Managerial Finance Report: Financial Analysis of Tesco and Sainsburry

VerifiedAdded on 2022/12/30

|13

|3522

|24

Report

AI Summary

This report provides a detailed financial analysis of Tesco and Sainsburry, two major retail companies. It begins with an introduction to financial management and its importance for organizations. The report then delves into ratio analysis, calculating and comparing key financial ratios such as current ratio, quick ratio, gross profit ratio, P/E ratio, net profit ratio, capital gearing ratio, return on capital employed, inventory turnover, dividend payout ratio, and earnings per share for both companies for the years 2018 and 2019. The analysis highlights the strengths and weaknesses of each company based on these ratios. Furthermore, the report explores investment appraisal techniques, though details are limited in the provided text. Finally, it discusses the limitations of both ratio analysis and investment appraisal techniques. The report concludes with recommendations for the companies based on the financial analysis.

Managerial

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1.................................................................................................................................3

Ratio analysis for the company Tesco and Sainsburry:...............................................................3

Recommendations:.......................................................................................................................7

Limitations for ratio analysis in order to know financial position:..............................................8

PORTFOLIO 2.................................................................................................................................9

Investment appraisal techniques:.................................................................................................9

Limitations for investment appraisal techniques for knowing better investment options:........10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1.................................................................................................................................3

Ratio analysis for the company Tesco and Sainsburry:...............................................................3

Recommendations:.......................................................................................................................7

Limitations for ratio analysis in order to know financial position:..............................................8

PORTFOLIO 2.................................................................................................................................9

Investment appraisal techniques:.................................................................................................9

Limitations for investment appraisal techniques for knowing better investment options:........10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

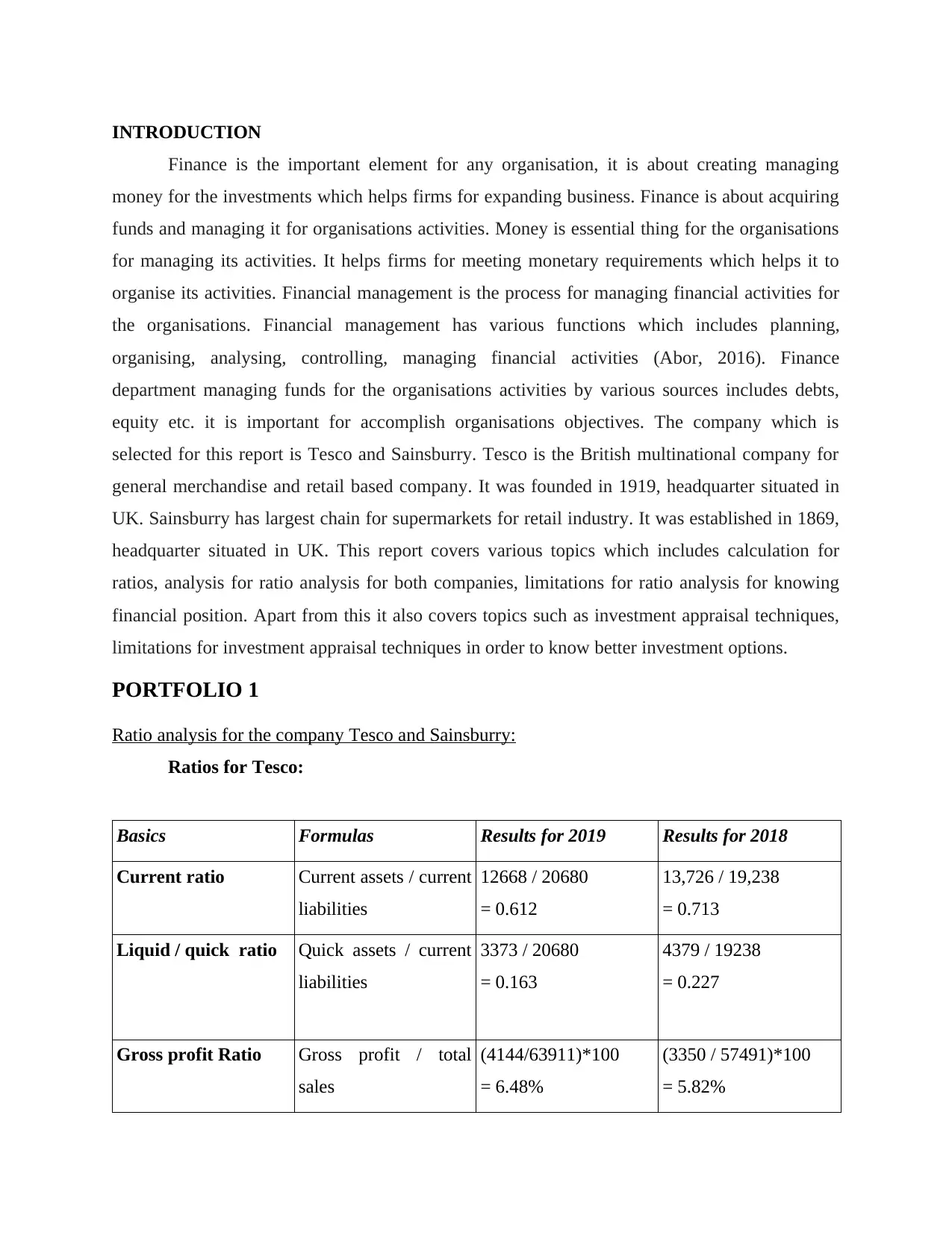

INTRODUCTION

Finance is the important element for any organisation, it is about creating managing

money for the investments which helps firms for expanding business. Finance is about acquiring

funds and managing it for organisations activities. Money is essential thing for the organisations

for managing its activities. It helps firms for meeting monetary requirements which helps it to

organise its activities. Financial management is the process for managing financial activities for

the organisations. Financial management has various functions which includes planning,

organising, analysing, controlling, managing financial activities (Abor, 2016). Finance

department managing funds for the organisations activities by various sources includes debts,

equity etc. it is important for accomplish organisations objectives. The company which is

selected for this report is Tesco and Sainsburry. Tesco is the British multinational company for

general merchandise and retail based company. It was founded in 1919, headquarter situated in

UK. Sainsburry has largest chain for supermarkets for retail industry. It was established in 1869,

headquarter situated in UK. This report covers various topics which includes calculation for

ratios, analysis for ratio analysis for both companies, limitations for ratio analysis for knowing

financial position. Apart from this it also covers topics such as investment appraisal techniques,

limitations for investment appraisal techniques in order to know better investment options.

PORTFOLIO 1

Ratio analysis for the company Tesco and Sainsburry:

Ratios for Tesco:

Basics Formulas Results for 2019 Results for 2018

Current ratio Current assets / current

liabilities

12668 / 20680

= 0.612

13,726 / 19,238

= 0.713

Liquid / quick ratio Quick assets / current

liabilities

3373 / 20680

= 0.163

4379 / 19238

= 0.227

Gross profit Ratio Gross profit / total

sales

(4144/63911)*100

= 6.48%

(3350 / 57491)*100

= 5.82%

Finance is the important element for any organisation, it is about creating managing

money for the investments which helps firms for expanding business. Finance is about acquiring

funds and managing it for organisations activities. Money is essential thing for the organisations

for managing its activities. It helps firms for meeting monetary requirements which helps it to

organise its activities. Financial management is the process for managing financial activities for

the organisations. Financial management has various functions which includes planning,

organising, analysing, controlling, managing financial activities (Abor, 2016). Finance

department managing funds for the organisations activities by various sources includes debts,

equity etc. it is important for accomplish organisations objectives. The company which is

selected for this report is Tesco and Sainsburry. Tesco is the British multinational company for

general merchandise and retail based company. It was founded in 1919, headquarter situated in

UK. Sainsburry has largest chain for supermarkets for retail industry. It was established in 1869,

headquarter situated in UK. This report covers various topics which includes calculation for

ratios, analysis for ratio analysis for both companies, limitations for ratio analysis for knowing

financial position. Apart from this it also covers topics such as investment appraisal techniques,

limitations for investment appraisal techniques in order to know better investment options.

PORTFOLIO 1

Ratio analysis for the company Tesco and Sainsburry:

Ratios for Tesco:

Basics Formulas Results for 2019 Results for 2018

Current ratio Current assets / current

liabilities

12668 / 20680

= 0.612

13,726 / 19,238

= 0.713

Liquid / quick ratio Quick assets / current

liabilities

3373 / 20680

= 0.163

4379 / 19238

= 0.227

Gross profit Ratio Gross profit / total

sales

(4144/63911)*100

= 6.48%

(3350 / 57491)*100

= 5.82%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

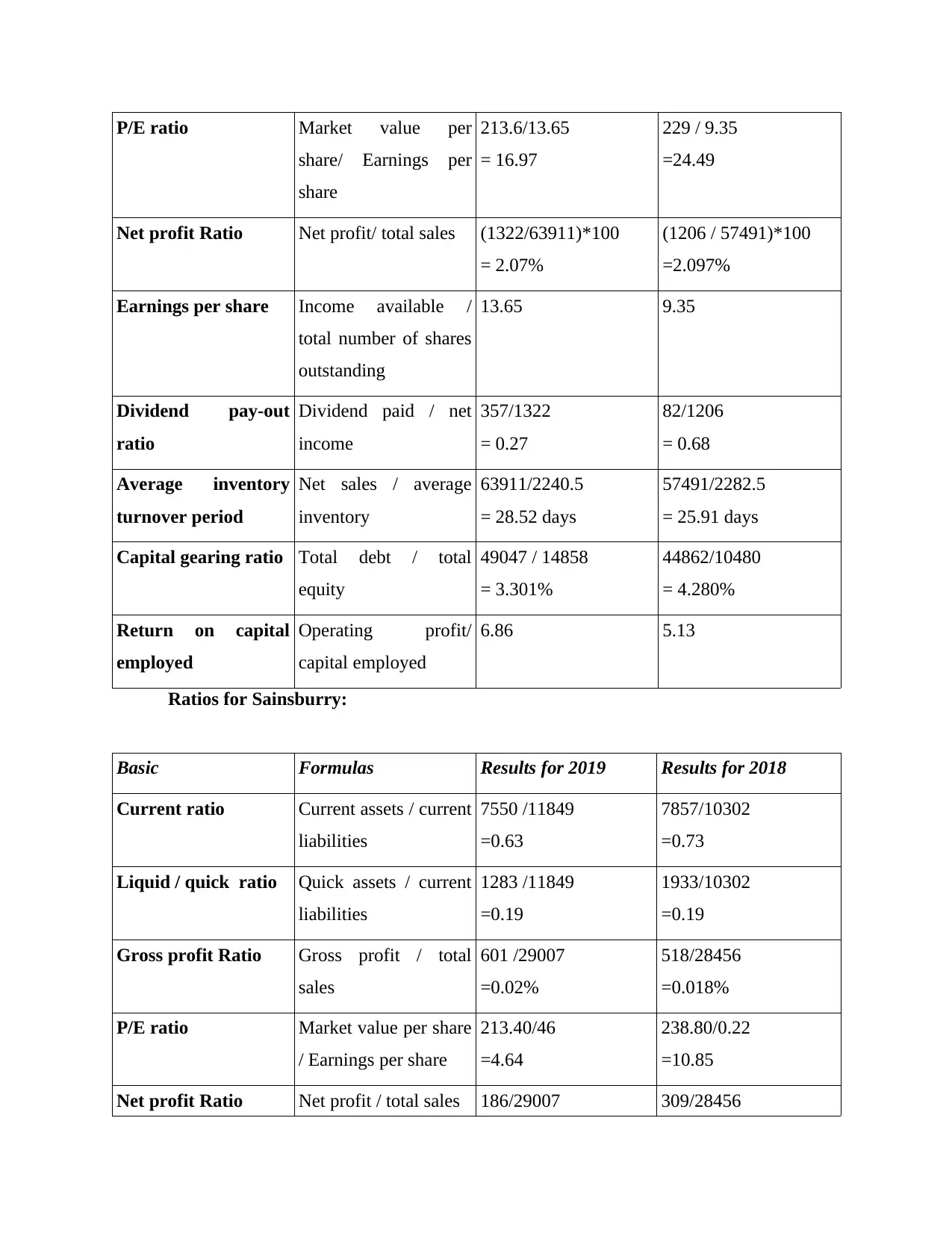

P/E ratio Market value per

share/ Earnings per

share

213.6/13.65

= 16.97

229 / 9.35

=24.49

Net profit Ratio Net profit/ total sales (1322/63911)*100

= 2.07%

(1206 / 57491)*100

=2.097%

Earnings per share Income available /

total number of shares

outstanding

13.65 9.35

Dividend pay-out

ratio

Dividend paid / net

income

357/1322

= 0.27

82/1206

= 0.68

Average inventory

turnover period

Net sales / average

inventory

63911/2240.5

= 28.52 days

57491/2282.5

= 25.91 days

Capital gearing ratio Total debt / total

equity

49047 / 14858

= 3.301%

44862/10480

= 4.280%

Return on capital

employed

Operating profit/

capital employed

6.86 5.13

Ratios for Sainsburry:

Basic Formulas Results for 2019 Results for 2018

Current ratio Current assets / current

liabilities

7550 /11849

=0.63

7857/10302

=0.73

Liquid / quick ratio Quick assets / current

liabilities

1283 /11849

=0.19

1933/10302

=0.19

Gross profit Ratio Gross profit / total

sales

601 /29007

=0.02%

518/28456

=0.018%

P/E ratio Market value per share

/ Earnings per share

213.40/46

=4.64

238.80/0.22

=10.85

Net profit Ratio Net profit / total sales 186/29007 309/28456

share/ Earnings per

share

213.6/13.65

= 16.97

229 / 9.35

=24.49

Net profit Ratio Net profit/ total sales (1322/63911)*100

= 2.07%

(1206 / 57491)*100

=2.097%

Earnings per share Income available /

total number of shares

outstanding

13.65 9.35

Dividend pay-out

ratio

Dividend paid / net

income

357/1322

= 0.27

82/1206

= 0.68

Average inventory

turnover period

Net sales / average

inventory

63911/2240.5

= 28.52 days

57491/2282.5

= 25.91 days

Capital gearing ratio Total debt / total

equity

49047 / 14858

= 3.301%

44862/10480

= 4.280%

Return on capital

employed

Operating profit/

capital employed

6.86 5.13

Ratios for Sainsburry:

Basic Formulas Results for 2019 Results for 2018

Current ratio Current assets / current

liabilities

7550 /11849

=0.63

7857/10302

=0.73

Liquid / quick ratio Quick assets / current

liabilities

1283 /11849

=0.19

1933/10302

=0.19

Gross profit Ratio Gross profit / total

sales

601 /29007

=0.02%

518/28456

=0.018%

P/E ratio Market value per share

/ Earnings per share

213.40/46

=4.64

238.80/0.22

=10.85

Net profit Ratio Net profit / total sales 186/29007 309/28456

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

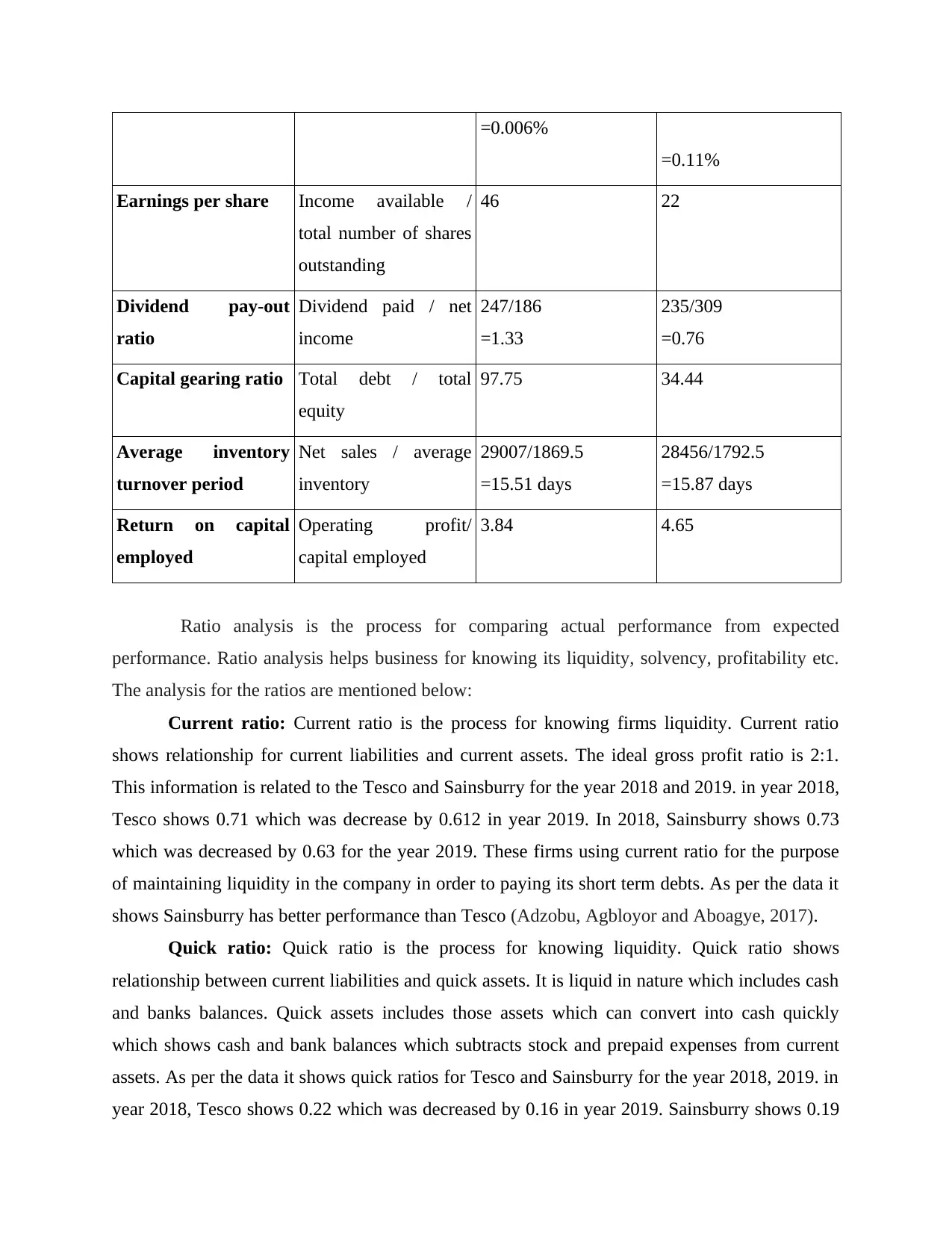

=0.006%

=0.11%

Earnings per share Income available /

total number of shares

outstanding

46 22

Dividend pay-out

ratio

Dividend paid / net

income

247/186

=1.33

235/309

=0.76

Capital gearing ratio Total debt / total

equity

97.75 34.44

Average inventory

turnover period

Net sales / average

inventory

29007/1869.5

=15.51 days

28456/1792.5

=15.87 days

Return on capital

employed

Operating profit/

capital employed

3.84 4.65

Ratio analysis is the process for comparing actual performance from expected

performance. Ratio analysis helps business for knowing its liquidity, solvency, profitability etc.

The analysis for the ratios are mentioned below:

Current ratio: Current ratio is the process for knowing firms liquidity. Current ratio

shows relationship for current liabilities and current assets. The ideal gross profit ratio is 2:1.

This information is related to the Tesco and Sainsburry for the year 2018 and 2019. in year 2018,

Tesco shows 0.71 which was decrease by 0.612 in year 2019. In 2018, Sainsburry shows 0.73

which was decreased by 0.63 for the year 2019. These firms using current ratio for the purpose

of maintaining liquidity in the company in order to paying its short term debts. As per the data it

shows Sainsburry has better performance than Tesco (Adzobu, Agbloyor and Aboagye, 2017).

Quick ratio: Quick ratio is the process for knowing liquidity. Quick ratio shows

relationship between current liabilities and quick assets. It is liquid in nature which includes cash

and banks balances. Quick assets includes those assets which can convert into cash quickly

which shows cash and bank balances which subtracts stock and prepaid expenses from current

assets. As per the data it shows quick ratios for Tesco and Sainsburry for the year 2018, 2019. in

year 2018, Tesco shows 0.22 which was decreased by 0.16 in year 2019. Sainsburry shows 0.19

=0.11%

Earnings per share Income available /

total number of shares

outstanding

46 22

Dividend pay-out

ratio

Dividend paid / net

income

247/186

=1.33

235/309

=0.76

Capital gearing ratio Total debt / total

equity

97.75 34.44

Average inventory

turnover period

Net sales / average

inventory

29007/1869.5

=15.51 days

28456/1792.5

=15.87 days

Return on capital

employed

Operating profit/

capital employed

3.84 4.65

Ratio analysis is the process for comparing actual performance from expected

performance. Ratio analysis helps business for knowing its liquidity, solvency, profitability etc.

The analysis for the ratios are mentioned below:

Current ratio: Current ratio is the process for knowing firms liquidity. Current ratio

shows relationship for current liabilities and current assets. The ideal gross profit ratio is 2:1.

This information is related to the Tesco and Sainsburry for the year 2018 and 2019. in year 2018,

Tesco shows 0.71 which was decrease by 0.612 in year 2019. In 2018, Sainsburry shows 0.73

which was decreased by 0.63 for the year 2019. These firms using current ratio for the purpose

of maintaining liquidity in the company in order to paying its short term debts. As per the data it

shows Sainsburry has better performance than Tesco (Adzobu, Agbloyor and Aboagye, 2017).

Quick ratio: Quick ratio is the process for knowing liquidity. Quick ratio shows

relationship between current liabilities and quick assets. It is liquid in nature which includes cash

and banks balances. Quick assets includes those assets which can convert into cash quickly

which shows cash and bank balances which subtracts stock and prepaid expenses from current

assets. As per the data it shows quick ratios for Tesco and Sainsburry for the year 2018, 2019. in

year 2018, Tesco shows 0.22 which was decreased by 0.16 in year 2019. Sainsburry shows 0.19

which was equal for the year 2019. These firms using this ratio for the purpose of maintain

liquidity in the company for paying its short term debts. As per the data it shows Sainsburry has

better performance than Tesco.

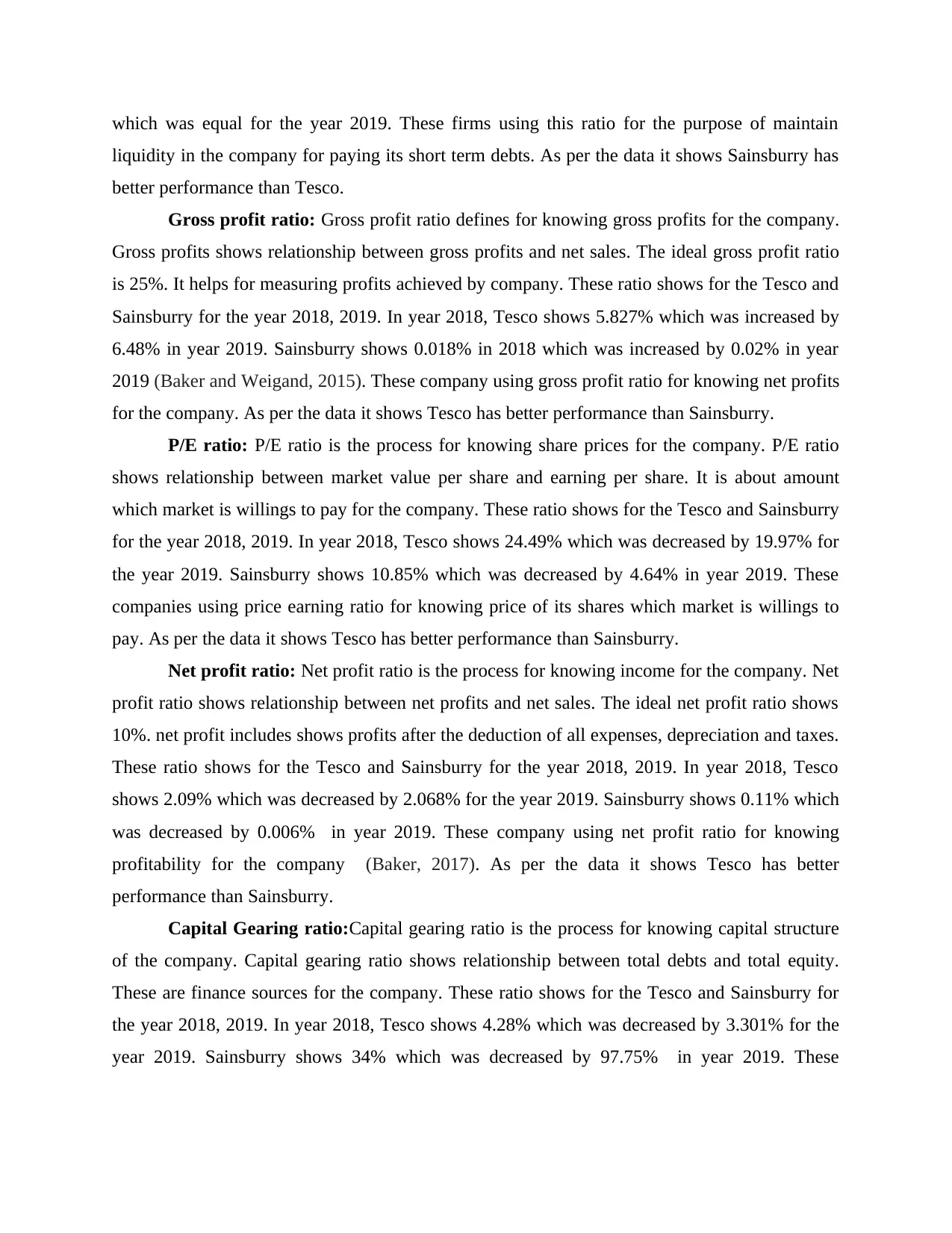

Gross profit ratio: Gross profit ratio defines for knowing gross profits for the company.

Gross profits shows relationship between gross profits and net sales. The ideal gross profit ratio

is 25%. It helps for measuring profits achieved by company. These ratio shows for the Tesco and

Sainsburry for the year 2018, 2019. In year 2018, Tesco shows 5.827% which was increased by

6.48% in year 2019. Sainsburry shows 0.018% in 2018 which was increased by 0.02% in year

2019 (Baker and Weigand, 2015). These company using gross profit ratio for knowing net profits

for the company. As per the data it shows Tesco has better performance than Sainsburry.

P/E ratio: P/E ratio is the process for knowing share prices for the company. P/E ratio

shows relationship between market value per share and earning per share. It is about amount

which market is willings to pay for the company. These ratio shows for the Tesco and Sainsburry

for the year 2018, 2019. In year 2018, Tesco shows 24.49% which was decreased by 19.97% for

the year 2019. Sainsburry shows 10.85% which was decreased by 4.64% in year 2019. These

companies using price earning ratio for knowing price of its shares which market is willings to

pay. As per the data it shows Tesco has better performance than Sainsburry.

Net profit ratio: Net profit ratio is the process for knowing income for the company. Net

profit ratio shows relationship between net profits and net sales. The ideal net profit ratio shows

10%. net profit includes shows profits after the deduction of all expenses, depreciation and taxes.

These ratio shows for the Tesco and Sainsburry for the year 2018, 2019. In year 2018, Tesco

shows 2.09% which was decreased by 2.068% for the year 2019. Sainsburry shows 0.11% which

was decreased by 0.006% in year 2019. These company using net profit ratio for knowing

profitability for the company (Baker, 2017). As per the data it shows Tesco has better

performance than Sainsburry.

Capital Gearing ratio:Capital gearing ratio is the process for knowing capital structure

of the company. Capital gearing ratio shows relationship between total debts and total equity.

These are finance sources for the company. These ratio shows for the Tesco and Sainsburry for

the year 2018, 2019. In year 2018, Tesco shows 4.28% which was decreased by 3.301% for the

year 2019. Sainsburry shows 34% which was decreased by 97.75% in year 2019. These

liquidity in the company for paying its short term debts. As per the data it shows Sainsburry has

better performance than Tesco.

Gross profit ratio: Gross profit ratio defines for knowing gross profits for the company.

Gross profits shows relationship between gross profits and net sales. The ideal gross profit ratio

is 25%. It helps for measuring profits achieved by company. These ratio shows for the Tesco and

Sainsburry for the year 2018, 2019. In year 2018, Tesco shows 5.827% which was increased by

6.48% in year 2019. Sainsburry shows 0.018% in 2018 which was increased by 0.02% in year

2019 (Baker and Weigand, 2015). These company using gross profit ratio for knowing net profits

for the company. As per the data it shows Tesco has better performance than Sainsburry.

P/E ratio: P/E ratio is the process for knowing share prices for the company. P/E ratio

shows relationship between market value per share and earning per share. It is about amount

which market is willings to pay for the company. These ratio shows for the Tesco and Sainsburry

for the year 2018, 2019. In year 2018, Tesco shows 24.49% which was decreased by 19.97% for

the year 2019. Sainsburry shows 10.85% which was decreased by 4.64% in year 2019. These

companies using price earning ratio for knowing price of its shares which market is willings to

pay. As per the data it shows Tesco has better performance than Sainsburry.

Net profit ratio: Net profit ratio is the process for knowing income for the company. Net

profit ratio shows relationship between net profits and net sales. The ideal net profit ratio shows

10%. net profit includes shows profits after the deduction of all expenses, depreciation and taxes.

These ratio shows for the Tesco and Sainsburry for the year 2018, 2019. In year 2018, Tesco

shows 2.09% which was decreased by 2.068% for the year 2019. Sainsburry shows 0.11% which

was decreased by 0.006% in year 2019. These company using net profit ratio for knowing

profitability for the company (Baker, 2017). As per the data it shows Tesco has better

performance than Sainsburry.

Capital Gearing ratio:Capital gearing ratio is the process for knowing capital structure

of the company. Capital gearing ratio shows relationship between total debts and total equity.

These are finance sources for the company. These ratio shows for the Tesco and Sainsburry for

the year 2018, 2019. In year 2018, Tesco shows 4.28% which was decreased by 3.301% for the

year 2019. Sainsburry shows 34% which was decreased by 97.75% in year 2019. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

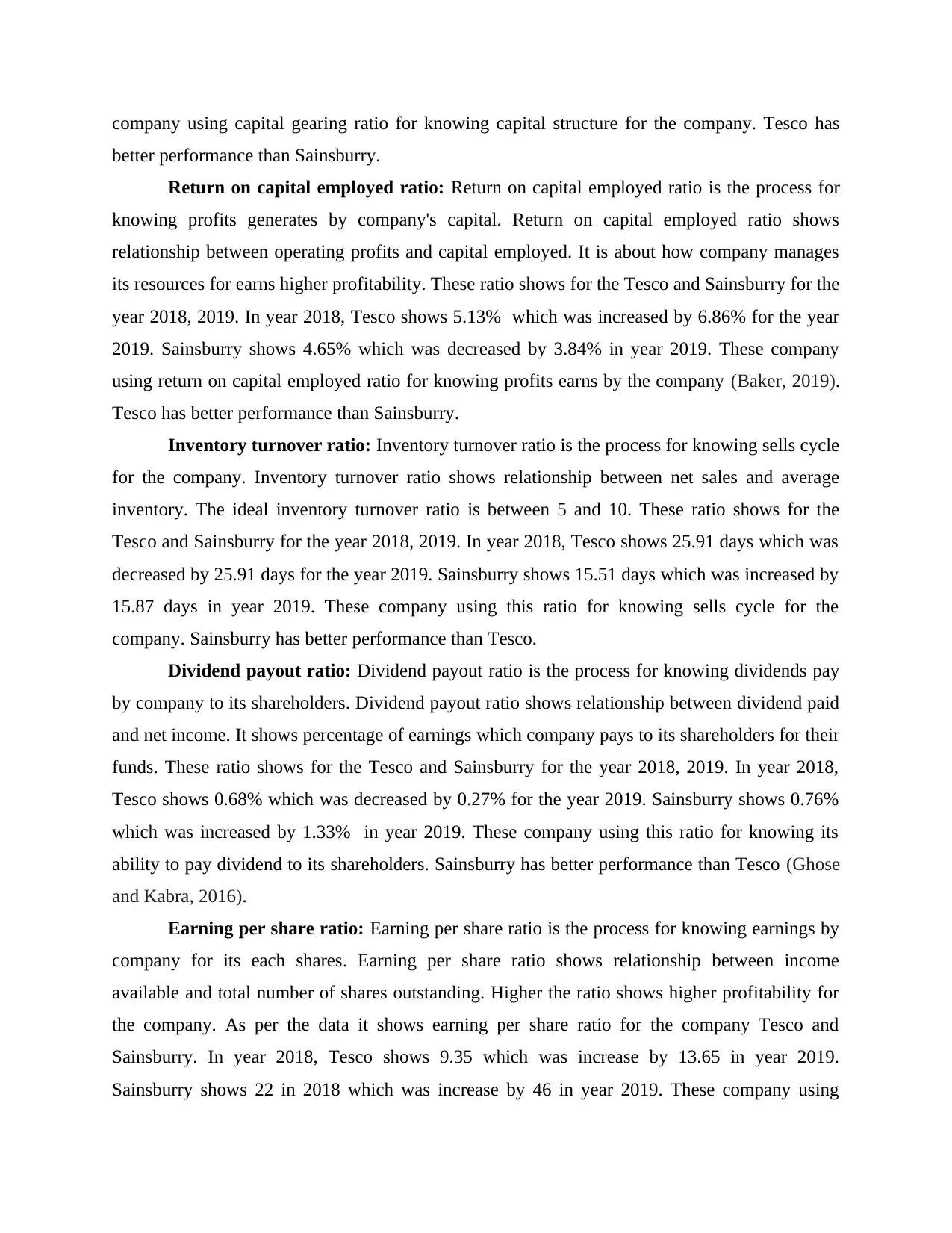

company using capital gearing ratio for knowing capital structure for the company. Tesco has

better performance than Sainsburry.

Return on capital employed ratio: Return on capital employed ratio is the process for

knowing profits generates by company's capital. Return on capital employed ratio shows

relationship between operating profits and capital employed. It is about how company manages

its resources for earns higher profitability. These ratio shows for the Tesco and Sainsburry for the

year 2018, 2019. In year 2018, Tesco shows 5.13% which was increased by 6.86% for the year

2019. Sainsburry shows 4.65% which was decreased by 3.84% in year 2019. These company

using return on capital employed ratio for knowing profits earns by the company (Baker, 2019).

Tesco has better performance than Sainsburry.

Inventory turnover ratio: Inventory turnover ratio is the process for knowing sells cycle

for the company. Inventory turnover ratio shows relationship between net sales and average

inventory. The ideal inventory turnover ratio is between 5 and 10. These ratio shows for the

Tesco and Sainsburry for the year 2018, 2019. In year 2018, Tesco shows 25.91 days which was

decreased by 25.91 days for the year 2019. Sainsburry shows 15.51 days which was increased by

15.87 days in year 2019. These company using this ratio for knowing sells cycle for the

company. Sainsburry has better performance than Tesco.

Dividend payout ratio: Dividend payout ratio is the process for knowing dividends pay

by company to its shareholders. Dividend payout ratio shows relationship between dividend paid

and net income. It shows percentage of earnings which company pays to its shareholders for their

funds. These ratio shows for the Tesco and Sainsburry for the year 2018, 2019. In year 2018,

Tesco shows 0.68% which was decreased by 0.27% for the year 2019. Sainsburry shows 0.76%

which was increased by 1.33% in year 2019. These company using this ratio for knowing its

ability to pay dividend to its shareholders. Sainsburry has better performance than Tesco (Ghose

and Kabra, 2016).

Earning per share ratio: Earning per share ratio is the process for knowing earnings by

company for its each shares. Earning per share ratio shows relationship between income

available and total number of shares outstanding. Higher the ratio shows higher profitability for

the company. As per the data it shows earning per share ratio for the company Tesco and

Sainsburry. In year 2018, Tesco shows 9.35 which was increase by 13.65 in year 2019.

Sainsburry shows 22 in 2018 which was increase by 46 in year 2019. These company using

better performance than Sainsburry.

Return on capital employed ratio: Return on capital employed ratio is the process for

knowing profits generates by company's capital. Return on capital employed ratio shows

relationship between operating profits and capital employed. It is about how company manages

its resources for earns higher profitability. These ratio shows for the Tesco and Sainsburry for the

year 2018, 2019. In year 2018, Tesco shows 5.13% which was increased by 6.86% for the year

2019. Sainsburry shows 4.65% which was decreased by 3.84% in year 2019. These company

using return on capital employed ratio for knowing profits earns by the company (Baker, 2019).

Tesco has better performance than Sainsburry.

Inventory turnover ratio: Inventory turnover ratio is the process for knowing sells cycle

for the company. Inventory turnover ratio shows relationship between net sales and average

inventory. The ideal inventory turnover ratio is between 5 and 10. These ratio shows for the

Tesco and Sainsburry for the year 2018, 2019. In year 2018, Tesco shows 25.91 days which was

decreased by 25.91 days for the year 2019. Sainsburry shows 15.51 days which was increased by

15.87 days in year 2019. These company using this ratio for knowing sells cycle for the

company. Sainsburry has better performance than Tesco.

Dividend payout ratio: Dividend payout ratio is the process for knowing dividends pay

by company to its shareholders. Dividend payout ratio shows relationship between dividend paid

and net income. It shows percentage of earnings which company pays to its shareholders for their

funds. These ratio shows for the Tesco and Sainsburry for the year 2018, 2019. In year 2018,

Tesco shows 0.68% which was decreased by 0.27% for the year 2019. Sainsburry shows 0.76%

which was increased by 1.33% in year 2019. These company using this ratio for knowing its

ability to pay dividend to its shareholders. Sainsburry has better performance than Tesco (Ghose

and Kabra, 2016).

Earning per share ratio: Earning per share ratio is the process for knowing earnings by

company for its each shares. Earning per share ratio shows relationship between income

available and total number of shares outstanding. Higher the ratio shows higher profitability for

the company. As per the data it shows earning per share ratio for the company Tesco and

Sainsburry. In year 2018, Tesco shows 9.35 which was increase by 13.65 in year 2019.

Sainsburry shows 22 in 2018 which was increase by 46 in year 2019. These company using

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earning per share ratio for knowing profitability of the company (Gitman, Juchau and Flanagan,

2015). Sainsburry has better performance than Tesco.

Recommendations:

From the above report it shows organisations should manage its current assets for paying

short term liabilities and managing its day to day activities.

For managing its gross profits firm should gives discounts, offers to customers so that

they can manage its sales.

For the improvement in net profit ratio for companies should decreases their indirect

expenses, using its resources efficiently which decreases its expenses which leads to

organisations higher profitability (HACIOGLU and Dincer, 2016).

Inventory turnover ratio shows organisations not managing its resources properly, it has

to manage its resources effectively and efficiently for higher sales.

For increasing earning per share, organisations has to increase its value by using

resources in the better way so that it can increase its value.

Limitations for ratio analysis in order to know financial position:

Ratio analysis information is historic, it is not current.

Ratio analysis does not take into account external factors includes the worldwide

recession.

Ratio analysis does not measure the human element of the organisations.

Ratio analysis can only be used for comparison with other firms of the same size and type

organisation.

It may be difficult for comparing with other businesses as they may not be willing for

share the information.

Ratio analysis helps in providing the historic data and on the basis of the past results is

generated it does not used the present data which affects the efficiency of the company.

The external factors affecting the accounting system is not taken into the account like the

factors includes the recession period which does not taken and accurate results cannot be

generated (Jitmaneeroj, 2018).

The ratio analysis become difficult while comparing as it does not give the accurate

results as different companies have different accounting so the information is not useful.

2015). Sainsburry has better performance than Tesco.

Recommendations:

From the above report it shows organisations should manage its current assets for paying

short term liabilities and managing its day to day activities.

For managing its gross profits firm should gives discounts, offers to customers so that

they can manage its sales.

For the improvement in net profit ratio for companies should decreases their indirect

expenses, using its resources efficiently which decreases its expenses which leads to

organisations higher profitability (HACIOGLU and Dincer, 2016).

Inventory turnover ratio shows organisations not managing its resources properly, it has

to manage its resources effectively and efficiently for higher sales.

For increasing earning per share, organisations has to increase its value by using

resources in the better way so that it can increase its value.

Limitations for ratio analysis in order to know financial position:

Ratio analysis information is historic, it is not current.

Ratio analysis does not take into account external factors includes the worldwide

recession.

Ratio analysis does not measure the human element of the organisations.

Ratio analysis can only be used for comparison with other firms of the same size and type

organisation.

It may be difficult for comparing with other businesses as they may not be willing for

share the information.

Ratio analysis helps in providing the historic data and on the basis of the past results is

generated it does not used the present data which affects the efficiency of the company.

The external factors affecting the accounting system is not taken into the account like the

factors includes the recession period which does not taken and accurate results cannot be

generated (Jitmaneeroj, 2018).

The ratio analysis become difficult while comparing as it does not give the accurate

results as different companies have different accounting so the information is not useful.

Ratio analysis can be compared only with the firms of the same types and the size no

other type of firm can be compared.

Ratio analysis contains information or prior period. In other words, in ratio analysis past

or historic data is utilised. Hence, it is not necessary that such interpretation of such data

provides adequate information according to current business situation.

Human element is not considered in computation of ratio analysis.

External factors, for example, worldwide recession is not taken into consideration on

calculation of ratio analysis. Although, it has huge impact on business (Li, Niskanen and

Niskanen, 2019).

It is not suitable to compare with entity that uses different accounting policies.

PORTFOLIO 2

Investment appraisal techniques:

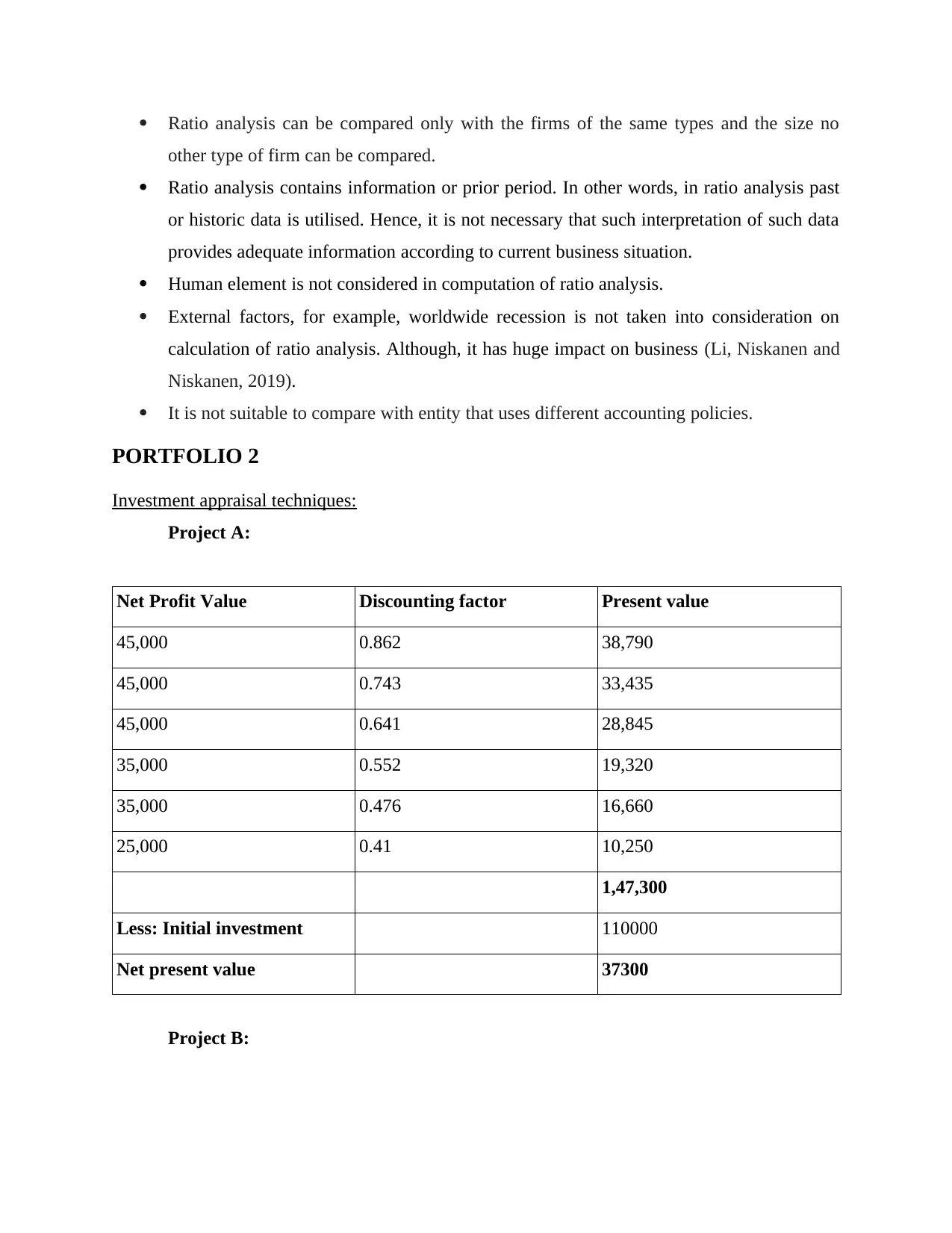

Project A:

Net Profit Value Discounting factor Present value

45,000 0.862 38,790

45,000 0.743 33,435

45,000 0.641 28,845

35,000 0.552 19,320

35,000 0.476 16,660

25,000 0.41 10,250

1,47,300

Less: Initial investment 110000

Net present value 37300

Project B:

other type of firm can be compared.

Ratio analysis contains information or prior period. In other words, in ratio analysis past

or historic data is utilised. Hence, it is not necessary that such interpretation of such data

provides adequate information according to current business situation.

Human element is not considered in computation of ratio analysis.

External factors, for example, worldwide recession is not taken into consideration on

calculation of ratio analysis. Although, it has huge impact on business (Li, Niskanen and

Niskanen, 2019).

It is not suitable to compare with entity that uses different accounting policies.

PORTFOLIO 2

Investment appraisal techniques:

Project A:

Net Profit Value Discounting factor Present value

45,000 0.862 38,790

45,000 0.743 33,435

45,000 0.641 28,845

35,000 0.552 19,320

35,000 0.476 16,660

25,000 0.41 10,250

1,47,300

Less: Initial investment 110000

Net present value 37300

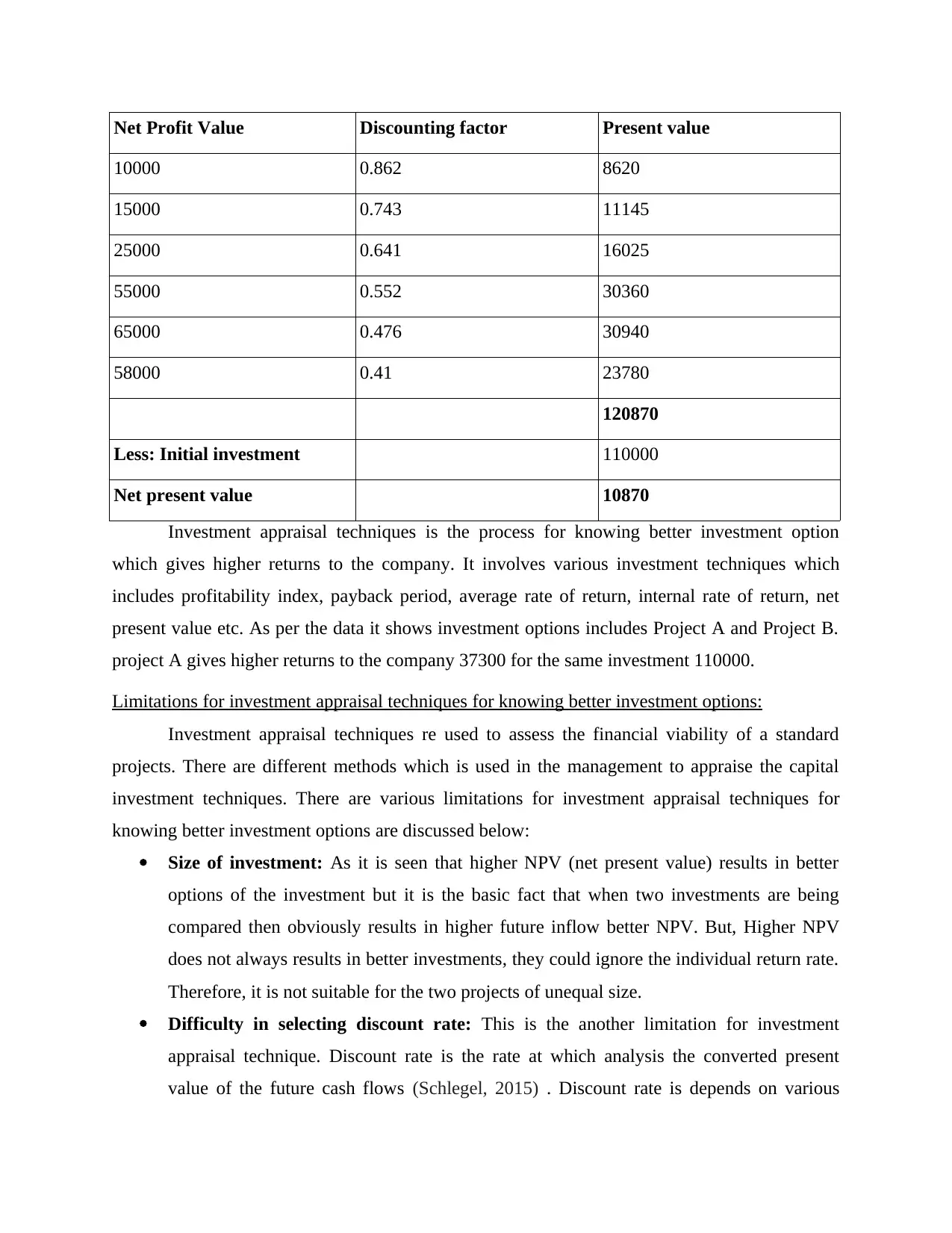

Project B:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Profit Value Discounting factor Present value

10000 0.862 8620

15000 0.743 11145

25000 0.641 16025

55000 0.552 30360

65000 0.476 30940

58000 0.41 23780

120870

Less: Initial investment 110000

Net present value 10870

Investment appraisal techniques is the process for knowing better investment option

which gives higher returns to the company. It involves various investment techniques which

includes profitability index, payback period, average rate of return, internal rate of return, net

present value etc. As per the data it shows investment options includes Project A and Project B.

project A gives higher returns to the company 37300 for the same investment 110000.

Limitations for investment appraisal techniques for knowing better investment options:

Investment appraisal techniques re used to assess the financial viability of a standard

projects. There are different methods which is used in the management to appraise the capital

investment techniques. There are various limitations for investment appraisal techniques for

knowing better investment options are discussed below:

Size of investment: As it is seen that higher NPV (net present value) results in better

options of the investment but it is the basic fact that when two investments are being

compared then obviously results in higher future inflow better NPV. But, Higher NPV

does not always results in better investments, they could ignore the individual return rate.

Therefore, it is not suitable for the two projects of unequal size.

Difficulty in selecting discount rate: This is the another limitation for investment

appraisal technique. Discount rate is the rate at which analysis the converted present

value of the future cash flows (Schlegel, 2015) . Discount rate is depends on various

10000 0.862 8620

15000 0.743 11145

25000 0.641 16025

55000 0.552 30360

65000 0.476 30940

58000 0.41 23780

120870

Less: Initial investment 110000

Net present value 10870

Investment appraisal techniques is the process for knowing better investment option

which gives higher returns to the company. It involves various investment techniques which

includes profitability index, payback period, average rate of return, internal rate of return, net

present value etc. As per the data it shows investment options includes Project A and Project B.

project A gives higher returns to the company 37300 for the same investment 110000.

Limitations for investment appraisal techniques for knowing better investment options:

Investment appraisal techniques re used to assess the financial viability of a standard

projects. There are different methods which is used in the management to appraise the capital

investment techniques. There are various limitations for investment appraisal techniques for

knowing better investment options are discussed below:

Size of investment: As it is seen that higher NPV (net present value) results in better

options of the investment but it is the basic fact that when two investments are being

compared then obviously results in higher future inflow better NPV. But, Higher NPV

does not always results in better investments, they could ignore the individual return rate.

Therefore, it is not suitable for the two projects of unequal size.

Difficulty in selecting discount rate: This is the another limitation for investment

appraisal technique. Discount rate is the rate at which analysis the converted present

value of the future cash flows (Schlegel, 2015) . Discount rate is depends on various

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

factors like calculative accuracy, risk involved etc. they can be easily convert into

mistakes. Also, factors like risk are changing over the period of time and can give

incorrect rate of return to the company which can cost heavily to the organisation.

Difficult in estimating cash flows and cost of capital: Another limitation is difficulty in

estimating appropriate future cash flows and cost of capital. Company analysis the

financial viability according to the basis of future cash flows but this can create difficulty

in ascertaining the cash flows. There are two types of risk involved in the company that is

structured and unstructured. This can be change dynamically in the company. Cost of

capital is the capital that is investment proposed is going to incur and analysis of which is

decided by the risk taken or not. If company make projects cost of capital then it might

not or may be take the risk or not.

Ignores money time value: Some techniques of investment like pay back period and

accounting rate ignore the money time value. Pay back period also ignore the cash flows

and make post pay pack period. This can give accurate profitability and revenue status for

the proposed projects ad cannot make the definite of the correctiveness of financial

advice generated according to the results.

Complicated to understand: This is the another limitation for investment appraisal

techniques. As techniques like pay back period are easy and feasible to understand but

they cannot make appropriate Net present value. However, net present value is difficulty

to understand and requires proper knowledge by the managers of the company to identify

cost of capital. On the other hand other methods like internal rate of return is is also

difficult to understand because it is the rate at which Net present value is equals to zero

(Singh, 2016). Sometimes non- conventional cash flows can give rise for internal rate of

return and also there is high chances of contradicting advices in IRR and NPV ratios in

proposed projects.

CONCLUSION

From the above report it has been concluded that finance is the process for acquiring and

managing funds for the organisations activities. Financial management is the process for

managing financial activities for the organisations. Financial management has various functions

which includes planning, organising, analysing, controlling, managing financial activities. Ratio

mistakes. Also, factors like risk are changing over the period of time and can give

incorrect rate of return to the company which can cost heavily to the organisation.

Difficult in estimating cash flows and cost of capital: Another limitation is difficulty in

estimating appropriate future cash flows and cost of capital. Company analysis the

financial viability according to the basis of future cash flows but this can create difficulty

in ascertaining the cash flows. There are two types of risk involved in the company that is

structured and unstructured. This can be change dynamically in the company. Cost of

capital is the capital that is investment proposed is going to incur and analysis of which is

decided by the risk taken or not. If company make projects cost of capital then it might

not or may be take the risk or not.

Ignores money time value: Some techniques of investment like pay back period and

accounting rate ignore the money time value. Pay back period also ignore the cash flows

and make post pay pack period. This can give accurate profitability and revenue status for

the proposed projects ad cannot make the definite of the correctiveness of financial

advice generated according to the results.

Complicated to understand: This is the another limitation for investment appraisal

techniques. As techniques like pay back period are easy and feasible to understand but

they cannot make appropriate Net present value. However, net present value is difficulty

to understand and requires proper knowledge by the managers of the company to identify

cost of capital. On the other hand other methods like internal rate of return is is also

difficult to understand because it is the rate at which Net present value is equals to zero

(Singh, 2016). Sometimes non- conventional cash flows can give rise for internal rate of

return and also there is high chances of contradicting advices in IRR and NPV ratios in

proposed projects.

CONCLUSION

From the above report it has been concluded that finance is the process for acquiring and

managing funds for the organisations activities. Financial management is the process for

managing financial activities for the organisations. Financial management has various functions

which includes planning, organising, analysing, controlling, managing financial activities. Ratio

analysis is the process for comparing actual performance from expected performance. Ratio

analysis helps business for knowing its liquidity, solvency, profitability etc. Investment appraisal

techniques is the process for knowing better investment option which gives higher returns to the

company. It involves various investment techniques which includes profitability index, payback

period, average rate of return, internal rate of return, net present value etc. Investment appraisal

techniques helps firms for achieving profitability.

analysis helps business for knowing its liquidity, solvency, profitability etc. Investment appraisal

techniques is the process for knowing better investment option which gives higher returns to the

company. It involves various investment techniques which includes profitability index, payback

period, average rate of return, internal rate of return, net present value etc. Investment appraisal

techniques helps firms for achieving profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.