Financial Analysis Report: Farsons and Heiniken Performance

VerifiedAdded on 2023/01/18

|24

|3731

|81

Report

AI Summary

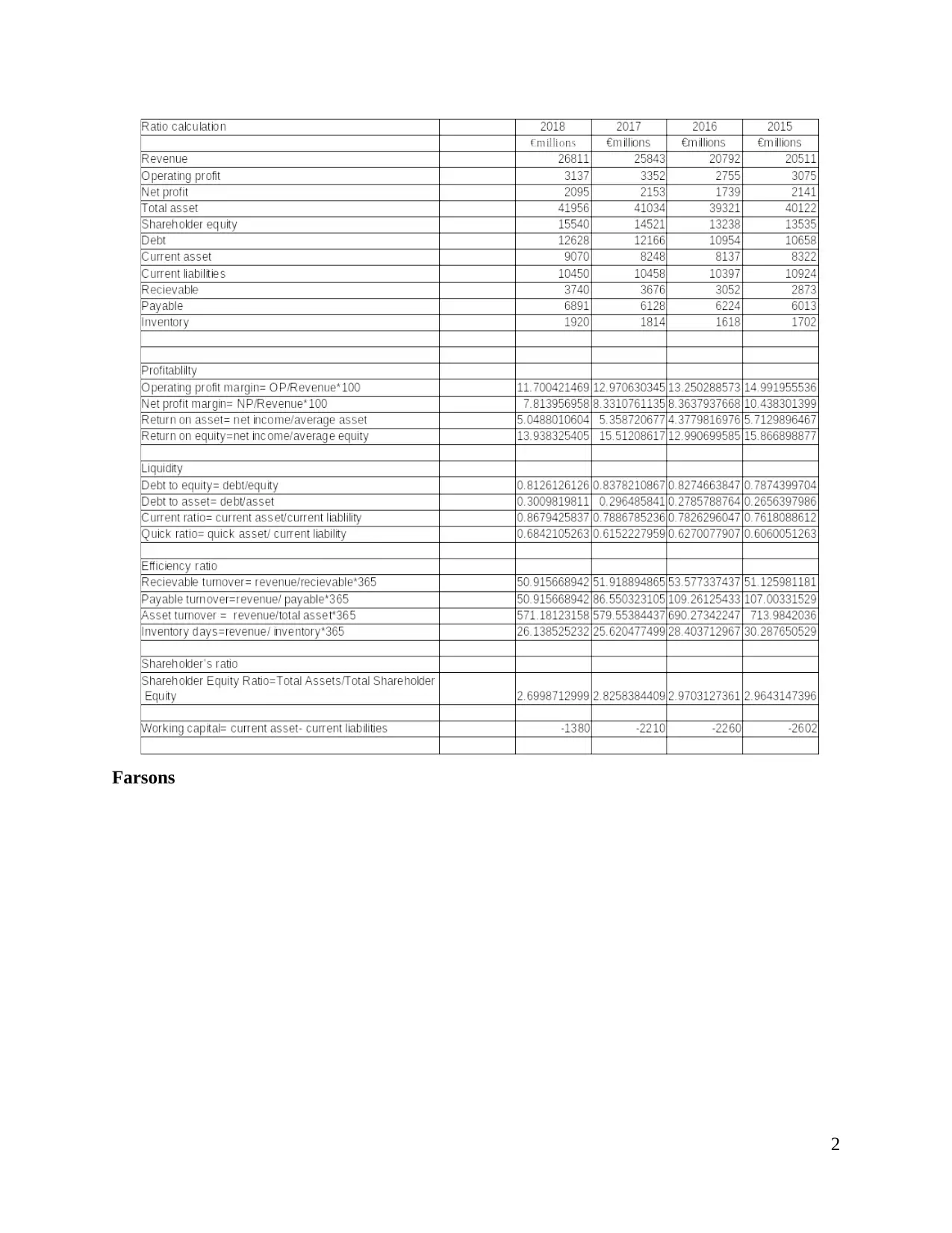

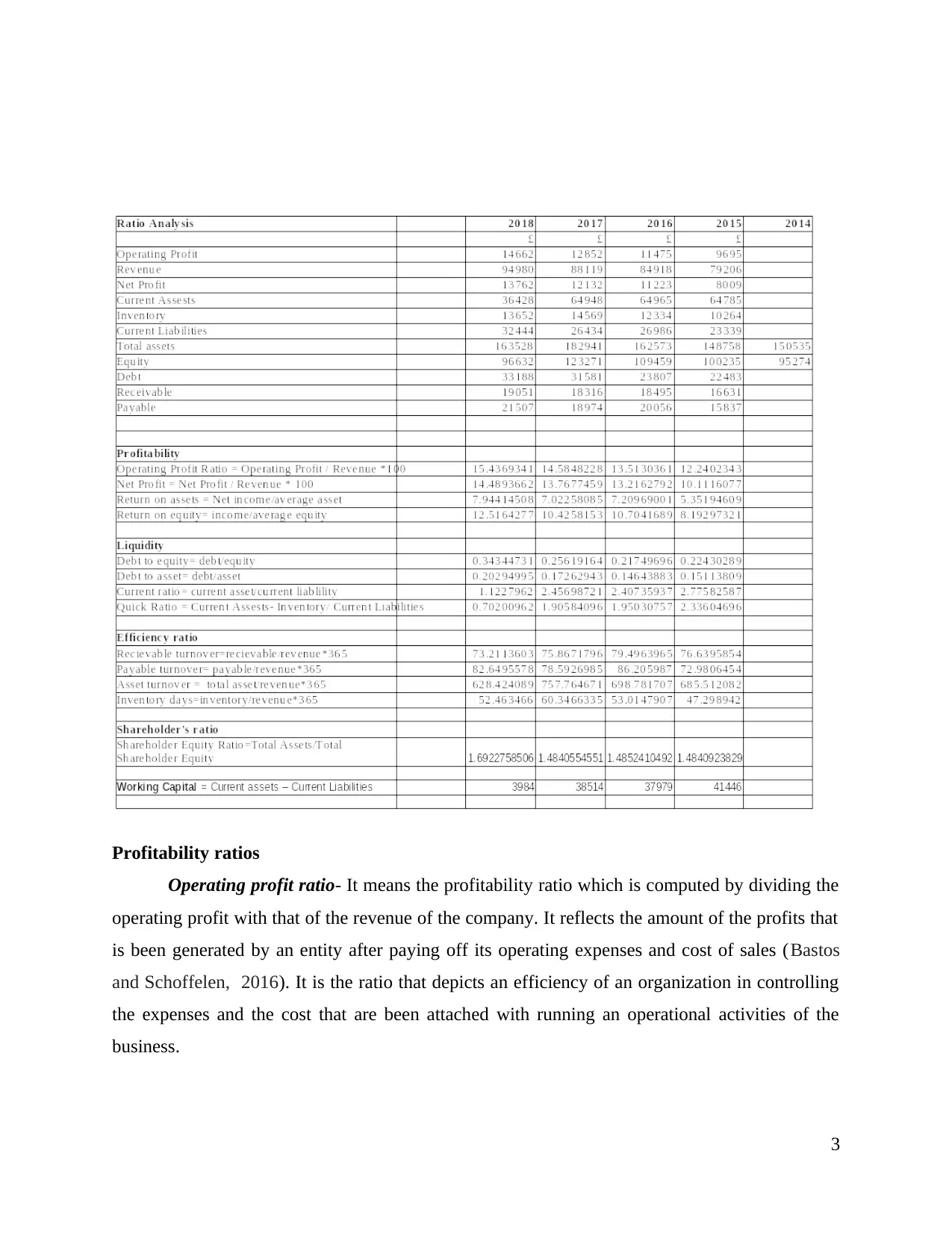

This report provides a comprehensive financial analysis comparing Farsons and Heiniken, two companies in the beverage industry. The analysis employs various financial techniques including ratio analysis (profitability, liquidity, leverage, and turnover ratios), horizontal and vertical analysis, to assess the companies' financial performance and position over a specific period. The report delves into the significance of working capital and cash flow statements for both companies, highlighting their impact on decision-making. The analysis offers insights into each company's strengths and weaknesses, providing a comparative view of their financial health and operational efficiency. The report evaluates key financial metrics such as operating profit ratio, net profit ratio, ROA, ROE, current ratio, quick ratio, debt-to-equity ratio, and asset turnover, among others. The findings offer valuable insights into the companies' ability to manage assets, meet obligations, and generate returns for shareholders. The report's conclusion summarizes the key findings and offers perspectives on the overall financial performance of Farsons and Heiniken.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.