Financial Auditing Report: National Australia Bank Financial Analysis

VerifiedAdded on 2020/02/24

|24

|4729

|34

Report

AI Summary

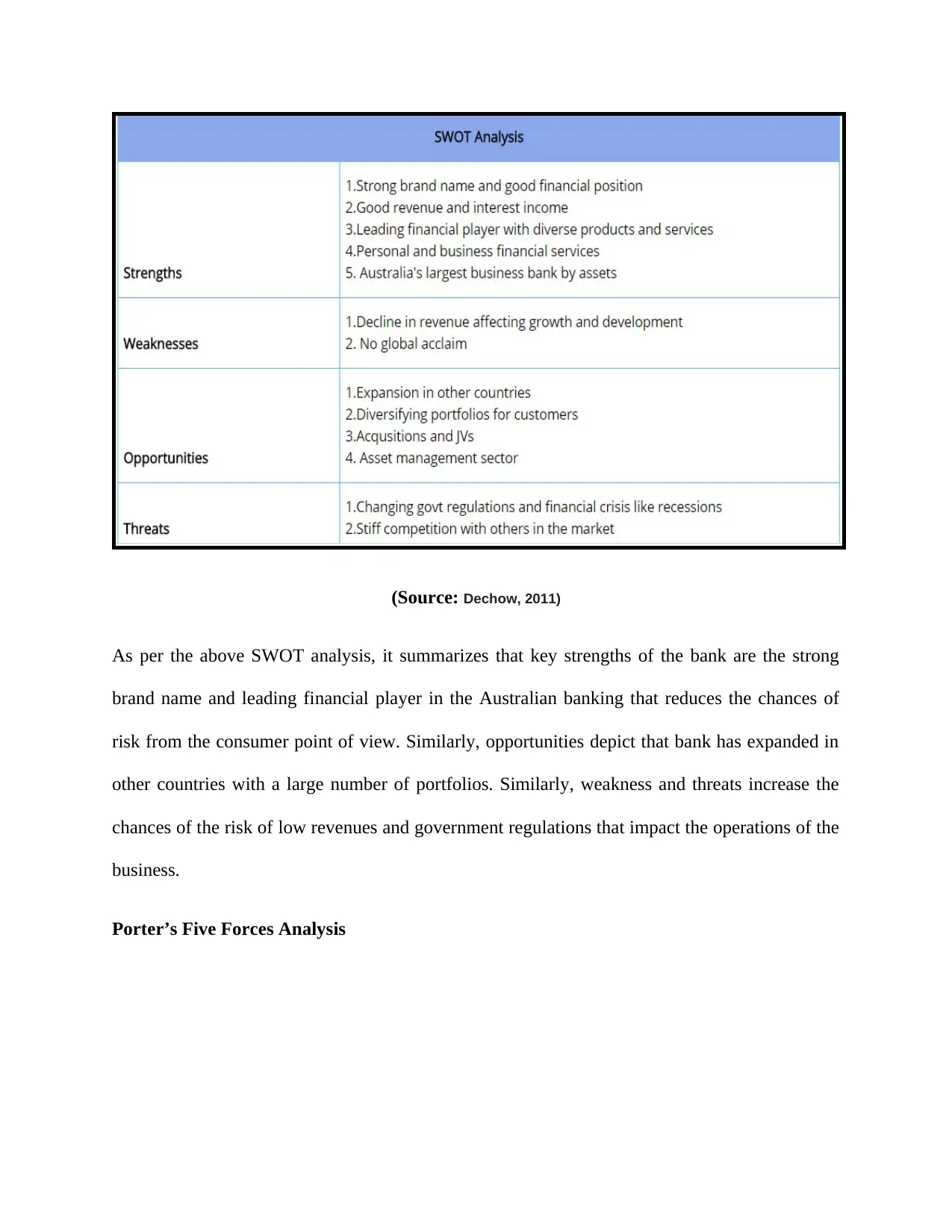

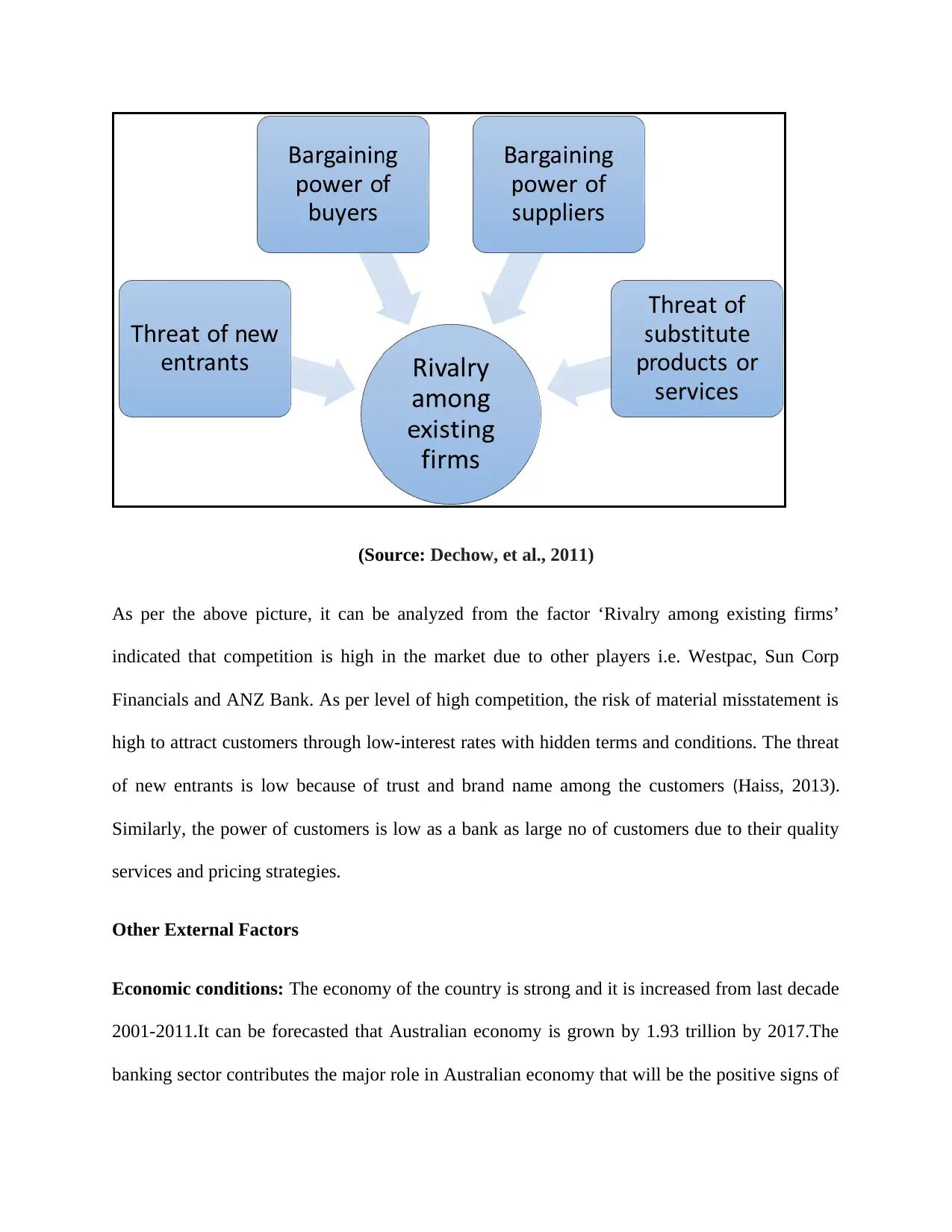

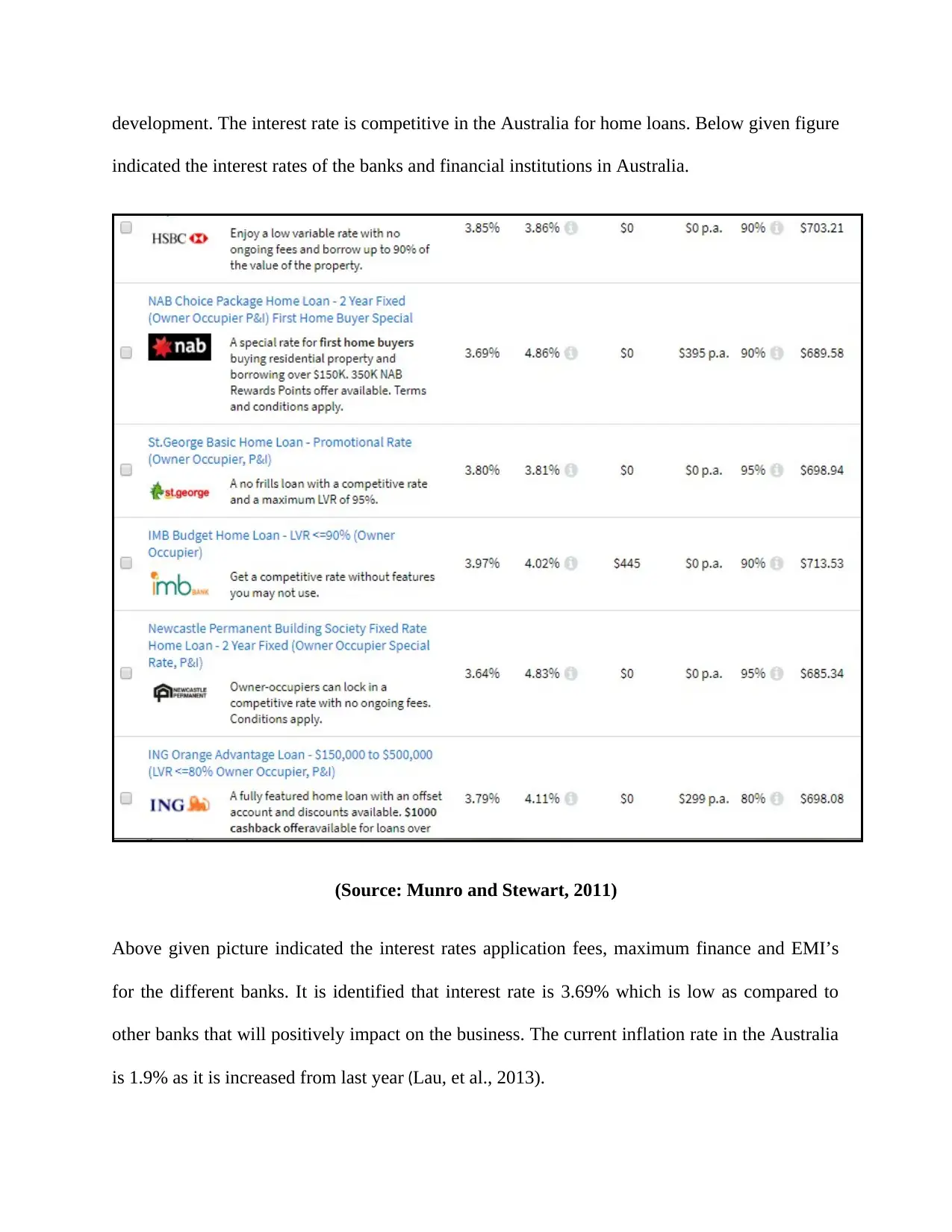

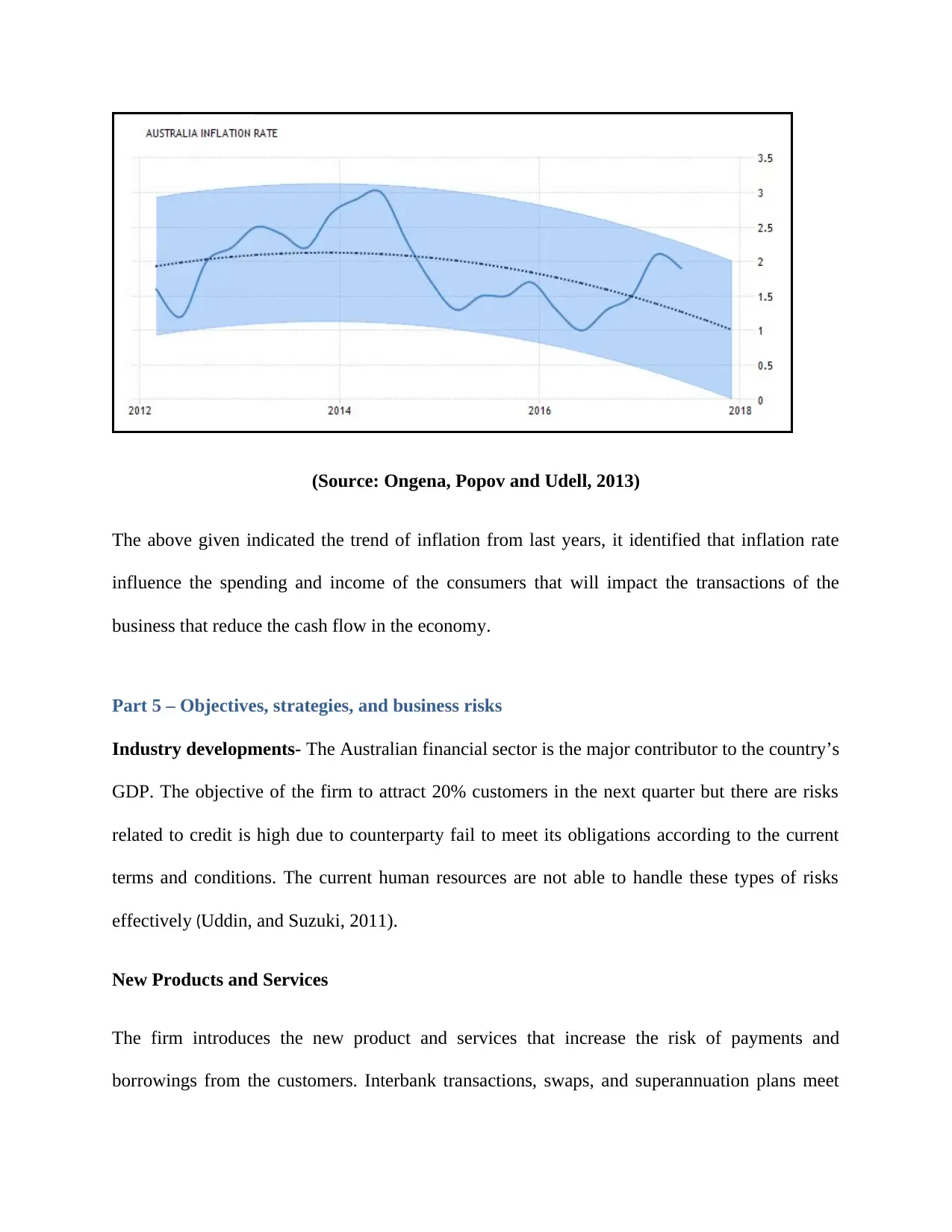

This report provides a detailed analysis of the National Australian Bank (NAB), focusing on the identification and assessment of material misstatements within its financial statements. The report begins with an executive summary and introduction, followed by an in-depth examination of the bank's nature, industry dynamics, and the legal and external environmental factors influencing its operations. The report also includes an analysis of the industry's size, growth, supply chain, major players, and critical success factors. Furthermore, it explores NAB's objectives, strategies, and business risks, including industry developments, new products, and regulatory requirements. The analysis extends to the bank's financial reporting practices, governance structure, and performance metrics through ratio analysis and SWOT and PESTLE analyses. The report concludes with an assessment of the overall risk levels impacting the company and its environment, drawing on information from various levels of its operations. This comprehensive report is a valuable resource for understanding the financial health and operational risks of NAB.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.