Financial Markets Analysis: Monetary Policy, IFC, and CAPM Evaluation

VerifiedAdded on 2022/08/20

|17

|4008

|10

Report

AI Summary

This report delves into the intricacies of financial markets, evaluating the effectiveness of monetary policy conducted by the Monetary Authority of Singapore (MAS) and its unique approach to maintain price stability. It then compares and contrasts Singapore and Hong Kong as leading international financial centers, highlighting the key differences that contribute to their success, with a focus on their financial structures and market dynamics. The report further explores the Capital Asset Pricing Model (CAPM), explaining its significance, implications, and inherent weaknesses. Finally, it addresses the concept of asymmetric information within financial markets, providing examples and assessing the role of these markets in mitigating information imbalances. The report provides a comprehensive overview of critical aspects of financial markets, offering valuable insights into various concepts and their practical implications.

Running Head: FINANCIAL MARKETS

FINANCIAL MARKETS

Name of the Student

Name of the University

Author Note

FINANCIAL MARKETS

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MARKETS

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Answer to Question1)............................................................................................................2

Effectiveness of Monetary Policy conducted by MAS..........................................................2

Answer to Question 2)...........................................................................................................4

Key Unique Differences to be Successful International Financial Centre.............................4

Answer to Question 3)...........................................................................................................8

Significance, Implications and Weaknesses of CAPM..........................................................8

Answer to Question 4).........................................................................................................10

Asymmetric Information and Solving Problem by Financial Markets................................10

Conclusion................................................................................................................................12

Reference..................................................................................................................................14

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Answer to Question1)............................................................................................................2

Effectiveness of Monetary Policy conducted by MAS..........................................................2

Answer to Question 2)...........................................................................................................4

Key Unique Differences to be Successful International Financial Centre.............................4

Answer to Question 3)...........................................................................................................8

Significance, Implications and Weaknesses of CAPM..........................................................8

Answer to Question 4).........................................................................................................10

Asymmetric Information and Solving Problem by Financial Markets................................10

Conclusion................................................................................................................................12

Reference..................................................................................................................................14

2FINANCIAL MARKETS

Introduction

Financial market is the place, where individuals are engaged in any form of the

financial transactions. This market is the platform, where sellers and buyers are engaged in

the sale and purchase of the financial products such as bonds, shares, mutual funds and

others. Financial market helps in creating liquidity, which allows to grow the businesses and

entrepreneurs for raising the money for ventures (Loh 2014). Hence, this report aims to

evaluate effectiveness of monetary policy conducted by MAS. Further, discussion will be on

key unique difference between the Hong Kong and Singapore that enables these countries to

be successful international financial centre. Moreover, explanation will be on significance,

implications and weaknesses of CAPM. Lastly, explanation will be on term asymmetric

information and assessment will be on the way financial markets helps in solving problems of

the asymmetric information.

Discussion

Answer to Question1)

Effectiveness of Monetary Policy conducted by MAS

The increasing globalization as well as rising flows of international capital has

resulted into complex determination of the appropriate monetary policy for the small and

open economies, for instance Singapore. The policymakers face challenge for assessing

different trade-off among the objectives of policy, evaluation of the economic development

that are likely to be most significant in medium term, identification of key constraints on

operating regime and estimating required degrees of the transparency of monetary policy. In

this particular context, unique monetary framework has been adopted by Singapore that is

centered on management of exchange rate and which is primarily aimed at promoting

stability of price, as the basis for the sustainable growth of economy (Baharumshah and Soon

Introduction

Financial market is the place, where individuals are engaged in any form of the

financial transactions. This market is the platform, where sellers and buyers are engaged in

the sale and purchase of the financial products such as bonds, shares, mutual funds and

others. Financial market helps in creating liquidity, which allows to grow the businesses and

entrepreneurs for raising the money for ventures (Loh 2014). Hence, this report aims to

evaluate effectiveness of monetary policy conducted by MAS. Further, discussion will be on

key unique difference between the Hong Kong and Singapore that enables these countries to

be successful international financial centre. Moreover, explanation will be on significance,

implications and weaknesses of CAPM. Lastly, explanation will be on term asymmetric

information and assessment will be on the way financial markets helps in solving problems of

the asymmetric information.

Discussion

Answer to Question1)

Effectiveness of Monetary Policy conducted by MAS

The increasing globalization as well as rising flows of international capital has

resulted into complex determination of the appropriate monetary policy for the small and

open economies, for instance Singapore. The policymakers face challenge for assessing

different trade-off among the objectives of policy, evaluation of the economic development

that are likely to be most significant in medium term, identification of key constraints on

operating regime and estimating required degrees of the transparency of monetary policy. In

this particular context, unique monetary framework has been adopted by Singapore that is

centered on management of exchange rate and which is primarily aimed at promoting

stability of price, as the basis for the sustainable growth of economy (Baharumshah and Soon

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MARKETS

2015). The policy framework of MAS focusses operationally on the management of

Singapore dollar against undisclosed basket of the currencies of big competitors and the

trading partners. This basket composition is revised and reviewed on periodically basis for

taking into account the changes in trade patterns of the Singapore, however, there is no

disclosure of details concerning boundaries and index of target band. MAS helps in guiding

rate of exchange to depreciate or appreciate. This depends mainly on whether the expected

pressures of inflationary are weaker and stronger (Mas.gov.sg. 2020). In case of recognizing

monetary policy lags, MAS measures stance of appropriate policy and it operates in the

forward-looking manner with the help of taking into account anticipated developments and

trends in external environment and domestic economy. The policies of MAS have been

complemented by the recent efforts for enhancing transparency and increasing disclosures

through release of “Monetary Policy Statement” and economic development analysis in its

“Macroeconomic Review” (IMF eLibrary. 2020).

The Singapore’s monetary policy is centred on rate of exchange. In open and small

economy of Singapore, rate of exchange is more effective tool for the maintenance of price

stability. “The Monetary Authority of Singapore” is the central bank of Singapore and

monitory policy is conducted for maintaining stability of price favorable to the sustained

growth of the economy. Further, MAS brings out full ranges of functions of the central

banking that is related to the formulation and implementation of monetary policy (Bianchi

and Deschamps 2018). The objective of MAS is enshrined in the act of MAS. One of the

main objectives of the monetary policy is ensuring lower inflation as sound basis for the

sustained growth of economy. The monetary policy of Singapore is centered on the

management of the exchange rate compared to interest rates or money supply. It reflects that

in open as well as small economy of Singapore, rate of exchange is most effective tool in

maintenance of the price stability (Loh 2014).

2015). The policy framework of MAS focusses operationally on the management of

Singapore dollar against undisclosed basket of the currencies of big competitors and the

trading partners. This basket composition is revised and reviewed on periodically basis for

taking into account the changes in trade patterns of the Singapore, however, there is no

disclosure of details concerning boundaries and index of target band. MAS helps in guiding

rate of exchange to depreciate or appreciate. This depends mainly on whether the expected

pressures of inflationary are weaker and stronger (Mas.gov.sg. 2020). In case of recognizing

monetary policy lags, MAS measures stance of appropriate policy and it operates in the

forward-looking manner with the help of taking into account anticipated developments and

trends in external environment and domestic economy. The policies of MAS have been

complemented by the recent efforts for enhancing transparency and increasing disclosures

through release of “Monetary Policy Statement” and economic development analysis in its

“Macroeconomic Review” (IMF eLibrary. 2020).

The Singapore’s monetary policy is centred on rate of exchange. In open and small

economy of Singapore, rate of exchange is more effective tool for the maintenance of price

stability. “The Monetary Authority of Singapore” is the central bank of Singapore and

monitory policy is conducted for maintaining stability of price favorable to the sustained

growth of the economy. Further, MAS brings out full ranges of functions of the central

banking that is related to the formulation and implementation of monetary policy (Bianchi

and Deschamps 2018). The objective of MAS is enshrined in the act of MAS. One of the

main objectives of the monetary policy is ensuring lower inflation as sound basis for the

sustained growth of economy. The monetary policy of Singapore is centered on the

management of the exchange rate compared to interest rates or money supply. It reflects that

in open as well as small economy of Singapore, rate of exchange is most effective tool in

maintenance of the price stability (Loh 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MARKETS

In open and small economy of Singapore, where the gross imports and exports of the

goods and services exceeds three hundred percent of the GDP and the expenditure is having

higher content of import, the rate of exchange has stronger impact on the inflation compared

to rate of interest. Consequently, framework of the monetary policy of MAS is centred on the

management of Singapore dollar against the trade-weighted basket of the currencies. It is

termed as “Singapore dollar nominal effective exchange rate”. MAS conducts the operations

of money market for providing sufficient liquidity for the well-functioning system of banking

and meeting the demand of banks for the reserve and the settlement balances (Mas.gov.sg.

2020).

Answer to Question 2)

Key Unique Differences to be Successful International Financial Centre

The position of Singapore is leading “international financial centre”. The rise of city

to the prominence as IFC is sign as well as determinant to the strength of economy. As per

latest interaction of “Global Financial Centre Index”, currently, Singapore is ranked in fourth

position for world’s most competitive centre of finance, trailing Hong Kong by only four

point, who is its closest competitor. Singapore is ranked in fourth position in “Xinhua-Dow

Jones International Centers Development Index” and Sixth in “Deloitte Wealth Management

Centre Ranking 2015”.

Hong Kong has been succeeded as an “international financial centre” because it is

having its historical design or accident, followed sound principles of the free market with the

minimal intervention of government. Market is having habit of moving around the artificial

barrier that is created against them. This free market is enshrined in the one country and two

principle system. Usually, Hong Kong is not challenged from the other centres, however, the

challenges come from the requirement to maintain confidence. There are two confidence

aspects, which affects market efficiency. The first one is requirement for the political

In open and small economy of Singapore, where the gross imports and exports of the

goods and services exceeds three hundred percent of the GDP and the expenditure is having

higher content of import, the rate of exchange has stronger impact on the inflation compared

to rate of interest. Consequently, framework of the monetary policy of MAS is centred on the

management of Singapore dollar against the trade-weighted basket of the currencies. It is

termed as “Singapore dollar nominal effective exchange rate”. MAS conducts the operations

of money market for providing sufficient liquidity for the well-functioning system of banking

and meeting the demand of banks for the reserve and the settlement balances (Mas.gov.sg.

2020).

Answer to Question 2)

Key Unique Differences to be Successful International Financial Centre

The position of Singapore is leading “international financial centre”. The rise of city

to the prominence as IFC is sign as well as determinant to the strength of economy. As per

latest interaction of “Global Financial Centre Index”, currently, Singapore is ranked in fourth

position for world’s most competitive centre of finance, trailing Hong Kong by only four

point, who is its closest competitor. Singapore is ranked in fourth position in “Xinhua-Dow

Jones International Centers Development Index” and Sixth in “Deloitte Wealth Management

Centre Ranking 2015”.

Hong Kong has been succeeded as an “international financial centre” because it is

having its historical design or accident, followed sound principles of the free market with the

minimal intervention of government. Market is having habit of moving around the artificial

barrier that is created against them. This free market is enshrined in the one country and two

principle system. Usually, Hong Kong is not challenged from the other centres, however, the

challenges come from the requirement to maintain confidence. There are two confidence

aspects, which affects market efficiency. The first one is requirement for the political

5FINANCIAL MARKETS

stability, in the absence of which market cannot thrive (Woo 2015). In this concern, Hong

Kong has enjoyed long political stability. This country applies concept of the one country and

two systems. However, the main reason behind success of Hong Kong as “international

financial centre” have been preserved in the basic law and Joint declaration. The second

aspect of confidence lies in freedom and ability of entrepreneur in making uses of their own

judgement and skills for acting in the best interest. The pool of the entrepreneurial talent of

Hong Kong is envy of world (Chiu 2018).

Singapore owes the strength from its derivative markets and foreign exchange,

whereas, Hong Kong succeeds on its offshore lending and industry of fund management.

Therefore, Hong Kong and the Singapore complements each other for providing the financial

services to the clients. Moreover, there consists of no “zero-sum competition” in between

two, each of which serves two different geographic regions. In case, if Singapore is not

successful in the development of its industry of fund management, then Hong Kong will be

affected badly. It is because industry in the region is still at the stage of infant and prospects

of market for the expansion is still great. Hence, deciding factor for Hong Kong or Singapore

to emerge as second IFC, will depend on the speed with which these two centres in order to

recover from the Asian financial crisis will be using technological development and efficient

provision of wide financial services or products ranges are tailored to international client’s

needs at the competitive prices (Edb.gov.hk. 2020).

Since 1960, Hong Kong and Singapore have been competing with each other to be

next IFC after Tokyo. When market of Asian dollar was first introduced, Singapore had head

start in year 1968. However, Hong Kong lagged behind due to its moratorium on the licenses

of banking arises from crisis of banking in year 1965 and also this country refused to abolish

interest withholding tax on the deposits of foreign currency. Despite of the hindrance, Hong

Kong gain its momentum afterwards through different measures for developing itself into the

stability, in the absence of which market cannot thrive (Woo 2015). In this concern, Hong

Kong has enjoyed long political stability. This country applies concept of the one country and

two systems. However, the main reason behind success of Hong Kong as “international

financial centre” have been preserved in the basic law and Joint declaration. The second

aspect of confidence lies in freedom and ability of entrepreneur in making uses of their own

judgement and skills for acting in the best interest. The pool of the entrepreneurial talent of

Hong Kong is envy of world (Chiu 2018).

Singapore owes the strength from its derivative markets and foreign exchange,

whereas, Hong Kong succeeds on its offshore lending and industry of fund management.

Therefore, Hong Kong and the Singapore complements each other for providing the financial

services to the clients. Moreover, there consists of no “zero-sum competition” in between

two, each of which serves two different geographic regions. In case, if Singapore is not

successful in the development of its industry of fund management, then Hong Kong will be

affected badly. It is because industry in the region is still at the stage of infant and prospects

of market for the expansion is still great. Hence, deciding factor for Hong Kong or Singapore

to emerge as second IFC, will depend on the speed with which these two centres in order to

recover from the Asian financial crisis will be using technological development and efficient

provision of wide financial services or products ranges are tailored to international client’s

needs at the competitive prices (Edb.gov.hk. 2020).

Since 1960, Hong Kong and Singapore have been competing with each other to be

next IFC after Tokyo. When market of Asian dollar was first introduced, Singapore had head

start in year 1968. However, Hong Kong lagged behind due to its moratorium on the licenses

of banking arises from crisis of banking in year 1965 and also this country refused to abolish

interest withholding tax on the deposits of foreign currency. Despite of the hindrance, Hong

Kong gain its momentum afterwards through different measures for developing itself into the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MARKETS

IFC (Hkma.gov.hk. 2020). After reversion to the rule of China in 1997, Hong Kong started

functioning as IFC with the China as its major neighborhood. On contrary, the government of

Singapore has publicly indicated that Singapore will be developed as second IFC in Asia-

Pacific region in next millennium after Tokyo. Therefore, Hong Kong and Singapore are

direct competitors in race of second place. Each one is having its own different comparative

advantage that makes the comparison somewhat difficult (Töpfer and Hall 2018).

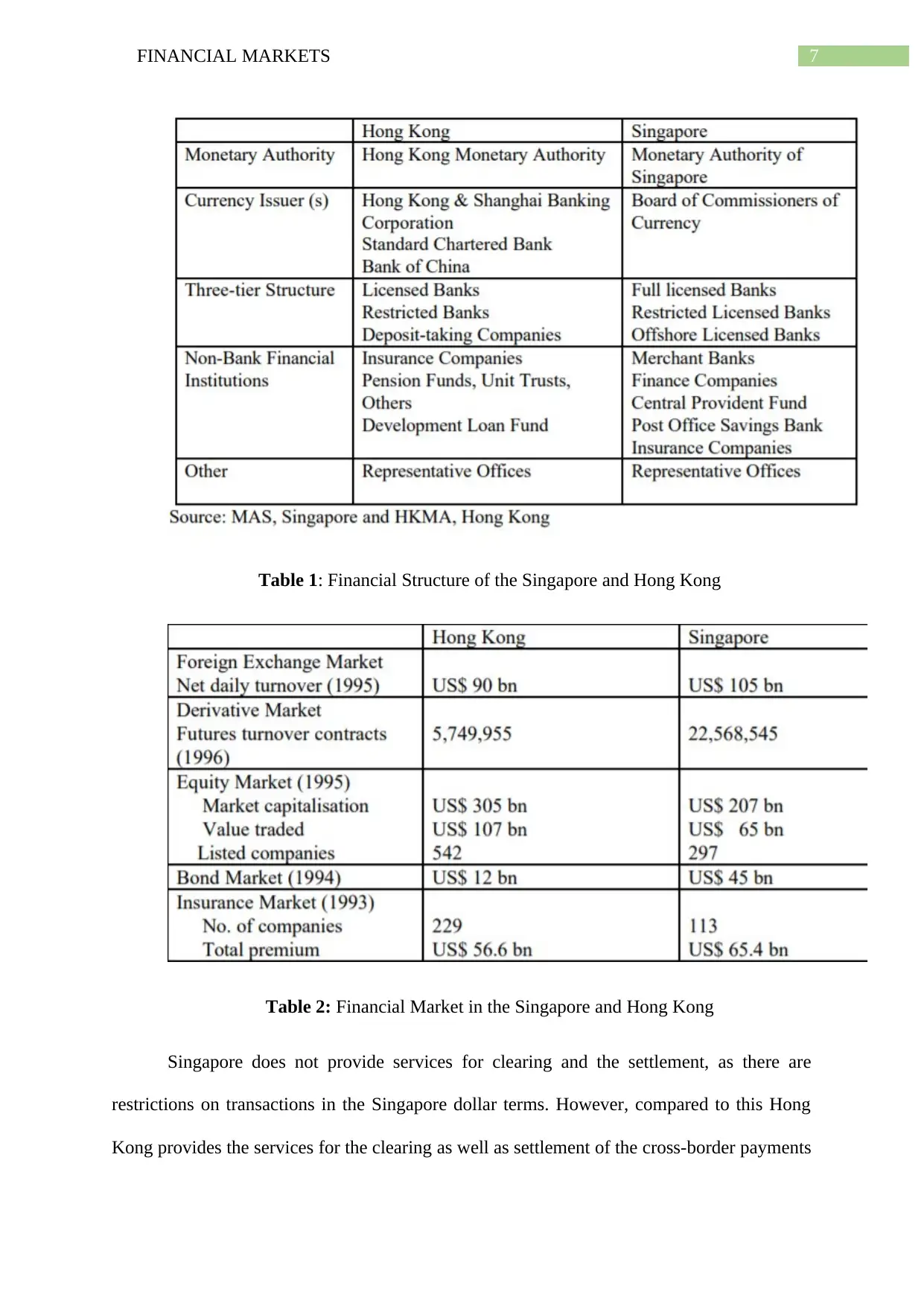

Singapore and Hong Kong share various similarities in their financial structure. Both

of the country does not own the central bank, rather they own respective authorities of

monetary, which does not have issuing powers. The issuing power is delegated to the third

party. The issuance of currency in Singapore is prerogative power of Currency board,

however, the exchange rate system of Singapore is under the managed floating system. In the

system of banking, each country follows the structure of three-tier with some of the variances

(Woo 2015). Hong Kong develops the integrated system of banking, tied with

internationalization of the Hong Kong dollar, whereas, Singapore is having offshore system

of banking, which is specialized in Asian-dollar market. In Hong Kong, “non-bank financial

institutions” are retained privatively including different funds of Hong Kong, where as

Singapore is having strong presence of the non-bank financial institutions. The government

of Singapore has been using staid institutions for the macroeconomic stabilization as well as

economic restructuring (Woo 2015).

IFC (Hkma.gov.hk. 2020). After reversion to the rule of China in 1997, Hong Kong started

functioning as IFC with the China as its major neighborhood. On contrary, the government of

Singapore has publicly indicated that Singapore will be developed as second IFC in Asia-

Pacific region in next millennium after Tokyo. Therefore, Hong Kong and Singapore are

direct competitors in race of second place. Each one is having its own different comparative

advantage that makes the comparison somewhat difficult (Töpfer and Hall 2018).

Singapore and Hong Kong share various similarities in their financial structure. Both

of the country does not own the central bank, rather they own respective authorities of

monetary, which does not have issuing powers. The issuing power is delegated to the third

party. The issuance of currency in Singapore is prerogative power of Currency board,

however, the exchange rate system of Singapore is under the managed floating system. In the

system of banking, each country follows the structure of three-tier with some of the variances

(Woo 2015). Hong Kong develops the integrated system of banking, tied with

internationalization of the Hong Kong dollar, whereas, Singapore is having offshore system

of banking, which is specialized in Asian-dollar market. In Hong Kong, “non-bank financial

institutions” are retained privatively including different funds of Hong Kong, where as

Singapore is having strong presence of the non-bank financial institutions. The government

of Singapore has been using staid institutions for the macroeconomic stabilization as well as

economic restructuring (Woo 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MARKETS

Table 1: Financial Structure of the Singapore and Hong Kong

Table 2: Financial Market in the Singapore and Hong Kong

Singapore does not provide services for clearing and the settlement, as there are

restrictions on transactions in the Singapore dollar terms. However, compared to this Hong

Kong provides the services for the clearing as well as settlement of the cross-border payments

Table 1: Financial Structure of the Singapore and Hong Kong

Table 2: Financial Market in the Singapore and Hong Kong

Singapore does not provide services for clearing and the settlement, as there are

restrictions on transactions in the Singapore dollar terms. However, compared to this Hong

Kong provides the services for the clearing as well as settlement of the cross-border payments

8FINANCIAL MARKETS

and transactions in the foreign exchange market of Hong Kong. Further, Singapore involves

large number of third country currencies, for instance, dollar of US, Deutschmark and Yen

with the local trading of currency amounts to not more than 5%. Contrary to this, the trade of

US$/HK$ predominates in foreign exchange market of Hong Kong (Chiu 2018).

Answer to Question 3)

Significance, Implications and Weaknesses of CAPM

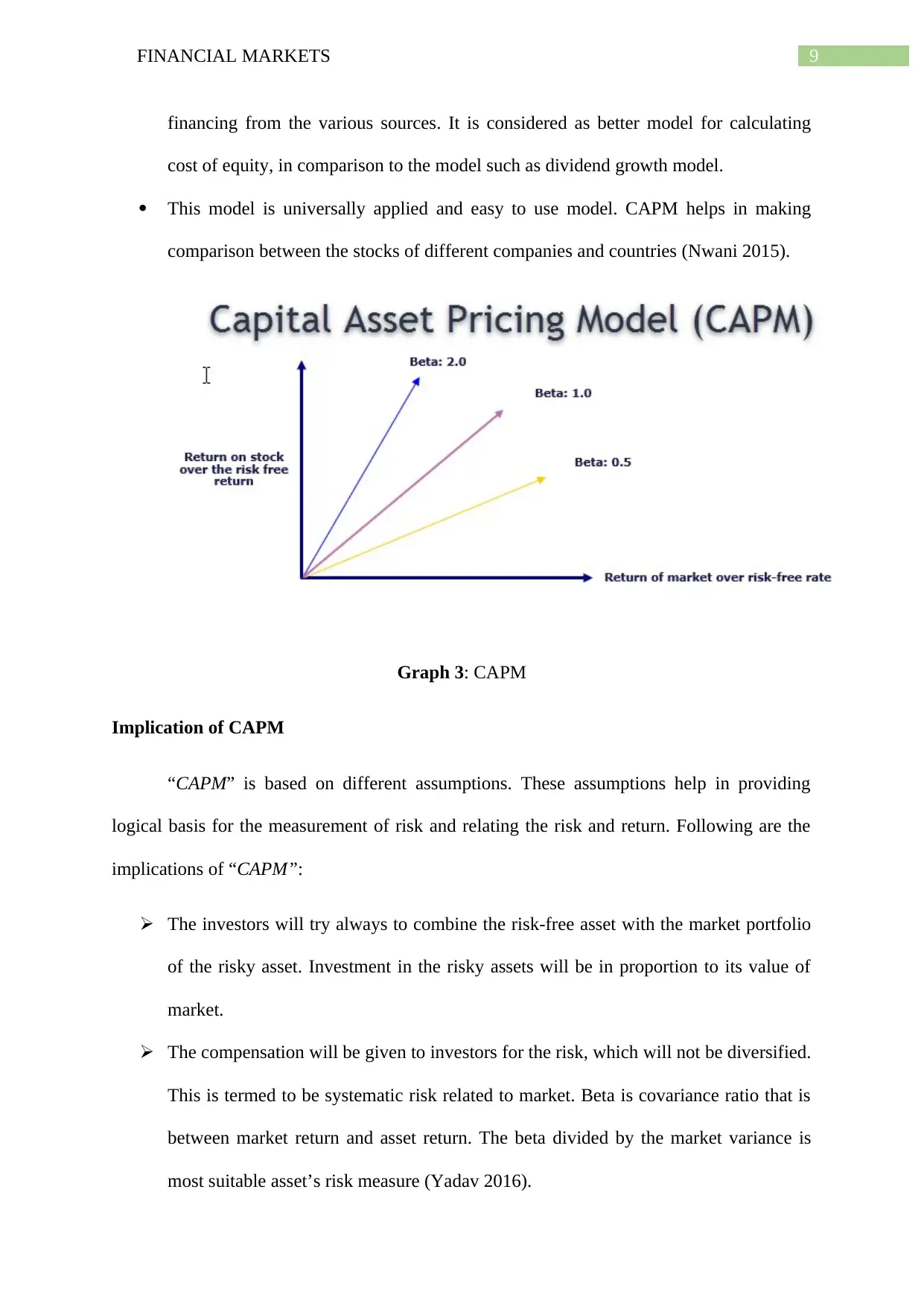

CAPM Significance

“CAPM” is measure of the relationship between the expected return and risk of

investment in the security. It is used for analyzing the securities and helps in pricing them,

given expected rate of the return and risk of investment in security. Every investment

involves certain risk. There might be difference between actual and expected return. Further,

cost of equity is the discount rate that is applied for expecting cash flows of equity that helps

in determining price that one is willing to pay for such flows of cash (Ronzani, Candido and

Maldonado 2017). By nature, investors are conservative, they decide to take risks only when

they can forecast return on their expectation from investment. The investors calculate and

they get the idea of required rate of return on the investment that is based on the assessment

of the risk using “CAPM” (Novak 2015). Following are the main significance of CAPM:

CAPM considers only market or systematic risk. This helps to eliminate vagueness

related with risk of the individual security and only the market general risk that has

degree of the certainty, becomes major factor. CAPM makes the assumption that

investors hold diversified set of portfolio and hence, unsystematic risk eradicates

between holdings of stock (Novak 2015).

CAPM is used widely in the industry of finance for the calculation of cost of equity

for the calculation of WACC that is used extensively for checking cost of the

and transactions in the foreign exchange market of Hong Kong. Further, Singapore involves

large number of third country currencies, for instance, dollar of US, Deutschmark and Yen

with the local trading of currency amounts to not more than 5%. Contrary to this, the trade of

US$/HK$ predominates in foreign exchange market of Hong Kong (Chiu 2018).

Answer to Question 3)

Significance, Implications and Weaknesses of CAPM

CAPM Significance

“CAPM” is measure of the relationship between the expected return and risk of

investment in the security. It is used for analyzing the securities and helps in pricing them,

given expected rate of the return and risk of investment in security. Every investment

involves certain risk. There might be difference between actual and expected return. Further,

cost of equity is the discount rate that is applied for expecting cash flows of equity that helps

in determining price that one is willing to pay for such flows of cash (Ronzani, Candido and

Maldonado 2017). By nature, investors are conservative, they decide to take risks only when

they can forecast return on their expectation from investment. The investors calculate and

they get the idea of required rate of return on the investment that is based on the assessment

of the risk using “CAPM” (Novak 2015). Following are the main significance of CAPM:

CAPM considers only market or systematic risk. This helps to eliminate vagueness

related with risk of the individual security and only the market general risk that has

degree of the certainty, becomes major factor. CAPM makes the assumption that

investors hold diversified set of portfolio and hence, unsystematic risk eradicates

between holdings of stock (Novak 2015).

CAPM is used widely in the industry of finance for the calculation of cost of equity

for the calculation of WACC that is used extensively for checking cost of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MARKETS

financing from the various sources. It is considered as better model for calculating

cost of equity, in comparison to the model such as dividend growth model.

This model is universally applied and easy to use model. CAPM helps in making

comparison between the stocks of different companies and countries (Nwani 2015).

Graph 3: CAPM

Implication of CAPM

“CAPM” is based on different assumptions. These assumptions help in providing

logical basis for the measurement of risk and relating the risk and return. Following are the

implications of “CAPM”:

The investors will try always to combine the risk-free asset with the market portfolio

of the risky asset. Investment in the risky assets will be in proportion to its value of

market.

The compensation will be given to investors for the risk, which will not be diversified.

This is termed to be systematic risk related to market. Beta is covariance ratio that is

between market return and asset return. The beta divided by the market variance is

most suitable asset’s risk measure (Yadav 2016).

financing from the various sources. It is considered as better model for calculating

cost of equity, in comparison to the model such as dividend growth model.

This model is universally applied and easy to use model. CAPM helps in making

comparison between the stocks of different companies and countries (Nwani 2015).

Graph 3: CAPM

Implication of CAPM

“CAPM” is based on different assumptions. These assumptions help in providing

logical basis for the measurement of risk and relating the risk and return. Following are the

implications of “CAPM”:

The investors will try always to combine the risk-free asset with the market portfolio

of the risky asset. Investment in the risky assets will be in proportion to its value of

market.

The compensation will be given to investors for the risk, which will not be diversified.

This is termed to be systematic risk related to market. Beta is covariance ratio that is

between market return and asset return. The beta divided by the market variance is

most suitable asset’s risk measure (Yadav 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MARKETS

Investors expects returns from the investment in accordance with risk. It indicates

linear relationship in between expected return of asset and its beta (Vendrame, Tucker

and Guermat 2016).

Weakness of CAPM

Apart from various benefits, CAPM also suffers from some weaknesses, which are as

follows:

Rf is yield on the short-term securities of government that is most commonly accepted

rate. However, the issue with this input is that daily changes in yield creates volatility.

It is difficult for determining proxy beta for properly assessment of project and can

affect the reliability of outcome.

CAPM is based on the various unrealistic assumptions.

Beta does not remain stable over period of time (Sattar 2017).

Answer to Question 4)

Asymmetric Information and Solving Problem by Financial Markets

Asymmetric information is the failure of information that occurs when one of the

party to the economic transaction, possesses more or greater material knowledge compared to

other party. It typically shows when the seller of goods or services is having better knowledge

in comparison to buyer. Almost all economic transactions are consisting of information

asymmetries. Asymmetric information is division and specialization of knowledge, which is

applied to business trade. For instance, typically doctors know more regarding the medical

practices compared to their patients. It is because doctors are having extensive backgrounds

of medical school, which their patients are not having. This equally applies to other

professions (Glode and Opp 2016).

Investors expects returns from the investment in accordance with risk. It indicates

linear relationship in between expected return of asset and its beta (Vendrame, Tucker

and Guermat 2016).

Weakness of CAPM

Apart from various benefits, CAPM also suffers from some weaknesses, which are as

follows:

Rf is yield on the short-term securities of government that is most commonly accepted

rate. However, the issue with this input is that daily changes in yield creates volatility.

It is difficult for determining proxy beta for properly assessment of project and can

affect the reliability of outcome.

CAPM is based on the various unrealistic assumptions.

Beta does not remain stable over period of time (Sattar 2017).

Answer to Question 4)

Asymmetric Information and Solving Problem by Financial Markets

Asymmetric information is the failure of information that occurs when one of the

party to the economic transaction, possesses more or greater material knowledge compared to

other party. It typically shows when the seller of goods or services is having better knowledge

in comparison to buyer. Almost all economic transactions are consisting of information

asymmetries. Asymmetric information is division and specialization of knowledge, which is

applied to business trade. For instance, typically doctors know more regarding the medical

practices compared to their patients. It is because doctors are having extensive backgrounds

of medical school, which their patients are not having. This equally applies to other

professions (Glode and Opp 2016).

11FINANCIAL MARKETS

In the financial market, asymmetric information is problem such as lending and

borrowing. In this market, borrower is having much better information regarding his financial

state in comparison to the lender. Further, lender finds its difficult to know whether there are

the chances that borrower will default. Lender to some of the extent tries overcoming this by

observing at the past history of credit and evidences of the reliable salary. It does not give full

picture, as it only gives limited set of information. Moreover, the consequences of this is that

the lenders charges higher rates for compensating for risk. In case of having perfect

information, the banks would not require to charge the risk premium (Fuchs, Öry and

Skrzypacz 2016).

Asymmetric information leads towards either adverse selection or moral hazards. The

occurrence of adverse selection is when undesired outcome happens because sellers and

buyers are having access to the various information and the occurrence of moral hazard is

when party takes risks because cost of the risk will not bear by party. Both of the situation

results in the failure of market (Benhabib, Liu and Wang 2016). Moreover, financial market

helps in solving the problems of asymmetric information by the help of following points:

Information Availability: It involves creation of the opportunities for having greater

access to the information to users. It is not possible for providing all information at a

time, however significant information should be given to user for making educated

decision.

Warranties and Guarantees: These benefits help in offering cushion to the

consumers against the faulty products. It is also beneficial in negotiation of the prices.

Subsidies and Taxes: The intervention of government by the policies is common in

the case of market imperfection. The government strikes balance between the losers

and gainers (Fuchs, Öry and Skrzypacz 2016).

In the financial market, asymmetric information is problem such as lending and

borrowing. In this market, borrower is having much better information regarding his financial

state in comparison to the lender. Further, lender finds its difficult to know whether there are

the chances that borrower will default. Lender to some of the extent tries overcoming this by

observing at the past history of credit and evidences of the reliable salary. It does not give full

picture, as it only gives limited set of information. Moreover, the consequences of this is that

the lenders charges higher rates for compensating for risk. In case of having perfect

information, the banks would not require to charge the risk premium (Fuchs, Öry and

Skrzypacz 2016).

Asymmetric information leads towards either adverse selection or moral hazards. The

occurrence of adverse selection is when undesired outcome happens because sellers and

buyers are having access to the various information and the occurrence of moral hazard is

when party takes risks because cost of the risk will not bear by party. Both of the situation

results in the failure of market (Benhabib, Liu and Wang 2016). Moreover, financial market

helps in solving the problems of asymmetric information by the help of following points:

Information Availability: It involves creation of the opportunities for having greater

access to the information to users. It is not possible for providing all information at a

time, however significant information should be given to user for making educated

decision.

Warranties and Guarantees: These benefits help in offering cushion to the

consumers against the faulty products. It is also beneficial in negotiation of the prices.

Subsidies and Taxes: The intervention of government by the policies is common in

the case of market imperfection. The government strikes balance between the losers

and gainers (Fuchs, Öry and Skrzypacz 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.