Financial and Management Accounting Report: Stephenson Ltd Analysis

VerifiedAdded on 2022/12/19

|11

|2570

|90

Report

AI Summary

This report provides a comprehensive financial analysis of Stephenson Ltd, examining its financial performance over two years. It begins by calculating gross and net profits, along with relevant ratios, to assess profitability trends. The report then delves into the reasons behind declining profits and cash flow issues, followed by recommendations for strategic improvements. Break-even and cost-volume-profit analyses are performed for 'The Climbing Cat' to determine profitable sales targets. The report further explores the advantages and disadvantages of Activity Based Costing. Finally, it analyzes variances between projected and actual figures, projecting their business consequences, and suggesting strategies for variance elimination or correction. The report concludes with an evaluation of the advantages and disadvantages of switching from Incremental Based Budgeting to Zero Based Budgeting.

Financial and

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

1. Calculate the Gross and Net (or Operating) Profit made by Stephenson Ltd in each

accounting year...........................................................................................................................1

2. Calculate the Gross Profit and Net Profit to Sales ratios for each year. Explain why each of

these ratios is significant when analysing profitability?.............................................................1

3. Reasons for the company’s declining profits and increasing cash flow problems between

2019 and 2020.............................................................................................................................2

4. Advise the directors of three strategies you would recommend to improve the financial

position of the company and explain in detail how these could lead to increased profits in the

next financial year.......................................................................................................................2

QUESTION 2...................................................................................................................................3

1. Calculate the Break Even Point of Production for ‘The Climbing Cat’.................................3

2. Use of either Break Even Analysis or Cost Volume Profit Analysis enable the company to

set profitable sales revenue targets?............................................................................................3

3. Advantages and disadvantages of switch to Activity Based Costing and explain how this

may help them to ensure that all lines are being priced profitably.............................................3

QUESTION 3...................................................................................................................................5

1. Calculation of three significant variances between projected and outrun figures...................5

2. An explanation for likely/possible causes of these variances.................................................5

3. Projection of potential consequences for the business of each of the variances you have

chosen..........................................................................................................................................5

4. Suggested strategies for elimination or correction of these variances– either through a

change in the current costing model or changes to operations....................................................5

QUESTION 1...................................................................................................................................1

1. Calculate the Gross and Net (or Operating) Profit made by Stephenson Ltd in each

accounting year...........................................................................................................................1

2. Calculate the Gross Profit and Net Profit to Sales ratios for each year. Explain why each of

these ratios is significant when analysing profitability?.............................................................1

3. Reasons for the company’s declining profits and increasing cash flow problems between

2019 and 2020.............................................................................................................................2

4. Advise the directors of three strategies you would recommend to improve the financial

position of the company and explain in detail how these could lead to increased profits in the

next financial year.......................................................................................................................2

QUESTION 2...................................................................................................................................3

1. Calculate the Break Even Point of Production for ‘The Climbing Cat’.................................3

2. Use of either Break Even Analysis or Cost Volume Profit Analysis enable the company to

set profitable sales revenue targets?............................................................................................3

3. Advantages and disadvantages of switch to Activity Based Costing and explain how this

may help them to ensure that all lines are being priced profitably.............................................3

QUESTION 3...................................................................................................................................5

1. Calculation of three significant variances between projected and outrun figures...................5

2. An explanation for likely/possible causes of these variances.................................................5

3. Projection of potential consequences for the business of each of the variances you have

chosen..........................................................................................................................................5

4. Suggested strategies for elimination or correction of these variances– either through a

change in the current costing model or changes to operations....................................................5

5. Evaluation of the advantages disadvantages of a switch from Incremental Based Budgeting

to Zero Based Budgeting.............................................................................................................6

REFERENCES................................................................................................................................8

to Zero Based Budgeting.............................................................................................................6

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

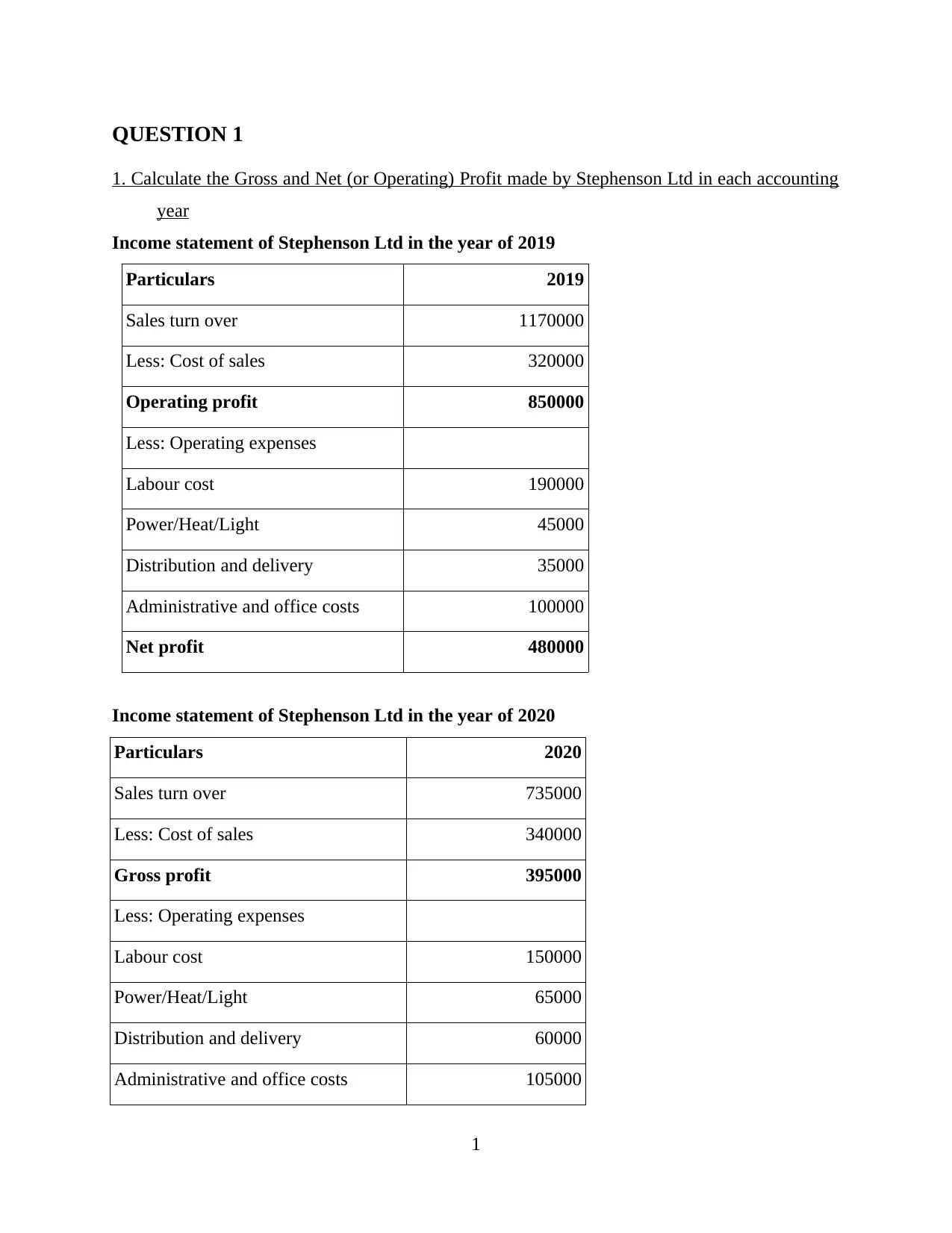

QUESTION 1

1. Calculate the Gross and Net (or Operating) Profit made by Stephenson Ltd in each accounting

year

Income statement of Stephenson Ltd in the year of 2019

Particulars 2019

Sales turn over 1170000

Less: Cost of sales 320000

Operating profit 850000

Less: Operating expenses

Labour cost 190000

Power/Heat/Light 45000

Distribution and delivery 35000

Administrative and office costs 100000

Net profit 480000

Income statement of Stephenson Ltd in the year of 2020

Particulars 2020

Sales turn over 735000

Less: Cost of sales 340000

Gross profit 395000

Less: Operating expenses

Labour cost 150000

Power/Heat/Light 65000

Distribution and delivery 60000

Administrative and office costs 105000

1

1. Calculate the Gross and Net (or Operating) Profit made by Stephenson Ltd in each accounting

year

Income statement of Stephenson Ltd in the year of 2019

Particulars 2019

Sales turn over 1170000

Less: Cost of sales 320000

Operating profit 850000

Less: Operating expenses

Labour cost 190000

Power/Heat/Light 45000

Distribution and delivery 35000

Administrative and office costs 100000

Net profit 480000

Income statement of Stephenson Ltd in the year of 2020

Particulars 2020

Sales turn over 735000

Less: Cost of sales 340000

Gross profit 395000

Less: Operating expenses

Labour cost 150000

Power/Heat/Light 65000

Distribution and delivery 60000

Administrative and office costs 105000

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit 15000

2. Calculate the Gross Profit and Net Profit to Sales ratios for each year. Explain why each of

these ratios is significant when analysing profitability?

Gross profit to sales ratio: Gross profit/Net sales*100

In 2019 = 850000 / 1170000 *100

= 72.65%

In 2020 = 395000 / 735000 * 100

= 53.74%

Net profit to sales ratio: Net profit/Net sales*100

In 2019 = 480000 / 1170000 *100

= 41.02%

In 2020 = 15000 / 735000 * 100

= 2.04%

3. Reasons for the company’s declining profits and increasing cash flow problems between 2019

and 2020

There are main reason of declining profit of the Stephenson Ltd that are mentioned

below:

Lower sales turn over

increase expenditure

Offer discount on early payment

Improve inventory

4. Advise the directors of three strategies you would recommend to improve the financial

position of the company and explain in detail how these could lead to increased profits in

the next financial year.

Financial health is a way to analysis of actual financial position of any small to to large

business entities. There are suggesting three strategies to improve financial position of

Stephenson Ltd such as:

Consider investment: Investment in real estate can be beneficial for company because

real estate value fluctuated and holds some value. It is essential aspect that must consider

2

2. Calculate the Gross Profit and Net Profit to Sales ratios for each year. Explain why each of

these ratios is significant when analysing profitability?

Gross profit to sales ratio: Gross profit/Net sales*100

In 2019 = 850000 / 1170000 *100

= 72.65%

In 2020 = 395000 / 735000 * 100

= 53.74%

Net profit to sales ratio: Net profit/Net sales*100

In 2019 = 480000 / 1170000 *100

= 41.02%

In 2020 = 15000 / 735000 * 100

= 2.04%

3. Reasons for the company’s declining profits and increasing cash flow problems between 2019

and 2020

There are main reason of declining profit of the Stephenson Ltd that are mentioned

below:

Lower sales turn over

increase expenditure

Offer discount on early payment

Improve inventory

4. Advise the directors of three strategies you would recommend to improve the financial

position of the company and explain in detail how these could lead to increased profits in

the next financial year.

Financial health is a way to analysis of actual financial position of any small to to large

business entities. There are suggesting three strategies to improve financial position of

Stephenson Ltd such as:

Consider investment: Investment in real estate can be beneficial for company because

real estate value fluctuated and holds some value. It is essential aspect that must consider

2

by the company to keep financial activities stable. Since a different set of rules apply to

foreigners markets because it is always best to hire experiment by local professionals.

Upgrade record keeping: It is most important strategy that when an entity use updated

accounting books so it helps to clearly present all the transactions hat occur in particular

financial year (Wahyuni and Putra, 2020).

Expand customer base: As for new clients company can invest in various marketing

tools that supports to brand in gain more visibility in case of enhance traffic. It is

essential to find the balance between the money that require to invest and expect to back

by attracting new customers.

These strategies are helping to increased profits because when company invest amount in

real estate so they are getting interest on their investment and many time earned large

profitability. By the expand customer base organisation sell out more products to company and

generate profitability. At the end by upgrade record keeping an entity analysis all the income and

expenditure in proper manner and take right decision that helps to increase profitability.

QUESTION 2

1. Calculate the Break Even Point of Production for ‘The Climbing Cat’.

Break even point for Climbing cat: Fixed cost / Selling price – variable cost

= 100,000 / 15 -5

= 100,000 / 10

= 10,000

2. Use of either Break Even Analysis or Cost Volume Profit Analysis enable the company to set

profitable sales revenue targets?

Break event analysis as well as cost volume profit analysis both are essential for set up

profitable sales revenues targets. There are mentioning different usage of these analysis:

A business sets a budget that depend upon different assumptions like revenues, costs,

product mixes and overall volumes. With the helps of CVP analysis focus on the impact

of budgeted profit and consider changes of such different elements (Oyewo and

AJIBOLADE, 2019).

3

foreigners markets because it is always best to hire experiment by local professionals.

Upgrade record keeping: It is most important strategy that when an entity use updated

accounting books so it helps to clearly present all the transactions hat occur in particular

financial year (Wahyuni and Putra, 2020).

Expand customer base: As for new clients company can invest in various marketing

tools that supports to brand in gain more visibility in case of enhance traffic. It is

essential to find the balance between the money that require to invest and expect to back

by attracting new customers.

These strategies are helping to increased profits because when company invest amount in

real estate so they are getting interest on their investment and many time earned large

profitability. By the expand customer base organisation sell out more products to company and

generate profitability. At the end by upgrade record keeping an entity analysis all the income and

expenditure in proper manner and take right decision that helps to increase profitability.

QUESTION 2

1. Calculate the Break Even Point of Production for ‘The Climbing Cat’.

Break even point for Climbing cat: Fixed cost / Selling price – variable cost

= 100,000 / 15 -5

= 100,000 / 10

= 10,000

2. Use of either Break Even Analysis or Cost Volume Profit Analysis enable the company to set

profitable sales revenue targets?

Break event analysis as well as cost volume profit analysis both are essential for set up

profitable sales revenues targets. There are mentioning different usage of these analysis:

A business sets a budget that depend upon different assumptions like revenues, costs,

product mixes and overall volumes. With the helps of CVP analysis focus on the impact

of budgeted profit and consider changes of such different elements (Oyewo and

AJIBOLADE, 2019).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Through cost volume analysis measure all the characteristics of economics that based on

the proposed items. On the basis of different accounting data analysis the sales quantity

that require for break event and sales quantity needed to generate a desired profit margin.

3. Advantages and disadvantages of switch to Activity Based Costing and explain how this may

help them to ensure that all lines are being priced profitably

Activity based costing: ABC is more often used in the industrial industry because it

improves the accuracy of cost statistics, resulting in virtually true costs and a clearer

classification of the costs generated by the firm during the development period. Target costs,

inventory costing, product portfolio profitability analysis, consumer financial accounting, and

process metrics all use this costing method. Activity-based costing is used to gain a deeper

understanding of prices, enabling businesses to have a better pricing policy. It has certain

advantages and disadvantages which are as follows:

Advantage

Accurate Product Cost- By reflecting on the cause and effect interaction in the cost

incurrence, ABC improves the precision and efficiency of commodity financing costs. It

acknowledges that actions, not goods, generate costs, and that products absorb activities.

ABC has more rational component prices in advanced production environments and

technologies, where functional areas overheads account for a significant portion of

overall costs (Ng, 2018).

Information about Cost Behaviour- ABC recognizes the true essence of expense

behaviours and assists in cost reduction and the identification of behaviours that bring

little benefit to the commodity. Managers can control certain fixed overhead costs with

ABC by exerting more control over the operations that result in these variable overhead

costs. This is so since certain fixed overhead costs' behaviour in relation to operations is

now more evident and transparent.

Disadvantage

Not suitable for Smaller Firms: ABC is useful in many ways for different

organizations. For example, a big industrial company may do it more effectively than a

small business. ABC is also expected to benefit companies who use cost-plus pricing

because it has reliable commodity costs. Firms that use market-based pricing, on the

4

the proposed items. On the basis of different accounting data analysis the sales quantity

that require for break event and sales quantity needed to generate a desired profit margin.

3. Advantages and disadvantages of switch to Activity Based Costing and explain how this may

help them to ensure that all lines are being priced profitably

Activity based costing: ABC is more often used in the industrial industry because it

improves the accuracy of cost statistics, resulting in virtually true costs and a clearer

classification of the costs generated by the firm during the development period. Target costs,

inventory costing, product portfolio profitability analysis, consumer financial accounting, and

process metrics all use this costing method. Activity-based costing is used to gain a deeper

understanding of prices, enabling businesses to have a better pricing policy. It has certain

advantages and disadvantages which are as follows:

Advantage

Accurate Product Cost- By reflecting on the cause and effect interaction in the cost

incurrence, ABC improves the precision and efficiency of commodity financing costs. It

acknowledges that actions, not goods, generate costs, and that products absorb activities.

ABC has more rational component prices in advanced production environments and

technologies, where functional areas overheads account for a significant portion of

overall costs (Ng, 2018).

Information about Cost Behaviour- ABC recognizes the true essence of expense

behaviours and assists in cost reduction and the identification of behaviours that bring

little benefit to the commodity. Managers can control certain fixed overhead costs with

ABC by exerting more control over the operations that result in these variable overhead

costs. This is so since certain fixed overhead costs' behaviour in relation to operations is

now more evident and transparent.

Disadvantage

Not suitable for Smaller Firms: ABC is useful in many ways for different

organizations. For example, a big industrial company may do it more effectively than a

small business. ABC is also expected to benefit companies who use cost-plus pricing

because it has reliable commodity costs. Firms that use market-based pricing, on the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

other hand, do not favour ABC. The implementation of ABC is often influenced by the

level of technologies in the manufacturing climate in each company.

Measurement difficulties: The measurements used to incorporate an ABC system are

the system's key costs and limitations. Management must predict the costs of operation

pools and define and calculate cost factors to operate as cost allocation bases in ABC

programs. Also the most simplistic ABC structures necessitate various estimates to assess

product and service prices. This calculation is prohibitively expensive. Activity expense

thresholds must also be revised on a regular basis (Fadjar and Sardjudin, 2020).

QUESTION 3

1. Calculation of three significant variances between projected and outrun figures.

Sales price variance: Budgeted sales – Actual sales

= 1000,000 – 660,000

= 340000 (F)

Material price variance: Budgeted material price – Actual material price

= 330000 – 410000

= 77000 (A)

Labour price variance: Budgeted labour variance – Actual labour variance

= 150000 – 220000

= 70000 (A)

2. An explanation for likely/possible causes of these variances

Material price variance: Reason for favourable material variance that overall decrease

in the market price level and buy of materials of less quality than the standard hat will be

presented as adverse manner.

Labour price variance: The reason of adverse labour price variance that use incorrect

standards, component trade off, pay premiums and many others.

Sales variance: Favourable sales variance present actual selling price is greater than

standard. It could outcomes in a deduction in demand and consider adverse sales variance. It

would mainly be caused as a administration by a management decision to enhance prices

possibly by the anticipation of cost enhance (Dang Le and Pham, 2021).

5

level of technologies in the manufacturing climate in each company.

Measurement difficulties: The measurements used to incorporate an ABC system are

the system's key costs and limitations. Management must predict the costs of operation

pools and define and calculate cost factors to operate as cost allocation bases in ABC

programs. Also the most simplistic ABC structures necessitate various estimates to assess

product and service prices. This calculation is prohibitively expensive. Activity expense

thresholds must also be revised on a regular basis (Fadjar and Sardjudin, 2020).

QUESTION 3

1. Calculation of three significant variances between projected and outrun figures.

Sales price variance: Budgeted sales – Actual sales

= 1000,000 – 660,000

= 340000 (F)

Material price variance: Budgeted material price – Actual material price

= 330000 – 410000

= 77000 (A)

Labour price variance: Budgeted labour variance – Actual labour variance

= 150000 – 220000

= 70000 (A)

2. An explanation for likely/possible causes of these variances

Material price variance: Reason for favourable material variance that overall decrease

in the market price level and buy of materials of less quality than the standard hat will be

presented as adverse manner.

Labour price variance: The reason of adverse labour price variance that use incorrect

standards, component trade off, pay premiums and many others.

Sales variance: Favourable sales variance present actual selling price is greater than

standard. It could outcomes in a deduction in demand and consider adverse sales variance. It

would mainly be caused as a administration by a management decision to enhance prices

possibly by the anticipation of cost enhance (Dang Le and Pham, 2021).

5

3. Projection of potential consequences for the business of each of the variances you have

chosen

The potential consequences of each variances in business that these variances are helping

to know actual results and how much differences are occur in the business. On the basis of these

variances know the actual performance of business in depth manner.

4. Suggested strategies for elimination or correction of these variances– either through a change

in the current costing model or changes to operations

There are applied different strategies for elimination and correction of such variances by

current costing model. Cost can be simply as money and resources that related with a

acquire/business transaction or any other activity. Various sectors are selecting these methods in

order to predict costs of their products that based on the nature of the manufacturing and kind of

output.

5. Evaluation of the advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting

ZBB: Zero-based budgeting (ZBB) is a budget planning system in which all costs for

any new cycle must be explained. The method of zero-based budgeting begins with a "zero

basis," and each role of an institution's needs and costs are evaluated. Budgets are then created

based on what is required for the next year, irrespective as to whether each plan is better or

smaller than the one before it (Abbasi, Khanmohammadi, Moradi and Mahmoodiyan, 2019).

There can be some advantages and disadvantages of ZBB which are as follows:

Benefits-

It Promotes Optimization in business process management- Streamlining spending and

concentrating on certain aspects that actually impact your company by adding value,

lowering costs, increasing performance, and so on lets you "trim the fat" and promote

long-term progress. Streamlining workflows and keeping tabs on spending aids proactive

decision-making, financial planning, and cash flow management, as well as exposing

ways to rethink goals at the initiative, agency, branch, and organizational levels.

It Prioritizes Resource Allocation Efficiency- Once a ZBB scheme is in operation, money

can be spent even more efficiently so all expenditures that return a good ROI (in income,

cost savings, value creation, etc.) receive the capital they need, whereas less important

6

chosen

The potential consequences of each variances in business that these variances are helping

to know actual results and how much differences are occur in the business. On the basis of these

variances know the actual performance of business in depth manner.

4. Suggested strategies for elimination or correction of these variances– either through a change

in the current costing model or changes to operations

There are applied different strategies for elimination and correction of such variances by

current costing model. Cost can be simply as money and resources that related with a

acquire/business transaction or any other activity. Various sectors are selecting these methods in

order to predict costs of their products that based on the nature of the manufacturing and kind of

output.

5. Evaluation of the advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting

ZBB: Zero-based budgeting (ZBB) is a budget planning system in which all costs for

any new cycle must be explained. The method of zero-based budgeting begins with a "zero

basis," and each role of an institution's needs and costs are evaluated. Budgets are then created

based on what is required for the next year, irrespective as to whether each plan is better or

smaller than the one before it (Abbasi, Khanmohammadi, Moradi and Mahmoodiyan, 2019).

There can be some advantages and disadvantages of ZBB which are as follows:

Benefits-

It Promotes Optimization in business process management- Streamlining spending and

concentrating on certain aspects that actually impact your company by adding value,

lowering costs, increasing performance, and so on lets you "trim the fat" and promote

long-term progress. Streamlining workflows and keeping tabs on spending aids proactive

decision-making, financial planning, and cash flow management, as well as exposing

ways to rethink goals at the initiative, agency, branch, and organizational levels.

It Prioritizes Resource Allocation Efficiency- Once a ZBB scheme is in operation, money

can be spent even more efficiently so all expenditures that return a good ROI (in income,

cost savings, value creation, etc.) receive the capital they need, whereas less important

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

line items are pushed down the list of priorities or omitted entirely instead of being added

to the next plan immediately.

Drawbacks

It Can Be Complex and Expensive- Zero-based budgeting, in contrast to conventional

budgeting methods, can be very expensive, as well as time-consuming and difficult to

execute. When making the move, the additional preparation involved (such as using any

new tools, workflows, etc.) as well as the fact each plan is designed from scratch rather

than depending on the (easier and quicker) data from the previous year will add

considerable cost. The burden can be too much for businesses with limited resources.

It’s Disruptive- For others, converting to ZBB can be mentally and intellectually

exhausting. Executives can find it hard to maintain the transition to promoting and

explaining each item in their budgets on a monthly basis, causing resistance that must be

overcome before you can work at maximum productivity (Valaskova, Kliestik and

Kovacova, 2018).

7

to the next plan immediately.

Drawbacks

It Can Be Complex and Expensive- Zero-based budgeting, in contrast to conventional

budgeting methods, can be very expensive, as well as time-consuming and difficult to

execute. When making the move, the additional preparation involved (such as using any

new tools, workflows, etc.) as well as the fact each plan is designed from scratch rather

than depending on the (easier and quicker) data from the previous year will add

considerable cost. The burden can be too much for businesses with limited resources.

It’s Disruptive- For others, converting to ZBB can be mentally and intellectually

exhausting. Executives can find it hard to maintain the transition to promoting and

explaining each item in their budgets on a monthly basis, causing resistance that must be

overcome before you can work at maximum productivity (Valaskova, Kliestik and

Kovacova, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Wahyuni, N. and Putra, Y., 2020. Towards understanding changes in management accounting in

the manufacturing industry in Indonesia. Accounting. 6(7). pp.1245-1252.

Oyewo, B. and AJIBOLADE, S., 2019. Does the use of strategic management accounting

techniques creates and sustains competitive advantage? Some empirical evidence.

Annals of Spiru Haret University. Economic Series. 19(2). pp.61-91.

Ng, A. W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

Fadjar, A. and Sardjudin, K. N., 2020. Factors that Influence Decision Making through the

Application of Management Accounting Information Systems. International Journal of

Psychosocial Rehabilitation. 24(2).

Dang, L., Le, T. and Pham, T., 2021. The effect of strategic management accounting on business

performance of sugar enterprises in Vietnam. Accounting. 7(5). pp.1085-1094.

Abbasi, B., Khanmohammadi, M., Moradi, Z. and Mahmoodiyan, T., 2019. Capacity Building of

Green Accounting Consequences Based on the Explanation of Strategic Management

Accounting Techniques. Iranian Journal of Finance. 3(4). pp.23-59.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia Copernicana. 9(1). pp.105-121.

8

Books and Journals

Wahyuni, N. and Putra, Y., 2020. Towards understanding changes in management accounting in

the manufacturing industry in Indonesia. Accounting. 6(7). pp.1245-1252.

Oyewo, B. and AJIBOLADE, S., 2019. Does the use of strategic management accounting

techniques creates and sustains competitive advantage? Some empirical evidence.

Annals of Spiru Haret University. Economic Series. 19(2). pp.61-91.

Ng, A. W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

Fadjar, A. and Sardjudin, K. N., 2020. Factors that Influence Decision Making through the

Application of Management Accounting Information Systems. International Journal of

Psychosocial Rehabilitation. 24(2).

Dang, L., Le, T. and Pham, T., 2021. The effect of strategic management accounting on business

performance of sugar enterprises in Vietnam. Accounting. 7(5). pp.1085-1094.

Abbasi, B., Khanmohammadi, M., Moradi, Z. and Mahmoodiyan, T., 2019. Capacity Building of

Green Accounting Consequences Based on the Explanation of Strategic Management

Accounting Techniques. Iranian Journal of Finance. 3(4). pp.23-59.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia Copernicana. 9(1). pp.105-121.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.