Financial Markets and Institutions Report: Hedging and Swap Analysis

VerifiedAdded on 2022/09/21

|6

|494

|22

Report

AI Summary

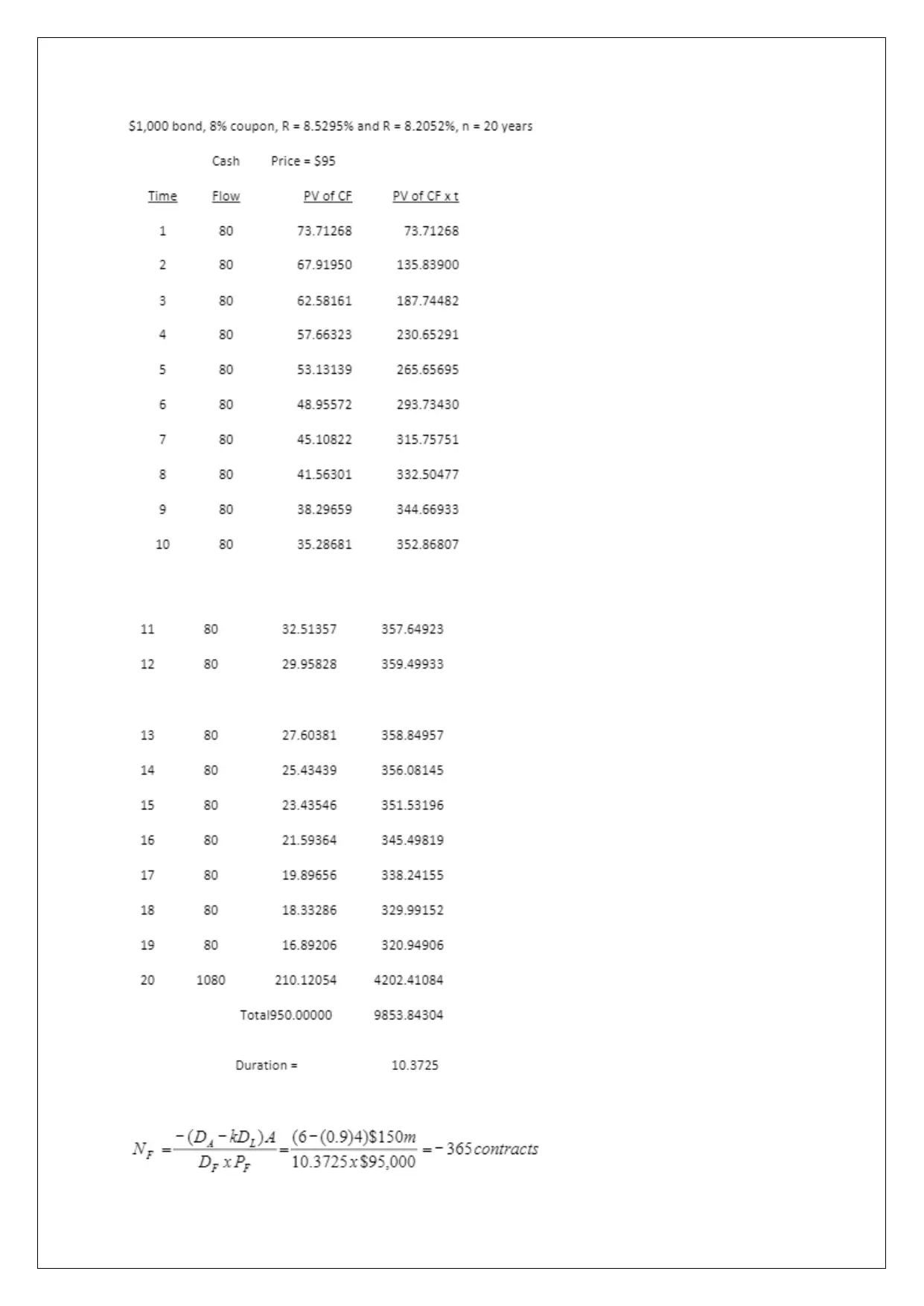

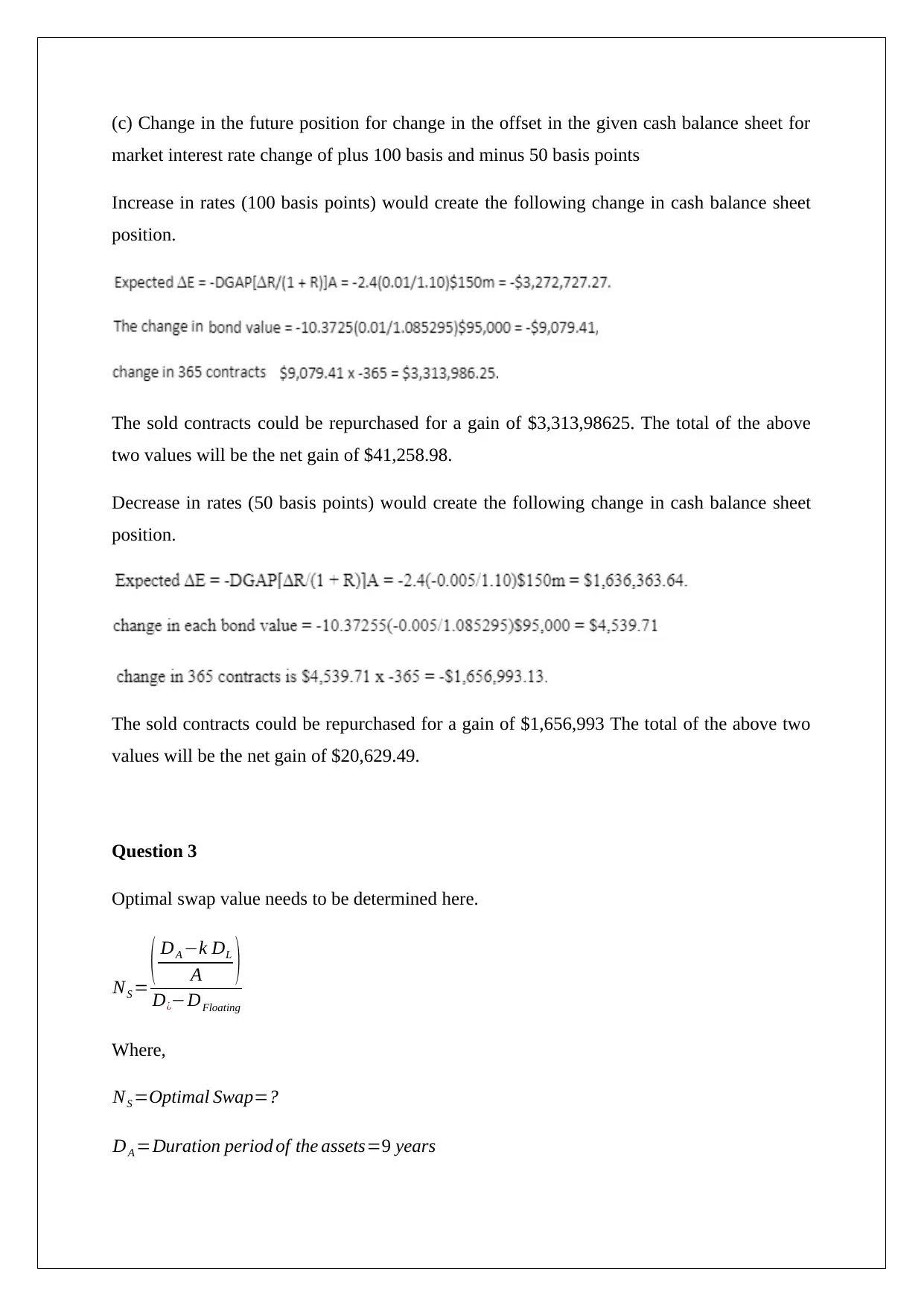

This report addresses a financial markets and institutions assignment focusing on risk management strategies for an Asian bank in response to rising interest rates. The solution analyzes the potential impact of interest rate changes on existing borrowers and bond holdings, proposing adjustments to lending norms and bond portfolio management. It also covers hedging strategies using futures contracts, determining whether to go short or long, and calculating the number of contracts needed for a macro hedge. The report includes detailed calculations to verify how changes in the futures position offset the changes in the cash balance sheet. Finally, the optimal swap value is determined, providing a comprehensive analysis of the financial instruments and strategies involved.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.