Accounting for Managers: Analyzing Business Performance Report

VerifiedAdded on 2020/05/16

|13

|2125

|146

Report

AI Summary

This report provides a detailed analysis of accounting principles for managers, focusing on profitability, cost allocation, and financial performance evaluation. The report addresses several key questions, including the profitability of Bonza Handtools Limited under different scenarios, the manufacturing capacity of The Tassie Company, and the allocation of overhead costs for ABC Limited. It explores various aspects of cost accounting, such as activity-based costing and overhead segmentation, and their importance in pricing strategies and decision-making. The analysis includes financial statements, profitability assessments, and recommendations based on the evaluation of different proposals. The report also references relevant literature in management and cost accounting to support its findings and recommendations.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR MANAGERS

Table of Contents

Answer 1: Bonza Handtools Limited..............................................................................................2

Answer 2: The Tassie Company......................................................................................................6

(i) Production capacity of the factory at 200,000 units per year:................................................6

(ii) Manufacturing ability of the factory with 180,000 units each year:......................................7

Question 3: ABC Limited................................................................................................................8

1. Allocation rate of Overhead:...................................................................................................8

2. Total costs associated with special order:................................................................................8

3. Cost related with special order:...............................................................................................8

4. Minimum price for each trailer:...............................................................................................9

5. Importance of activity-based costing with different overhead cost pools for pricing.............9

Question 4: Role of overhead segmentation in allocating overhead costs to individual jobs or

services............................................................................................................................................9

References:....................................................................................................................................11

Table of Contents

Answer 1: Bonza Handtools Limited..............................................................................................2

Answer 2: The Tassie Company......................................................................................................6

(i) Production capacity of the factory at 200,000 units per year:................................................6

(ii) Manufacturing ability of the factory with 180,000 units each year:......................................7

Question 3: ABC Limited................................................................................................................8

1. Allocation rate of Overhead:...................................................................................................8

2. Total costs associated with special order:................................................................................8

3. Cost related with special order:...............................................................................................8

4. Minimum price for each trailer:...............................................................................................9

5. Importance of activity-based costing with different overhead cost pools for pricing.............9

Question 4: Role of overhead segmentation in allocating overhead costs to individual jobs or

services............................................................................................................................................9

References:....................................................................................................................................11

2ACCOUNTING FOR MANAGERS

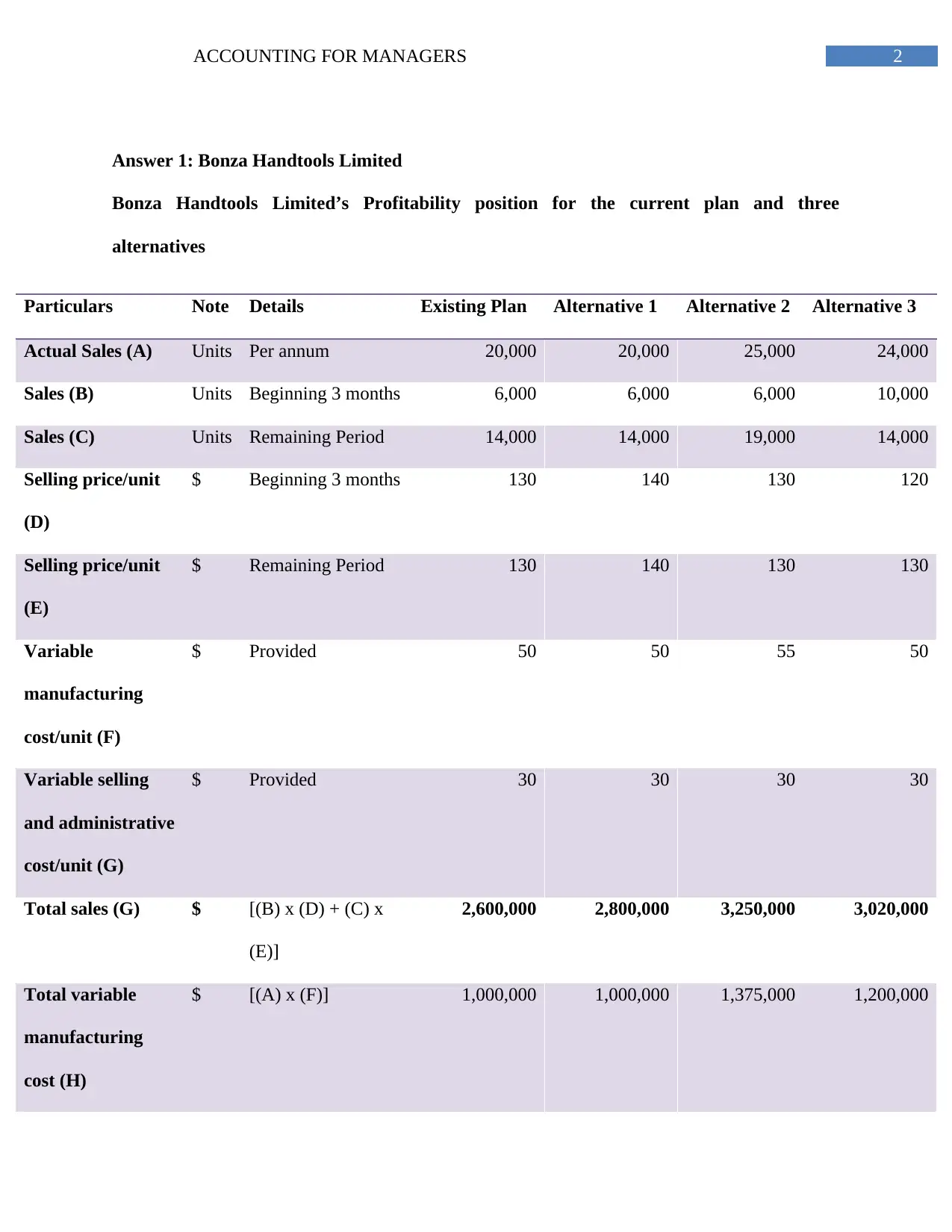

Answer 1: Bonza Handtools Limited

Bonza Handtools Limited’s Profitability position for the current plan and three

alternatives

Particulars Note Details Existing Plan Alternative 1 Alternative 2 Alternative 3

Actual Sales (A) Units Per annum 20,000 20,000 25,000 24,000

Sales (B) Units Beginning 3 months 6,000 6,000 6,000 10,000

Sales (C) Units Remaining Period 14,000 14,000 19,000 14,000

Selling price/unit

(D)

$ Beginning 3 months 130 140 130 120

Selling price/unit

(E)

$ Remaining Period 130 140 130 130

Variable

manufacturing

cost/unit (F)

$ Provided 50 50 55 50

Variable selling

and administrative

cost/unit (G)

$ Provided 30 30 30 30

Total sales (G) $ [(B) x (D) + (C) x

(E)]

2,600,000 2,800,000 3,250,000 3,020,000

Total variable

manufacturing

cost (H)

$ [(A) x (F)] 1,000,000 1,000,000 1,375,000 1,200,000

Answer 1: Bonza Handtools Limited

Bonza Handtools Limited’s Profitability position for the current plan and three

alternatives

Particulars Note Details Existing Plan Alternative 1 Alternative 2 Alternative 3

Actual Sales (A) Units Per annum 20,000 20,000 25,000 24,000

Sales (B) Units Beginning 3 months 6,000 6,000 6,000 10,000

Sales (C) Units Remaining Period 14,000 14,000 19,000 14,000

Selling price/unit

(D)

$ Beginning 3 months 130 140 130 120

Selling price/unit

(E)

$ Remaining Period 130 140 130 130

Variable

manufacturing

cost/unit (F)

$ Provided 50 50 55 50

Variable selling

and administrative

cost/unit (G)

$ Provided 30 30 30 30

Total sales (G) $ [(B) x (D) + (C) x

(E)]

2,600,000 2,800,000 3,250,000 3,020,000

Total variable

manufacturing

cost (H)

$ [(A) x (F)] 1,000,000 1,000,000 1,375,000 1,200,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR MANAGERS

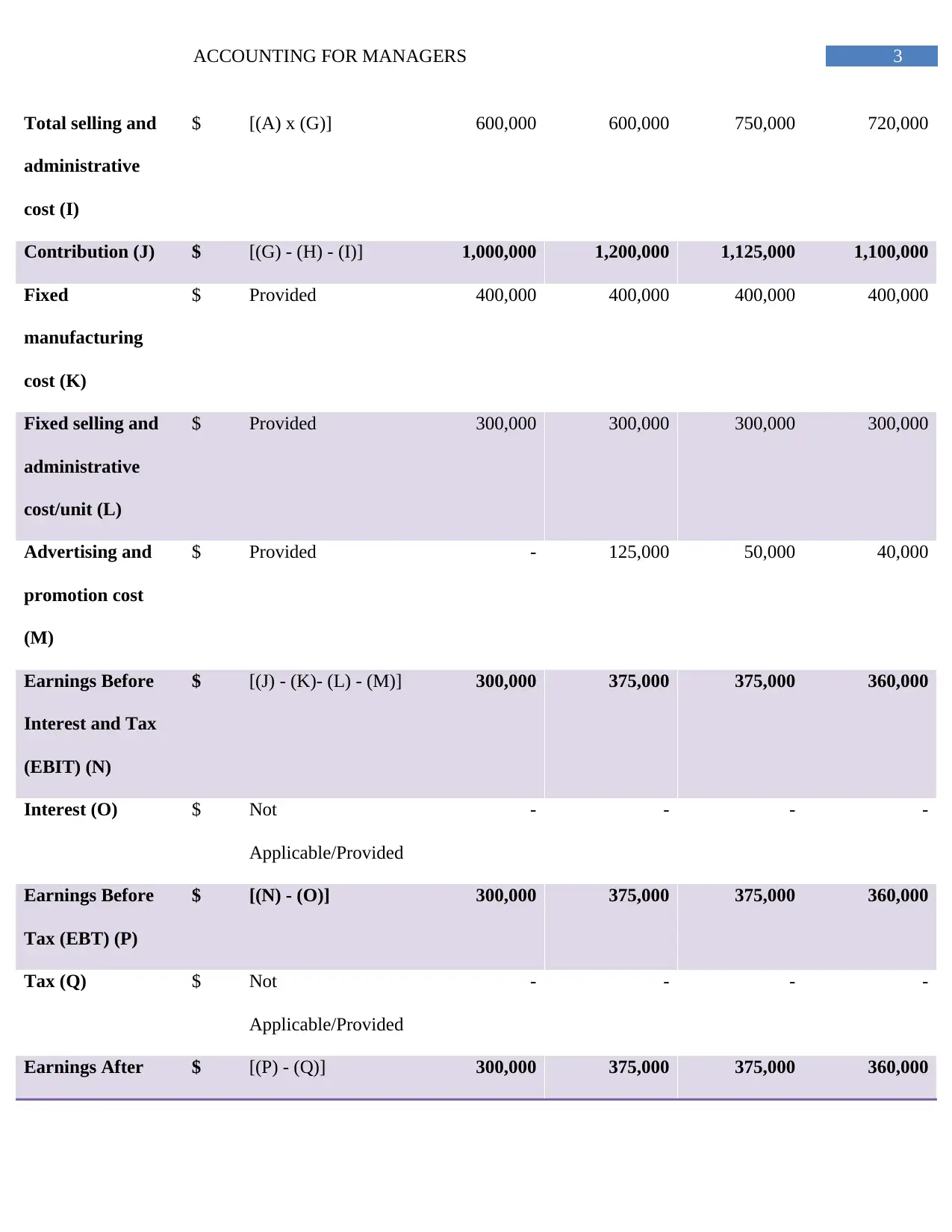

Total selling and

administrative

cost (I)

$ [(A) x (G)] 600,000 600,000 750,000 720,000

Contribution (J) $ [(G) - (H) - (I)] 1,000,000 1,200,000 1,125,000 1,100,000

Fixed

manufacturing

cost (K)

$ Provided 400,000 400,000 400,000 400,000

Fixed selling and

administrative

cost/unit (L)

$ Provided 300,000 300,000 300,000 300,000

Advertising and

promotion cost

(M)

$ Provided - 125,000 50,000 40,000

Earnings Before

Interest and Tax

(EBIT) (N)

$ [(J) - (K)- (L) - (M)] 300,000 375,000 375,000 360,000

Interest (O) $ Not

Applicable/Provided

- - - -

Earnings Before

Tax (EBT) (P)

$ [(N) - (O)] 300,000 375,000 375,000 360,000

Tax (Q) $ Not

Applicable/Provided

- - - -

Earnings After $ [(P) - (Q)] 300,000 375,000 375,000 360,000

Total selling and

administrative

cost (I)

$ [(A) x (G)] 600,000 600,000 750,000 720,000

Contribution (J) $ [(G) - (H) - (I)] 1,000,000 1,200,000 1,125,000 1,100,000

Fixed

manufacturing

cost (K)

$ Provided 400,000 400,000 400,000 400,000

Fixed selling and

administrative

cost/unit (L)

$ Provided 300,000 300,000 300,000 300,000

Advertising and

promotion cost

(M)

$ Provided - 125,000 50,000 40,000

Earnings Before

Interest and Tax

(EBIT) (N)

$ [(J) - (K)- (L) - (M)] 300,000 375,000 375,000 360,000

Interest (O) $ Not

Applicable/Provided

- - - -

Earnings Before

Tax (EBT) (P)

$ [(N) - (O)] 300,000 375,000 375,000 360,000

Tax (Q) $ Not

Applicable/Provided

- - - -

Earnings After $ [(P) - (Q)] 300,000 375,000 375,000 360,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR MANAGERS

Tax (EAT)

To,

The Directors of Bonza Handtools Limited

Date: 04.01.2018

Subject: Evaluation of the three present proposals

Respected Sir,

After detailed elaboration regarding the three present proposals, the report was prepared

through indicating the impact and advantages of the proposals within the company. These are

explained under:

Proposal 1:

Considering the Jan Rossi proposal, the company’s accountant indicated that selling price

requires being $140 per unit for increasing its total profit level. The table above clearly indicates

that the company can observe a profit increase from $300,000 to $375,000 because of which the

amount will boost to $75,000. An increased profit margin can be attained with support of

suitable advertising campaign that has expenses of $125,000 (Schmidt, Götze and Sygulla 2015).

Conversely, the company’s risk level might be increased in case the advertising campaign is not

capable to gather attention of the consumers. Because of this, there will be significant drop in the

company’s promotion and advertising expense.

Proposal 2:

Tax (EAT)

To,

The Directors of Bonza Handtools Limited

Date: 04.01.2018

Subject: Evaluation of the three present proposals

Respected Sir,

After detailed elaboration regarding the three present proposals, the report was prepared

through indicating the impact and advantages of the proposals within the company. These are

explained under:

Proposal 1:

Considering the Jan Rossi proposal, the company’s accountant indicated that selling price

requires being $140 per unit for increasing its total profit level. The table above clearly indicates

that the company can observe a profit increase from $300,000 to $375,000 because of which the

amount will boost to $75,000. An increased profit margin can be attained with support of

suitable advertising campaign that has expenses of $125,000 (Schmidt, Götze and Sygulla 2015).

Conversely, the company’s risk level might be increased in case the advertising campaign is not

capable to gather attention of the consumers. Because of this, there will be significant drop in the

company’s promotion and advertising expense.

Proposal 2:

5ACCOUNTING FOR MANAGERS

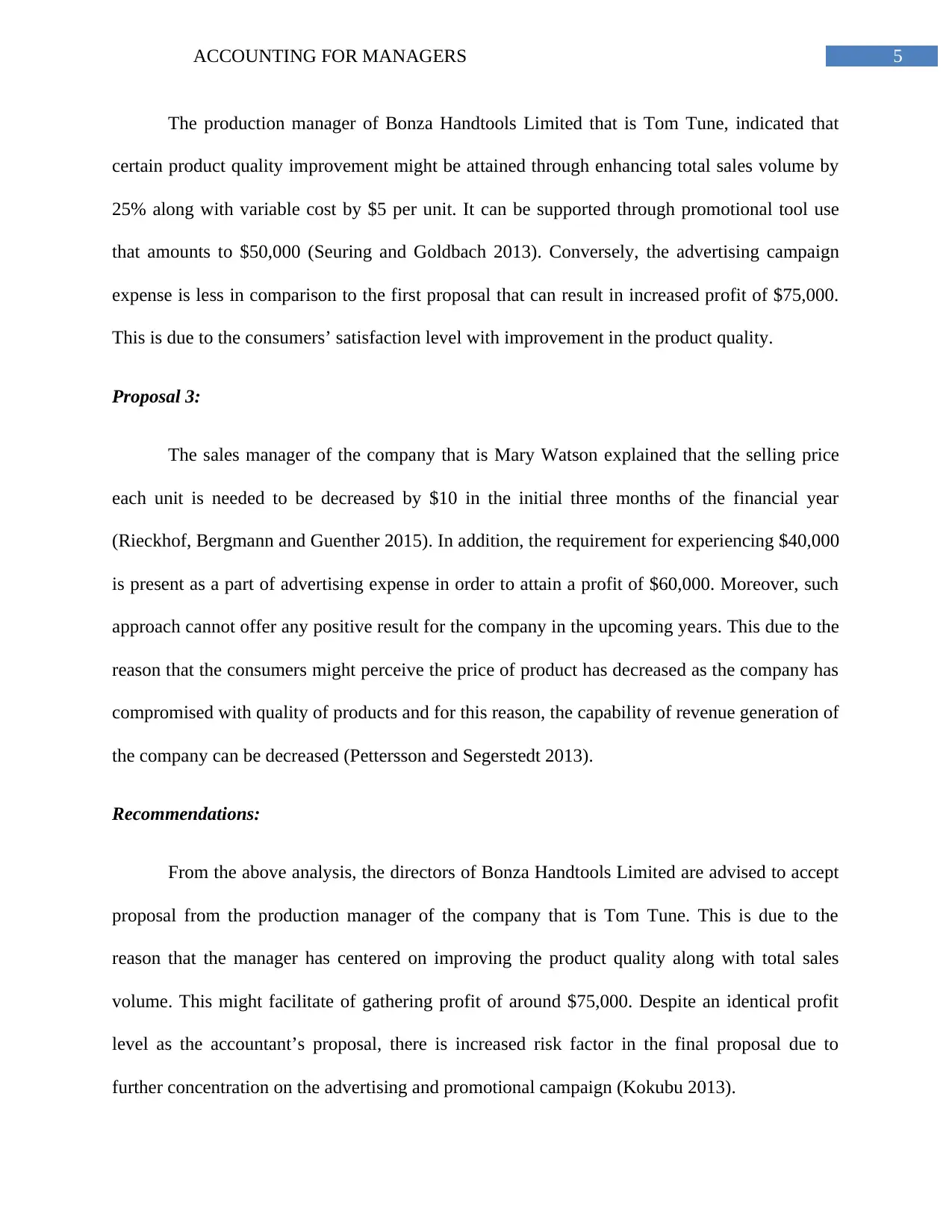

The production manager of Bonza Handtools Limited that is Tom Tune, indicated that

certain product quality improvement might be attained through enhancing total sales volume by

25% along with variable cost by $5 per unit. It can be supported through promotional tool use

that amounts to $50,000 (Seuring and Goldbach 2013). Conversely, the advertising campaign

expense is less in comparison to the first proposal that can result in increased profit of $75,000.

This is due to the consumers’ satisfaction level with improvement in the product quality.

Proposal 3:

The sales manager of the company that is Mary Watson explained that the selling price

each unit is needed to be decreased by $10 in the initial three months of the financial year

(Rieckhof, Bergmann and Guenther 2015). In addition, the requirement for experiencing $40,000

is present as a part of advertising expense in order to attain a profit of $60,000. Moreover, such

approach cannot offer any positive result for the company in the upcoming years. This due to the

reason that the consumers might perceive the price of product has decreased as the company has

compromised with quality of products and for this reason, the capability of revenue generation of

the company can be decreased (Pettersson and Segerstedt 2013).

Recommendations:

From the above analysis, the directors of Bonza Handtools Limited are advised to accept

proposal from the production manager of the company that is Tom Tune. This is due to the

reason that the manager has centered on improving the product quality along with total sales

volume. This might facilitate of gathering profit of around $75,000. Despite an identical profit

level as the accountant’s proposal, there is increased risk factor in the final proposal due to

further concentration on the advertising and promotional campaign (Kokubu 2013).

The production manager of Bonza Handtools Limited that is Tom Tune, indicated that

certain product quality improvement might be attained through enhancing total sales volume by

25% along with variable cost by $5 per unit. It can be supported through promotional tool use

that amounts to $50,000 (Seuring and Goldbach 2013). Conversely, the advertising campaign

expense is less in comparison to the first proposal that can result in increased profit of $75,000.

This is due to the consumers’ satisfaction level with improvement in the product quality.

Proposal 3:

The sales manager of the company that is Mary Watson explained that the selling price

each unit is needed to be decreased by $10 in the initial three months of the financial year

(Rieckhof, Bergmann and Guenther 2015). In addition, the requirement for experiencing $40,000

is present as a part of advertising expense in order to attain a profit of $60,000. Moreover, such

approach cannot offer any positive result for the company in the upcoming years. This due to the

reason that the consumers might perceive the price of product has decreased as the company has

compromised with quality of products and for this reason, the capability of revenue generation of

the company can be decreased (Pettersson and Segerstedt 2013).

Recommendations:

From the above analysis, the directors of Bonza Handtools Limited are advised to accept

proposal from the production manager of the company that is Tom Tune. This is due to the

reason that the manager has centered on improving the product quality along with total sales

volume. This might facilitate of gathering profit of around $75,000. Despite an identical profit

level as the accountant’s proposal, there is increased risk factor in the final proposal due to

further concentration on the advertising and promotional campaign (Kokubu 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR MANAGERS

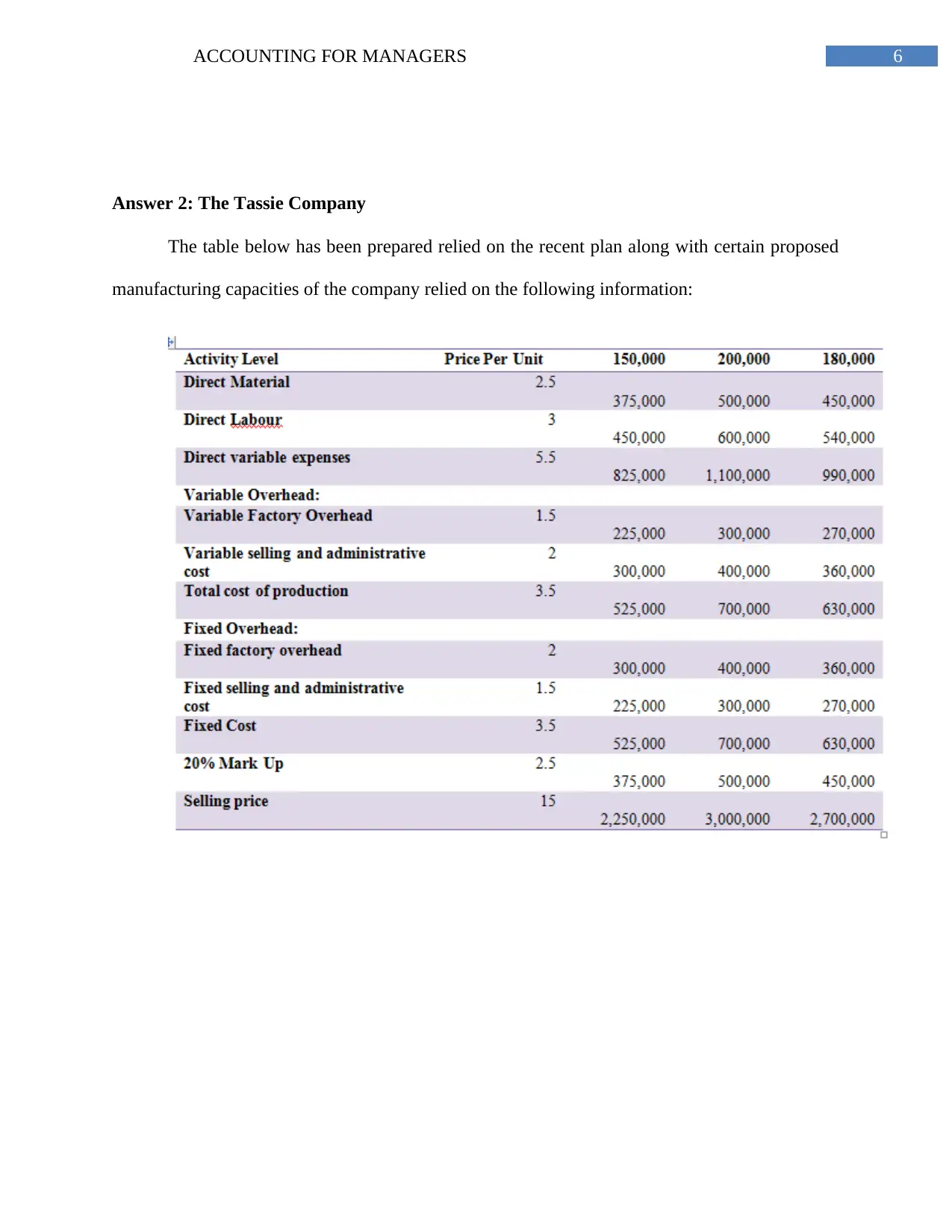

Answer 2: The Tassie Company

The table below has been prepared relied on the recent plan along with certain proposed

manufacturing capacities of the company relied on the following information:

Answer 2: The Tassie Company

The table below has been prepared relied on the recent plan along with certain proposed

manufacturing capacities of the company relied on the following information:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGERS

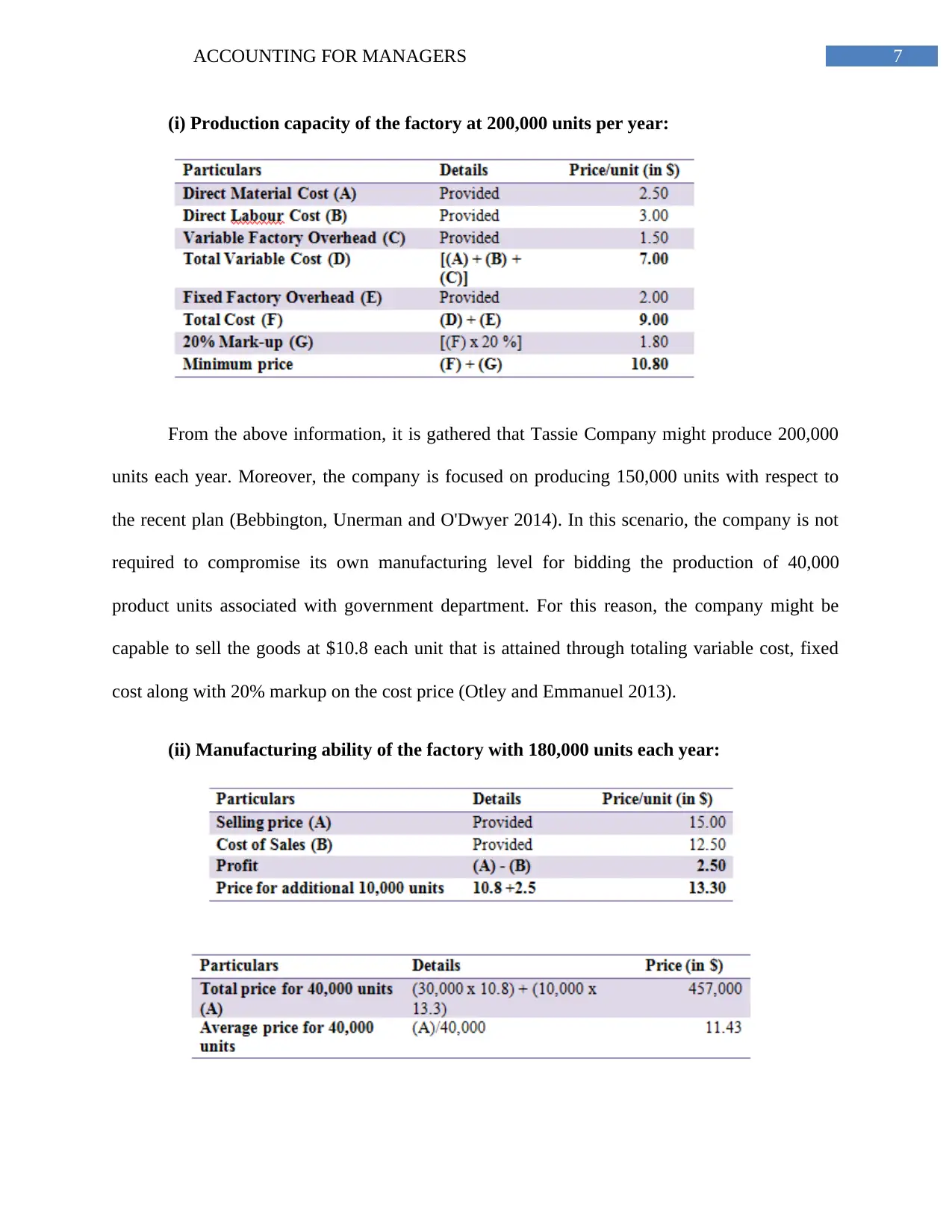

(i) Production capacity of the factory at 200,000 units per year:

From the above information, it is gathered that Tassie Company might produce 200,000

units each year. Moreover, the company is focused on producing 150,000 units with respect to

the recent plan (Bebbington, Unerman and O'Dwyer 2014). In this scenario, the company is not

required to compromise its own manufacturing level for bidding the production of 40,000

product units associated with government department. For this reason, the company might be

capable to sell the goods at $10.8 each unit that is attained through totaling variable cost, fixed

cost along with 20% markup on the cost price (Otley and Emmanuel 2013).

(ii) Manufacturing ability of the factory with 180,000 units each year:

(i) Production capacity of the factory at 200,000 units per year:

From the above information, it is gathered that Tassie Company might produce 200,000

units each year. Moreover, the company is focused on producing 150,000 units with respect to

the recent plan (Bebbington, Unerman and O'Dwyer 2014). In this scenario, the company is not

required to compromise its own manufacturing level for bidding the production of 40,000

product units associated with government department. For this reason, the company might be

capable to sell the goods at $10.8 each unit that is attained through totaling variable cost, fixed

cost along with 20% markup on the cost price (Otley and Emmanuel 2013).

(ii) Manufacturing ability of the factory with 180,000 units each year:

8ACCOUNTING FOR MANAGERS

Relied on the current situation, the Tassie Company might manufacture more than

180,000 units each year and conversely, the present production level is around 150,000 units

each year. For this reason, the company is needed to give away 10,000 units of individual

production, within which it attains profit of around $2.50 each unit in order to accept the

government contrast (Drury 2013). Therefore, for initial beginning 30,000 units, the first price

can be $10.80 and for some more units, the amount might be $13.30 each unit. Moreover, the

overall average price of 40,000 units has been recorded at $11.43 (Klychova et al. 2015).

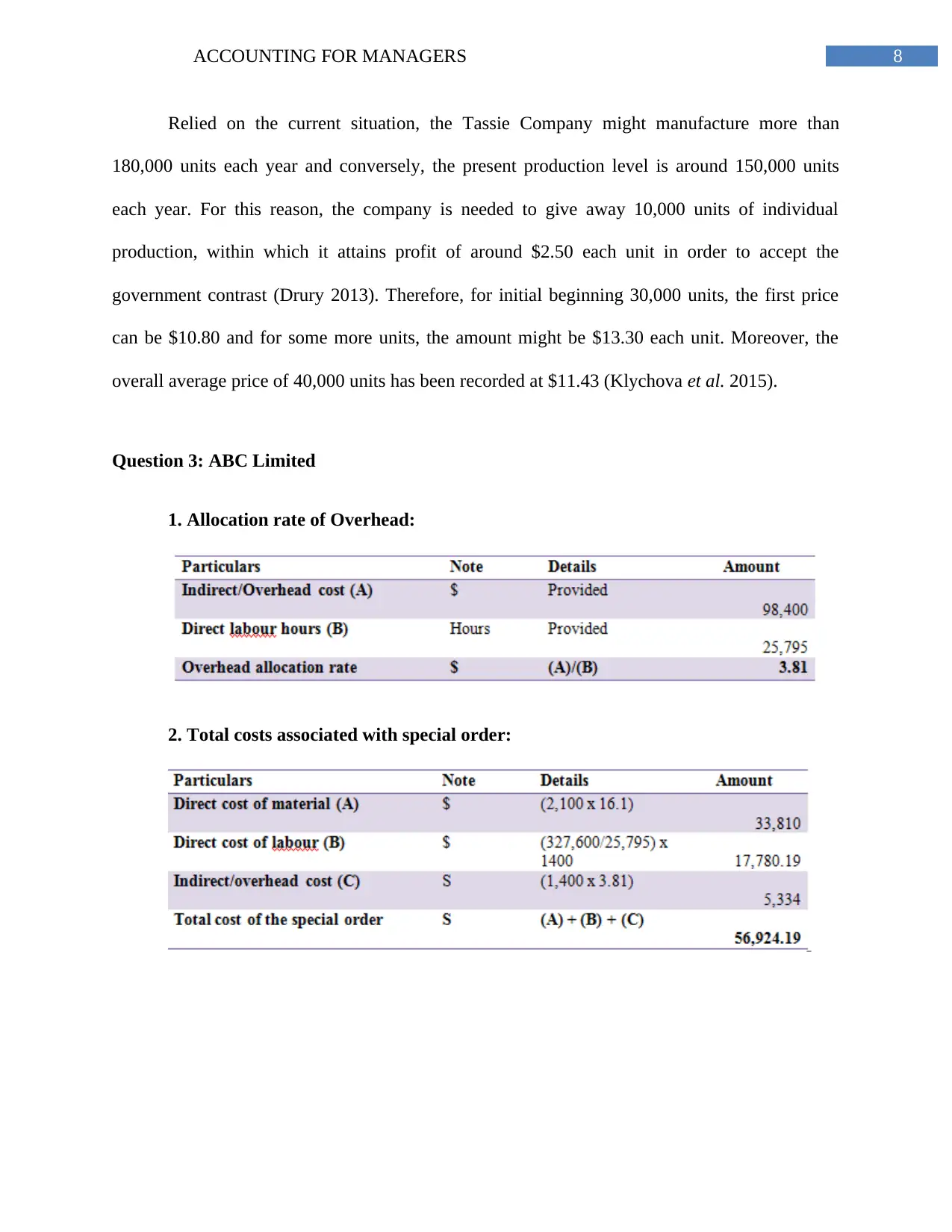

Question 3: ABC Limited

1. Allocation rate of Overhead:

2. Total costs associated with special order:

Relied on the current situation, the Tassie Company might manufacture more than

180,000 units each year and conversely, the present production level is around 150,000 units

each year. For this reason, the company is needed to give away 10,000 units of individual

production, within which it attains profit of around $2.50 each unit in order to accept the

government contrast (Drury 2013). Therefore, for initial beginning 30,000 units, the first price

can be $10.80 and for some more units, the amount might be $13.30 each unit. Moreover, the

overall average price of 40,000 units has been recorded at $11.43 (Klychova et al. 2015).

Question 3: ABC Limited

1. Allocation rate of Overhead:

2. Total costs associated with special order:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR MANAGERS

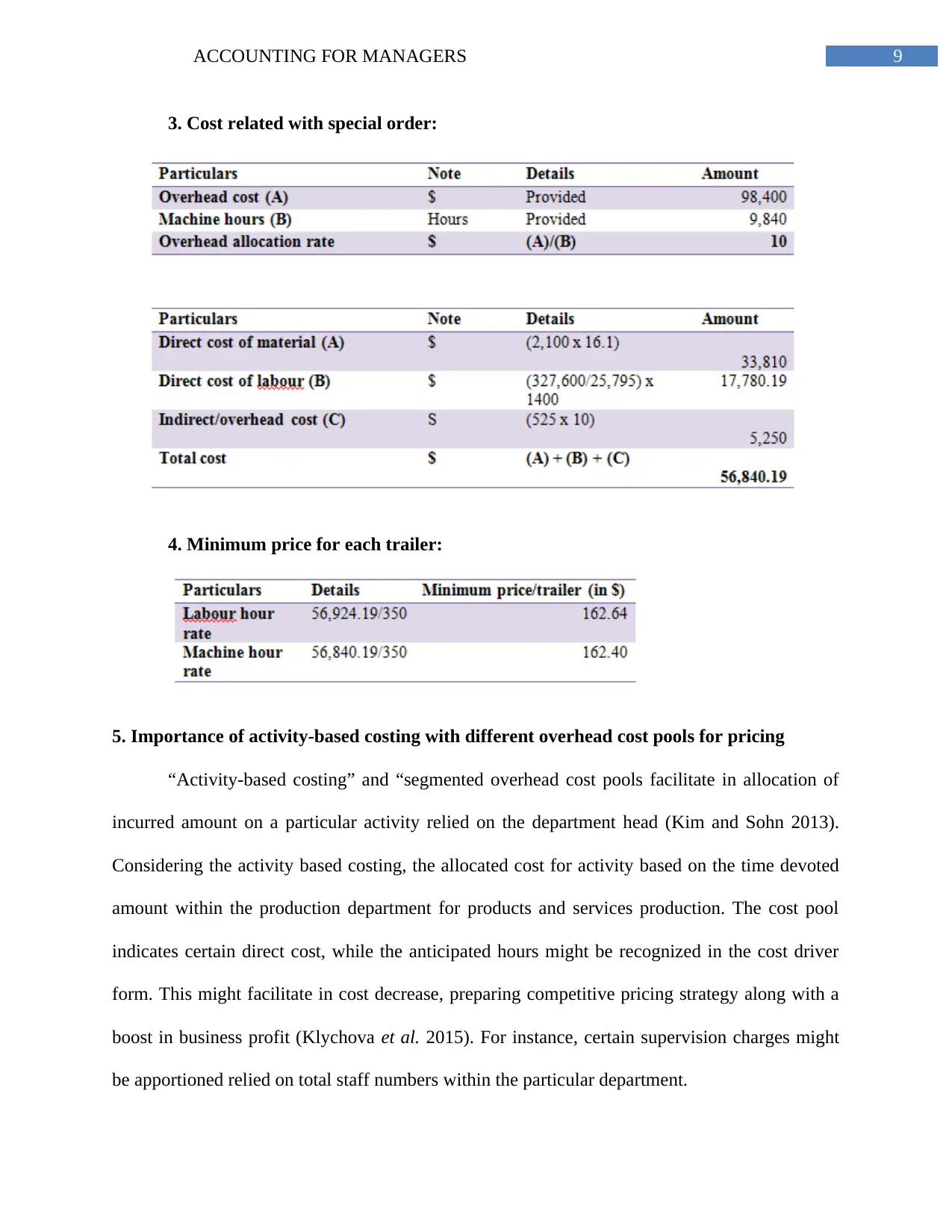

3. Cost related with special order:

4. Minimum price for each trailer:

5. Importance of activity-based costing with different overhead cost pools for pricing

“Activity-based costing” and “segmented overhead cost pools facilitate in allocation of

incurred amount on a particular activity relied on the department head (Kim and Sohn 2013).

Considering the activity based costing, the allocated cost for activity based on the time devoted

amount within the production department for products and services production. The cost pool

indicates certain direct cost, while the anticipated hours might be recognized in the cost driver

form. This might facilitate in cost decrease, preparing competitive pricing strategy along with a

boost in business profit (Klychova et al. 2015). For instance, certain supervision charges might

be apportioned relied on total staff numbers within the particular department.

3. Cost related with special order:

4. Minimum price for each trailer:

5. Importance of activity-based costing with different overhead cost pools for pricing

“Activity-based costing” and “segmented overhead cost pools facilitate in allocation of

incurred amount on a particular activity relied on the department head (Kim and Sohn 2013).

Considering the activity based costing, the allocated cost for activity based on the time devoted

amount within the production department for products and services production. The cost pool

indicates certain direct cost, while the anticipated hours might be recognized in the cost driver

form. This might facilitate in cost decrease, preparing competitive pricing strategy along with a

boost in business profit (Klychova et al. 2015). For instance, certain supervision charges might

be apportioned relied on total staff numbers within the particular department.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR MANAGERS

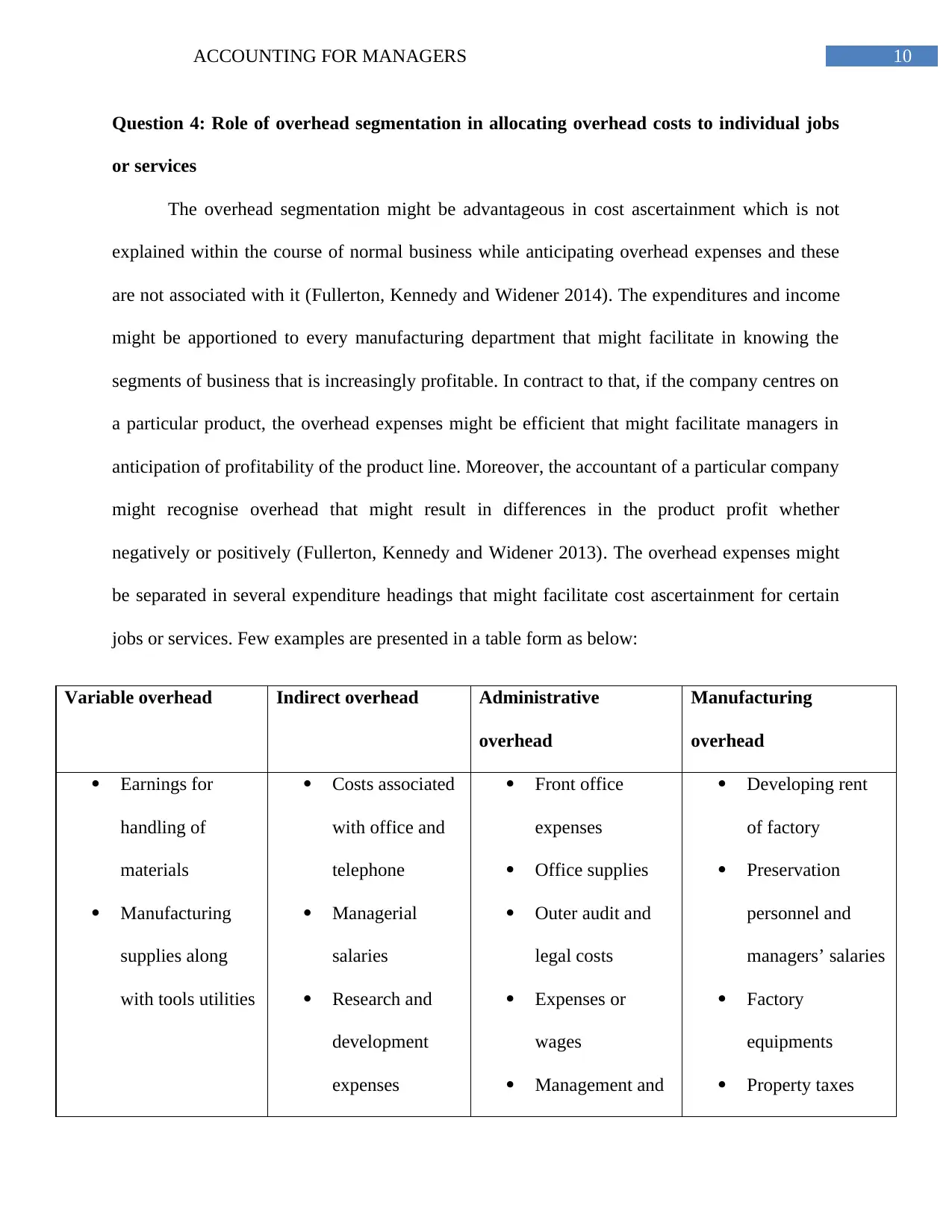

Question 4: Role of overhead segmentation in allocating overhead costs to individual jobs

or services

The overhead segmentation might be advantageous in cost ascertainment which is not

explained within the course of normal business while anticipating overhead expenses and these

are not associated with it (Fullerton, Kennedy and Widener 2014). The expenditures and income

might be apportioned to every manufacturing department that might facilitate in knowing the

segments of business that is increasingly profitable. In contract to that, if the company centres on

a particular product, the overhead expenses might be efficient that might facilitate managers in

anticipation of profitability of the product line. Moreover, the accountant of a particular company

might recognise overhead that might result in differences in the product profit whether

negatively or positively (Fullerton, Kennedy and Widener 2013). The overhead expenses might

be separated in several expenditure headings that might facilitate cost ascertainment for certain

jobs or services. Few examples are presented in a table form as below:

Variable overhead Indirect overhead Administrative

overhead

Manufacturing

overhead

Earnings for

handling of

materials

Manufacturing

supplies along

with tools utilities

Costs associated

with office and

telephone

Managerial

salaries

Research and

development

expenses

Front office

expenses

Office supplies

Outer audit and

legal costs

Expenses or

wages

Management and

Developing rent

of factory

Preservation

personnel and

managers’ salaries

Factory

equipments

Property taxes

Question 4: Role of overhead segmentation in allocating overhead costs to individual jobs

or services

The overhead segmentation might be advantageous in cost ascertainment which is not

explained within the course of normal business while anticipating overhead expenses and these

are not associated with it (Fullerton, Kennedy and Widener 2014). The expenditures and income

might be apportioned to every manufacturing department that might facilitate in knowing the

segments of business that is increasingly profitable. In contract to that, if the company centres on

a particular product, the overhead expenses might be efficient that might facilitate managers in

anticipation of profitability of the product line. Moreover, the accountant of a particular company

might recognise overhead that might result in differences in the product profit whether

negatively or positively (Fullerton, Kennedy and Widener 2013). The overhead expenses might

be separated in several expenditure headings that might facilitate cost ascertainment for certain

jobs or services. Few examples are presented in a table form as below:

Variable overhead Indirect overhead Administrative

overhead

Manufacturing

overhead

Earnings for

handling of

materials

Manufacturing

supplies along

with tools utilities

Costs associated

with office and

telephone

Managerial

salaries

Research and

development

expenses

Front office

expenses

Office supplies

Outer audit and

legal costs

Expenses or

wages

Management and

Developing rent

of factory

Preservation

personnel and

managers’ salaries

Factory

equipments

Property taxes

11ACCOUNTING FOR MANAGERS

Legal fees

Fees of

accounting and

auditing

selling utilities

Sales office and

lease of

administration

Janitorial staffs

Wages

Legal fees

Fees of

accounting and

auditing

selling utilities

Sales office and

lease of

administration

Janitorial staffs

Wages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.