Financial Accounting Report: Evaluating Management Accounting Tools

VerifiedAdded on 2021/02/20

|12

|2792

|26

Report

AI Summary

This financial accounting report delves into the application of various management accounting tools to enhance organizational financial performance. It begins by defining financial accounting and its role in recording and reporting financial transactions for internal and external stakeholders. The report then critically evaluates the use of techniques such as the balanced scorecard, just-in-time inventory management, total quality management, flexible budgeting, cost-volume-profit analysis, and Six Sigma. It examines how each tool contributes to improved efficiency, reduced costs, customer satisfaction, and overall sustainable success. The report highlights the benefits and limitations of each method, emphasizing their role in addressing financial challenges and achieving a competitive edge. The conclusion summarizes the key findings, emphasizing the significant contribution of management accounting tools in improving organizational performance, reducing costs, and enhancing profitability.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...............................................................................................................1

Critically evaluating the use of the management accounting tools in enhancing the

financial performance ....................................................................................................1

CONCLUSION...................................................................................................................4

REFERENCES..................................................................................................................5

INTRODUCTION...............................................................................................................1

Critically evaluating the use of the management accounting tools in enhancing the

financial performance ....................................................................................................1

CONCLUSION...................................................................................................................4

REFERENCES..................................................................................................................5

INTRODUCTION

Financial accounting means the process that keeps the track on the financial

transactions of an organization. Under this, standardized guidelines are been used for

recording, presenting and summarizing the transactions in order to report the financial

statement to the internal and the external users so that they could be able to make the

suitable decisions in relation to their investment and stake. The financial report

formulated reflects the performance and the position of the company in the market by

communicating the information in relation to its profitability, assets, liabilities and

equities. The present report is based on the uses of the several management

accounting techniques in getting better financial results or in improving the financial

performance of the enterprise.

Critically evaluating the use of the management accounting tools in enhancing the

financial performance

According to Cooper, Ezzamel and Qu, (2017), it has been viewed that, For

attaining customer satisfaction and customer loyalty for the organization, Managers

must make use of the management accounting techniques such as balanced scorecard,

just-in-time, total quality management, break-even analysis, six sigma etc (Nguyen and

et.al., 2017). These techniques will be enabling the managers in gaining sustainable

performance within the company which in turn helps in improving the performance of the

employees and in reaching the competitive edge over competitors within the overall

market across the world.

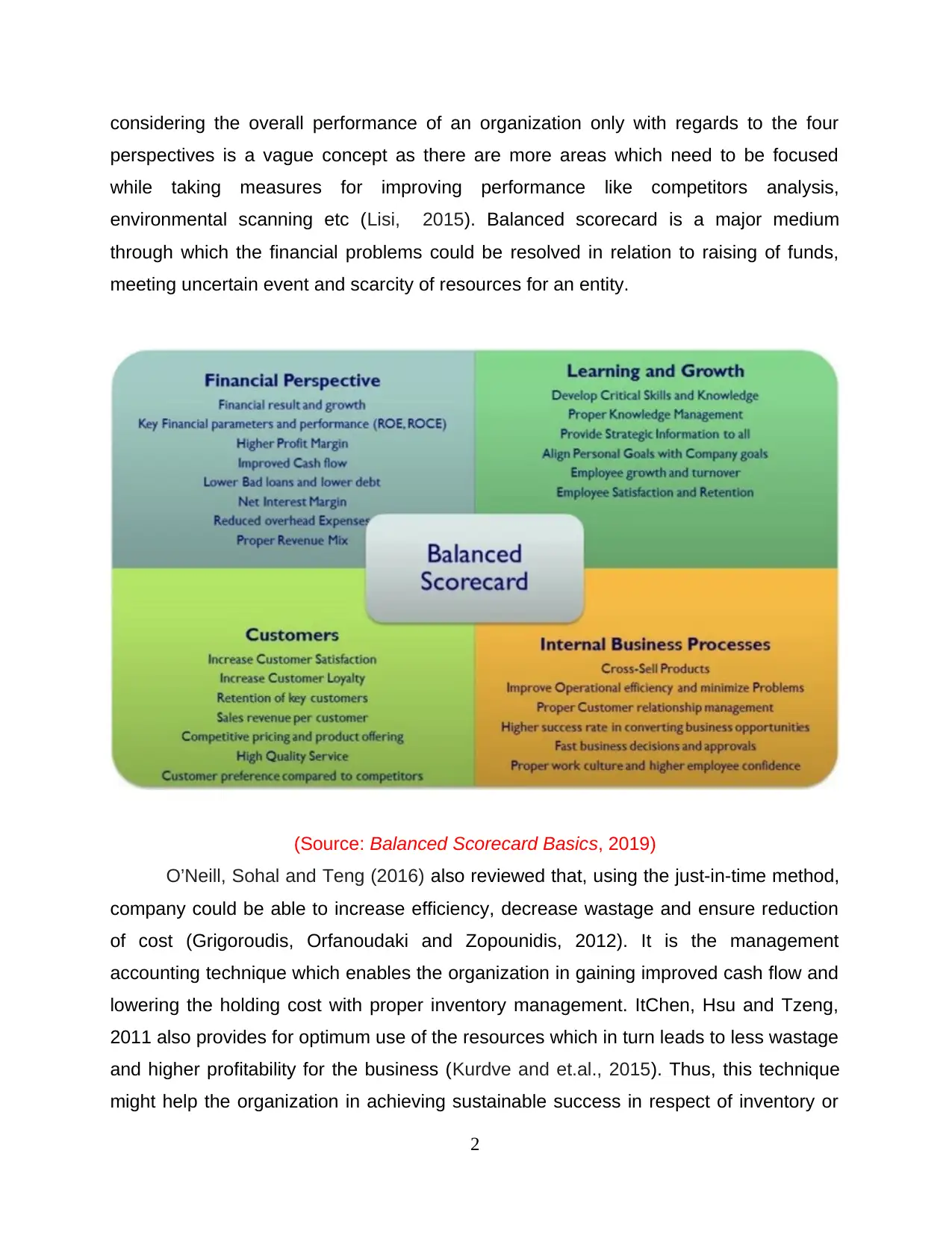

In order to match with the market trend, it is important for the managers to adopt

Balanced Scorecard tool which could help the organization in meeting with the changing

business needs and in resolving its financial problems (Parida and et.al., 2015).

Balanced scorecard is the method that facilitates comprehensive and the balanced

framework in order to judge the performance of an organization by taking into

consideration four major perspectives that is financial, customer, production process

and the growth outcome (Chen, Hsu and Tzeng, 2011). It helps the management in

functioning the company in the unique way. This technique assist managers in

enhancing the performance by setting up of the objectives aChen, Hsu and Tzeng,

2011nd the measures for the performance in relation to the perspectives. However,

1

Financial accounting means the process that keeps the track on the financial

transactions of an organization. Under this, standardized guidelines are been used for

recording, presenting and summarizing the transactions in order to report the financial

statement to the internal and the external users so that they could be able to make the

suitable decisions in relation to their investment and stake. The financial report

formulated reflects the performance and the position of the company in the market by

communicating the information in relation to its profitability, assets, liabilities and

equities. The present report is based on the uses of the several management

accounting techniques in getting better financial results or in improving the financial

performance of the enterprise.

Critically evaluating the use of the management accounting tools in enhancing the

financial performance

According to Cooper, Ezzamel and Qu, (2017), it has been viewed that, For

attaining customer satisfaction and customer loyalty for the organization, Managers

must make use of the management accounting techniques such as balanced scorecard,

just-in-time, total quality management, break-even analysis, six sigma etc (Nguyen and

et.al., 2017). These techniques will be enabling the managers in gaining sustainable

performance within the company which in turn helps in improving the performance of the

employees and in reaching the competitive edge over competitors within the overall

market across the world.

In order to match with the market trend, it is important for the managers to adopt

Balanced Scorecard tool which could help the organization in meeting with the changing

business needs and in resolving its financial problems (Parida and et.al., 2015).

Balanced scorecard is the method that facilitates comprehensive and the balanced

framework in order to judge the performance of an organization by taking into

consideration four major perspectives that is financial, customer, production process

and the growth outcome (Chen, Hsu and Tzeng, 2011). It helps the management in

functioning the company in the unique way. This technique assist managers in

enhancing the performance by setting up of the objectives aChen, Hsu and Tzeng,

2011nd the measures for the performance in relation to the perspectives. However,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considering the overall performance of an organization only with regards to the four

perspectives is a vague concept as there are more areas which need to be focused

while taking measures for improving performance like competitors analysis,

environmental scanning etc (Lisi, 2015). Balanced scorecard is a major medium

through which the financial problems could be resolved in relation to raising of funds,

meeting uncertain event and scarcity of resources for an entity.

(Source: Balanced Scorecard Basics, 2019)

O’Neill, Sohal and Teng (2016) also reviewed that, using the just-in-time method,

company could be able to increase efficiency, decrease wastage and ensure reduction

of cost (Grigoroudis, Orfanoudaki and Zopounidis, 2012). It is the management

accounting technique which enables the organization in gaining improved cash flow and

lowering the holding cost with proper inventory management. ItChen, Hsu and Tzeng,

2011 also provides for optimum use of the resources which in turn leads to less wastage

and higher profitability for the business (Kurdve and et.al., 2015). Thus, this technique

might help the organization in achieving sustainable success in respect of inventory or

2

perspectives is a vague concept as there are more areas which need to be focused

while taking measures for improving performance like competitors analysis,

environmental scanning etc (Lisi, 2015). Balanced scorecard is a major medium

through which the financial problems could be resolved in relation to raising of funds,

meeting uncertain event and scarcity of resources for an entity.

(Source: Balanced Scorecard Basics, 2019)

O’Neill, Sohal and Teng (2016) also reviewed that, using the just-in-time method,

company could be able to increase efficiency, decrease wastage and ensure reduction

of cost (Grigoroudis, Orfanoudaki and Zopounidis, 2012). It is the management

accounting technique which enables the organization in gaining improved cash flow and

lowering the holding cost with proper inventory management. ItChen, Hsu and Tzeng,

2011 also provides for optimum use of the resources which in turn leads to less wastage

and higher profitability for the business (Kurdve and et.al., 2015). Thus, this technique

might help the organization in achieving sustainable success in respect of inventory or

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

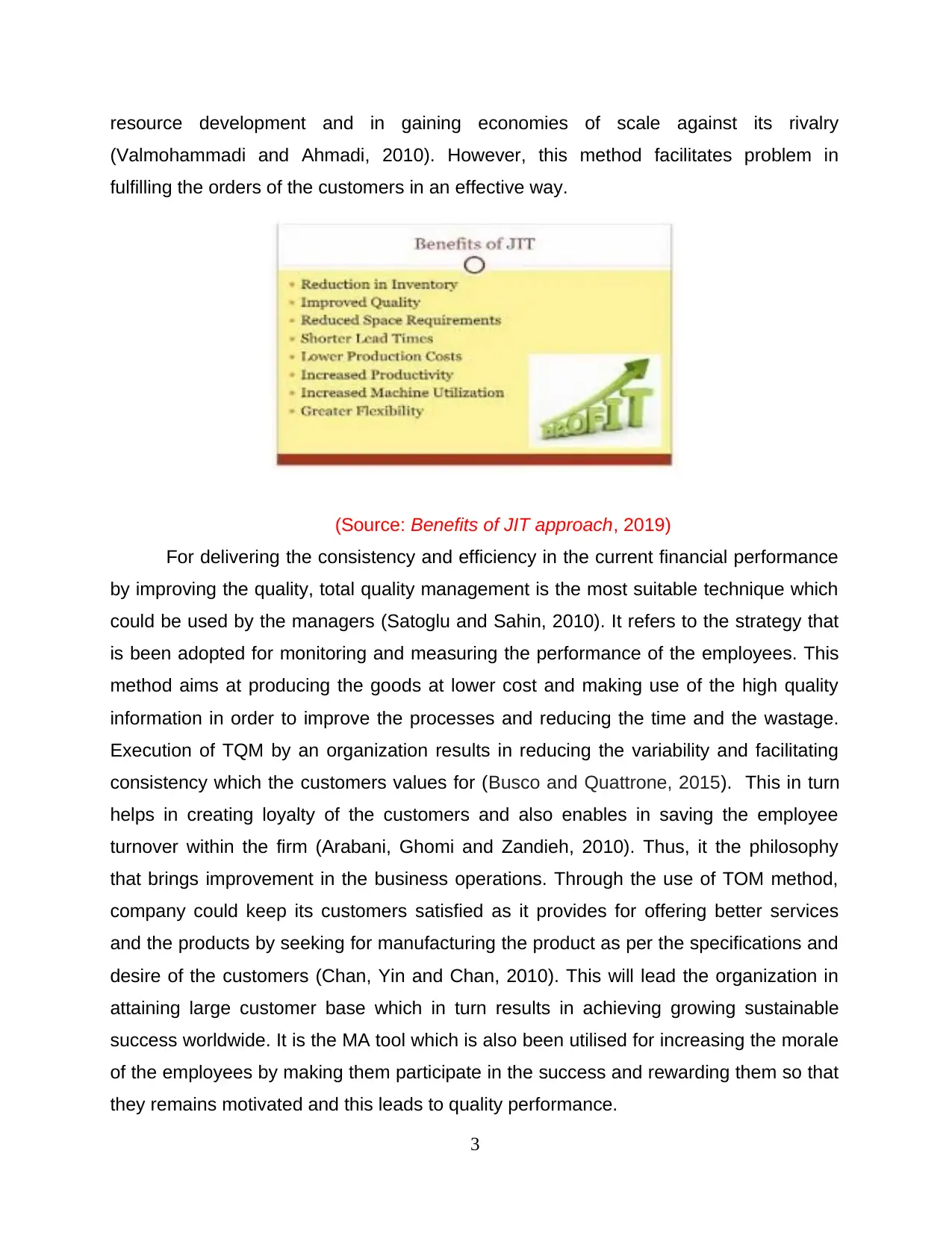

resource development and in gaining economies of scale against its rivalry

(Valmohammadi and Ahmadi, 2010). However, this method facilitates problem in

fulfilling the orders of the customers in an effective way.

(Source: Benefits of JIT approach, 2019)

For delivering the consistency and efficiency in the current financial performance

by improving the quality, total quality management is the most suitable technique which

could be used by the managers (Satoglu and Sahin, 2010). It refers to the strategy that

is been adopted for monitoring and measuring the performance of the employees. This

method aims at producing the goods at lower cost and making use of the high quality

information in order to improve the processes and reducing the time and the wastage.

Execution of TQM by an organization results in reducing the variability and facilitating

consistency which the customers values for (Busco and Quattrone, 2015). This in turn

helps in creating loyalty of the customers and also enables in saving the employee

turnover within the firm (Arabani, Ghomi and Zandieh, 2010). Thus, it the philosophy

that brings improvement in the business operations. Through the use of TOM method,

company could keep its customers satisfied as it provides for offering better services

and the products by seeking for manufacturing the product as per the specifications and

desire of the customers (Chan, Yin and Chan, 2010). This will lead the organization in

attaining large customer base which in turn results in achieving growing sustainable

success worldwide. It is the MA tool which is also been utilised for increasing the morale

of the employees by making them participate in the success and rewarding them so that

they remains motivated and this leads to quality performance.

3

(Valmohammadi and Ahmadi, 2010). However, this method facilitates problem in

fulfilling the orders of the customers in an effective way.

(Source: Benefits of JIT approach, 2019)

For delivering the consistency and efficiency in the current financial performance

by improving the quality, total quality management is the most suitable technique which

could be used by the managers (Satoglu and Sahin, 2010). It refers to the strategy that

is been adopted for monitoring and measuring the performance of the employees. This

method aims at producing the goods at lower cost and making use of the high quality

information in order to improve the processes and reducing the time and the wastage.

Execution of TQM by an organization results in reducing the variability and facilitating

consistency which the customers values for (Busco and Quattrone, 2015). This in turn

helps in creating loyalty of the customers and also enables in saving the employee

turnover within the firm (Arabani, Ghomi and Zandieh, 2010). Thus, it the philosophy

that brings improvement in the business operations. Through the use of TOM method,

company could keep its customers satisfied as it provides for offering better services

and the products by seeking for manufacturing the product as per the specifications and

desire of the customers (Chan, Yin and Chan, 2010). This will lead the organization in

attaining large customer base which in turn results in achieving growing sustainable

success worldwide. It is the MA tool which is also been utilised for increasing the morale

of the employees by making them participate in the success and rewarding them so that

they remains motivated and this leads to quality performance.

3

(Source: Total Quality management, 2019)

Lin, Su and Higgins, (2016) highlighted that, for adjusting the changes and

anticipating the future, company can use flexible budget which referred as the budget

that changes with the change in the level of the output or the other resources of an

enterprise (Talib, Rahman and Qureshi, 2010). Preparation of this budget provides an

organization a better view regarding the changes that incurred in the sales with respect

4

Lin, Su and Higgins, (2016) highlighted that, for adjusting the changes and

anticipating the future, company can use flexible budget which referred as the budget

that changes with the change in the level of the output or the other resources of an

enterprise (Talib, Rahman and Qureshi, 2010). Preparation of this budget provides an

organization a better view regarding the changes that incurred in the sales with respect

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to changes in the production level. This budget helps in making the comparison in

between the actual and the standard output, cost and the performance so that

appropriate measures could be adopted on a timely basis such as cost control, flexibility

etc (Akgün and et.al., 2010). It facilitates correct estimates regarding the future

requirements and in fulfilling the objectives effectively and efficiently.

For the purpose of making the assessment of the profitable investment project,

cost volume profit analysis is counted as the best method as it describes the profit

behaviour towards a change in the volume and the cost. It is also called as the break-

even analysis because it helps in finding out the point of break-even that in respect of

targeting the operating income (Pepper and Spedding, 2010). It assist the organization

in choosing the best investment proposal that will be generating larger returns and also

sets the basis for making an effective plan in relation to the marketing efforts of the

business. It also helps in developing the base for performing a budgeting activity.

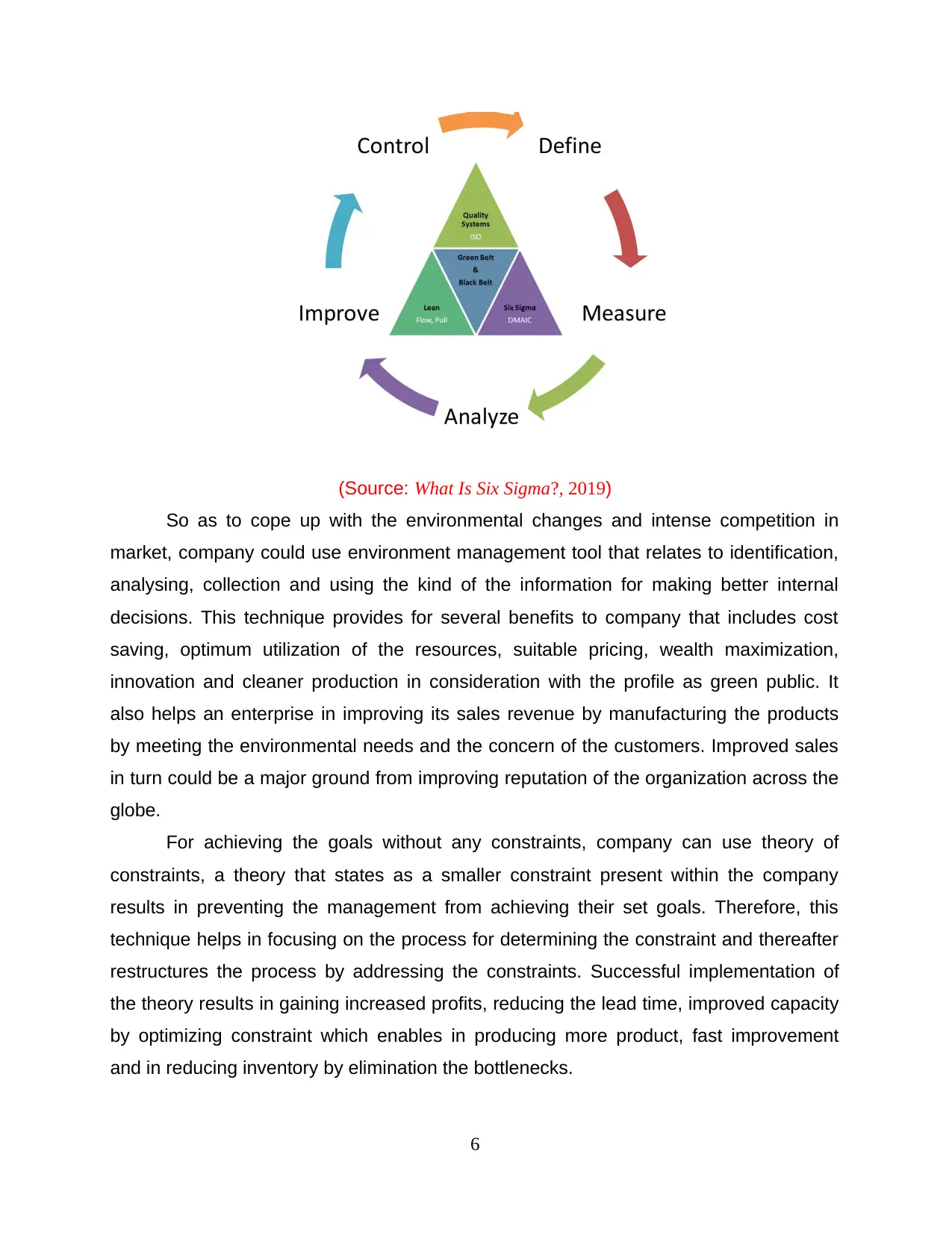

Phan and Baird, (2015) stated that, for eliminating the defects and in order to

reduce the variability in the process, an organization can make use of the Six Sigma

technique, which provides for improvement, validation and measurement of the

activities. It is the most useful technique through which an entity could be able to attain

reduction in its operational cost and also improves the customer service as it determines

the variations that the customers are been experiencing and creating interaction with

them so that their view can be assessed and actions could be taken accordingly. It also

facilitates constant excellence in the process and delivering a quality product to the

customers effectively (Antony, 2010). This method improves the accuracy, policy

compliance and the controls within the entire value chain and in reducing the defects

that might occur in each and every opportunity.

5

between the actual and the standard output, cost and the performance so that

appropriate measures could be adopted on a timely basis such as cost control, flexibility

etc (Akgün and et.al., 2010). It facilitates correct estimates regarding the future

requirements and in fulfilling the objectives effectively and efficiently.

For the purpose of making the assessment of the profitable investment project,

cost volume profit analysis is counted as the best method as it describes the profit

behaviour towards a change in the volume and the cost. It is also called as the break-

even analysis because it helps in finding out the point of break-even that in respect of

targeting the operating income (Pepper and Spedding, 2010). It assist the organization

in choosing the best investment proposal that will be generating larger returns and also

sets the basis for making an effective plan in relation to the marketing efforts of the

business. It also helps in developing the base for performing a budgeting activity.

Phan and Baird, (2015) stated that, for eliminating the defects and in order to

reduce the variability in the process, an organization can make use of the Six Sigma

technique, which provides for improvement, validation and measurement of the

activities. It is the most useful technique through which an entity could be able to attain

reduction in its operational cost and also improves the customer service as it determines

the variations that the customers are been experiencing and creating interaction with

them so that their view can be assessed and actions could be taken accordingly. It also

facilitates constant excellence in the process and delivering a quality product to the

customers effectively (Antony, 2010). This method improves the accuracy, policy

compliance and the controls within the entire value chain and in reducing the defects

that might occur in each and every opportunity.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: What Is Six Sigma?, 2019)

So as to cope up with the environmental changes and intense competition in

market, company could use environment management tool that relates to identification,

analysing, collection and using the kind of the information for making better internal

decisions. This technique provides for several benefits to company that includes cost

saving, optimum utilization of the resources, suitable pricing, wealth maximization,

innovation and cleaner production in consideration with the profile as green public. It

also helps an enterprise in improving its sales revenue by manufacturing the products

by meeting the environmental needs and the concern of the customers. Improved sales

in turn could be a major ground from improving reputation of the organization across the

globe.

For achieving the goals without any constraints, company can use theory of

constraints, a theory that states as a smaller constraint present within the company

results in preventing the management from achieving their set goals. Therefore, this

technique helps in focusing on the process for determining the constraint and thereafter

restructures the process by addressing the constraints. Successful implementation of

the theory results in gaining increased profits, reducing the lead time, improved capacity

by optimizing constraint which enables in producing more product, fast improvement

and in reducing inventory by elimination the bottlenecks.

6

So as to cope up with the environmental changes and intense competition in

market, company could use environment management tool that relates to identification,

analysing, collection and using the kind of the information for making better internal

decisions. This technique provides for several benefits to company that includes cost

saving, optimum utilization of the resources, suitable pricing, wealth maximization,

innovation and cleaner production in consideration with the profile as green public. It

also helps an enterprise in improving its sales revenue by manufacturing the products

by meeting the environmental needs and the concern of the customers. Improved sales

in turn could be a major ground from improving reputation of the organization across the

globe.

For achieving the goals without any constraints, company can use theory of

constraints, a theory that states as a smaller constraint present within the company

results in preventing the management from achieving their set goals. Therefore, this

technique helps in focusing on the process for determining the constraint and thereafter

restructures the process by addressing the constraints. Successful implementation of

the theory results in gaining increased profits, reducing the lead time, improved capacity

by optimizing constraint which enables in producing more product, fast improvement

and in reducing inventory by elimination the bottlenecks.

6

Thus, these were the different technique that could be adopted by the

organization for gaining constant efficiency in the financial performance and reducing

the pressure among the employees so that they could be able work with high morale in

achieving the short term financial results for an entity (Taticchi and et.al., 2015). Such

management accounting tools also helps an entity in attaining satisfaction of the

customers and reducing the switching of the customers towards other competitors. This

in turn enables achieving competitive advantage over the rivalry.

By doing assessment, it has found that management accounting techniques

provide high level of assistance in achieving sustainable performance. Moreover,

balance scorecard technique assists in developing competent framework by taking into

account both monetary and non-monetary aspects. In addition to this, TQM technique

assists in eliminating undesirable activities from operations and thereby improves quality

of products or services. Furthermore, in addition to this, JIT technique helps in saving

storage expenses to the significant level. In this way, all the techniques of management

accounting facilitates sustainable performance of an organization.

CONCLUSION

By summing up the above report it has been concluded that financial accounting

plays an essential role in maintaining the record of the financial information and

reporting it to the users so that effective decisions can be taken. It also facilitates

comparison between the results of various years so that changes could be assessed

and appropriate measures could be taken in order to gain sustainable and growing

success in the long run. In order to make the investment in profitable channels, an entity

uses the management accounting techniques for making the suitable decisions. It can

be summarized from balance scorecard, six sigma, TQM and JIT are the most effectual

tools which contributes in performance improvement significantly. It can be stated from

the evaluation that management accounting tools make significant contribution in

organizational performance by reducing cost and improving quality as well as

profitability aspect.

7

organization for gaining constant efficiency in the financial performance and reducing

the pressure among the employees so that they could be able work with high morale in

achieving the short term financial results for an entity (Taticchi and et.al., 2015). Such

management accounting tools also helps an entity in attaining satisfaction of the

customers and reducing the switching of the customers towards other competitors. This

in turn enables achieving competitive advantage over the rivalry.

By doing assessment, it has found that management accounting techniques

provide high level of assistance in achieving sustainable performance. Moreover,

balance scorecard technique assists in developing competent framework by taking into

account both monetary and non-monetary aspects. In addition to this, TQM technique

assists in eliminating undesirable activities from operations and thereby improves quality

of products or services. Furthermore, in addition to this, JIT technique helps in saving

storage expenses to the significant level. In this way, all the techniques of management

accounting facilitates sustainable performance of an organization.

CONCLUSION

By summing up the above report it has been concluded that financial accounting

plays an essential role in maintaining the record of the financial information and

reporting it to the users so that effective decisions can be taken. It also facilitates

comparison between the results of various years so that changes could be assessed

and appropriate measures could be taken in order to gain sustainable and growing

success in the long run. In order to make the investment in profitable channels, an entity

uses the management accounting techniques for making the suitable decisions. It can

be summarized from balance scorecard, six sigma, TQM and JIT are the most effectual

tools which contributes in performance improvement significantly. It can be stated from

the evaluation that management accounting tools make significant contribution in

organizational performance by reducing cost and improving quality as well as

profitability aspect.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Akgün, A.E. and et.al., 2014. The mediator role of learning capability and business

innovativeness between total quality management and financial

performance. International Journal of Production Research. 52(3). pp.888-901.

Antony, J., 2011. Six Sigma vs Lean: Some perspectives from leading academics and

practitioners. International Journal of Productivity and Performance

Management. 60(2). pp.185-190.

Arabani, A. B., Ghomi, S. F. and Zandieh, M., 2010. A multi-criteria cross-docking

scheduling with just-in-time approach. The International Journal of Advanced

Manufacturing Technology. 49(5-8). pp.741-756.

Busco, C. and Quattrone, P., 2015. Exploring how the balanced scorecard engages and

unfolds: Articulating the visual power of accounting inscriptions. Contemporary

Accounting Research. 32(3). pp.1236-1262.

Chan, H. K., Yin, S. and Chan, F. T., 2010. Implementing just-in-time philosophy to

reverse logistics systems: a review. International Journal of Production

Research. 48(21). pp.6293-6313.

Chen, F. H., Hsu, T. S. and Tzeng, G. H., 2011. A balanced scorecard approach to

establish a performance evaluation and relationship model for hot spring hotels

based on a hybrid MCDM model combining DEMATEL and ANP. International

Journal of Hospitality Management. 30(4). pp.908-932.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management

accounting idea: The case of the balanced scorecard. Contemporary Accounting

Research. 34(2). pp.991-1025.

Grigoroudis, E., Orfanoudaki, E. and Zopounidis, C., 2012. Strategic performance

measurement in a healthcare organisation: A multiple criteria approach based on

balanced scorecard. Omega. 40(1). pp.104-119.

Kurdve, M. and et.al., 2015. Waste flow mapping to improve sustainability of waste

management: a case study approach. Journal of Cleaner Production. 98. pp.304-

315.

8

Books and Journals

Akgün, A.E. and et.al., 2014. The mediator role of learning capability and business

innovativeness between total quality management and financial

performance. International Journal of Production Research. 52(3). pp.888-901.

Antony, J., 2011. Six Sigma vs Lean: Some perspectives from leading academics and

practitioners. International Journal of Productivity and Performance

Management. 60(2). pp.185-190.

Arabani, A. B., Ghomi, S. F. and Zandieh, M., 2010. A multi-criteria cross-docking

scheduling with just-in-time approach. The International Journal of Advanced

Manufacturing Technology. 49(5-8). pp.741-756.

Busco, C. and Quattrone, P., 2015. Exploring how the balanced scorecard engages and

unfolds: Articulating the visual power of accounting inscriptions. Contemporary

Accounting Research. 32(3). pp.1236-1262.

Chan, H. K., Yin, S. and Chan, F. T., 2010. Implementing just-in-time philosophy to

reverse logistics systems: a review. International Journal of Production

Research. 48(21). pp.6293-6313.

Chen, F. H., Hsu, T. S. and Tzeng, G. H., 2011. A balanced scorecard approach to

establish a performance evaluation and relationship model for hot spring hotels

based on a hybrid MCDM model combining DEMATEL and ANP. International

Journal of Hospitality Management. 30(4). pp.908-932.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management

accounting idea: The case of the balanced scorecard. Contemporary Accounting

Research. 34(2). pp.991-1025.

Grigoroudis, E., Orfanoudaki, E. and Zopounidis, C., 2012. Strategic performance

measurement in a healthcare organisation: A multiple criteria approach based on

balanced scorecard. Omega. 40(1). pp.104-119.

Kurdve, M. and et.al., 2015. Waste flow mapping to improve sustainability of waste

management: a case study approach. Journal of Cleaner Production. 98. pp.304-

315.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lin, H. F., Su, J. Q. and Higgins, A., 2016. How dynamic capabilities affect adoption of

management innovations. Journal of Business Research. 69(2). pp.862-876.

Lisi, I. E., 2015. Translating environmental motivations into performance: The role of

environmental performance measurement systems. Management Accounting

Research. 29. pp.27-44.

Nguyen, T.T. and et.al., 2017. Effect of transformational-leadership style and

management control system on managerial performance. Journal of Business

Research. 70. pp.202-213.

O’Neill, P., Sohal, A. and Teng, C. W., 2016. Quality management approaches and their

impact on firms׳ financial performance–An Australian study. International Journal

of Production Economics. 171. pp.381-393.

Parida, A. and et.al., 2015. Performance measurement and management for

maintenance: a literature review. Journal of Quality in Maintenance

Engineering. 21(1). pp.2-33.

Pepper, M. P. and Spedding, T. A., 2010. The evolution of lean Six Sigma. International

Journal of Quality & Reliability Management. 27(2). pp.138-155.

Phan, T. N. and Baird, K., 2015. The comprehensiveness of environmental

management systems: The influence of institutional pressures and the impact on

environmental performance. Journal of environmental management. 160. pp.45-

56.

Satoglu, S. I. and Sahin, I. E., 2010. Design of a just-in-time periodic material supply

system for the assembly lines and an application in electronics industry. The

International Journal of Advanced Manufacturing Technology. 65(1-4). pp.319-332.

Talib, F., Rahman, Z. and Qureshi, M. N., 2010. The relationship between total quality

management and quality performance in the service industry: a theoretical model.

Taticchi, P. and et.al., 2015. A review of decision-support tools and performance

measurement and sustainable supply chain management. International Journal of

Production Research. 53(21). pp.6473-6494.

Valmohammadi, C. and Ahmadi, M., 2010. The impact of knowledge management

practices on organizational performance: A balanced scorecard approach. Journal

of Enterprise Information Management. 28(1). pp.131-159.

9

management innovations. Journal of Business Research. 69(2). pp.862-876.

Lisi, I. E., 2015. Translating environmental motivations into performance: The role of

environmental performance measurement systems. Management Accounting

Research. 29. pp.27-44.

Nguyen, T.T. and et.al., 2017. Effect of transformational-leadership style and

management control system on managerial performance. Journal of Business

Research. 70. pp.202-213.

O’Neill, P., Sohal, A. and Teng, C. W., 2016. Quality management approaches and their

impact on firms׳ financial performance–An Australian study. International Journal

of Production Economics. 171. pp.381-393.

Parida, A. and et.al., 2015. Performance measurement and management for

maintenance: a literature review. Journal of Quality in Maintenance

Engineering. 21(1). pp.2-33.

Pepper, M. P. and Spedding, T. A., 2010. The evolution of lean Six Sigma. International

Journal of Quality & Reliability Management. 27(2). pp.138-155.

Phan, T. N. and Baird, K., 2015. The comprehensiveness of environmental

management systems: The influence of institutional pressures and the impact on

environmental performance. Journal of environmental management. 160. pp.45-

56.

Satoglu, S. I. and Sahin, I. E., 2010. Design of a just-in-time periodic material supply

system for the assembly lines and an application in electronics industry. The

International Journal of Advanced Manufacturing Technology. 65(1-4). pp.319-332.

Talib, F., Rahman, Z. and Qureshi, M. N., 2010. The relationship between total quality

management and quality performance in the service industry: a theoretical model.

Taticchi, P. and et.al., 2015. A review of decision-support tools and performance

measurement and sustainable supply chain management. International Journal of

Production Research. 53(21). pp.6473-6494.

Valmohammadi, C. and Ahmadi, M., 2010. The impact of knowledge management

practices on organizational performance: A balanced scorecard approach. Journal

of Enterprise Information Management. 28(1). pp.131-159.

9

Online

Balanced Scorecard Basics. 2019. Online. Available through: <

https://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard>.

What Is Six Sigma?. 2019. Online. Available through: <

https://www.sixsigmadaily.com/what-is-six-sigma/ >.

Total Quality management. 2019. Online. Available through: < https://asq.org/quality-

resources/total-quality-management >.

Benefits of JIT approach. 2019. Online. Available through: <

https://www.accountingtools.com/articles/the-advantages-and-disadvantages-of-just-in-

time-inventory.html >.

10

Balanced Scorecard Basics. 2019. Online. Available through: <

https://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard>.

What Is Six Sigma?. 2019. Online. Available through: <

https://www.sixsigmadaily.com/what-is-six-sigma/ >.

Total Quality management. 2019. Online. Available through: < https://asq.org/quality-

resources/total-quality-management >.

Benefits of JIT approach. 2019. Online. Available through: <

https://www.accountingtools.com/articles/the-advantages-and-disadvantages-of-just-in-

time-inventory.html >.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.