Managing Operations and Finance: Adidas vs. Puma Financial Report

VerifiedAdded on 2022/08/24

|29

|3738

|11

Report

AI Summary

This report provides a comprehensive financial analysis of Adidas and Puma, two leading companies in the sportswear industry. The analysis begins with an overview of the industry and a company background, followed by an examination of their business strategies and operational analyses. The core of the report focuses on evaluating the financial performance of both companies using key financial ratios, including net profit margin, operating return on equity, and return on capital employed. Risk analysis is also conducted, looking at current and debt-equity ratios, and operating leverage. Furthermore, managerial performance, market performance, and sustainability aspects are assessed, providing a holistic view of each company's financial health and operational effectiveness. The report concludes with a comparative analysis of both companies, highlighting their strengths, weaknesses, and overall financial performance in the competitive sportswear market.

Running head: MANAGE OPERATIONS AND FINANCE

Manage Operations and Finance

Name of the Student

Name of the University

Authors Note

Course ID

Manage Operations and Finance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGE OPERATIONS AND FINANCE

Table of Contents

Chapter 1: Operational Analysis...................................................................................3

1: Introduction:..........................................................................................................3

2: Industry Analysis:..................................................................................................3

3: Company overview:..............................................................................................4

4: Business strategy:.................................................................................................6

5: Operational Analysis:............................................................................................7

Chapter 2 Evaluation of performance...........................................................................8

1: Financial performance..........................................................................................8

Table 1: Net profit margin...................................................................................8

Table 2: Operating return on equity......................................................................9

Table 3: Return on capital employed..............................................................10

2: Risk analysis.......................................................................................................11

Table 5: Current ratio........................................................................................11

Table 6: Debt equity ratio.................................................................................12

Table 7: Operating leverage................................................................................13

3: Managerial Performance.....................................................................................14

Table 8: Asset turnover....................................................................................14

Table 9: Inventory turnover..............................................................................16

Table 10: Debt collection period......................................................................17

4: Market Performance:..........................................................................................17

Table 11: Earnings per Share...........................................................................18

Table 12: Price-Earnings per share....................................................................19

Table 13: Dividend Yield.....................................................................................19

6: Sustainability and CSR:..........................................................................................20

7: Conclusion:.............................................................................................................21

References:................................................................................................................22

Table of Contents

Chapter 1: Operational Analysis...................................................................................3

1: Introduction:..........................................................................................................3

2: Industry Analysis:..................................................................................................3

3: Company overview:..............................................................................................4

4: Business strategy:.................................................................................................6

5: Operational Analysis:............................................................................................7

Chapter 2 Evaluation of performance...........................................................................8

1: Financial performance..........................................................................................8

Table 1: Net profit margin...................................................................................8

Table 2: Operating return on equity......................................................................9

Table 3: Return on capital employed..............................................................10

2: Risk analysis.......................................................................................................11

Table 5: Current ratio........................................................................................11

Table 6: Debt equity ratio.................................................................................12

Table 7: Operating leverage................................................................................13

3: Managerial Performance.....................................................................................14

Table 8: Asset turnover....................................................................................14

Table 9: Inventory turnover..............................................................................16

Table 10: Debt collection period......................................................................17

4: Market Performance:..........................................................................................17

Table 11: Earnings per Share...........................................................................18

Table 12: Price-Earnings per share....................................................................19

Table 13: Dividend Yield.....................................................................................19

6: Sustainability and CSR:..........................................................................................20

7: Conclusion:.............................................................................................................21

References:................................................................................................................22

2MANAGE OPERATIONS AND FINANCE

Appendix A: Adidas:...................................................................................................24

Appendix B: PUMA.....................................................................................................26

Appendix A: Adidas:...................................................................................................24

Appendix B: PUMA.....................................................................................................26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGE OPERATIONS AND FINANCE

Chapter 1: Operational Analysis

1: Introduction:

The analysis of financial statement is regarded as the procedure of reviewing

and assessing an organization’s financial statement in order to make improved

financial decision for better future income (Schroeder, Clark and Cathey 2019). The

external stakeholders normally make use of financial reports to gain an

understanding of overall financial health of the company for evaluating the financial

performance and business values.

Adidas AG is the multinational company, founded and having its headquarter

in Germany. The company designs and manufacture shoes, clothing and

accessories. It is regarded as the largest sportswear manufacturer in Europe and the

second largest in the world after Nike. While, PUMA is a German multinational

corporation which designs and manufactures athletic as well as casual footwear,

accessories and apparel that has its headquarter in Germany. It is regarded as the

third largest sportswear brand in the world. The company was founded in the year

1948 by Rudolf and his brother Adolf Dassler. However, the relationship among the

two brothers deteriorated until the two decided to split in 1948 and forming two

separate entities namely Adidas and PUMA. Both the companies are presently

located in Germany, Herzogenaurach.

The present report will be analysing the financial performance of both the

companies based on the data accumulated from the financial reports of 2017 and

2018 respectively. By performing a comparative analysis an understanding of the

two company’s profitability situations can be obtained in sportswear sector.

2: Industry Analysis:

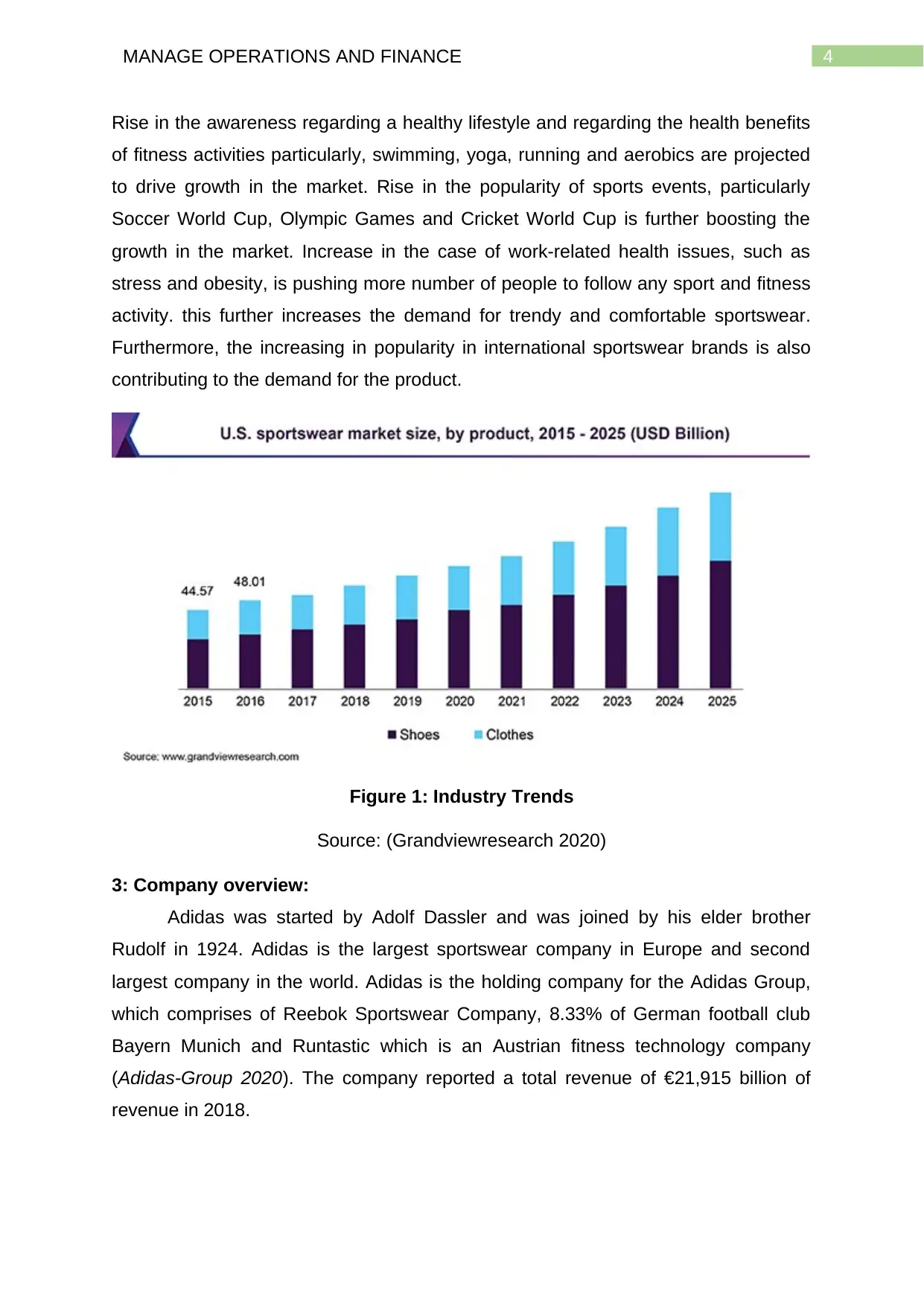

The market for sports apparel was valued at $239.78 billion during 2018 and it

is projected to grow CAGR 10.4% by the year 2025. During 2018, the segment of

men and women end user amounted to greater than half of the share in total sports

apparel market and it is anticipated to grow more than half of the share in the overall

sports accessories and apparel market (Grandviewresearch 2020). The anticipated

forecasted growth stands CAGR of 4.6% all through the forecast period.

Chapter 1: Operational Analysis

1: Introduction:

The analysis of financial statement is regarded as the procedure of reviewing

and assessing an organization’s financial statement in order to make improved

financial decision for better future income (Schroeder, Clark and Cathey 2019). The

external stakeholders normally make use of financial reports to gain an

understanding of overall financial health of the company for evaluating the financial

performance and business values.

Adidas AG is the multinational company, founded and having its headquarter

in Germany. The company designs and manufacture shoes, clothing and

accessories. It is regarded as the largest sportswear manufacturer in Europe and the

second largest in the world after Nike. While, PUMA is a German multinational

corporation which designs and manufactures athletic as well as casual footwear,

accessories and apparel that has its headquarter in Germany. It is regarded as the

third largest sportswear brand in the world. The company was founded in the year

1948 by Rudolf and his brother Adolf Dassler. However, the relationship among the

two brothers deteriorated until the two decided to split in 1948 and forming two

separate entities namely Adidas and PUMA. Both the companies are presently

located in Germany, Herzogenaurach.

The present report will be analysing the financial performance of both the

companies based on the data accumulated from the financial reports of 2017 and

2018 respectively. By performing a comparative analysis an understanding of the

two company’s profitability situations can be obtained in sportswear sector.

2: Industry Analysis:

The market for sports apparel was valued at $239.78 billion during 2018 and it

is projected to grow CAGR 10.4% by the year 2025. During 2018, the segment of

men and women end user amounted to greater than half of the share in total sports

apparel market and it is anticipated to grow more than half of the share in the overall

sports accessories and apparel market (Grandviewresearch 2020). The anticipated

forecasted growth stands CAGR of 4.6% all through the forecast period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGE OPERATIONS AND FINANCE

Rise in the awareness regarding a healthy lifestyle and regarding the health benefits

of fitness activities particularly, swimming, yoga, running and aerobics are projected

to drive growth in the market. Rise in the popularity of sports events, particularly

Soccer World Cup, Olympic Games and Cricket World Cup is further boosting the

growth in the market. Increase in the case of work-related health issues, such as

stress and obesity, is pushing more number of people to follow any sport and fitness

activity. this further increases the demand for trendy and comfortable sportswear.

Furthermore, the increasing in popularity in international sportswear brands is also

contributing to the demand for the product.

Figure 1: Industry Trends

Source: (Grandviewresearch 2020)

3: Company overview:

Adidas was started by Adolf Dassler and was joined by his elder brother

Rudolf in 1924. Adidas is the largest sportswear company in Europe and second

largest company in the world. Adidas is the holding company for the Adidas Group,

which comprises of Reebok Sportswear Company, 8.33% of German football club

Bayern Munich and Runtastic which is an Austrian fitness technology company

(Adidas-Group 2020). The company reported a total revenue of €21,915 billion of

revenue in 2018.

Rise in the awareness regarding a healthy lifestyle and regarding the health benefits

of fitness activities particularly, swimming, yoga, running and aerobics are projected

to drive growth in the market. Rise in the popularity of sports events, particularly

Soccer World Cup, Olympic Games and Cricket World Cup is further boosting the

growth in the market. Increase in the case of work-related health issues, such as

stress and obesity, is pushing more number of people to follow any sport and fitness

activity. this further increases the demand for trendy and comfortable sportswear.

Furthermore, the increasing in popularity in international sportswear brands is also

contributing to the demand for the product.

Figure 1: Industry Trends

Source: (Grandviewresearch 2020)

3: Company overview:

Adidas was started by Adolf Dassler and was joined by his elder brother

Rudolf in 1924. Adidas is the largest sportswear company in Europe and second

largest company in the world. Adidas is the holding company for the Adidas Group,

which comprises of Reebok Sportswear Company, 8.33% of German football club

Bayern Munich and Runtastic which is an Austrian fitness technology company

(Adidas-Group 2020). The company reported a total revenue of €21,915 billion of

revenue in 2018.

5MANAGE OPERATIONS AND FINANCE

Figure 2: Adidas Logo

Source: (Adidas-Group 2020)

PUMA, on the other hand, is the third largest company of sportswear and

accessories in the world. The company was founded by in 1948 by Rudolf Dassler

which has its base in Herzogenaurach, Germany. PUMA employs greater than

13,000 people across the world and sells its product in greater than 120 countries

(PUMA SE 2020). PUMA has been listed as public company since 1986 and since

2013 the company has been led by a former football professional Bjorn Gulden.

Figure 3: PUMA Logo

Source: (PUMA SE 2020)

Figure 2: Adidas Logo

Source: (Adidas-Group 2020)

PUMA, on the other hand, is the third largest company of sportswear and

accessories in the world. The company was founded by in 1948 by Rudolf Dassler

which has its base in Herzogenaurach, Germany. PUMA employs greater than

13,000 people across the world and sells its product in greater than 120 countries

(PUMA SE 2020). PUMA has been listed as public company since 1986 and since

2013 the company has been led by a former football professional Bjorn Gulden.

Figure 3: PUMA Logo

Source: (PUMA SE 2020)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGE OPERATIONS AND FINANCE

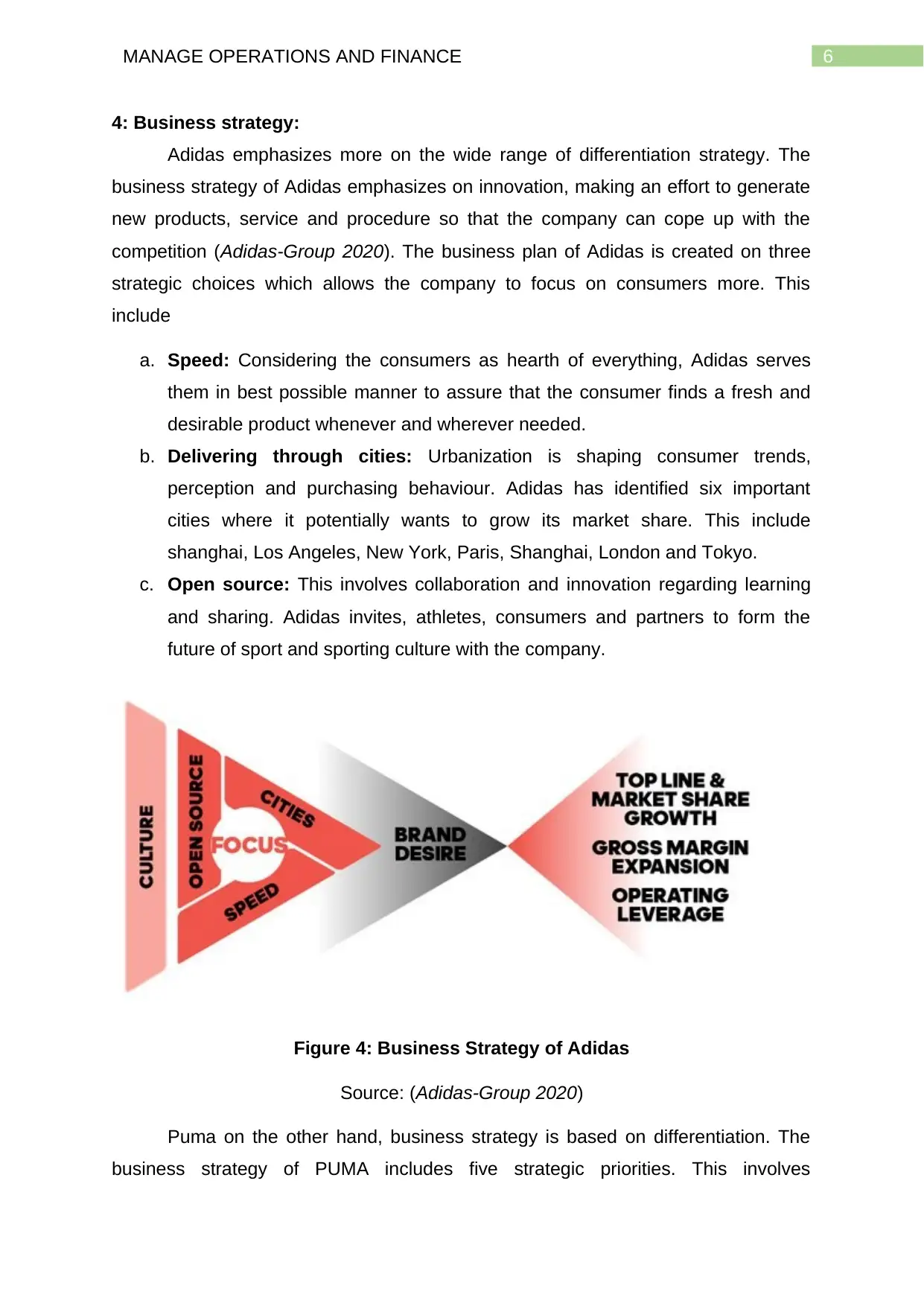

4: Business strategy:

Adidas emphasizes more on the wide range of differentiation strategy. The

business strategy of Adidas emphasizes on innovation, making an effort to generate

new products, service and procedure so that the company can cope up with the

competition (Adidas-Group 2020). The business plan of Adidas is created on three

strategic choices which allows the company to focus on consumers more. This

include

a. Speed: Considering the consumers as hearth of everything, Adidas serves

them in best possible manner to assure that the consumer finds a fresh and

desirable product whenever and wherever needed.

b. Delivering through cities: Urbanization is shaping consumer trends,

perception and purchasing behaviour. Adidas has identified six important

cities where it potentially wants to grow its market share. This include

shanghai, Los Angeles, New York, Paris, Shanghai, London and Tokyo.

c. Open source: This involves collaboration and innovation regarding learning

and sharing. Adidas invites, athletes, consumers and partners to form the

future of sport and sporting culture with the company.

Figure 4: Business Strategy of Adidas

Source: (Adidas-Group 2020)

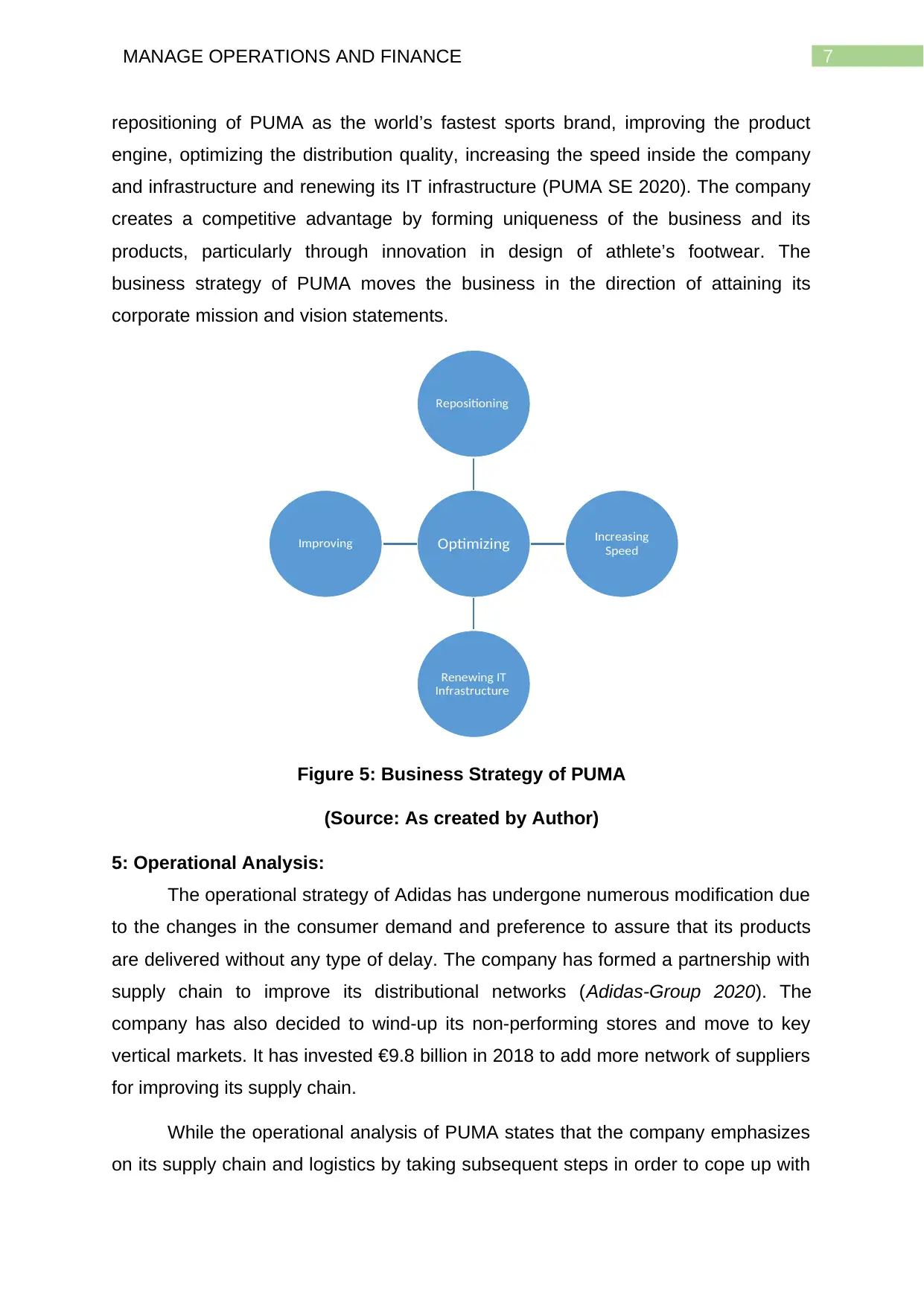

Puma on the other hand, business strategy is based on differentiation. The

business strategy of PUMA includes five strategic priorities. This involves

4: Business strategy:

Adidas emphasizes more on the wide range of differentiation strategy. The

business strategy of Adidas emphasizes on innovation, making an effort to generate

new products, service and procedure so that the company can cope up with the

competition (Adidas-Group 2020). The business plan of Adidas is created on three

strategic choices which allows the company to focus on consumers more. This

include

a. Speed: Considering the consumers as hearth of everything, Adidas serves

them in best possible manner to assure that the consumer finds a fresh and

desirable product whenever and wherever needed.

b. Delivering through cities: Urbanization is shaping consumer trends,

perception and purchasing behaviour. Adidas has identified six important

cities where it potentially wants to grow its market share. This include

shanghai, Los Angeles, New York, Paris, Shanghai, London and Tokyo.

c. Open source: This involves collaboration and innovation regarding learning

and sharing. Adidas invites, athletes, consumers and partners to form the

future of sport and sporting culture with the company.

Figure 4: Business Strategy of Adidas

Source: (Adidas-Group 2020)

Puma on the other hand, business strategy is based on differentiation. The

business strategy of PUMA includes five strategic priorities. This involves

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE OPERATIONS AND FINANCE

repositioning of PUMA as the world’s fastest sports brand, improving the product

engine, optimizing the distribution quality, increasing the speed inside the company

and infrastructure and renewing its IT infrastructure (PUMA SE 2020). The company

creates a competitive advantage by forming uniqueness of the business and its

products, particularly through innovation in design of athlete’s footwear. The

business strategy of PUMA moves the business in the direction of attaining its

corporate mission and vision statements.

Figure 5: Business Strategy of PUMA

(Source: As created by Author)

5: Operational Analysis:

The operational strategy of Adidas has undergone numerous modification due

to the changes in the consumer demand and preference to assure that its products

are delivered without any type of delay. The company has formed a partnership with

supply chain to improve its distributional networks (Adidas-Group 2020). The

company has also decided to wind-up its non-performing stores and move to key

vertical markets. It has invested €9.8 billion in 2018 to add more network of suppliers

for improving its supply chain.

While the operational analysis of PUMA states that the company emphasizes

on its supply chain and logistics by taking subsequent steps in order to cope up with

Optimizing

Repositioning

Increasing

Speed

Renewing IT

Infrastructure

Improving

repositioning of PUMA as the world’s fastest sports brand, improving the product

engine, optimizing the distribution quality, increasing the speed inside the company

and infrastructure and renewing its IT infrastructure (PUMA SE 2020). The company

creates a competitive advantage by forming uniqueness of the business and its

products, particularly through innovation in design of athlete’s footwear. The

business strategy of PUMA moves the business in the direction of attaining its

corporate mission and vision statements.

Figure 5: Business Strategy of PUMA

(Source: As created by Author)

5: Operational Analysis:

The operational strategy of Adidas has undergone numerous modification due

to the changes in the consumer demand and preference to assure that its products

are delivered without any type of delay. The company has formed a partnership with

supply chain to improve its distributional networks (Adidas-Group 2020). The

company has also decided to wind-up its non-performing stores and move to key

vertical markets. It has invested €9.8 billion in 2018 to add more network of suppliers

for improving its supply chain.

While the operational analysis of PUMA states that the company emphasizes

on its supply chain and logistics by taking subsequent steps in order to cope up with

Optimizing

Repositioning

Increasing

Speed

Renewing IT

Infrastructure

Improving

8MANAGE OPERATIONS AND FINANCE

the risk and barriers that might arise because of the changes in consumer taste and

preference (PUMA SE 2020). To meet the demands of the urbanized customers, it is

implemented SCM concept which provides them about the ideas logistics and supply

chain on priority. PUMA has collaborated with the global logistics company so that it

can reach customers across several target markets.

Chapter 2 Evaluation of performance

1: Financial performance

Net Profit Margin:

The net profit margin ratio is a profitability metric which measures the

percentage of dollars earned by business as profit by the end of the year (No 2018).

The formula is

Net Profit Margin=( Net Profit before interest ∧tax

Turnover )∗100

Net Profit Margin

Addidas Puma

2017 2018 2017 2018

10% 11% 6% 5%

Table 1: Net profit margin

(Source: As created by author)

The net profit margin for Adidas in 2017 stood 10% while in 2018 it increased

to 11%. PUMA reported a relatively lower net profit margin of 6% and 5% in 2017

and 2018 respectively.

the risk and barriers that might arise because of the changes in consumer taste and

preference (PUMA SE 2020). To meet the demands of the urbanized customers, it is

implemented SCM concept which provides them about the ideas logistics and supply

chain on priority. PUMA has collaborated with the global logistics company so that it

can reach customers across several target markets.

Chapter 2 Evaluation of performance

1: Financial performance

Net Profit Margin:

The net profit margin ratio is a profitability metric which measures the

percentage of dollars earned by business as profit by the end of the year (No 2018).

The formula is

Net Profit Margin=( Net Profit before interest ∧tax

Turnover )∗100

Net Profit Margin

Addidas Puma

2017 2018 2017 2018

10% 11% 6% 5%

Table 1: Net profit margin

(Source: As created by author)

The net profit margin for Adidas in 2017 stood 10% while in 2018 it increased

to 11%. PUMA reported a relatively lower net profit margin of 6% and 5% in 2017

and 2018 respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGE OPERATIONS AND FINANCE

2017 2018 2017 2018

Addidas Puma

10%

11%

6% 5%

Net Profit Margin

Figure 6: Net Profit Margin

(Source: As created by author)

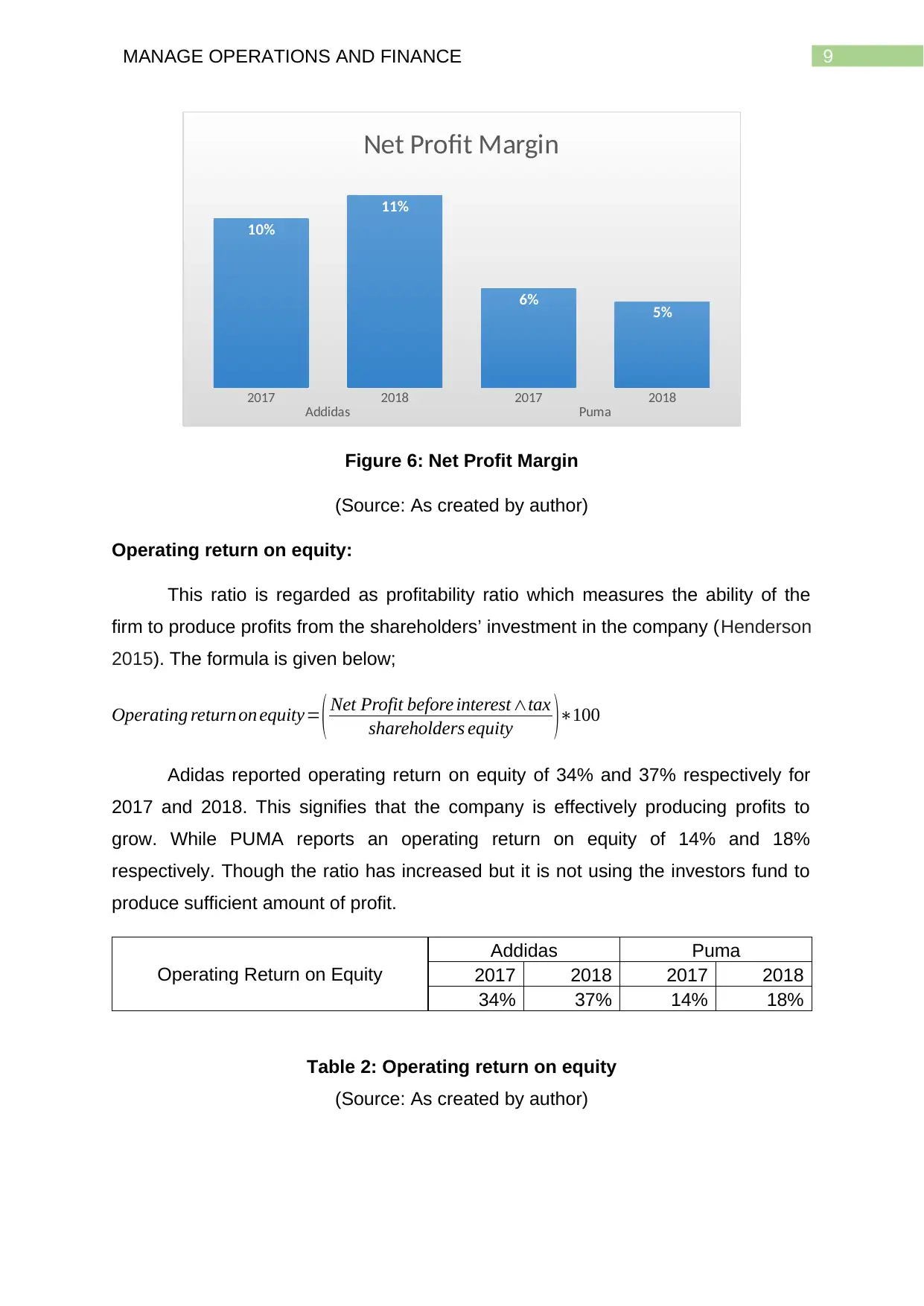

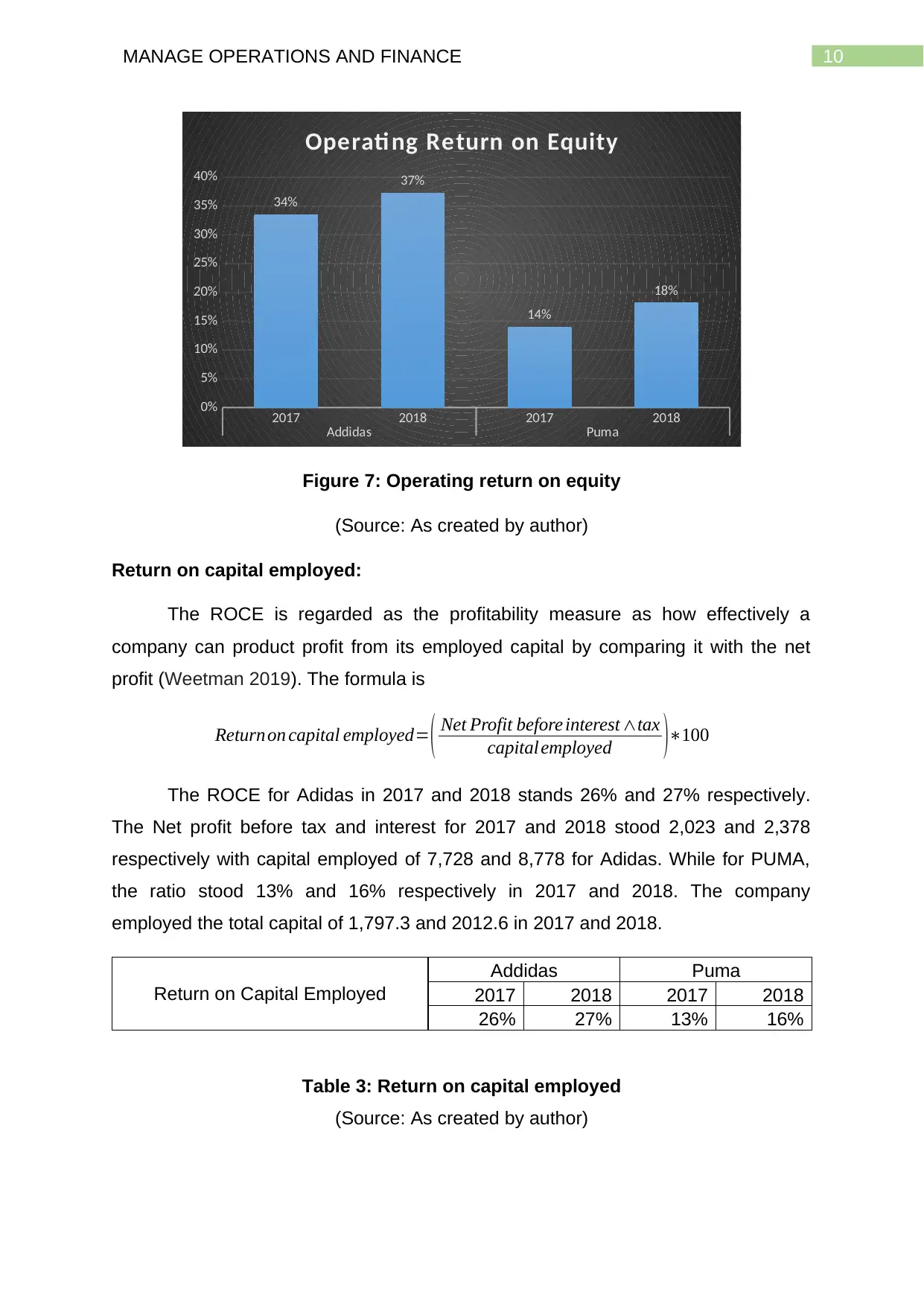

Operating return on equity:

This ratio is regarded as profitability ratio which measures the ability of the

firm to produce profits from the shareholders’ investment in the company (Henderson

2015). The formula is given below;

Operating return on equity= ( Net Profit before interest ∧tax

shareholders equity )∗100

Adidas reported operating return on equity of 34% and 37% respectively for

2017 and 2018. This signifies that the company is effectively producing profits to

grow. While PUMA reports an operating return on equity of 14% and 18%

respectively. Though the ratio has increased but it is not using the investors fund to

produce sufficient amount of profit.

Operating Return on Equity

Addidas Puma

2017 2018 2017 2018

34% 37% 14% 18%

Table 2: Operating return on equity

(Source: As created by author)

2017 2018 2017 2018

Addidas Puma

10%

11%

6% 5%

Net Profit Margin

Figure 6: Net Profit Margin

(Source: As created by author)

Operating return on equity:

This ratio is regarded as profitability ratio which measures the ability of the

firm to produce profits from the shareholders’ investment in the company (Henderson

2015). The formula is given below;

Operating return on equity= ( Net Profit before interest ∧tax

shareholders equity )∗100

Adidas reported operating return on equity of 34% and 37% respectively for

2017 and 2018. This signifies that the company is effectively producing profits to

grow. While PUMA reports an operating return on equity of 14% and 18%

respectively. Though the ratio has increased but it is not using the investors fund to

produce sufficient amount of profit.

Operating Return on Equity

Addidas Puma

2017 2018 2017 2018

34% 37% 14% 18%

Table 2: Operating return on equity

(Source: As created by author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGE OPERATIONS AND FINANCE

2017 2018 2017 2018

Addidas Puma

0%

5%

10%

15%

20%

25%

30%

35%

40%

34%

37%

14%

18%

Operati ng Return on Equity

Figure 7: Operating return on equity

(Source: As created by author)

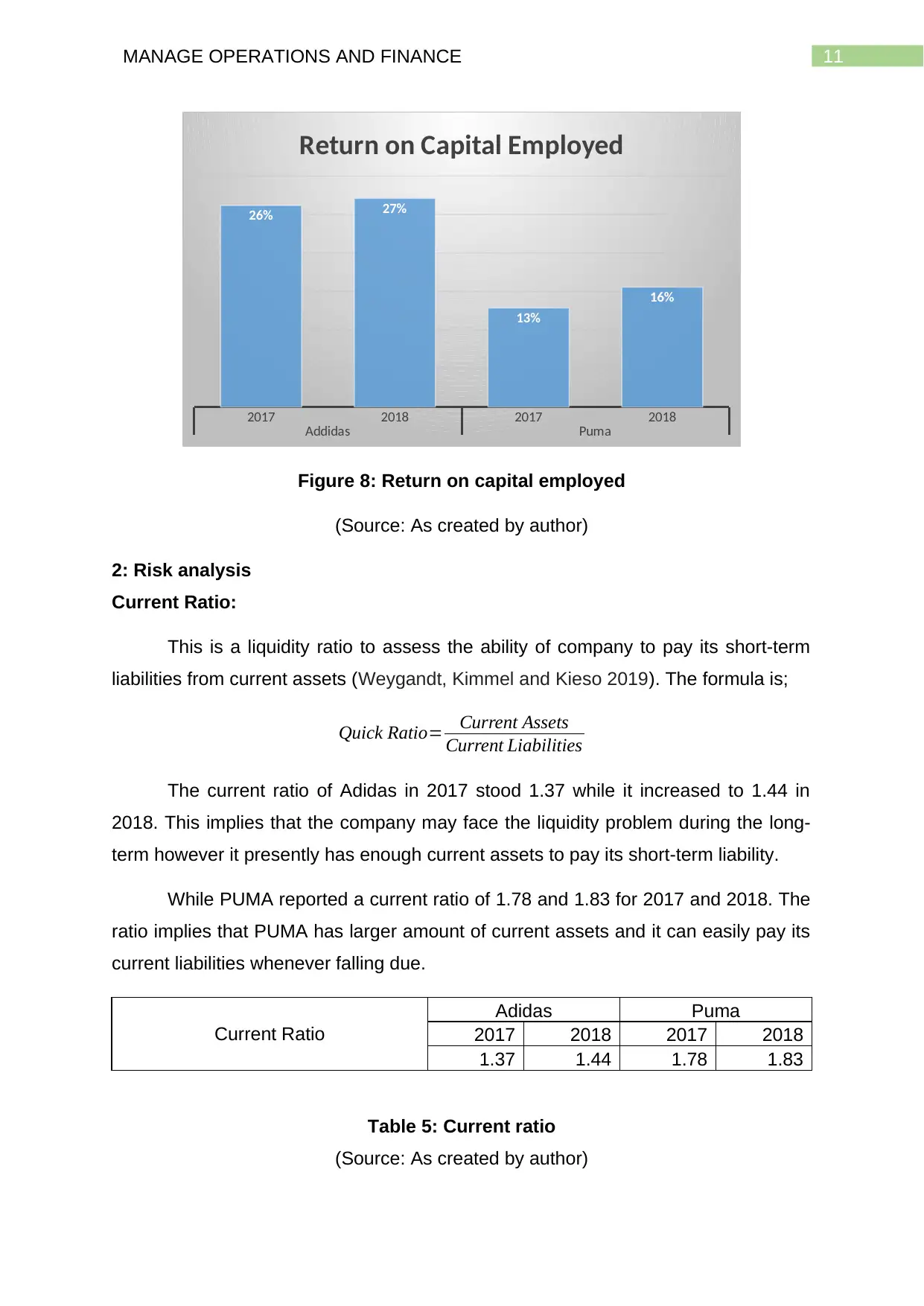

Return on capital employed:

The ROCE is regarded as the profitability measure as how effectively a

company can product profit from its employed capital by comparing it with the net

profit (Weetman 2019). The formula is

Returnon capital employed= ( Net Profit before interest ∧tax

capital employed )∗100

The ROCE for Adidas in 2017 and 2018 stands 26% and 27% respectively.

The Net profit before tax and interest for 2017 and 2018 stood 2,023 and 2,378

respectively with capital employed of 7,728 and 8,778 for Adidas. While for PUMA,

the ratio stood 13% and 16% respectively in 2017 and 2018. The company

employed the total capital of 1,797.3 and 2012.6 in 2017 and 2018.

Return on Capital Employed

Addidas Puma

2017 2018 2017 2018

26% 27% 13% 16%

Table 3: Return on capital employed

(Source: As created by author)

2017 2018 2017 2018

Addidas Puma

0%

5%

10%

15%

20%

25%

30%

35%

40%

34%

37%

14%

18%

Operati ng Return on Equity

Figure 7: Operating return on equity

(Source: As created by author)

Return on capital employed:

The ROCE is regarded as the profitability measure as how effectively a

company can product profit from its employed capital by comparing it with the net

profit (Weetman 2019). The formula is

Returnon capital employed= ( Net Profit before interest ∧tax

capital employed )∗100

The ROCE for Adidas in 2017 and 2018 stands 26% and 27% respectively.

The Net profit before tax and interest for 2017 and 2018 stood 2,023 and 2,378

respectively with capital employed of 7,728 and 8,778 for Adidas. While for PUMA,

the ratio stood 13% and 16% respectively in 2017 and 2018. The company

employed the total capital of 1,797.3 and 2012.6 in 2017 and 2018.

Return on Capital Employed

Addidas Puma

2017 2018 2017 2018

26% 27% 13% 16%

Table 3: Return on capital employed

(Source: As created by author)

11MANAGE OPERATIONS AND FINANCE

2017 2018 2017 2018

Addidas Puma

26% 27%

13%

16%

Return on Capital Employed

Figure 8: Return on capital employed

(Source: As created by author)

2: Risk analysis

Current Ratio:

This is a liquidity ratio to assess the ability of company to pay its short-term

liabilities from current assets (Weygandt, Kimmel and Kieso 2019). The formula is;

Quick Ratio= Current Assets

Current Liabilities

The current ratio of Adidas in 2017 stood 1.37 while it increased to 1.44 in

2018. This implies that the company may face the liquidity problem during the long-

term however it presently has enough current assets to pay its short-term liability.

While PUMA reported a current ratio of 1.78 and 1.83 for 2017 and 2018. The

ratio implies that PUMA has larger amount of current assets and it can easily pay its

current liabilities whenever falling due.

Current Ratio

Adidas Puma

2017 2018 2017 2018

1.37 1.44 1.78 1.83

Table 5: Current ratio

(Source: As created by author)

2017 2018 2017 2018

Addidas Puma

26% 27%

13%

16%

Return on Capital Employed

Figure 8: Return on capital employed

(Source: As created by author)

2: Risk analysis

Current Ratio:

This is a liquidity ratio to assess the ability of company to pay its short-term

liabilities from current assets (Weygandt, Kimmel and Kieso 2019). The formula is;

Quick Ratio= Current Assets

Current Liabilities

The current ratio of Adidas in 2017 stood 1.37 while it increased to 1.44 in

2018. This implies that the company may face the liquidity problem during the long-

term however it presently has enough current assets to pay its short-term liability.

While PUMA reported a current ratio of 1.78 and 1.83 for 2017 and 2018. The

ratio implies that PUMA has larger amount of current assets and it can easily pay its

current liabilities whenever falling due.

Current Ratio

Adidas Puma

2017 2018 2017 2018

1.37 1.44 1.78 1.83

Table 5: Current ratio

(Source: As created by author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.