Accounts for Managers: Analysis of Cash Flow and Profitability

VerifiedAdded on 2021/01/01

|10

|2103

|183

Report

AI Summary

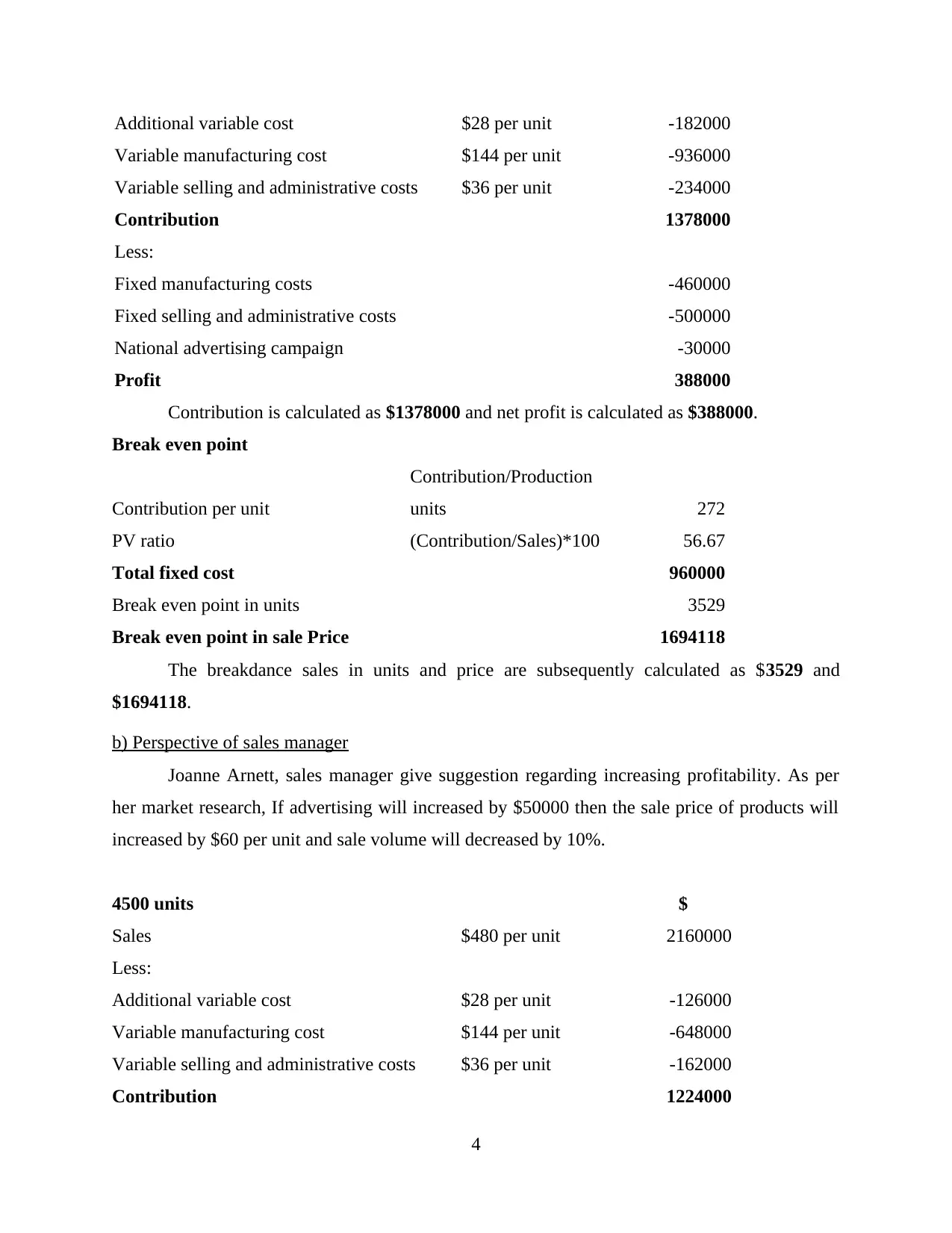

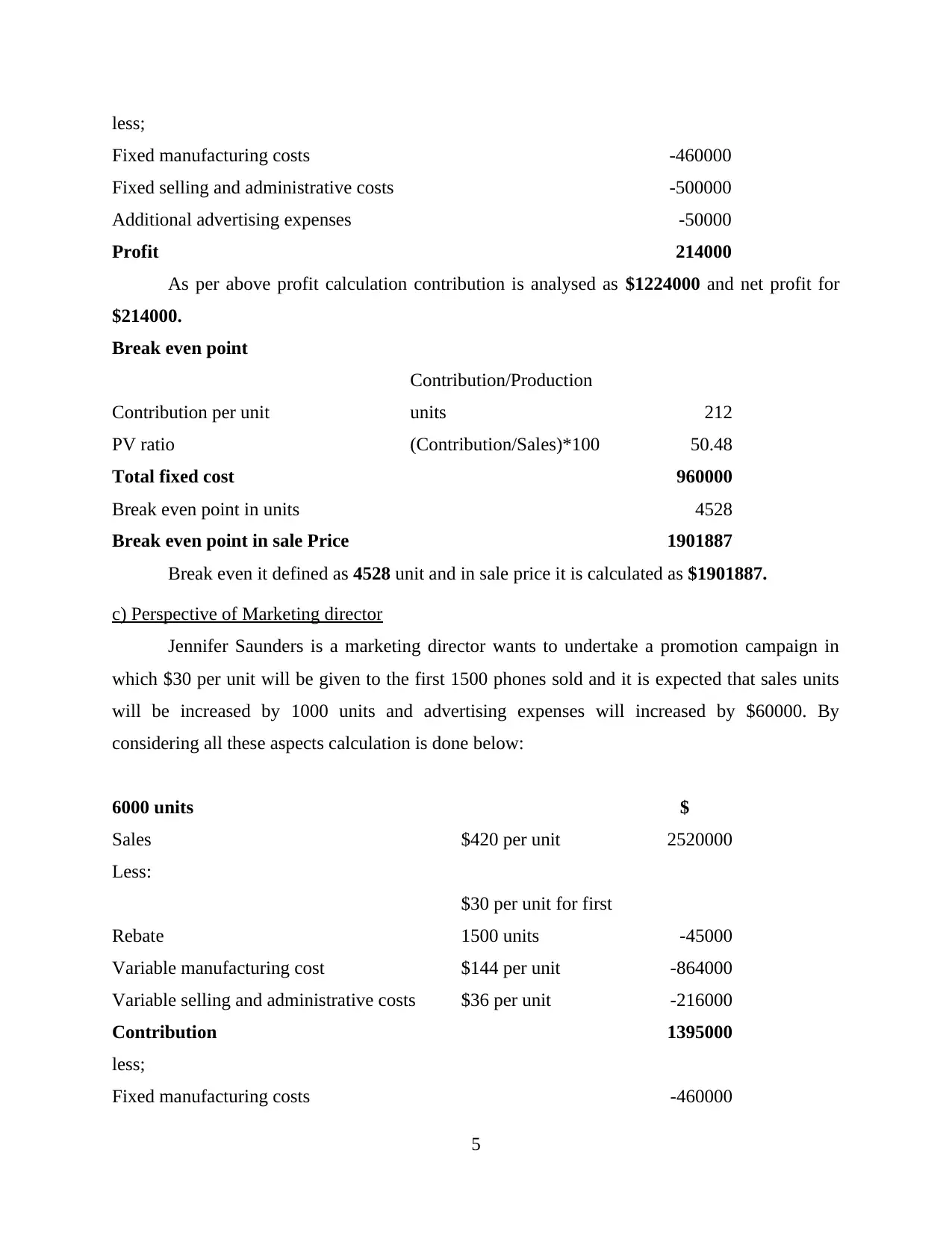

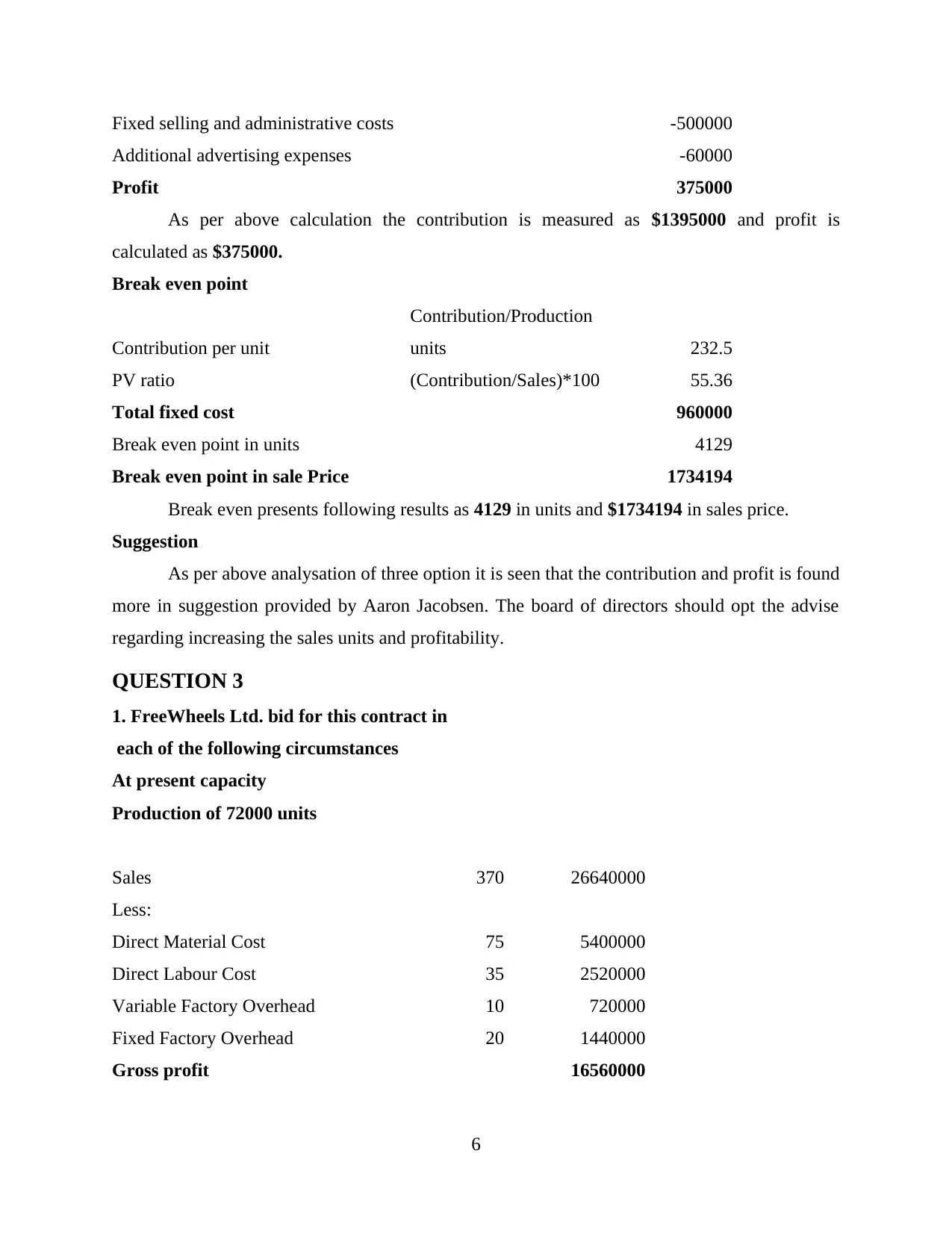

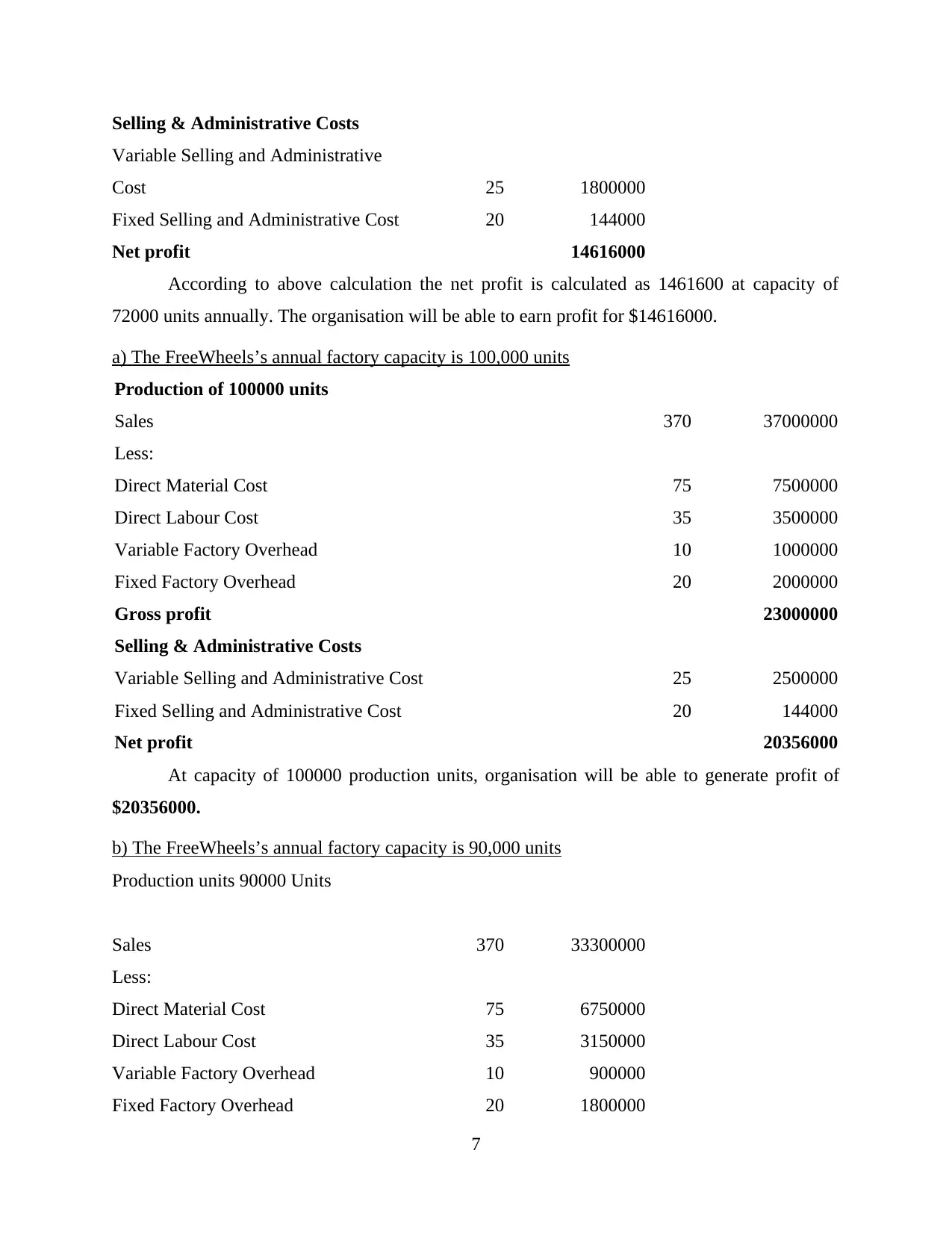

This report provides a detailed analysis of accounting concepts relevant to managers, focusing on cash conversion cycles, profitability, and strategic decision-making. It begins with an introduction to accounting's role in assessing business performance and then calculates the cash conversion cycle for Telstra Corporation. The report then presents a case study of Telesmart Ltd, exploring different perspectives from production, sales, and marketing managers to improve profitability. It includes break-even analysis and profit calculations for each scenario. Finally, the report evaluates a contract bid for FreeWheels Ltd, considering different production capacities and their impact on profitability. The conclusion summarizes the key findings and recommendations for improving sales volume and financial outcomes. The report uses various financial metrics and scenarios to illustrate accounting principles and assist in management decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.