Project Report: Managing Financial Performance of Unilever PLC

VerifiedAdded on 2020/04/21

|23

|8093

|142

Project

AI Summary

This project report provides a comprehensive analysis of Unilever PLC's financial performance. It begins with an introduction to financial performance measurement, emphasizing the importance of both financial and non-financial factors. The report then delves into a detailed ratio analysis of Unilever PLC, comparing its performance to competitors like PepsiCo, and evaluating metrics such as return on capital employed, gross profit margin, operating profit margin, gearing ratios, and interest coverage. The report also includes a peer review, comparing Unilever's market position and financial health with its competitors. Further, the report explores the impact of budgetary techniques using Capital Land plc as a case study and evaluates the significance of performance measurement techniques. Finally, the report addresses key issues related to significant expenditure decisions, offering insights into strategic financial management. The project incorporates financial statements, macroeconomic factors, and competitive analysis to provide a holistic understanding of Unilever's financial standing.

Running Head: Managing Financial Performance

1

Project Report: Managing Financial Performance

1

Project Report: Managing Financial Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing Financial Performance 2

Contents

Introduction.......................................................................................................................3

Financial performance of Unilever plc.............................................................................4

Ratio analysis................................................................................................................4

Peer review...................................................................................................................5

Budgetary techniques........................................................................................................7

Performance Measurement techniques...........................................................................11

Key issues related to significant expenditure.................................................................15

Conclusion......................................................................................................................17

References.......................................................................................................................19

Contents

Introduction.......................................................................................................................3

Financial performance of Unilever plc.............................................................................4

Ratio analysis................................................................................................................4

Peer review...................................................................................................................5

Budgetary techniques........................................................................................................7

Performance Measurement techniques...........................................................................11

Key issues related to significant expenditure.................................................................15

Conclusion......................................................................................................................17

References.......................................................................................................................19

Managing Financial Performance 3

Introduction:

Financial performance of a company depends over various financial factors as well as

non financial factors of the company. It becomes mandatory for every investors as well as

chief financial officer of the company to evaluate and analyze the performance and the

position of the company to make various decisions in a better way. Measurement of financial

performance of an organization could be done through conducting various studies and

methods such as the financial performance of a company could be evaluated through

conducting the study of ratio analysis or the budgetary reports could also assist the

organization to identify the changes into the financial position. Further various other methods

such as variance analysis, measurement techniques, better strategies of the company,

competitor position of the company, market position of the company, changes in the industry,

economical position, financial boom or crisis etc also make an impact over the financial

position of a company.

In the given report, various methods of measuring the financial performance has been

evaluated and for each study, different companies have been taken into the concern and the

performance evaluation and analysis study has been done over those companies so that the

better understanding could be enhanced over the performance and financial measurement

techniques. Firstly, the study of ratio analysis has been done over the Unilever Plc to analyze

that how the company is performing in terms of finance in the company. For this study,

various competitors of the company have been analyzed so that a better conclusion could be

given. Financial statement of the company has been analyzed for this study as well as the

macro economical factors have also been taken into the context to evaluate the position of the

company into the economy.

In addition, study has been performed over the budgetary techniques and their

importance in an international company which is Capital Land plc. This study depicts that

how the budgetary techniques make an impact over the financial position of the company.

Through this study, it has been evaluated that how the budgetary techniques affect the

operational performance of a company. It depict that the better the budgetary techniques and

their implementation would be in an organization, the better the position of the company

could be evaluated and better strategy could be made.

More, the study has been performed over the performance measurement techniques

and their impact over the position and the performance of the company. Through these

Introduction:

Financial performance of a company depends over various financial factors as well as

non financial factors of the company. It becomes mandatory for every investors as well as

chief financial officer of the company to evaluate and analyze the performance and the

position of the company to make various decisions in a better way. Measurement of financial

performance of an organization could be done through conducting various studies and

methods such as the financial performance of a company could be evaluated through

conducting the study of ratio analysis or the budgetary reports could also assist the

organization to identify the changes into the financial position. Further various other methods

such as variance analysis, measurement techniques, better strategies of the company,

competitor position of the company, market position of the company, changes in the industry,

economical position, financial boom or crisis etc also make an impact over the financial

position of a company.

In the given report, various methods of measuring the financial performance has been

evaluated and for each study, different companies have been taken into the concern and the

performance evaluation and analysis study has been done over those companies so that the

better understanding could be enhanced over the performance and financial measurement

techniques. Firstly, the study of ratio analysis has been done over the Unilever Plc to analyze

that how the company is performing in terms of finance in the company. For this study,

various competitors of the company have been analyzed so that a better conclusion could be

given. Financial statement of the company has been analyzed for this study as well as the

macro economical factors have also been taken into the context to evaluate the position of the

company into the economy.

In addition, study has been performed over the budgetary techniques and their

importance in an international company which is Capital Land plc. This study depicts that

how the budgetary techniques make an impact over the financial position of the company.

Through this study, it has been evaluated that how the budgetary techniques affect the

operational performance of a company. It depict that the better the budgetary techniques and

their implementation would be in an organization, the better the position of the company

could be evaluated and better strategy could be made.

More, the study has been performed over the performance measurement techniques

and their impact over the position and the performance of the company. Through these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing Financial Performance 4

techniques, it has been found that how the performance of an organization could be evaluated

and the environment of the organization could be impacted. Lastly, it has been evaluated that

how an organization taka a decision about spending some expenditure over diversification of

the organization or some other investment proposal.

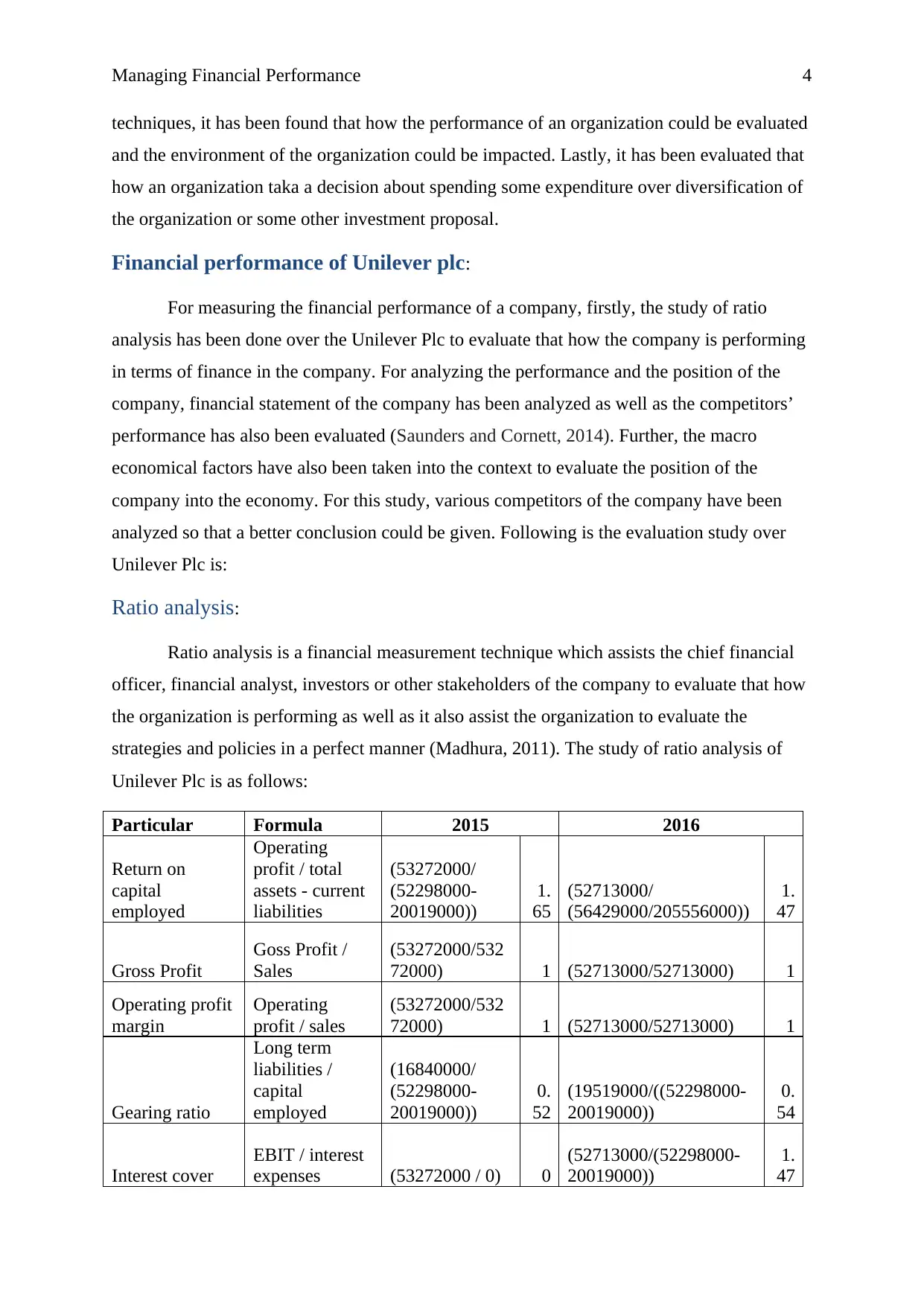

Financial performance of Unilever plc:

For measuring the financial performance of a company, firstly, the study of ratio

analysis has been done over the Unilever Plc to evaluate that how the company is performing

in terms of finance in the company. For analyzing the performance and the position of the

company, financial statement of the company has been analyzed as well as the competitors’

performance has also been evaluated (Saunders and Cornett, 2014). Further, the macro

economical factors have also been taken into the context to evaluate the position of the

company into the economy. For this study, various competitors of the company have been

analyzed so that a better conclusion could be given. Following is the evaluation study over

Unilever Plc is:

Ratio analysis:

Ratio analysis is a financial measurement technique which assists the chief financial

officer, financial analyst, investors or other stakeholders of the company to evaluate that how

the organization is performing as well as it also assist the organization to evaluate the

strategies and policies in a perfect manner (Madhura, 2011). The study of ratio analysis of

Unilever Plc is as follows:

Particular Formula 2015 2016

Return on

capital

employed

Operating

profit / total

assets - current

liabilities

(53272000/

(52298000-

20019000))

1.

65

(52713000/

(56429000/205556000))

1.

47

Gross Profit

Goss Profit /

Sales

(53272000/532

72000) 1 (52713000/52713000) 1

Operating profit

margin

Operating

profit / sales

(53272000/532

72000) 1 (52713000/52713000) 1

Gearing ratio

Long term

liabilities /

capital

employed

(16840000/

(52298000-

20019000))

0.

52

(19519000/((52298000-

20019000))

0.

54

Interest cover

EBIT / interest

expenses (53272000 / 0) 0

(52713000/(52298000-

20019000))

1.

47

techniques, it has been found that how the performance of an organization could be evaluated

and the environment of the organization could be impacted. Lastly, it has been evaluated that

how an organization taka a decision about spending some expenditure over diversification of

the organization or some other investment proposal.

Financial performance of Unilever plc:

For measuring the financial performance of a company, firstly, the study of ratio

analysis has been done over the Unilever Plc to evaluate that how the company is performing

in terms of finance in the company. For analyzing the performance and the position of the

company, financial statement of the company has been analyzed as well as the competitors’

performance has also been evaluated (Saunders and Cornett, 2014). Further, the macro

economical factors have also been taken into the context to evaluate the position of the

company into the economy. For this study, various competitors of the company have been

analyzed so that a better conclusion could be given. Following is the evaluation study over

Unilever Plc is:

Ratio analysis:

Ratio analysis is a financial measurement technique which assists the chief financial

officer, financial analyst, investors or other stakeholders of the company to evaluate that how

the organization is performing as well as it also assist the organization to evaluate the

strategies and policies in a perfect manner (Madhura, 2011). The study of ratio analysis of

Unilever Plc is as follows:

Particular Formula 2015 2016

Return on

capital

employed

Operating

profit / total

assets - current

liabilities

(53272000/

(52298000-

20019000))

1.

65

(52713000/

(56429000/205556000))

1.

47

Gross Profit

Goss Profit /

Sales

(53272000/532

72000) 1 (52713000/52713000) 1

Operating profit

margin

Operating

profit / sales

(53272000/532

72000) 1 (52713000/52713000) 1

Gearing ratio

Long term

liabilities /

capital

employed

(16840000/

(52298000-

20019000))

0.

52

(19519000/((52298000-

20019000))

0.

54

Interest cover

EBIT / interest

expenses (53272000 / 0) 0

(52713000/(52298000-

20019000))

1.

47

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

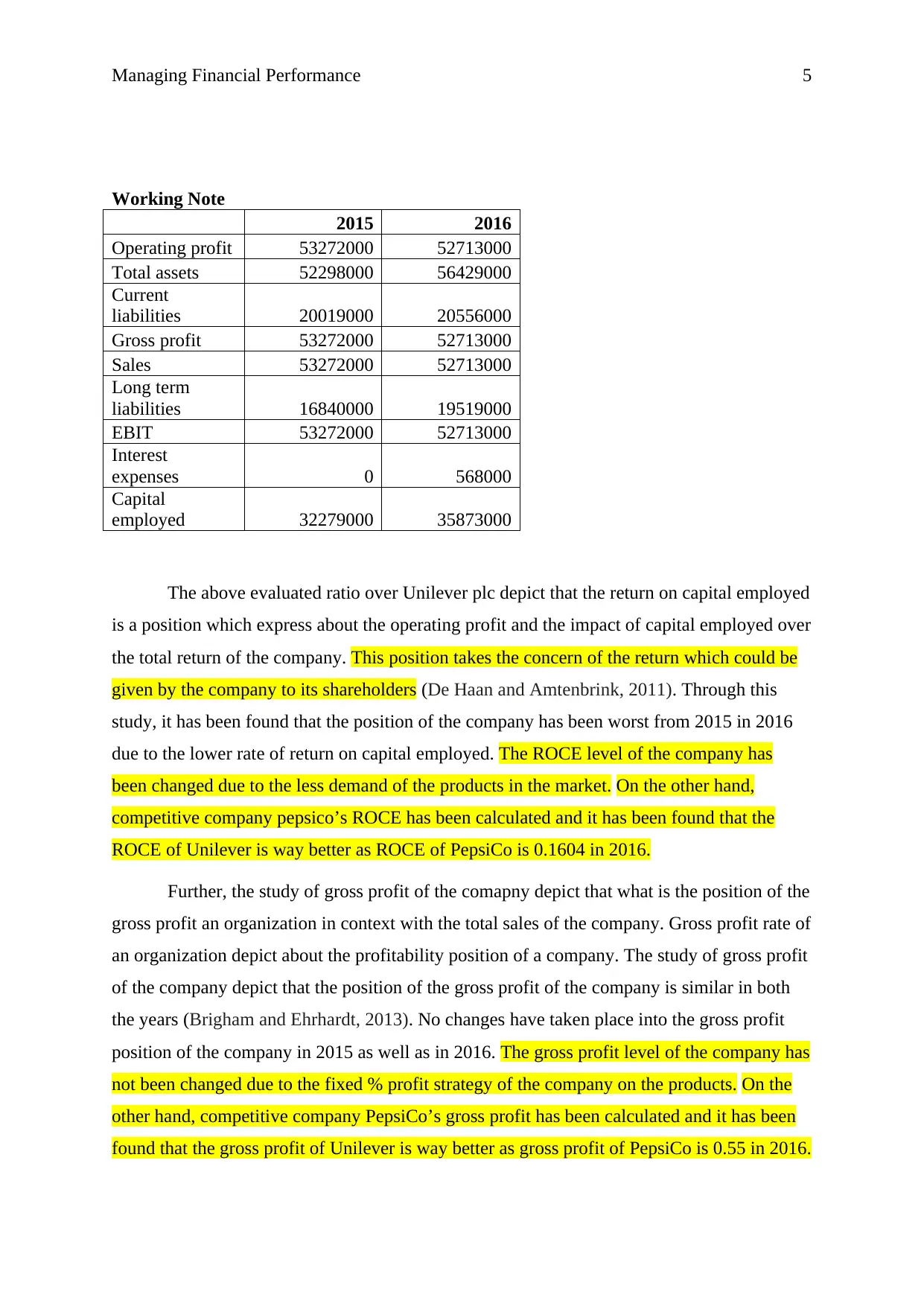

Managing Financial Performance 5

Working Note

2015 2016

Operating profit 53272000 52713000

Total assets 52298000 56429000

Current

liabilities 20019000 20556000

Gross profit 53272000 52713000

Sales 53272000 52713000

Long term

liabilities 16840000 19519000

EBIT 53272000 52713000

Interest

expenses 0 568000

Capital

employed 32279000 35873000

The above evaluated ratio over Unilever plc depict that the return on capital employed

is a position which express about the operating profit and the impact of capital employed over

the total return of the company. This position takes the concern of the return which could be

given by the company to its shareholders (De Haan and Amtenbrink, 2011). Through this

study, it has been found that the position of the company has been worst from 2015 in 2016

due to the lower rate of return on capital employed. The ROCE level of the company has

been changed due to the less demand of the products in the market. On the other hand,

competitive company pepsico’s ROCE has been calculated and it has been found that the

ROCE of Unilever is way better as ROCE of PepsiCo is 0.1604 in 2016.

Further, the study of gross profit of the comapny depict that what is the position of the

gross profit an organization in context with the total sales of the company. Gross profit rate of

an organization depict about the profitability position of a company. The study of gross profit

of the company depict that the position of the gross profit of the company is similar in both

the years (Brigham and Ehrhardt, 2013). No changes have taken place into the gross profit

position of the company in 2015 as well as in 2016. The gross profit level of the company has

not been changed due to the fixed % profit strategy of the company on the products. On the

other hand, competitive company PepsiCo’s gross profit has been calculated and it has been

found that the gross profit of Unilever is way better as gross profit of PepsiCo is 0.55 in 2016.

Working Note

2015 2016

Operating profit 53272000 52713000

Total assets 52298000 56429000

Current

liabilities 20019000 20556000

Gross profit 53272000 52713000

Sales 53272000 52713000

Long term

liabilities 16840000 19519000

EBIT 53272000 52713000

Interest

expenses 0 568000

Capital

employed 32279000 35873000

The above evaluated ratio over Unilever plc depict that the return on capital employed

is a position which express about the operating profit and the impact of capital employed over

the total return of the company. This position takes the concern of the return which could be

given by the company to its shareholders (De Haan and Amtenbrink, 2011). Through this

study, it has been found that the position of the company has been worst from 2015 in 2016

due to the lower rate of return on capital employed. The ROCE level of the company has

been changed due to the less demand of the products in the market. On the other hand,

competitive company pepsico’s ROCE has been calculated and it has been found that the

ROCE of Unilever is way better as ROCE of PepsiCo is 0.1604 in 2016.

Further, the study of gross profit of the comapny depict that what is the position of the

gross profit an organization in context with the total sales of the company. Gross profit rate of

an organization depict about the profitability position of a company. The study of gross profit

of the company depict that the position of the gross profit of the company is similar in both

the years (Brigham and Ehrhardt, 2013). No changes have taken place into the gross profit

position of the company in 2015 as well as in 2016. The gross profit level of the company has

not been changed due to the fixed % profit strategy of the company on the products. On the

other hand, competitive company PepsiCo’s gross profit has been calculated and it has been

found that the gross profit of Unilever is way better as gross profit of PepsiCo is 0.55 in 2016.

Managing Financial Performance 6

More, the study of operating profit margin of the comapny depict that what is the

position of the operating profit an organization in context with the total sales of the company.

Operating profit rate of an organization depict about the profitability position of a company.

The study of operating profit of the company depict that the position of the operating profit of

the company is similar in both the years. No changes have taken place into the operating

profit position of the company in 2015 as well as in 2016.

Further, the position of gearing ratios of the company has been evaluated. This study

of gearing ratios depict about the position of the capital employed on the basis of the capital

employed of the company (Weygandt, Kimmel and Kieso, 2015). This depict that what is the

position of the long term liabilities in the context of the capital employed of the company.

Through this study, it has been found that the position of the company has been better from

2015 in 2016 due to the higher rate of return on capital employed. The operating profit level

of the company has not been changed due to the fixed % profit strategy of the company on

the products. On the other hand, competitive company PepsiCo’s operating profit has been

calculated and it has been found that the operating profit of Unilever is way better as

operating profit of PepsiCo is 0.1325 in 2016.

Further, the position of interest coverage of the company has been evaluated. This

study of interest coverage depicts about the position of the EBIT on the basis of the interest

expenses of the company. This depict that what is the position of the interest in the context of

the total profit of the company (Von Hagen and Harden, 2014). Through this study, it has

been found that the position of the company depict about the higher expenditure from 2015 in

2016 due to the higher rate of interest in 2016. On the other hand, competitive company

PepsiCo’s interest coverage ratio has been calculated and it has been found that the interest

coverage ratio of PepsiCo is way better as interest coverage ratio of PepsiCo is 8.61 in 2016.

Peer review:

Further, the competitor of the company has been analyzed to identify the position of

the company in the market and the performance of the company in comparison of its

competitors. And the macro economical factors of the company have also been analyzed to

identify the position of the economy and its impact over the performance and the position of

the company (Stevenson and Sum, 2002). Through the competitor and peer analysis, it has

been found that the position of the Unilever plc is much better in comparison of the

competitors. The main competitor of the Unilever plc is PepsiCo Limited. This depict that the

More, the study of operating profit margin of the comapny depict that what is the

position of the operating profit an organization in context with the total sales of the company.

Operating profit rate of an organization depict about the profitability position of a company.

The study of operating profit of the company depict that the position of the operating profit of

the company is similar in both the years. No changes have taken place into the operating

profit position of the company in 2015 as well as in 2016.

Further, the position of gearing ratios of the company has been evaluated. This study

of gearing ratios depict about the position of the capital employed on the basis of the capital

employed of the company (Weygandt, Kimmel and Kieso, 2015). This depict that what is the

position of the long term liabilities in the context of the capital employed of the company.

Through this study, it has been found that the position of the company has been better from

2015 in 2016 due to the higher rate of return on capital employed. The operating profit level

of the company has not been changed due to the fixed % profit strategy of the company on

the products. On the other hand, competitive company PepsiCo’s operating profit has been

calculated and it has been found that the operating profit of Unilever is way better as

operating profit of PepsiCo is 0.1325 in 2016.

Further, the position of interest coverage of the company has been evaluated. This

study of interest coverage depicts about the position of the EBIT on the basis of the interest

expenses of the company. This depict that what is the position of the interest in the context of

the total profit of the company (Von Hagen and Harden, 2014). Through this study, it has

been found that the position of the company depict about the higher expenditure from 2015 in

2016 due to the higher rate of interest in 2016. On the other hand, competitive company

PepsiCo’s interest coverage ratio has been calculated and it has been found that the interest

coverage ratio of PepsiCo is way better as interest coverage ratio of PepsiCo is 8.61 in 2016.

Peer review:

Further, the competitor of the company has been analyzed to identify the position of

the company in the market and the performance of the company in comparison of its

competitors. And the macro economical factors of the company have also been analyzed to

identify the position of the economy and its impact over the performance and the position of

the company (Stevenson and Sum, 2002). Through the competitor and peer analysis, it has

been found that the position of the Unilever plc is much better in comparison of the

competitors. The main competitor of the Unilever plc is PepsiCo Limited. This depict that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing Financial Performance 7

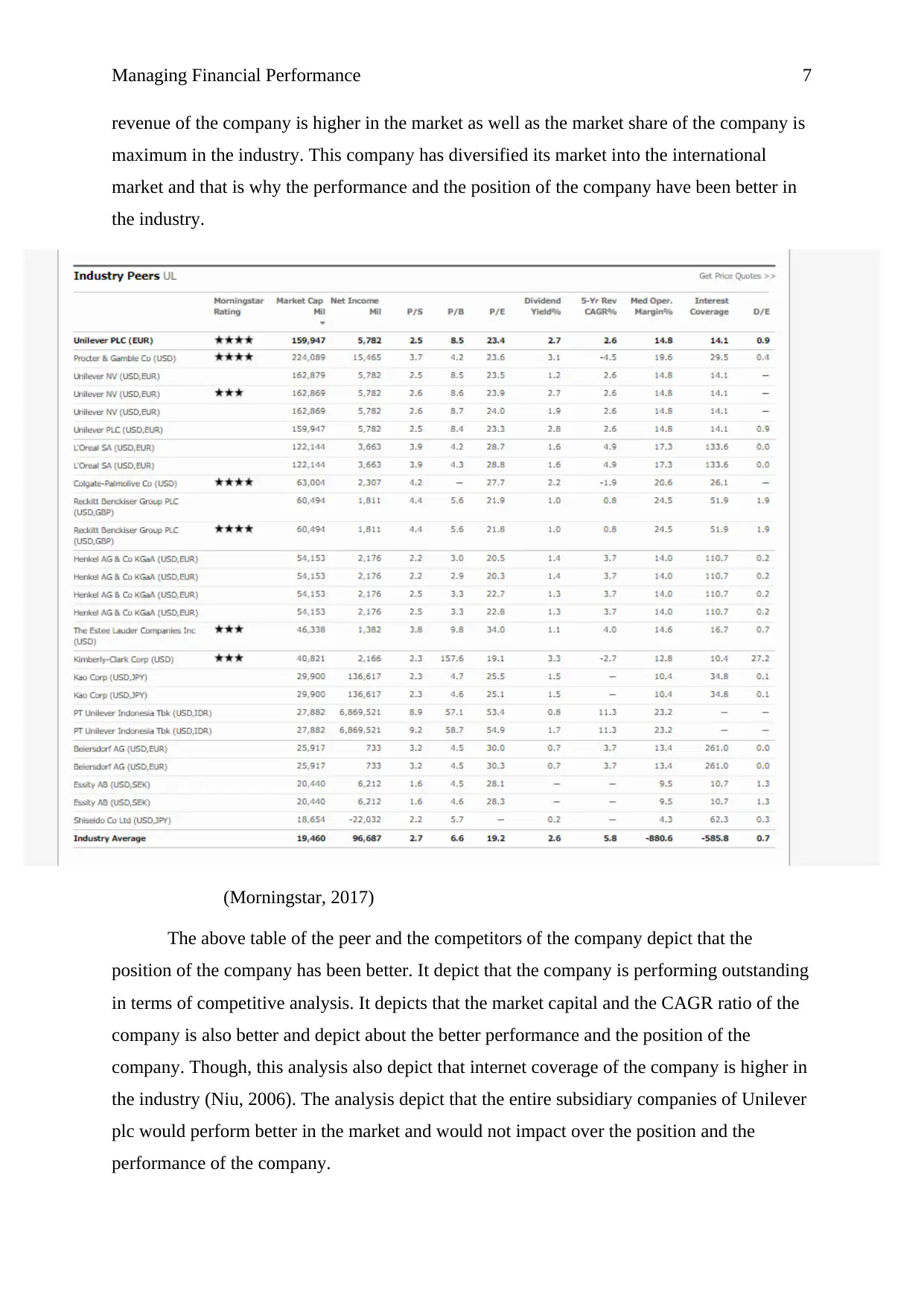

revenue of the company is higher in the market as well as the market share of the company is

maximum in the industry. This company has diversified its market into the international

market and that is why the performance and the position of the company have been better in

the industry.

(Morningstar, 2017)

The above table of the peer and the competitors of the company depict that the

position of the company has been better. It depict that the company is performing outstanding

in terms of competitive analysis. It depicts that the market capital and the CAGR ratio of the

company is also better and depict about the better performance and the position of the

company. Though, this analysis also depict that internet coverage of the company is higher in

the industry (Niu, 2006). The analysis depict that the entire subsidiary companies of Unilever

plc would perform better in the market and would not impact over the position and the

performance of the company.

revenue of the company is higher in the market as well as the market share of the company is

maximum in the industry. This company has diversified its market into the international

market and that is why the performance and the position of the company have been better in

the industry.

(Morningstar, 2017)

The above table of the peer and the competitors of the company depict that the

position of the company has been better. It depict that the company is performing outstanding

in terms of competitive analysis. It depicts that the market capital and the CAGR ratio of the

company is also better and depict about the better performance and the position of the

company. Though, this analysis also depict that internet coverage of the company is higher in

the industry (Niu, 2006). The analysis depict that the entire subsidiary companies of Unilever

plc would perform better in the market and would not impact over the position and the

performance of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing Financial Performance 8

The macro economical factors of the country depict about the various changes into the

industry in last few years which has affected the position and the profitability state of the

company. Through this analysis, it has been observed that currently, the entire international

market is suffering with the huge loss. Investors have divested their amount from the

industries and the market and thus the liquid position of the companies have been affected

and it has also affected the operations of the company. Further, the government interference

of the company has also been evaluated and it has been found that the government do not

interact more into the FMCG industry of the country (Juan García-Teruel and Martinez-

Solano, 2007). The operations and the functions of the company are evaluated according to

the industry regulations.

Further, the environmental aspect of the company has also been evaluated to identify

and analyze that how the environment and the society is impacted over the position,

performance and stability of the organization. Through the evaluation, it has been found that

the environmental factor of the economy is according to the functions of the company and do

not affect the operations of the company and lastly, the corporate governance policies of the

company has also been evaluated to identify the performance and the position of the company

in the society and it has been found that the company has planned various CSR programmes

to evaluate the performance of the company in terms of managing the social responsibility

(Horngren, 2009).

Thus, through this study, it has been found that the position and the performance of

the Unilever plc in terms of financial and non financial factor of the company is better than

any other company in the industry.

Budgetary techniques:

For measuring the financial performance of a company, secondly, the study of

budgetary techniques has been done over the capital land plc to evaluate that how the

company is performing in terms of finance in the company. In addition, study has been

performed over the budgetary techniques and their importance in Capital land plc. This study

depicts that how the budgetary techniques make an impact over the financial position of the

company. Through this study, it has been evaluated that how the budgetary techniques affect

the operational performance of a company. It depict that the better the budgetary techniques

and their implementation would be in an organization, the better the position of the company

could be evaluated and better strategy could be made (Hogarth and Makridakis, 2011).

The macro economical factors of the country depict about the various changes into the

industry in last few years which has affected the position and the profitability state of the

company. Through this analysis, it has been observed that currently, the entire international

market is suffering with the huge loss. Investors have divested their amount from the

industries and the market and thus the liquid position of the companies have been affected

and it has also affected the operations of the company. Further, the government interference

of the company has also been evaluated and it has been found that the government do not

interact more into the FMCG industry of the country (Juan García-Teruel and Martinez-

Solano, 2007). The operations and the functions of the company are evaluated according to

the industry regulations.

Further, the environmental aspect of the company has also been evaluated to identify

and analyze that how the environment and the society is impacted over the position,

performance and stability of the organization. Through the evaluation, it has been found that

the environmental factor of the economy is according to the functions of the company and do

not affect the operations of the company and lastly, the corporate governance policies of the

company has also been evaluated to identify the performance and the position of the company

in the society and it has been found that the company has planned various CSR programmes

to evaluate the performance of the company in terms of managing the social responsibility

(Horngren, 2009).

Thus, through this study, it has been found that the position and the performance of

the Unilever plc in terms of financial and non financial factor of the company is better than

any other company in the industry.

Budgetary techniques:

For measuring the financial performance of a company, secondly, the study of

budgetary techniques has been done over the capital land plc to evaluate that how the

company is performing in terms of finance in the company. In addition, study has been

performed over the budgetary techniques and their importance in Capital land plc. This study

depicts that how the budgetary techniques make an impact over the financial position of the

company. Through this study, it has been evaluated that how the budgetary techniques affect

the operational performance of a company. It depict that the better the budgetary techniques

and their implementation would be in an organization, the better the position of the company

could be evaluated and better strategy could be made (Hogarth and Makridakis, 2011).

Managing Financial Performance 9

Capital land plc is operating is business into the international market. This

organization is one of the largest organizations in real estate industry. Various strategies and

policies of this company have helped the organization to enhance the business and make the

organization’s performance better. Further, the financial and non financial, both the factors of

the company are depicting about the positive performance of the company. In this report,

study has been performed over the budgetary techniques and its impact over the financial

position of the company (Graham, Harvey and Puri, 2013).

The budgetary techniques are of many types and it affects and manages the position

and performance of the company in various ways. These techniques depict that an

organization must be very caution while evaluating and identifying the best budgetary

techniques and its implementation over the organization. The best budgetary techniques of an

international company assist the Capital Land plc in managing the financial performance of

its manufacturing department as follows:

Forecast the future sales:

It is quite tough for an organization to evaluate and identify the future of the business.

For forecasting the changes and the performance of the company in the future, company

could use the budgetary technique. Budgetary techniques help the Capital Land Plc in

identifying the market position and the prediction about the future which helps the

organization to make various better decisions about the performance and the sales of the

company. Budgetary techniques take the concern of historical data and the prediction about

the future and on the basis of those figures and information, future sales of the capital land

plc is evaluated by the management of the company so that the goods could be manufactured

by the manufacturing management accordingly (Garrison, Noreen, Brewer and McGowan,

2010).

Forecast the future consumption:

At the same time, it is quite tough for an organization to evaluate and identify the

future expenses and the changes of the business. For forecasting the changes and the

performance of the company in the future, company could take the help of various methods

so that the budgetary reports could be prepared. Budgetary techniques help the Capital Land

Plc in identifying the customers’ needs and the demand through communicating the same

with the marketing team of the organization. The information from marketing department

would help the organization to make various better decisions about the performance and the

Capital land plc is operating is business into the international market. This

organization is one of the largest organizations in real estate industry. Various strategies and

policies of this company have helped the organization to enhance the business and make the

organization’s performance better. Further, the financial and non financial, both the factors of

the company are depicting about the positive performance of the company. In this report,

study has been performed over the budgetary techniques and its impact over the financial

position of the company (Graham, Harvey and Puri, 2013).

The budgetary techniques are of many types and it affects and manages the position

and performance of the company in various ways. These techniques depict that an

organization must be very caution while evaluating and identifying the best budgetary

techniques and its implementation over the organization. The best budgetary techniques of an

international company assist the Capital Land plc in managing the financial performance of

its manufacturing department as follows:

Forecast the future sales:

It is quite tough for an organization to evaluate and identify the future of the business.

For forecasting the changes and the performance of the company in the future, company

could use the budgetary technique. Budgetary techniques help the Capital Land Plc in

identifying the market position and the prediction about the future which helps the

organization to make various better decisions about the performance and the sales of the

company. Budgetary techniques take the concern of historical data and the prediction about

the future and on the basis of those figures and information, future sales of the capital land

plc is evaluated by the management of the company so that the goods could be manufactured

by the manufacturing management accordingly (Garrison, Noreen, Brewer and McGowan,

2010).

Forecast the future consumption:

At the same time, it is quite tough for an organization to evaluate and identify the

future expenses and the changes of the business. For forecasting the changes and the

performance of the company in the future, company could take the help of various methods

so that the budgetary reports could be prepared. Budgetary techniques help the Capital Land

Plc in identifying the customers’ needs and the demand through communicating the same

with the marketing team of the organization. The information from marketing department

would help the organization to make various better decisions about the performance and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing Financial Performance 10

total consumption of the company. Budgetary techniques take the concern of various non

financial information and financial data to forecast the future consumption of the capital land

plc so that the goods could be manufactured by the manufacturing management accordingly.

Capacity of the machineries:

Further, Capital Land Plc finds it tough to identify the total capacity of the

machineries. This problem could be resolved through communicating the same with the

technical team of the organization. The information from technical department helps the

organization to make various better decisions about the performance and the total

manufacturing capacity of the company. Budgetary techniques take the concern of non

financial information and financial data to forecast the machineries capacity of the capital

land plc so that the goods could be manufactured by the manufacturing management

accordingly (Faleti and Myrick, 2012).

A tool for decision making:

Capital land plc makes various decisions about the performance and the position of

the company on the basis of budgetary reports. In this issue, Budgetary techniques help the

Capital Land Plc in identifying the various non financial information and financial data to

forecast the performance and the total profitability position of the company. The information

from budgetary techniques helps the organization to make various better decisions about the

total goods which is manufactured by the manufacturing management of the capital land plc.

Monitor business performance:

More, it has been evaluated that monitoring the business performance of the company

is a tough task. Budgetary techniques help the Capital Land Plc in identifying the

performance of the company through identifying the various non financial information and

financial data. This technique monitors all the related aspect through conducting the various

studies over entire related factors and thus it becomes easy for the analyst and the

manufacturing manager of the company to monitor the business performance (Weygandt,

Kimmel and Kieso, 2015). Variance analysis study is the most used technique to identify the

performance of the company and the position of the company in the market.

Generates the sense of care:

More, budgetary techniques help the Capital Land Plc and its managers to identify

and evaluate all the related factors and their responsibilities. This technique helps the line

total consumption of the company. Budgetary techniques take the concern of various non

financial information and financial data to forecast the future consumption of the capital land

plc so that the goods could be manufactured by the manufacturing management accordingly.

Capacity of the machineries:

Further, Capital Land Plc finds it tough to identify the total capacity of the

machineries. This problem could be resolved through communicating the same with the

technical team of the organization. The information from technical department helps the

organization to make various better decisions about the performance and the total

manufacturing capacity of the company. Budgetary techniques take the concern of non

financial information and financial data to forecast the machineries capacity of the capital

land plc so that the goods could be manufactured by the manufacturing management

accordingly (Faleti and Myrick, 2012).

A tool for decision making:

Capital land plc makes various decisions about the performance and the position of

the company on the basis of budgetary reports. In this issue, Budgetary techniques help the

Capital Land Plc in identifying the various non financial information and financial data to

forecast the performance and the total profitability position of the company. The information

from budgetary techniques helps the organization to make various better decisions about the

total goods which is manufactured by the manufacturing management of the capital land plc.

Monitor business performance:

More, it has been evaluated that monitoring the business performance of the company

is a tough task. Budgetary techniques help the Capital Land Plc in identifying the

performance of the company through identifying the various non financial information and

financial data. This technique monitors all the related aspect through conducting the various

studies over entire related factors and thus it becomes easy for the analyst and the

manufacturing manager of the company to monitor the business performance (Weygandt,

Kimmel and Kieso, 2015). Variance analysis study is the most used technique to identify the

performance of the company and the position of the company in the market.

Generates the sense of care:

More, budgetary techniques help the Capital Land Plc and its managers to identify

and evaluate all the related factors and their responsibilities. This technique helps the line

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing Financial Performance 11

managers and middle level manager to generate and enhance the sense of caution and care to

improve the responsibility level. It evaluates the administration of the Capital Land Plc to

study about all the related factors (Davies and Crawford, 2011).

Guides the management:

More, budgetary techniques help the Capital Land Plc and its managers to make some

new policies and strategies according to the position and the performance of the organization.

This technique helps the top level management and middle level management to guide the

lower level management and labour so that they could perform their duties perfectly

(Weygandt, Kimmel and Kieso, 2015). It evaluates the administration of the Capital Land Plc

to study about all the related factors.

Assists in directing:

Further, budgetary techniques help the Capital Land Plc and its managers to make

some direction plans according to the changes and the prediction about the organization. This

technique helps the manufacturing managers to generate and enhance the sense of

responsibility in the labour and the employees of the organization. It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company (Warren, Reeve and Duchac, 2013).

Management involvement:

Further, budgetary techniques help the Capital Land Plc and its managers to set up a

coordination and communication program so that the better evaluation over the position and

performance could be done. This technique helps the manufacturing managers to identify

various financial data and non financial information such as the market prediction, choice of

the customers, competitor position, supplier’s state etc (Van der Stede, 2011). It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company.

Objective definition:

It is required for every organization to identify the objectives of the business so that

the work could be done in the same way. Further, budgetary techniques help the Capital Land

Plc and its managers to define the goals and the objectives of the organization. This technique

helps the manufacturing managers to evaluate and define the objectives to the labour and the

employees of the organization. It evaluates the administration of the Capital Land Plc to

managers and middle level manager to generate and enhance the sense of caution and care to

improve the responsibility level. It evaluates the administration of the Capital Land Plc to

study about all the related factors (Davies and Crawford, 2011).

Guides the management:

More, budgetary techniques help the Capital Land Plc and its managers to make some

new policies and strategies according to the position and the performance of the organization.

This technique helps the top level management and middle level management to guide the

lower level management and labour so that they could perform their duties perfectly

(Weygandt, Kimmel and Kieso, 2015). It evaluates the administration of the Capital Land Plc

to study about all the related factors.

Assists in directing:

Further, budgetary techniques help the Capital Land Plc and its managers to make

some direction plans according to the changes and the prediction about the organization. This

technique helps the manufacturing managers to generate and enhance the sense of

responsibility in the labour and the employees of the organization. It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company (Warren, Reeve and Duchac, 2013).

Management involvement:

Further, budgetary techniques help the Capital Land Plc and its managers to set up a

coordination and communication program so that the better evaluation over the position and

performance could be done. This technique helps the manufacturing managers to identify

various financial data and non financial information such as the market prediction, choice of

the customers, competitor position, supplier’s state etc (Van der Stede, 2011). It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company.

Objective definition:

It is required for every organization to identify the objectives of the business so that

the work could be done in the same way. Further, budgetary techniques help the Capital Land

Plc and its managers to define the goals and the objectives of the organization. This technique

helps the manufacturing managers to evaluate and define the objectives to the labour and the

employees of the organization. It evaluates the administration of the Capital Land Plc to

Managing Financial Performance 12

improve the performance and the position of the company (Radebaugh, Gray and Black,

2006).

Compels management:

Further, budgetary techniques help the Capital Land Plc and its managers to set up a

coordination and communication program so that the better evaluation over the position and

performance could be done. This technique helps the manufacturing managers to identify

various financial data and non financial information such as the market prediction, choice of

the customers, competitor position, supplier’s state etc (Nobes and Parker, 2008). It evaluates

the administration of the Capital Land Plc to improve the performance and the position of the

company.

Promotes communication and coordination:

More, budgetary techniques help the Capital Land Plc and its managers to make some

new policies and strategies according to the position and the performance of the organization.

This technique helps the top level management and middle level management to set the

communication so that they could perform their duties perfectly. It evaluates the

administration of the Capital Land Plc to study about all the related factors (Needles, Powers

and Crosson, 2013).

Define responsibility:

Further, budgetary techniques help the Capital Land Plc and its managers to define the

responsibilities of the organization. This technique helps the manufacturing managers to

evaluate and define the responsibilities to the labour and the employees of the organization. It

evaluates the administration of the Capital Land Plc to improve the performance and the

position of the company (Marginson, 2009).

Motivates employees and labour:

Further, budgetary techniques help the Capital Land Plc and its managers to make

some direction plans according to the changes and the prediction about the organization. This

technique helps the manufacturing managers to generate and enhance the sense of

responsibility in the labour and the employees of the organization. It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company (Lafond and Roychowdhury, 2008).

improve the performance and the position of the company (Radebaugh, Gray and Black,

2006).

Compels management:

Further, budgetary techniques help the Capital Land Plc and its managers to set up a

coordination and communication program so that the better evaluation over the position and

performance could be done. This technique helps the manufacturing managers to identify

various financial data and non financial information such as the market prediction, choice of

the customers, competitor position, supplier’s state etc (Nobes and Parker, 2008). It evaluates

the administration of the Capital Land Plc to improve the performance and the position of the

company.

Promotes communication and coordination:

More, budgetary techniques help the Capital Land Plc and its managers to make some

new policies and strategies according to the position and the performance of the organization.

This technique helps the top level management and middle level management to set the

communication so that they could perform their duties perfectly. It evaluates the

administration of the Capital Land Plc to study about all the related factors (Needles, Powers

and Crosson, 2013).

Define responsibility:

Further, budgetary techniques help the Capital Land Plc and its managers to define the

responsibilities of the organization. This technique helps the manufacturing managers to

evaluate and define the responsibilities to the labour and the employees of the organization. It

evaluates the administration of the Capital Land Plc to improve the performance and the

position of the company (Marginson, 2009).

Motivates employees and labour:

Further, budgetary techniques help the Capital Land Plc and its managers to make

some direction plans according to the changes and the prediction about the organization. This

technique helps the manufacturing managers to generate and enhance the sense of

responsibility in the labour and the employees of the organization. It evaluates the

administration of the Capital Land Plc to improve the performance and the position of the

company (Lafond and Roychowdhury, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.