Comprehensive Financial Performance Analysis: Alumex PLC MBA Report

VerifiedAdded on 2022/01/21

|30

|6618

|191

Report

AI Summary

This report offers a comprehensive analysis of the financial performance of Alumex PLC, a prominent aluminum product manufacturer in Sri Lanka, utilizing its annual reports. The analysis begins with an introduction to the company, emphasizing the importance of annual reports for stakeholders, particularly investors and employees. It then differentiates between financial statements of limited companies and other legal entities, comparing features of financial statements of limited companies with sole proprietorships and partnerships. The report delves into working capital and the working capital cycle to identify and suggest solutions for working capital issues. Furthermore, it examines Alumex PLC's sources of finance over the past three years, including their advantages and disadvantages. Finally, the report includes a capital budgeting analysis, presenting a forecasted cash flow statement and calculating key metrics such as Accounting Rate of Return, Payback Period, Net Present Value, and Internal Rate of Return to assess the viability of a planned project.

Analysis of Financial Performance of

Alumex PLC

MASTER OF BUSINESS ADMINISTRATION

Alumex PLC

MASTER OF BUSINESS ADMINISTRATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PAGE 9

Executive summary

This comprehensive report has mainly conducted along with the analysis done utilizing the

annual reports of Alumex PLC, which is a leading aluminum product manufacture in Sri

Lanka. Commencing from an introduction given to the recognized organization, then the

importance of using annual reports is discussed in investors’ and employees’ perspectives.

From that analysis it is evident that the company is favorable to invest. Third chapter briefs

the differences between the financial statements of limited companies and other legal entities.

Comparison done in this section comparing the features of financial statements of limited

companies with sole proprietorships and partnerships. The report flows towards most

significant analysis done in the fourth chapter by analyzing the working capital and the

working capital cycle in order to identify the working capital issues faces by the organization.

Suggestions are given in overcoming such issues by handling relevant components. Fifth

chapter is all about sources of finances which have been used by Alumex PLC in the last

three years and further to that advantages and disadvantages of those sources have been

discussed. Before concluding the report, it contains details regarding capital budgeting.

Forecasted cash flow statement has been prepared and along with the amounts forecasted

Accounting rate of return, Payback period, and Net present Value and Internal rate of return

has calculated to analyze the proceedings of the project that had planned.

PAGE 9

This comprehensive report has mainly conducted along with the analysis done utilizing the

annual reports of Alumex PLC, which is a leading aluminum product manufacture in Sri

Lanka. Commencing from an introduction given to the recognized organization, then the

importance of using annual reports is discussed in investors’ and employees’ perspectives.

From that analysis it is evident that the company is favorable to invest. Third chapter briefs

the differences between the financial statements of limited companies and other legal entities.

Comparison done in this section comparing the features of financial statements of limited

companies with sole proprietorships and partnerships. The report flows towards most

significant analysis done in the fourth chapter by analyzing the working capital and the

working capital cycle in order to identify the working capital issues faces by the organization.

Suggestions are given in overcoming such issues by handling relevant components. Fifth

chapter is all about sources of finances which have been used by Alumex PLC in the last

three years and further to that advantages and disadvantages of those sources have been

discussed. Before concluding the report, it contains details regarding capital budgeting.

Forecasted cash flow statement has been prepared and along with the amounts forecasted

Accounting rate of return, Payback period, and Net present Value and Internal rate of return

has calculated to analyze the proceedings of the project that had planned.

PAGE 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table of Content

Acknowledgement......................................................................................................................i

Executive summary....................................................................................................................ii

Table of Content.......................................................................................................................iii

List of figures.............................................................................................................................v

List of Tables............................................................................................................................vi

1. Introduction........................................................................................................................1

2. Importance of annual reports to the stakeholders..............................................................2

2.1 Investors’ Perspective..................................................................................................2

2.1.1 Profitability..........................................................................................................2

2.1.2 Company history..................................................................................................2

2.1.3 Type of the company............................................................................................3

2.1.4 Liquidity...............................................................................................................3

2.2 Employees’ perspective...............................................................................................4

2.2.1 Reputation............................................................................................................4

2.2.2 Career growth.......................................................................................................4

2.2.3 Salaries and other benefits...................................................................................4

2.2.4 Training and development...................................................................................4

3. Differences between financial statements of organizations...............................................5

3.1 Limited liability company Vs Sole proprietorship......................................................5

3.2 Limited liability company Vs Partnership...................................................................6

4. Analysis of working capital and working capital cycle.....................................................8

4.1 Working capital (WC) analysis...................................................................................8

4.2 Working capital cycle (WCC) analysis.......................................................................9

4.3 How Alumex PLC can effectively manage the working capital cycle......................11

5. Analysis of sources of finance.........................................................................................13

5.1 Equity........................................................................................................................13

5.2 Liabilities...................................................................................................................13

5.3 Assets.........................................................................................................................15

6. Investment Appraisal.......................................................................................................16

6.1 Projected Cash Flow Statement.................................................................................16

6.1.2 Accounting Rate of Return........................................................................................17

6.1.3 Payback Period..........................................................................................................18

6.1.4 Net Present Value......................................................................................................18

PAGE 9

Acknowledgement......................................................................................................................i

Executive summary....................................................................................................................ii

Table of Content.......................................................................................................................iii

List of figures.............................................................................................................................v

List of Tables............................................................................................................................vi

1. Introduction........................................................................................................................1

2. Importance of annual reports to the stakeholders..............................................................2

2.1 Investors’ Perspective..................................................................................................2

2.1.1 Profitability..........................................................................................................2

2.1.2 Company history..................................................................................................2

2.1.3 Type of the company............................................................................................3

2.1.4 Liquidity...............................................................................................................3

2.2 Employees’ perspective...............................................................................................4

2.2.1 Reputation............................................................................................................4

2.2.2 Career growth.......................................................................................................4

2.2.3 Salaries and other benefits...................................................................................4

2.2.4 Training and development...................................................................................4

3. Differences between financial statements of organizations...............................................5

3.1 Limited liability company Vs Sole proprietorship......................................................5

3.2 Limited liability company Vs Partnership...................................................................6

4. Analysis of working capital and working capital cycle.....................................................8

4.1 Working capital (WC) analysis...................................................................................8

4.2 Working capital cycle (WCC) analysis.......................................................................9

4.3 How Alumex PLC can effectively manage the working capital cycle......................11

5. Analysis of sources of finance.........................................................................................13

5.1 Equity........................................................................................................................13

5.2 Liabilities...................................................................................................................13

5.3 Assets.........................................................................................................................15

6. Investment Appraisal.......................................................................................................16

6.1 Projected Cash Flow Statement.................................................................................16

6.1.2 Accounting Rate of Return........................................................................................17

6.1.3 Payback Period..........................................................................................................18

6.1.4 Net Present Value......................................................................................................18

PAGE 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6.1.3 internal Rate of Return..............................................................................................19

7. Conclusion.......................................................................................................................20

References................................................................................................................................21

Appendix..................................................................................................................................22

List of Tables

Table 1: Profitability ratio analysis of Alumex PLC.................................................................2

Table 2: Financial ratio analysis of Alumex PLC......................................................................3

Table 4: Income statement differences - PLC vs Sole proprietorship.......................................5

Table 5: Differences of statement of financial position - PLC vs Sole proprietorship..............6

Table 6: Differences of income statement - PLC vs Partnership...............................................7

Table 7: Differences of statement of financial position - PLC vs Partnership..........................7

Table 8: Working capital movement of Alumex PLC.............................................................11

Table 9: WCC Analysis of Alumex PLC.................................................................................11

Table 10: Equity of Alumex PLC as source of finance...........................................................13

Table 11: Advantages and disadvantagess of equity...............................................................13

Table 12: Liabilities as sources of finance...............................................................................14

Table 13: Values of Accounting Rate of Return, Payback Period, Net Present Value, Internal Rate of

Return

..................................................................................................................................................14

PAGE 9

7. Conclusion.......................................................................................................................20

References................................................................................................................................21

Appendix..................................................................................................................................22

List of Tables

Table 1: Profitability ratio analysis of Alumex PLC.................................................................2

Table 2: Financial ratio analysis of Alumex PLC......................................................................3

Table 4: Income statement differences - PLC vs Sole proprietorship.......................................5

Table 5: Differences of statement of financial position - PLC vs Sole proprietorship..............6

Table 6: Differences of income statement - PLC vs Partnership...............................................7

Table 7: Differences of statement of financial position - PLC vs Partnership..........................7

Table 8: Working capital movement of Alumex PLC.............................................................11

Table 9: WCC Analysis of Alumex PLC.................................................................................11

Table 10: Equity of Alumex PLC as source of finance...........................................................13

Table 11: Advantages and disadvantagess of equity...............................................................13

Table 12: Liabilities as sources of finance...............................................................................14

Table 13: Values of Accounting Rate of Return, Payback Period, Net Present Value, Internal Rate of

Return

..................................................................................................................................................14

PAGE 9

1. Introduction

Alumex PLC can be recognized as a leading aluminum products manufacturer in Sri Lanka

which was establishment in 1986 as a South Korean-Sri Lankan joint venture. Currently the

company is owned by the Hayleys group and the market has expanded into the international

markets including Europe, USA, Asia and Africa. The company undertakes a comprehensive

offering of architectural, residential and industrial products made available through the

national and retail distribution system, while ensuring the international standards of their

products (Alumex Group.com, 2021). As leading specialists in the manufacture of a

comprehensive range of highly specialized aluminum extrusions, products, and services. To

date it employs approximately 953 employees in all of its operations. Alumex PLC is a

limited Liability company, incorporated in Sri Lanka in 2007.

Alumex is currently conducting their operations based in Sri Lanka, but aggressively market

their product across the globe. They highlight their innovation capacities and product

variations as their key strengths which have led them to acquire a competitive market share.

The company currently holds a market capitalization of LKR 5.69 Bn with 299.30 Mn shares

outstanding (Financial Times, 2020).

The fundamental analysis has been done to compare and contrast the financial performance

of Alumex PLC over the course of last three years. Various theories and formulas used to

analyze the data such as financial ratios, working capital and capital budgeting to get the

desired outcome.

2. Usefulness of Annual report to the stakeholder

“A stakeholder is a party that has an interest in a company and can either affect or be

affected by the business. The primary stakeholders in a typical corporation are its investors,

employees, customers, and suppliers” (Fernando, 2021). With the increasing attention

on corporate social responsibility, the concept has been extended to include communities,

governments, and trade associations as well. An entity's stakeholders can be both internal and

external to the organization.

PAGE 9

Alumex PLC can be recognized as a leading aluminum products manufacturer in Sri Lanka

which was establishment in 1986 as a South Korean-Sri Lankan joint venture. Currently the

company is owned by the Hayleys group and the market has expanded into the international

markets including Europe, USA, Asia and Africa. The company undertakes a comprehensive

offering of architectural, residential and industrial products made available through the

national and retail distribution system, while ensuring the international standards of their

products (Alumex Group.com, 2021). As leading specialists in the manufacture of a

comprehensive range of highly specialized aluminum extrusions, products, and services. To

date it employs approximately 953 employees in all of its operations. Alumex PLC is a

limited Liability company, incorporated in Sri Lanka in 2007.

Alumex is currently conducting their operations based in Sri Lanka, but aggressively market

their product across the globe. They highlight their innovation capacities and product

variations as their key strengths which have led them to acquire a competitive market share.

The company currently holds a market capitalization of LKR 5.69 Bn with 299.30 Mn shares

outstanding (Financial Times, 2020).

The fundamental analysis has been done to compare and contrast the financial performance

of Alumex PLC over the course of last three years. Various theories and formulas used to

analyze the data such as financial ratios, working capital and capital budgeting to get the

desired outcome.

2. Usefulness of Annual report to the stakeholder

“A stakeholder is a party that has an interest in a company and can either affect or be

affected by the business. The primary stakeholders in a typical corporation are its investors,

employees, customers, and suppliers” (Fernando, 2021). With the increasing attention

on corporate social responsibility, the concept has been extended to include communities,

governments, and trade associations as well. An entity's stakeholders can be both internal and

external to the organization.

PAGE 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

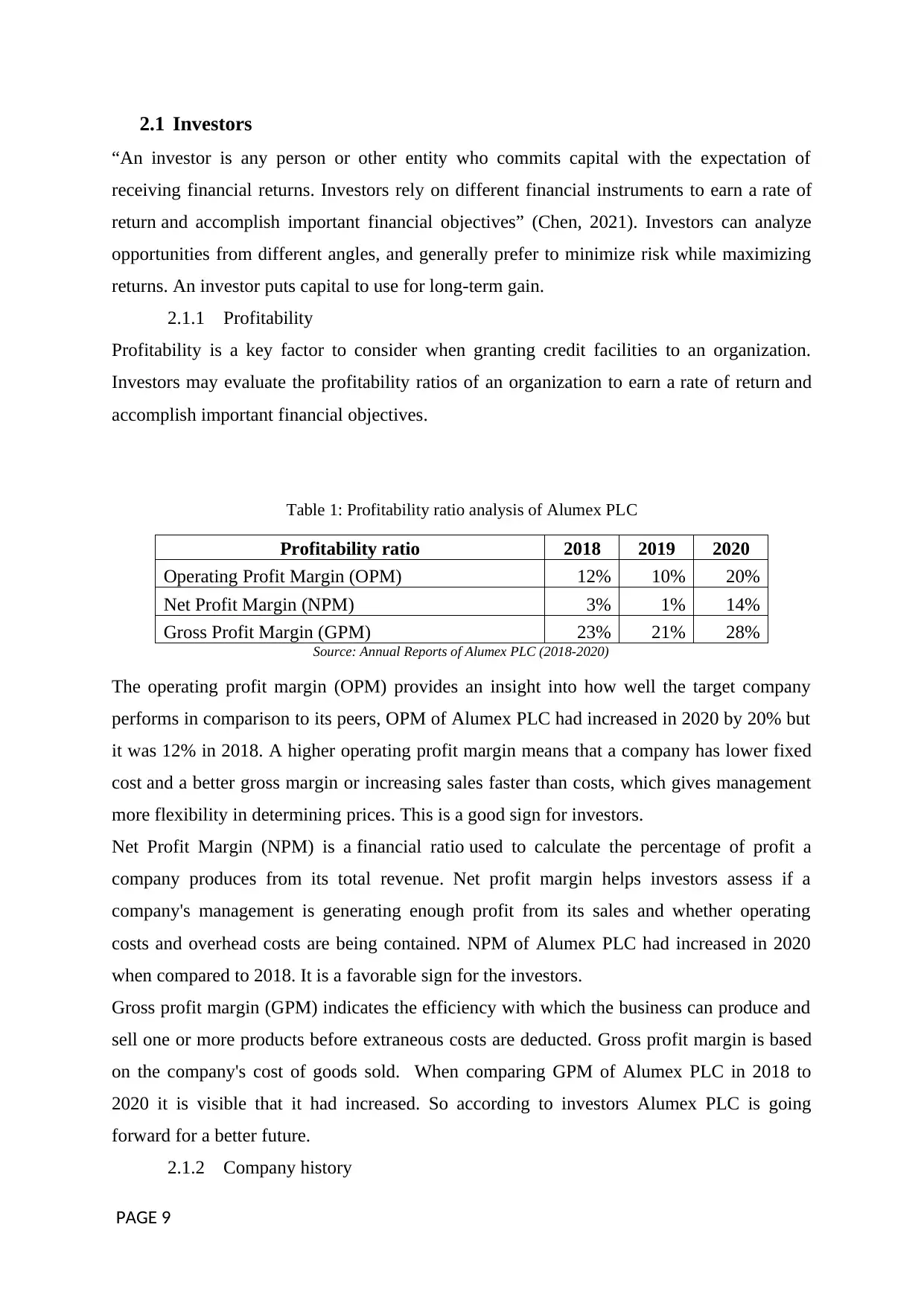

2.1 Investors

“An investor is any person or other entity who commits capital with the expectation of

receiving financial returns. Investors rely on different financial instruments to earn a rate of

return and accomplish important financial objectives” (Chen, 2021). Investors can analyze

opportunities from different angles, and generally prefer to minimize risk while maximizing

returns. An investor puts capital to use for long-term gain.

2.1.1 Profitability

Profitability is a key factor to consider when granting credit facilities to an organization.

Investors may evaluate the profitability ratios of an organization to earn a rate of return and

accomplish important financial objectives.

Table 1: Profitability ratio analysis of Alumex PLC

Profitability ratio 2018 2019 2020

Operating Profit Margin (OPM) 12% 10% 20%

Net Profit Margin (NPM) 3% 1% 14%

Gross Profit Margin (GPM) 23% 21% 28%

Source: Annual Reports of Alumex PLC (2018-2020)

The operating profit margin (OPM) provides an insight into how well the target company

performs in comparison to its peers, OPM of Alumex PLC had increased in 2020 by 20% but

it was 12% in 2018. A higher operating profit margin means that a company has lower fixed

cost and a better gross margin or increasing sales faster than costs, which gives management

more flexibility in determining prices. This is a good sign for investors.

Net Profit Margin (NPM) is a financial ratio used to calculate the percentage of profit a

company produces from its total revenue. Net profit margin helps investors assess if a

company's management is generating enough profit from its sales and whether operating

costs and overhead costs are being contained. NPM of Alumex PLC had increased in 2020

when compared to 2018. It is a favorable sign for the investors.

Gross profit margin (GPM) indicates the efficiency with which the business can produce and

sell one or more products before extraneous costs are deducted. Gross profit margin is based

on the company's cost of goods sold. When comparing GPM of Alumex PLC in 2018 to

2020 it is visible that it had increased. So according to investors Alumex PLC is going

forward for a better future.

2.1.2 Company history

PAGE 9

“An investor is any person or other entity who commits capital with the expectation of

receiving financial returns. Investors rely on different financial instruments to earn a rate of

return and accomplish important financial objectives” (Chen, 2021). Investors can analyze

opportunities from different angles, and generally prefer to minimize risk while maximizing

returns. An investor puts capital to use for long-term gain.

2.1.1 Profitability

Profitability is a key factor to consider when granting credit facilities to an organization.

Investors may evaluate the profitability ratios of an organization to earn a rate of return and

accomplish important financial objectives.

Table 1: Profitability ratio analysis of Alumex PLC

Profitability ratio 2018 2019 2020

Operating Profit Margin (OPM) 12% 10% 20%

Net Profit Margin (NPM) 3% 1% 14%

Gross Profit Margin (GPM) 23% 21% 28%

Source: Annual Reports of Alumex PLC (2018-2020)

The operating profit margin (OPM) provides an insight into how well the target company

performs in comparison to its peers, OPM of Alumex PLC had increased in 2020 by 20% but

it was 12% in 2018. A higher operating profit margin means that a company has lower fixed

cost and a better gross margin or increasing sales faster than costs, which gives management

more flexibility in determining prices. This is a good sign for investors.

Net Profit Margin (NPM) is a financial ratio used to calculate the percentage of profit a

company produces from its total revenue. Net profit margin helps investors assess if a

company's management is generating enough profit from its sales and whether operating

costs and overhead costs are being contained. NPM of Alumex PLC had increased in 2020

when compared to 2018. It is a favorable sign for the investors.

Gross profit margin (GPM) indicates the efficiency with which the business can produce and

sell one or more products before extraneous costs are deducted. Gross profit margin is based

on the company's cost of goods sold. When comparing GPM of Alumex PLC in 2018 to

2020 it is visible that it had increased. So according to investors Alumex PLC is going

forward for a better future.

2.1.2 Company history

PAGE 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Considering a company’s history, assists the investors to get an assurance regarding its

establishment and reputation when making decisions in financing the firm. Being a firm in

the industry for over 30 years,

2.1.3 Type of the company

Being the local market leader of aluminum products manufacturing, company has a huge

reputation in both domestic and global markets. Since Alumex’s export market expanded to

most of the European and Asian countries, investors may assume that the demand for the

products is well established.

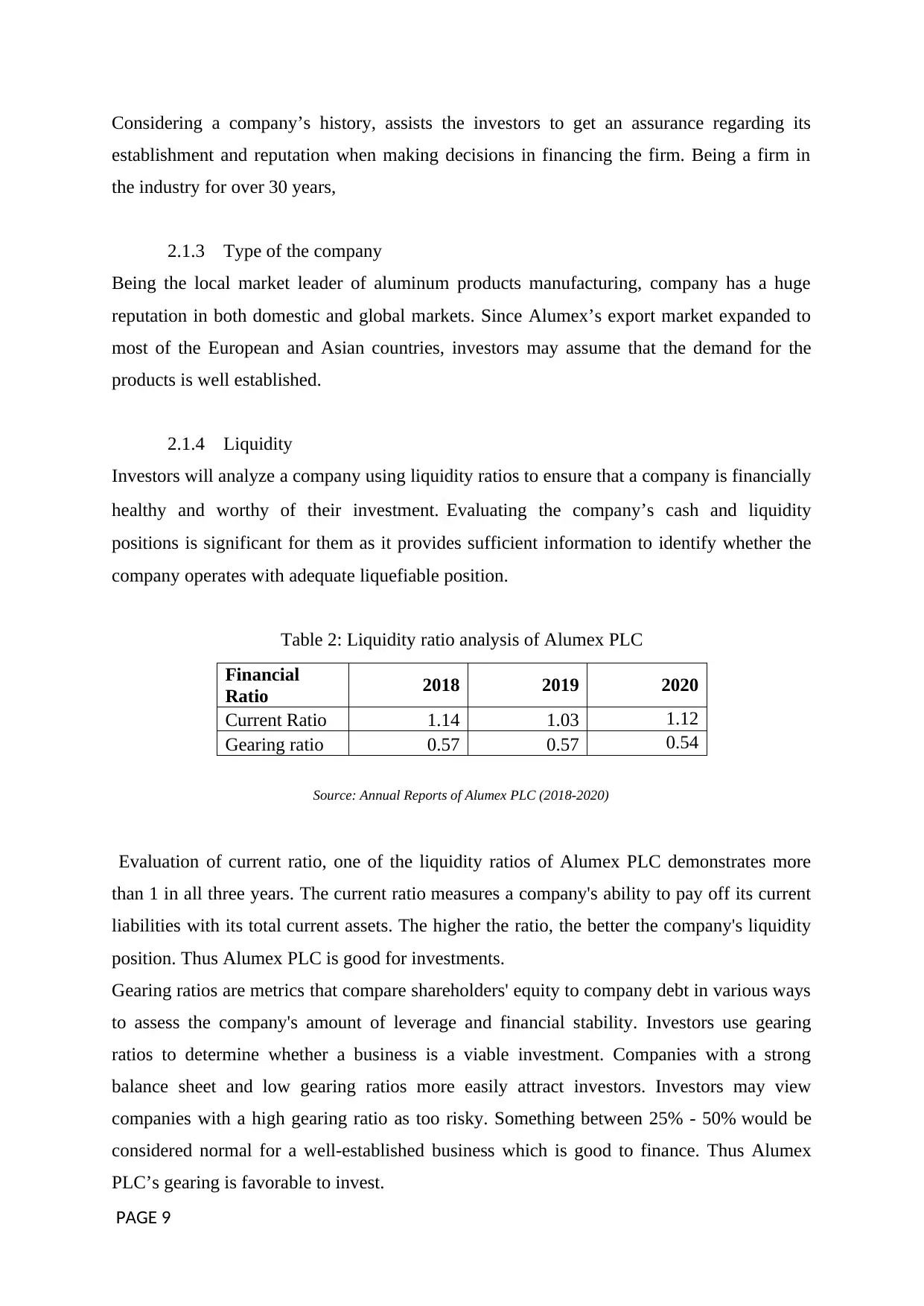

2.1.4 Liquidity

Investors will analyze a company using liquidity ratios to ensure that a company is financially

healthy and worthy of their investment. Evaluating the company’s cash and liquidity

positions is significant for them as it provides sufficient information to identify whether the

company operates with adequate liquefiable position.

Table 2: Liquidity ratio analysis of Alumex PLC

Source: Annual Reports of Alumex PLC (2018-2020)

Evaluation of current ratio, one of the liquidity ratios of Alumex PLC demonstrates more

than 1 in all three years. The current ratio measures a company's ability to pay off its current

liabilities with its total current assets. The higher the ratio, the better the company's liquidity

position. Thus Alumex PLC is good for investments.

Gearing ratios are metrics that compare shareholders' equity to company debt in various ways

to assess the company's amount of leverage and financial stability. Investors use gearing

ratios to determine whether a business is a viable investment. Companies with a strong

balance sheet and low gearing ratios more easily attract investors. Investors may view

companies with a high gearing ratio as too risky. Something between 25% - 50% would be

considered normal for a well-established business which is good to finance. Thus Alumex

PLC’s gearing is favorable to invest.

PAGE 9

Financial

Ratio 2018 2019 2020

Current Ratio 1.14 1.03 1.12

Gearing ratio 0.57 0.57 0.54

establishment and reputation when making decisions in financing the firm. Being a firm in

the industry for over 30 years,

2.1.3 Type of the company

Being the local market leader of aluminum products manufacturing, company has a huge

reputation in both domestic and global markets. Since Alumex’s export market expanded to

most of the European and Asian countries, investors may assume that the demand for the

products is well established.

2.1.4 Liquidity

Investors will analyze a company using liquidity ratios to ensure that a company is financially

healthy and worthy of their investment. Evaluating the company’s cash and liquidity

positions is significant for them as it provides sufficient information to identify whether the

company operates with adequate liquefiable position.

Table 2: Liquidity ratio analysis of Alumex PLC

Source: Annual Reports of Alumex PLC (2018-2020)

Evaluation of current ratio, one of the liquidity ratios of Alumex PLC demonstrates more

than 1 in all three years. The current ratio measures a company's ability to pay off its current

liabilities with its total current assets. The higher the ratio, the better the company's liquidity

position. Thus Alumex PLC is good for investments.

Gearing ratios are metrics that compare shareholders' equity to company debt in various ways

to assess the company's amount of leverage and financial stability. Investors use gearing

ratios to determine whether a business is a viable investment. Companies with a strong

balance sheet and low gearing ratios more easily attract investors. Investors may view

companies with a high gearing ratio as too risky. Something between 25% - 50% would be

considered normal for a well-established business which is good to finance. Thus Alumex

PLC’s gearing is favorable to invest.

PAGE 9

Financial

Ratio 2018 2019 2020

Current Ratio 1.14 1.03 1.12

Gearing ratio 0.57 0.57 0.54

2.2 Employees

According to the oxford dictionary (2021), employee is a person employed for wages or

salary, especially at non-executive level. Every employee is expecting a secured employment

where they can get groomed, motivated and developed in their career. Employees also are

often shareholders. So, like other shareholders, these employees can use the annual report to

help gauge their investment in the company. Accordingly, they’ll consider some factors when

choosing their employer.

2.2.1 Reputation

Being the market leader, a well-built reputation is available for Alumex with a considerable

market share over 50%. It is a fully-integrated aluminum extrusions manufacturer since the

1986. Further, Alumex is the first Company in the Sri Lankan and the South Asian region to

be accredited with both these international certifications. Company is leading specialists in

the manufacture of a comprehensive range of highly specialized aluminum extrusions,

products, and services.

2.2.2 Career growth

According to the annual reports, “HR policies and strategies including recruitment, wages/

salaries, benefits, promotions and increments are solely based on merit.” Alumex follows the

performance evaluation process when considering promotion opportunities. Since, the firm

involve in manufacturing products which has more industrial value, attention is given to

acquire more skilled employees and paths are created to get their skills further developed

inside the organization by attending to relevant training programs. ‘Balance score card

method’ is used to evaluate the performance of executive and clerical supervisory grade

employees.

2.2.3 Salaries and other benefits

As stated in the 2020-2021 annual report, company extend comprehensive financial and non-

financial welfare benefits to all permanent employees. In monetized terms, we spent

Rs. 841 million to provide these benefits along with Rs. 525 million as salaries and

wages. A cost of living allowance, production incentive allowance, attendance allowances,

shift allowance, shift productivity bonuses, etc included for nonexecutive employees and the

company has recently introduced a production incentive mechanism as well.

PAGE 9

According to the oxford dictionary (2021), employee is a person employed for wages or

salary, especially at non-executive level. Every employee is expecting a secured employment

where they can get groomed, motivated and developed in their career. Employees also are

often shareholders. So, like other shareholders, these employees can use the annual report to

help gauge their investment in the company. Accordingly, they’ll consider some factors when

choosing their employer.

2.2.1 Reputation

Being the market leader, a well-built reputation is available for Alumex with a considerable

market share over 50%. It is a fully-integrated aluminum extrusions manufacturer since the

1986. Further, Alumex is the first Company in the Sri Lankan and the South Asian region to

be accredited with both these international certifications. Company is leading specialists in

the manufacture of a comprehensive range of highly specialized aluminum extrusions,

products, and services.

2.2.2 Career growth

According to the annual reports, “HR policies and strategies including recruitment, wages/

salaries, benefits, promotions and increments are solely based on merit.” Alumex follows the

performance evaluation process when considering promotion opportunities. Since, the firm

involve in manufacturing products which has more industrial value, attention is given to

acquire more skilled employees and paths are created to get their skills further developed

inside the organization by attending to relevant training programs. ‘Balance score card

method’ is used to evaluate the performance of executive and clerical supervisory grade

employees.

2.2.3 Salaries and other benefits

As stated in the 2020-2021 annual report, company extend comprehensive financial and non-

financial welfare benefits to all permanent employees. In monetized terms, we spent

Rs. 841 million to provide these benefits along with Rs. 525 million as salaries and

wages. A cost of living allowance, production incentive allowance, attendance allowances,

shift allowance, shift productivity bonuses, etc included for nonexecutive employees and the

company has recently introduced a production incentive mechanism as well.

PAGE 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2.4 Training and development

Proper training and development program mechanism can be seen within the organization

where they have focused on skill development, leadership, engineering, first aid, fire

trainings, quality assurance and health and safety. According to annual reports, Alumex PLC

give their employees an ‘equal opportunity’ to develop their careers.

Average training hours were pre-determined based on the employment category and post-

training assessment mechanism is available to measure effectiveness of the training.

Company Extend strategic training opportunities and encourage and offer funding to

employees to take up further studies. Employees will positively evaluate these as advantages.

3. Differences between the financial statements

Based on the legal entity type, organizations can be categorized and preparing financial

statements is getting vary depend on its legal entity type. Alumex PLC is a limited

Liability company, incorporated in Sri Lanka in 2007.

A comparison will be conducted in this chapter between the financial statements of Public

Limited companies with sole proprietorships and partnerships.

3.1 Public Limited company Vs Sole proprietorship

Table 4: Differences between Income Statement and Balance Sheet of PLC and Proprietorship.

Income statement

Attribute Public Limited Company Proprietorship

Profit Net profit is considered as the profit

earned by the company after

meeting all the expenses such as

interests and taxes. Operating profit

is obtained before deducting

interests and taxes.

Net profit and operating profit are

considered the same.

Dividends Dividends are distributed among

ordinary shareholders of a company.

PLC dispenses retained earnings

Stocks are not issued and dividends

are not being paid. Profit earned is

entirely owned by the owner.

PAGE 9

Proper training and development program mechanism can be seen within the organization

where they have focused on skill development, leadership, engineering, first aid, fire

trainings, quality assurance and health and safety. According to annual reports, Alumex PLC

give their employees an ‘equal opportunity’ to develop their careers.

Average training hours were pre-determined based on the employment category and post-

training assessment mechanism is available to measure effectiveness of the training.

Company Extend strategic training opportunities and encourage and offer funding to

employees to take up further studies. Employees will positively evaluate these as advantages.

3. Differences between the financial statements

Based on the legal entity type, organizations can be categorized and preparing financial

statements is getting vary depend on its legal entity type. Alumex PLC is a limited

Liability company, incorporated in Sri Lanka in 2007.

A comparison will be conducted in this chapter between the financial statements of Public

Limited companies with sole proprietorships and partnerships.

3.1 Public Limited company Vs Sole proprietorship

Table 4: Differences between Income Statement and Balance Sheet of PLC and Proprietorship.

Income statement

Attribute Public Limited Company Proprietorship

Profit Net profit is considered as the profit

earned by the company after

meeting all the expenses such as

interests and taxes. Operating profit

is obtained before deducting

interests and taxes.

Net profit and operating profit are

considered the same.

Dividends Dividends are distributed among

ordinary shareholders of a company.

PLC dispenses retained earnings

Stocks are not issued and dividends

are not being paid. Profit earned is

entirely owned by the owner.

PAGE 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through an announcement of a per-

share payout after the company has

paid income taxes.

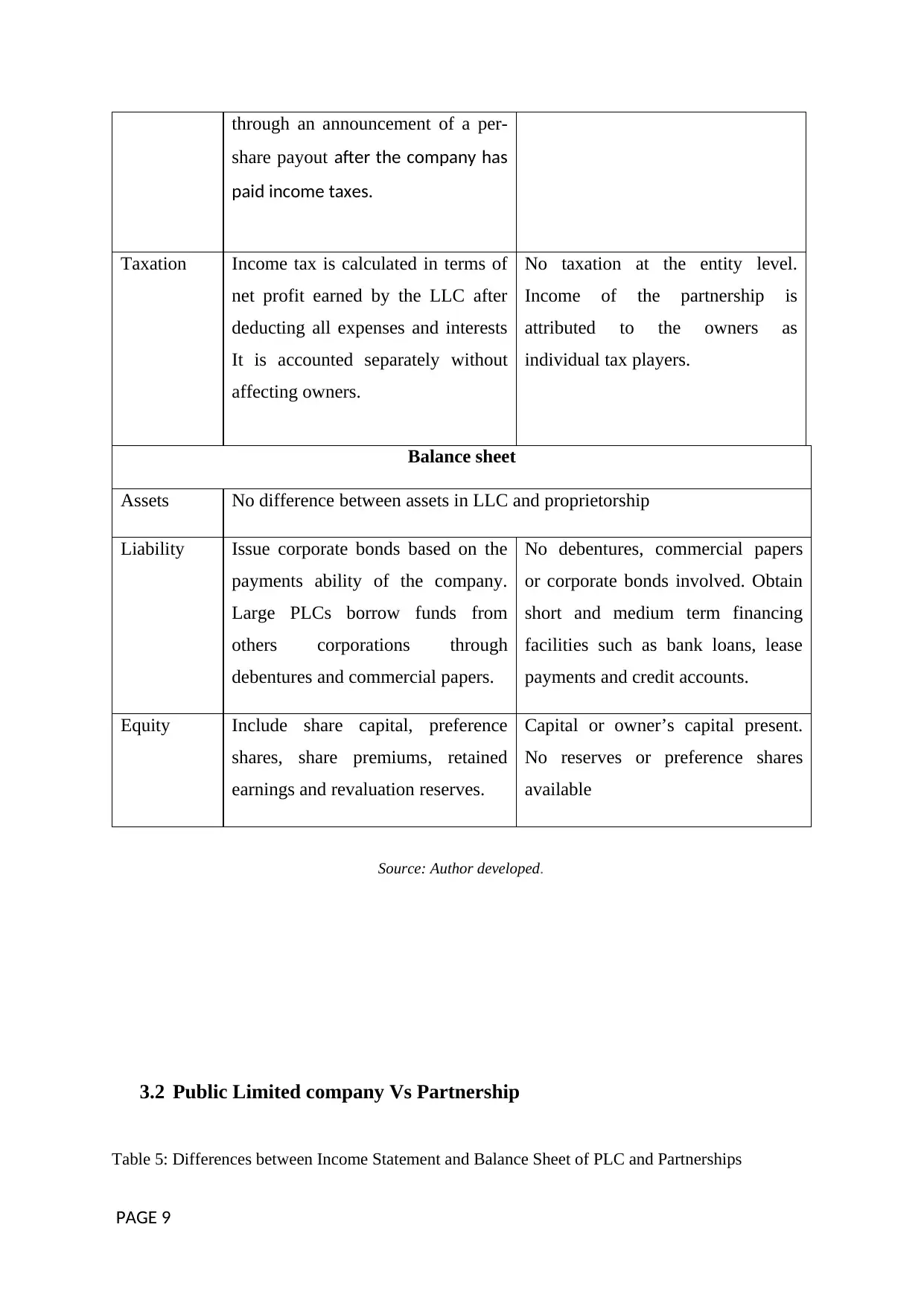

Taxation Income tax is calculated in terms of

net profit earned by the LLC after

deducting all expenses and interests

It is accounted separately without

affecting owners.

No taxation at the entity level.

Income of the partnership is

attributed to the owners as

individual tax players.

Balance sheet

Assets No difference between assets in LLC and proprietorship

Liability Issue corporate bonds based on the

payments ability of the company.

Large PLCs borrow funds from

others corporations through

debentures and commercial papers.

No debentures, commercial papers

or corporate bonds involved. Obtain

short and medium term financing

facilities such as bank loans, lease

payments and credit accounts.

Equity Include share capital, preference

shares, share premiums, retained

earnings and revaluation reserves.

Capital or owner’s capital present.

No reserves or preference shares

available

Source: Author developed.

3.2 Public Limited company Vs Partnership

Table 5: Differences between Income Statement and Balance Sheet of PLC and Partnerships

PAGE 9

share payout after the company has

paid income taxes.

Taxation Income tax is calculated in terms of

net profit earned by the LLC after

deducting all expenses and interests

It is accounted separately without

affecting owners.

No taxation at the entity level.

Income of the partnership is

attributed to the owners as

individual tax players.

Balance sheet

Assets No difference between assets in LLC and proprietorship

Liability Issue corporate bonds based on the

payments ability of the company.

Large PLCs borrow funds from

others corporations through

debentures and commercial papers.

No debentures, commercial papers

or corporate bonds involved. Obtain

short and medium term financing

facilities such as bank loans, lease

payments and credit accounts.

Equity Include share capital, preference

shares, share premiums, retained

earnings and revaluation reserves.

Capital or owner’s capital present.

No reserves or preference shares

available

Source: Author developed.

3.2 Public Limited company Vs Partnership

Table 5: Differences between Income Statement and Balance Sheet of PLC and Partnerships

PAGE 9

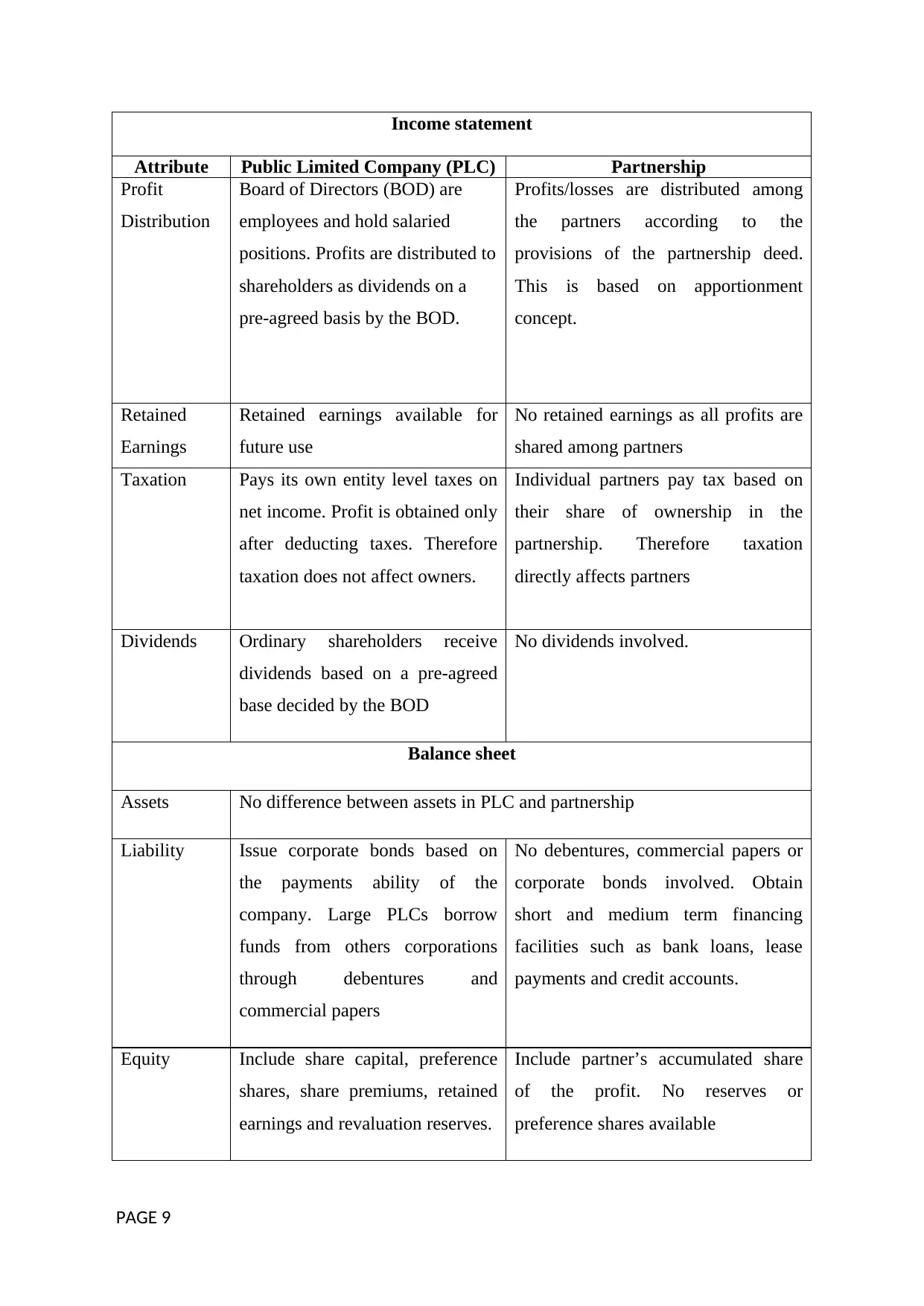

Income statement

Attribute Public Limited Company (PLC) Partnership

Profit

Distribution

Board of Directors (BOD) are

employees and hold salaried

positions. Profits are distributed to

shareholders as dividends on a

pre-agreed basis by the BOD.

Profits/losses are distributed among

the partners according to the

provisions of the partnership deed.

This is based on apportionment

concept.

Retained

Earnings

Retained earnings available for

future use

No retained earnings as all profits are

shared among partners

Taxation Pays its own entity level taxes on

net income. Profit is obtained only

after deducting taxes. Therefore

taxation does not affect owners.

Individual partners pay tax based on

their share of ownership in the

partnership. Therefore taxation

directly affects partners

Dividends Ordinary shareholders receive

dividends based on a pre-agreed

base decided by the BOD

No dividends involved.

Balance sheet

Assets No difference between assets in PLC and partnership

Liability Issue corporate bonds based on

the payments ability of the

company. Large PLCs borrow

funds from others corporations

through debentures and

commercial papers

No debentures, commercial papers or

corporate bonds involved. Obtain

short and medium term financing

facilities such as bank loans, lease

payments and credit accounts.

Equity Include share capital, preference

shares, share premiums, retained

earnings and revaluation reserves.

Include partner’s accumulated share

of the profit. No reserves or

preference shares available

PAGE 9

Attribute Public Limited Company (PLC) Partnership

Profit

Distribution

Board of Directors (BOD) are

employees and hold salaried

positions. Profits are distributed to

shareholders as dividends on a

pre-agreed basis by the BOD.

Profits/losses are distributed among

the partners according to the

provisions of the partnership deed.

This is based on apportionment

concept.

Retained

Earnings

Retained earnings available for

future use

No retained earnings as all profits are

shared among partners

Taxation Pays its own entity level taxes on

net income. Profit is obtained only

after deducting taxes. Therefore

taxation does not affect owners.

Individual partners pay tax based on

their share of ownership in the

partnership. Therefore taxation

directly affects partners

Dividends Ordinary shareholders receive

dividends based on a pre-agreed

base decided by the BOD

No dividends involved.

Balance sheet

Assets No difference between assets in PLC and partnership

Liability Issue corporate bonds based on

the payments ability of the

company. Large PLCs borrow

funds from others corporations

through debentures and

commercial papers

No debentures, commercial papers or

corporate bonds involved. Obtain

short and medium term financing

facilities such as bank loans, lease

payments and credit accounts.

Equity Include share capital, preference

shares, share premiums, retained

earnings and revaluation reserves.

Include partner’s accumulated share

of the profit. No reserves or

preference shares available

PAGE 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.