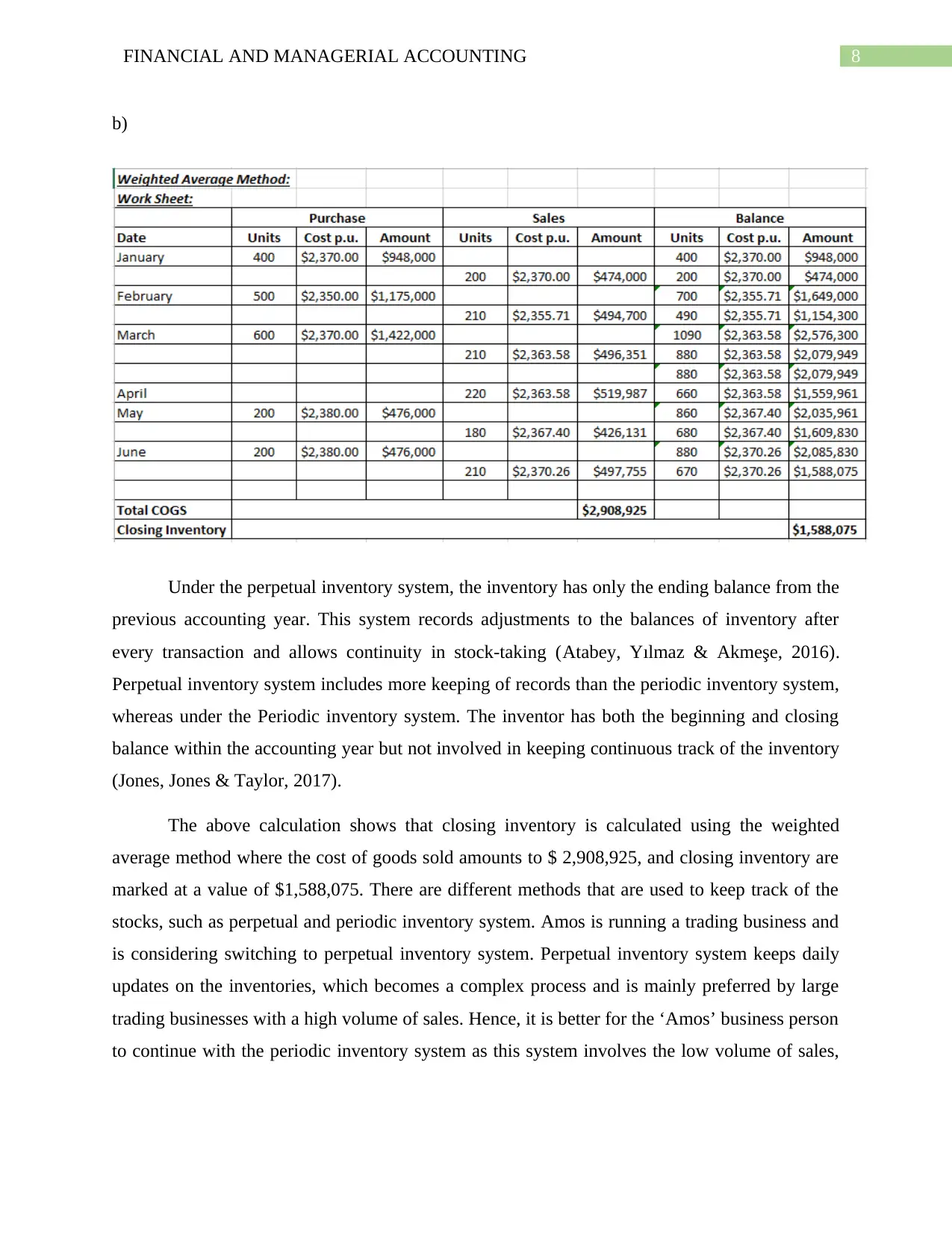

This document presents a comprehensive solution to a Financial and Managerial Accounting (ACC202) Tutor-Marked Assignment (TMA). The assignment explores several key aspects of financial accounting, including the analysis of annual reports, which encompasses the presentation of financial information to stakeholders, and the evaluation of a company's performance. The solution provides detailed adjustment entries and financial statements, including an income statement, balance sheet, and statement of changes in equity for DIY Pte Ltd. It also includes a worksheet demonstrating unadjusted and adjusted trial balances. Furthermore, the assignment delves into inventory management, comparing the FIFO and weighted average methods for calculating gross profit and ending inventory costs. Finally, the solution discusses perpetual and periodic inventory systems, evaluating their suitability for a trading business.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.