Financial and Non-Financial Dimensions in Management Accounting

VerifiedAdded on 2023/06/10

|11

|1754

|297

Report

AI Summary

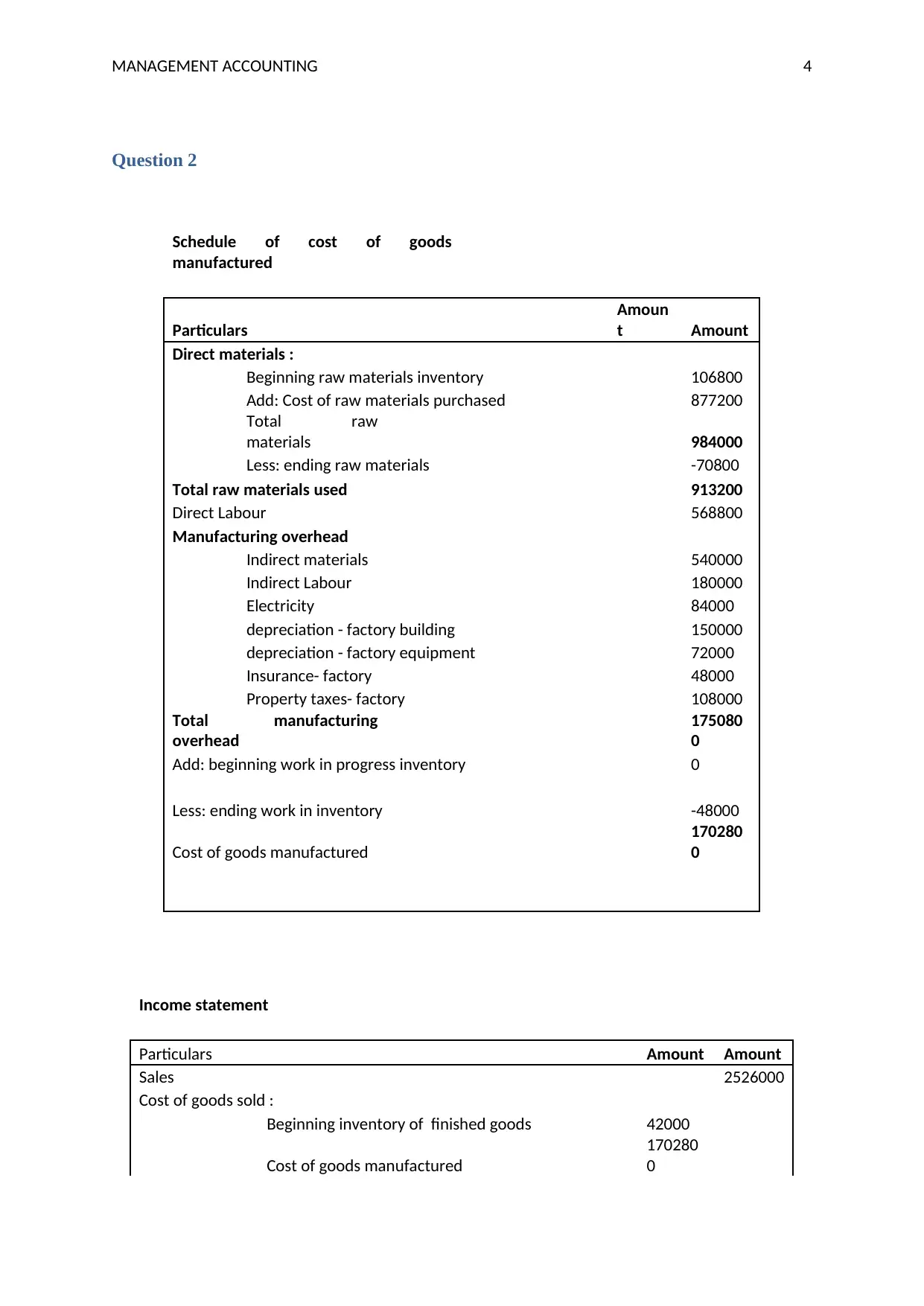

This management accounting report provides a comprehensive analysis of various financial and non-financial aspects of a business. It covers topics such as cost-benefit analysis of expanding product lines, the importance of financial and non-financial information for decision-making, and the calculation of the cost of goods manufactured using different costing methods like weighted average and FIFO. Additionally, it discusses the characteristics of services, including intangibility, inseparability, variability, and perishability, and how these factors affect industries like electricity, telecommunications, and education. The report includes detailed calculations of manufacturing costs, income statements, and cost of goods sold schedules, offering a thorough understanding of management accounting principles and their practical applications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.