Financial Resources Report: Management and Financial Accounting

VerifiedAdded on 2023/01/13

|14

|2581

|68

Report

AI Summary

This report provides a comprehensive analysis of financial resources, focusing on management and financial accounting principles. It delves into the significance of financial resources for organizations, using Swipe-wire as a case study. The report explains the differences between management and financial accounting and explores capital budgeting techniques such as cost-benefit analysis, payback period, accounting rate of return, net present value, and internal rate of return. Through these techniques, the report evaluates different project alternatives and provides a detailed analysis of financial ratios, including gross profit margin, net profit margin, return on capital invested, return on assets, return on equity, current ratio, and acid-test ratio. The analysis compares financial performance between 2017 and 2018, offering suggestions for improvement. The report concludes by highlighting the importance of financial resource management for organizational success.

Financial Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial resources are those factors by which an organisation generate their monetary funds.

This report is prepared on the basis of examine concept of financial resources, managerial and

financial accounting.

In this report capital budgeting techniques and financial ratios are uses for taking business

decision for choosing best alternative option compare with others.

Financial resources are those factors by which an organisation generate their monetary funds.

This report is prepared on the basis of examine concept of financial resources, managerial and

financial accounting.

In this report capital budgeting techniques and financial ratios are uses for taking business

decision for choosing best alternative option compare with others.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Explanation of management and financial accounting................................................................1

Difference between management and financial accounting with respective users......................1

QUESTION2....................................................................................................................................2

Cost benefit analysis....................................................................................................................2

Payback period.............................................................................................................................3

Accounting rate of return.............................................................................................................4

Net present value and internal rate of return................................................................................5

Analysis and conclusion..............................................................................................................6

QUESTION 3...................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Comparison of ratios....................................................................................................................8

Suggestions for improvement......................................................................................................9

CONCLUSION................................................................................................................................9

REFRENCES.................................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Explanation of management and financial accounting................................................................1

Difference between management and financial accounting with respective users......................1

QUESTION2....................................................................................................................................2

Cost benefit analysis....................................................................................................................2

Payback period.............................................................................................................................3

Accounting rate of return.............................................................................................................4

Net present value and internal rate of return................................................................................5

Analysis and conclusion..............................................................................................................6

QUESTION 3...................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Comparison of ratios....................................................................................................................8

Suggestions for improvement......................................................................................................9

CONCLUSION................................................................................................................................9

REFRENCES.................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial resources represent collection of monetary funds of an organisation. These play

vital role in running an organisation successfully. Managers use these resources to carry out

their managerial functions effectively. In this report Swipe- wire is taken. Concept of

management and financial accounting has been described and techniques of captain

budgeting for taking decision has been defined.

QUESTION 1

Explanation of management and financial accounting

Management accounting: It define as a process of collecting financial and non-financial

information in a way which help managers to perform their managerial function effectively.

It is also known as managerial accounting. Manager of Swipe-wire use this technique for

taking short term as well as long term strategic decision and enhancing performance of their

organisation. Reports generated through management accounting are used by management

to make necessary decisions. These reports are known as Management accounts and these

are for internal use of any organisation (Thakur Kumar Pandit Singh and Satashia 2016,

December).

Financial Accounting: It is a process of collecting, recording and analysing monetary

transactions of a business entity. It is a part of accounting process which help an

organisation to present their financial data in better way. Manager of Swipe-wire use this

technique for identify their financial position at specific time period. They use financial

accounting for the purpose of representing their financial status to various stakeholders i.e.

shareholders, government, customers.

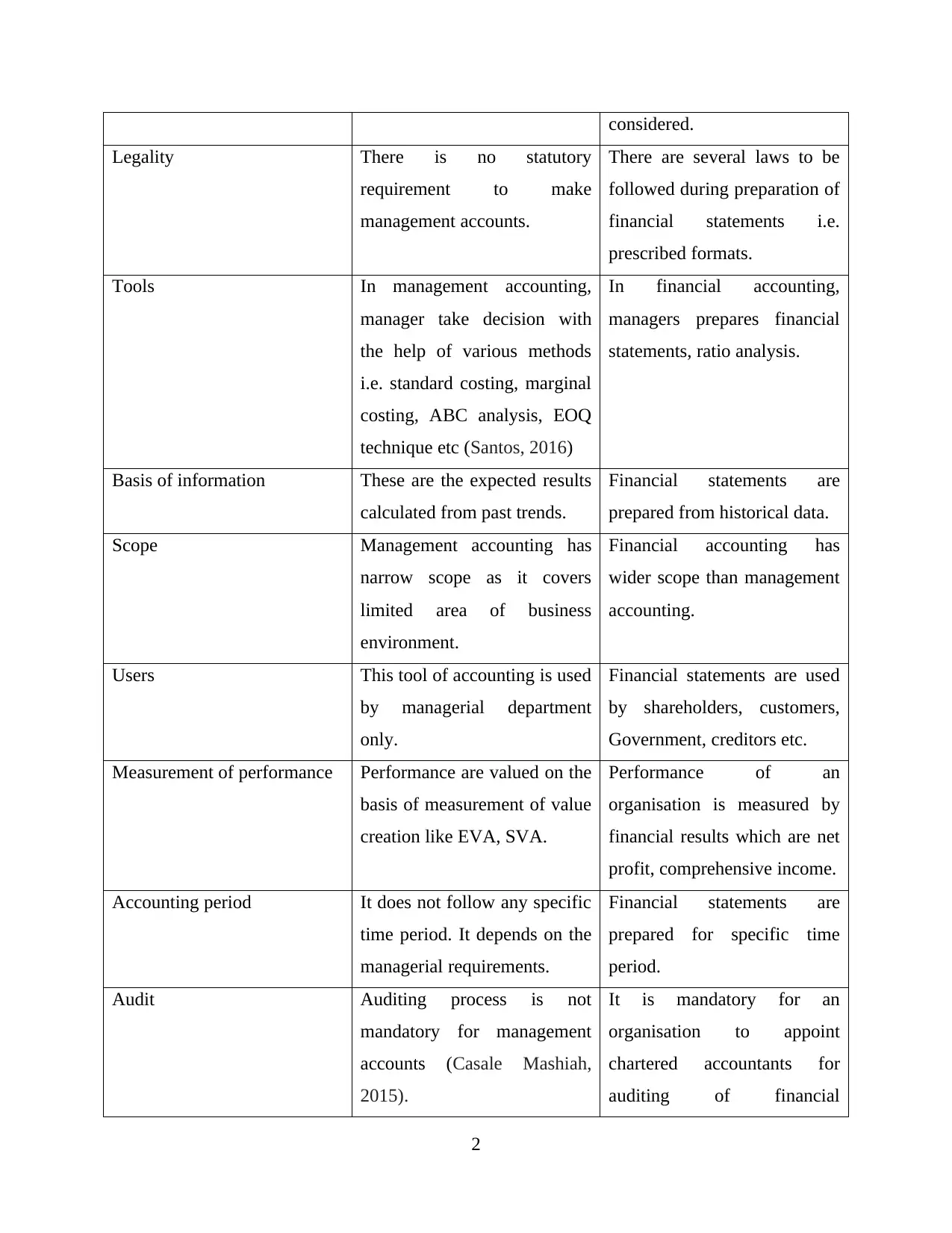

Difference between management and financial accounting with respective users

Particulars Management Accounting Financial Accounting

Objective Main purpose of this

technique is to provide

essential accounting

information for internal use to

make strategic decisions.

Main objective of this

technique is to analyse

financial position of an entity

and provide necessary

information to external users.

Type of transactions It deals with financial as well

as non-financial transactions.

In financial accounting only

monetary transactions are

1

Financial resources represent collection of monetary funds of an organisation. These play

vital role in running an organisation successfully. Managers use these resources to carry out

their managerial functions effectively. In this report Swipe- wire is taken. Concept of

management and financial accounting has been described and techniques of captain

budgeting for taking decision has been defined.

QUESTION 1

Explanation of management and financial accounting

Management accounting: It define as a process of collecting financial and non-financial

information in a way which help managers to perform their managerial function effectively.

It is also known as managerial accounting. Manager of Swipe-wire use this technique for

taking short term as well as long term strategic decision and enhancing performance of their

organisation. Reports generated through management accounting are used by management

to make necessary decisions. These reports are known as Management accounts and these

are for internal use of any organisation (Thakur Kumar Pandit Singh and Satashia 2016,

December).

Financial Accounting: It is a process of collecting, recording and analysing monetary

transactions of a business entity. It is a part of accounting process which help an

organisation to present their financial data in better way. Manager of Swipe-wire use this

technique for identify their financial position at specific time period. They use financial

accounting for the purpose of representing their financial status to various stakeholders i.e.

shareholders, government, customers.

Difference between management and financial accounting with respective users

Particulars Management Accounting Financial Accounting

Objective Main purpose of this

technique is to provide

essential accounting

information for internal use to

make strategic decisions.

Main objective of this

technique is to analyse

financial position of an entity

and provide necessary

information to external users.

Type of transactions It deals with financial as well

as non-financial transactions.

In financial accounting only

monetary transactions are

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered.

Legality There is no statutory

requirement to make

management accounts.

There are several laws to be

followed during preparation of

financial statements i.e.

prescribed formats.

Tools In management accounting,

manager take decision with

the help of various methods

i.e. standard costing, marginal

costing, ABC analysis, EOQ

technique etc (Santos, 2016)

In financial accounting,

managers prepares financial

statements, ratio analysis.

Basis of information These are the expected results

calculated from past trends.

Financial statements are

prepared from historical data.

Scope Management accounting has

narrow scope as it covers

limited area of business

environment.

Financial accounting has

wider scope than management

accounting.

Users This tool of accounting is used

by managerial department

only.

Financial statements are used

by shareholders, customers,

Government, creditors etc.

Measurement of performance Performance are valued on the

basis of measurement of value

creation like EVA, SVA.

Performance of an

organisation is measured by

financial results which are net

profit, comprehensive income.

Accounting period It does not follow any specific

time period. It depends on the

managerial requirements.

Financial statements are

prepared for specific time

period.

Audit Auditing process is not

mandatory for management

accounts (Casale Mashiah,

2015).

It is mandatory for an

organisation to appoint

chartered accountants for

auditing of financial

2

Legality There is no statutory

requirement to make

management accounts.

There are several laws to be

followed during preparation of

financial statements i.e.

prescribed formats.

Tools In management accounting,

manager take decision with

the help of various methods

i.e. standard costing, marginal

costing, ABC analysis, EOQ

technique etc (Santos, 2016)

In financial accounting,

managers prepares financial

statements, ratio analysis.

Basis of information These are the expected results

calculated from past trends.

Financial statements are

prepared from historical data.

Scope Management accounting has

narrow scope as it covers

limited area of business

environment.

Financial accounting has

wider scope than management

accounting.

Users This tool of accounting is used

by managerial department

only.

Financial statements are used

by shareholders, customers,

Government, creditors etc.

Measurement of performance Performance are valued on the

basis of measurement of value

creation like EVA, SVA.

Performance of an

organisation is measured by

financial results which are net

profit, comprehensive income.

Accounting period It does not follow any specific

time period. It depends on the

managerial requirements.

Financial statements are

prepared for specific time

period.

Audit Auditing process is not

mandatory for management

accounts (Casale Mashiah,

2015).

It is mandatory for an

organisation to appoint

chartered accountants for

auditing of financial

2

statements.

QUESTION 2

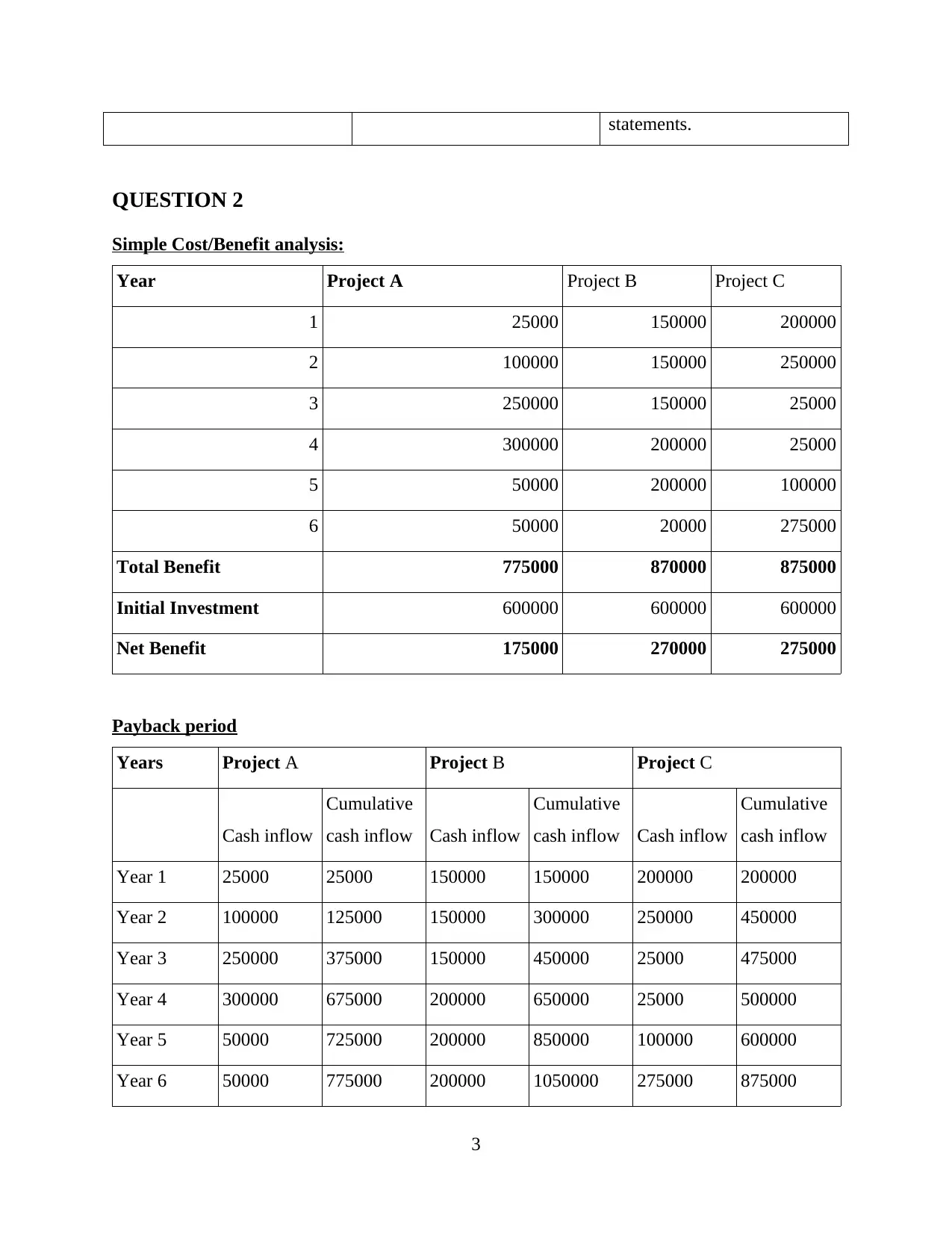

Simple Cost/Benefit analysis:

Year Project A Project B Project C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 20000 275000

Total Benefit 775000 870000 875000

Initial Investment 600000 600000 600000

Net Benefit 175000 270000 275000

Payback period

Years Project A Project B Project C

Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow

Year 1 25000 25000 150000 150000 200000 200000

Year 2 100000 125000 150000 300000 250000 450000

Year 3 250000 375000 150000 450000 25000 475000

Year 4 300000 675000 200000 650000 25000 500000

Year 5 50000 725000 200000 850000 100000 600000

Year 6 50000 775000 200000 1050000 275000 875000

3

QUESTION 2

Simple Cost/Benefit analysis:

Year Project A Project B Project C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 20000 275000

Total Benefit 775000 870000 875000

Initial Investment 600000 600000 600000

Net Benefit 175000 270000 275000

Payback period

Years Project A Project B Project C

Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow Cash inflow

Cumulative

cash inflow

Year 1 25000 25000 150000 150000 200000 200000

Year 2 100000 125000 150000 300000 250000 450000

Year 3 250000 375000 150000 450000 25000 475000

Year 4 300000 675000 200000 650000 25000 500000

Year 5 50000 725000 200000 850000 100000 600000

Year 6 50000 775000 200000 1050000 275000 875000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formula: Completed year + Initial investment – cumulative cash inflow at the end of the

year / Cash flow of next year

Project A: 3 + 600000 – 375000 / 300000

= 3 + 225000 / 300000

= 3 + 0.75

= 3.75 years

Project B: 3 + 600000 – 450000 / 200000

= 3 + 150000 / 200000

= 3 + 0.75

= 3.75 years

Project C: According to the cumulative cash flow of project C the payback period is

Year 5 because 600000 will be recovered in this year (Zamani Svanström Peters and Rydberg,

2015).

Accounting rate of return

Accounting rate of return:

Formula: Average net income / Initial investment * 100

Calculation of net income:

Formula: Net cash inflow – depreciation

Depreciation = Initial investment / life of project

= 600000 / 6

= 100000

Years

Project A Deduct

depreciation

Project B Deduct

depreciation

Project C Deduct

depreciationCash inflow Cash inflow Cash inflow

Year 1 25000 100000 150000 100000 200000 100000

Year 2 100000 100000 150000 100000 250000 100000

Year 3 250000 100000 150000 100000 25000 100000

Year 4 300000 100000 200000 100000 25000 100000

Year 5 50000 100000 200000 100000 100000 100000

Year 6 50000 100000 200000 100000 275000 100000

4

year / Cash flow of next year

Project A: 3 + 600000 – 375000 / 300000

= 3 + 225000 / 300000

= 3 + 0.75

= 3.75 years

Project B: 3 + 600000 – 450000 / 200000

= 3 + 150000 / 200000

= 3 + 0.75

= 3.75 years

Project C: According to the cumulative cash flow of project C the payback period is

Year 5 because 600000 will be recovered in this year (Zamani Svanström Peters and Rydberg,

2015).

Accounting rate of return

Accounting rate of return:

Formula: Average net income / Initial investment * 100

Calculation of net income:

Formula: Net cash inflow – depreciation

Depreciation = Initial investment / life of project

= 600000 / 6

= 100000

Years

Project A Deduct

depreciation

Project B Deduct

depreciation

Project C Deduct

depreciationCash inflow Cash inflow Cash inflow

Year 1 25000 100000 150000 100000 200000 100000

Year 2 100000 100000 150000 100000 250000 100000

Year 3 250000 100000 150000 100000 25000 100000

Year 4 300000 100000 200000 100000 25000 100000

Year 5 50000 100000 200000 100000 100000 100000

Year 6 50000 100000 200000 100000 275000 100000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

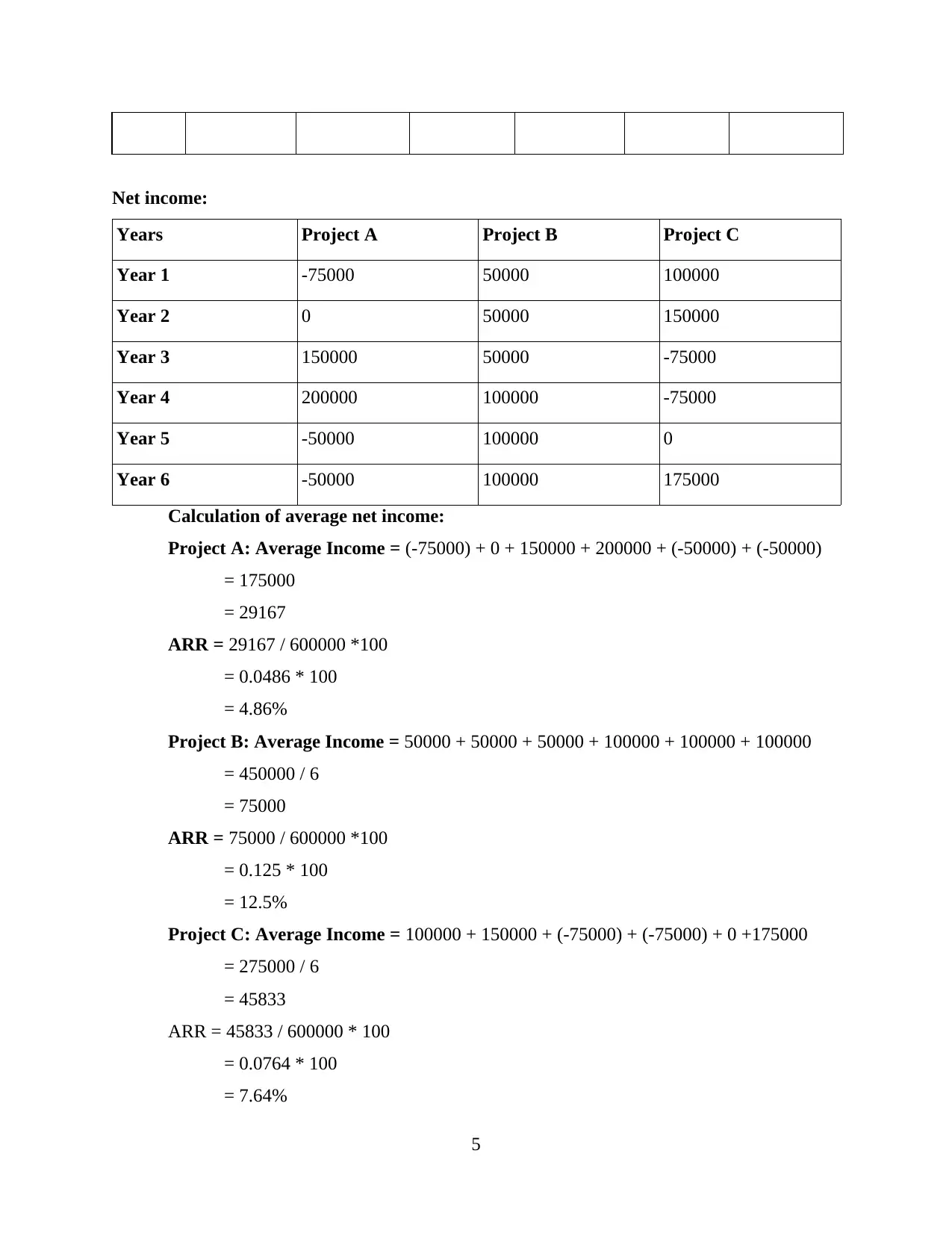

Net income:

Years Project A Project B Project C

Year 1 -75000 50000 100000

Year 2 0 50000 150000

Year 3 150000 50000 -75000

Year 4 200000 100000 -75000

Year 5 -50000 100000 0

Year 6 -50000 100000 175000

Calculation of average net income:

Project A: Average Income = (-75000) + 0 + 150000 + 200000 + (-50000) + (-50000)

= 175000

= 29167

ARR = 29167 / 600000 *100

= 0.0486 * 100

= 4.86%

Project B: Average Income = 50000 + 50000 + 50000 + 100000 + 100000 + 100000

= 450000 / 6

= 75000

ARR = 75000 / 600000 *100

= 0.125 * 100

= 12.5%

Project C: Average Income = 100000 + 150000 + (-75000) + (-75000) + 0 +175000

= 275000 / 6

= 45833

ARR = 45833 / 600000 * 100

= 0.0764 * 100

= 7.64%

5

Years Project A Project B Project C

Year 1 -75000 50000 100000

Year 2 0 50000 150000

Year 3 150000 50000 -75000

Year 4 200000 100000 -75000

Year 5 -50000 100000 0

Year 6 -50000 100000 175000

Calculation of average net income:

Project A: Average Income = (-75000) + 0 + 150000 + 200000 + (-50000) + (-50000)

= 175000

= 29167

ARR = 29167 / 600000 *100

= 0.0486 * 100

= 4.86%

Project B: Average Income = 50000 + 50000 + 50000 + 100000 + 100000 + 100000

= 450000 / 6

= 75000

ARR = 75000 / 600000 *100

= 0.125 * 100

= 12.5%

Project C: Average Income = 100000 + 150000 + (-75000) + (-75000) + 0 +175000

= 275000 / 6

= 45833

ARR = 45833 / 600000 * 100

= 0.0764 * 100

= 7.64%

5

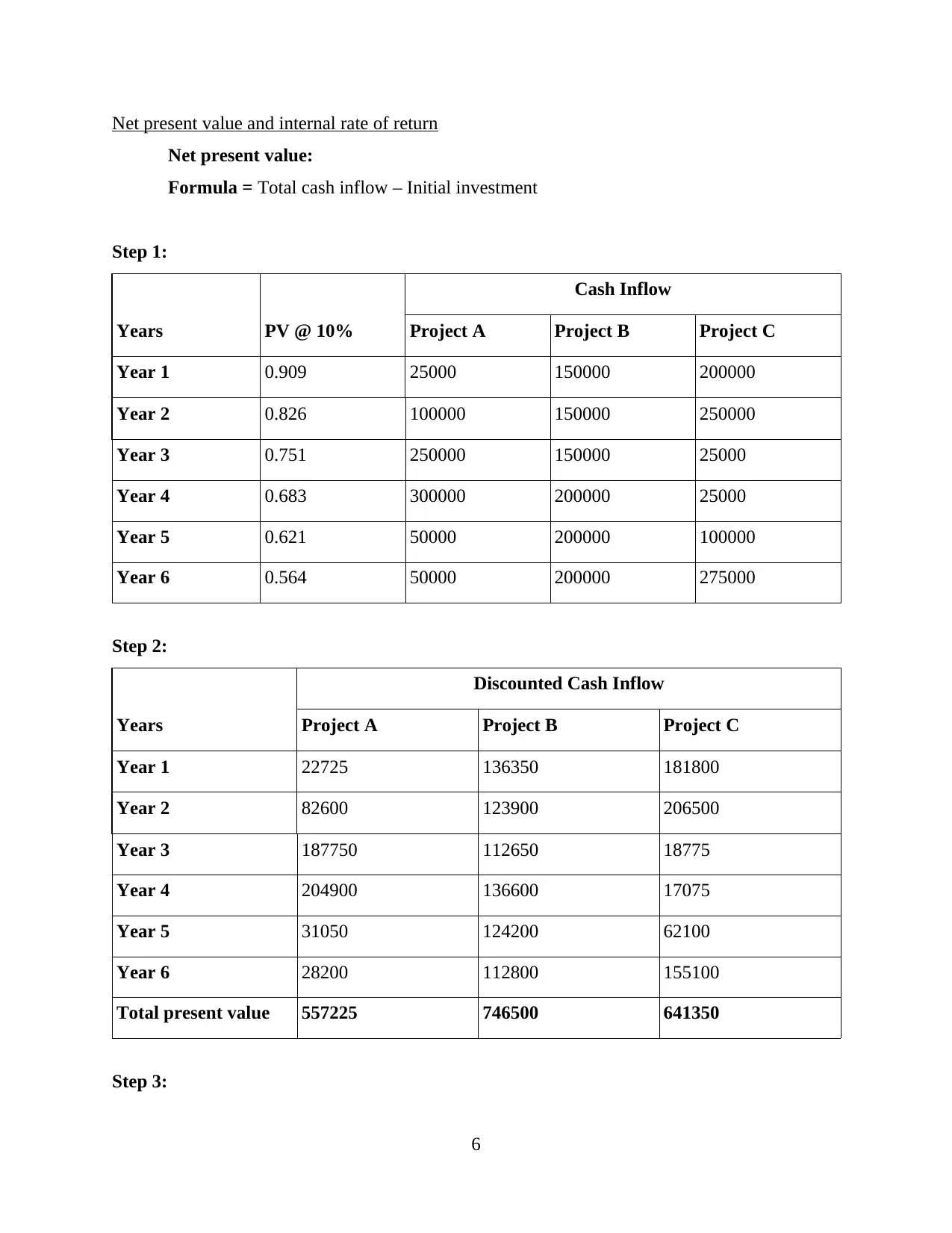

Net present value and internal rate of return

Net present value:

Formula = Total cash inflow – Initial investment

Step 1:

Years PV @ 10%

Cash Inflow

Project A Project B Project C

Year 1 0.909 25000 150000 200000

Year 2 0.826 100000 150000 250000

Year 3 0.751 250000 150000 25000

Year 4 0.683 300000 200000 25000

Year 5 0.621 50000 200000 100000

Year 6 0.564 50000 200000 275000

Step 2:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

Total present value 557225 746500 641350

Step 3:

6

Net present value:

Formula = Total cash inflow – Initial investment

Step 1:

Years PV @ 10%

Cash Inflow

Project A Project B Project C

Year 1 0.909 25000 150000 200000

Year 2 0.826 100000 150000 250000

Year 3 0.751 250000 150000 25000

Year 4 0.683 300000 200000 25000

Year 5 0.621 50000 200000 100000

Year 6 0.564 50000 200000 275000

Step 2:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

Total present value 557225 746500 641350

Step 3:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

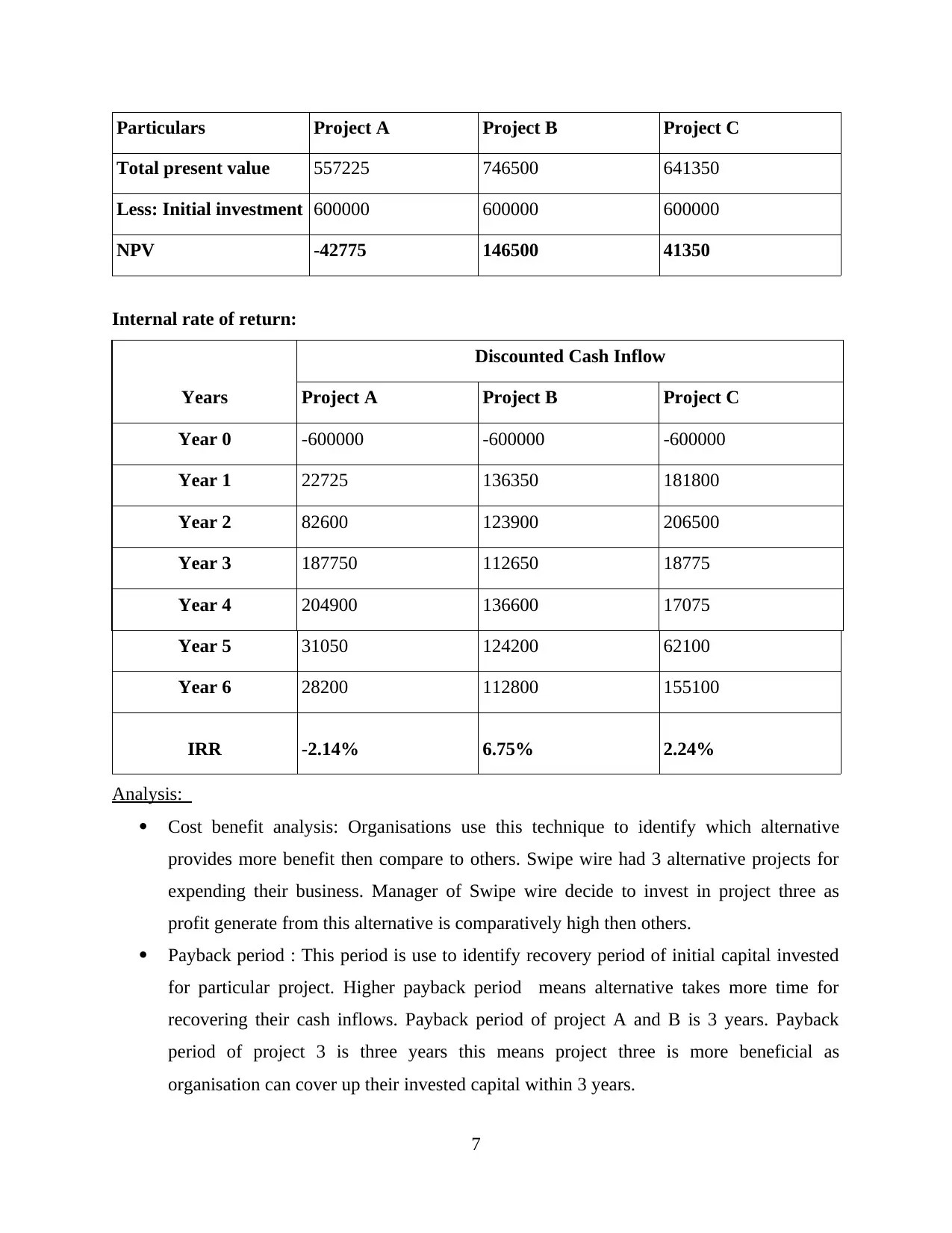

Particulars Project A Project B Project C

Total present value 557225 746500 641350

Less: Initial investment 600000 600000 600000

NPV -42775 146500 41350

Internal rate of return:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 0 -600000 -600000 -600000

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

IRR -2.14% 6.75% 2.24%

Analysis:

Cost benefit analysis: Organisations use this technique to identify which alternative

provides more benefit then compare to others. Swipe wire had 3 alternative projects for

expending their business. Manager of Swipe wire decide to invest in project three as

profit generate from this alternative is comparatively high then others.

Payback period : This period is use to identify recovery period of initial capital invested

for particular project. Higher payback period means alternative takes more time for

recovering their cash inflows. Payback period of project A and B is 3 years. Payback

period of project 3 is three years this means project three is more beneficial as

organisation can cover up their invested capital within 3 years.

7

Total present value 557225 746500 641350

Less: Initial investment 600000 600000 600000

NPV -42775 146500 41350

Internal rate of return:

Years

Discounted Cash Inflow

Project A Project B Project C

Year 0 -600000 -600000 -600000

Year 1 22725 136350 181800

Year 2 82600 123900 206500

Year 3 187750 112650 18775

Year 4 204900 136600 17075

Year 5 31050 124200 62100

Year 6 28200 112800 155100

IRR -2.14% 6.75% 2.24%

Analysis:

Cost benefit analysis: Organisations use this technique to identify which alternative

provides more benefit then compare to others. Swipe wire had 3 alternative projects for

expending their business. Manager of Swipe wire decide to invest in project three as

profit generate from this alternative is comparatively high then others.

Payback period : This period is use to identify recovery period of initial capital invested

for particular project. Higher payback period means alternative takes more time for

recovering their cash inflows. Payback period of project A and B is 3 years. Payback

period of project 3 is three years this means project three is more beneficial as

organisation can cover up their invested capital within 3 years.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

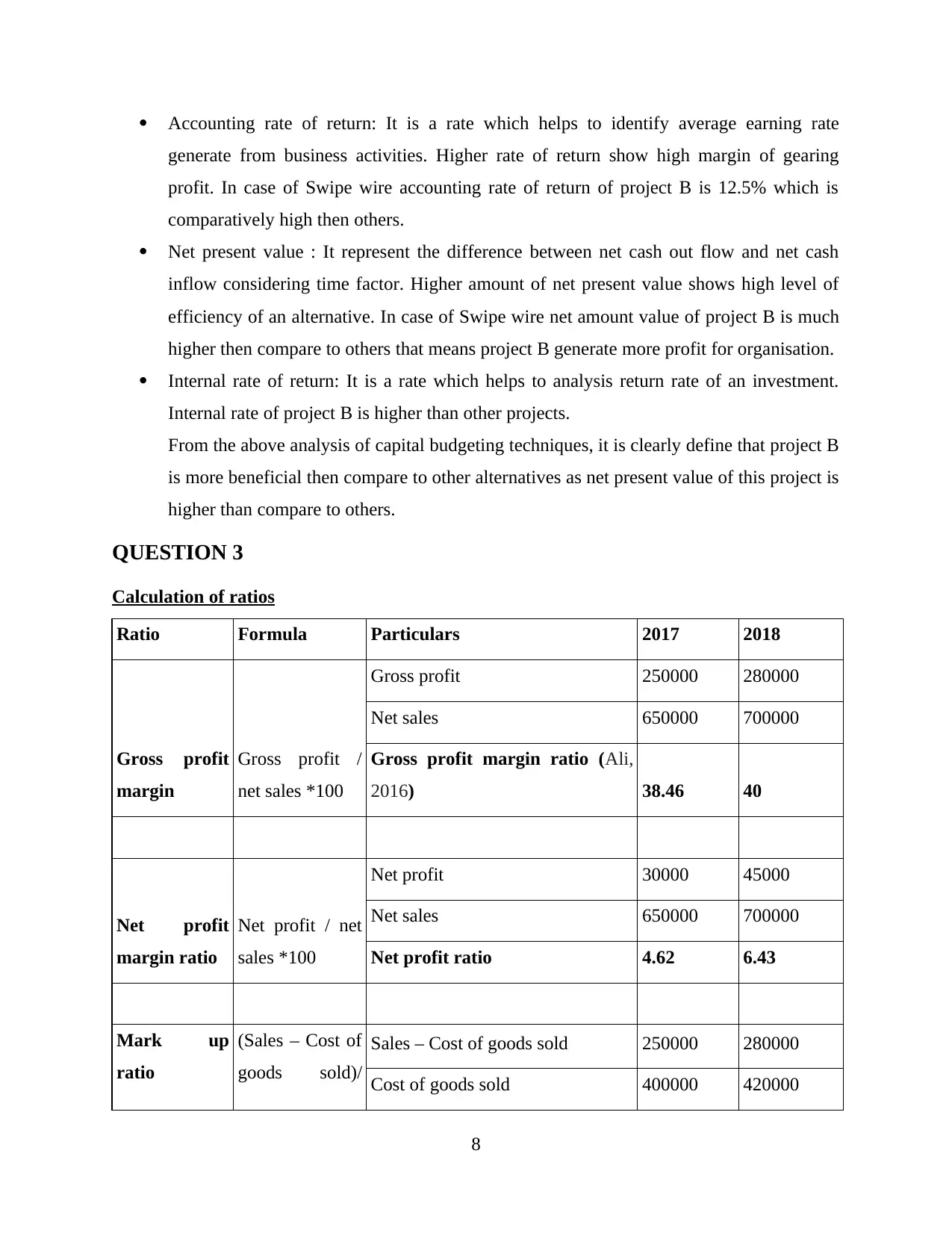

Accounting rate of return: It is a rate which helps to identify average earning rate

generate from business activities. Higher rate of return show high margin of gearing

profit. In case of Swipe wire accounting rate of return of project B is 12.5% which is

comparatively high then others.

Net present value : It represent the difference between net cash out flow and net cash

inflow considering time factor. Higher amount of net present value shows high level of

efficiency of an alternative. In case of Swipe wire net amount value of project B is much

higher then compare to others that means project B generate more profit for organisation.

Internal rate of return: It is a rate which helps to analysis return rate of an investment.

Internal rate of project B is higher than other projects.

From the above analysis of capital budgeting techniques, it is clearly define that project B

is more beneficial then compare to other alternatives as net present value of this project is

higher than compare to others.

QUESTION 3

Calculation of ratios

Ratio Formula Particulars 2017 2018

Gross profit

margin

Gross profit /

net sales *100

Gross profit 250000 280000

Net sales 650000 700000

Gross profit margin ratio (Ali,

2016) 38.46 40

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

Mark up

ratio

(Sales – Cost of

goods sold)/

Sales – Cost of goods sold 250000 280000

Cost of goods sold 400000 420000

8

generate from business activities. Higher rate of return show high margin of gearing

profit. In case of Swipe wire accounting rate of return of project B is 12.5% which is

comparatively high then others.

Net present value : It represent the difference between net cash out flow and net cash

inflow considering time factor. Higher amount of net present value shows high level of

efficiency of an alternative. In case of Swipe wire net amount value of project B is much

higher then compare to others that means project B generate more profit for organisation.

Internal rate of return: It is a rate which helps to analysis return rate of an investment.

Internal rate of project B is higher than other projects.

From the above analysis of capital budgeting techniques, it is clearly define that project B

is more beneficial then compare to other alternatives as net present value of this project is

higher than compare to others.

QUESTION 3

Calculation of ratios

Ratio Formula Particulars 2017 2018

Gross profit

margin

Gross profit /

net sales *100

Gross profit 250000 280000

Net sales 650000 700000

Gross profit margin ratio (Ali,

2016) 38.46 40

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

Mark up

ratio

(Sales – Cost of

goods sold)/

Sales – Cost of goods sold 250000 280000

Cost of goods sold 400000 420000

8

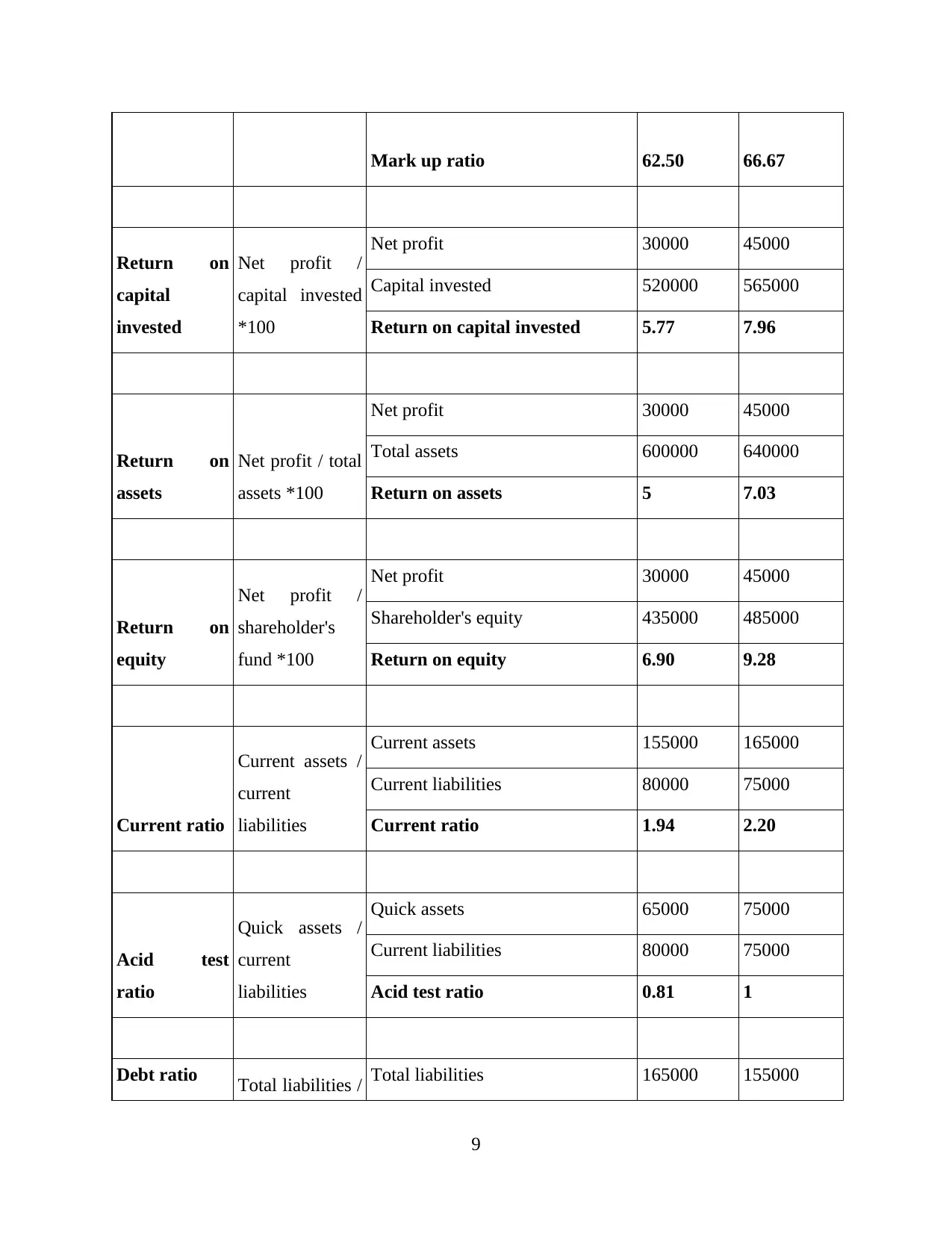

Mark up ratio 62.50 66.67

Return on

capital

invested

Net profit /

capital invested

*100

Net profit 30000 45000

Capital invested 520000 565000

Return on capital invested 5.77 7.96

Return on

assets

Net profit / total

assets *100

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 7.03

Return on

equity

Net profit /

shareholder's

fund *100

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 9.28

Current ratio

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Acid test

ratio

Quick assets /

current

liabilities

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

Debt ratio Total liabilities / Total liabilities 165000 155000

9

Return on

capital

invested

Net profit /

capital invested

*100

Net profit 30000 45000

Capital invested 520000 565000

Return on capital invested 5.77 7.96

Return on

assets

Net profit / total

assets *100

Net profit 30000 45000

Total assets 600000 640000

Return on assets 5 7.03

Return on

equity

Net profit /

shareholder's

fund *100

Net profit 30000 45000

Shareholder's equity 435000 485000

Return on equity 6.90 9.28

Current ratio

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

Acid test

ratio

Quick assets /

current

liabilities

Quick assets 65000 75000

Current liabilities 80000 75000

Acid test ratio 0.81 1

Debt ratio Total liabilities / Total liabilities 165000 155000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.