Financial Markets and Monetary Policy: UK Economic Analysis Report

VerifiedAdded on 2021/06/15

|13

|3241

|29

Report

AI Summary

This report provides an in-depth analysis of financial markets and monetary policy within the United Kingdom. It begins with an examination of the loanable funds doctrine, exploring how factors such as economic development, inflation, and government spending influence the demand and supply of loanable funds. The report then delves into the impacts of fixed versus floating exchange rate systems on the UK economy, considering the advantages and disadvantages of each. Furthermore, it assesses the relationship between interest rates and exchange rates, explaining how changes in UK interest rates can affect capital flows and the value of the pound. The report also includes graphical representations to illustrate key concepts, providing a comprehensive overview of the UK's financial landscape and the implications of various monetary policy decisions.

Running head: FINANCIAL MARKETS AND MONETARY POLICY

Financial markets and monetary policy

Name of the student:

Name of the University:

Author note

Financial markets and monetary policy

Name of the student:

Name of the University:

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MARKETS AND MONETARY POLICY

Table of Contents

Answer 1:.............................................................................................................................................2

Answer 2:.............................................................................................................................................5

Answer 3:.............................................................................................................................................8

Reference:..........................................................................................................................................11

Table of Contents

Answer 1:.............................................................................................................................................2

Answer 2:.............................................................................................................................................5

Answer 3:.............................................................................................................................................8

Reference:..........................................................................................................................................11

2FINANCIAL MARKETS AND MONETARY POLICY

Answer 1:

Loanable fund doctrine is an economic theory of the market interest rate which can be

explained through the demand and supply framework of loanable fund (Taylor 2016). By the

term loanable fund different form of credit, loans, savings deposits and bonds are meant.

Back in 1930, the loan able fund doctrine was established, which was the extension of the

classical theory that determined the interest rate by investment and savings as per the theory,

total amount of the credit that an economy possess can be exceed private savings due to the

fact that banking system may be such a position where it can create credit out of the thin air

(Jakab and Kumhof 2015). UK, under this scenario market equilibrium of loanable fund is

not only influenced by the propensity to save or invest rather it is also influenced by the fiat

credit and money as well.

From this perspective it can be said that different components impact demand and

supply of loanable belongings. According to the given scenario, it's far required to observe

that whether or not monetary development, swelling, government consumption, the supply of

loanable fund and reserve funds of a household have any effect on demand and supply of this

property or now not. Interest for loanable subsidizes basically originates from one-of-a-kind

aspects, for example, mission, storing and dissaving’s. On the other facet, the supply of

loanable funds originate from investment price range, bank cash rate, dishoarding and

disinvestment (Nyambura 2014).

Given situation:

The given situation has expressed that in the UK monetary development has stayed

high throughout the preceding years however in next 365 days from now this price may

additionally grow to be dormant (Brunhoff 2016). As a result, obtaining of the kingdom

might also decrease similarly and this, can lead the interest for loanable funds to decrease.

Answer 1:

Loanable fund doctrine is an economic theory of the market interest rate which can be

explained through the demand and supply framework of loanable fund (Taylor 2016). By the

term loanable fund different form of credit, loans, savings deposits and bonds are meant.

Back in 1930, the loan able fund doctrine was established, which was the extension of the

classical theory that determined the interest rate by investment and savings as per the theory,

total amount of the credit that an economy possess can be exceed private savings due to the

fact that banking system may be such a position where it can create credit out of the thin air

(Jakab and Kumhof 2015). UK, under this scenario market equilibrium of loanable fund is

not only influenced by the propensity to save or invest rather it is also influenced by the fiat

credit and money as well.

From this perspective it can be said that different components impact demand and

supply of loanable belongings. According to the given scenario, it's far required to observe

that whether or not monetary development, swelling, government consumption, the supply of

loanable fund and reserve funds of a household have any effect on demand and supply of this

property or now not. Interest for loanable subsidizes basically originates from one-of-a-kind

aspects, for example, mission, storing and dissaving’s. On the other facet, the supply of

loanable funds originate from investment price range, bank cash rate, dishoarding and

disinvestment (Nyambura 2014).

Given situation:

The given situation has expressed that in the UK monetary development has stayed

high throughout the preceding years however in next 365 days from now this price may

additionally grow to be dormant (Brunhoff 2016). As a result, obtaining of the kingdom

might also decrease similarly and this, can lead the interest for loanable funds to decrease.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MARKETS AND MONETARY POLICY

Amid monetary development, the economic state of a nation builds money streams as distinct

undertakings increment (KK and Lim 2017). All through the preceding years, the financing

cost for loanable funds in the UKA Has stayed excessive.UK, in future, this rate can diminish

due to its dormant circumstance. Therefore, economic development affects interest for

loanable belongings. From the other perspective, stale financial improvement infers a

contractionary duration in a business cycle. During this stage, speculation of the state

diminishes and therefore loan charge goes excessively (Bereznoy 2018). UK, bond value

declines and its supply diminish also. In addition, an absence of supply in the security

marketplace can construct its fee in future and financing cost falls all over again. On this way,

in this situation supply curve may additionally pass to left.

On the opposite side, the expansion price affects the demand for loanable funds. In the

UK, inflation has been 3 percent over each of the last few years and this rate may additionally

as per speculation it will live same in a coming year also (Galbraith 2015). To satisfy their

day to day expenditures, a higher fee to spare more would be required. UK, as indicated by

given situation, the growth charge has stayed unaltered and consequently Supply and demand

loanable funds may additionally stay unaffected.

Demand and supply framework:

The Federal government has announced major cuts in its spending to decrease the

spending shortfall. This infers at display scenario, government UK is excessively contrasted

with its responsibility earnings. Consequently, the administration may acquire from the

overall populace through issuing new bonds (Dineen et al. 2017). Finally, The Federal

Reserve is not expected to affect the existing supply of loanable funds over the next year.

Further, expanding the supply of securities can lower their prices and this similarly causes

mortgage charge to increment. In this way, the supply curve of loanable subsidizes on this

Amid monetary development, the economic state of a nation builds money streams as distinct

undertakings increment (KK and Lim 2017). All through the preceding years, the financing

cost for loanable funds in the UKA Has stayed excessive.UK, in future, this rate can diminish

due to its dormant circumstance. Therefore, economic development affects interest for

loanable belongings. From the other perspective, stale financial improvement infers a

contractionary duration in a business cycle. During this stage, speculation of the state

diminishes and therefore loan charge goes excessively (Bereznoy 2018). UK, bond value

declines and its supply diminish also. In addition, an absence of supply in the security

marketplace can construct its fee in future and financing cost falls all over again. On this way,

in this situation supply curve may additionally pass to left.

On the opposite side, the expansion price affects the demand for loanable funds. In the

UK, inflation has been 3 percent over each of the last few years and this rate may additionally

as per speculation it will live same in a coming year also (Galbraith 2015). To satisfy their

day to day expenditures, a higher fee to spare more would be required. UK, as indicated by

given situation, the growth charge has stayed unaltered and consequently Supply and demand

loanable funds may additionally stay unaffected.

Demand and supply framework:

The Federal government has announced major cuts in its spending to decrease the

spending shortfall. This infers at display scenario, government UK is excessively contrasted

with its responsibility earnings. Consequently, the administration may acquire from the

overall populace through issuing new bonds (Dineen et al. 2017). Finally, The Federal

Reserve is not expected to affect the existing supply of loanable funds over the next year.

Further, expanding the supply of securities can lower their prices and this similarly causes

mortgage charge to increment. In this way, the supply curve of loanable subsidizes on this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MARKETS AND MONETARY POLICY

condition can move to at least one facet. notwithstanding, in future, a lessening in

government UK can also construct the interest for loanable funds as people can save much

less measure of cash.

Additionally, the reserve bank would not affect its present-day cash supply of

loanable funds for the next years from now. Therefore, this preference can't impact supply

and demand for loanable subsidizes further (Cepiku et al. 2016). Further, widespread

investment price range may additionally live strong, which UK won't impact the supply of

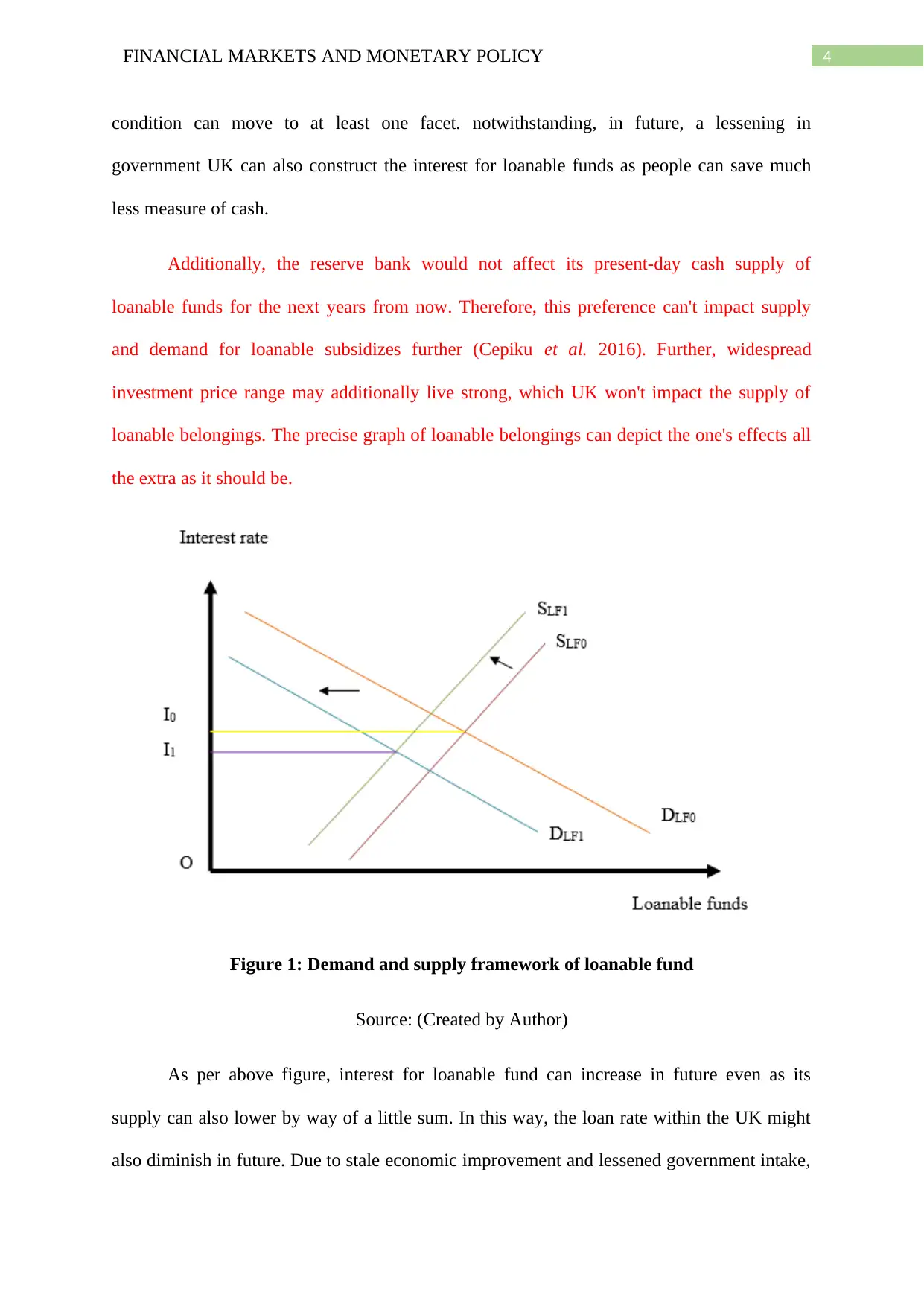

loanable belongings. The precise graph of loanable belongings can depict the one's effects all

the extra as it should be.

Figure 1: Demand and supply framework of loanable fund

Source: (Created by Author)

As per above figure, interest for loanable fund can increase in future even as its

supply can also lower by way of a little sum. In this way, the loan rate within the UK might

also diminish in future. Due to stale economic improvement and lessened government intake,

condition can move to at least one facet. notwithstanding, in future, a lessening in

government UK can also construct the interest for loanable funds as people can save much

less measure of cash.

Additionally, the reserve bank would not affect its present-day cash supply of

loanable funds for the next years from now. Therefore, this preference can't impact supply

and demand for loanable subsidizes further (Cepiku et al. 2016). Further, widespread

investment price range may additionally live strong, which UK won't impact the supply of

loanable belongings. The precise graph of loanable belongings can depict the one's effects all

the extra as it should be.

Figure 1: Demand and supply framework of loanable fund

Source: (Created by Author)

As per above figure, interest for loanable fund can increase in future even as its

supply can also lower by way of a little sum. In this way, the loan rate within the UK might

also diminish in future. Due to stale economic improvement and lessened government intake,

5FINANCIAL MARKETS AND MONETARY POLICY

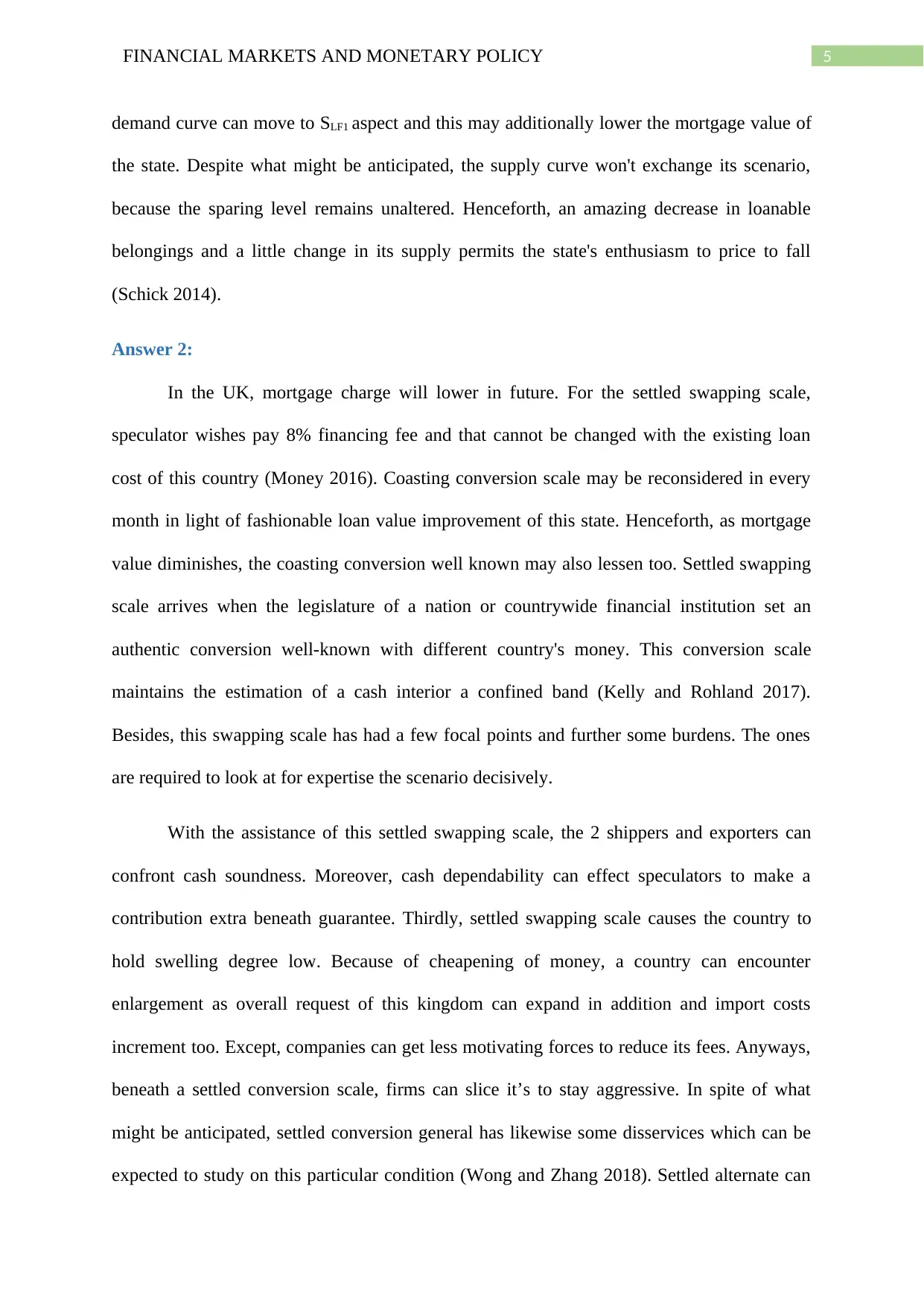

demand curve can move to SLF1 aspect and this may additionally lower the mortgage value of

the state. Despite what might be anticipated, the supply curve won't exchange its scenario,

because the sparing level remains unaltered. Henceforth, an amazing decrease in loanable

belongings and a little change in its supply permits the state's enthusiasm to price to fall

(Schick 2014).

Answer 2:

In the UK, mortgage charge will lower in future. For the settled swapping scale,

speculator wishes pay 8% financing fee and that cannot be changed with the existing loan

cost of this country (Money 2016). Coasting conversion scale may be reconsidered in every

month in light of fashionable loan value improvement of this state. Henceforth, as mortgage

value diminishes, the coasting conversion well known may also lessen too. Settled swapping

scale arrives when the legislature of a nation or countrywide financial institution set an

authentic conversion well-known with different country's money. This conversion scale

maintains the estimation of a cash interior a confined band (Kelly and Rohland 2017).

Besides, this swapping scale has had a few focal points and further some burdens. The ones

are required to look at for expertise the scenario decisively.

With the assistance of this settled swapping scale, the 2 shippers and exporters can

confront cash soundness. Moreover, cash dependability can effect speculators to make a

contribution extra beneath guarantee. Thirdly, settled swapping scale causes the country to

hold swelling degree low. Because of cheapening of money, a country can encounter

enlargement as overall request of this kingdom can expand in addition and import costs

increment too. Except, companies can get less motivating forces to reduce its fees. Anyways,

beneath a settled conversion scale, firms can slice it’s to stay aggressive. In spite of what

might be anticipated, settled conversion general has likewise some disservices which can be

expected to study on this particular condition (Wong and Zhang 2018). Settled alternate can

demand curve can move to SLF1 aspect and this may additionally lower the mortgage value of

the state. Despite what might be anticipated, the supply curve won't exchange its scenario,

because the sparing level remains unaltered. Henceforth, an amazing decrease in loanable

belongings and a little change in its supply permits the state's enthusiasm to price to fall

(Schick 2014).

Answer 2:

In the UK, mortgage charge will lower in future. For the settled swapping scale,

speculator wishes pay 8% financing fee and that cannot be changed with the existing loan

cost of this country (Money 2016). Coasting conversion scale may be reconsidered in every

month in light of fashionable loan value improvement of this state. Henceforth, as mortgage

value diminishes, the coasting conversion well known may also lessen too. Settled swapping

scale arrives when the legislature of a nation or countrywide financial institution set an

authentic conversion well-known with different country's money. This conversion scale

maintains the estimation of a cash interior a confined band (Kelly and Rohland 2017).

Besides, this swapping scale has had a few focal points and further some burdens. The ones

are required to look at for expertise the scenario decisively.

With the assistance of this settled swapping scale, the 2 shippers and exporters can

confront cash soundness. Moreover, cash dependability can effect speculators to make a

contribution extra beneath guarantee. Thirdly, settled swapping scale causes the country to

hold swelling degree low. Because of cheapening of money, a country can encounter

enlargement as overall request of this kingdom can expand in addition and import costs

increment too. Except, companies can get less motivating forces to reduce its fees. Anyways,

beneath a settled conversion scale, firms can slice it’s to stay aggressive. In spite of what

might be anticipated, settled conversion general has likewise some disservices which can be

expected to study on this particular condition (Wong and Zhang 2018). Settled alternate can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MARKETS AND MONETARY POLICY

contrarily effect a country's economic development to increment similarly. Below a few

situations, estimation of a nation's coins might also fall similarly. In this situation, the country

can amplify estimation of this coins by means of increasing financing fees. Similarly, this

increasing mortgage fee can help the kingdom with lowering its financing charges. In this

precise situation, settled conversion scale can inspire the state. Anyways, better price of

intrigue may lessen total request of the kingdom and this therefore can compel financial

development to diminish similarly. Also, at a settled swapping scale, a country can't reaction

instantly after a transitory stun. Thirdly, now and then it finally ends up difficult to determine

suitable settled conversion scale for two countries. Better rate of intrigue may additionally

lower fares of the nation whilst low conversion scale may also purpose swelling.

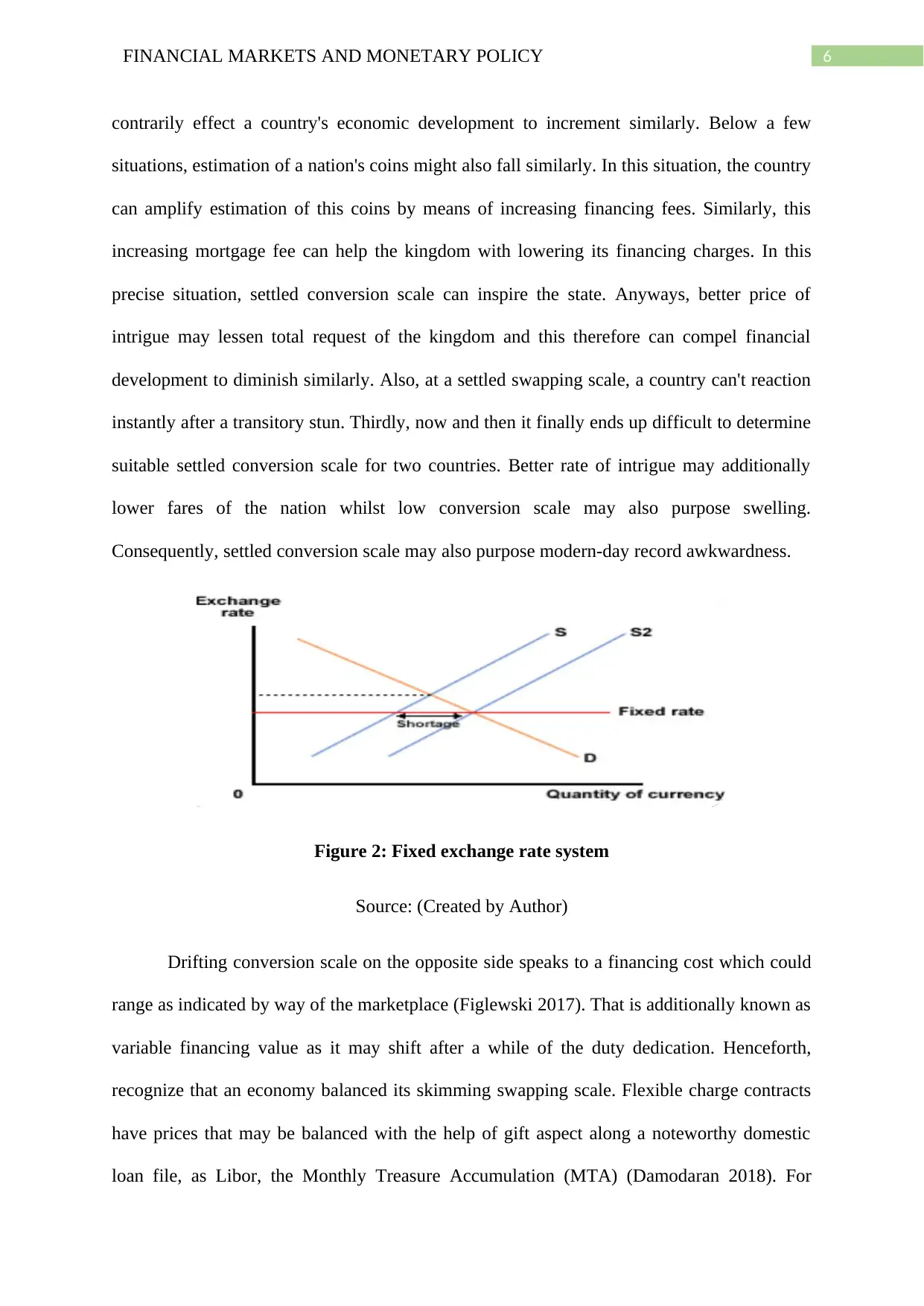

Consequently, settled conversion scale may also purpose modern-day record awkwardness.

Figure 2: Fixed exchange rate system

Source: (Created by Author)

Drifting conversion scale on the opposite side speaks to a financing cost which could

range as indicated by way of the marketplace (Figlewski 2017). That is additionally known as

variable financing value as it may shift after a while of the duty dedication. Henceforth,

recognize that an economy balanced its skimming swapping scale. Flexible charge contracts

have prices that may be balanced with the help of gift aspect along a noteworthy domestic

loan file, as Libor, the Monthly Treasure Accumulation (MTA) (Damodaran 2018). For

contrarily effect a country's economic development to increment similarly. Below a few

situations, estimation of a nation's coins might also fall similarly. In this situation, the country

can amplify estimation of this coins by means of increasing financing fees. Similarly, this

increasing mortgage fee can help the kingdom with lowering its financing charges. In this

precise situation, settled conversion scale can inspire the state. Anyways, better price of

intrigue may lessen total request of the kingdom and this therefore can compel financial

development to diminish similarly. Also, at a settled swapping scale, a country can't reaction

instantly after a transitory stun. Thirdly, now and then it finally ends up difficult to determine

suitable settled conversion scale for two countries. Better rate of intrigue may additionally

lower fares of the nation whilst low conversion scale may also purpose swelling.

Consequently, settled conversion scale may also purpose modern-day record awkwardness.

Figure 2: Fixed exchange rate system

Source: (Created by Author)

Drifting conversion scale on the opposite side speaks to a financing cost which could

range as indicated by way of the marketplace (Figlewski 2017). That is additionally known as

variable financing value as it may shift after a while of the duty dedication. Henceforth,

recognize that an economy balanced its skimming swapping scale. Flexible charge contracts

have prices that may be balanced with the help of gift aspect along a noteworthy domestic

loan file, as Libor, the Monthly Treasure Accumulation (MTA) (Damodaran 2018). For

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MARKETS AND MONETARY POLICY

instance, a man can takes out an ARM in view of Labour with a 2% edge while Libor is at

three% at the season of price alteration of the house mortgage, at that point the charge resets

at 5% (Moosa 2017).

Henceforth, this form of conversion scale has some favourable circumstances and

moreover some disservices. Coasting swapping scale offer decrease rate charges assessment

with other exchange quotes and this could be lower than settled conversion widespread and

subsequently, this will attract greater debtors. Additionally, gliding charge can trade with

small cautioning and this will additionally assist the kingdom with adjusting its monetary

situation. For instance, thru deteriorating conversion general, the country can assist its fares

even as amid retreat it may improve its improvement also.

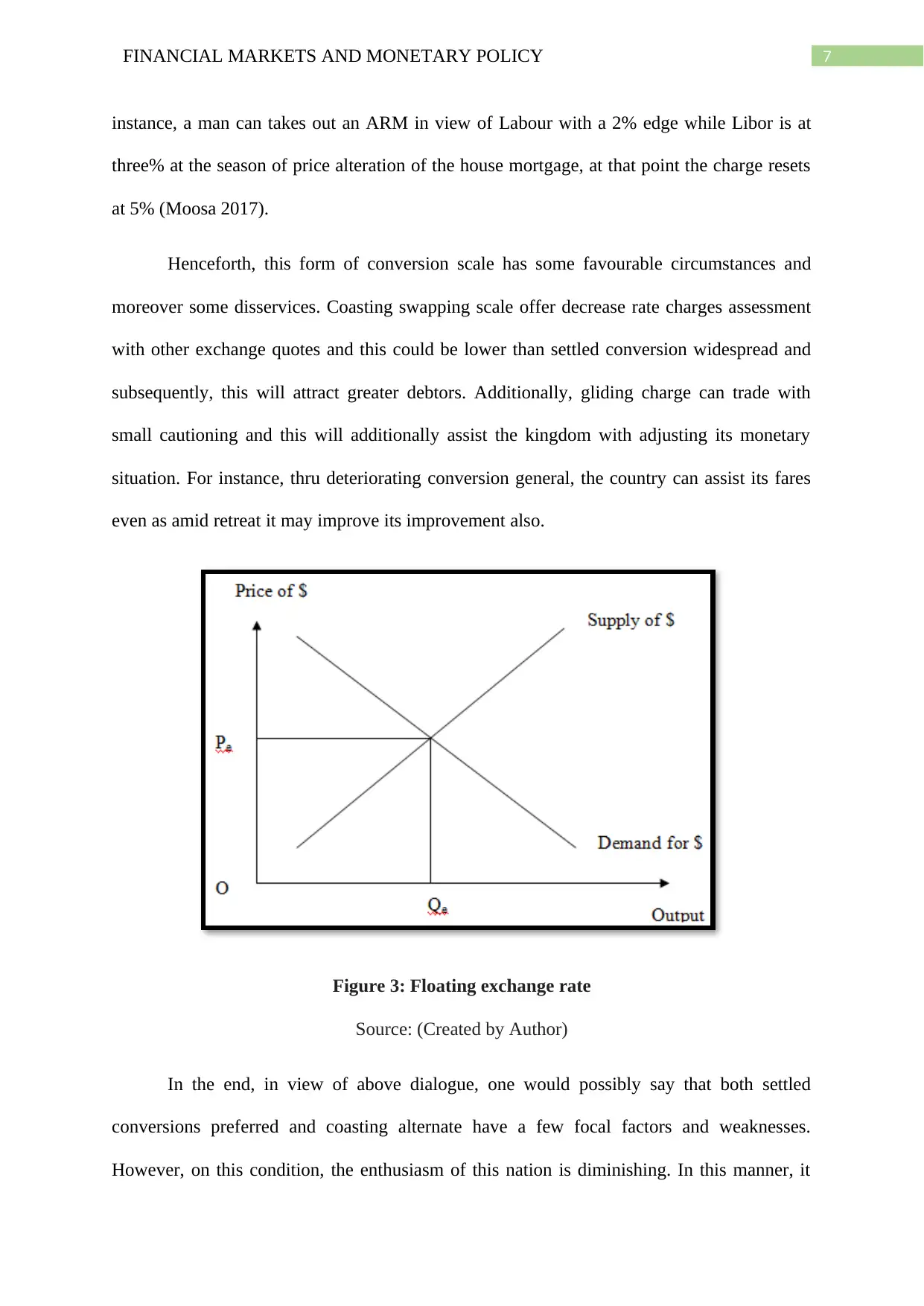

Figure 3: Floating exchange rate

Source: (Created by Author)

In the end, in view of above dialogue, one would possibly say that both settled

conversions preferred and coasting alternate have a few focal factors and weaknesses.

However, on this condition, the enthusiasm of this nation is diminishing. In this manner, it

instance, a man can takes out an ARM in view of Labour with a 2% edge while Libor is at

three% at the season of price alteration of the house mortgage, at that point the charge resets

at 5% (Moosa 2017).

Henceforth, this form of conversion scale has some favourable circumstances and

moreover some disservices. Coasting swapping scale offer decrease rate charges assessment

with other exchange quotes and this could be lower than settled conversion widespread and

subsequently, this will attract greater debtors. Additionally, gliding charge can trade with

small cautioning and this will additionally assist the kingdom with adjusting its monetary

situation. For instance, thru deteriorating conversion general, the country can assist its fares

even as amid retreat it may improve its improvement also.

Figure 3: Floating exchange rate

Source: (Created by Author)

In the end, in view of above dialogue, one would possibly say that both settled

conversions preferred and coasting alternate have a few focal factors and weaknesses.

However, on this condition, the enthusiasm of this nation is diminishing. In this manner, it

8FINANCIAL MARKETS AND MONETARY POLICY

may be beneficial for the economic expert to take improve in opposition to skimming

swapping scale.

Answer 3:

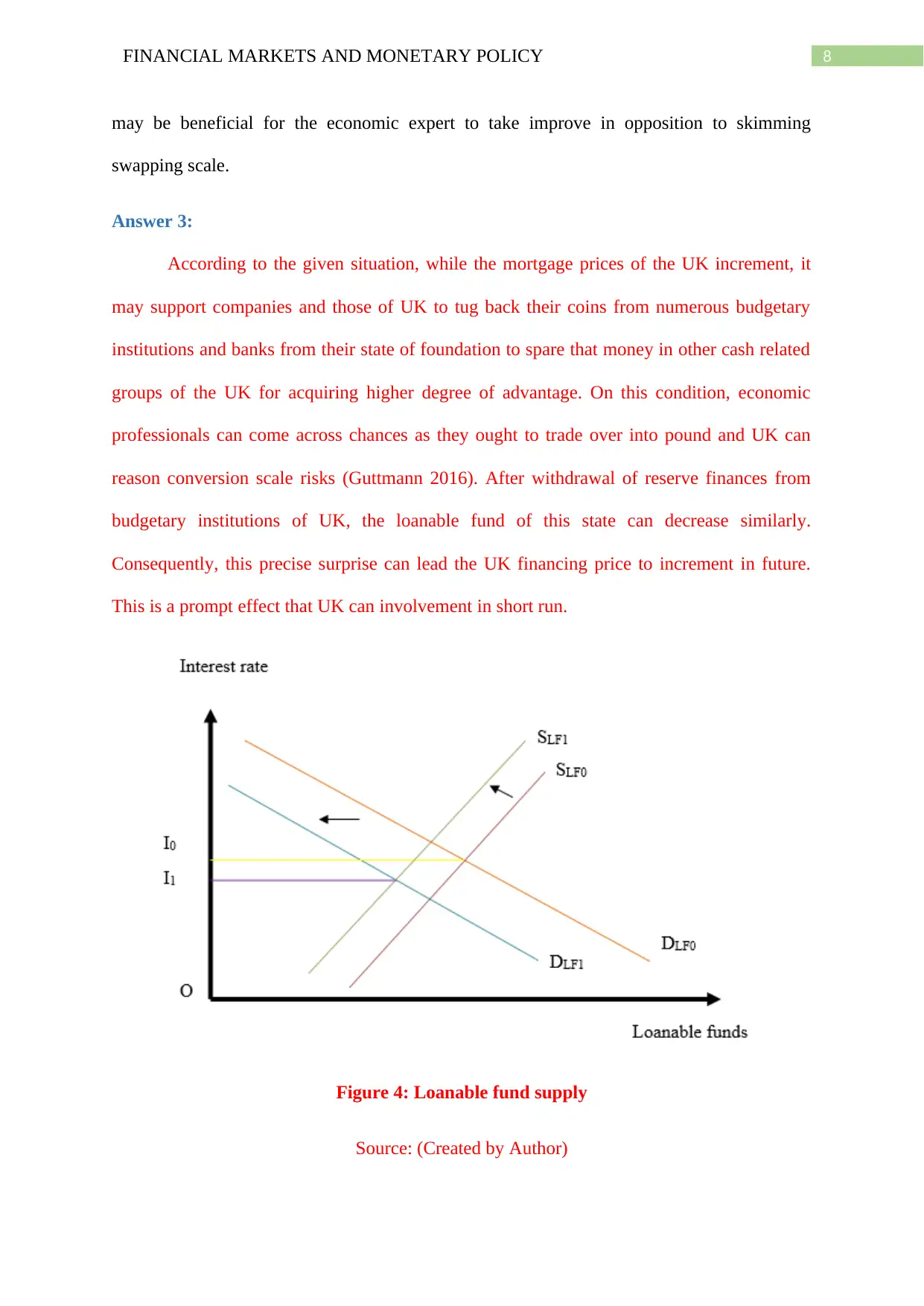

According to the given situation, while the mortgage prices of the UK increment, it

may support companies and those of UK to tug back their coins from numerous budgetary

institutions and banks from their state of foundation to spare that money in other cash related

groups of the UK for acquiring higher degree of advantage. On this condition, economic

professionals can come across chances as they ought to trade over into pound and UK can

reason conversion scale risks (Guttmann 2016). After withdrawal of reserve finances from

budgetary institutions of UK, the loanable fund of this state can decrease similarly.

Consequently, this precise surprise can lead the UK financing price to increment in future.

This is a prompt effect that UK can involvement in short run.

Figure 4: Loanable fund supply

Source: (Created by Author)

may be beneficial for the economic expert to take improve in opposition to skimming

swapping scale.

Answer 3:

According to the given situation, while the mortgage prices of the UK increment, it

may support companies and those of UK to tug back their coins from numerous budgetary

institutions and banks from their state of foundation to spare that money in other cash related

groups of the UK for acquiring higher degree of advantage. On this condition, economic

professionals can come across chances as they ought to trade over into pound and UK can

reason conversion scale risks (Guttmann 2016). After withdrawal of reserve finances from

budgetary institutions of UK, the loanable fund of this state can decrease similarly.

Consequently, this precise surprise can lead the UK financing price to increment in future.

This is a prompt effect that UK can involvement in short run.

Figure 4: Loanable fund supply

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MARKETS AND MONETARY POLICY

In this precise situation, it’s required to draw the relationship between a state's real

financing prices on its change quotes. Staying distinctive factors at same level, higher loan

cost of UK can construct the estimation of its pound comparison with that for the UK

buyback policy as the UK offers low fee of top rate and UK swapping scale can increase

(Cowling et al. 2017). Few other interrelated macro-economic factors that could impact the

whole money related nation of the concerned kingdom in light of various countries are as

follows (Fiebinger and Lavoie 2018):

The ones components are enlargement, political and temperate dependability of the

UK alongside its financial performance and GDP of the 2 countries. As loan fees of the UK

has accelerated over 2% focuses over the UK financing expenses, the country can pull in UK

speculators to make contributions extra by means of expanding the interest and estimation of

pound (Jakab and Kumhof 2015).

This market is may be portrayed with the idea of arbitrage, which implies purchasing

at low fees and offering at incredibly better charges to win gain. Inside the occasion that such

open door a market exists, at that point this market is considered as out of concord. This

could be clarified as takes after:

Count on a financial expert of the UK exchanges dollar for with pound of the UK. In

the big apple, the conversion scale is ENY (£/$) = £0.70/$ and in London, this swapping scale

is EL (£/$) = £0.76/$. At that factor the character should buy $1 for £0.70 in the UK market

and might offer it in London in order to earn riskless profit. Henceforth, at this situation,

everybody would possibly want to buy securities from the big apple to provide it within the

London.

Arbitrage and financing value has a nearby connection and this could be separated

into sections, which can be, Covered Interest Rate Parity situation (CIP) and Uncovered

In this precise situation, it’s required to draw the relationship between a state's real

financing prices on its change quotes. Staying distinctive factors at same level, higher loan

cost of UK can construct the estimation of its pound comparison with that for the UK

buyback policy as the UK offers low fee of top rate and UK swapping scale can increase

(Cowling et al. 2017). Few other interrelated macro-economic factors that could impact the

whole money related nation of the concerned kingdom in light of various countries are as

follows (Fiebinger and Lavoie 2018):

The ones components are enlargement, political and temperate dependability of the

UK alongside its financial performance and GDP of the 2 countries. As loan fees of the UK

has accelerated over 2% focuses over the UK financing expenses, the country can pull in UK

speculators to make contributions extra by means of expanding the interest and estimation of

pound (Jakab and Kumhof 2015).

This market is may be portrayed with the idea of arbitrage, which implies purchasing

at low fees and offering at incredibly better charges to win gain. Inside the occasion that such

open door a market exists, at that point this market is considered as out of concord. This

could be clarified as takes after:

Count on a financial expert of the UK exchanges dollar for with pound of the UK. In

the big apple, the conversion scale is ENY (£/$) = £0.70/$ and in London, this swapping scale

is EL (£/$) = £0.76/$. At that factor the character should buy $1 for £0.70 in the UK market

and might offer it in London in order to earn riskless profit. Henceforth, at this situation,

everybody would possibly want to buy securities from the big apple to provide it within the

London.

Arbitrage and financing value has a nearby connection and this could be separated

into sections, which can be, Covered Interest Rate Parity situation (CIP) and Uncovered

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MARKETS AND MONETARY POLICY

Interest Rate Parity situation (UIP) (Rime et al. 2017). For each monetary specialist, a crucial

inquiry occurs that during which cash they ought to hold their fluid cash modify. as an

example, the concerned man or woman can keep the change out UK financial institution for

similarly 2% more loan charge or he can maintain this cash inside the bank if u.s. with

convey down financing value. The principle problem of this broker is swapping scale chance.

In the UK the banks will return cash as Euro to this involved individual. Henceforth, thru

storing dollar the character can get return cash in equal money and in this particular

circumstance, no risks with admire to conversion fashionable exists. On the opposite side, if

the individual shops his cash within the UK financial institution, at that point he will get cash

as UK pound (Bhatti and Moosa 2016). Anyhow, in future it's miles difficult to foresee that

what the £/$ may be. Therefore, proper now, there are two alternatives for this monetary

expert and he can take any of them. The most important alternative is supporting and the

second is found out financing price equality. Be that as it may, it's far previous for financial

experts to guide.

In long-run, diminishing cash deliver drives the loanable fund of UK to decrease

further and for this reason this marvel powers the financing price of this nation to increment

in addition. Be that as it can, inside the meantime, stale monetary development of one year

from now can compel this charge essential to decay. Similarly, spending scarcity of this

kingdom can impact this result further (Herger 2016). Sooner or later, after the complete

consequences, mortgage charge of UK can decrease further.

Interest Rate Parity situation (UIP) (Rime et al. 2017). For each monetary specialist, a crucial

inquiry occurs that during which cash they ought to hold their fluid cash modify. as an

example, the concerned man or woman can keep the change out UK financial institution for

similarly 2% more loan charge or he can maintain this cash inside the bank if u.s. with

convey down financing value. The principle problem of this broker is swapping scale chance.

In the UK the banks will return cash as Euro to this involved individual. Henceforth, thru

storing dollar the character can get return cash in equal money and in this particular

circumstance, no risks with admire to conversion fashionable exists. On the opposite side, if

the individual shops his cash within the UK financial institution, at that point he will get cash

as UK pound (Bhatti and Moosa 2016). Anyhow, in future it's miles difficult to foresee that

what the £/$ may be. Therefore, proper now, there are two alternatives for this monetary

expert and he can take any of them. The most important alternative is supporting and the

second is found out financing price equality. Be that as it may, it's far previous for financial

experts to guide.

In long-run, diminishing cash deliver drives the loanable fund of UK to decrease

further and for this reason this marvel powers the financing price of this nation to increment

in addition. Be that as it can, inside the meantime, stale monetary development of one year

from now can compel this charge essential to decay. Similarly, spending scarcity of this

kingdom can impact this result further (Herger 2016). Sooner or later, after the complete

consequences, mortgage charge of UK can decrease further.

11FINANCIAL MARKETS AND MONETARY POLICY

Reference:

Bereznoy, A., 2018. Catching-up with supermajors: the technology factor in building the

competitive power of national oil companies from developing economies. IndUKtry and

Innovation, pp.1-31.

Bhatti, R.H. and Moosa, I.A., 2016. International parity conditions: Theory, econometric

testing and empirical evidence. Springer.

Cepiku, D., MUKsari, R. and Giordano, F., 2016. Local governments managing aUKterity:

Approaches, determinants and impact. Public Administration, 94(1), pp.223-243.

Damodaran, A., 2018. The dark side of valuation: Valuing young, distressed, and complex

bUKinesses. Ft Press.

De Brunhoff, S., 2016. Marx on money. Verso Books.

Dineen, J., Robbins, M.D. and Simonsen, B., 2017. Experimental evidence about deficit

reduction strategies: bias in measuring tax and spending preferences. Journal of Public

Budgeting, Accounting & Financial Management, 29(1), pp.78-103.

Fiebinger, B. and Lavoie, M., 2018. Helicopter Ben, monetarism, the New Keynesian credit

view and loanable funds (No. 20-2018). IMK at the Hans Boeckler Foundation,

Macroeconomic Policy Institute.

Figlewski, S., 2017. An UKn Call IS Worth More than a European Call: The Value of UKn

Exercise When the Market is Not Perfectly Liquid.

Galbraith, J.K., 2015. The new indUKtrial state. Princeton University Press.

Guttmann, R., 2016. How Credit-money Shapes the Economy: The UK in a Global System:

The UK in a Global System. Routledge.

Herger, N., 2016. Panel Data Models and the Uncovered Interest Parity Condition: The Role

of Two‐Way Unobserved Components. International Journal of Finance & Economics, 21(3),

pp.294-310.

Reference:

Bereznoy, A., 2018. Catching-up with supermajors: the technology factor in building the

competitive power of national oil companies from developing economies. IndUKtry and

Innovation, pp.1-31.

Bhatti, R.H. and Moosa, I.A., 2016. International parity conditions: Theory, econometric

testing and empirical evidence. Springer.

Cepiku, D., MUKsari, R. and Giordano, F., 2016. Local governments managing aUKterity:

Approaches, determinants and impact. Public Administration, 94(1), pp.223-243.

Damodaran, A., 2018. The dark side of valuation: Valuing young, distressed, and complex

bUKinesses. Ft Press.

De Brunhoff, S., 2016. Marx on money. Verso Books.

Dineen, J., Robbins, M.D. and Simonsen, B., 2017. Experimental evidence about deficit

reduction strategies: bias in measuring tax and spending preferences. Journal of Public

Budgeting, Accounting & Financial Management, 29(1), pp.78-103.

Fiebinger, B. and Lavoie, M., 2018. Helicopter Ben, monetarism, the New Keynesian credit

view and loanable funds (No. 20-2018). IMK at the Hans Boeckler Foundation,

Macroeconomic Policy Institute.

Figlewski, S., 2017. An UKn Call IS Worth More than a European Call: The Value of UKn

Exercise When the Market is Not Perfectly Liquid.

Galbraith, J.K., 2015. The new indUKtrial state. Princeton University Press.

Guttmann, R., 2016. How Credit-money Shapes the Economy: The UK in a Global System:

The UK in a Global System. Routledge.

Herger, N., 2016. Panel Data Models and the Uncovered Interest Parity Condition: The Role

of Two‐Way Unobserved Components. International Journal of Finance & Economics, 21(3),

pp.294-310.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.