Intermediate Financial Reporting: M&S Plc Performance Analysis

VerifiedAdded on 2021/01/01

|15

|2998

|300

Report

AI Summary

This report provides a comprehensive financial analysis of Marks & Spencer Plc (M&S) over a three-year period, focusing on key performance indicators. The analysis includes a detailed examination of profitability ratios (ROCE, ROE, asset turnover, gross profit margin, and net profit margin), liquidity ratios (current ratio and quick ratio), management ratios (inventory turnover, trade receivables collection period, and trade payables payment period), solvency ratios (debt to equity, debt to capital employed, and interest cover ratio), and investment ratios (EPS, P/E ratio, earning yield and dividend cover). The report interprets the trends and implications of each ratio, offering insights into the company's financial health, efficiency, and ability to meet its obligations. Furthermore, it explores cash flow and share price movements, providing a holistic view of M&S Plc's financial performance and position within the retail sector. The report also considers the competitive environment and its impact on the company's financial outcomes, offering recommendations for improvement.

INTERMEDIATE FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

The financial statements are to be analysed so that performance can be analysed. M&S

Plc will be analysed on the basis of profitability, liquidity, solvency, efficiency, management and

shareholder positions for last three years. The share price movements along with cash flows

movements will be identified as well. Hence, financial position of organisation will be analysed.

The financial statements are to be analysed so that performance can be analysed. M&S

Plc will be analysed on the basis of profitability, liquidity, solvency, efficiency, management and

shareholder positions for last three years. The share price movements along with cash flows

movements will be identified as well. Hence, financial position of organisation will be analysed.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Analysing financial performance of Marks & Spencer Plc for last three years..........................1

1. Profitability (Refer Appendix 1).............................................................................................1

2. Liquidity (Refer Appendix 2)..................................................................................................2

3. Management (Refer Appendix 3)............................................................................................3

4. Solvency (Refer Appendix 4)..................................................................................................4

5. Investment (Refer Appendix 5)...............................................................................................4

6. Cash Flow movement over the years......................................................................................5

7. Share Price movement and performance.................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

1. Profitability Ratios................................................................................................................11

2. Liquidity Ratios.....................................................................................................................11

3. Management Ratios...............................................................................................................11

4. Solvency Ratios.....................................................................................................................12

5. Investment Ratios..................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Analysing financial performance of Marks & Spencer Plc for last three years..........................1

1. Profitability (Refer Appendix 1).............................................................................................1

2. Liquidity (Refer Appendix 2)..................................................................................................2

3. Management (Refer Appendix 3)............................................................................................3

4. Solvency (Refer Appendix 4)..................................................................................................4

5. Investment (Refer Appendix 5)...............................................................................................4

6. Cash Flow movement over the years......................................................................................5

7. Share Price movement and performance.................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

1. Profitability Ratios................................................................................................................11

2. Liquidity Ratios.....................................................................................................................11

3. Management Ratios...............................................................................................................11

4. Solvency Ratios.....................................................................................................................12

5. Investment Ratios..................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial analysis is vital aspect for assessing overall financial position of company.

Present report deals with M&S Plc, giant in retail sector of the UK having worldwide operations

which will be analysed regarding its past three years' performance on the basis of ratio analysis.

Several ratios will be computed for getting clear picture whether corporate is adequately

performing or not. On the other side, cash flow movements for past years will be analysed. Share

prices movements and performance in the market will be identified through historical share

prices included by preparing area chart. Thus, overall performance of organisation will be

analysed for providing better aspect to stakeholders for taking decisions.

MAIN BODY

Analysing financial performance of Marks & Spencer Plc for last three years

1. Profitability (Refer Appendix 1)

Interpretation-

The profitability ratios are computed which provides clarity regarding the position of

M&S Plc for last three years. ROCE was 10.44 % in 2014 which decreased to 9.86 % in 2015

and further minimised to 7.68 % in 2016 showing that firm is unable to utilise assets for getting

operating profits in effective manner. On the other hand, ROE is another useful ratio implying

how investment made by shareholders are utilised by company up to a great extent. The ratio

was 20.14 % in 2014, reduced to 16.47 % in 2015 and further decreased to 12.25 %. This shows

that M&S Plc is not effectively using equity for getting higher net profits. While, Asset turnover

ratio is also calculated for showing how effectively average assets are utilised for garnering sales

in the best manner possible. Higher the ratio, better for organisation. Ratio was 1.33 % in 2014

which decreased to 1.28 % in next year and reached 1.27 % highlighting that organisation is not

using assets adequately to generate sales (Annual Report of Marks and Spencer Group Plc. 2014-

15. 2015).

It can be analysed that M&S Plc had low asset turnover ratio which it should take care

into account and properly utilise its assets for producing sales in a better manner. This will

provide it with higher sales and assets will offer higher sales quite effectually. On the other hand,

gross profit ratio is also being calculated showing that figure was 37.50 % in 2014 which

increased to 38.70 % in the year 2015. Furthermore, it climbed to 39.10 % in later year showing

that organisation is properly analysing expenses and reducing it for maximising gross profits.

1

Financial analysis is vital aspect for assessing overall financial position of company.

Present report deals with M&S Plc, giant in retail sector of the UK having worldwide operations

which will be analysed regarding its past three years' performance on the basis of ratio analysis.

Several ratios will be computed for getting clear picture whether corporate is adequately

performing or not. On the other side, cash flow movements for past years will be analysed. Share

prices movements and performance in the market will be identified through historical share

prices included by preparing area chart. Thus, overall performance of organisation will be

analysed for providing better aspect to stakeholders for taking decisions.

MAIN BODY

Analysing financial performance of Marks & Spencer Plc for last three years

1. Profitability (Refer Appendix 1)

Interpretation-

The profitability ratios are computed which provides clarity regarding the position of

M&S Plc for last three years. ROCE was 10.44 % in 2014 which decreased to 9.86 % in 2015

and further minimised to 7.68 % in 2016 showing that firm is unable to utilise assets for getting

operating profits in effective manner. On the other hand, ROE is another useful ratio implying

how investment made by shareholders are utilised by company up to a great extent. The ratio

was 20.14 % in 2014, reduced to 16.47 % in 2015 and further decreased to 12.25 %. This shows

that M&S Plc is not effectively using equity for getting higher net profits. While, Asset turnover

ratio is also calculated for showing how effectively average assets are utilised for garnering sales

in the best manner possible. Higher the ratio, better for organisation. Ratio was 1.33 % in 2014

which decreased to 1.28 % in next year and reached 1.27 % highlighting that organisation is not

using assets adequately to generate sales (Annual Report of Marks and Spencer Group Plc. 2014-

15. 2015).

It can be analysed that M&S Plc had low asset turnover ratio which it should take care

into account and properly utilise its assets for producing sales in a better manner. This will

provide it with higher sales and assets will offer higher sales quite effectually. On the other hand,

gross profit ratio is also being calculated showing that figure was 37.50 % in 2014 which

increased to 38.70 % in the year 2015. Furthermore, it climbed to 39.10 % in later year showing

that organisation is properly analysing expenses and reducing it for maximising gross profits.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This has led to year after year elevation in gross profit margin in the best manner possible

manner. On the other hand, net profit margin has been calculated for last three years. It was

5.09% and 4.72 % in 2014 and 2015 consecutively. While, it further decreased to 3.85 % in 2016

implying that organisation is not reducing its overall expenses which has led to reduction in

every year of company (Annual Report of Marks and Spencer Group Plc. 2015-16. 2016). Thus,

it is required to effectively enhance profitability position as firm's performance is not appropriate

in relation to past years. The competitive environment can be analysed because due to difficult

trading conditions in the international market, net profit was decreased to 3.85 % in 2016 and

continued fall in profits are ascertained. However, strong growth in food market has saved

company in further deducting its position with regards to profits.

2. Liquidity (Refer Appendix 2)

Interpretation-

The liquidity ratios provide clear picture of firm's liquidity position in meeting out its

liabilities of short-term period. The most important ratios belonging to this category are current

ratio and quick ratio. Current ratio means how efficiently company can meet its short-term

liabilities that lapse within one year time period. Standard current ratio is 2:1 which means that

for every one liability, there should be 2 assets highlighting the safe position of organisation in

effectively paying out its obligations in the best way possible (Greco, Figueira and Ehrgott,

2016). The ratio of M&S Plc was 0.58 in 2014, less than the standard range of current ratio.

However, it reached to 0.69 in 2015 and remain unchanged in next year as well. This means that

current ratio of corporate is below par and it could face difficulties in getting obligations paid-off

in stipulated time period.

Quick ratio is another useful ratio in analysing liquidity position of company with

relation to extreme liquid assets. It is helpful for getting into account how effectively M&S Plc

can pay-off its liabilities with liquid or quick assets. The term quick assets is arrived after

deducting prepaid expenses and inventories from the current assets. The standard quick ratio is

1:1 which highlights that for every 1 liability, firm should have 1 liquid asset, then only it will be

able to make for its obligations in effectual manner and no shortcomings will arise (Li, 2015).

The figure was 0.21 in 2014 which increased to 0.25 in 2015. Moreover, in later year, quick ratio

of M&S Plc increased by 0.02 and reached 0.27. This clearly indicates that firm is able to

improve upon its quick ratio, but it will face difficulties in meeting extreme short-term

2

manner. On the other hand, net profit margin has been calculated for last three years. It was

5.09% and 4.72 % in 2014 and 2015 consecutively. While, it further decreased to 3.85 % in 2016

implying that organisation is not reducing its overall expenses which has led to reduction in

every year of company (Annual Report of Marks and Spencer Group Plc. 2015-16. 2016). Thus,

it is required to effectively enhance profitability position as firm's performance is not appropriate

in relation to past years. The competitive environment can be analysed because due to difficult

trading conditions in the international market, net profit was decreased to 3.85 % in 2016 and

continued fall in profits are ascertained. However, strong growth in food market has saved

company in further deducting its position with regards to profits.

2. Liquidity (Refer Appendix 2)

Interpretation-

The liquidity ratios provide clear picture of firm's liquidity position in meeting out its

liabilities of short-term period. The most important ratios belonging to this category are current

ratio and quick ratio. Current ratio means how efficiently company can meet its short-term

liabilities that lapse within one year time period. Standard current ratio is 2:1 which means that

for every one liability, there should be 2 assets highlighting the safe position of organisation in

effectively paying out its obligations in the best way possible (Greco, Figueira and Ehrgott,

2016). The ratio of M&S Plc was 0.58 in 2014, less than the standard range of current ratio.

However, it reached to 0.69 in 2015 and remain unchanged in next year as well. This means that

current ratio of corporate is below par and it could face difficulties in getting obligations paid-off

in stipulated time period.

Quick ratio is another useful ratio in analysing liquidity position of company with

relation to extreme liquid assets. It is helpful for getting into account how effectively M&S Plc

can pay-off its liabilities with liquid or quick assets. The term quick assets is arrived after

deducting prepaid expenses and inventories from the current assets. The standard quick ratio is

1:1 which highlights that for every 1 liability, firm should have 1 liquid asset, then only it will be

able to make for its obligations in effectual manner and no shortcomings will arise (Li, 2015).

The figure was 0.21 in 2014 which increased to 0.25 in 2015. Moreover, in later year, quick ratio

of M&S Plc increased by 0.02 and reached 0.27. This clearly indicates that firm is able to

improve upon its quick ratio, but it will face difficulties in meeting extreme short-term

2

obligations in the right manner at right time. The competitive environment can be assessed as

short-term obligations are difficult for accomplishing trading conditions as conversion of current

assets are complex in clothing and home and organisation needs to focus priorly so as to attain

good growth and pay for obligations in effective manner.

3. Management (Refer Appendix 3)

Interpretation-

Management ratios provide clarity with regards to efficiency of entire management in

meeting requirements of department. Inventory turnover ratio indicates how efficiently and

frequently replenish stock for easing-off production and maximise the same. It can be analysed

that ratio was 7.98 in 2014 which decreased to 7.69 in later year, however, it reached to 8.05 in

2016. Hence, company's position is overall good. While, trade receivables collection period

highlights how appropriately and quickly, M&S Plc attains outstanding amount of debtors in

effective way. Lower the ratio, better for the organisation (Valickova, Havranek and Horvath,

2015). Ratio was 87.80 days in 2014 which reduced to 82.33 in 2015 signifying that company is

able to gain quicker amount from debtors. While, it increased in 2016 to 88.15 showing

inefficiency of taking amount from debtors.

On the other side, trade payables payment period shows how quickly suppliers are paid

by company quite effectually. Lesser the ratio, better position of company. Ratio was 60 days in

2014 which slightly elevated in next year to 60.92 days. However, it then alleviated to 56.49 in

2016 showing that M&S Plc is able to make timely and quick payments to suppliers on credit

goods owned by it. This means that management ratios of company is good and it is able to pay

outstanding amount to suppliers and creditors quite effectually. Moreover, regarding stock ratio,

it is needed that organisation should quickly replenish inventories so as to protect it from getting

spoiled (Damodaran, 2016). This is required in order to reduce or eliminate wastage of resources

with ease. While, organisation should more quickly pay to suppliers in order to avail discounts.

However, overall position of M&S Plc is adequate as classified with the help of ratios.

Competitive environment has affected management of M&S Plc as trade receivables are

not providing quicker payments to company because rival business are providing more credit

period for payments in effective manner. However, it is paying quickly to its suppliers which is

reflected in trade payables payment period which is decreased.

3

short-term obligations are difficult for accomplishing trading conditions as conversion of current

assets are complex in clothing and home and organisation needs to focus priorly so as to attain

good growth and pay for obligations in effective manner.

3. Management (Refer Appendix 3)

Interpretation-

Management ratios provide clarity with regards to efficiency of entire management in

meeting requirements of department. Inventory turnover ratio indicates how efficiently and

frequently replenish stock for easing-off production and maximise the same. It can be analysed

that ratio was 7.98 in 2014 which decreased to 7.69 in later year, however, it reached to 8.05 in

2016. Hence, company's position is overall good. While, trade receivables collection period

highlights how appropriately and quickly, M&S Plc attains outstanding amount of debtors in

effective way. Lower the ratio, better for the organisation (Valickova, Havranek and Horvath,

2015). Ratio was 87.80 days in 2014 which reduced to 82.33 in 2015 signifying that company is

able to gain quicker amount from debtors. While, it increased in 2016 to 88.15 showing

inefficiency of taking amount from debtors.

On the other side, trade payables payment period shows how quickly suppliers are paid

by company quite effectually. Lesser the ratio, better position of company. Ratio was 60 days in

2014 which slightly elevated in next year to 60.92 days. However, it then alleviated to 56.49 in

2016 showing that M&S Plc is able to make timely and quick payments to suppliers on credit

goods owned by it. This means that management ratios of company is good and it is able to pay

outstanding amount to suppliers and creditors quite effectually. Moreover, regarding stock ratio,

it is needed that organisation should quickly replenish inventories so as to protect it from getting

spoiled (Damodaran, 2016). This is required in order to reduce or eliminate wastage of resources

with ease. While, organisation should more quickly pay to suppliers in order to avail discounts.

However, overall position of M&S Plc is adequate as classified with the help of ratios.

Competitive environment has affected management of M&S Plc as trade receivables are

not providing quicker payments to company because rival business are providing more credit

period for payments in effective manner. However, it is paying quickly to its suppliers which is

reflected in trade payables payment period which is decreased.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Solvency (Refer Appendix 4)

Interpretation-

The solvency ratios are computed for M&S Plc highlighting whether it is able to find

perfect strike and balance in capital structure or not. It can be ascertained that debt to equity ratio

shows how much debt is available in respect to equity, termed as shareholder's investment

(Crowder and Reganold, 2015). The standard ratio is 0.40 which means that 40 % of debt should

be used in capital structure and remaining 60 % with equity showing perfect solvency of

company in meeting long-term obligations in the best manner possible. Ratio was 1.92 in 2014

which decreased to 1.56 in next year and further to 1.46 in 2016. It implies that organisation is

steadily reducing debt in its capital structure and moving to use equity.

Debt to capital employed means that debt being available to company in respect to total

capital employed (deducting current liabilities from total assets). This ratio should be below 0.40

as it is ideal ratio. The figure were 0.94 in 2014 reduced to 0.82 and 0.79 in 2015 and 2016

consecutively. This shows that ratio over the years is decreased and M&S Plc is able to take

good advantage of both debt and equity in judicious manner. However, debt is much higher and

it seems that organisation might default in paying its debt obligations Apart from it, interest

cover ratio is being calculated highlighting how easily organisation can make payments of

interest expenses on outstanding debt.

Lower the ratio, higher burden of debt on company and chances of bankruptcy. The ratio

of M&S Plc was 4.17 in 2014 which increased to 5.14 in 2015. However, it decreased to 4.20 in

2016, thus, it will some difficulty in making interest payments on debt. It can be ascertained that

solvency position of organisation should be enhanced so that it may be able to attain good

balance in capital structure (Edwards, Schwab and Shevlin, 2015). Over-reliance on debt must be

ignored and company should rely on equity also in order to reduce debt burden in effective

manner. The competitive environment of M&S Plc can be analysed and solvency position of

company has become inadequate because of its over-reliance on debt for making up its capital

structure. This has also led to increase in cost of debt. It is needed to prepare strategy and issue

more shares and attain equity for capital requirements.

5. Investment (Refer Appendix 5)

Interpretation-

4

Interpretation-

The solvency ratios are computed for M&S Plc highlighting whether it is able to find

perfect strike and balance in capital structure or not. It can be ascertained that debt to equity ratio

shows how much debt is available in respect to equity, termed as shareholder's investment

(Crowder and Reganold, 2015). The standard ratio is 0.40 which means that 40 % of debt should

be used in capital structure and remaining 60 % with equity showing perfect solvency of

company in meeting long-term obligations in the best manner possible. Ratio was 1.92 in 2014

which decreased to 1.56 in next year and further to 1.46 in 2016. It implies that organisation is

steadily reducing debt in its capital structure and moving to use equity.

Debt to capital employed means that debt being available to company in respect to total

capital employed (deducting current liabilities from total assets). This ratio should be below 0.40

as it is ideal ratio. The figure were 0.94 in 2014 reduced to 0.82 and 0.79 in 2015 and 2016

consecutively. This shows that ratio over the years is decreased and M&S Plc is able to take

good advantage of both debt and equity in judicious manner. However, debt is much higher and

it seems that organisation might default in paying its debt obligations Apart from it, interest

cover ratio is being calculated highlighting how easily organisation can make payments of

interest expenses on outstanding debt.

Lower the ratio, higher burden of debt on company and chances of bankruptcy. The ratio

of M&S Plc was 4.17 in 2014 which increased to 5.14 in 2015. However, it decreased to 4.20 in

2016, thus, it will some difficulty in making interest payments on debt. It can be ascertained that

solvency position of organisation should be enhanced so that it may be able to attain good

balance in capital structure (Edwards, Schwab and Shevlin, 2015). Over-reliance on debt must be

ignored and company should rely on equity also in order to reduce debt burden in effective

manner. The competitive environment of M&S Plc can be analysed and solvency position of

company has become inadequate because of its over-reliance on debt for making up its capital

structure. This has also led to increase in cost of debt. It is needed to prepare strategy and issue

more shares and attain equity for capital requirements.

5. Investment (Refer Appendix 5)

Interpretation-

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be interpreted that EPS shows portion of profit of company which is allocated to

each share of stock. Higher EPS highlights profitability of organisation. Ratio was 0.64 in 2014

which decreased to 0.59 and further reduced to 0.49 in 2016. It highlights that profitability

position of company is declined. On the other hand, Price to earnings ratio means amount

investor is willing to pay for particular share (Francis and et.al., 2015). Ratio was 5.52 in 2014

which maximised to 7.64 in 2015 and it decreased to 7.02. Thus, it was adequate for M&S Plc

despite of low ratio in 2016 compared to previous years.

Earning yield is reverse of price to earnings ratio as it provides percentage of each

amount of money invested in stock that was gained by it. Ratio in 2014 was 0.18 % in 2014

which reached to 0.13 % in 2015 and increased to 0.14 % in later year. This shows that earnings

are improved despite it decreased in 2015. Other one is dividend cover which measures number

of times, company could easily pay dividends to its stockholders. It reflects higher profits earned

which are then disbursed to shareholders in respect of their shareholdings.

Dividend cover was 16.41 times in 2014 which decreased to 14.76 times in next year.

Furthermore, figure was degraded to 11 times in the financial year 2016. This shows that firm is

unable to offer frequent dividends to shareholders because of low earnings (Roberts, 2015).

Dividend yield shows amount of dividends relative to its market value per share in effective

manner. Higher the dividend yield, better for the investors to get adequate dividends. In 2014,

figure was 3.65 % which increased to 4.17 % in further year. In addition to this, figure reached to

5.66 % highlighting that company satisfies its shareholders and keeping in mind market

fluctuations, good dividend yield ratio is earned. Competitive environment of company can be

analysed as EPS is declined and other investment ratios are declined because of currency risks

and market risk which has affected company's stock price in the market where it operates.

Dividends are to paid and for that M&S Plc has to outperform in its every segments for

generating profits.

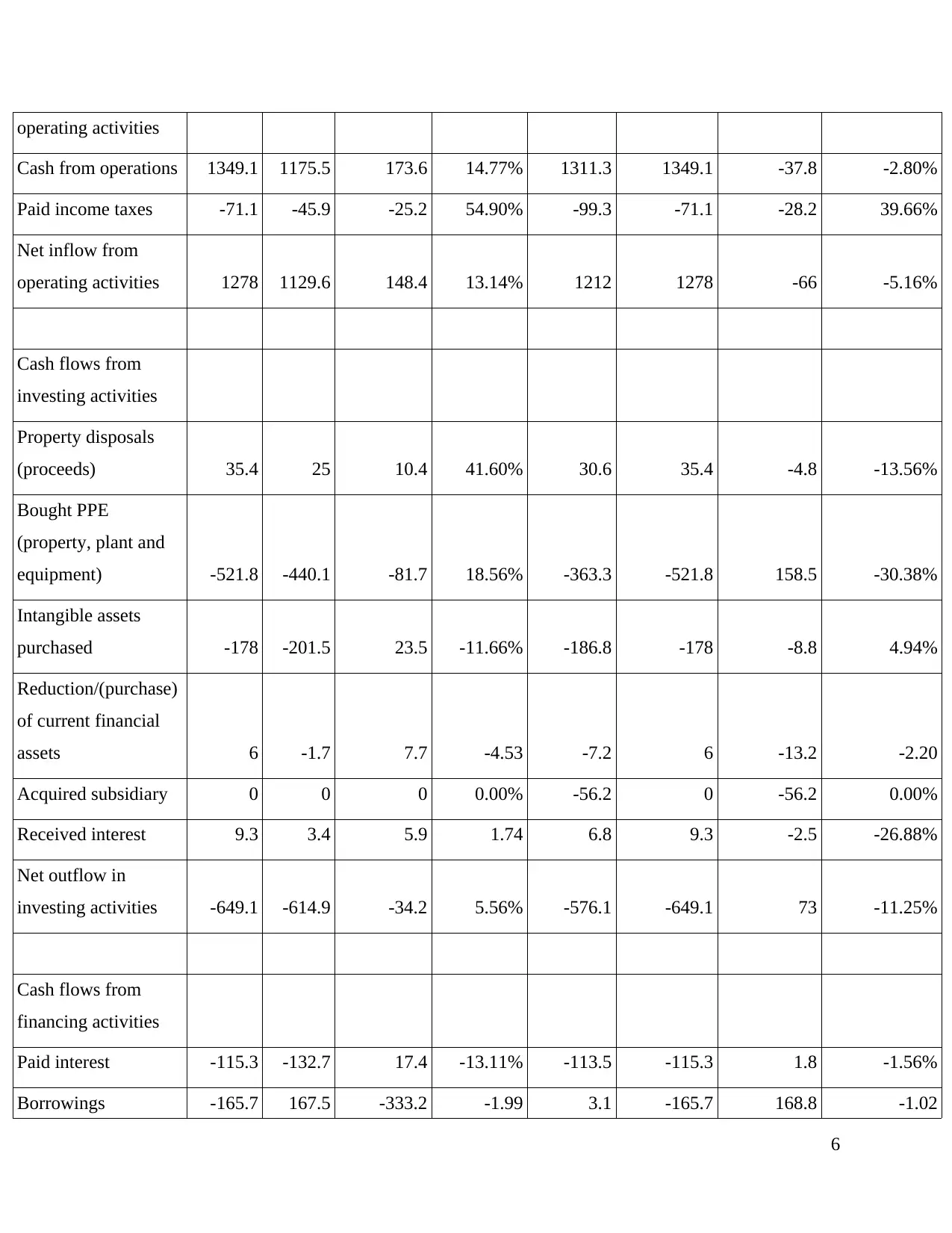

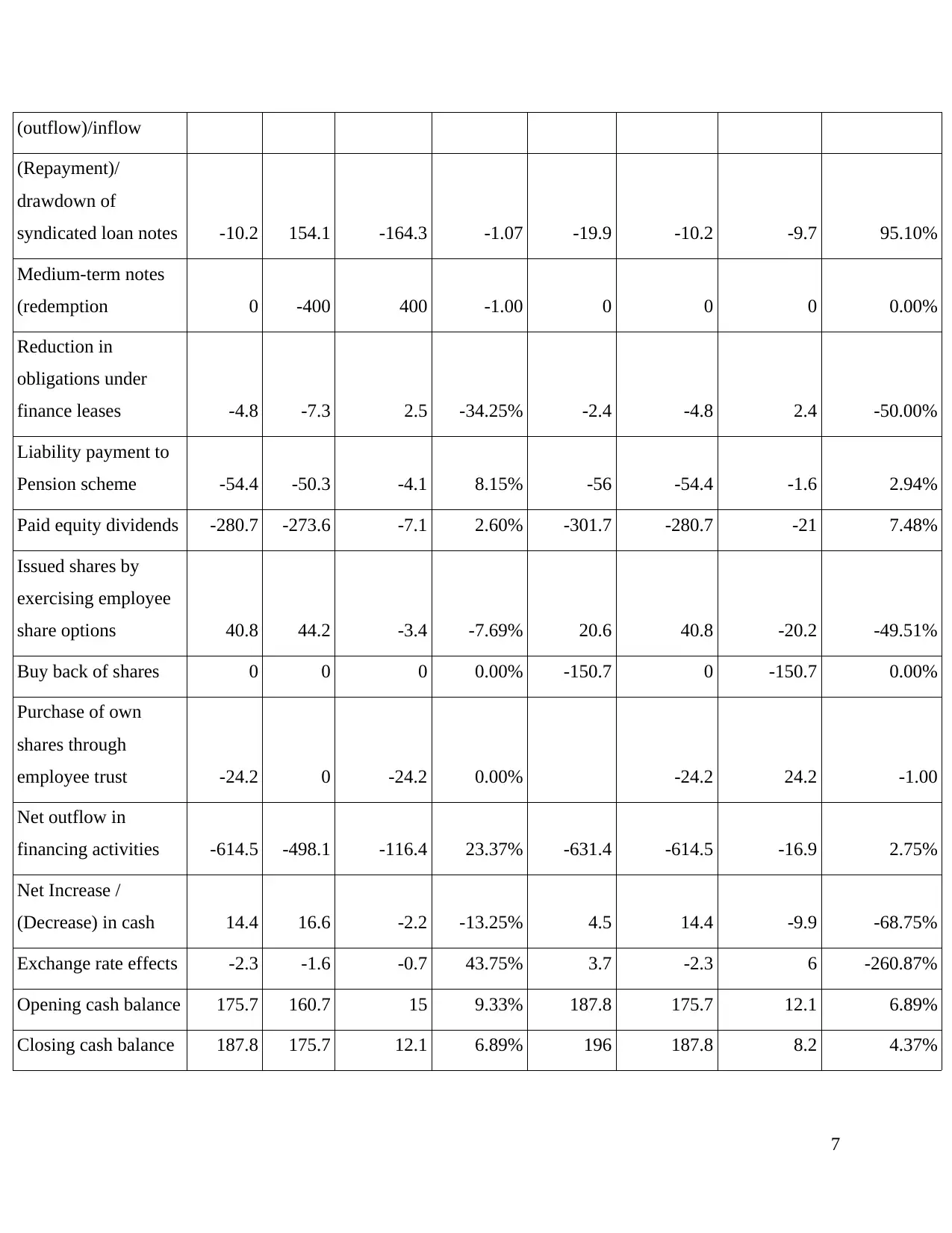

6. Cash Flow movement over the years

Horizontal Analysis of Cash Flow Statement for Marks and Spencer Plc

Increase / (Decrease) Increase / (Decrease)

Particulars 2015 2014 Amount % change 2016 2015 Amount % change

Cash flows from

5

each share of stock. Higher EPS highlights profitability of organisation. Ratio was 0.64 in 2014

which decreased to 0.59 and further reduced to 0.49 in 2016. It highlights that profitability

position of company is declined. On the other hand, Price to earnings ratio means amount

investor is willing to pay for particular share (Francis and et.al., 2015). Ratio was 5.52 in 2014

which maximised to 7.64 in 2015 and it decreased to 7.02. Thus, it was adequate for M&S Plc

despite of low ratio in 2016 compared to previous years.

Earning yield is reverse of price to earnings ratio as it provides percentage of each

amount of money invested in stock that was gained by it. Ratio in 2014 was 0.18 % in 2014

which reached to 0.13 % in 2015 and increased to 0.14 % in later year. This shows that earnings

are improved despite it decreased in 2015. Other one is dividend cover which measures number

of times, company could easily pay dividends to its stockholders. It reflects higher profits earned

which are then disbursed to shareholders in respect of their shareholdings.

Dividend cover was 16.41 times in 2014 which decreased to 14.76 times in next year.

Furthermore, figure was degraded to 11 times in the financial year 2016. This shows that firm is

unable to offer frequent dividends to shareholders because of low earnings (Roberts, 2015).

Dividend yield shows amount of dividends relative to its market value per share in effective

manner. Higher the dividend yield, better for the investors to get adequate dividends. In 2014,

figure was 3.65 % which increased to 4.17 % in further year. In addition to this, figure reached to

5.66 % highlighting that company satisfies its shareholders and keeping in mind market

fluctuations, good dividend yield ratio is earned. Competitive environment of company can be

analysed as EPS is declined and other investment ratios are declined because of currency risks

and market risk which has affected company's stock price in the market where it operates.

Dividends are to paid and for that M&S Plc has to outperform in its every segments for

generating profits.

6. Cash Flow movement over the years

Horizontal Analysis of Cash Flow Statement for Marks and Spencer Plc

Increase / (Decrease) Increase / (Decrease)

Particulars 2015 2014 Amount % change 2016 2015 Amount % change

Cash flows from

5

operating activities

Cash from operations 1349.1 1175.5 173.6 14.77% 1311.3 1349.1 -37.8 -2.80%

Paid income taxes -71.1 -45.9 -25.2 54.90% -99.3 -71.1 -28.2 39.66%

Net inflow from

operating activities 1278 1129.6 148.4 13.14% 1212 1278 -66 -5.16%

Cash flows from

investing activities

Property disposals

(proceeds) 35.4 25 10.4 41.60% 30.6 35.4 -4.8 -13.56%

Bought PPE

(property, plant and

equipment) -521.8 -440.1 -81.7 18.56% -363.3 -521.8 158.5 -30.38%

Intangible assets

purchased -178 -201.5 23.5 -11.66% -186.8 -178 -8.8 4.94%

Reduction/(purchase)

of current financial

assets 6 -1.7 7.7 -4.53 -7.2 6 -13.2 -2.20

Acquired subsidiary 0 0 0 0.00% -56.2 0 -56.2 0.00%

Received interest 9.3 3.4 5.9 1.74 6.8 9.3 -2.5 -26.88%

Net outflow in

investing activities -649.1 -614.9 -34.2 5.56% -576.1 -649.1 73 -11.25%

Cash flows from

financing activities

Paid interest -115.3 -132.7 17.4 -13.11% -113.5 -115.3 1.8 -1.56%

Borrowings -165.7 167.5 -333.2 -1.99 3.1 -165.7 168.8 -1.02

6

Cash from operations 1349.1 1175.5 173.6 14.77% 1311.3 1349.1 -37.8 -2.80%

Paid income taxes -71.1 -45.9 -25.2 54.90% -99.3 -71.1 -28.2 39.66%

Net inflow from

operating activities 1278 1129.6 148.4 13.14% 1212 1278 -66 -5.16%

Cash flows from

investing activities

Property disposals

(proceeds) 35.4 25 10.4 41.60% 30.6 35.4 -4.8 -13.56%

Bought PPE

(property, plant and

equipment) -521.8 -440.1 -81.7 18.56% -363.3 -521.8 158.5 -30.38%

Intangible assets

purchased -178 -201.5 23.5 -11.66% -186.8 -178 -8.8 4.94%

Reduction/(purchase)

of current financial

assets 6 -1.7 7.7 -4.53 -7.2 6 -13.2 -2.20

Acquired subsidiary 0 0 0 0.00% -56.2 0 -56.2 0.00%

Received interest 9.3 3.4 5.9 1.74 6.8 9.3 -2.5 -26.88%

Net outflow in

investing activities -649.1 -614.9 -34.2 5.56% -576.1 -649.1 73 -11.25%

Cash flows from

financing activities

Paid interest -115.3 -132.7 17.4 -13.11% -113.5 -115.3 1.8 -1.56%

Borrowings -165.7 167.5 -333.2 -1.99 3.1 -165.7 168.8 -1.02

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(outflow)/inflow

(Repayment)/

drawdown of

syndicated loan notes -10.2 154.1 -164.3 -1.07 -19.9 -10.2 -9.7 95.10%

Medium-term notes

(redemption 0 -400 400 -1.00 0 0 0 0.00%

Reduction in

obligations under

finance leases -4.8 -7.3 2.5 -34.25% -2.4 -4.8 2.4 -50.00%

Liability payment to

Pension scheme -54.4 -50.3 -4.1 8.15% -56 -54.4 -1.6 2.94%

Paid equity dividends -280.7 -273.6 -7.1 2.60% -301.7 -280.7 -21 7.48%

Issued shares by

exercising employee

share options 40.8 44.2 -3.4 -7.69% 20.6 40.8 -20.2 -49.51%

Buy back of shares 0 0 0 0.00% -150.7 0 -150.7 0.00%

Purchase of own

shares through

employee trust -24.2 0 -24.2 0.00% -24.2 24.2 -1.00

Net outflow in

financing activities -614.5 -498.1 -116.4 23.37% -631.4 -614.5 -16.9 2.75%

Net Increase /

(Decrease) in cash 14.4 16.6 -2.2 -13.25% 4.5 14.4 -9.9 -68.75%

Exchange rate effects -2.3 -1.6 -0.7 43.75% 3.7 -2.3 6 -260.87%

Opening cash balance 175.7 160.7 15 9.33% 187.8 175.7 12.1 6.89%

Closing cash balance 187.8 175.7 12.1 6.89% 196 187.8 8.2 4.37%

7

(Repayment)/

drawdown of

syndicated loan notes -10.2 154.1 -164.3 -1.07 -19.9 -10.2 -9.7 95.10%

Medium-term notes

(redemption 0 -400 400 -1.00 0 0 0 0.00%

Reduction in

obligations under

finance leases -4.8 -7.3 2.5 -34.25% -2.4 -4.8 2.4 -50.00%

Liability payment to

Pension scheme -54.4 -50.3 -4.1 8.15% -56 -54.4 -1.6 2.94%

Paid equity dividends -280.7 -273.6 -7.1 2.60% -301.7 -280.7 -21 7.48%

Issued shares by

exercising employee

share options 40.8 44.2 -3.4 -7.69% 20.6 40.8 -20.2 -49.51%

Buy back of shares 0 0 0 0.00% -150.7 0 -150.7 0.00%

Purchase of own

shares through

employee trust -24.2 0 -24.2 0.00% -24.2 24.2 -1.00

Net outflow in

financing activities -614.5 -498.1 -116.4 23.37% -631.4 -614.5 -16.9 2.75%

Net Increase /

(Decrease) in cash 14.4 16.6 -2.2 -13.25% 4.5 14.4 -9.9 -68.75%

Exchange rate effects -2.3 -1.6 -0.7 43.75% 3.7 -2.3 6 -260.87%

Opening cash balance 175.7 160.7 15 9.33% 187.8 175.7 12.1 6.89%

Closing cash balance 187.8 175.7 12.1 6.89% 196 187.8 8.2 4.37%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

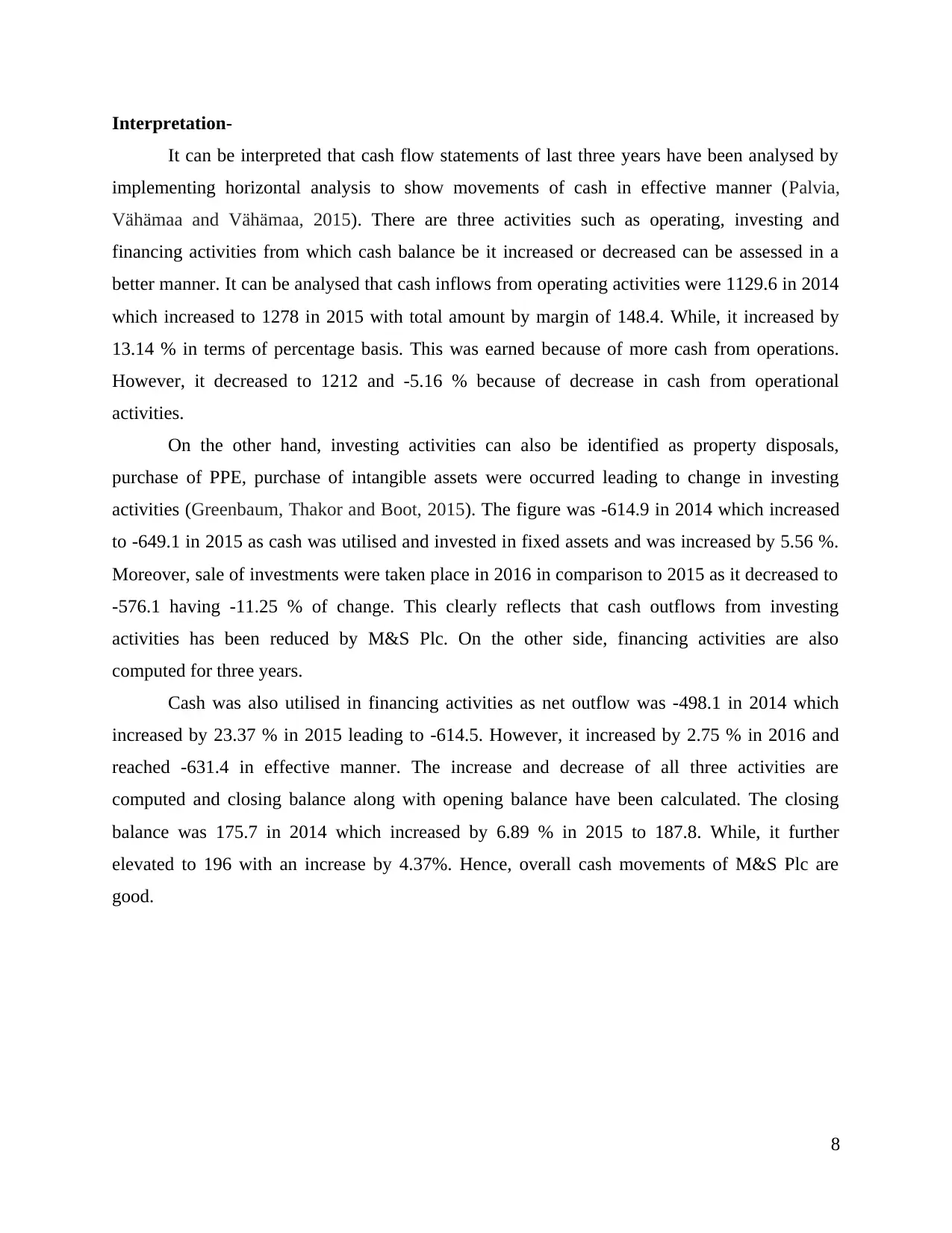

Interpretation-

It can be interpreted that cash flow statements of last three years have been analysed by

implementing horizontal analysis to show movements of cash in effective manner (Palvia,

Vähämaa and Vähämaa, 2015). There are three activities such as operating, investing and

financing activities from which cash balance be it increased or decreased can be assessed in a

better manner. It can be analysed that cash inflows from operating activities were 1129.6 in 2014

which increased to 1278 in 2015 with total amount by margin of 148.4. While, it increased by

13.14 % in terms of percentage basis. This was earned because of more cash from operations.

However, it decreased to 1212 and -5.16 % because of decrease in cash from operational

activities.

On the other hand, investing activities can also be identified as property disposals,

purchase of PPE, purchase of intangible assets were occurred leading to change in investing

activities (Greenbaum, Thakor and Boot, 2015). The figure was -614.9 in 2014 which increased

to -649.1 in 2015 as cash was utilised and invested in fixed assets and was increased by 5.56 %.

Moreover, sale of investments were taken place in 2016 in comparison to 2015 as it decreased to

-576.1 having -11.25 % of change. This clearly reflects that cash outflows from investing

activities has been reduced by M&S Plc. On the other side, financing activities are also

computed for three years.

Cash was also utilised in financing activities as net outflow was -498.1 in 2014 which

increased by 23.37 % in 2015 leading to -614.5. However, it increased by 2.75 % in 2016 and

reached -631.4 in effective manner. The increase and decrease of all three activities are

computed and closing balance along with opening balance have been calculated. The closing

balance was 175.7 in 2014 which increased by 6.89 % in 2015 to 187.8. While, it further

elevated to 196 with an increase by 4.37%. Hence, overall cash movements of M&S Plc are

good.

8

It can be interpreted that cash flow statements of last three years have been analysed by

implementing horizontal analysis to show movements of cash in effective manner (Palvia,

Vähämaa and Vähämaa, 2015). There are three activities such as operating, investing and

financing activities from which cash balance be it increased or decreased can be assessed in a

better manner. It can be analysed that cash inflows from operating activities were 1129.6 in 2014

which increased to 1278 in 2015 with total amount by margin of 148.4. While, it increased by

13.14 % in terms of percentage basis. This was earned because of more cash from operations.

However, it decreased to 1212 and -5.16 % because of decrease in cash from operational

activities.

On the other hand, investing activities can also be identified as property disposals,

purchase of PPE, purchase of intangible assets were occurred leading to change in investing

activities (Greenbaum, Thakor and Boot, 2015). The figure was -614.9 in 2014 which increased

to -649.1 in 2015 as cash was utilised and invested in fixed assets and was increased by 5.56 %.

Moreover, sale of investments were taken place in 2016 in comparison to 2015 as it decreased to

-576.1 having -11.25 % of change. This clearly reflects that cash outflows from investing

activities has been reduced by M&S Plc. On the other side, financing activities are also

computed for three years.

Cash was also utilised in financing activities as net outflow was -498.1 in 2014 which

increased by 23.37 % in 2015 leading to -614.5. However, it increased by 2.75 % in 2016 and

reached -631.4 in effective manner. The increase and decrease of all three activities are

computed and closing balance along with opening balance have been calculated. The closing

balance was 175.7 in 2014 which increased by 6.89 % in 2015 to 187.8. While, it further

elevated to 196 with an increase by 4.37%. Hence, overall cash movements of M&S Plc are

good.

8

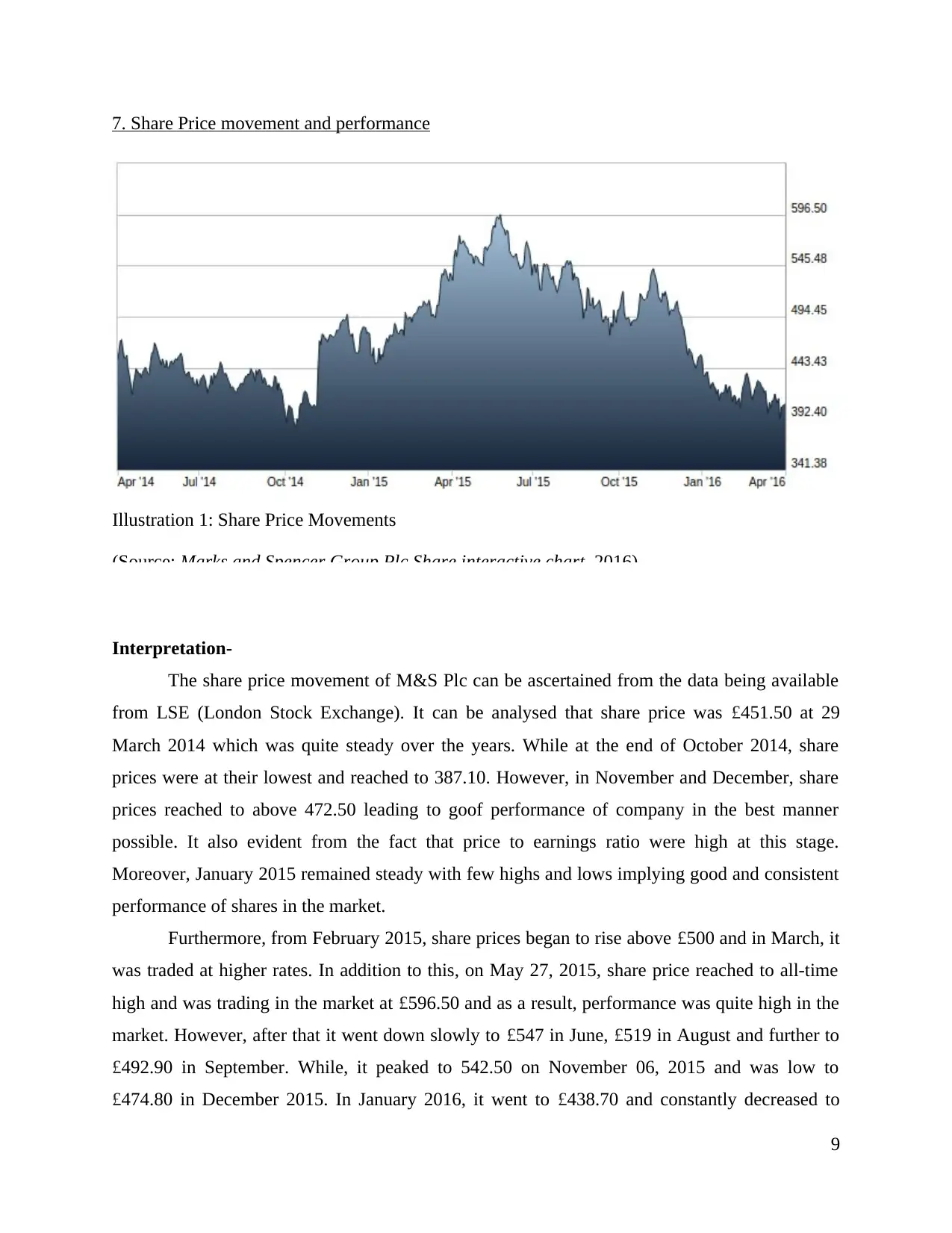

7. Share Price movement and performance

Illustration 1: Share Price Movements

(Source: Marks and Spencer Group Plc Share interactive chart, 2016)

Interpretation-

The share price movement of M&S Plc can be ascertained from the data being available

from LSE (London Stock Exchange). It can be analysed that share price was £451.50 at 29

March 2014 which was quite steady over the years. While at the end of October 2014, share

prices were at their lowest and reached to 387.10. However, in November and December, share

prices reached to above 472.50 leading to goof performance of company in the best manner

possible. It also evident from the fact that price to earnings ratio were high at this stage.

Moreover, January 2015 remained steady with few highs and lows implying good and consistent

performance of shares in the market.

Furthermore, from February 2015, share prices began to rise above £500 and in March, it

was traded at higher rates. In addition to this, on May 27, 2015, share price reached to all-time

high and was trading in the market at £596.50 and as a result, performance was quite high in the

market. However, after that it went down slowly to £547 in June, £519 in August and further to

£492.90 in September. While, it peaked to 542.50 on November 06, 2015 and was low to

£474.80 in December 2015. In January 2016, it went to £438.70 and constantly decreased to

9

Illustration 1: Share Price Movements

(Source: Marks and Spencer Group Plc Share interactive chart, 2016)

Interpretation-

The share price movement of M&S Plc can be ascertained from the data being available

from LSE (London Stock Exchange). It can be analysed that share price was £451.50 at 29

March 2014 which was quite steady over the years. While at the end of October 2014, share

prices were at their lowest and reached to 387.10. However, in November and December, share

prices reached to above 472.50 leading to goof performance of company in the best manner

possible. It also evident from the fact that price to earnings ratio were high at this stage.

Moreover, January 2015 remained steady with few highs and lows implying good and consistent

performance of shares in the market.

Furthermore, from February 2015, share prices began to rise above £500 and in March, it

was traded at higher rates. In addition to this, on May 27, 2015, share price reached to all-time

high and was trading in the market at £596.50 and as a result, performance was quite high in the

market. However, after that it went down slowly to £547 in June, £519 in August and further to

£492.90 in September. While, it peaked to 542.50 on November 06, 2015 and was low to

£474.80 in December 2015. In January 2016, it went to £438.70 and constantly decreased to

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.