Report: Singapore Financial Market Analysis and Strategies

VerifiedAdded on 2020/04/01

|16

|3258

|31

Report

AI Summary

This comprehensive report analyzes the Singapore financial market, focusing on the behavior of the money market, interest rate fluctuations, and the expected inflation rate. It examines the impact of interest rates on the Singapore Overseas Bank over the past three years, providing a trend ana...

Running head: FINANCIAL MARKET

Financial Market

Name of the Student

Name of the University

Author Note

Financial Market

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MARKET

Table of Contents

Table of Contents.............................................................................................................................1

Introduction......................................................................................................................................2

Money Market Behavior..................................................................................................................3

Behavior of Singapore Money market in the next six months........................................................5

Expected Inflation rate.................................................................................................................6

Loan able fund theory..................................................................................................................7

Sources of Funding......................................................................................................................7

Gross Profit......................................................................................................................................8

Money market Instruments..............................................................................................................9

Risks & Obstacles..........................................................................................................................11

Currency risk and Obstacles that are likely to occur.....................................................................11

References......................................................................................................................................13

Table of Contents

Table of Contents.............................................................................................................................1

Introduction......................................................................................................................................2

Money Market Behavior..................................................................................................................3

Behavior of Singapore Money market in the next six months........................................................5

Expected Inflation rate.................................................................................................................6

Loan able fund theory..................................................................................................................7

Sources of Funding......................................................................................................................7

Gross Profit......................................................................................................................................8

Money market Instruments..............................................................................................................9

Risks & Obstacles..........................................................................................................................11

Currency risk and Obstacles that are likely to occur.....................................................................11

References......................................................................................................................................13

2FINANCIAL MARKET

Executive Summary

The main aim of this report is to showcase the analysis concerning Singapore’s economic

outlook and using it to supplement the investment strategies which is given from the data the

expected variation in the interest rate of the country Singapore. This report is prepared to provide

a analysis which shows how money interest rates can affect the money market in the Singapore

Bank. The report shows the impact of interest rates on the Bank for the last three years. It will

show the trend in the rise and fall of the interest rates in the Bank.

The report shows the findings and the forecasting for the Singapore’s interest rates in the

next six months. It provides various strategies that the Singapore Overseas Bank shall undertake

to combat the risks. These are the strategies which are predicted by the Singapore Inter Bank

Offer Rate.

In order to conclude we can say that the report helps to know and predict how interest

rate causes the risks and benefits to the bank in Singapore and how the Singapore Overseas Bank

will maximize its profit from the situation in the Singapore current economic situation. In order

to discuss and have a thorough overview the risk involved from the proposed strategy is

discussed and it is also discussed how to overcome the situation.

Executive Summary

The main aim of this report is to showcase the analysis concerning Singapore’s economic

outlook and using it to supplement the investment strategies which is given from the data the

expected variation in the interest rate of the country Singapore. This report is prepared to provide

a analysis which shows how money interest rates can affect the money market in the Singapore

Bank. The report shows the impact of interest rates on the Bank for the last three years. It will

show the trend in the rise and fall of the interest rates in the Bank.

The report shows the findings and the forecasting for the Singapore’s interest rates in the

next six months. It provides various strategies that the Singapore Overseas Bank shall undertake

to combat the risks. These are the strategies which are predicted by the Singapore Inter Bank

Offer Rate.

In order to conclude we can say that the report helps to know and predict how interest

rate causes the risks and benefits to the bank in Singapore and how the Singapore Overseas Bank

will maximize its profit from the situation in the Singapore current economic situation. In order

to discuss and have a thorough overview the risk involved from the proposed strategy is

discussed and it is also discussed how to overcome the situation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MARKET

Introduction

The report deals with the money market scenario in the Singapore. After analyzing that

we are the money market dealing team and is working for a reputed Singapore Overseas Bank.

Through the analysis and presentation of the historical data for the last three years is has been

found out that the interest has been constant during the year 2014 and 2015 but it has fluctuated

during the second half of 2016.Tis situation due to the reason because the United States Federal

Reserve decided to increase the interest rate and thereby it had impacted on the interest rates of

Singapore thereby resulted in the increase in the interest rates in the Singapore Overseas Bank.

In this report it has been described about the Singapore money market behavior and our

team will analyze and predict the Singapore interest for the next six months. Based o the

prediction and analysis, strategies are made and implemented and which forecast the risk

involving those strategies and hoe the bank will ultimately maximize its profit in the scenario

taking in the factor posed by money market (Bruno and Shin, 2015).

Introduction

The report deals with the money market scenario in the Singapore. After analyzing that

we are the money market dealing team and is working for a reputed Singapore Overseas Bank.

Through the analysis and presentation of the historical data for the last three years is has been

found out that the interest has been constant during the year 2014 and 2015 but it has fluctuated

during the second half of 2016.Tis situation due to the reason because the United States Federal

Reserve decided to increase the interest rate and thereby it had impacted on the interest rates of

Singapore thereby resulted in the increase in the interest rates in the Singapore Overseas Bank.

In this report it has been described about the Singapore money market behavior and our

team will analyze and predict the Singapore interest for the next six months. Based o the

prediction and analysis, strategies are made and implemented and which forecast the risk

involving those strategies and hoe the bank will ultimately maximize its profit in the scenario

taking in the factor posed by money market (Bruno and Shin, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MARKET

Money Market Behavior

2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Interest Rate

Series 1

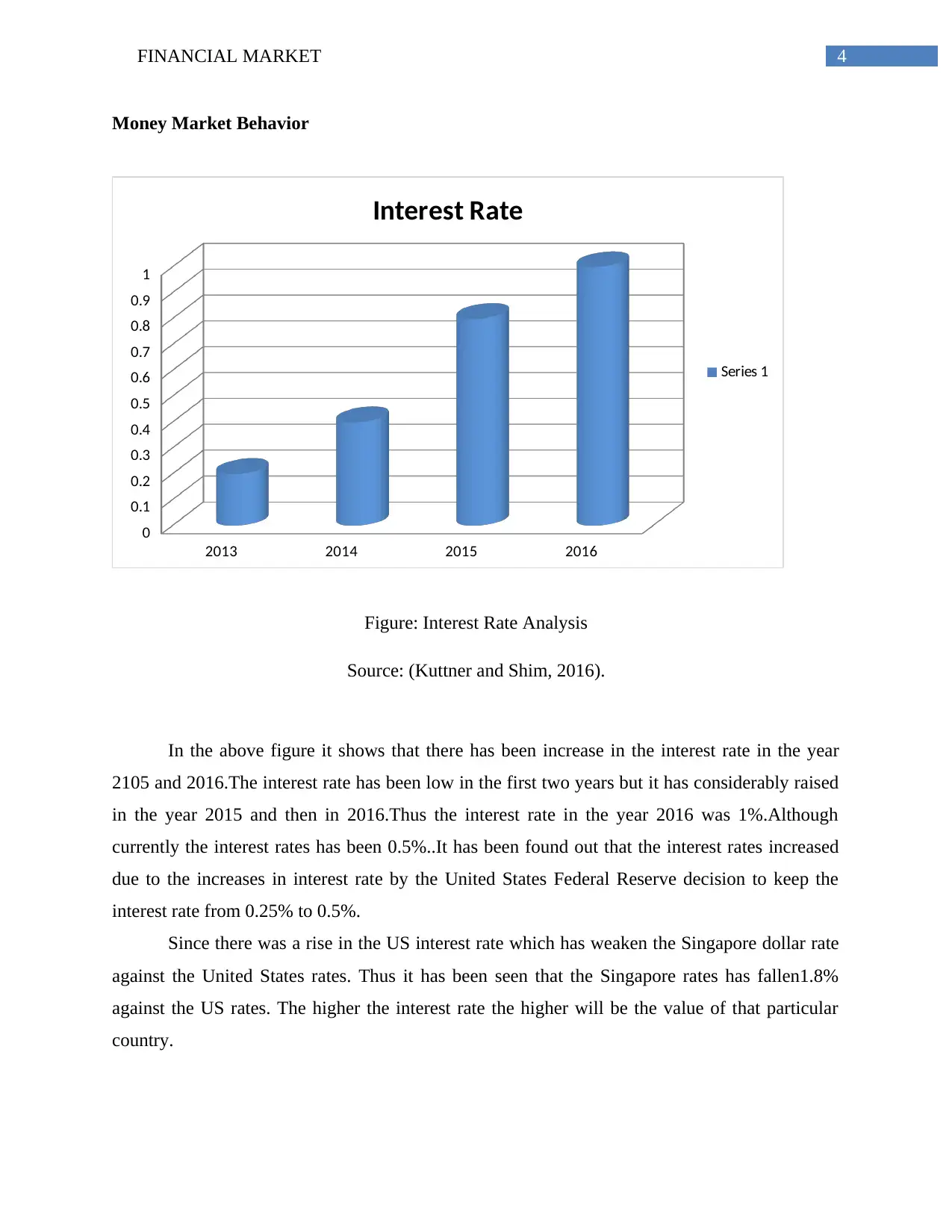

Figure: Interest Rate Analysis

Source: (Kuttner and Shim, 2016).

In the above figure it shows that there has been increase in the interest rate in the year

2105 and 2016.The interest rate has been low in the first two years but it has considerably raised

in the year 2015 and then in 2016.Thus the interest rate in the year 2016 was 1%.Although

currently the interest rates has been 0.5%..It has been found out that the interest rates increased

due to the increases in interest rate by the United States Federal Reserve decision to keep the

interest rate from 0.25% to 0.5%.

Since there was a rise in the US interest rate which has weaken the Singapore dollar rate

against the United States rates. Thus it has been seen that the Singapore rates has fallen1.8%

against the US rates. The higher the interest rate the higher will be the value of that particular

country.

Money Market Behavior

2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Interest Rate

Series 1

Figure: Interest Rate Analysis

Source: (Kuttner and Shim, 2016).

In the above figure it shows that there has been increase in the interest rate in the year

2105 and 2016.The interest rate has been low in the first two years but it has considerably raised

in the year 2015 and then in 2016.Thus the interest rate in the year 2016 was 1%.Although

currently the interest rates has been 0.5%..It has been found out that the interest rates increased

due to the increases in interest rate by the United States Federal Reserve decision to keep the

interest rate from 0.25% to 0.5%.

Since there was a rise in the US interest rate which has weaken the Singapore dollar rate

against the United States rates. Thus it has been seen that the Singapore rates has fallen1.8%

against the US rates. The higher the interest rate the higher will be the value of that particular

country.

5FINANCIAL MARKET

The Singapore interbank rate is use as a bench mark for the using to predict the rate of

mortgage loan and the lending rates. In the near times it has been seen that the US rates have

been increased which eventually depreciated the value of Singapore dollar.

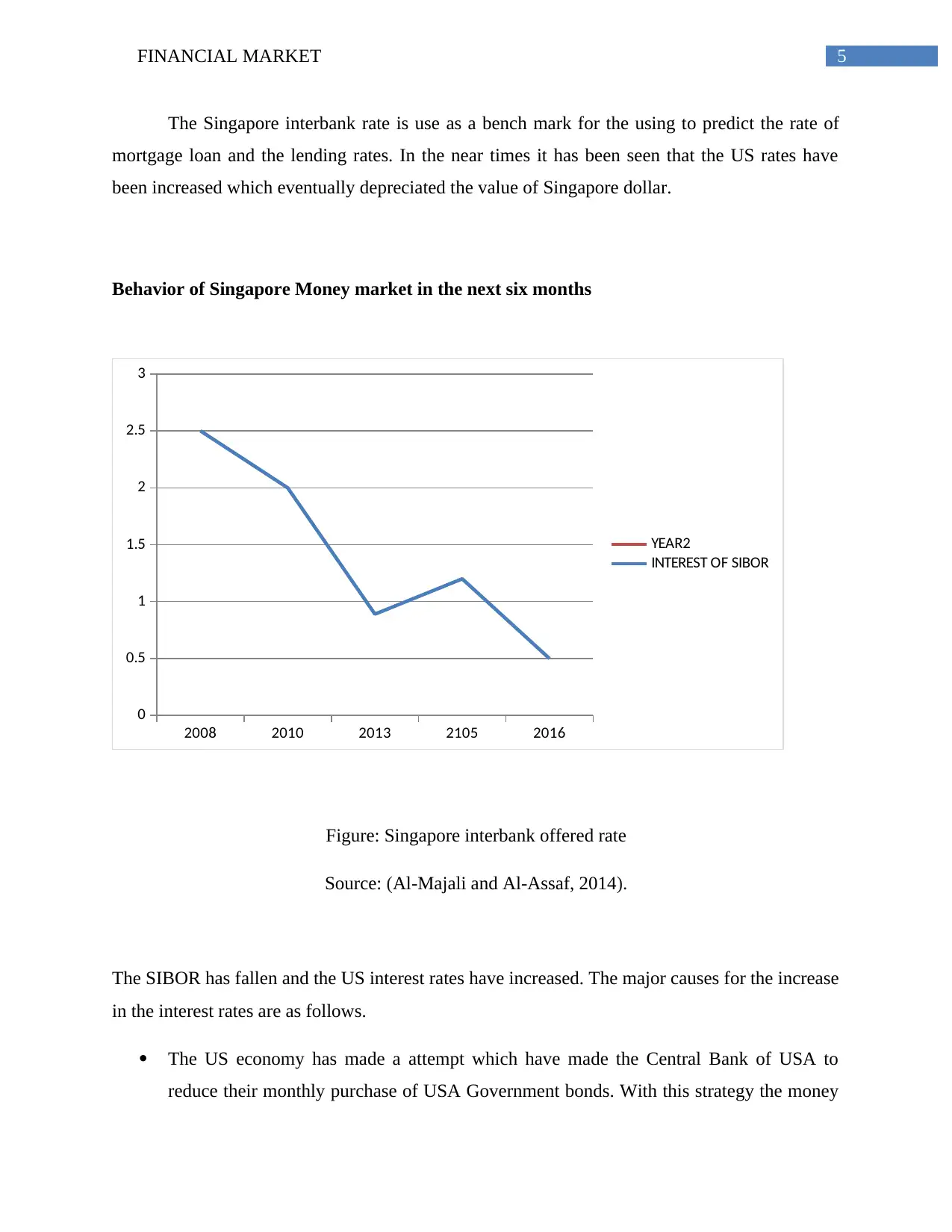

Behavior of Singapore Money market in the next six months

2008 2010 2013 2105 2016

0

0.5

1

1.5

2

2.5

3

YEAR2

INTEREST OF SIBOR

Figure: Singapore interbank offered rate

Source: (Al-Majali and Al-Assaf, 2014).

The SIBOR has fallen and the US interest rates have increased. The major causes for the increase

in the interest rates are as follows.

The US economy has made a attempt which have made the Central Bank of USA to

reduce their monthly purchase of USA Government bonds. With this strategy the money

The Singapore interbank rate is use as a bench mark for the using to predict the rate of

mortgage loan and the lending rates. In the near times it has been seen that the US rates have

been increased which eventually depreciated the value of Singapore dollar.

Behavior of Singapore Money market in the next six months

2008 2010 2013 2105 2016

0

0.5

1

1.5

2

2.5

3

YEAR2

INTEREST OF SIBOR

Figure: Singapore interbank offered rate

Source: (Al-Majali and Al-Assaf, 2014).

The SIBOR has fallen and the US interest rates have increased. The major causes for the increase

in the interest rates are as follows.

The US economy has made a attempt which have made the Central Bank of USA to

reduce their monthly purchase of USA Government bonds. With this strategy the money

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MARKET

has been limited in the bank and the banks charge higher interest rates from the

borrowers (Turner, 2014).

The strength of USD is much higher than the strength of the Singapore dollar which have

resulted in the stable Singapore dollar rates. Thus there has been a rapid increase in dollar

and therefore a fall in SIBOR.

In order to remain competitive the ASEAN have reduced the volatility of the SGD

against Singapore dollar.

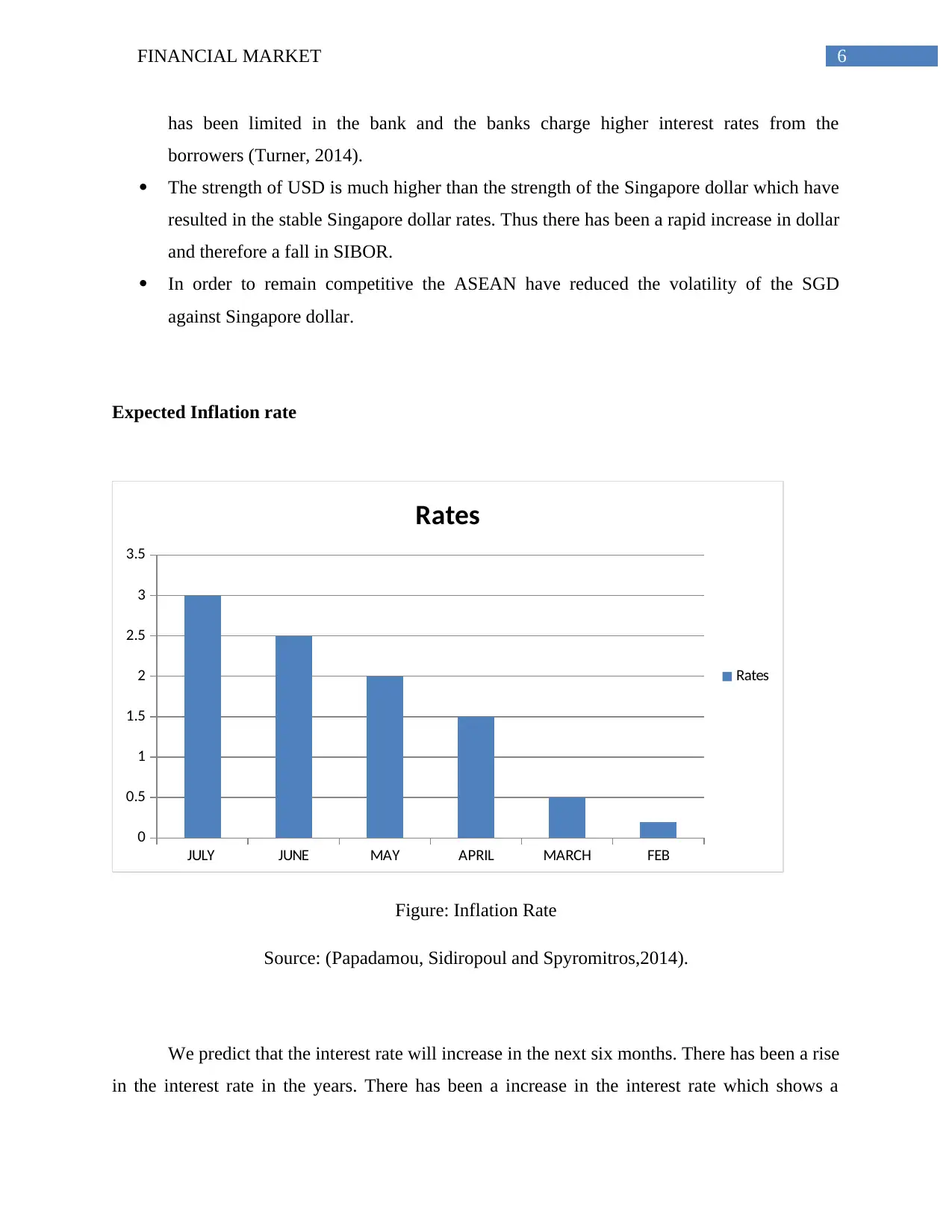

Expected Inflation rate

JULY JUNE MAY APRIL MARCH FEB

0

0.5

1

1.5

2

2.5

3

3.5

Rates

Rates

Figure: Inflation Rate

Source: (Papadamou, Sidiropoul and Spyromitros,2014).

We predict that the interest rate will increase in the next six months. There has been a rise

in the interest rate in the years. There has been a increase in the interest rate which shows a

has been limited in the bank and the banks charge higher interest rates from the

borrowers (Turner, 2014).

The strength of USD is much higher than the strength of the Singapore dollar which have

resulted in the stable Singapore dollar rates. Thus there has been a rapid increase in dollar

and therefore a fall in SIBOR.

In order to remain competitive the ASEAN have reduced the volatility of the SGD

against Singapore dollar.

Expected Inflation rate

JULY JUNE MAY APRIL MARCH FEB

0

0.5

1

1.5

2

2.5

3

3.5

Rates

Rates

Figure: Inflation Rate

Source: (Papadamou, Sidiropoul and Spyromitros,2014).

We predict that the interest rate will increase in the next six months. There has been a rise

in the interest rate in the years. There has been a increase in the interest rate which shows a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MARKET

increase I the value of the economy. The inflation rate is expected to increase with time. We will

predict that there will be a rise in the inflation rate that will rebound the Singapore’s deflation

Loan able fund theory

There is an inverse relationship between the loan able funds and the interest rates since

there is a direct relationship between the loan able funds and the interest rates.

As the interest rate in the Singapore is expected to rise then the demand will fall. The

loan able funds will rise and the higher interest encourages loans and the business will supply

funds (Van Leuvensteijn et al, 2013).

Sources of Funding

Singapore Treasury Bills (T-Bills)

T-bills are a form of instrument in the money market issued by the Monetary Authority

of Singapore (MAS). The minimum requirement for investment is S$1000 using cash or CPF

savings. Once every 3 months, the MAS will put up the auction on a Monday on SGS website as

well as the newspaper. Since T-bills are regarded as risk-free and highly liquid, the interest paid

out usually pales in comparison to other form of investments. Although the rates are usually

consistent from year to year, factors such as macroeconomic conditions and monetary policies of

the country will still play a part in determining the rise of fall of the interests. The pricing of T-

bills are also influenced by the level of investor’s confidence such that demand would rise during

recessions and vice-versa.

Example of a Sum

A sum of $50m will be used for Overnight Cash with a predicted amount of 950 transactions

with the Bid and Offer Rate for Trusty Bank’s Overnight Transactions are stated below.

increase I the value of the economy. The inflation rate is expected to increase with time. We will

predict that there will be a rise in the inflation rate that will rebound the Singapore’s deflation

Loan able fund theory

There is an inverse relationship between the loan able funds and the interest rates since

there is a direct relationship between the loan able funds and the interest rates.

As the interest rate in the Singapore is expected to rise then the demand will fall. The

loan able funds will rise and the higher interest encourages loans and the business will supply

funds (Van Leuvensteijn et al, 2013).

Sources of Funding

Singapore Treasury Bills (T-Bills)

T-bills are a form of instrument in the money market issued by the Monetary Authority

of Singapore (MAS). The minimum requirement for investment is S$1000 using cash or CPF

savings. Once every 3 months, the MAS will put up the auction on a Monday on SGS website as

well as the newspaper. Since T-bills are regarded as risk-free and highly liquid, the interest paid

out usually pales in comparison to other form of investments. Although the rates are usually

consistent from year to year, factors such as macroeconomic conditions and monetary policies of

the country will still play a part in determining the rise of fall of the interests. The pricing of T-

bills are also influenced by the level of investor’s confidence such that demand would rise during

recessions and vice-versa.

Example of a Sum

A sum of $50m will be used for Overnight Cash with a predicted amount of 950 transactions

with the Bid and Offer Rate for Trusty Bank’s Overnight Transactions are stated below.

8FINANCIAL MARKET

Bid Rate (%) Offer Rate (%)

0.76 0.98

Simple Interest Formula: I = PV x I x T

I= interest rate

T = no. of days/365

Gross Profit

$301.38 x 950 = $286311

As given, the anticipated profits after calculations over the period of 6 months will be $286,311.

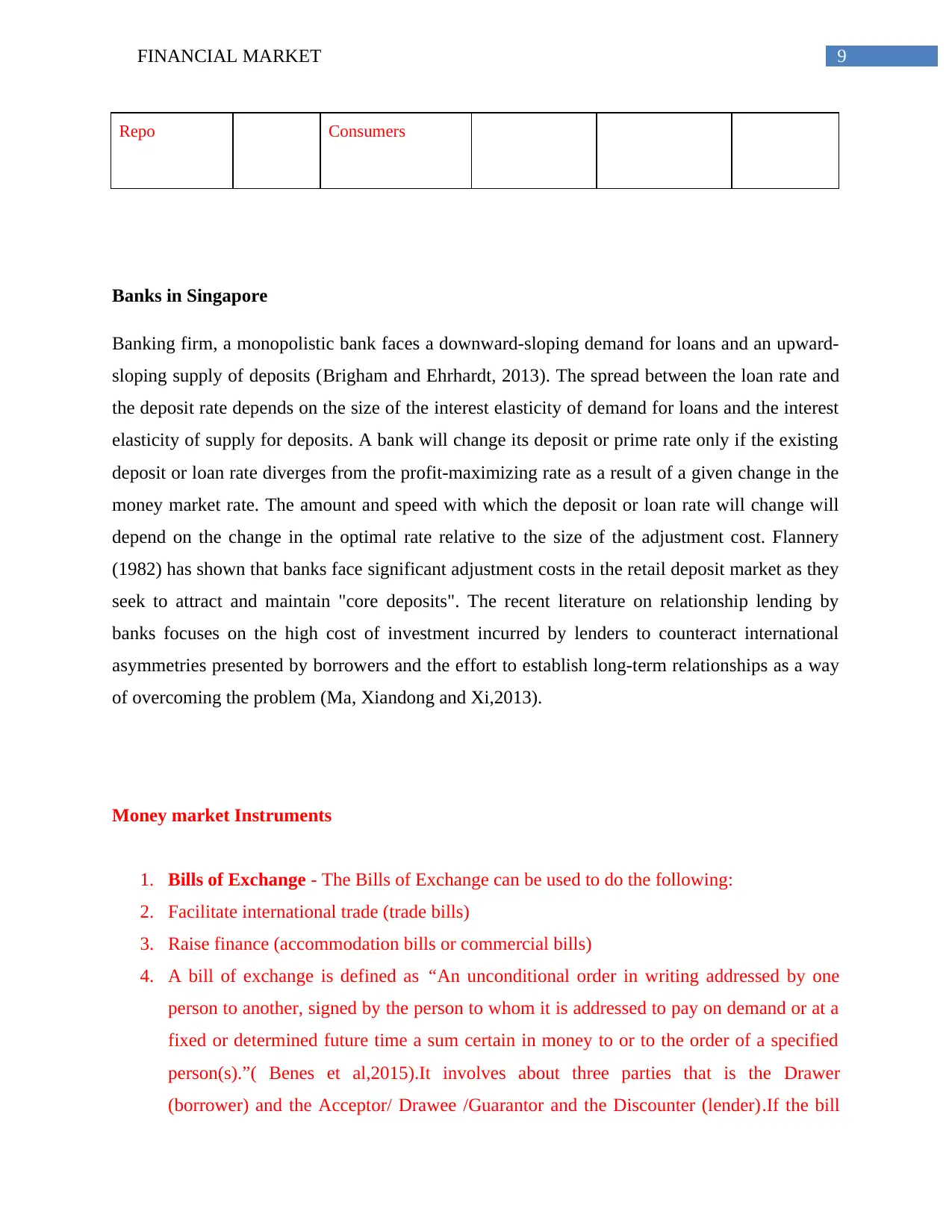

Instrument Maturity Target Market Role of

Trading

Capital

Required

Strategy

Fixed Deposit 12

months

MNCs &

Consumers

Borrower (sell) SGD$ 100 m Price

Making

Fixed term

loan

3 months MNCs &

Consumers

Lender SGD$ 50 m Price

Making

Overnight 6 months MNCs & Lender SGD$ 50 m Speculation

Bid Rate (%) Offer Rate (%)

0.76 0.98

Simple Interest Formula: I = PV x I x T

I= interest rate

T = no. of days/365

Gross Profit

$301.38 x 950 = $286311

As given, the anticipated profits after calculations over the period of 6 months will be $286,311.

Instrument Maturity Target Market Role of

Trading

Capital

Required

Strategy

Fixed Deposit 12

months

MNCs &

Consumers

Borrower (sell) SGD$ 100 m Price

Making

Fixed term

loan

3 months MNCs &

Consumers

Lender SGD$ 50 m Price

Making

Overnight 6 months MNCs & Lender SGD$ 50 m Speculation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MARKET

Repo Consumers

Banks in Singapore

Banking firm, a monopolistic bank faces a downward-sloping demand for loans and an upward-

sloping supply of deposits (Brigham and Ehrhardt, 2013). The spread between the loan rate and

the deposit rate depends on the size of the interest elasticity of demand for loans and the interest

elasticity of supply for deposits. A bank will change its deposit or prime rate only if the existing

deposit or loan rate diverges from the profit-maximizing rate as a result of a given change in the

money market rate. The amount and speed with which the deposit or loan rate will change will

depend on the change in the optimal rate relative to the size of the adjustment cost. Flannery

(1982) has shown that banks face significant adjustment costs in the retail deposit market as they

seek to attract and maintain "core deposits". The recent literature on relationship lending by

banks focuses on the high cost of investment incurred by lenders to counteract international

asymmetries presented by borrowers and the effort to establish long-term relationships as a way

of overcoming the problem (Ma, Xiandong and Xi,2013).

Money market Instruments

1. Bills of Exchange - The Bills of Exchange can be used to do the following:

2. Facilitate international trade (trade bills)

3. Raise finance (accommodation bills or commercial bills)

4. A bill of exchange is defined as “An unconditional order in writing addressed by one

person to another, signed by the person to whom it is addressed to pay on demand or at a

fixed or determined future time a sum certain in money to or to the order of a specified

person(s).”( Benes et al,2015).It involves about three parties that is the Drawer

(borrower) and the Acceptor/ Drawee /Guarantor and the Discounter (lender).If the bill

Repo Consumers

Banks in Singapore

Banking firm, a monopolistic bank faces a downward-sloping demand for loans and an upward-

sloping supply of deposits (Brigham and Ehrhardt, 2013). The spread between the loan rate and

the deposit rate depends on the size of the interest elasticity of demand for loans and the interest

elasticity of supply for deposits. A bank will change its deposit or prime rate only if the existing

deposit or loan rate diverges from the profit-maximizing rate as a result of a given change in the

money market rate. The amount and speed with which the deposit or loan rate will change will

depend on the change in the optimal rate relative to the size of the adjustment cost. Flannery

(1982) has shown that banks face significant adjustment costs in the retail deposit market as they

seek to attract and maintain "core deposits". The recent literature on relationship lending by

banks focuses on the high cost of investment incurred by lenders to counteract international

asymmetries presented by borrowers and the effort to establish long-term relationships as a way

of overcoming the problem (Ma, Xiandong and Xi,2013).

Money market Instruments

1. Bills of Exchange - The Bills of Exchange can be used to do the following:

2. Facilitate international trade (trade bills)

3. Raise finance (accommodation bills or commercial bills)

4. A bill of exchange is defined as “An unconditional order in writing addressed by one

person to another, signed by the person to whom it is addressed to pay on demand or at a

fixed or determined future time a sum certain in money to or to the order of a specified

person(s).”( Benes et al,2015).It involves about three parties that is the Drawer

(borrower) and the Acceptor/ Drawee /Guarantor and the Discounter (lender).If the bill

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MARKET

of exchange is sold in the secondary market, it must be endorsed and in which incurs a

“contingent liability”.

5. Commercial Paper- The commercial paper includes the P – Notes or the commercial

paper. It is essentially called the IOU.The commercial paper is issued by the large

organizations or companies having an excellent credit rating and is having a good capital

structure. Thus the commercial paper is sold and no contingent liability arises a it arises

in the bills of exchange. Thus the commercial bills yields higher than BAB’s (Ghosh,

2016).

6. Treasury Notes- The treasury notes represents the Notes issued by the Government in

order to raise the short term finance. The notes are issued weekly by the tender with

maturity of a period of five, thirteen or twenty six weeks. The treasury notes are accused

to be active in the secondary market amongst the commercial banks (Melvin and Norrbin,

2017).The treasury notes are very liquid instruments and it can be bought and sold by the

Central Bank in this secondary market. Thus the treasury bills have yields lower than the

BAB’s.

7. Certificate of Deposit – The Certificate of Deposit is essentially the promissory notes

that are issued by the banks. The instruments have a maturity of ninety days and one

eighty days. The yield rate which is same as BAB’s.The instrument is usually traded in

the secondary market. It thus have a a minimum denomination which is $ 50000

(Papadamou, Sidiropoulos and Spyromitros, 2017).

8.

of exchange is sold in the secondary market, it must be endorsed and in which incurs a

“contingent liability”.

5. Commercial Paper- The commercial paper includes the P – Notes or the commercial

paper. It is essentially called the IOU.The commercial paper is issued by the large

organizations or companies having an excellent credit rating and is having a good capital

structure. Thus the commercial paper is sold and no contingent liability arises a it arises

in the bills of exchange. Thus the commercial bills yields higher than BAB’s (Ghosh,

2016).

6. Treasury Notes- The treasury notes represents the Notes issued by the Government in

order to raise the short term finance. The notes are issued weekly by the tender with

maturity of a period of five, thirteen or twenty six weeks. The treasury notes are accused

to be active in the secondary market amongst the commercial banks (Melvin and Norrbin,

2017).The treasury notes are very liquid instruments and it can be bought and sold by the

Central Bank in this secondary market. Thus the treasury bills have yields lower than the

BAB’s.

7. Certificate of Deposit – The Certificate of Deposit is essentially the promissory notes

that are issued by the banks. The instruments have a maturity of ninety days and one

eighty days. The yield rate which is same as BAB’s.The instrument is usually traded in

the secondary market. It thus have a a minimum denomination which is $ 50000

(Papadamou, Sidiropoulos and Spyromitros, 2017).

8.

11FINANCIAL MARKET

Risks & Obstacles

Before implementing the strategies, we need to consider the vital facts about risk and

obstacles that company could face. The risk factors are dependent upon China and US economy

and the interest rate. As a company operating in Singapore, all companies within Singapore are

exposed to risks presented in Singapore’s environment, as well as some default risks of the

market or industry.

Currency risk and Obstacles that are likely to occur

Singapore has a lot of trade with China and USA. This causes Singapore dollar to be

influenced by the changes of the economies of those countries. Recently, the economic condition

in China causes them the cut their interest rate by 0.25%, and this reduction result in an

instability of currency in Singapore (Bertay, Demirgüç-Kunt and Huizinga, 2013).

1. Interest Rate Risk

Singapore’s relationship with USA both politically and economically presents both

opportunity and risks to companies in Singapore. Singapore’s economy is heavily relied on

USA’s economy. The US government recently increased their interest rate, and this increment

will have an impact on the interest rate in Singapore (Filardo, Genberg and Hofmann, 2016.).

2. Exchange Rate Risk

For companies that have partnered foreign companies will also have to face exchange rate

risk. When two trading companies from different country have a business transaction, at least

one party will have to face the exchange rate risk of dealing with another currency. A slight

change of exchange rate in the market can cause one party to pay more, or receive less (Jamilov

and Égert, 2014).

3. Market Volatility

Specifically for the money market trading strategy, the short term financing create a risk in

volatility of the market. This volatility causes the return to be unstable and there is a possibility

for a company to receive a lesser return at the end of the contract, than as stated during the

Risks & Obstacles

Before implementing the strategies, we need to consider the vital facts about risk and

obstacles that company could face. The risk factors are dependent upon China and US economy

and the interest rate. As a company operating in Singapore, all companies within Singapore are

exposed to risks presented in Singapore’s environment, as well as some default risks of the

market or industry.

Currency risk and Obstacles that are likely to occur

Singapore has a lot of trade with China and USA. This causes Singapore dollar to be

influenced by the changes of the economies of those countries. Recently, the economic condition

in China causes them the cut their interest rate by 0.25%, and this reduction result in an

instability of currency in Singapore (Bertay, Demirgüç-Kunt and Huizinga, 2013).

1. Interest Rate Risk

Singapore’s relationship with USA both politically and economically presents both

opportunity and risks to companies in Singapore. Singapore’s economy is heavily relied on

USA’s economy. The US government recently increased their interest rate, and this increment

will have an impact on the interest rate in Singapore (Filardo, Genberg and Hofmann, 2016.).

2. Exchange Rate Risk

For companies that have partnered foreign companies will also have to face exchange rate

risk. When two trading companies from different country have a business transaction, at least

one party will have to face the exchange rate risk of dealing with another currency. A slight

change of exchange rate in the market can cause one party to pay more, or receive less (Jamilov

and Égert, 2014).

3. Market Volatility

Specifically for the money market trading strategy, the short term financing create a risk in

volatility of the market. This volatility causes the return to be unstable and there is a possibility

for a company to receive a lesser return at the end of the contract, than as stated during the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12FINANCIAL MARKET

beginning of the contract. The cost of transaction for short term financing of money market

strategy is also more costly compared to other financing instruments.

4. Instrument Risk

This arises when there is adverse condition in the market and there is counterpart default and

credit risk. The money market will consist of the fixed deposits and the treasury bills and the

commercial paper. There is a number of risk then there is less risk due to security and capital

structure. In case there is crisis all over the World the borrowers will have to fail if they buy the

instrument so there is a risk

5. Reinvestment Risk

This risk is of investing in the funds at a lower rate and there the yield will be lower. The

task of managing the reinvestment is very difficult and the short term rates are volatile. In

money market they invest on short term instruments when the yield curve is flat. Since there

money market instruments are very volatile there may be reinvestment risk which needs to be

eliminated.

6. Counterparty Risk

In case of this risk the issuer or the debtor will have the obligation to pay back the

borrowed amount. This will lead the investors to sell off the commercial paper, irrespective

of issuer, selling off indiscriminately. Banks stopped lending to each other, cash markets

froze and multiple counterparties.

7. To manage counterparty risk, RECM only invests in counterparties with strong balance

sheets – and analyses their prudential liquidity requirements, as required by the Reserve

Bank, to identify banks that are facing potential liquidity pressure. RECM Executive

Chairman Piet Viljoen explains: “Even though poor quality counterparties generally pay

higher yields, we generally avoid the

8. Political Risk

beginning of the contract. The cost of transaction for short term financing of money market

strategy is also more costly compared to other financing instruments.

4. Instrument Risk

This arises when there is adverse condition in the market and there is counterpart default and

credit risk. The money market will consist of the fixed deposits and the treasury bills and the

commercial paper. There is a number of risk then there is less risk due to security and capital

structure. In case there is crisis all over the World the borrowers will have to fail if they buy the

instrument so there is a risk

5. Reinvestment Risk

This risk is of investing in the funds at a lower rate and there the yield will be lower. The

task of managing the reinvestment is very difficult and the short term rates are volatile. In

money market they invest on short term instruments when the yield curve is flat. Since there

money market instruments are very volatile there may be reinvestment risk which needs to be

eliminated.

6. Counterparty Risk

In case of this risk the issuer or the debtor will have the obligation to pay back the

borrowed amount. This will lead the investors to sell off the commercial paper, irrespective

of issuer, selling off indiscriminately. Banks stopped lending to each other, cash markets

froze and multiple counterparties.

7. To manage counterparty risk, RECM only invests in counterparties with strong balance

sheets – and analyses their prudential liquidity requirements, as required by the Reserve

Bank, to identify banks that are facing potential liquidity pressure. RECM Executive

Chairman Piet Viljoen explains: “Even though poor quality counterparties generally pay

higher yields, we generally avoid the

8. Political Risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL MARKET

9. There have been a number of steps that has been taken to combat the political risk which

has a implication on the money market. This is due to the reason that the money market

has on the supply of the market. This is due to the fact that has on the supply of the

market and on the exchange risk. The money market players are the large institutional

bodies which have good hold over the market and of the risks involved there are also

interest and also market risks.

10.

9. There have been a number of steps that has been taken to combat the political risk which

has a implication on the money market. This is due to the reason that the money market

has on the supply of the market. This is due to the fact that has on the supply of the

market and on the exchange risk. The money market players are the large institutional

bodies which have good hold over the market and of the risks involved there are also

interest and also market risks.

10.

14FINANCIAL MARKET

References

Al-Majali, A.A. and Al-Assaf, G.I., 2014. Long-run and short-run relationship between stock

market index and main macroeconomic variables performance in Jordan. European Scientific

Journal, ESJ, 10(10).

Benes, J., Berg, A., Portillo, R.A. and Vavra, D., 2015. Modeling sterilized interventions and

balance sheet effects of monetary policy in a New-Keynesian framework. Open Economies

Review, 26(1), pp.81-108.

Bertay, A.C., Demirgüç-Kunt, A. and Huizinga, H., 2013. Do we need big banks? Evidence on

performance, strategy and market discipline. Journal of Financial Intermediation, 22(4), pp.532-

558.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Bruno, V. and Shin, H.S., 2015. Capital flows and the risk-taking channel of monetary

policy. Journal of Monetary Economics, 71, pp.119-132.

Filardo, A., Genberg, H. and Hofmann, B., 2016. Monetary analysis and the global financial

cycle: An Asian central bank perspective. Journal of Asian Economics, 46, pp.1-16.

Ghosh, A., 2016. How does banking sector globalization affect banking crisis?. Journal of

Financial Stability, 25, pp.70-82.

Jamilov, R. and Égert, B., 2014. Interest rate pass-through and monetary policy asymmetry: A

journey into the Caucasian black box. Journal of Asian Economics, 31, pp.57-70.

Kuttner, K.N. and Shim, I., 2016. Can non-interest rate policies stabilize housing markets?

Evidence from a panel of 57 economies. Journal of Financial Stability, 26, pp.31-44.

Loo, H.T., Ang, H.L., Chan, J.Y., Goh, Y.W. and Tan, S.M., 2017. The Determinants of Credit

Risk in Five Selected Southeast Asian Countries(Doctoral dissertation, UTAR).

References

Al-Majali, A.A. and Al-Assaf, G.I., 2014. Long-run and short-run relationship between stock

market index and main macroeconomic variables performance in Jordan. European Scientific

Journal, ESJ, 10(10).

Benes, J., Berg, A., Portillo, R.A. and Vavra, D., 2015. Modeling sterilized interventions and

balance sheet effects of monetary policy in a New-Keynesian framework. Open Economies

Review, 26(1), pp.81-108.

Bertay, A.C., Demirgüç-Kunt, A. and Huizinga, H., 2013. Do we need big banks? Evidence on

performance, strategy and market discipline. Journal of Financial Intermediation, 22(4), pp.532-

558.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Bruno, V. and Shin, H.S., 2015. Capital flows and the risk-taking channel of monetary

policy. Journal of Monetary Economics, 71, pp.119-132.

Filardo, A., Genberg, H. and Hofmann, B., 2016. Monetary analysis and the global financial

cycle: An Asian central bank perspective. Journal of Asian Economics, 46, pp.1-16.

Ghosh, A., 2016. How does banking sector globalization affect banking crisis?. Journal of

Financial Stability, 25, pp.70-82.

Jamilov, R. and Égert, B., 2014. Interest rate pass-through and monetary policy asymmetry: A

journey into the Caucasian black box. Journal of Asian Economics, 31, pp.57-70.

Kuttner, K.N. and Shim, I., 2016. Can non-interest rate policies stabilize housing markets?

Evidence from a panel of 57 economies. Journal of Financial Stability, 26, pp.31-44.

Loo, H.T., Ang, H.L., Chan, J.Y., Goh, Y.W. and Tan, S.M., 2017. The Determinants of Credit

Risk in Five Selected Southeast Asian Countries(Doctoral dissertation, UTAR).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15FINANCIAL MARKET

Ma, G., Xiandong, Y. and Xi, L., 2013. China’s evolving reserve requirements. Journal of

Chinese Economic and Business Studies, 11(2), pp.117-137.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Papadamou, S., Sidiropoulos, M. and Spyromitros, E., 2014. Does central bank transparency

affect stock market volatility?. Journal of International Financial Markets, Institutions and

Money, 31, pp.362-377.

Papadamou, S., Sidiropoulos, M. and Spyromitros, E., 2017. Does central bank independence

affect stock market volatility?. Research in International Business and Finance.

Turner, P., 2014. The global long-term interest rate, financial risks and policy choices in EMEs.

Van Leuvensteijn, M., Sørensen, C.K., Bikker, J.A. and Van Rixtel, A.A., 2013. Impact of bank

competition on the interest rate pass-through in the euro area. Applied Economics, 45(11),

pp.1359-1380.

Ma, G., Xiandong, Y. and Xi, L., 2013. China’s evolving reserve requirements. Journal of

Chinese Economic and Business Studies, 11(2), pp.117-137.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Papadamou, S., Sidiropoulos, M. and Spyromitros, E., 2014. Does central bank transparency

affect stock market volatility?. Journal of International Financial Markets, Institutions and

Money, 31, pp.362-377.

Papadamou, S., Sidiropoulos, M. and Spyromitros, E., 2017. Does central bank independence

affect stock market volatility?. Research in International Business and Finance.

Turner, P., 2014. The global long-term interest rate, financial risks and policy choices in EMEs.

Van Leuvensteijn, M., Sørensen, C.K., Bikker, J.A. and Van Rixtel, A.A., 2013. Impact of bank

competition on the interest rate pass-through in the euro area. Applied Economics, 45(11),

pp.1359-1380.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.