Financial Market Assessment: Yield Curves, Bonds, and Loanable Funds

VerifiedAdded on 2023/01/05

|12

|4159

|64

Homework Assignment

AI Summary

This document provides a comprehensive solution to a financial market assessment, addressing key concepts in finance. The assessment begins with an analysis of yield curves for the US and Europe, comparing and contrasting their shapes and implications for economic growth and interest rates. The solution then proceeds to calculate the market price of corporate bonds issued by a European company, considering factors like coupon rates and time to maturity. Furthermore, the document explores the impact of tax cuts on the supply and demand for loanable funds using the loanable funds model and explaining the effect on interest rates. The assessment also includes time value of money calculations, comparing investment options from different banks and determining the optimal choice based on compounding frequency. Finally, the document analyzes three contract options for a professional football player, using present value calculations to determine the most financially beneficial contract. The document provides detailed calculations and explanations for each question, offering a complete and well-structured solution to the assessment.

School

Program code BP314

Course/unit name FINANCIAL MARKET

Course/unit code BAFI1002

Name of lecturer/teacher

Name of tutor/marker

Student/s

Family name

Declaration and statement of authorship

1. I/we hold a copy of this work that can be produced if the original is lost/damaged.

2. This work is my/our original work and no part of it has been copied from any other

student’s work or from any other source except where due acknowledgement is made.

3. No part of this work has been written for me/us by any other person except where such

collaboration has been authorised by the lecturer/teacher concerned.

4. I/we have correctly acknowledged the re-use of any of my/our own previously submitted work within

this submission.

5. I/we give permission for this work to be reproduced, communicated, compared and archived for the

purpose of detecting plagiarism.

6. I/we give permission for a copy of my/our marked work to be retained by the school for

review and comparison, including review by external examiners.

I/we understand that:

7. plagiarism is the presentation of the work, idea or creation of another person as though it is

my/our own. It is a form of cheating and is a very serious academic offence that may lead to

exclusion from the University. Plagiarised material can be drawn from, and presented in,

written, graphic and visual form, including electronic data and oral presentations. Plagiarism

occurs when the origin of the material used is not appropriately cited.

8. plagiarism includes the act of assisting or allowing another person to plagiarise or to copy my/our

work.

Student signature/s

I/we declare that I/we have read and understood the declaration and statement of authorship.

1NGUYEN THI THU TAM

Further information relating to the penalties for plagiarism, that range from a notation on your

student file to expulsion from the University, is contained in the Student Conduct Regulation,

Division 2. Academic Misconduct and the Assessment Policy that are available on the Policies

and Procedures website at rmit.edu.au/about/governance-management/policies.

Copies of this form can be downloaded from the student forms webpage at

rmit.edu.au/students/student-essentials/forms/assessment-forms.

Financial Market Assessment 3

Program code BP314

Course/unit name FINANCIAL MARKET

Course/unit code BAFI1002

Name of lecturer/teacher

Name of tutor/marker

Student/s

Family name

Declaration and statement of authorship

1. I/we hold a copy of this work that can be produced if the original is lost/damaged.

2. This work is my/our original work and no part of it has been copied from any other

student’s work or from any other source except where due acknowledgement is made.

3. No part of this work has been written for me/us by any other person except where such

collaboration has been authorised by the lecturer/teacher concerned.

4. I/we have correctly acknowledged the re-use of any of my/our own previously submitted work within

this submission.

5. I/we give permission for this work to be reproduced, communicated, compared and archived for the

purpose of detecting plagiarism.

6. I/we give permission for a copy of my/our marked work to be retained by the school for

review and comparison, including review by external examiners.

I/we understand that:

7. plagiarism is the presentation of the work, idea or creation of another person as though it is

my/our own. It is a form of cheating and is a very serious academic offence that may lead to

exclusion from the University. Plagiarised material can be drawn from, and presented in,

written, graphic and visual form, including electronic data and oral presentations. Plagiarism

occurs when the origin of the material used is not appropriately cited.

8. plagiarism includes the act of assisting or allowing another person to plagiarise or to copy my/our

work.

Student signature/s

I/we declare that I/we have read and understood the declaration and statement of authorship.

1NGUYEN THI THU TAM

Further information relating to the penalties for plagiarism, that range from a notation on your

student file to expulsion from the University, is contained in the Student Conduct Regulation,

Division 2. Academic Misconduct and the Assessment Policy that are available on the Policies

and Procedures website at rmit.edu.au/about/governance-management/policies.

Copies of this form can be downloaded from the student forms webpage at

rmit.edu.au/students/student-essentials/forms/assessment-forms.

Financial Market Assessment 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

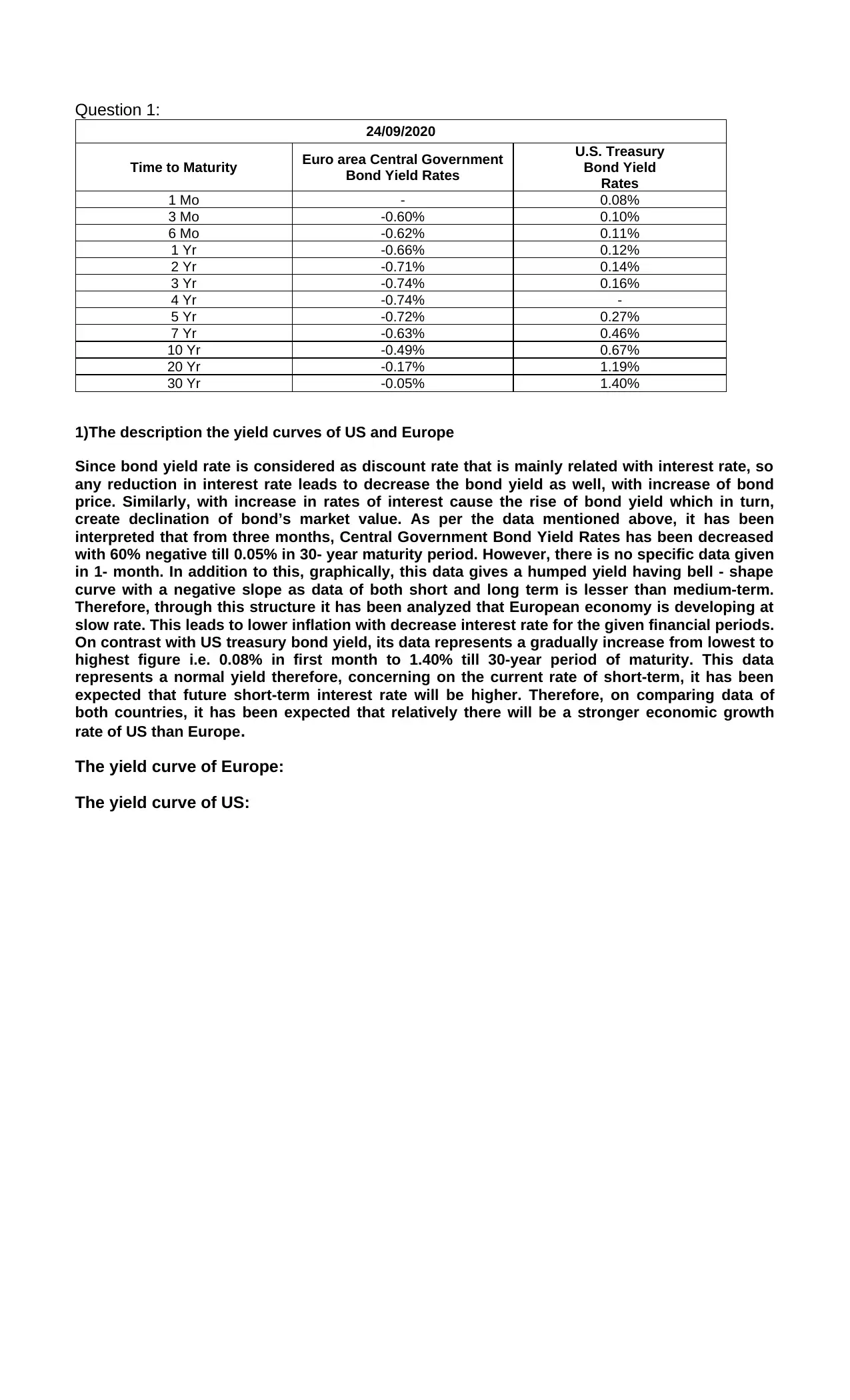

Question 1:

24/09/2020

Time to Maturity Euro area Central Government

Bond Yield Rates

U.S. Treasury

Bond Yield

Rates

1 Mo - 0.08%

3 Mo -0.60% 0.10%

6 Mo -0.62% 0.11%

1 Yr -0.66% 0.12%

2 Yr -0.71% 0.14%

3 Yr -0.74% 0.16%

4 Yr -0.74% -

5 Yr -0.72% 0.27%

7 Yr -0.63% 0.46%

10 Yr -0.49% 0.67%

20 Yr -0.17% 1.19%

30 Yr -0.05% 1.40%

1)The description the yield curves of US and Europe

Since bond yield rate is considered as discount rate that is mainly related with interest rate, so

any reduction in interest rate leads to decrease the bond yield as well, with increase of bond

price. Similarly, with increase in rates of interest cause the rise of bond yield which in turn,

create declination of bond’s market value. As per the data mentioned above, it has been

interpreted that from three months, Central Government Bond Yield Rates has been decreased

with 60% negative till 0.05% in 30- year maturity period. However, there is no specific data given

in 1- month. In addition to this, graphically, this data gives a humped yield having bell - shape

curve with a negative slope as data of both short and long term is lesser than medium-term.

Therefore, through this structure it has been analyzed that European economy is developing at

slow rate. This leads to lower inflation with decrease interest rate for the given financial periods.

On contrast with US treasury bond yield, its data represents a gradually increase from lowest to

highest figure i.e. 0.08% in first month to 1.40% till 30-year period of maturity. This data

represents a normal yield therefore, concerning on the current rate of short-term, it has been

expected that future short-term interest rate will be higher. Therefore, on comparing data of

both countries, it has been expected that relatively there will be a stronger economic growth

rate of US than Europe.

The yield curve of Europe:

The yield curve of US:

24/09/2020

Time to Maturity Euro area Central Government

Bond Yield Rates

U.S. Treasury

Bond Yield

Rates

1 Mo - 0.08%

3 Mo -0.60% 0.10%

6 Mo -0.62% 0.11%

1 Yr -0.66% 0.12%

2 Yr -0.71% 0.14%

3 Yr -0.74% 0.16%

4 Yr -0.74% -

5 Yr -0.72% 0.27%

7 Yr -0.63% 0.46%

10 Yr -0.49% 0.67%

20 Yr -0.17% 1.19%

30 Yr -0.05% 1.40%

1)The description the yield curves of US and Europe

Since bond yield rate is considered as discount rate that is mainly related with interest rate, so

any reduction in interest rate leads to decrease the bond yield as well, with increase of bond

price. Similarly, with increase in rates of interest cause the rise of bond yield which in turn,

create declination of bond’s market value. As per the data mentioned above, it has been

interpreted that from three months, Central Government Bond Yield Rates has been decreased

with 60% negative till 0.05% in 30- year maturity period. However, there is no specific data given

in 1- month. In addition to this, graphically, this data gives a humped yield having bell - shape

curve with a negative slope as data of both short and long term is lesser than medium-term.

Therefore, through this structure it has been analyzed that European economy is developing at

slow rate. This leads to lower inflation with decrease interest rate for the given financial periods.

On contrast with US treasury bond yield, its data represents a gradually increase from lowest to

highest figure i.e. 0.08% in first month to 1.40% till 30-year period of maturity. This data

represents a normal yield therefore, concerning on the current rate of short-term, it has been

expected that future short-term interest rate will be higher. Therefore, on comparing data of

both countries, it has been expected that relatively there will be a stronger economic growth

rate of US than Europe.

The yield curve of Europe:

The yield curve of US:

QUESTION 1 (continued)

1) Calculate the market price of each bond on 24th September 2020 that issued by North Polar

Ltd., a European company specialises in manufacturing semiconductors, using the yield

curve data provided in the table above. What is the current total value of minimum application?

Corporate Bonds Fact Sheet

Issuer North Polar Ltd.

Issuing date 24th September 2020

Bond expiration date 24th September 2025

Face value € 1000 per bond.

Minimum application 50 Bonds (€ 50,000)

Interest rate Floating Interest Rate. The Interest Rate is the sum of the

Market Rate plus the Margin.

Coupon rate (annual) Central Government Bond Yield + 1.86% p.a.

Coupon payment Annually (coupon payment is paid on 10th July every year)

Market Yield 4.5%

[4 marks]

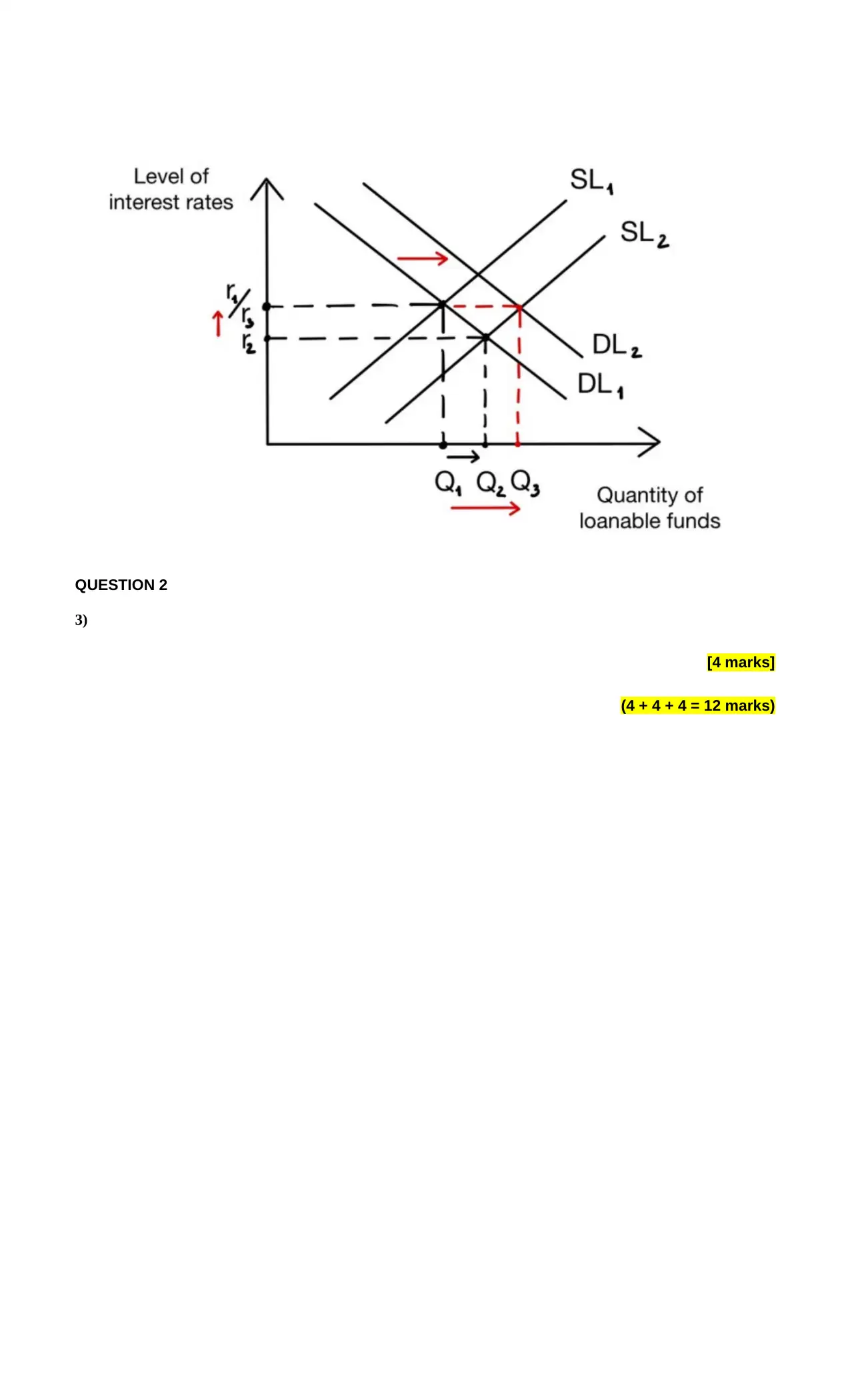

2) Suppose the Australian government has announced tax cuts for the business sector. Using

the loanable funds model, explain how this will impact the supply of and demand for

loanable funds and the interest rate in Australia. (Explain your answer using diagrams).

Coupon rate (annual) = – 0.72% + 1.86% = 1.14%

INT = 1.14% x € 1000 = € 11.4

k_d= 4.5% = 0.045

Bond price = = € 852.50

Current total value of 50 Bonds = € 852.50 x 50 = € 42,624.84 € 42,625

To determine the supply and demand for loanable funds in Australia, interaction between both factors

i.e. supply and demand loanable funds are determined first to evaluate the interest rates. So, using

loanable funds model, level of interest rate could be partially explained.

1) Calculate the market price of each bond on 24th September 2020 that issued by North Polar

Ltd., a European company specialises in manufacturing semiconductors, using the yield

curve data provided in the table above. What is the current total value of minimum application?

Corporate Bonds Fact Sheet

Issuer North Polar Ltd.

Issuing date 24th September 2020

Bond expiration date 24th September 2025

Face value € 1000 per bond.

Minimum application 50 Bonds (€ 50,000)

Interest rate Floating Interest Rate. The Interest Rate is the sum of the

Market Rate plus the Margin.

Coupon rate (annual) Central Government Bond Yield + 1.86% p.a.

Coupon payment Annually (coupon payment is paid on 10th July every year)

Market Yield 4.5%

[4 marks]

2) Suppose the Australian government has announced tax cuts for the business sector. Using

the loanable funds model, explain how this will impact the supply of and demand for

loanable funds and the interest rate in Australia. (Explain your answer using diagrams).

Coupon rate (annual) = – 0.72% + 1.86% = 1.14%

INT = 1.14% x € 1000 = € 11.4

k_d= 4.5% = 0.045

Bond price = = € 852.50

Current total value of 50 Bonds = € 852.50 x 50 = € 42,624.84 € 42,625

To determine the supply and demand for loanable funds in Australia, interaction between both factors

i.e. supply and demand loanable funds are determined first to evaluate the interest rates. So, using

loanable funds model, level of interest rate could be partially explained.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

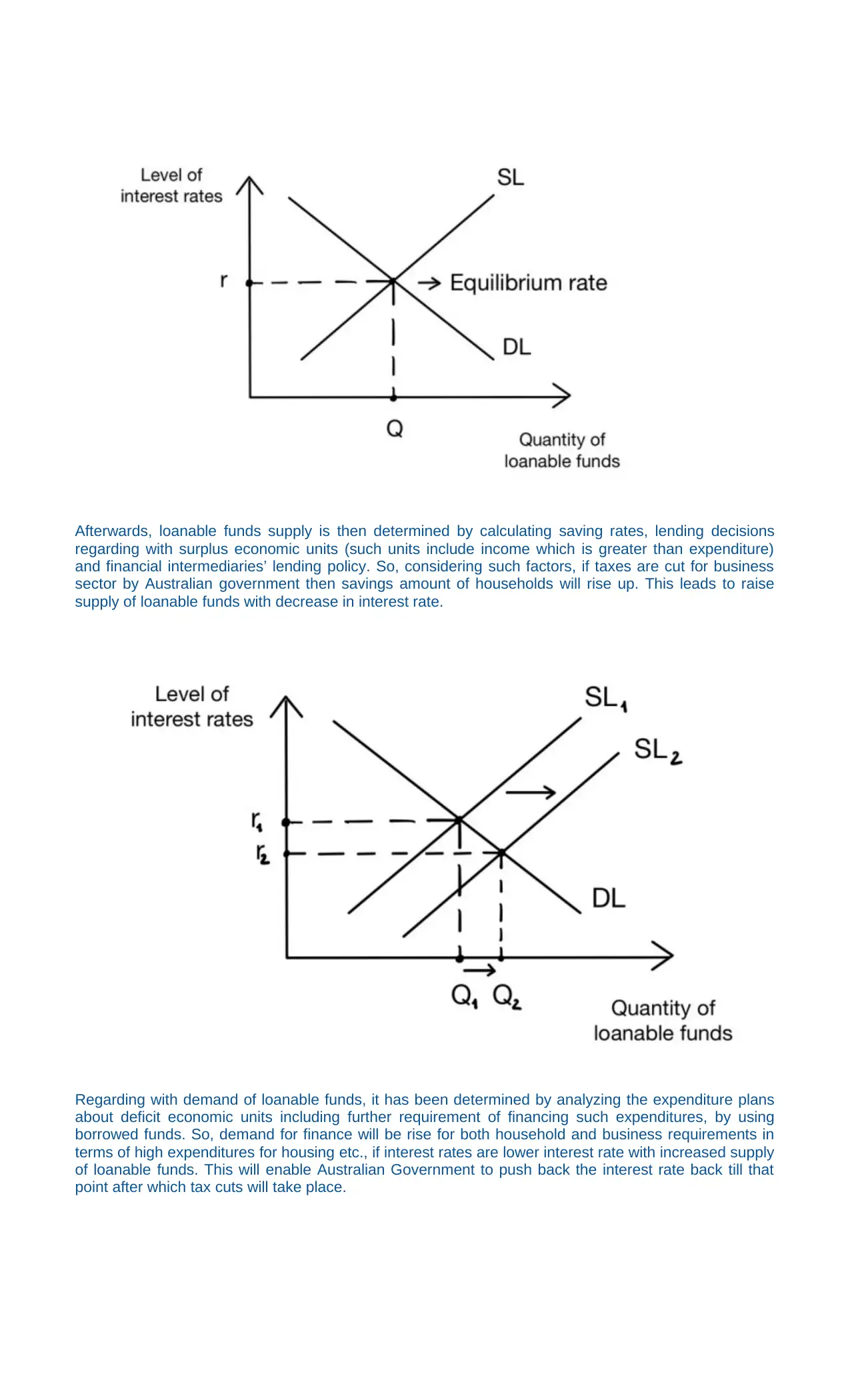

Afterwards, loanable funds supply is then determined by calculating saving rates, lending decisions

regarding with surplus economic units (such units include income which is greater than expenditure)

and financial intermediaries’ lending policy. So, considering such factors, if taxes are cut for business

sector by Australian government then savings amount of households will rise up. This leads to raise

supply of loanable funds with decrease in interest rate.

Regarding with demand of loanable funds, it has been determined by analyzing the expenditure plans

about deficit economic units including further requirement of financing such expenditures, by using

borrowed funds. So, demand for finance will be rise for both household and business requirements in

terms of high expenditures for housing etc., if interest rates are lower interest rate with increased supply

of loanable funds. This will enable Australian Government to push back the interest rate back till that

point after which tax cuts will take place.

regarding with surplus economic units (such units include income which is greater than expenditure)

and financial intermediaries’ lending policy. So, considering such factors, if taxes are cut for business

sector by Australian government then savings amount of households will rise up. This leads to raise

supply of loanable funds with decrease in interest rate.

Regarding with demand of loanable funds, it has been determined by analyzing the expenditure plans

about deficit economic units including further requirement of financing such expenditures, by using

borrowed funds. So, demand for finance will be rise for both household and business requirements in

terms of high expenditures for housing etc., if interest rates are lower interest rate with increased supply

of loanable funds. This will enable Australian Government to push back the interest rate back till that

point after which tax cuts will take place.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

3)

[4 marks]

(4 + 4 + 4 = 12 marks)

3)

[4 marks]

(4 + 4 + 4 = 12 marks)

QUESTION 2

(TIME VALUE OF MONEY)

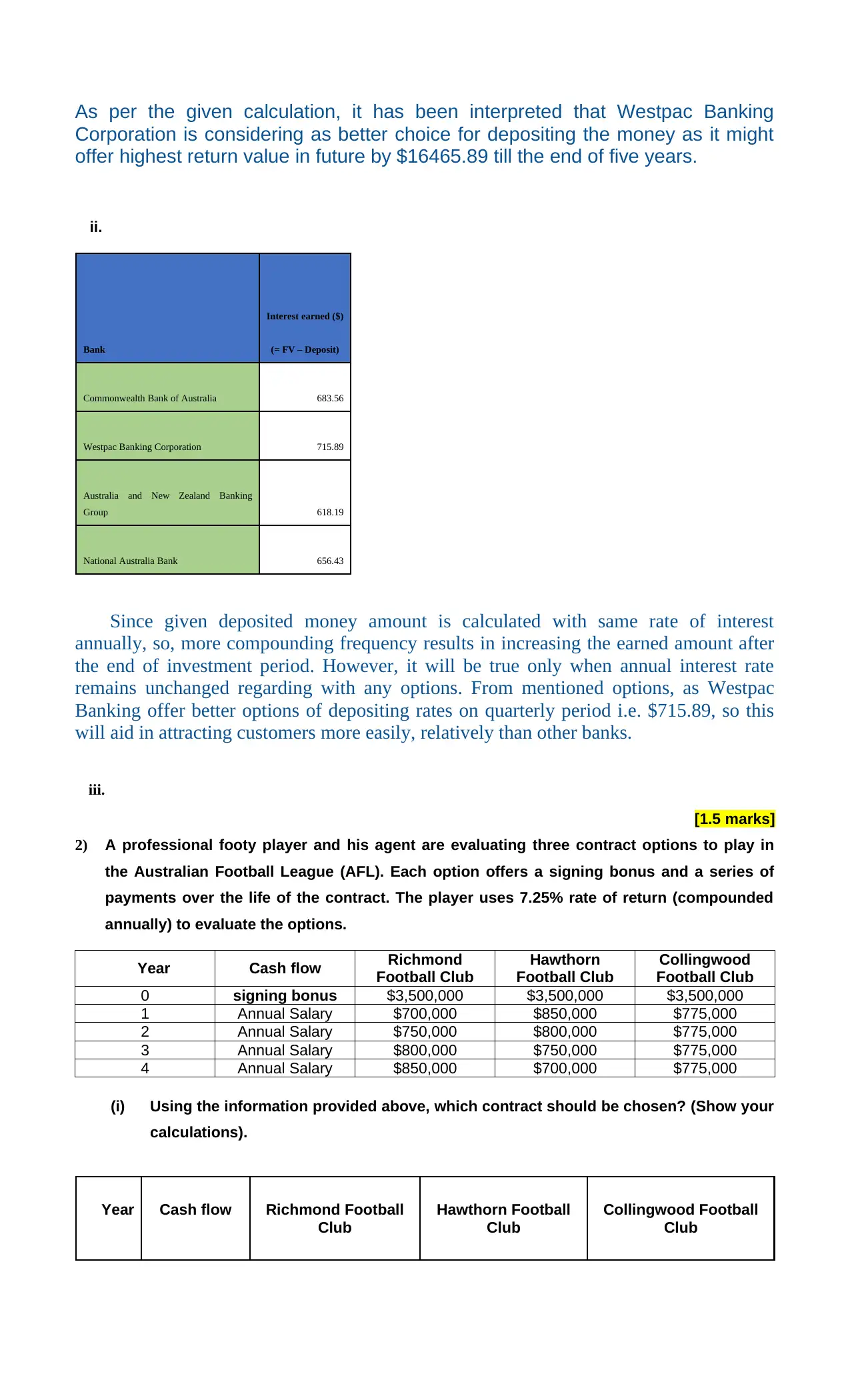

1) You have just received a bonus of $15,750 and are looking to deposit the money in a bank

for 5 years. You have investigated the annual deposit rate of several Australian banks and

collected the following information:

Bank Annual rate Compounding frequency

Commonwealth Bank of Australia 0.85% Monthly

Westpac Banking Corporation 0.89% Quarterly

Australia and New Zealand Banking Group 0.77% Daily

National Australia Bank 0.82% Annually

i. To determine which bank you should deposit your money in, calculate how much money

you will earn at the end of 5 years at each bank. (round your answer to 2 decimal

places).

[4.5 marks]

ii. You understand that the more frequently interest is earned in each year, the more you

will have at the end of your investment horizon. Is this always true? Discuss this

statement considering your answer from the previous part.

Bank

Annual

rate Compounding frequency Future value ($)

Commonwealth Bank of Australia 0.85% 12 16433.56

Westpac Banking Corporation 0.89% 4 16465.89

Australia and New Zealand Banking Group 0.77% 365 16368.19

National Australia Bank 0.82% 1 16406.43

Amount of money to be deposited ($) 15,750

- Commonwealth Bank of Australia

FV = PV x (1 + r) n = 15,750 x (1 + (0.85%/12))60 = $16,433.56

- Westpac Banking Corporation

FV = PV x (1+r) n = 15,750 x (1+(0.89%/4))20 = $16,465.89

- Australia and New Zealand Banking Group

FV = PV x (1+r) n = 15,750 x (1 + (0.77%/365))1825 = $16,368.19

- National Australia Bank

FV = PV x (1+r) n = 15,750 x (1 + 0.82%)5 = $16,406.43

(TIME VALUE OF MONEY)

1) You have just received a bonus of $15,750 and are looking to deposit the money in a bank

for 5 years. You have investigated the annual deposit rate of several Australian banks and

collected the following information:

Bank Annual rate Compounding frequency

Commonwealth Bank of Australia 0.85% Monthly

Westpac Banking Corporation 0.89% Quarterly

Australia and New Zealand Banking Group 0.77% Daily

National Australia Bank 0.82% Annually

i. To determine which bank you should deposit your money in, calculate how much money

you will earn at the end of 5 years at each bank. (round your answer to 2 decimal

places).

[4.5 marks]

ii. You understand that the more frequently interest is earned in each year, the more you

will have at the end of your investment horizon. Is this always true? Discuss this

statement considering your answer from the previous part.

Bank

Annual

rate Compounding frequency Future value ($)

Commonwealth Bank of Australia 0.85% 12 16433.56

Westpac Banking Corporation 0.89% 4 16465.89

Australia and New Zealand Banking Group 0.77% 365 16368.19

National Australia Bank 0.82% 1 16406.43

Amount of money to be deposited ($) 15,750

- Commonwealth Bank of Australia

FV = PV x (1 + r) n = 15,750 x (1 + (0.85%/12))60 = $16,433.56

- Westpac Banking Corporation

FV = PV x (1+r) n = 15,750 x (1+(0.89%/4))20 = $16,465.89

- Australia and New Zealand Banking Group

FV = PV x (1+r) n = 15,750 x (1 + (0.77%/365))1825 = $16,368.19

- National Australia Bank

FV = PV x (1+r) n = 15,750 x (1 + 0.82%)5 = $16,406.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the given calculation, it has been interpreted that Westpac Banking

Corporation is considering as better choice for depositing the money as it might

offer highest return value in future by $16465.89 till the end of five years.

ii.

Bank

Interest earned ($)

(= FV – Deposit)

Commonwealth Bank of Australia 683.56

Westpac Banking Corporation 715.89

Australia and New Zealand Banking

Group 618.19

National Australia Bank 656.43

Since given deposited money amount is calculated with same rate of interest

annually, so, more compounding frequency results in increasing the earned amount after

the end of investment period. However, it will be true only when annual interest rate

remains unchanged regarding with any options. From mentioned options, as Westpac

Banking offer better options of depositing rates on quarterly period i.e. $715.89, so this

will aid in attracting customers more easily, relatively than other banks.

iii.

[1.5 marks]

2) A professional footy player and his agent are evaluating three contract options to play in

the Australian Football League (AFL). Each option offers a signing bonus and a series of

payments over the life of the contract. The player uses 7.25% rate of return (compounded

annually) to evaluate the options.

Year Cash flow Richmond

Football Club

Hawthorn

Football Club

Collingwood

Football Club

0 signing bonus $3,500,000 $3,500,000 $3,500,000

1 Annual Salary $700,000 $850,000 $775,000

2 Annual Salary $750,000 $800,000 $775,000

3 Annual Salary $800,000 $750,000 $775,000

4 Annual Salary $850,000 $700,000 $775,000

(i) Using the information provided above, which contract should be chosen? (Show your

calculations).

Year Cash flow Richmond Football

Club

Hawthorn Football

Club

Collingwood Football

Club

Corporation is considering as better choice for depositing the money as it might

offer highest return value in future by $16465.89 till the end of five years.

ii.

Bank

Interest earned ($)

(= FV – Deposit)

Commonwealth Bank of Australia 683.56

Westpac Banking Corporation 715.89

Australia and New Zealand Banking

Group 618.19

National Australia Bank 656.43

Since given deposited money amount is calculated with same rate of interest

annually, so, more compounding frequency results in increasing the earned amount after

the end of investment period. However, it will be true only when annual interest rate

remains unchanged regarding with any options. From mentioned options, as Westpac

Banking offer better options of depositing rates on quarterly period i.e. $715.89, so this

will aid in attracting customers more easily, relatively than other banks.

iii.

[1.5 marks]

2) A professional footy player and his agent are evaluating three contract options to play in

the Australian Football League (AFL). Each option offers a signing bonus and a series of

payments over the life of the contract. The player uses 7.25% rate of return (compounded

annually) to evaluate the options.

Year Cash flow Richmond

Football Club

Hawthorn

Football Club

Collingwood

Football Club

0 signing bonus $3,500,000 $3,500,000 $3,500,000

1 Annual Salary $700,000 $850,000 $775,000

2 Annual Salary $750,000 $800,000 $775,000

3 Annual Salary $800,000 $750,000 $775,000

4 Annual Salary $850,000 $700,000 $775,000

(i) Using the information provided above, which contract should be chosen? (Show your

calculations).

Year Cash flow Richmond Football

Club

Hawthorn Football

Club

Collingwood Football

Club

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0 signing

bonus

$3,500,000 $3,500,000 $3,500,000

1 Annual

Salary

$700,000 $850,000 $775,000

2 Annual

Salary

$750,000 $800,000 $775,000

3 Annual

Salary

$800,000 $750,000 $775,000

4 Annual

Salary

$850,000 $700,000 $775,000

(i)

Richmond Football Club:

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 700,000 x (1+7.25%)-1 = $652,680.65

Year 2: PV2 = FV2(1+r)-n = 750,000 x (1+7.25%)-2 = $652,028.62

Year 3: PV3 = FV3(1+r)-n = 800,000 x (1+7.25%)-3 = $648,482.24

Year 4: PV4 = FV4(1+r)-n = 850,000 x (1+7.25%)-4 = $642,435.78

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 652,680.65 + 652,028.62 + 648,482.24 + 642,435.78

= $6,095,627.29

Hawthorn Football Club

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 850,000 x (1+7.25%)-1 = $792,540.79

Year 2: PV2 = FV2(1+r)-n = 800,000 x (1+7.25%)-2 = $695,497.2

Year 3: PV3 = FV3(1+r)-n = 750,000 x (1+7.25%)-3 = $607,952.1

Year 4: PV4 = FV4(1+r)-n = 700,000 x (1+7.25%)-4 = $529,064.76

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 792,540.79 + 695,497.2 + 607,952.1 + 529,064.76

= $6,125,054.85

bonus

$3,500,000 $3,500,000 $3,500,000

1 Annual

Salary

$700,000 $850,000 $775,000

2 Annual

Salary

$750,000 $800,000 $775,000

3 Annual

Salary

$800,000 $750,000 $775,000

4 Annual

Salary

$850,000 $700,000 $775,000

(i)

Richmond Football Club:

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 700,000 x (1+7.25%)-1 = $652,680.65

Year 2: PV2 = FV2(1+r)-n = 750,000 x (1+7.25%)-2 = $652,028.62

Year 3: PV3 = FV3(1+r)-n = 800,000 x (1+7.25%)-3 = $648,482.24

Year 4: PV4 = FV4(1+r)-n = 850,000 x (1+7.25%)-4 = $642,435.78

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 652,680.65 + 652,028.62 + 648,482.24 + 642,435.78

= $6,095,627.29

Hawthorn Football Club

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 850,000 x (1+7.25%)-1 = $792,540.79

Year 2: PV2 = FV2(1+r)-n = 800,000 x (1+7.25%)-2 = $695,497.2

Year 3: PV3 = FV3(1+r)-n = 750,000 x (1+7.25%)-3 = $607,952.1

Year 4: PV4 = FV4(1+r)-n = 700,000 x (1+7.25%)-4 = $529,064.76

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 792,540.79 + 695,497.2 + 607,952.1 + 529,064.76

= $6,125,054.85

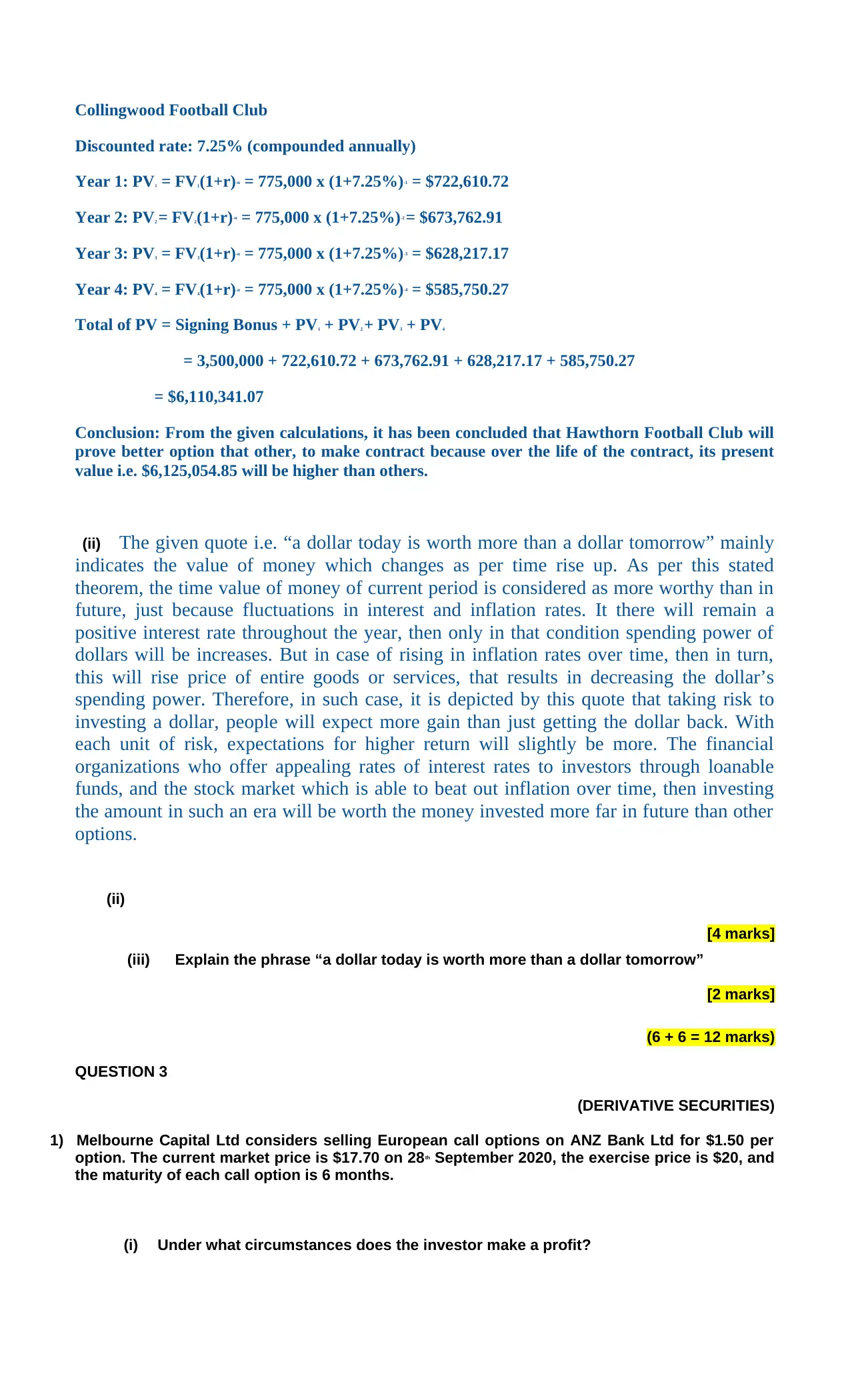

Collingwood Football Club

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 775,000 x (1+7.25%)-1 = $722,610.72

Year 2: PV2 = FV2(1+r)-n = 775,000 x (1+7.25%)-2 = $673,762.91

Year 3: PV3 = FV3(1+r)-n = 775,000 x (1+7.25%)-3 = $628,217.17

Year 4: PV4 = FV4(1+r)-n = 775,000 x (1+7.25%)-4 = $585,750.27

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 722,610.72 + 673,762.91 + 628,217.17 + 585,750.27

= $6,110,341.07

Conclusion: From the given calculations, it has been concluded that Hawthorn Football Club will

prove better option that other, to make contract because over the life of the contract, its present

value i.e. $6,125,054.85 will be higher than others.

(ii) The given quote i.e. “a dollar today is worth more than a dollar tomorrow” mainly

indicates the value of money which changes as per time rise up. As per this stated

theorem, the time value of money of current period is considered as more worthy than in

future, just because fluctuations in interest and inflation rates. It there will remain a

positive interest rate throughout the year, then only in that condition spending power of

dollars will be increases. But in case of rising in inflation rates over time, then in turn,

this will rise price of entire goods or services, that results in decreasing the dollar’s

spending power. Therefore, in such case, it is depicted by this quote that taking risk to

investing a dollar, people will expect more gain than just getting the dollar back. With

each unit of risk, expectations for higher return will slightly be more. The financial

organizations who offer appealing rates of interest rates to investors through loanable

funds, and the stock market which is able to beat out inflation over time, then investing

the amount in such an era will be worth the money invested more far in future than other

options.

(ii)

[4 marks]

(iii) Explain the phrase “a dollar today is worth more than a dollar tomorrow”

[2 marks]

(6 + 6 = 12 marks)

QUESTION 3

(DERIVATIVE SECURITIES)

1) Melbourne Capital Ltd considers selling European call options on ANZ Bank Ltd for $1.50 per

option. The current market price is $17.70 on 28th September 2020, the exercise price is $20, and

the maturity of each call option is 6 months.

(i) Under what circumstances does the investor make a profit?

Discounted rate: 7.25% (compounded annually)

Year 1: PV1 = FV1(1+r)-n = 775,000 x (1+7.25%)-1 = $722,610.72

Year 2: PV2 = FV2(1+r)-n = 775,000 x (1+7.25%)-2 = $673,762.91

Year 3: PV3 = FV3(1+r)-n = 775,000 x (1+7.25%)-3 = $628,217.17

Year 4: PV4 = FV4(1+r)-n = 775,000 x (1+7.25%)-4 = $585,750.27

Total of PV = Signing Bonus + PV1 + PV2 + PV3 + PV4

= 3,500,000 + 722,610.72 + 673,762.91 + 628,217.17 + 585,750.27

= $6,110,341.07

Conclusion: From the given calculations, it has been concluded that Hawthorn Football Club will

prove better option that other, to make contract because over the life of the contract, its present

value i.e. $6,125,054.85 will be higher than others.

(ii) The given quote i.e. “a dollar today is worth more than a dollar tomorrow” mainly

indicates the value of money which changes as per time rise up. As per this stated

theorem, the time value of money of current period is considered as more worthy than in

future, just because fluctuations in interest and inflation rates. It there will remain a

positive interest rate throughout the year, then only in that condition spending power of

dollars will be increases. But in case of rising in inflation rates over time, then in turn,

this will rise price of entire goods or services, that results in decreasing the dollar’s

spending power. Therefore, in such case, it is depicted by this quote that taking risk to

investing a dollar, people will expect more gain than just getting the dollar back. With

each unit of risk, expectations for higher return will slightly be more. The financial

organizations who offer appealing rates of interest rates to investors through loanable

funds, and the stock market which is able to beat out inflation over time, then investing

the amount in such an era will be worth the money invested more far in future than other

options.

(ii)

[4 marks]

(iii) Explain the phrase “a dollar today is worth more than a dollar tomorrow”

[2 marks]

(6 + 6 = 12 marks)

QUESTION 3

(DERIVATIVE SECURITIES)

1) Melbourne Capital Ltd considers selling European call options on ANZ Bank Ltd for $1.50 per

option. The current market price is $17.70 on 28th September 2020, the exercise price is $20, and

the maturity of each call option is 6 months.

(i) Under what circumstances does the investor make a profit?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

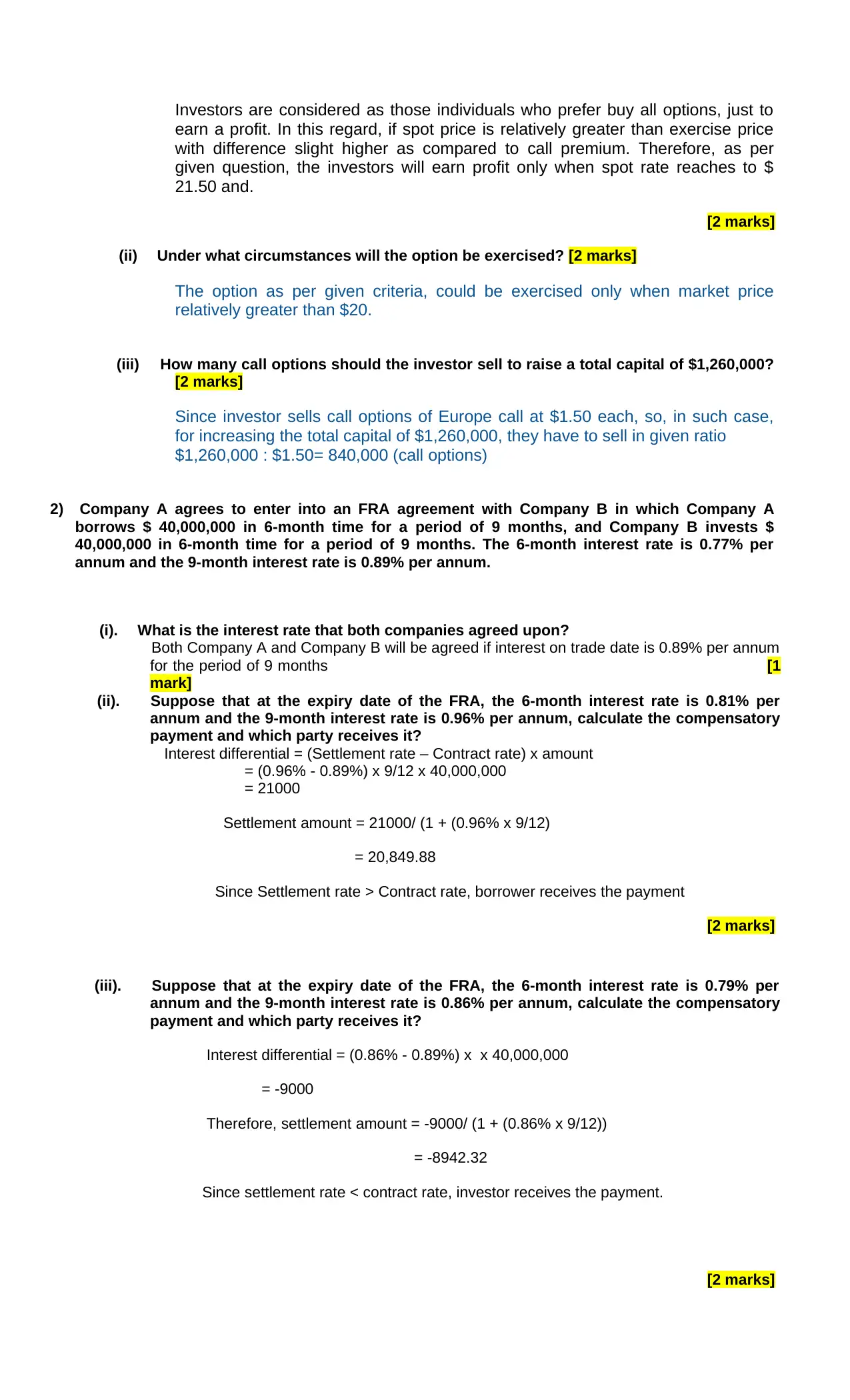

Investors are considered as those individuals who prefer buy all options, just to

earn a profit. In this regard, if spot price is relatively greater than exercise price

with difference slight higher as compared to call premium. Therefore, as per

given question, the investors will earn profit only when spot rate reaches to $

21.50 and.

[2 marks]

(ii) Under what circumstances will the option be exercised? [2 marks]

The option as per given criteria, could be exercised only when market price

relatively greater than $20.

(iii) How many call options should the investor sell to raise a total capital of $1,260,000?

[2 marks]

Since investor sells call options of Europe call at $1.50 each, so, in such case,

for increasing the total capital of $1,260,000, they have to sell in given ratio

$1,260,000 : $1.50= 840,000 (call options)

2) Company A agrees to enter into an FRA agreement with Company B in which Company A

borrows $ 40,000,000 in 6-month time for a period of 9 months, and Company B invests $

40,000,000 in 6-month time for a period of 9 months. The 6-month interest rate is 0.77% per

annum and the 9-month interest rate is 0.89% per annum.

(i). What is the interest rate that both companies agreed upon?

Both Company A and Company B will be agreed if interest on trade date is 0.89% per annum

for the period of 9 months [1

mark]

(ii). Suppose that at the expiry date of the FRA, the 6-month interest rate is 0.81% per

annum and the 9-month interest rate is 0.96% per annum, calculate the compensatory

payment and which party receives it?

Interest differential = (Settlement rate – Contract rate) x amount

= (0.96% - 0.89%) x 9/12 x 40,000,000

= 21000

Settlement amount = 21000/ (1 + (0.96% x 9/12)

= 20,849.88

Since Settlement rate > Contract rate, borrower receives the payment

[2 marks]

(iii). Suppose that at the expiry date of the FRA, the 6-month interest rate is 0.79% per

annum and the 9-month interest rate is 0.86% per annum, calculate the compensatory

payment and which party receives it?

Interest differential = (0.86% - 0.89%) x x 40,000,000

= -9000

Therefore, settlement amount = -9000/ (1 + (0.86% x 9/12))

= -8942.32

Since settlement rate < contract rate, investor receives the payment.

[2 marks]

earn a profit. In this regard, if spot price is relatively greater than exercise price

with difference slight higher as compared to call premium. Therefore, as per

given question, the investors will earn profit only when spot rate reaches to $

21.50 and.

[2 marks]

(ii) Under what circumstances will the option be exercised? [2 marks]

The option as per given criteria, could be exercised only when market price

relatively greater than $20.

(iii) How many call options should the investor sell to raise a total capital of $1,260,000?

[2 marks]

Since investor sells call options of Europe call at $1.50 each, so, in such case,

for increasing the total capital of $1,260,000, they have to sell in given ratio

$1,260,000 : $1.50= 840,000 (call options)

2) Company A agrees to enter into an FRA agreement with Company B in which Company A

borrows $ 40,000,000 in 6-month time for a period of 9 months, and Company B invests $

40,000,000 in 6-month time for a period of 9 months. The 6-month interest rate is 0.77% per

annum and the 9-month interest rate is 0.89% per annum.

(i). What is the interest rate that both companies agreed upon?

Both Company A and Company B will be agreed if interest on trade date is 0.89% per annum

for the period of 9 months [1

mark]

(ii). Suppose that at the expiry date of the FRA, the 6-month interest rate is 0.81% per

annum and the 9-month interest rate is 0.96% per annum, calculate the compensatory

payment and which party receives it?

Interest differential = (Settlement rate – Contract rate) x amount

= (0.96% - 0.89%) x 9/12 x 40,000,000

= 21000

Settlement amount = 21000/ (1 + (0.96% x 9/12)

= 20,849.88

Since Settlement rate > Contract rate, borrower receives the payment

[2 marks]

(iii). Suppose that at the expiry date of the FRA, the 6-month interest rate is 0.79% per

annum and the 9-month interest rate is 0.86% per annum, calculate the compensatory

payment and which party receives it?

Interest differential = (0.86% - 0.89%) x x 40,000,000

= -9000

Therefore, settlement amount = -9000/ (1 + (0.86% x 9/12))

= -8942.32

Since settlement rate < contract rate, investor receives the payment.

[2 marks]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

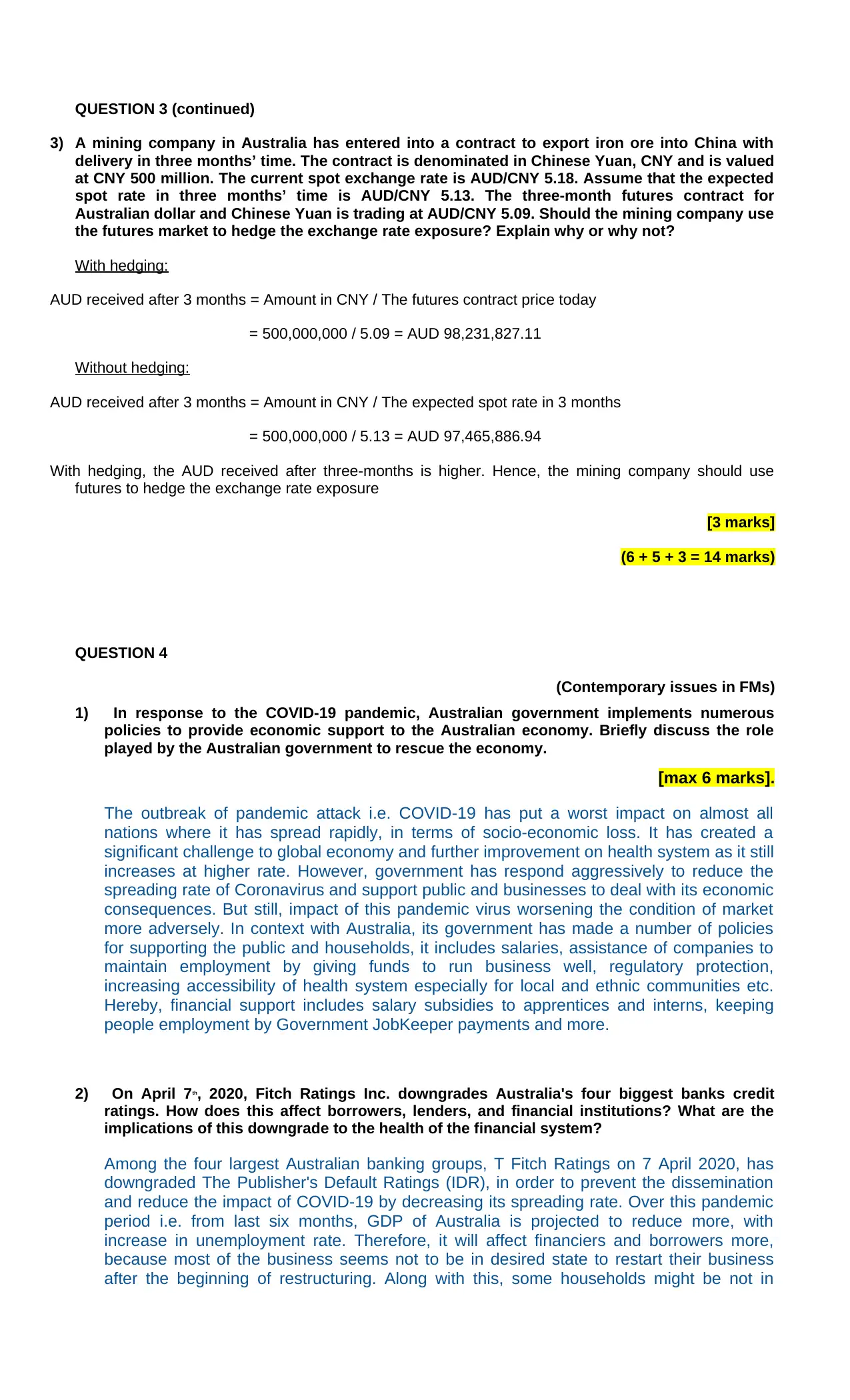

QUESTION 3 (continued)

3) A mining company in Australia has entered into a contract to export iron ore into China with

delivery in three months’ time. The contract is denominated in Chinese Yuan, CNY and is valued

at CNY 500 million. The current spot exchange rate is AUD/CNY 5.18. Assume that the expected

spot rate in three months’ time is AUD/CNY 5.13. The three-month futures contract for

Australian dollar and Chinese Yuan is trading at AUD/CNY 5.09. Should the mining company use

the futures market to hedge the exchange rate exposure? Explain why or why not?

With hedging:

AUD received after 3 months = Amount in CNY / The futures contract price today

= 500,000,000 / 5.09 = AUD 98,231,827.11

Without hedging:

AUD received after 3 months = Amount in CNY / The expected spot rate in 3 months

= 500,000,000 / 5.13 = AUD 97,465,886.94

With hedging, the AUD received after three-months is higher. Hence, the mining company should use

futures to hedge the exchange rate exposure

[3 marks]

(6 + 5 + 3 = 14 marks)

QUESTION 4

(Contemporary issues in FMs)

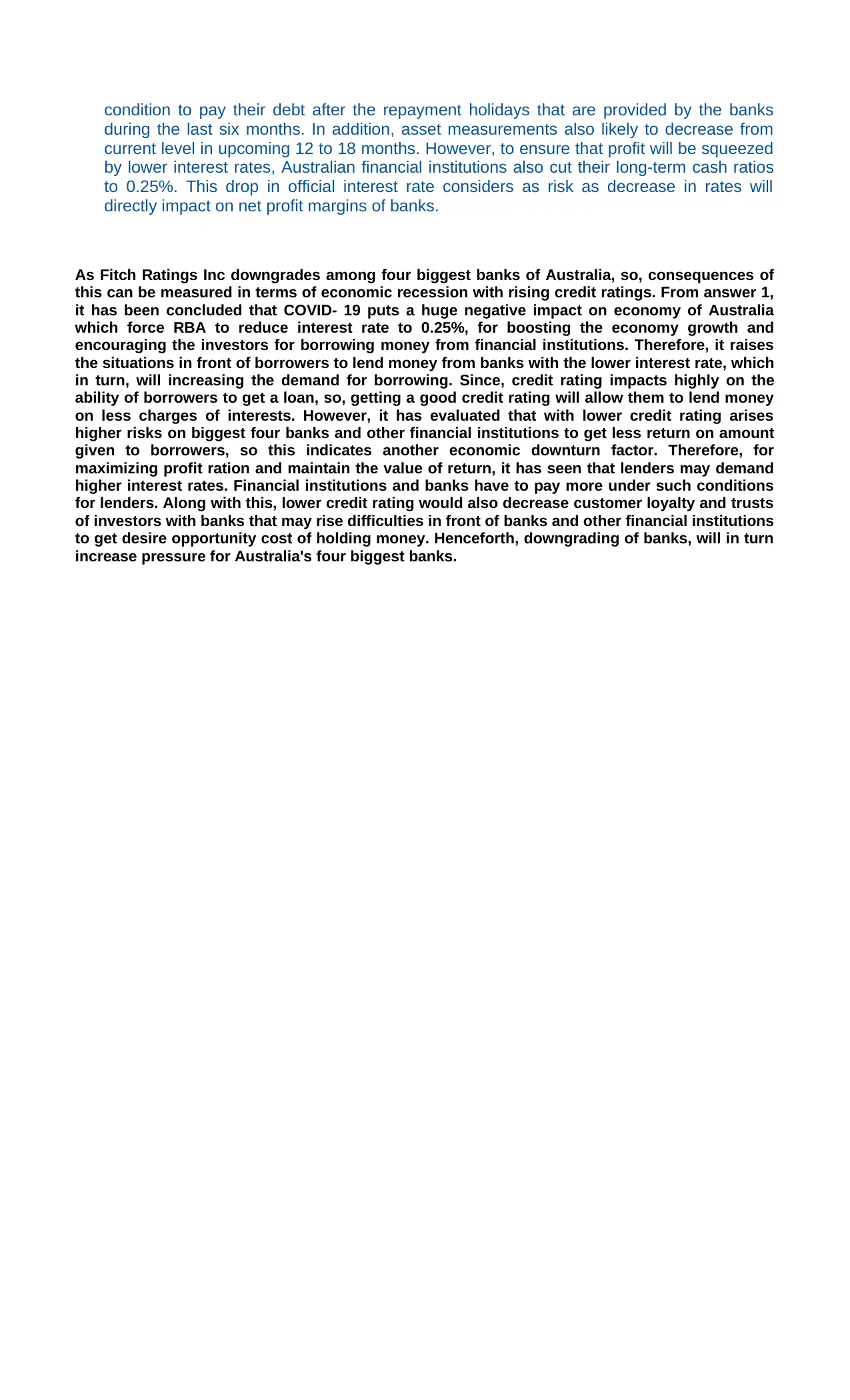

1) In response to the COVID-19 pandemic, Australian government implements numerous

policies to provide economic support to the Australian economy. Briefly discuss the role

played by the Australian government to rescue the economy.

[max 6 marks].

The outbreak of pandemic attack i.e. COVID-19 has put a worst impact on almost all

nations where it has spread rapidly, in terms of socio-economic loss. It has created a

significant challenge to global economy and further improvement on health system as it still

increases at higher rate. However, government has respond aggressively to reduce the

spreading rate of Coronavirus and support public and businesses to deal with its economic

consequences. But still, impact of this pandemic virus worsening the condition of market

more adversely. In context with Australia, its government has made a number of policies

for supporting the public and households, it includes salaries, assistance of companies to

maintain employment by giving funds to run business well, regulatory protection,

increasing accessibility of health system especially for local and ethnic communities etc.

Hereby, financial support includes salary subsidies to apprentices and interns, keeping

people employment by Government JobKeeper payments and more.

2) On April 7th, 2020, Fitch Ratings Inc. downgrades Australia's four biggest banks credit

ratings. How does this affect borrowers, lenders, and financial institutions? What are the

implications of this downgrade to the health of the financial system?

Among the four largest Australian banking groups, T Fitch Ratings on 7 April 2020, has

downgraded The Publisher's Default Ratings (IDR), in order to prevent the dissemination

and reduce the impact of COVID-19 by decreasing its spreading rate. Over this pandemic

period i.e. from last six months, GDP of Australia is projected to reduce more, with

increase in unemployment rate. Therefore, it will affect financiers and borrowers more,

because most of the business seems not to be in desired state to restart their business

after the beginning of restructuring. Along with this, some households might be not in

3) A mining company in Australia has entered into a contract to export iron ore into China with

delivery in three months’ time. The contract is denominated in Chinese Yuan, CNY and is valued

at CNY 500 million. The current spot exchange rate is AUD/CNY 5.18. Assume that the expected

spot rate in three months’ time is AUD/CNY 5.13. The three-month futures contract for

Australian dollar and Chinese Yuan is trading at AUD/CNY 5.09. Should the mining company use

the futures market to hedge the exchange rate exposure? Explain why or why not?

With hedging:

AUD received after 3 months = Amount in CNY / The futures contract price today

= 500,000,000 / 5.09 = AUD 98,231,827.11

Without hedging:

AUD received after 3 months = Amount in CNY / The expected spot rate in 3 months

= 500,000,000 / 5.13 = AUD 97,465,886.94

With hedging, the AUD received after three-months is higher. Hence, the mining company should use

futures to hedge the exchange rate exposure

[3 marks]

(6 + 5 + 3 = 14 marks)

QUESTION 4

(Contemporary issues in FMs)

1) In response to the COVID-19 pandemic, Australian government implements numerous

policies to provide economic support to the Australian economy. Briefly discuss the role

played by the Australian government to rescue the economy.

[max 6 marks].

The outbreak of pandemic attack i.e. COVID-19 has put a worst impact on almost all

nations where it has spread rapidly, in terms of socio-economic loss. It has created a

significant challenge to global economy and further improvement on health system as it still

increases at higher rate. However, government has respond aggressively to reduce the

spreading rate of Coronavirus and support public and businesses to deal with its economic

consequences. But still, impact of this pandemic virus worsening the condition of market

more adversely. In context with Australia, its government has made a number of policies

for supporting the public and households, it includes salaries, assistance of companies to

maintain employment by giving funds to run business well, regulatory protection,

increasing accessibility of health system especially for local and ethnic communities etc.

Hereby, financial support includes salary subsidies to apprentices and interns, keeping

people employment by Government JobKeeper payments and more.

2) On April 7th, 2020, Fitch Ratings Inc. downgrades Australia's four biggest banks credit

ratings. How does this affect borrowers, lenders, and financial institutions? What are the

implications of this downgrade to the health of the financial system?

Among the four largest Australian banking groups, T Fitch Ratings on 7 April 2020, has

downgraded The Publisher's Default Ratings (IDR), in order to prevent the dissemination

and reduce the impact of COVID-19 by decreasing its spreading rate. Over this pandemic

period i.e. from last six months, GDP of Australia is projected to reduce more, with

increase in unemployment rate. Therefore, it will affect financiers and borrowers more,

because most of the business seems not to be in desired state to restart their business

after the beginning of restructuring. Along with this, some households might be not in

condition to pay their debt after the repayment holidays that are provided by the banks

during the last six months. In addition, asset measurements also likely to decrease from

current level in upcoming 12 to 18 months. However, to ensure that profit will be squeezed

by lower interest rates, Australian financial institutions also cut their long-term cash ratios

to 0.25%. This drop in official interest rate considers as risk as decrease in rates will

directly impact on net profit margins of banks.

As Fitch Ratings Inc downgrades among four biggest banks of Australia, so, consequences of

this can be measured in terms of economic recession with rising credit ratings. From answer 1,

it has been concluded that COVID- 19 puts a huge negative impact on economy of Australia

which force RBA to reduce interest rate to 0.25%, for boosting the economy growth and

encouraging the investors for borrowing money from financial institutions. Therefore, it raises

the situations in front of borrowers to lend money from banks with the lower interest rate, which

in turn, will increasing the demand for borrowing. Since, credit rating impacts highly on the

ability of borrowers to get a loan, so, getting a good credit rating will allow them to lend money

on less charges of interests. However, it has evaluated that with lower credit rating arises

higher risks on biggest four banks and other financial institutions to get less return on amount

given to borrowers, so this indicates another economic downturn factor. Therefore, for

maximizing profit ration and maintain the value of return, it has seen that lenders may demand

higher interest rates. Financial institutions and banks have to pay more under such conditions

for lenders. Along with this, lower credit rating would also decrease customer loyalty and trusts

of investors with banks that may rise difficulties in front of banks and other financial institutions

to get desire opportunity cost of holding money. Henceforth, downgrading of banks, will in turn

increase pressure for Australia's four biggest banks.

during the last six months. In addition, asset measurements also likely to decrease from

current level in upcoming 12 to 18 months. However, to ensure that profit will be squeezed

by lower interest rates, Australian financial institutions also cut their long-term cash ratios

to 0.25%. This drop in official interest rate considers as risk as decrease in rates will

directly impact on net profit margins of banks.

As Fitch Ratings Inc downgrades among four biggest banks of Australia, so, consequences of

this can be measured in terms of economic recession with rising credit ratings. From answer 1,

it has been concluded that COVID- 19 puts a huge negative impact on economy of Australia

which force RBA to reduce interest rate to 0.25%, for boosting the economy growth and

encouraging the investors for borrowing money from financial institutions. Therefore, it raises

the situations in front of borrowers to lend money from banks with the lower interest rate, which

in turn, will increasing the demand for borrowing. Since, credit rating impacts highly on the

ability of borrowers to get a loan, so, getting a good credit rating will allow them to lend money

on less charges of interests. However, it has evaluated that with lower credit rating arises

higher risks on biggest four banks and other financial institutions to get less return on amount

given to borrowers, so this indicates another economic downturn factor. Therefore, for

maximizing profit ration and maintain the value of return, it has seen that lenders may demand

higher interest rates. Financial institutions and banks have to pay more under such conditions

for lenders. Along with this, lower credit rating would also decrease customer loyalty and trusts

of investors with banks that may rise difficulties in front of banks and other financial institutions

to get desire opportunity cost of holding money. Henceforth, downgrading of banks, will in turn

increase pressure for Australia's four biggest banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.