Analyzing Financial Techniques in Business Decision Making

VerifiedAdded on 2023/06/12

|7

|1279

|467

Report

AI Summary

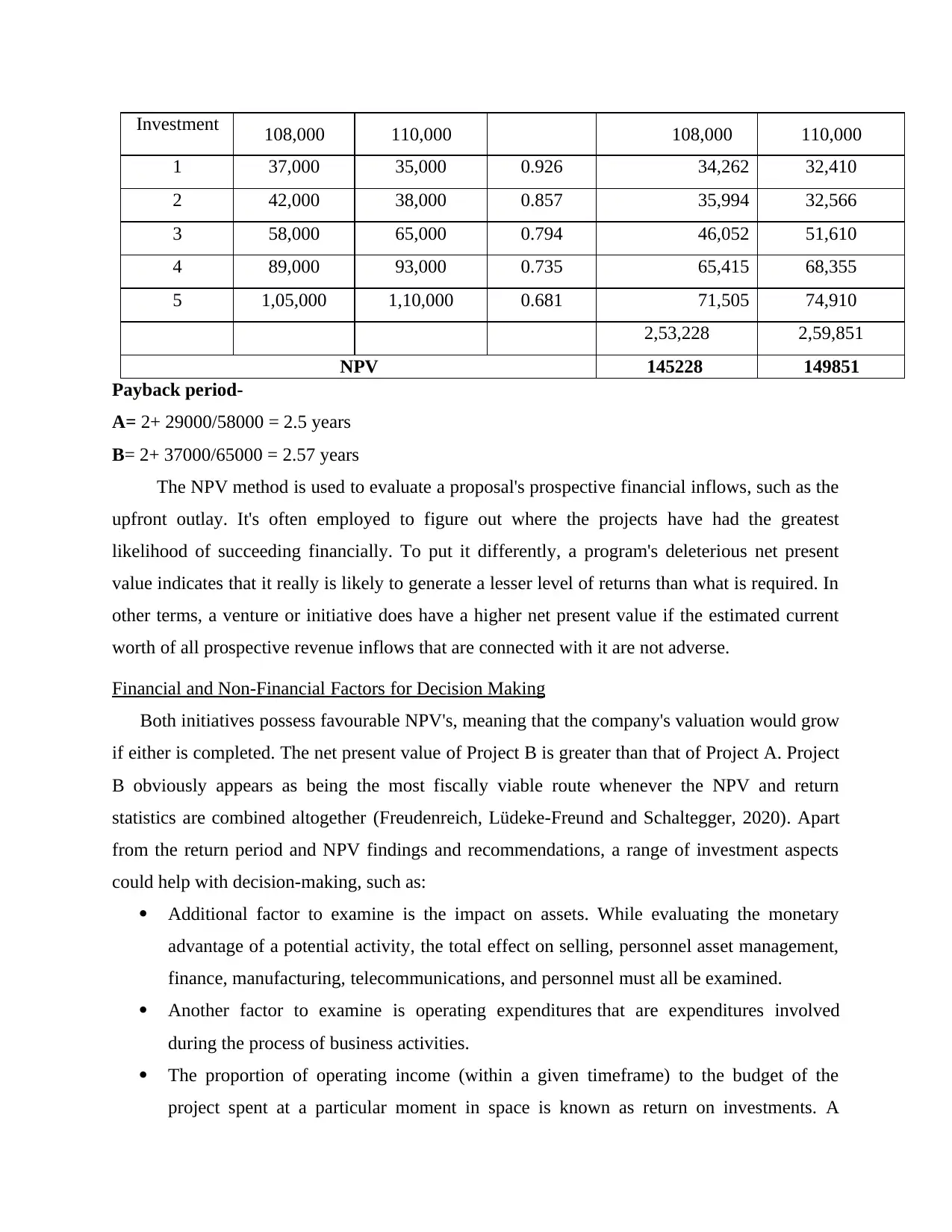

This report assesses corporate decision-making by examining key financial techniques, specifically the payback period and Net Present Value (NPV). It emphasizes the importance of evaluating various options and selecting the most promising alternative for long-term investments, such as purchasing property, facilities, and equipment. The payback period method, suitable for short-term businesses, estimates the time required to recoup an initial investment but overlooks the time value of money. The NPV method evaluates prospective financial inflows, aiding in determining project viability; a positive NPV indicates a potentially successful venture. The analysis includes a comparison of two projects, A and B, with different initial outlays and predicted yields, highlighting that Project B, with a higher NPV, is the more fiscally viable option. Beyond financial metrics, the report considers non-financial factors like the impact on assets, operating expenditures, return on investment (ROI), and net profitability, as well as employee enthusiasm and customer satisfaction, all of which influence overall business success. The report concludes that effective corporate decision-making requires a comprehensive financial analysis combined with consideration of broader operational and social impacts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.