Financial Analysis of Metro Inc.: Business and Competitor Review

VerifiedAdded on 2020/03/16

|30

|4882

|424

Report

AI Summary

This report offers a comprehensive financial analysis of Metro Inc., a major Canadian supermarket chain. It begins with an executive summary and an introduction to the report's objectives. The core of the report dissects Metro Inc.'s current business and financial health, utilizing ratio analysis to evaluate liquidity, solvency, and profitability. The analysis covers working capital, acid test ratio, current ratio, debt to total assets, times interest earned, and return on equity. Furthermore, the report critically analyzes the industrial sector and the financial performance of three key competitors: Loblaw Companies, Walmart, and Costco. A comparative assessment of Metro Inc.'s financial strengths and weaknesses against its competitors is provided. Finally, the report concludes with strategic recommendations for Metro Inc. aimed at improving its financial position, including suggestions for equity financing and debt management. The report references financial statements and data from 2015 and 2016 to support its analysis and findings.

Running head: FINANCIAL ANALYSIS OF METRO INC

Financial Analysis of Metro Inc

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Analysis of Metro Inc

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS OF METRO INC

Executive Summary:

The current report aims to select and evaluate the financial performance of Metro Inc,

which is a popular supermarket in the province of Canada. It is one of the giant food retailers in

the provinces of Ontario and Quebec in Canada. The report focuses on dissecting the existing

business and financial health of Metro Inc. In addition, it concentrates on providing critical

evaluation of the overall industry and the financial appraisal of the three chosen competitors that

include Loblaw Companies, Wal-Mart and Costco.

It has been assessed that Metro Inc has stable financial position and the investors could

buy shares for earning higher returns in future. In addition, Metro Inc has increased demand in

the market, as it could release its inventory at a faster rate compared to its competitors. Thus, it

needs to issue new equity shares for raising funds through equity financing to minimise the

overall debt burden.

Executive Summary:

The current report aims to select and evaluate the financial performance of Metro Inc,

which is a popular supermarket in the province of Canada. It is one of the giant food retailers in

the provinces of Ontario and Quebec in Canada. The report focuses on dissecting the existing

business and financial health of Metro Inc. In addition, it concentrates on providing critical

evaluation of the overall industry and the financial appraisal of the three chosen competitors that

include Loblaw Companies, Wal-Mart and Costco.

It has been assessed that Metro Inc has stable financial position and the investors could

buy shares for earning higher returns in future. In addition, Metro Inc has increased demand in

the market, as it could release its inventory at a faster rate compared to its competitors. Thus, it

needs to issue new equity shares for raising funds through equity financing to minimise the

overall debt burden.

2FINANCIAL ANALYSIS OF METRO INC

Table of Contents

Introduction:....................................................................................................................................3

Analysis of the current business and financial health of Metro Inc:...............................................3

Critical analysis of the industrial sector and financial evaluation of three competitors:...............18

Critical appraisal of the financial strengths and weaknesses of Metro Inc in comparison to the

chosen competitors:.......................................................................................................................19

Recommendations for Metro Inc:..................................................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

Appendices:...................................................................................................................................24

Table of Contents

Introduction:....................................................................................................................................3

Analysis of the current business and financial health of Metro Inc:...............................................3

Critical analysis of the industrial sector and financial evaluation of three competitors:...............18

Critical appraisal of the financial strengths and weaknesses of Metro Inc in comparison to the

chosen competitors:.......................................................................................................................19

Recommendations for Metro Inc:..................................................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

Appendices:...................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS OF METRO INC

Introduction:

The current report aims to select and evaluate the financial performance of Metro Inc,

which is a popular supermarket in the province of Canada. It is one of the giant food retailers in

the provinces of Ontario and Quebec in Canada (Corpo.metro.ca, 2017). The report focuses on

dissecting the existing business and financial health of Metro Inc. The second segment of the

report concentrates on providing critical evaluation of the overall industry and the financial

appraisal of the three chosen competitors that include Loblaw Companies, Wal-Mart and Costco.

The third and fourth segments of the paper focus on critical appraisal of the financial strengths

and weaknesses of Metro Inc in contrast to its rivals and the financial techniques used

respectively. Finally, the report sheds light on providing recommendations to Metro Inc that

would help in improving the overall financial position and performance of the organisation in the

Canadian market.

Analysis of the current business and financial health of Metro Inc:

Existing business scenario of Metro Inc:

It has been observed that Metro Inc would consolidate its five traditional banners of food

store in Ontario under the name Metro. It has lend support through investment of $200 million in

upgrading the store facilities, marketing and food offering for forming the largest grocery banner

of the nation (Newswire.ca, 2017). This decision has been undertaken to rebrand the name of the

organisation for capitalising on marketing and operating efficacies through unity of individual

strengths of the current banners in Ontario along with sharing effective practices with the stores

in Ontario and Quebec. Finally, it has earned revenue of around $11 billion having employee

Introduction:

The current report aims to select and evaluate the financial performance of Metro Inc,

which is a popular supermarket in the province of Canada. It is one of the giant food retailers in

the provinces of Ontario and Quebec in Canada (Corpo.metro.ca, 2017). The report focuses on

dissecting the existing business and financial health of Metro Inc. The second segment of the

report concentrates on providing critical evaluation of the overall industry and the financial

appraisal of the three chosen competitors that include Loblaw Companies, Wal-Mart and Costco.

The third and fourth segments of the paper focus on critical appraisal of the financial strengths

and weaknesses of Metro Inc in contrast to its rivals and the financial techniques used

respectively. Finally, the report sheds light on providing recommendations to Metro Inc that

would help in improving the overall financial position and performance of the organisation in the

Canadian market.

Analysis of the current business and financial health of Metro Inc:

Existing business scenario of Metro Inc:

It has been observed that Metro Inc would consolidate its five traditional banners of food

store in Ontario under the name Metro. It has lend support through investment of $200 million in

upgrading the store facilities, marketing and food offering for forming the largest grocery banner

of the nation (Newswire.ca, 2017). This decision has been undertaken to rebrand the name of the

organisation for capitalising on marketing and operating efficacies through unity of individual

strengths of the current banners in Ontario along with sharing effective practices with the stores

in Ontario and Quebec. Finally, it has earned revenue of around $11 billion having employee

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS OF METRO INC

base of 65,000, it has become the leader in the Canadian food sector (Brigham & Ehrhardt,

2013).

Financial health of Metro Inc:

The financial health of Metro Inc could be evaluated with the help of ratio analysis, as

this analysis helps in ascertaining the overall financial position and performance of an

organisation in its operating market (Batta, Ganguly & Rosett, 2014). The following categories

of ratios are considered for evaluating the financial health of Metro Inc:

Liquidity category:

In the words of Bodie (2013), liquidity ratios help in gauging the ability of an

organisation in paying debt obligations and safety margin through the computation of various

metrics. These metrics include the following:

Working capital

Acid test ratio

Current ratio

Cash current debt coverage

Receivables turnover

Average collection period (in days)

Inventory turnover

Days in inventory

Days payable

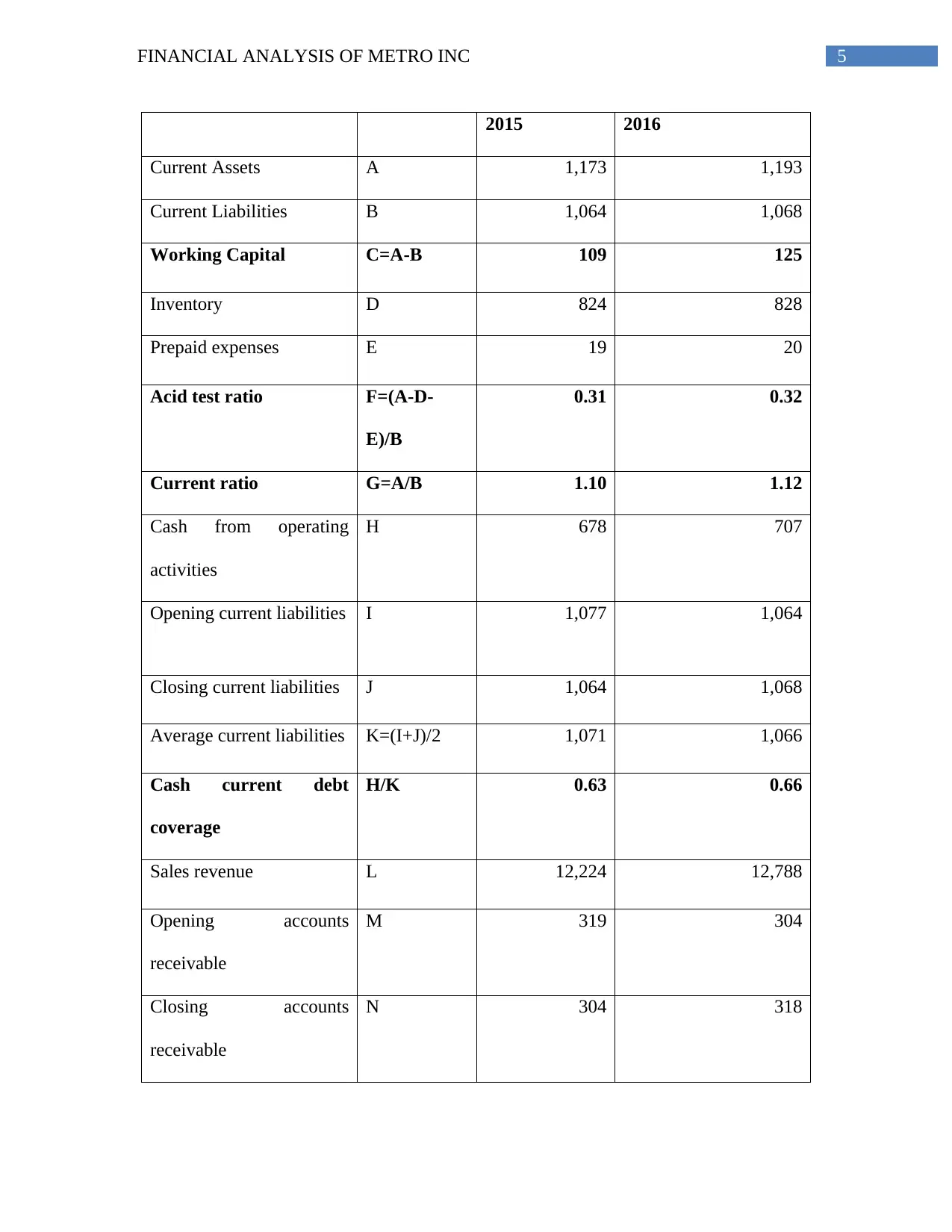

Particulars Details Metro Inc

base of 65,000, it has become the leader in the Canadian food sector (Brigham & Ehrhardt,

2013).

Financial health of Metro Inc:

The financial health of Metro Inc could be evaluated with the help of ratio analysis, as

this analysis helps in ascertaining the overall financial position and performance of an

organisation in its operating market (Batta, Ganguly & Rosett, 2014). The following categories

of ratios are considered for evaluating the financial health of Metro Inc:

Liquidity category:

In the words of Bodie (2013), liquidity ratios help in gauging the ability of an

organisation in paying debt obligations and safety margin through the computation of various

metrics. These metrics include the following:

Working capital

Acid test ratio

Current ratio

Cash current debt coverage

Receivables turnover

Average collection period (in days)

Inventory turnover

Days in inventory

Days payable

Particulars Details Metro Inc

5FINANCIAL ANALYSIS OF METRO INC

2015 2016

Current Assets A 1,173 1,193

Current Liabilities B 1,064 1,068

Working Capital C=A-B 109 125

Inventory D 824 828

Prepaid expenses E 19 20

Acid test ratio F=(A-D-

E)/B

0.31 0.32

Current ratio G=A/B 1.10 1.12

Cash from operating

activities

H 678 707

Opening current liabilities I 1,077 1,064

Closing current liabilities J 1,064 1,068

Average current liabilities K=(I+J)/2 1,071 1,066

Cash current debt

coverage

H/K 0.63 0.66

Sales revenue L 12,224 12,788

Opening accounts

receivable

M 319 304

Closing accounts

receivable

N 304 318

2015 2016

Current Assets A 1,173 1,193

Current Liabilities B 1,064 1,068

Working Capital C=A-B 109 125

Inventory D 824 828

Prepaid expenses E 19 20

Acid test ratio F=(A-D-

E)/B

0.31 0.32

Current ratio G=A/B 1.10 1.12

Cash from operating

activities

H 678 707

Opening current liabilities I 1,077 1,064

Closing current liabilities J 1,064 1,068

Average current liabilities K=(I+J)/2 1,071 1,066

Cash current debt

coverage

H/K 0.63 0.66

Sales revenue L 12,224 12,788

Opening accounts

receivable

M 319 304

Closing accounts

receivable

N 304 318

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS OF METRO INC

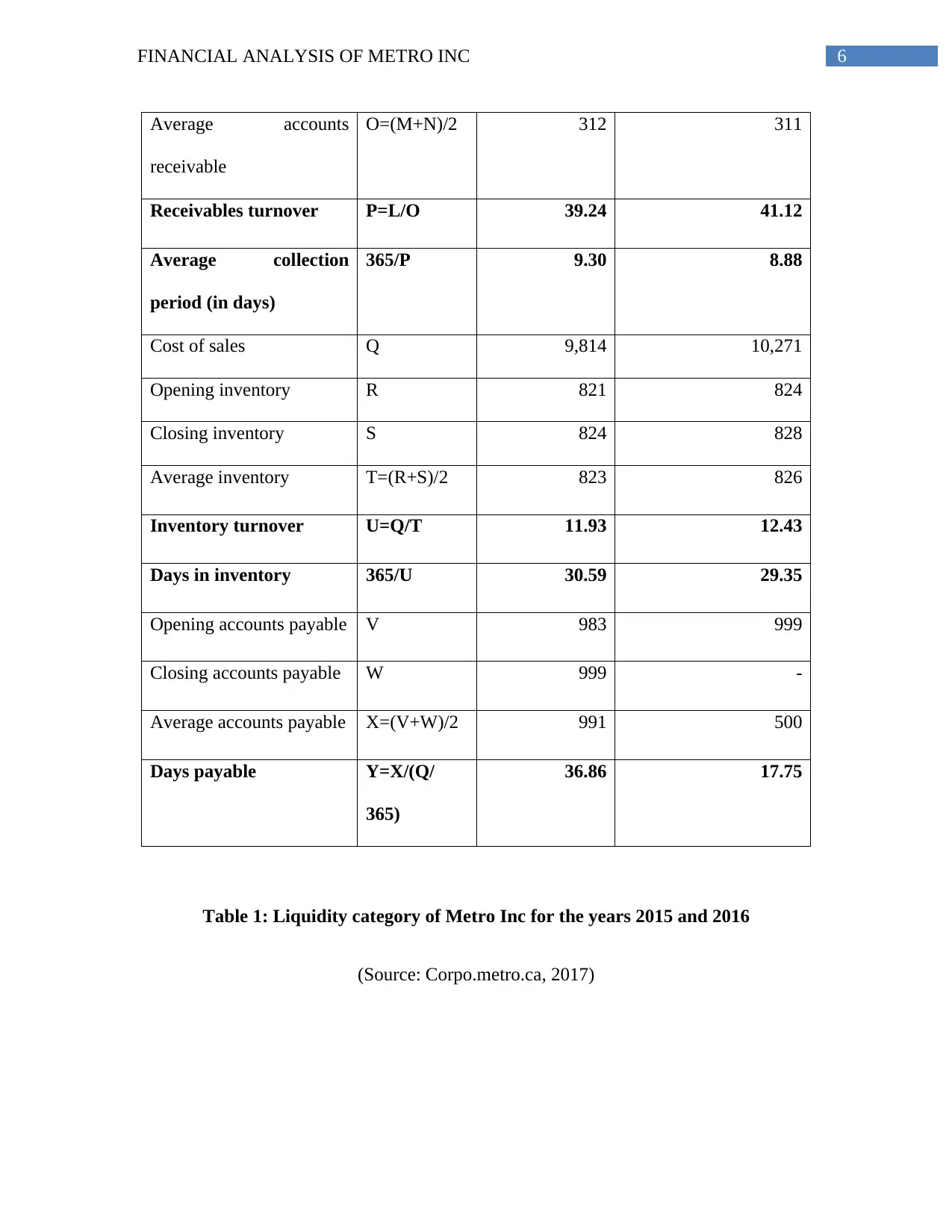

Average accounts

receivable

O=(M+N)/2 312 311

Receivables turnover P=L/O 39.24 41.12

Average collection

period (in days)

365/P 9.30 8.88

Cost of sales Q 9,814 10,271

Opening inventory R 821 824

Closing inventory S 824 828

Average inventory T=(R+S)/2 823 826

Inventory turnover U=Q/T 11.93 12.43

Days in inventory 365/U 30.59 29.35

Opening accounts payable V 983 999

Closing accounts payable W 999 -

Average accounts payable X=(V+W)/2 991 500

Days payable Y=X/(Q/

365)

36.86 17.75

Table 1: Liquidity category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

Average accounts

receivable

O=(M+N)/2 312 311

Receivables turnover P=L/O 39.24 41.12

Average collection

period (in days)

365/P 9.30 8.88

Cost of sales Q 9,814 10,271

Opening inventory R 821 824

Closing inventory S 824 828

Average inventory T=(R+S)/2 823 826

Inventory turnover U=Q/T 11.93 12.43

Days in inventory 365/U 30.59 29.35

Opening accounts payable V 983 999

Closing accounts payable W 999 -

Average accounts payable X=(V+W)/2 991 500

Days payable Y=X/(Q/

365)

36.86 17.75

Table 1: Liquidity category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS OF METRO INC

Working Capital Acid test ratio Current ratio Cash current

debt coverage

-

20

40

60

80

100

120

140

109.00

0.31 1.10 0.63

125.00

0.32 1.12 0.66

Liquidity category of Metro Inc

2015

2016

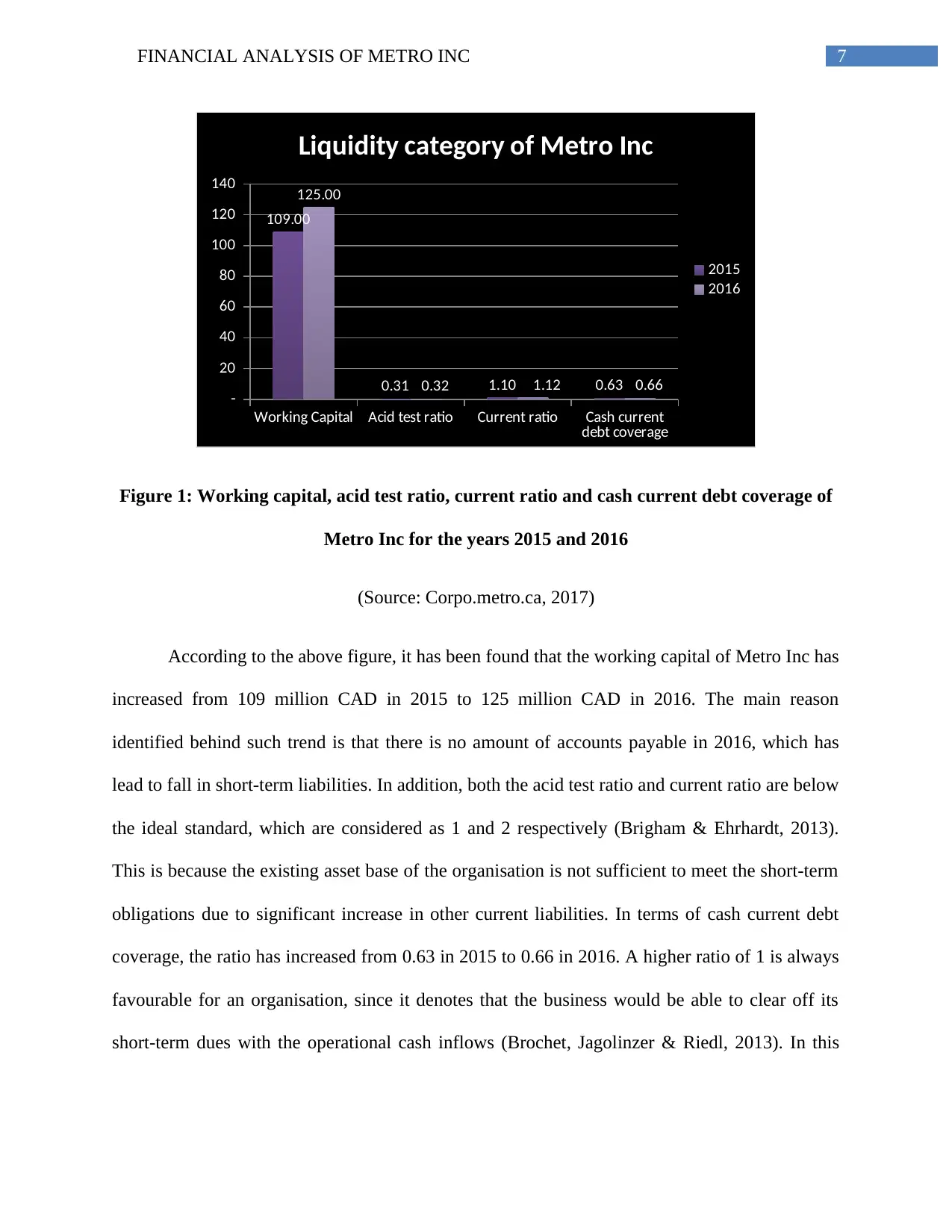

Figure 1: Working capital, acid test ratio, current ratio and cash current debt coverage of

Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

According to the above figure, it has been found that the working capital of Metro Inc has

increased from 109 million CAD in 2015 to 125 million CAD in 2016. The main reason

identified behind such trend is that there is no amount of accounts payable in 2016, which has

lead to fall in short-term liabilities. In addition, both the acid test ratio and current ratio are below

the ideal standard, which are considered as 1 and 2 respectively (Brigham & Ehrhardt, 2013).

This is because the existing asset base of the organisation is not sufficient to meet the short-term

obligations due to significant increase in other current liabilities. In terms of cash current debt

coverage, the ratio has increased from 0.63 in 2015 to 0.66 in 2016. A higher ratio of 1 is always

favourable for an organisation, since it denotes that the business would be able to clear off its

short-term dues with the operational cash inflows (Brochet, Jagolinzer & Riedl, 2013). In this

Working Capital Acid test ratio Current ratio Cash current

debt coverage

-

20

40

60

80

100

120

140

109.00

0.31 1.10 0.63

125.00

0.32 1.12 0.66

Liquidity category of Metro Inc

2015

2016

Figure 1: Working capital, acid test ratio, current ratio and cash current debt coverage of

Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

According to the above figure, it has been found that the working capital of Metro Inc has

increased from 109 million CAD in 2015 to 125 million CAD in 2016. The main reason

identified behind such trend is that there is no amount of accounts payable in 2016, which has

lead to fall in short-term liabilities. In addition, both the acid test ratio and current ratio are below

the ideal standard, which are considered as 1 and 2 respectively (Brigham & Ehrhardt, 2013).

This is because the existing asset base of the organisation is not sufficient to meet the short-term

obligations due to significant increase in other current liabilities. In terms of cash current debt

coverage, the ratio has increased from 0.63 in 2015 to 0.66 in 2016. A higher ratio of 1 is always

favourable for an organisation, since it denotes that the business would be able to clear off its

short-term dues with the operational cash inflows (Brochet, Jagolinzer & Riedl, 2013). In this

8FINANCIAL ANALYSIS OF METRO INC

case, it is below the desired standard, which denotes the struggling liquidity position of Metro

Inc.

Receivables

turnover Average

collection

period (in

days)

Inventory

turnover Days in

inventory Days payable

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00 39.24

9.30 11.93

30.59

36.86

41.12

8.88 12.43

29.35

17.75

Liquidity category of Metro Inc

2015

2016

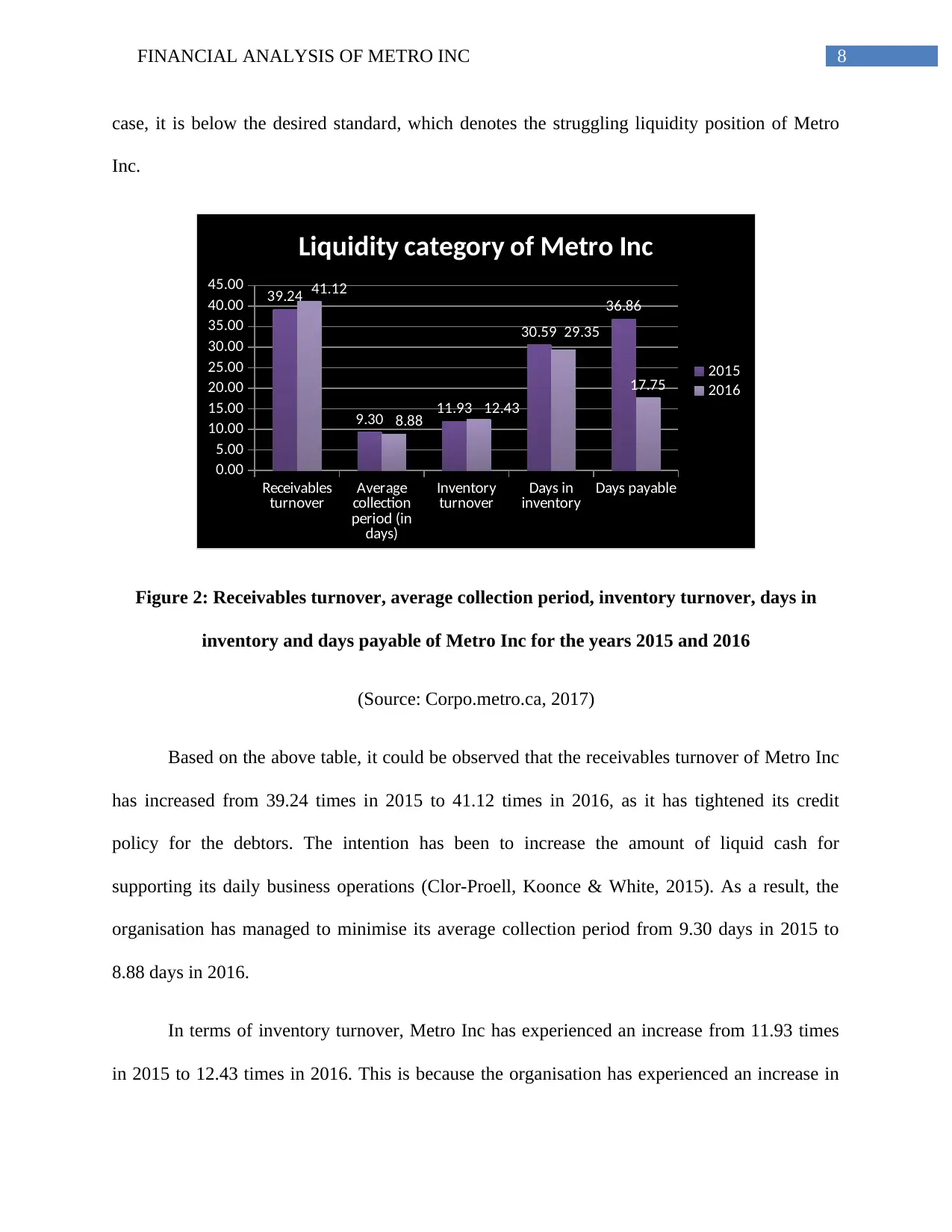

Figure 2: Receivables turnover, average collection period, inventory turnover, days in

inventory and days payable of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

Based on the above table, it could be observed that the receivables turnover of Metro Inc

has increased from 39.24 times in 2015 to 41.12 times in 2016, as it has tightened its credit

policy for the debtors. The intention has been to increase the amount of liquid cash for

supporting its daily business operations (Clor-Proell, Koonce & White, 2015). As a result, the

organisation has managed to minimise its average collection period from 9.30 days in 2015 to

8.88 days in 2016.

In terms of inventory turnover, Metro Inc has experienced an increase from 11.93 times

in 2015 to 12.43 times in 2016. This is because the organisation has experienced an increase in

case, it is below the desired standard, which denotes the struggling liquidity position of Metro

Inc.

Receivables

turnover Average

collection

period (in

days)

Inventory

turnover Days in

inventory Days payable

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00 39.24

9.30 11.93

30.59

36.86

41.12

8.88 12.43

29.35

17.75

Liquidity category of Metro Inc

2015

2016

Figure 2: Receivables turnover, average collection period, inventory turnover, days in

inventory and days payable of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

Based on the above table, it could be observed that the receivables turnover of Metro Inc

has increased from 39.24 times in 2015 to 41.12 times in 2016, as it has tightened its credit

policy for the debtors. The intention has been to increase the amount of liquid cash for

supporting its daily business operations (Clor-Proell, Koonce & White, 2015). As a result, the

organisation has managed to minimise its average collection period from 9.30 days in 2015 to

8.88 days in 2016.

In terms of inventory turnover, Metro Inc has experienced an increase from 11.93 times

in 2015 to 12.43 times in 2016. This is because the organisation has experienced an increase in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS OF METRO INC

overall revenue base due to rise in market demand and this has helped in releasing the inventory

at a faster rate (Coates IV, 2014). As a result, Metro Inc has managed to discharge its inventory

from 30.59 days in 2015 to 29.35 days in 2016. However, in terms of payables, the creditors are

not willing to accept any delay in payments due to the declining market reputation. In addition,

the overall debt burden of the organisation has resulted in loss of trust for the investors and thus,

Metro Inc has to clear their payments within shorter timeframe (Weygandt, Kimmel & Kieso,

2015).

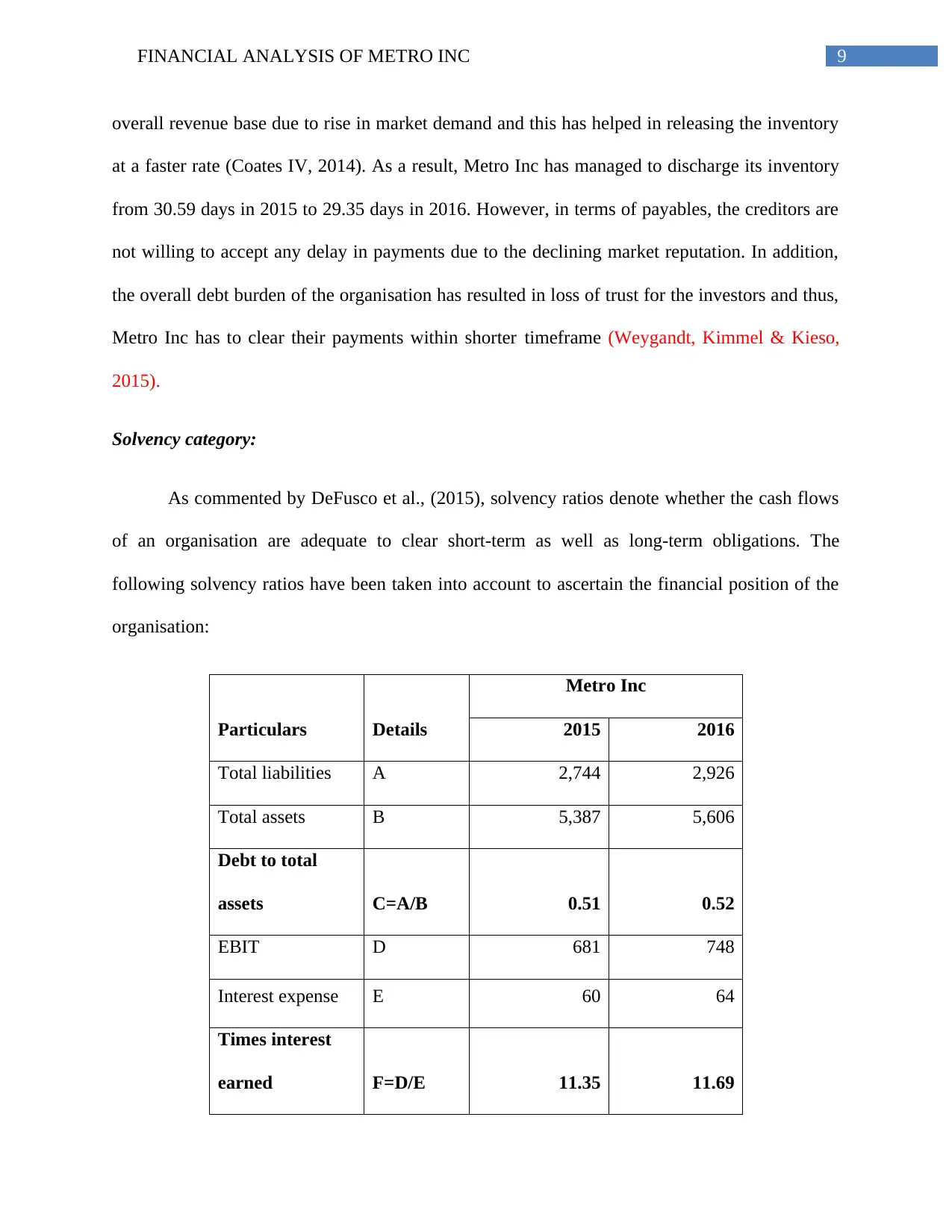

Solvency category:

As commented by DeFusco et al., (2015), solvency ratios denote whether the cash flows

of an organisation are adequate to clear short-term as well as long-term obligations. The

following solvency ratios have been taken into account to ascertain the financial position of the

organisation:

Particulars Details

Metro Inc

2015 2016

Total liabilities A 2,744 2,926

Total assets B 5,387 5,606

Debt to total

assets C=A/B 0.51 0.52

EBIT D 681 748

Interest expense E 60 64

Times interest

earned F=D/E 11.35 11.69

overall revenue base due to rise in market demand and this has helped in releasing the inventory

at a faster rate (Coates IV, 2014). As a result, Metro Inc has managed to discharge its inventory

from 30.59 days in 2015 to 29.35 days in 2016. However, in terms of payables, the creditors are

not willing to accept any delay in payments due to the declining market reputation. In addition,

the overall debt burden of the organisation has resulted in loss of trust for the investors and thus,

Metro Inc has to clear their payments within shorter timeframe (Weygandt, Kimmel & Kieso,

2015).

Solvency category:

As commented by DeFusco et al., (2015), solvency ratios denote whether the cash flows

of an organisation are adequate to clear short-term as well as long-term obligations. The

following solvency ratios have been taken into account to ascertain the financial position of the

organisation:

Particulars Details

Metro Inc

2015 2016

Total liabilities A 2,744 2,926

Total assets B 5,387 5,606

Debt to total

assets C=A/B 0.51 0.52

EBIT D 681 748

Interest expense E 60 64

Times interest

earned F=D/E 11.35 11.69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS OF METRO INC

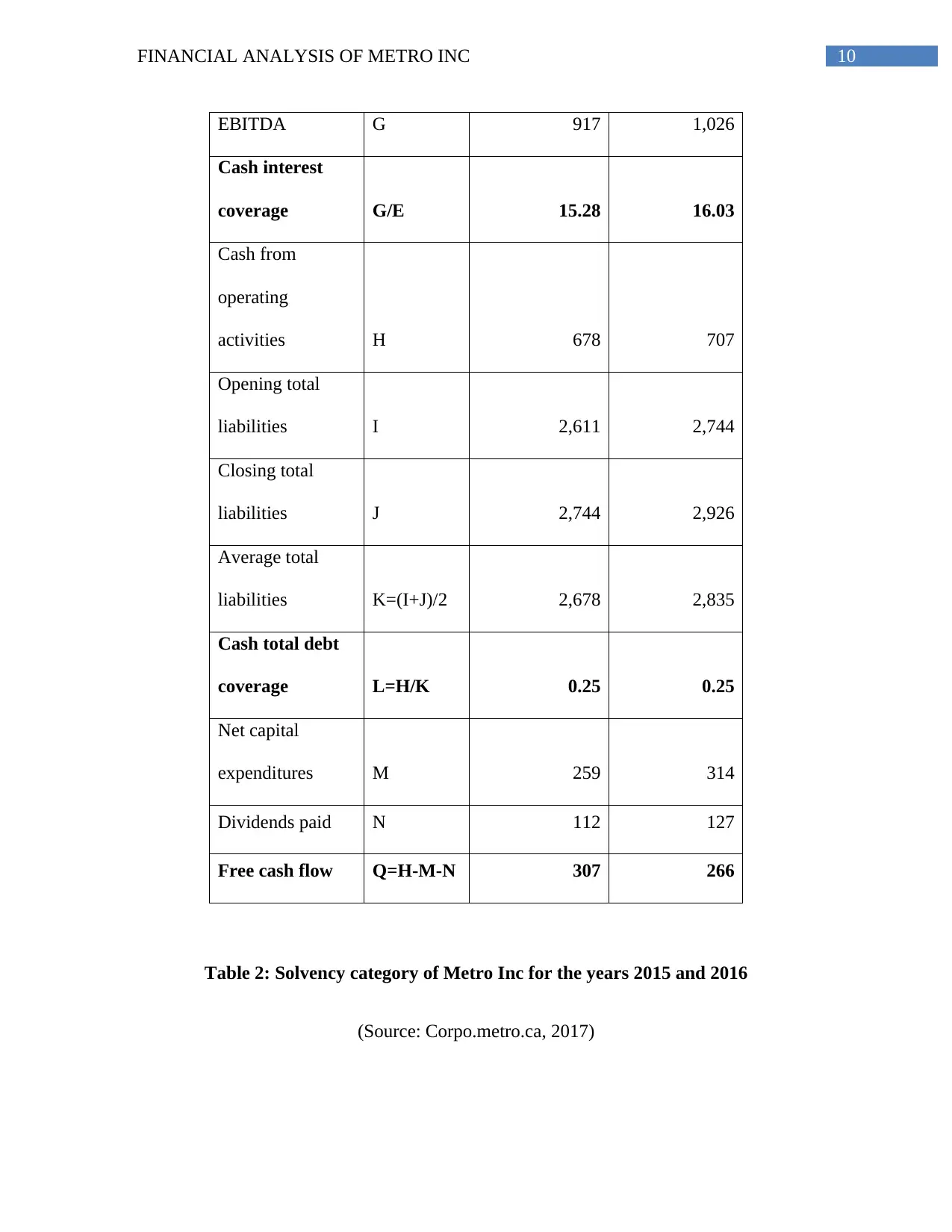

EBITDA G 917 1,026

Cash interest

coverage G/E 15.28 16.03

Cash from

operating

activities H 678 707

Opening total

liabilities I 2,611 2,744

Closing total

liabilities J 2,744 2,926

Average total

liabilities K=(I+J)/2 2,678 2,835

Cash total debt

coverage L=H/K 0.25 0.25

Net capital

expenditures M 259 314

Dividends paid N 112 127

Free cash flow Q=H-M-N 307 266

Table 2: Solvency category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

EBITDA G 917 1,026

Cash interest

coverage G/E 15.28 16.03

Cash from

operating

activities H 678 707

Opening total

liabilities I 2,611 2,744

Closing total

liabilities J 2,744 2,926

Average total

liabilities K=(I+J)/2 2,678 2,835

Cash total debt

coverage L=H/K 0.25 0.25

Net capital

expenditures M 259 314

Dividends paid N 112 127

Free cash flow Q=H-M-N 307 266

Table 2: Solvency category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

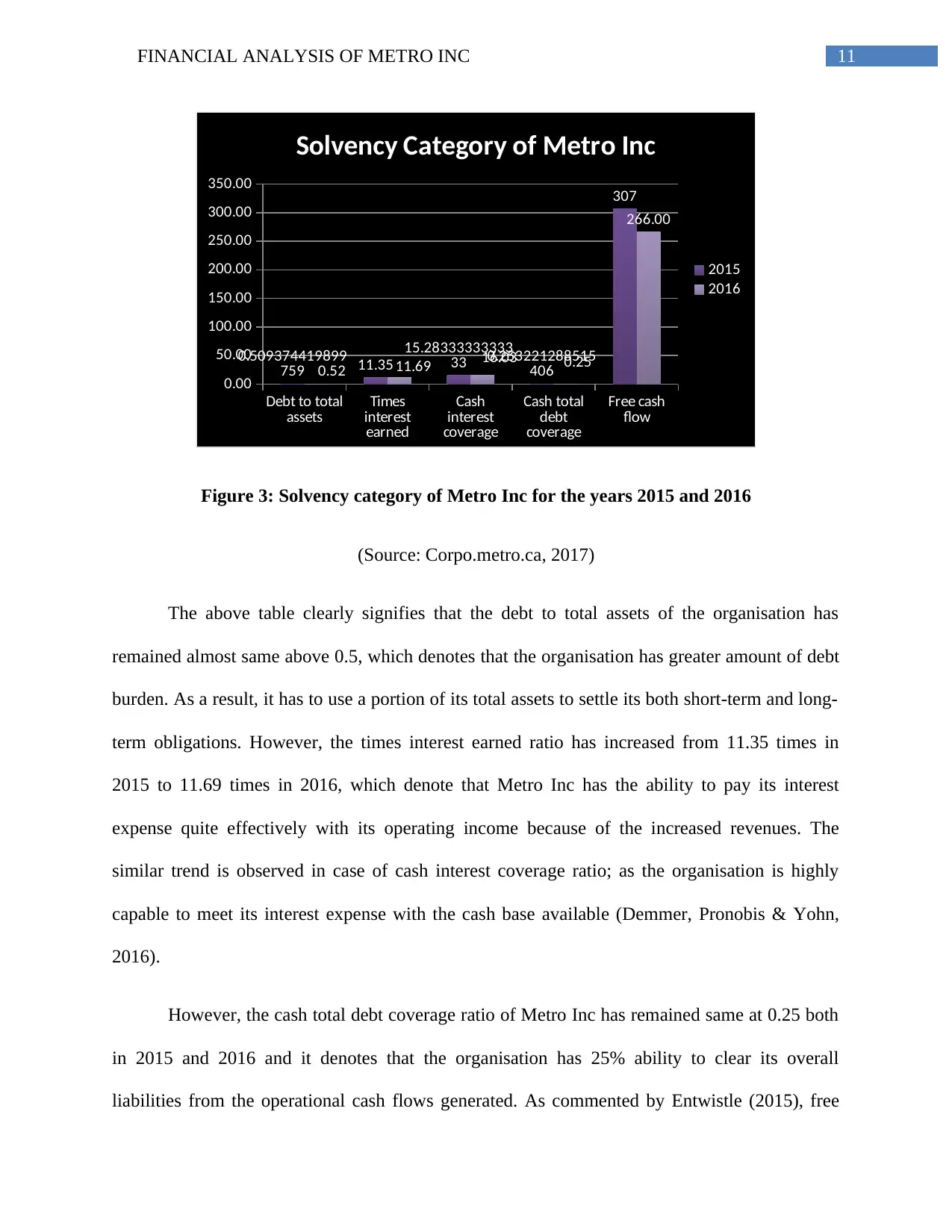

11FINANCIAL ANALYSIS OF METRO INC

Debt to total

assets Times

interest

earned

Cash

interest

coverage

Cash total

debt

coverage

Free cash

flow

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

0.509374419899

759 11.35

15.28333333333

33 0.253221288515

406

307

0.52 11.69 16.03 0.25

266.00

Solvency Category of Metro Inc

2015

2016

Figure 3: Solvency category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

The above table clearly signifies that the debt to total assets of the organisation has

remained almost same above 0.5, which denotes that the organisation has greater amount of debt

burden. As a result, it has to use a portion of its total assets to settle its both short-term and long-

term obligations. However, the times interest earned ratio has increased from 11.35 times in

2015 to 11.69 times in 2016, which denote that Metro Inc has the ability to pay its interest

expense quite effectively with its operating income because of the increased revenues. The

similar trend is observed in case of cash interest coverage ratio; as the organisation is highly

capable to meet its interest expense with the cash base available (Demmer, Pronobis & Yohn,

2016).

However, the cash total debt coverage ratio of Metro Inc has remained same at 0.25 both

in 2015 and 2016 and it denotes that the organisation has 25% ability to clear its overall

liabilities from the operational cash flows generated. As commented by Entwistle (2015), free

Debt to total

assets Times

interest

earned

Cash

interest

coverage

Cash total

debt

coverage

Free cash

flow

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

0.509374419899

759 11.35

15.28333333333

33 0.253221288515

406

307

0.52 11.69 16.03 0.25

266.00

Solvency Category of Metro Inc

2015

2016

Figure 3: Solvency category of Metro Inc for the years 2015 and 2016

(Source: Corpo.metro.ca, 2017)

The above table clearly signifies that the debt to total assets of the organisation has

remained almost same above 0.5, which denotes that the organisation has greater amount of debt

burden. As a result, it has to use a portion of its total assets to settle its both short-term and long-

term obligations. However, the times interest earned ratio has increased from 11.35 times in

2015 to 11.69 times in 2016, which denote that Metro Inc has the ability to pay its interest

expense quite effectively with its operating income because of the increased revenues. The

similar trend is observed in case of cash interest coverage ratio; as the organisation is highly

capable to meet its interest expense with the cash base available (Demmer, Pronobis & Yohn,

2016).

However, the cash total debt coverage ratio of Metro Inc has remained same at 0.25 both

in 2015 and 2016 and it denotes that the organisation has 25% ability to clear its overall

liabilities from the operational cash flows generated. As commented by Entwistle (2015), free

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.