Accounting for Managers: Financial Statement Analysis Report

VerifiedAdded on 2020/09/03

|15

|3439

|29

Report

AI Summary

This report provides a comprehensive overview of accounting principles relevant for managers, covering a range of topics including the differentiation between financial and management accounting reports, classification of accounting terms, analysis of financial structure, and the distinction between cash flow budgets and statements of cash flows. The report also explores depreciation, financial ratios, profitability and solvency analysis, variable cost computations, contribution margin, break-even output, and the preparation of price quotations. Furthermore, it delves into the impact of debt, changes in owner's equity, and the reasons for retaining profits within a business. The report utilizes financial ratios to assess the financial performance of a company and provides insights into its profitability and solvency. It also includes calculations for variable costs, contribution margins, and break-even points, culminating in a conclusion and references.

Accounting for Managers 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

A. Differentiating between financial accounting report and management accounting report1

Q.2 Classifying the following terms:-....................................................................................1

C) Analysing the financial structure of the public company:-...............................................2

D) Differentiating between a cash flow budget and a statement of cash flows:-..................2

E. Depreciation and importance of depreciation in business point of view- .........................3

F. Comparing the pair and determining which is larger aspects:-..........................................3

Question 2........................................................................................................................................4

A. Financial position and performance that affected by not taking into account the fact that a

debt:-.......................................................................................................................................4

B. Factors that causing negative cash flow from operating activity:-....................................4

C. Changes in owner equity:- ................................................................................................4

D. Explaining the reasons why business owners would leave profits in the business rather

than withdrawing them for personal use:- .............................................................................5

Question 3........................................................................................................................................5

A) Calculation of financial ratios...........................................................................................5

B) Report about the profitability and solvency of the company............................................7

Question 4........................................................................................................................................7

A) Computation of variable cost per glass.............................................................................7

B) Contribution per margin....................................................................................................7

C) Break-even output.............................................................................................................8

D) Acceptance of order..........................................................................................................8

E) Conclusion.........................................................................................................................8

F) Calculation of Profit and Loss..........................................................................................8

Question 5........................................................................................................................................8

Preparation of Price Quotation for Job No. 43.......................................................................8

Question 6........................................................................................................................................9

C. Retained profit and earnings...........................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

A. Differentiating between financial accounting report and management accounting report1

Q.2 Classifying the following terms:-....................................................................................1

C) Analysing the financial structure of the public company:-...............................................2

D) Differentiating between a cash flow budget and a statement of cash flows:-..................2

E. Depreciation and importance of depreciation in business point of view- .........................3

F. Comparing the pair and determining which is larger aspects:-..........................................3

Question 2........................................................................................................................................4

A. Financial position and performance that affected by not taking into account the fact that a

debt:-.......................................................................................................................................4

B. Factors that causing negative cash flow from operating activity:-....................................4

C. Changes in owner equity:- ................................................................................................4

D. Explaining the reasons why business owners would leave profits in the business rather

than withdrawing them for personal use:- .............................................................................5

Question 3........................................................................................................................................5

A) Calculation of financial ratios...........................................................................................5

B) Report about the profitability and solvency of the company............................................7

Question 4........................................................................................................................................7

A) Computation of variable cost per glass.............................................................................7

B) Contribution per margin....................................................................................................7

C) Break-even output.............................................................................................................8

D) Acceptance of order..........................................................................................................8

E) Conclusion.........................................................................................................................8

F) Calculation of Profit and Loss..........................................................................................8

Question 5........................................................................................................................................8

Preparation of Price Quotation for Job No. 43.......................................................................8

Question 6........................................................................................................................................9

C. Retained profit and earnings...........................................................................................10

d) non financial information that venture capitalist concern about......................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is quite useful for management to analyse business transactions. Present

report deals with various accounting practices which are used by the management to assess

performance of business and take enhanced decisions. Thus, accounting practices aids in making

better decisions by the management.

Question 1

A. Differentiating between financial accounting report and management accounting report

The major difference between management accounting and financial accounting report is

management accounting reports presented internally and financial accounting report is presented

for the external stakeholders. Financial accounting reports shows present the financial healt of

the company while management accounting reports concerning the day to day operation and

helping to the managers in decision making process.

Financial accounting examples: 1. Balance sheet- A balance sheet shows of a company assets

liabilities, and shareholders equity. 2.Income statement- Income statement of a company shows

company expenses and revenue over a certain time of period (Scott, 2015).

Management accounting examples:-1. Budget report- budget reports shows expected revenues

and expenses incurred in a certain time period.

2. Job costing report- the cost incurred by specific job and compared with revenue expectation.

Q.2 Classifying the following terms:-

Paid up capital- paid up capital is the total amount of money which company receive in

exchange of shares. In balance sheet paid up capital shown under the shareholders' equity

section.

Bank loan- a bank loan is current liabilities that represent the debt which paid up in the

following mention year.

Provision of annual leave – In balance sheet provision of annual leave shown in current

liabilities. This provision made is made for the respect of annual leave entitlement.

1

Accounting is quite useful for management to analyse business transactions. Present

report deals with various accounting practices which are used by the management to assess

performance of business and take enhanced decisions. Thus, accounting practices aids in making

better decisions by the management.

Question 1

A. Differentiating between financial accounting report and management accounting report

The major difference between management accounting and financial accounting report is

management accounting reports presented internally and financial accounting report is presented

for the external stakeholders. Financial accounting reports shows present the financial healt of

the company while management accounting reports concerning the day to day operation and

helping to the managers in decision making process.

Financial accounting examples: 1. Balance sheet- A balance sheet shows of a company assets

liabilities, and shareholders equity. 2.Income statement- Income statement of a company shows

company expenses and revenue over a certain time of period (Scott, 2015).

Management accounting examples:-1. Budget report- budget reports shows expected revenues

and expenses incurred in a certain time period.

2. Job costing report- the cost incurred by specific job and compared with revenue expectation.

Q.2 Classifying the following terms:-

Paid up capital- paid up capital is the total amount of money which company receive in

exchange of shares. In balance sheet paid up capital shown under the shareholders' equity

section.

Bank loan- a bank loan is current liabilities that represent the debt which paid up in the

following mention year.

Provision of annual leave – In balance sheet provision of annual leave shown in current

liabilities. This provision made is made for the respect of annual leave entitlement.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Brand name and Intellectual property- Brand name and intellectual property are

considered as capital assets and recorded in balance sheet as intangible assets.

Account receivable – account receivable represents a money which owned by its

customers and in balance sheet account receivable recorded as current assets.

Prepaid insurance premium- It is the portion of total insurance that have been paid in

advance so in balance sheet prepaid insurance premium considered in assets side.

Deposit paid by a customer for work yet to be done – this term concern in balance sheet

as current liabilities (Libby, 2017).

Retained profit- Retained profit is the total percentage of net earning by the company and

recorded under shareholders' equity in balance sheet.

C) Analysing the financial structure of the public company:-

1. In a public company ownership is spread among the general public in form of shares

which are freely traded in stock exchange. Public company can transform into private company

by buy back shares from shareholders. A public company can transform into private company by

sterilization the memorandum of association and the article of association in the company.

2. Apart from shareholders investors and lenders, creditor, management of a company and

government shown interest in financial statement (Khairi and Baridwan, 2015). Commercial

banks, employees and prospective investor have shown interest in financial statements.

D) Differentiating between a cash flow budget and a statement of cash flows:-

One of the major difference between these two is that statement of cash flow is required

for the making of financial statement. Statement of cash flows shows cash inflow and cash

outflow in relevance of company operating activity and financing activity. While the cash budget

is prepared for the upcoming period. Cash budget is the prepared for the planning and utility of

manager.

2

considered as capital assets and recorded in balance sheet as intangible assets.

Account receivable – account receivable represents a money which owned by its

customers and in balance sheet account receivable recorded as current assets.

Prepaid insurance premium- It is the portion of total insurance that have been paid in

advance so in balance sheet prepaid insurance premium considered in assets side.

Deposit paid by a customer for work yet to be done – this term concern in balance sheet

as current liabilities (Libby, 2017).

Retained profit- Retained profit is the total percentage of net earning by the company and

recorded under shareholders' equity in balance sheet.

C) Analysing the financial structure of the public company:-

1. In a public company ownership is spread among the general public in form of shares

which are freely traded in stock exchange. Public company can transform into private company

by buy back shares from shareholders. A public company can transform into private company by

sterilization the memorandum of association and the article of association in the company.

2. Apart from shareholders investors and lenders, creditor, management of a company and

government shown interest in financial statement (Khairi and Baridwan, 2015). Commercial

banks, employees and prospective investor have shown interest in financial statements.

D) Differentiating between a cash flow budget and a statement of cash flows:-

One of the major difference between these two is that statement of cash flow is required

for the making of financial statement. Statement of cash flows shows cash inflow and cash

outflow in relevance of company operating activity and financing activity. While the cash budget

is prepared for the upcoming period. Cash budget is the prepared for the planning and utility of

manager.

2

E. Depreciation and importance of depreciation in business point of view-

Depreciation means the monetary value of an assets decreases over a certain time period

while using of assets and obsolescences. It shows the reduction value of assets. Depreciation is to

used for the reducing the historical value of assets. For replacing or purchasing new assets. Many

companies used depreciation as a tax benefits point of view because depreciation is non cash

expense in income statements.

For instance if a company purchase a $900 machinery on 13th april of 2008 and take

$100 worth of depreciation in 2008 and then additional $100 per year for the next eight years. At

the end of eight years the value of assets is zero.

F. Comparing the pair and determining which is larger aspects:-

Gross profit and Net Profit – gross profit is the first level of the profit in income

statements and it only shows sales revenue less from cost of goods sold and term of net

profit is much wider. Net profit contain all revenues less from all expenses (Christensen,

Lee, Walker and Zeng, 2015).

Paid up capital and owners equity- Paid up capital can never surpass the owner equity.

The owner equity stated the authorized capital which shows upward bound.

Earning per share and dividend per share - earning per share is much broader then the

dividend per share it shows profitability of a company is per share of its stock.

Current assets and current liabilities – current assets much be larger because current

assets contains all cash and cash equivalents receivables.

Operating profit and net profit- net profit is much wider and broader term because net

profit shows after operating expenses deducting from the total revenues.

3

Depreciation means the monetary value of an assets decreases over a certain time period

while using of assets and obsolescences. It shows the reduction value of assets. Depreciation is to

used for the reducing the historical value of assets. For replacing or purchasing new assets. Many

companies used depreciation as a tax benefits point of view because depreciation is non cash

expense in income statements.

For instance if a company purchase a $900 machinery on 13th april of 2008 and take

$100 worth of depreciation in 2008 and then additional $100 per year for the next eight years. At

the end of eight years the value of assets is zero.

F. Comparing the pair and determining which is larger aspects:-

Gross profit and Net Profit – gross profit is the first level of the profit in income

statements and it only shows sales revenue less from cost of goods sold and term of net

profit is much wider. Net profit contain all revenues less from all expenses (Christensen,

Lee, Walker and Zeng, 2015).

Paid up capital and owners equity- Paid up capital can never surpass the owner equity.

The owner equity stated the authorized capital which shows upward bound.

Earning per share and dividend per share - earning per share is much broader then the

dividend per share it shows profitability of a company is per share of its stock.

Current assets and current liabilities – current assets much be larger because current

assets contains all cash and cash equivalents receivables.

Operating profit and net profit- net profit is much wider and broader term because net

profit shows after operating expenses deducting from the total revenues.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

A. Financial position and performance that affected by not taking into account the fact that a

debt:-

A bad debt of company is non fault-finding for a company's operation. Financial debt can

be larger in nature and that directly affect the financial position of the company. For instance:-

Bad Debt expense – bad debts refers to the loss in financial statement because amount of sold

good and services is not paid by the customers. Bad debts recorded as a selling and

administration expenses and shown in the income statement. While calculating net income the

related account of bad debts and accounts of receivables both affected the financial statements.

B. Factors that causing negative cash flow from operating activity:-

1. Dwindling net income – it is the major factor causing in reducing the cash flow from

operating profit from one period to next time period (Diatmika, Irianto and Baridwan,

2016).

2. Declining sales or margin contraction – aforementioned loss of pricing power and

declining aggregate demand in the market can cause the negative cash inflow from the

operating activities.

3. Changing in the working capital – Increase or decrease of current assets and current

liabilities affects the cash flow statements. For instance – labour inventory turnover,

growth in days sales, declining in days payable outstanding.

Yes this is not ideal situation for any company the negative cash flow from operating

activity indicates the poor financial performance and position in a company.

C. Changes in owner equity:-

Revenue & Expenses - revenue is the inflow of all assets uprise out of selling of goods

and services that directly affect the net profit of a company and owners capital if

revenues increase that means there is significantly change in owners capital.

4

A. Financial position and performance that affected by not taking into account the fact that a

debt:-

A bad debt of company is non fault-finding for a company's operation. Financial debt can

be larger in nature and that directly affect the financial position of the company. For instance:-

Bad Debt expense – bad debts refers to the loss in financial statement because amount of sold

good and services is not paid by the customers. Bad debts recorded as a selling and

administration expenses and shown in the income statement. While calculating net income the

related account of bad debts and accounts of receivables both affected the financial statements.

B. Factors that causing negative cash flow from operating activity:-

1. Dwindling net income – it is the major factor causing in reducing the cash flow from

operating profit from one period to next time period (Diatmika, Irianto and Baridwan,

2016).

2. Declining sales or margin contraction – aforementioned loss of pricing power and

declining aggregate demand in the market can cause the negative cash inflow from the

operating activities.

3. Changing in the working capital – Increase or decrease of current assets and current

liabilities affects the cash flow statements. For instance – labour inventory turnover,

growth in days sales, declining in days payable outstanding.

Yes this is not ideal situation for any company the negative cash flow from operating

activity indicates the poor financial performance and position in a company.

C. Changes in owner equity:-

Revenue & Expenses - revenue is the inflow of all assets uprise out of selling of goods

and services that directly affect the net profit of a company and owners capital if

revenues increase that means there is significantly change in owners capital.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact of Equity structure – when a company loses money during the normal cause of

business resulted will their decreasing in equity of owners capital. This term affects when

the owner take out cash for personal use and paying cash for an expense.

Interest Rates – interest rates changes the company profit secure or unsecured loans with

fixed or floating rates affect the operating activities of business. If there is higher rate of

interest in loans that mean directing affecting the business activities (Zeff, 2016).

D. Explaining the reasons why business owners would leave profits in the business rather than

withdrawing them for personal use:-

1. Better Return on Investment:- A higher rate of return on investment assisting the

owner to not withdrawing all money from business. A higher rate of return making the financial

structure strong. If business owners would leave the profit in the organization resulted company

financial and income statements shows a better growth (Accounting, 2018). It also promotes the

strategies to increase sales revenue for instance:- increase productivity of your staff, develop new

product lines, find new customers. If company face any type of financial crisis management can

use the owners' equity fund for the reducing the impact of the organization. More ownerships'

equity promotes the long term business strategies for expanding the operational areas.

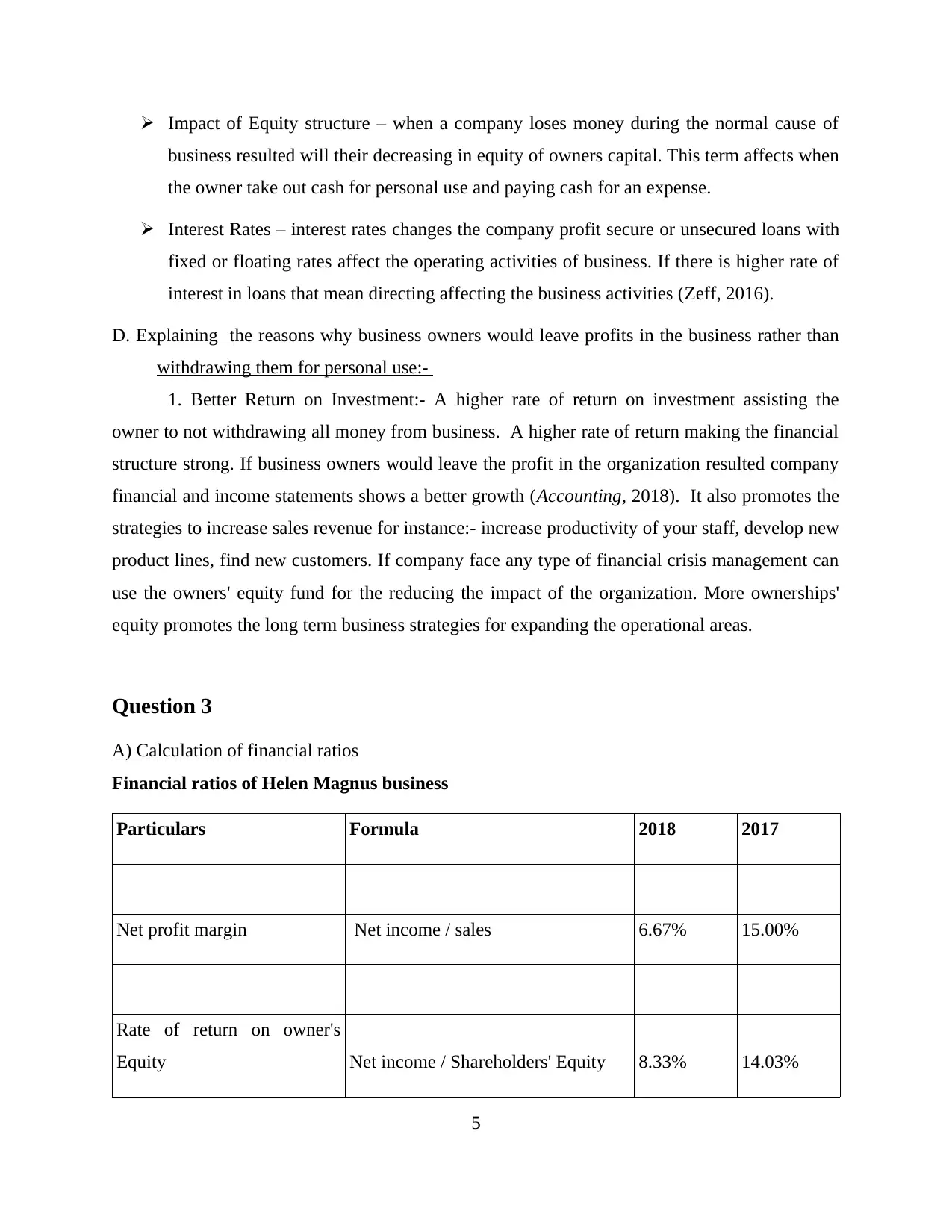

Question 3

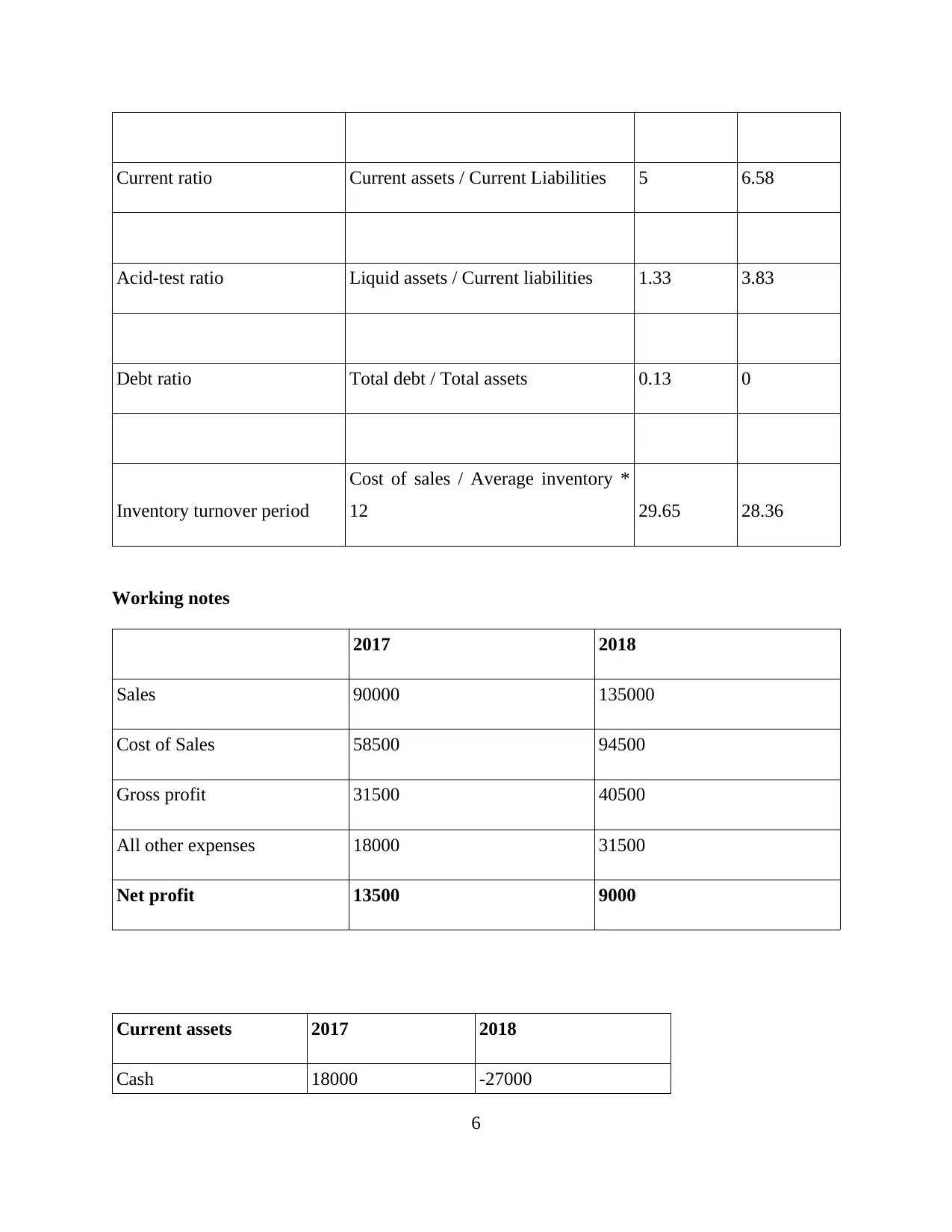

A) Calculation of financial ratios

Financial ratios of Helen Magnus business

Particulars Formula 2018 2017

Net profit margin Net income / sales 6.67% 15.00%

Rate of return on owner's

Equity Net income / Shareholders' Equity 8.33% 14.03%

5

business resulted will their decreasing in equity of owners capital. This term affects when

the owner take out cash for personal use and paying cash for an expense.

Interest Rates – interest rates changes the company profit secure or unsecured loans with

fixed or floating rates affect the operating activities of business. If there is higher rate of

interest in loans that mean directing affecting the business activities (Zeff, 2016).

D. Explaining the reasons why business owners would leave profits in the business rather than

withdrawing them for personal use:-

1. Better Return on Investment:- A higher rate of return on investment assisting the

owner to not withdrawing all money from business. A higher rate of return making the financial

structure strong. If business owners would leave the profit in the organization resulted company

financial and income statements shows a better growth (Accounting, 2018). It also promotes the

strategies to increase sales revenue for instance:- increase productivity of your staff, develop new

product lines, find new customers. If company face any type of financial crisis management can

use the owners' equity fund for the reducing the impact of the organization. More ownerships'

equity promotes the long term business strategies for expanding the operational areas.

Question 3

A) Calculation of financial ratios

Financial ratios of Helen Magnus business

Particulars Formula 2018 2017

Net profit margin Net income / sales 6.67% 15.00%

Rate of return on owner's

Equity Net income / Shareholders' Equity 8.33% 14.03%

5

Current ratio Current assets / Current Liabilities 5 6.58

Acid-test ratio Liquid assets / Current liabilities 1.33 3.83

Debt ratio Total debt / Total assets 0.13 0

Inventory turnover period

Cost of sales / Average inventory *

12 29.65 28.36

Working notes

2017 2018

Sales 90000 135000

Cost of Sales 58500 94500

Gross profit 31500 40500

All other expenses 18000 31500

Net profit 13500 9000

Current assets 2017 2018

Cash 18000 -27000

6

Acid-test ratio Liquid assets / Current liabilities 1.33 3.83

Debt ratio Total debt / Total assets 0.13 0

Inventory turnover period

Cost of sales / Average inventory *

12 29.65 28.36

Working notes

2017 2018

Sales 90000 135000

Cost of Sales 58500 94500

Gross profit 31500 40500

All other expenses 18000 31500

Net profit 13500 9000

Current assets 2017 2018

Cash 18000 -27000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

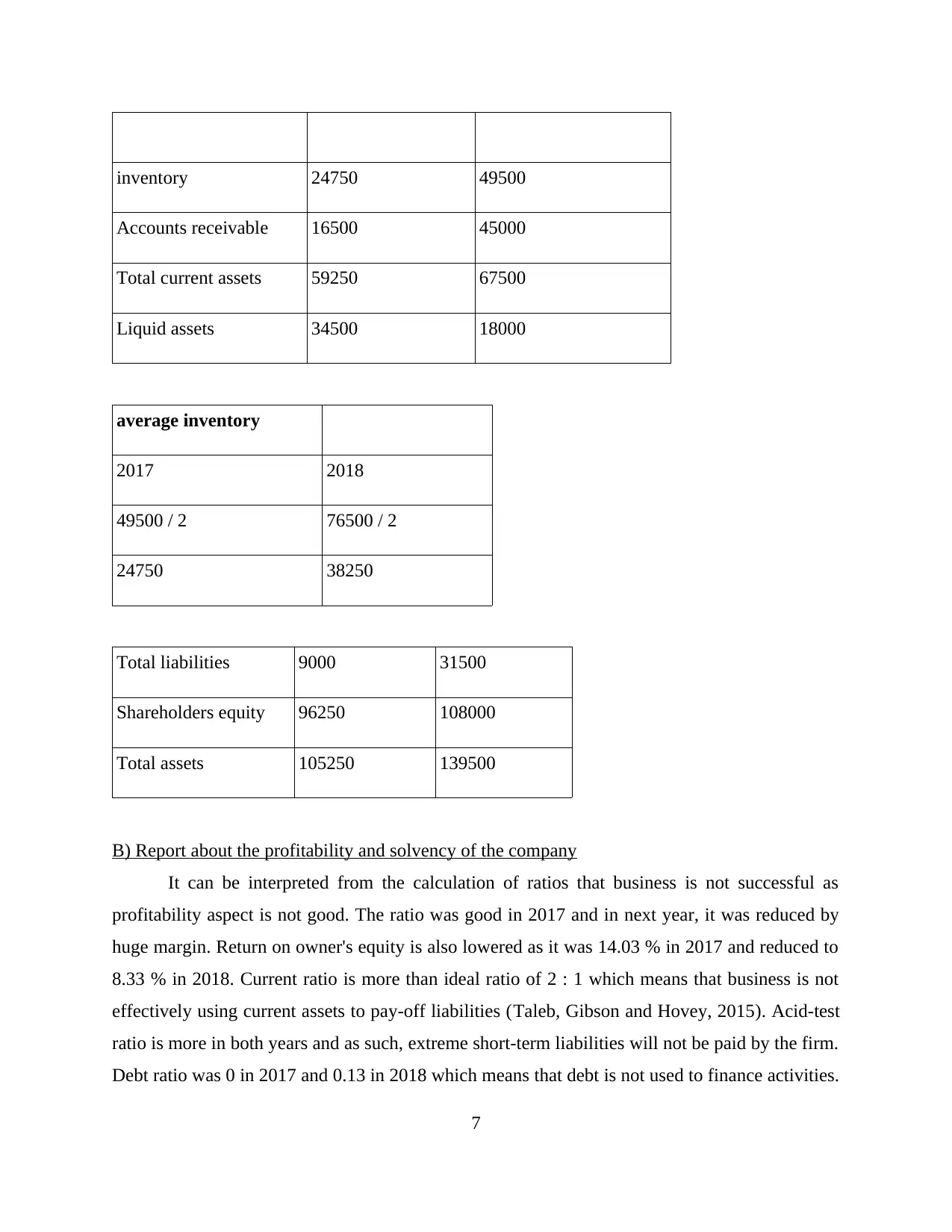

inventory 24750 49500

Accounts receivable 16500 45000

Total current assets 59250 67500

Liquid assets 34500 18000

average inventory

2017 2018

49500 / 2 76500 / 2

24750 38250

Total liabilities 9000 31500

Shareholders equity 96250 108000

Total assets 105250 139500

B) Report about the profitability and solvency of the company

It can be interpreted from the calculation of ratios that business is not successful as

profitability aspect is not good. The ratio was good in 2017 and in next year, it was reduced by

huge margin. Return on owner's equity is also lowered as it was 14.03 % in 2017 and reduced to

8.33 % in 2018. Current ratio is more than ideal ratio of 2 : 1 which means that business is not

effectively using current assets to pay-off liabilities (Taleb, Gibson and Hovey, 2015). Acid-test

ratio is more in both years and as such, extreme short-term liabilities will not be paid by the firm.

Debt ratio was 0 in 2017 and 0.13 in 2018 which means that debt is not used to finance activities.

7

Accounts receivable 16500 45000

Total current assets 59250 67500

Liquid assets 34500 18000

average inventory

2017 2018

49500 / 2 76500 / 2

24750 38250

Total liabilities 9000 31500

Shareholders equity 96250 108000

Total assets 105250 139500

B) Report about the profitability and solvency of the company

It can be interpreted from the calculation of ratios that business is not successful as

profitability aspect is not good. The ratio was good in 2017 and in next year, it was reduced by

huge margin. Return on owner's equity is also lowered as it was 14.03 % in 2017 and reduced to

8.33 % in 2018. Current ratio is more than ideal ratio of 2 : 1 which means that business is not

effectively using current assets to pay-off liabilities (Taleb, Gibson and Hovey, 2015). Acid-test

ratio is more in both years and as such, extreme short-term liabilities will not be paid by the firm.

Debt ratio was 0 in 2017 and 0.13 in 2018 which means that debt is not used to finance activities.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory turnover period was 28 days in previous year but increased to 29 days which means

that to stock is not quickly replenish to achieve sales. Thus, financial performance of the

business is not good.

Question 4

A) Computation of variable cost per glass

The variable costs consist of raw material of 2, machine operator labour of 15 hours and

transport and distribution of 1. Total per unit variable cost is 3

B) Contribution per margin

Formula of Contribution per margin = Selling price per unit – Variable cost per unit

= 5 – 3

= 2

C) Break-even output

Break-even output = N / P - V

Where N is Number of units sold, P = Price per unit, V = Variable cost per unit

= 0 / 3.5 – 2.03

= 0 /1.47

= 0

D) Acceptance of order

The order should not be accepted by the Glassy Ltd as per unit cost is 3.50 of wine glass.

If 1000 special order is received, cost per unit is 1.80. On the other hand, deducting transport

expenses, total cost comes out to 2.5. Thus, original cost – special order cost = 2.5 – 1.80 = 0.7

which means there is a loss of 0.7 on per unit of wine glass. Thus, it should not be accepted.

E) Conclusion

The order can be received when normal price of 3.50 or more than that is provided to

make 1000 wine glasses as profit would increase.

F) Calculation of Profit and Loss

The profit on wine glasses = 2000 * 3.5 = 7000 and on champagne glasses = 600 * 5 =

3000

8

that to stock is not quickly replenish to achieve sales. Thus, financial performance of the

business is not good.

Question 4

A) Computation of variable cost per glass

The variable costs consist of raw material of 2, machine operator labour of 15 hours and

transport and distribution of 1. Total per unit variable cost is 3

B) Contribution per margin

Formula of Contribution per margin = Selling price per unit – Variable cost per unit

= 5 – 3

= 2

C) Break-even output

Break-even output = N / P - V

Where N is Number of units sold, P = Price per unit, V = Variable cost per unit

= 0 / 3.5 – 2.03

= 0 /1.47

= 0

D) Acceptance of order

The order should not be accepted by the Glassy Ltd as per unit cost is 3.50 of wine glass.

If 1000 special order is received, cost per unit is 1.80. On the other hand, deducting transport

expenses, total cost comes out to 2.5. Thus, original cost – special order cost = 2.5 – 1.80 = 0.7

which means there is a loss of 0.7 on per unit of wine glass. Thus, it should not be accepted.

E) Conclusion

The order can be received when normal price of 3.50 or more than that is provided to

make 1000 wine glasses as profit would increase.

F) Calculation of Profit and Loss

The profit on wine glasses = 2000 * 3.5 = 7000 and on champagne glasses = 600 * 5 =

3000

8

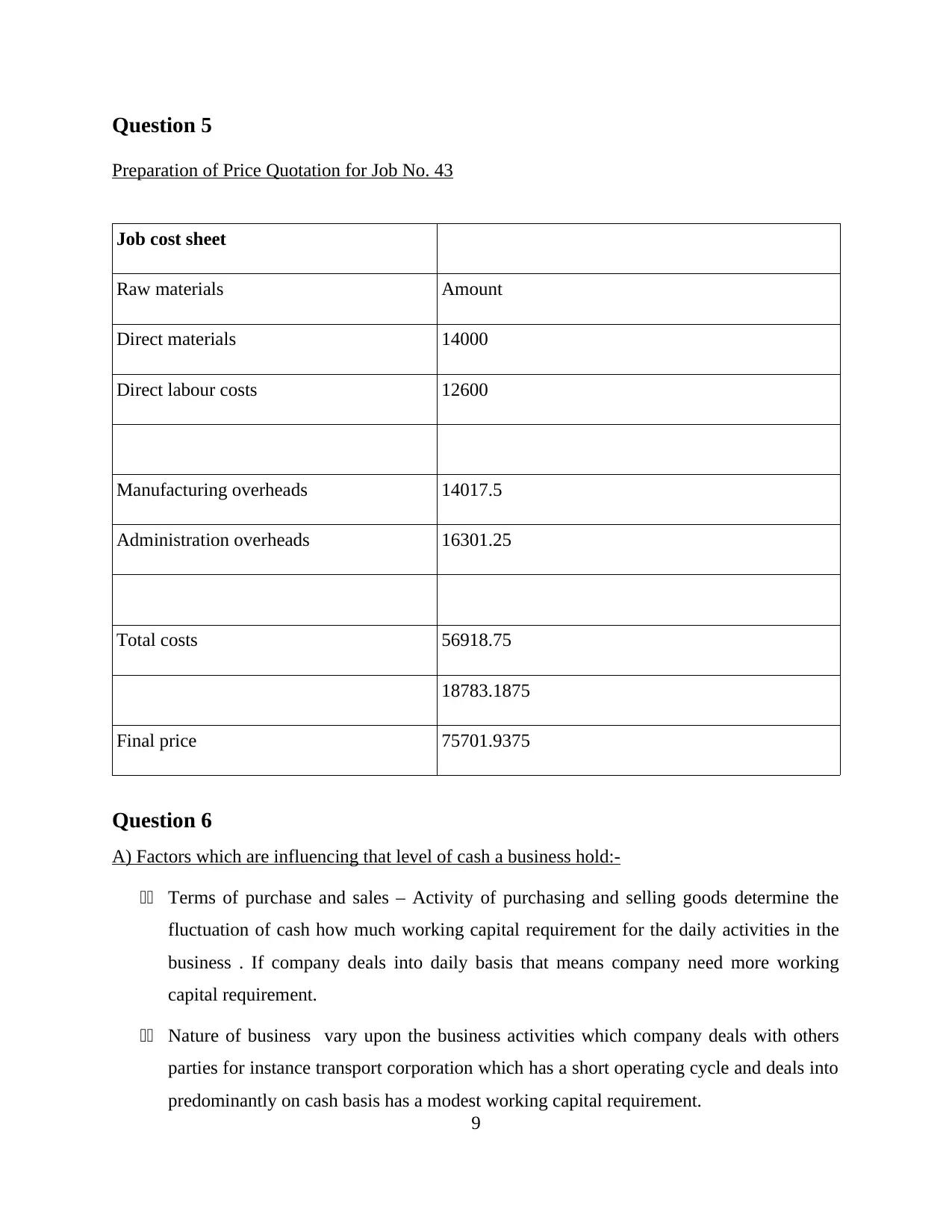

Question 5

Preparation of Price Quotation for Job No. 43

Job cost sheet

Raw materials Amount

Direct materials 14000

Direct labour costs 12600

Manufacturing overheads 14017.5

Administration overheads 16301.25

Total costs 56918.75

18783.1875

Final price 75701.9375

Question 6

A) Factors which are influencing that level of cash a business hold:-

11 Terms of purchase and sales – Activity of purchasing and selling goods determine the

fluctuation of cash how much working capital requirement for the daily activities in the

business . If company deals into daily basis that means company need more working

capital requirement.

11 Nature of business vary upon the business activities which company deals with others

parties for instance transport corporation which has a short operating cycle and deals into

predominantly on cash basis has a modest working capital requirement.

9

Preparation of Price Quotation for Job No. 43

Job cost sheet

Raw materials Amount

Direct materials 14000

Direct labour costs 12600

Manufacturing overheads 14017.5

Administration overheads 16301.25

Total costs 56918.75

18783.1875

Final price 75701.9375

Question 6

A) Factors which are influencing that level of cash a business hold:-

11 Terms of purchase and sales – Activity of purchasing and selling goods determine the

fluctuation of cash how much working capital requirement for the daily activities in the

business . If company deals into daily basis that means company need more working

capital requirement.

11 Nature of business vary upon the business activities which company deals with others

parties for instance transport corporation which has a short operating cycle and deals into

predominantly on cash basis has a modest working capital requirement.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.