Financial Mathematics Assignment - University Finance Module

VerifiedAdded on 2022/09/26

|11

|1555

|24

Homework Assignment

AI Summary

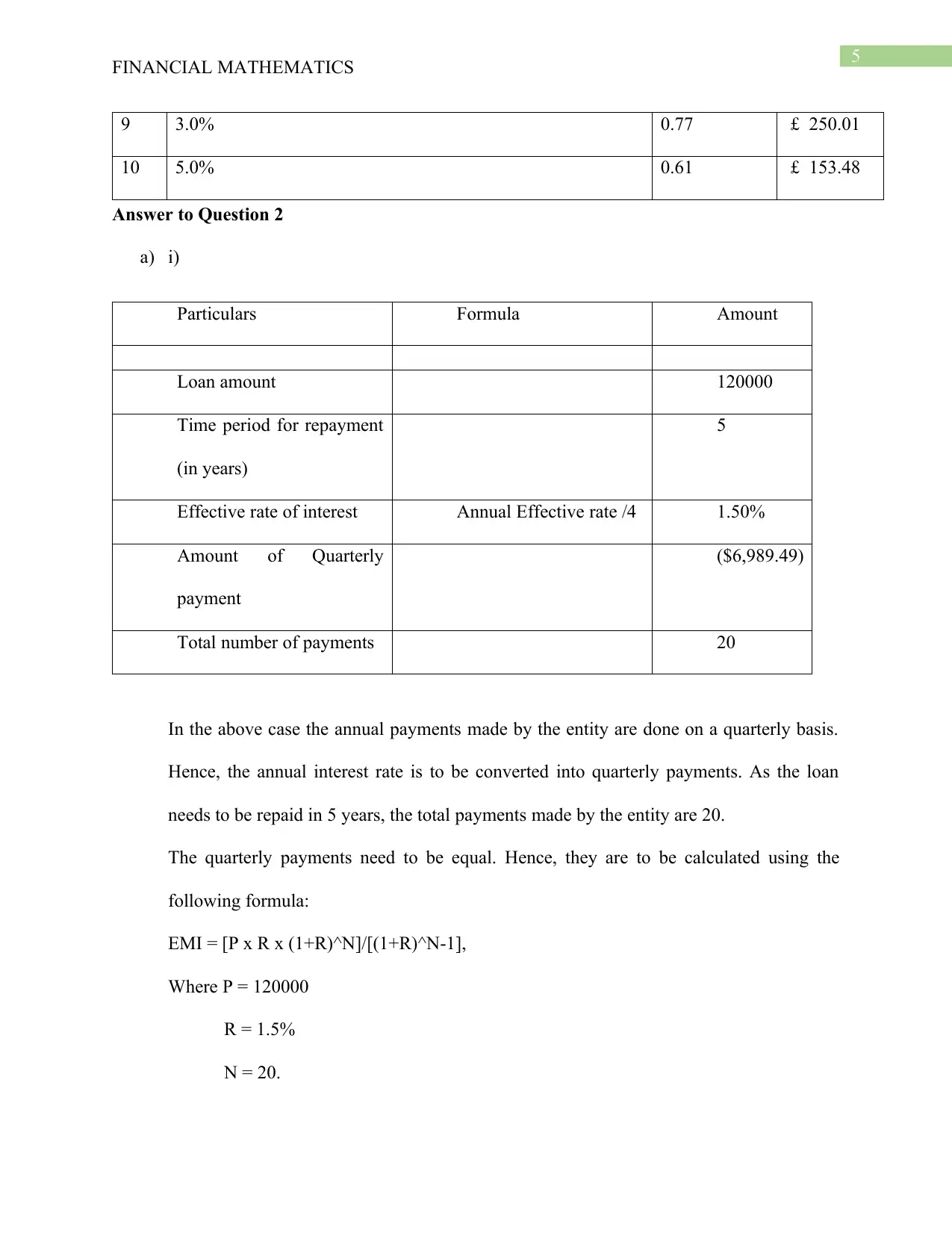

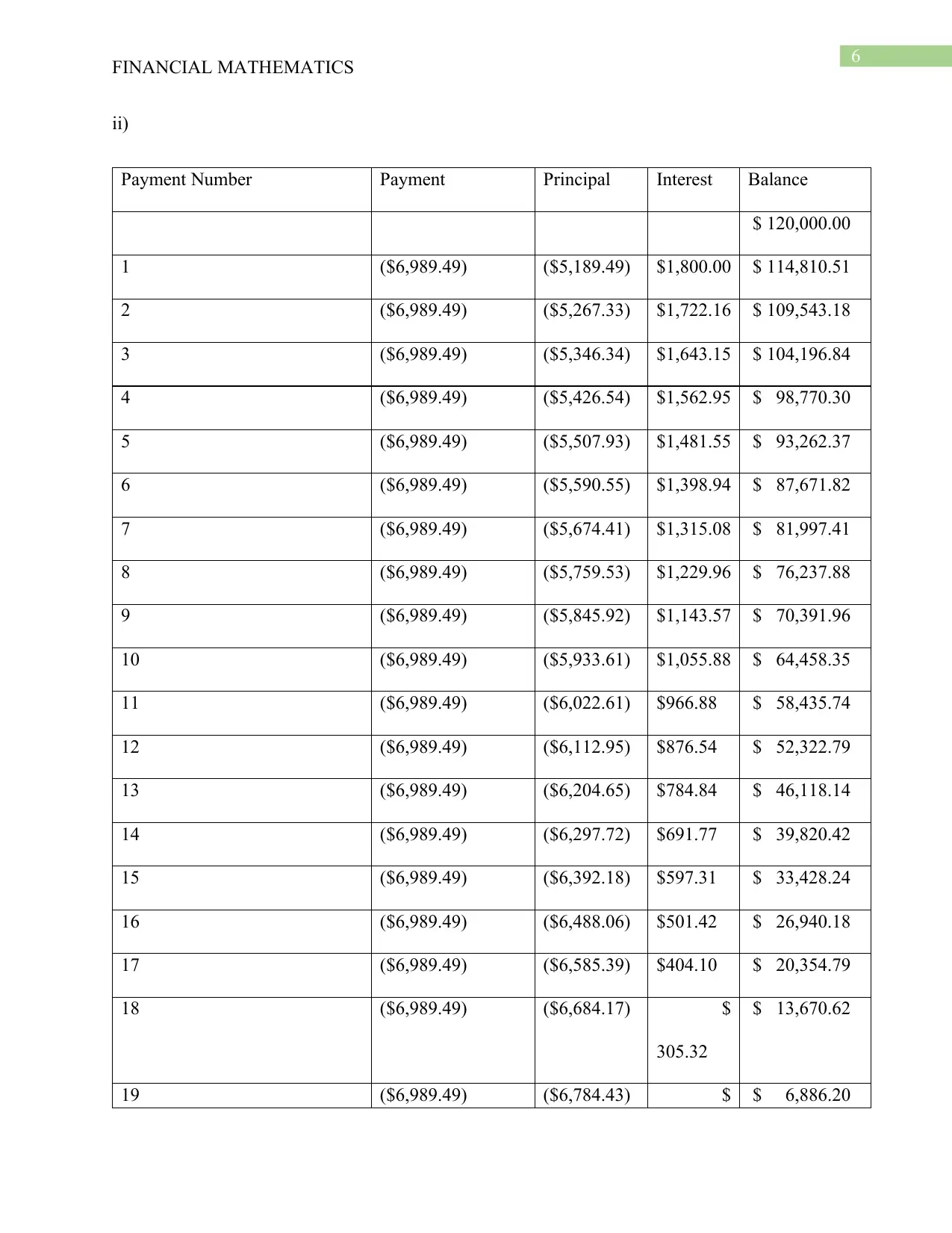

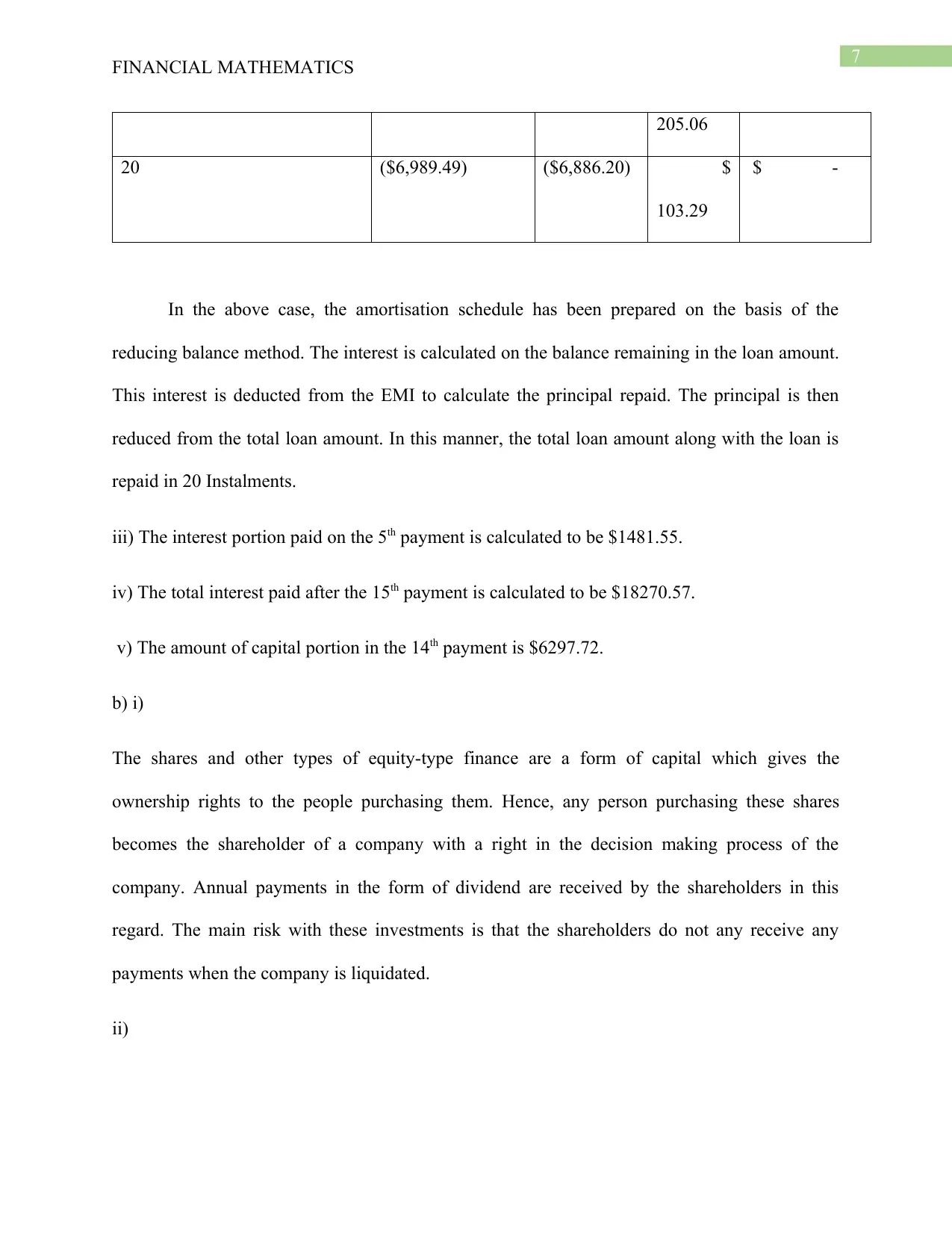

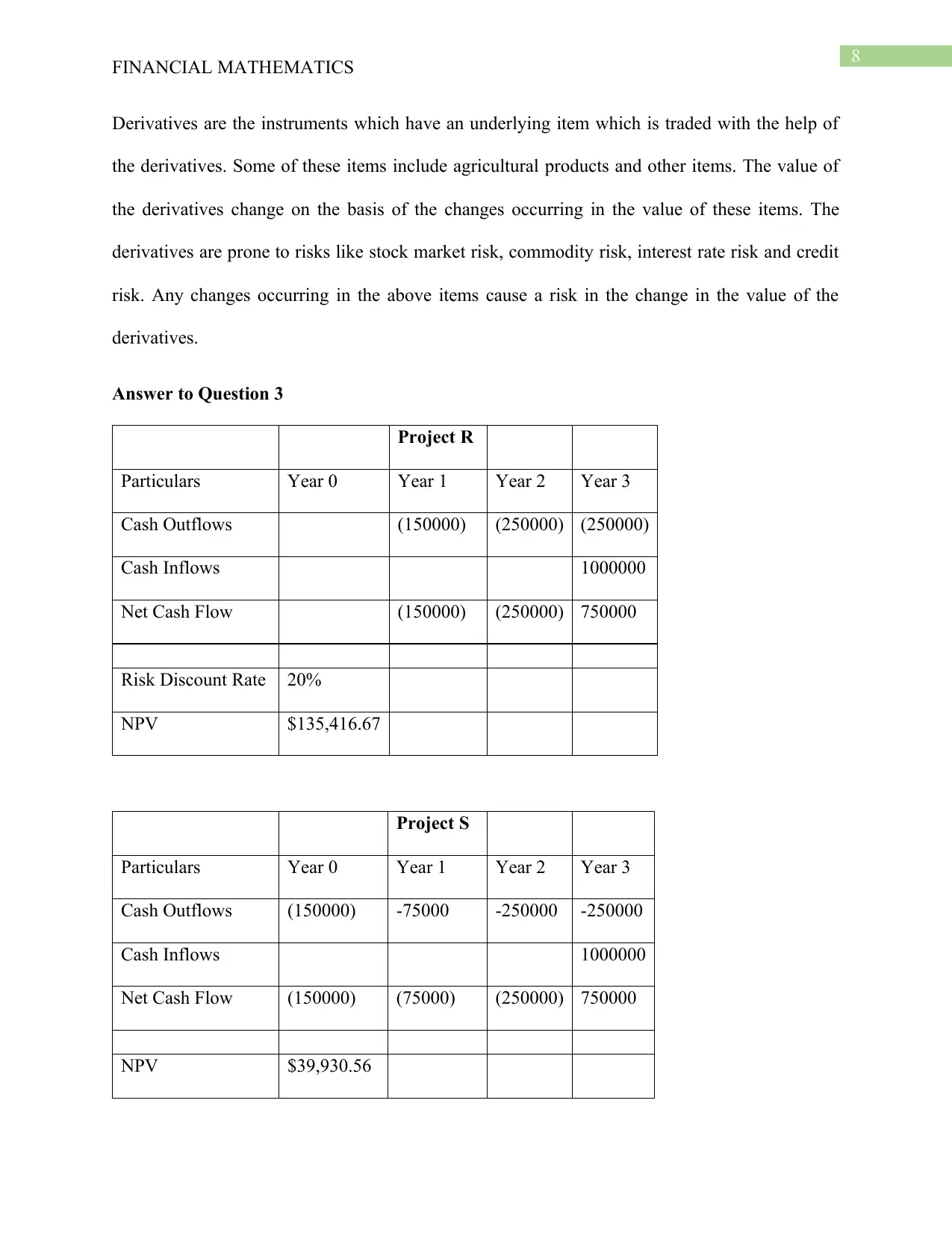

This financial mathematics assignment solution addresses several key concepts in finance. It begins with calculating the immediate payment from a discounted receivable, followed by comparing simple interest investments over different time periods. The solution then explores compound interest calculations with varying interest rates and compounding frequencies, and determines the present value of a series of payments. A loan amortization schedule is presented, along with calculations of interest and principal payments. The assignment also covers equity finance, derivatives, and project evaluation using NPV and IRR methods. The document includes detailed calculations and explanations for each problem, providing a comprehensive understanding of the financial principles involved. It offers a thorough analysis of financial concepts, making it a valuable resource for students studying finance. The assignment covers a range of topics, including time value of money, investment analysis, and financial instruments. The solution also includes a detailed breakdown of financial concepts.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.