Financial Analysis Report: Liquidity, Ratios, and Stakeholder Analysis

VerifiedAdded on 2020/03/04

|5

|1748

|59

Report

AI Summary

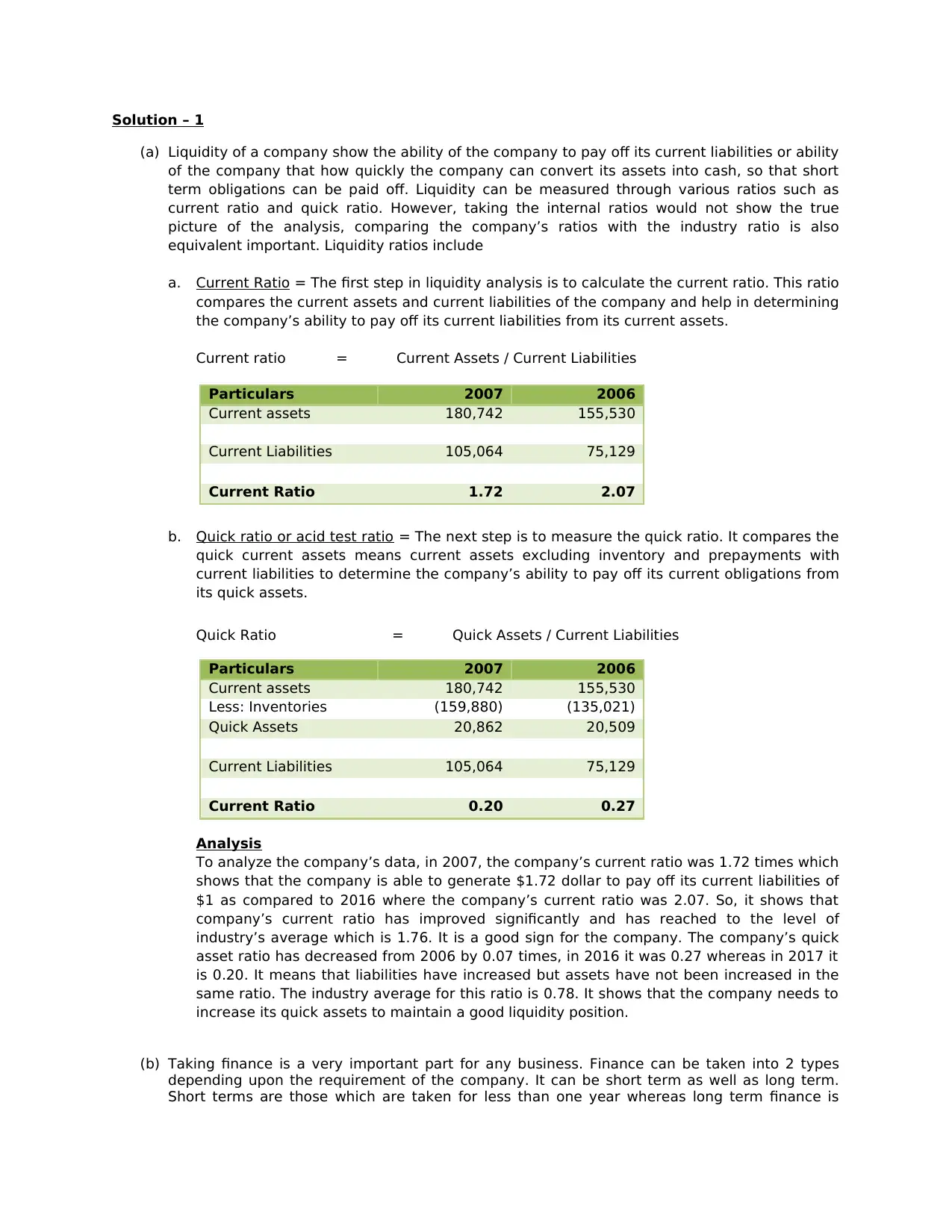

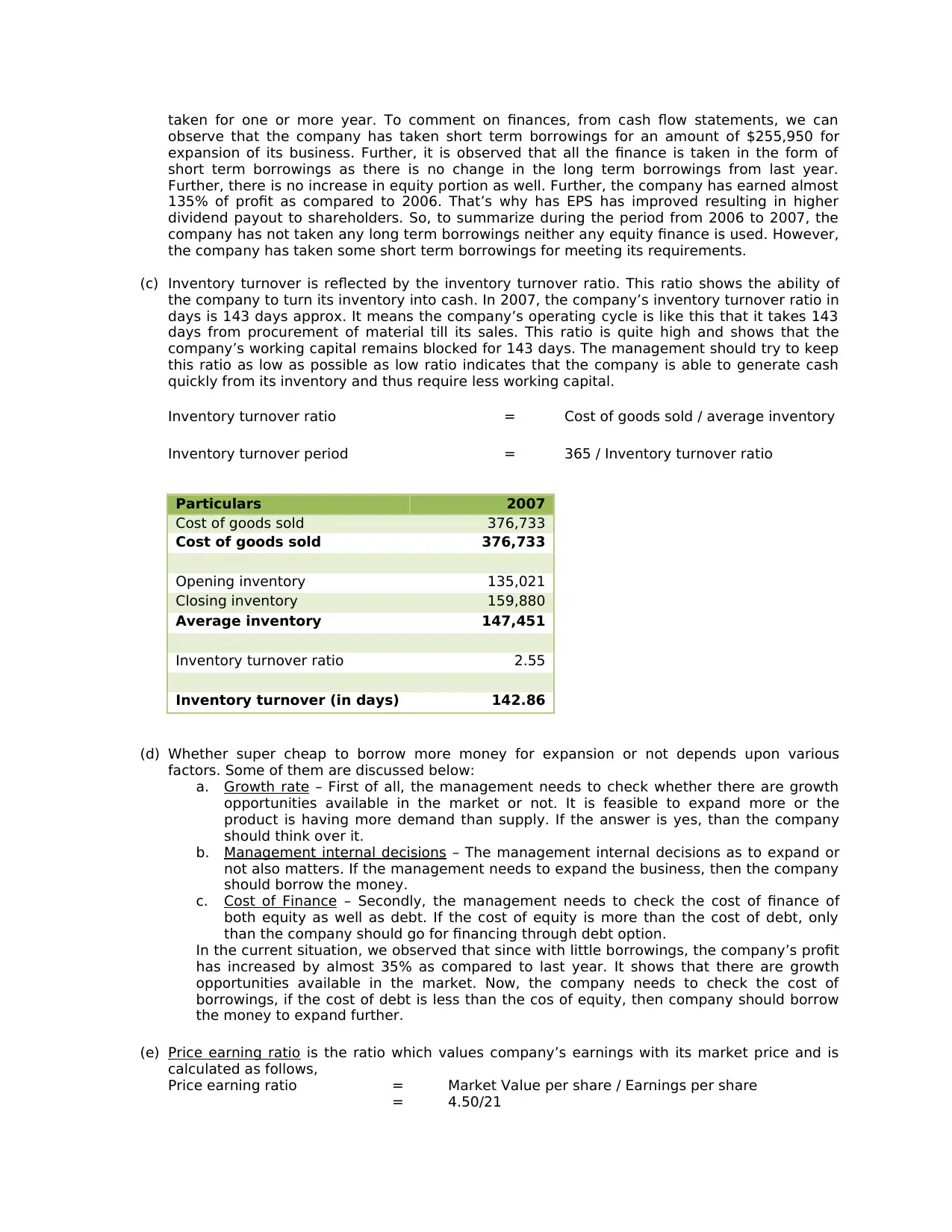

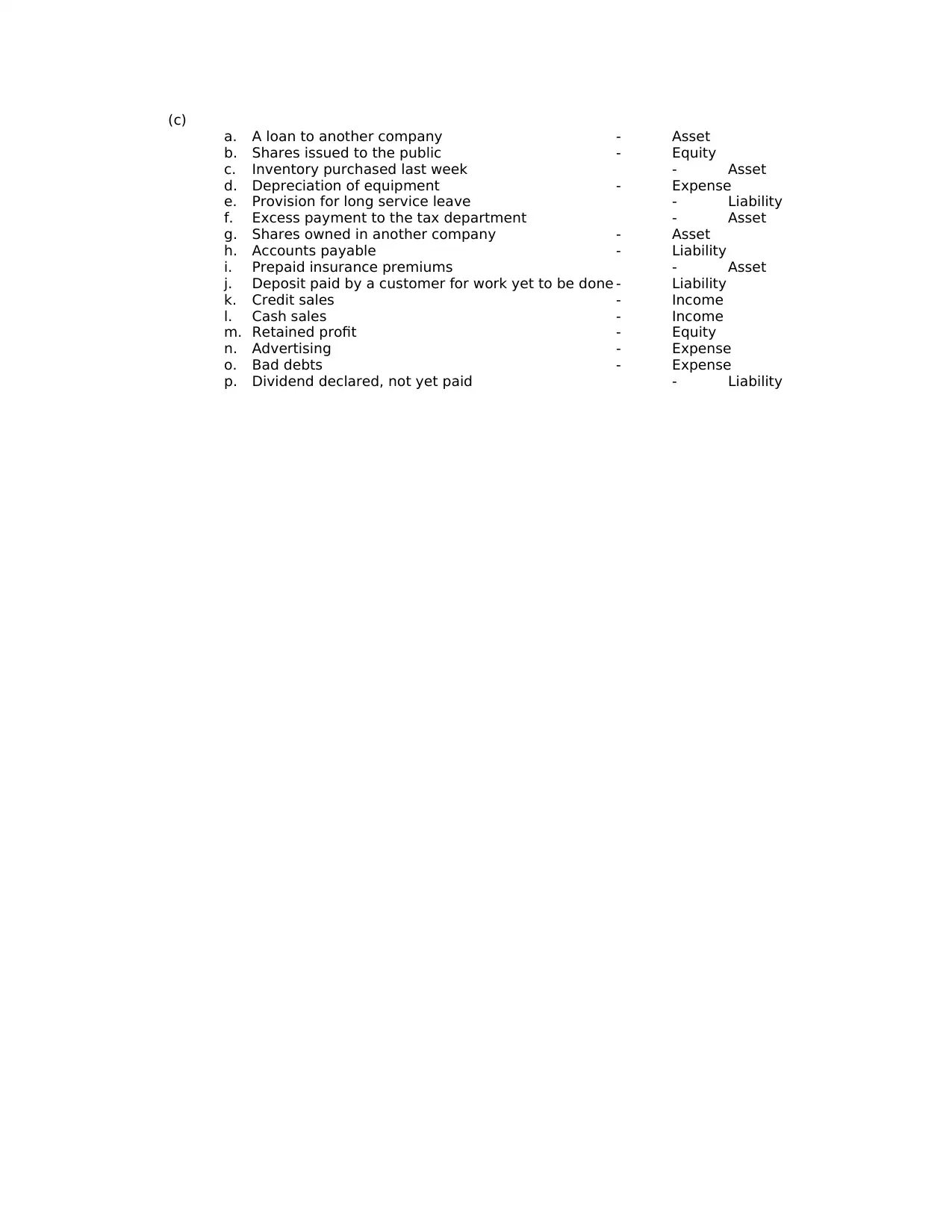

This report provides a financial analysis of a company, focusing on liquidity and key financial ratios. The analysis includes the calculation and interpretation of the current ratio, quick ratio, and inventory turnover ratio to assess the company's ability to meet its short-term obligations and manage its working capital. The report also examines the company's financing strategies, including short-term borrowings and the use of equity, and discusses the impact of these decisions on profitability and shareholder value. Furthermore, the report evaluates the company's price-earnings ratio and dividend yield ratio to assess its market valuation and attractiveness to investors. The report also identifies and explains the information needs of different users of financial statements, including equity shareholders, investors/lenders, potential investors/creditors/suppliers, and government agencies. Finally, the report categorizes various financial transactions as assets, liabilities, equity, income, or expenses, providing a comprehensive overview of the company's financial position and performance.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.