Financial Performance Analysis: Variance Analysis and Budgeting

VerifiedAdded on 2022/12/28

|13

|2787

|36

Homework Assignment

AI Summary

This assignment analyzes financial performance, covering various aspects of costing, variance analysis, and budgeting. The first question delves into activity-based costing (ABC) versus absorption costing, including calculations of overhead allocation and profit analysis for different products (lipstick, lip balm, and lip gloss). It also discusses the role of sensitivity analysis in managing uncertainties. The second question focuses on variance analysis, calculating material usage, mix, and yield variances. It also critiques the current system of calculating and reporting variances for assessing production manager performance. The final question explores zero-based budgeting (ZBB) and its role in planning and coordination, contrasting it with incremental budgeting.

Financial performance (online exam)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................6

Question 3........................................................................................................................................8

Question 1........................................................................................................................................3

Question 2........................................................................................................................................6

Question 3........................................................................................................................................8

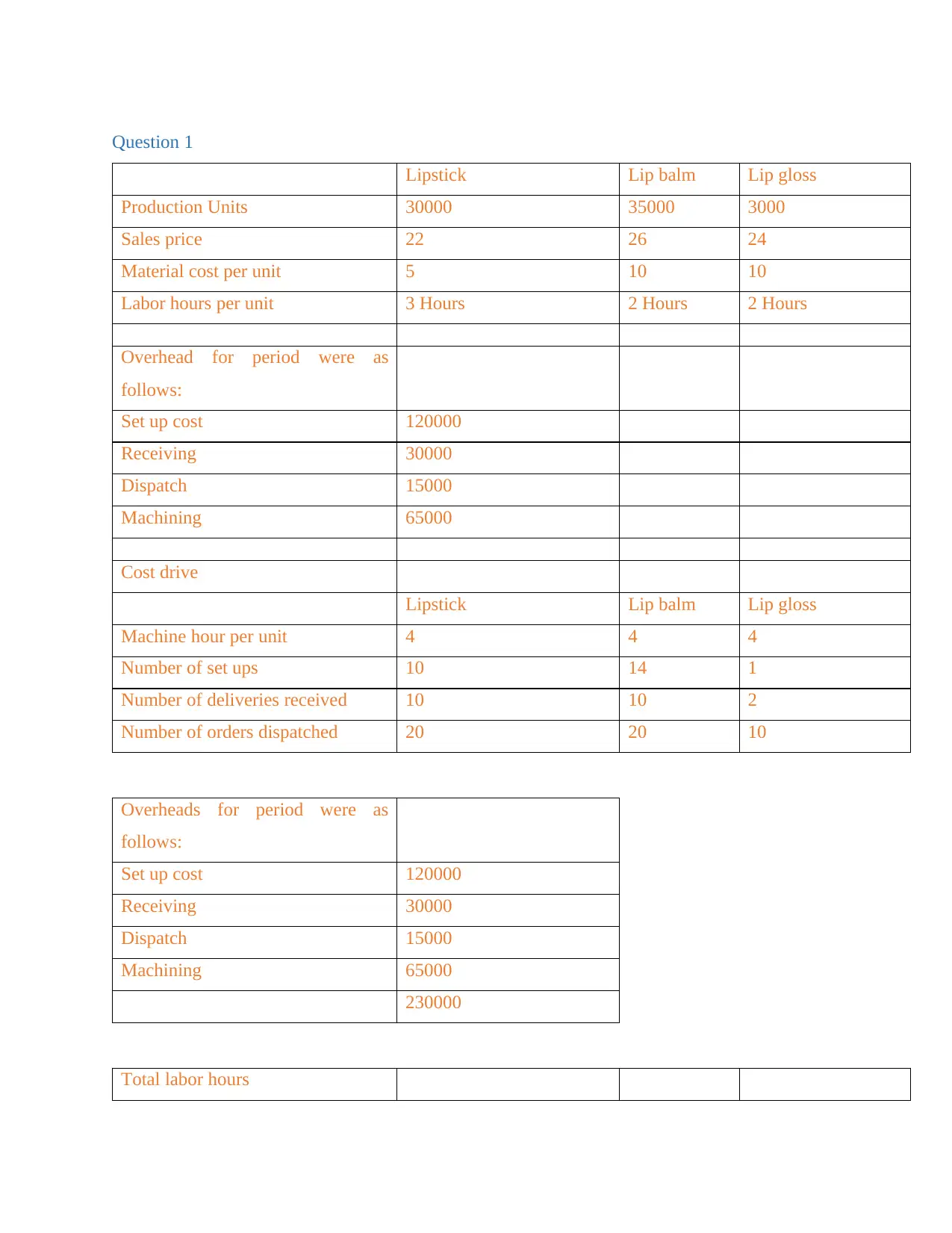

Question 1

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Sales price 22 26 24

Material cost per unit 5 10 10

Labor hours per unit 3 Hours 2 Hours 2 Hours

Overhead for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

Cost drive

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Number of set ups 10 14 1

Number of deliveries received 10 10 2

Number of orders dispatched 20 20 10

Overheads for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

230000

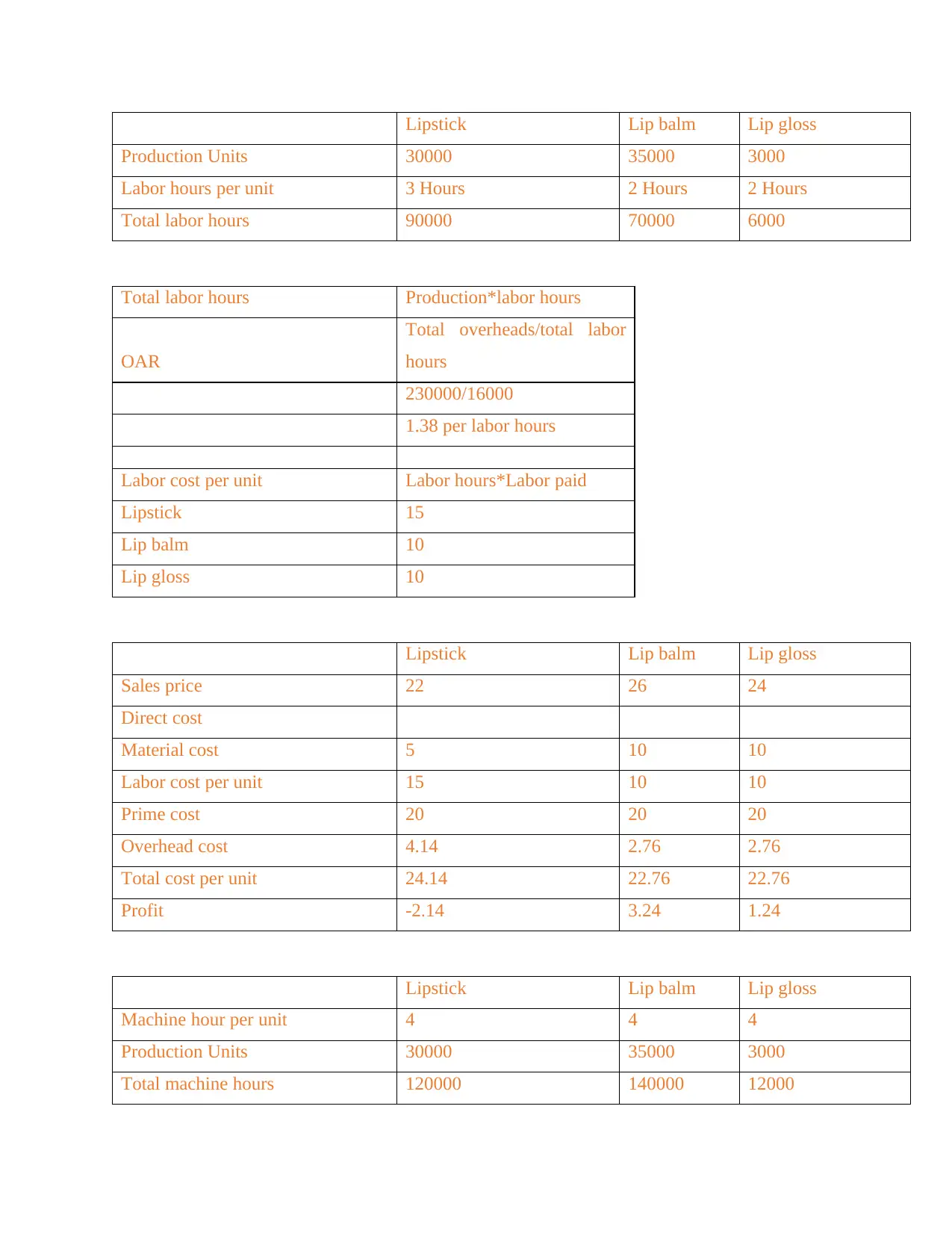

Total labor hours

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Sales price 22 26 24

Material cost per unit 5 10 10

Labor hours per unit 3 Hours 2 Hours 2 Hours

Overhead for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

Cost drive

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Number of set ups 10 14 1

Number of deliveries received 10 10 2

Number of orders dispatched 20 20 10

Overheads for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

230000

Total labor hours

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Labor hours per unit 3 Hours 2 Hours 2 Hours

Total labor hours 90000 70000 6000

Total labor hours Production*labor hours

OAR

Total overheads/total labor

hours

230000/16000

1.38 per labor hours

Labor cost per unit Labor hours*Labor paid

Lipstick 15

Lip balm 10

Lip gloss 10

Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overhead cost 4.14 2.76 2.76

Total cost per unit 24.14 22.76 22.76

Profit -2.14 3.24 1.24

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Production Units 30000 35000 3000

Total machine hours 120000 140000 12000

Production Units 30000 35000 3000

Labor hours per unit 3 Hours 2 Hours 2 Hours

Total labor hours 90000 70000 6000

Total labor hours Production*labor hours

OAR

Total overheads/total labor

hours

230000/16000

1.38 per labor hours

Labor cost per unit Labor hours*Labor paid

Lipstick 15

Lip balm 10

Lip gloss 10

Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overhead cost 4.14 2.76 2.76

Total cost per unit 24.14 22.76 22.76

Profit -2.14 3.24 1.24

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Production Units 30000 35000 3000

Total machine hours 120000 140000 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OAR

Machining/Total machine

hours

65000/272000

0.238

Lipstick

Lip

balm

Lip

gloss

Tot

al

OAR/Cost

driver

Setup 10 14 1 25 120000/25 4800

Deliveries

received 10 10 2 22 30000/22

1363.

63

Orders

dispatched 20 20 10 50 15000/50 300

Overhea

ds Appropriation

OAR/cost

driver Total

Lipstic

k

Lip

balm

Lip

gloss

Set up

cost Number of set ups 4800 120000 48000 67200 4800

Receivi

ng Number of deliveries 1363.63 30000

13636.

36

13636.3

6

2727.2

7

Dispatc

h

Number of orders

dispatched 300 15000 6000 6000 3000

Machini

ng Machine hours 0.238 65000 28560 33320 2856

Total

96196.

36

120156.

36

13383.

27

Number of

units 30000 35000 3000

Machining/Total machine

hours

65000/272000

0.238

Lipstick

Lip

balm

Lip

gloss

Tot

al

OAR/Cost

driver

Setup 10 14 1 25 120000/25 4800

Deliveries

received 10 10 2 22 30000/22

1363.

63

Orders

dispatched 20 20 10 50 15000/50 300

Overhea

ds Appropriation

OAR/cost

driver Total

Lipstic

k

Lip

balm

Lip

gloss

Set up

cost Number of set ups 4800 120000 48000 67200 4800

Receivi

ng Number of deliveries 1363.63 30000

13636.

36

13636.3

6

2727.2

7

Dispatc

h

Number of orders

dispatched 300 15000 6000 6000 3000

Machini

ng Machine hours 0.238 65000 28560 33320 2856

Total

96196.

36

120156.

36

13383.

27

Number of

units 30000 35000 3000

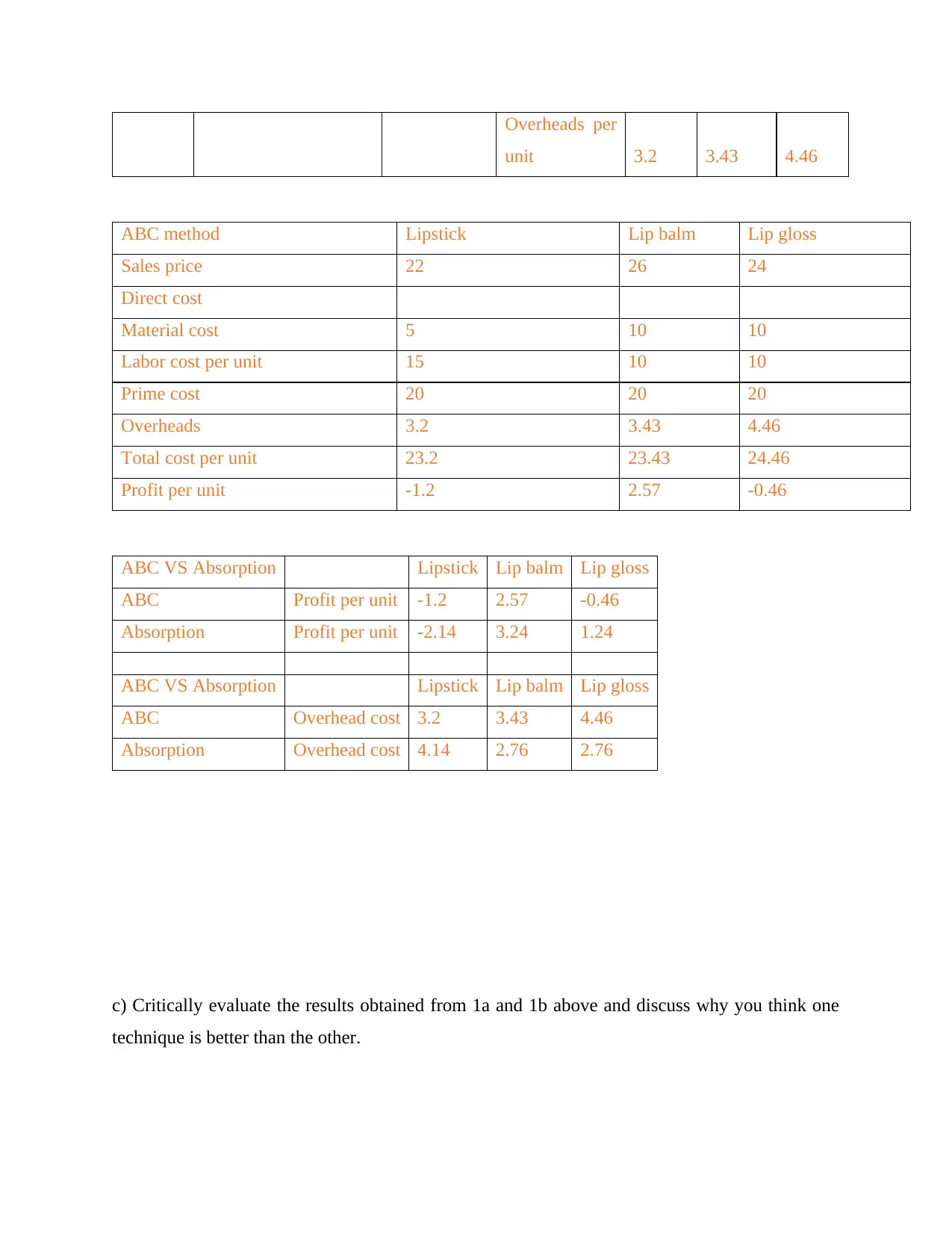

Overheads per

unit 3.2 3.43 4.46

ABC method Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overheads 3.2 3.43 4.46

Total cost per unit 23.2 23.43 24.46

Profit per unit -1.2 2.57 -0.46

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Profit per unit -1.2 2.57 -0.46

Absorption Profit per unit -2.14 3.24 1.24

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Overhead cost 3.2 3.43 4.46

Absorption Overhead cost 4.14 2.76 2.76

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.

unit 3.2 3.43 4.46

ABC method Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overheads 3.2 3.43 4.46

Total cost per unit 23.2 23.43 24.46

Profit per unit -1.2 2.57 -0.46

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Profit per unit -1.2 2.57 -0.46

Absorption Profit per unit -2.14 3.24 1.24

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Overhead cost 3.2 3.43 4.46

Absorption Overhead cost 4.14 2.76 2.76

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the grounds of the aforementioned estimate, it can be concluded that the two methods include

various kinds of things and amounts. As long as there is a distinct production volume. The cost

of absorption is 4.14, 2.76 and 2.76 for three goods. Although the cost per unit benefit in ABC is

3.2, 3.43 and 4.46 overall.

Absorption costing- Absorption costs are a management accounting scheme that collects all the

costs involved with the purchase of a single commodity, also called total absorption costs. This

approach is used to account for direct and indirect expenses such as direct supplies, direct labor,

leases and insurance (Miroshnychenko, Barontini and Testa, 2017). Costs of absorption are

required for variable costing under commonly agreed GAAPs. Absorption costing is also

recognized as complete costing, since it covers all costs involved with output. Variable costs are

associated labor and material costs. Fixed costs include leasing, protection, and benefits. Semi-

variable costs include power charges for the facility. Thus, at maximum discount, all prices are

borne by the manufacturer regardless of the product being offered. Absorption costing allows

reliable accounting of the cost of production, as opposed to contingent costing, which takes into

account only variable costs. The system of costing method allows the recording of high benefit

for a high valuation of the closed inventory. This is because the expense of output is completely

consumed.

ABC costing- Costing based on operation is a costing approach that defines operational

operations and assigns all goods and resources to the expense of each activity in accordance with

the real consumption for each one. This model thus attributes more administrative costs to direct

costs than traditional costs (Wang and Sarkis, 2017). This costing accounting approach considers

the link between prices, overhead operations and the goods produced and applies indirect costs

less arbitrarily to the products than typical costs. However, it is impossible to delegate a

commodity to secondary charges, such as marketing and workplace compensation. Activity-

based costing has risen in value in recent years, as (1) direct labor rates have risen dramatically,

(2) direct labor cost may not equate with efficient labor hours or direct operating hours, (3)

market share and consumer demand uniqueness have decreased, and (4) some manufactured in

large quantities, whereas others are produced in big quantity.

d) Discuss how sensitivity analysis helps managers to cope with uncertainties.

various kinds of things and amounts. As long as there is a distinct production volume. The cost

of absorption is 4.14, 2.76 and 2.76 for three goods. Although the cost per unit benefit in ABC is

3.2, 3.43 and 4.46 overall.

Absorption costing- Absorption costs are a management accounting scheme that collects all the

costs involved with the purchase of a single commodity, also called total absorption costs. This

approach is used to account for direct and indirect expenses such as direct supplies, direct labor,

leases and insurance (Miroshnychenko, Barontini and Testa, 2017). Costs of absorption are

required for variable costing under commonly agreed GAAPs. Absorption costing is also

recognized as complete costing, since it covers all costs involved with output. Variable costs are

associated labor and material costs. Fixed costs include leasing, protection, and benefits. Semi-

variable costs include power charges for the facility. Thus, at maximum discount, all prices are

borne by the manufacturer regardless of the product being offered. Absorption costing allows

reliable accounting of the cost of production, as opposed to contingent costing, which takes into

account only variable costs. The system of costing method allows the recording of high benefit

for a high valuation of the closed inventory. This is because the expense of output is completely

consumed.

ABC costing- Costing based on operation is a costing approach that defines operational

operations and assigns all goods and resources to the expense of each activity in accordance with

the real consumption for each one. This model thus attributes more administrative costs to direct

costs than traditional costs (Wang and Sarkis, 2017). This costing accounting approach considers

the link between prices, overhead operations and the goods produced and applies indirect costs

less arbitrarily to the products than typical costs. However, it is impossible to delegate a

commodity to secondary charges, such as marketing and workplace compensation. Activity-

based costing has risen in value in recent years, as (1) direct labor rates have risen dramatically,

(2) direct labor cost may not equate with efficient labor hours or direct operating hours, (3)

market share and consumer demand uniqueness have decreased, and (4) some manufactured in

large quantities, whereas others are produced in big quantity.

d) Discuss how sensitivity analysis helps managers to cope with uncertainties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A study of sensibilities defines how various values of an independent variable control, under

certain conditions, a particular variable. Analysis of sensitivity is a business plan that specifies

how target parameters are influenced based on changes in additional variability’s called input

variables (Galant and Cadez, 2017). This paradigm is also known as what-if research or

simulation analysis. It is a method of estimating the result of a decision given a number of

variables. An analysis tool can decide how the variations in a variable influence the result by

generating a specified set of variables. When sensitivity analysis is carried out, the objective and

feedback variables – or independent and dependent variables are thoroughly analyzed. The

analyst looks at how the variables change and how the input variable influences the goal.

Review of sensitivity could be used to forecast public firms' share prices. Including the business

profits, numbers of stocks, debt/equity ratios and numbers of competing players in the industry,

some of the factors that influence stock prices. By choosing various predictions or adding

different factors, analyzes may be refined on future asset values. It can also be used to assess the

effects on bond values of shifts in interest rates. In this case, the independent interest rates differ,

while bond values are dependent.

Analysis of sensitivity allows management to determine the reasons that a project will result in

lower profit, which impacts its net profit (Li, Ngniatedema and Chen, 2017). Managers

determine when, after using sensitivity analyses, to handle the risks inherent with a new

company or initiative. The sensitivity analysis is a means of determining if a condition is

different from the main assumptions. This aims to monitor a strategy's risk profile. It helps to

determine if the output depends on a given input value.

Question 2

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did

use

(KG)

Difference(K

G)

Standar

d

cost/kg

($)

Variance(

$)

Alpha 1840 2200 360A 2 720A

certain conditions, a particular variable. Analysis of sensitivity is a business plan that specifies

how target parameters are influenced based on changes in additional variability’s called input

variables (Galant and Cadez, 2017). This paradigm is also known as what-if research or

simulation analysis. It is a method of estimating the result of a decision given a number of

variables. An analysis tool can decide how the variations in a variable influence the result by

generating a specified set of variables. When sensitivity analysis is carried out, the objective and

feedback variables – or independent and dependent variables are thoroughly analyzed. The

analyst looks at how the variables change and how the input variable influences the goal.

Review of sensitivity could be used to forecast public firms' share prices. Including the business

profits, numbers of stocks, debt/equity ratios and numbers of competing players in the industry,

some of the factors that influence stock prices. By choosing various predictions or adding

different factors, analyzes may be refined on future asset values. It can also be used to assess the

effects on bond values of shifts in interest rates. In this case, the independent interest rates differ,

while bond values are dependent.

Analysis of sensitivity allows management to determine the reasons that a project will result in

lower profit, which impacts its net profit (Li, Ngniatedema and Chen, 2017). Managers

determine when, after using sensitivity analyses, to handle the risks inherent with a new

company or initiative. The sensitivity analysis is a means of determining if a condition is

different from the main assumptions. This aims to monitor a strategy's risk profile. It helps to

determine if the output depends on a given input value.

Question 2

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did

use

(KG)

Difference(K

G)

Standar

d

cost/kg

($)

Variance(

$)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gam

ma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM

AQA

M

Difference(KG

)

Standard

cost/kg

($)

Variance($

)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamm

a 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM

Difference(K

G)

Std

cost/kg

($)

Variance($

)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamm

a 920 936.67 16.67A 1 16.67

5520 5620 333.33A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

Gam

ma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM

AQA

M

Difference(KG

)

Standard

cost/kg

($)

Variance($

)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamm

a 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM

Difference(K

G)

Std

cost/kg

($)

Variance($

)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamm

a 920 936.67 16.67A 1 16.67

5520 5620 333.33A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The raw material price variances included in study are likely beyond the scope of the

manufacturing manager and are mostly the responsibility of the procurement manager. In

addition, the project manager is not interested in setting the regular blend (Santis, Albuquerque

and Lizarelli, 2016). It is demoralizing to keep management responsible for differences they

cannot regulate.

There is to be little need in scheduling differences. Prices and efficiency of the three materials

are unpredictable and the use of ex ante prices and use requirements can offer a skewed view of

mixing and yield differences. Failure to isolate uncontrollable preparation variances can be

demoralizing.

Despite improvements in the quality and price of products, the basic mixture for the substance

has not improved in five years. It can also cause the project manager to undertake control

decisions on the basis of differences that are measured on the basis of out-of-date specifications.

As Kappa Co does not actually have reviews or comments, there is a lack of a true image of the

success of the project manager. There is still no obeying to the measured variances. Since Kappa

Co does not seem to put much emphasis on differences, the project manager would not be able to

control costs that could become apathetic, that could adversely affect Kappa Co as a whole.

This can be shown by looking at the entire utilization variance registered, which indicates a

favorable variance of $580, such that the project manager might expect good efficiency. Even so,

if the use variation is viewed in more depth, by means of the mix and yield measurements, it can

be found that it was motivated by a shift in the mix. There is a clear connection between the two.

Materials combination variation and material yield variance, by using a blend of products that

varied from the default, resulting in savings of $913·33; nevertheless, the yield was slightly

smaller than would have been obtained by Kappa Co had the conventional mix of products been

applied to. Even adjusting the mix may have an effect on consistency and, as a result, revenue,

and there is little detail on this.

manufacturing manager and are mostly the responsibility of the procurement manager. In

addition, the project manager is not interested in setting the regular blend (Santis, Albuquerque

and Lizarelli, 2016). It is demoralizing to keep management responsible for differences they

cannot regulate.

There is to be little need in scheduling differences. Prices and efficiency of the three materials

are unpredictable and the use of ex ante prices and use requirements can offer a skewed view of

mixing and yield differences. Failure to isolate uncontrollable preparation variances can be

demoralizing.

Despite improvements in the quality and price of products, the basic mixture for the substance

has not improved in five years. It can also cause the project manager to undertake control

decisions on the basis of differences that are measured on the basis of out-of-date specifications.

As Kappa Co does not actually have reviews or comments, there is a lack of a true image of the

success of the project manager. There is still no obeying to the measured variances. Since Kappa

Co does not seem to put much emphasis on differences, the project manager would not be able to

control costs that could become apathetic, that could adversely affect Kappa Co as a whole.

This can be shown by looking at the entire utilization variance registered, which indicates a

favorable variance of $580, such that the project manager might expect good efficiency. Even so,

if the use variation is viewed in more depth, by means of the mix and yield measurements, it can

be found that it was motivated by a shift in the mix. There is a clear connection between the two.

Materials combination variation and material yield variance, by using a blend of products that

varied from the default, resulting in savings of $913·33; nevertheless, the yield was slightly

smaller than would have been obtained by Kappa Co had the conventional mix of products been

applied to. Even adjusting the mix may have an effect on consistency and, as a result, revenue,

and there is little detail on this.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

Zero-based budgeting (ZBB) is a method from start to make a budget. The budget does not

depend on prior budgets. The plan stops at zero instead. For zero-based financial planning,

before applying it to the main feature, they need to explain any cost (Wahyudin and Solikhah,

2017). The aim of zero-based financial planning is to minimize expenditure by focusing at where

it is possible to cut expenses. Zero-based budgeting (ZBB) is a strategy that helps balance

corporate spending with financial priorities. The plan allows organizations to construct their

annual budget from zero per year and tests were performed that all aspects of the yearly budget

are expense, appropriate and generate better savings.

Role of ZBB in planning and coordination:

ZBB encourages top-level strategic priorities to be incorporated in the budgeting phase by

connecting them to the firm's particular functional regions, where expenditures can be grouped

first and then assessed against past performance and existing goals. It also strengthens

departmental teamwork and collaboration and motivates workers by engaging them in decision-

making.Many market issues accompany this style of strategy. In addition, during the planning of

a proposal, the possible adjustments in the next year are often taken into account, beyond

previous practice. If there is some drawback or mistake in the prior year's budget that has not

been found by any entity so far, it is very hard to schedule an appropriate budget for the years to

come. These elements are solved in the zero lose budgeting process.

Incremental budgeting: Incremental budgeting is a form of budgeting mechanism that is focused

on the premise that by having only certain minor adjustments to the existing budget, a budget

deal can better be created. In other words, the actual budget is used for budgetary control as a

basis on which additional adjustments are applied or deducted to assess new budget sums from

the base amounts. Incremental budgeting is widely known as the most restrictive strategy of all

types of financial planning. The best budgeting approach is gradual budgeting. Since it utilizes

the plan for the present period to estimate the future plan, detailed estimates are not needed.

Often, in the budgeting process, only a few assumptions are needed. Finally, the flexibility of the

approach helps the operations of the business to save time in the budgetary control.

Zero-based budgeting (ZBB) is a method from start to make a budget. The budget does not

depend on prior budgets. The plan stops at zero instead. For zero-based financial planning,

before applying it to the main feature, they need to explain any cost (Wahyudin and Solikhah,

2017). The aim of zero-based financial planning is to minimize expenditure by focusing at where

it is possible to cut expenses. Zero-based budgeting (ZBB) is a strategy that helps balance

corporate spending with financial priorities. The plan allows organizations to construct their

annual budget from zero per year and tests were performed that all aspects of the yearly budget

are expense, appropriate and generate better savings.

Role of ZBB in planning and coordination:

ZBB encourages top-level strategic priorities to be incorporated in the budgeting phase by

connecting them to the firm's particular functional regions, where expenditures can be grouped

first and then assessed against past performance and existing goals. It also strengthens

departmental teamwork and collaboration and motivates workers by engaging them in decision-

making.Many market issues accompany this style of strategy. In addition, during the planning of

a proposal, the possible adjustments in the next year are often taken into account, beyond

previous practice. If there is some drawback or mistake in the prior year's budget that has not

been found by any entity so far, it is very hard to schedule an appropriate budget for the years to

come. These elements are solved in the zero lose budgeting process.

Incremental budgeting: Incremental budgeting is a form of budgeting mechanism that is focused

on the premise that by having only certain minor adjustments to the existing budget, a budget

deal can better be created. In other words, the actual budget is used for budgetary control as a

basis on which additional adjustments are applied or deducted to assess new budget sums from

the base amounts. Incremental budgeting is widely known as the most restrictive strategy of all

types of financial planning. The best budgeting approach is gradual budgeting. Since it utilizes

the plan for the present period to estimate the future plan, detailed estimates are not needed.

Often, in the budgeting process, only a few assumptions are needed. Finally, the flexibility of the

approach helps the operations of the business to save time in the budgetary control.

Role of IB in planning and coordination:

Incrementalbudgets are important to demonstrate the budgetary consequences of the plans, to

describe the tools needed to implement these plans and to provide a way of evaluating, assessing

and monitoring the outcomes achieved as opposed to the plans (Nollet, Filis and Mitrokostas,

2016). The budget should also stop immediate crises, too. Incremental budgeting is an essential

aspect of planning for administration, based on the idea of making a minor adjustment to the

present budget to meet the new budget. Only incremental sums are applied to meet the latest

numbers budgeted. There is no set rule for hitting the incremental budget, but a strategy is

pursued. The cumulative budgeting strategy continues with the premise that the costs

accumulated in the prior year will be the starting point for the current year's projections. An

insight into the benefits and drawbacks of incremental budgeting can help understand the notion.

The budget used for the present fiscal year will become the framework for focusing on the

spending allocation for the next year. The analysts expect that all agencies will keep running at

their current spending level, and if any extra amount is needed, the budgeting figures for the next

year will be applied. Cases where spending could be smaller can, in the light of such

expectations, result in a budget cut from the existing base year.

Incrementalbudgets are important to demonstrate the budgetary consequences of the plans, to

describe the tools needed to implement these plans and to provide a way of evaluating, assessing

and monitoring the outcomes achieved as opposed to the plans (Nollet, Filis and Mitrokostas,

2016). The budget should also stop immediate crises, too. Incremental budgeting is an essential

aspect of planning for administration, based on the idea of making a minor adjustment to the

present budget to meet the new budget. Only incremental sums are applied to meet the latest

numbers budgeted. There is no set rule for hitting the incremental budget, but a strategy is

pursued. The cumulative budgeting strategy continues with the premise that the costs

accumulated in the prior year will be the starting point for the current year's projections. An

insight into the benefits and drawbacks of incremental budgeting can help understand the notion.

The budget used for the present fiscal year will become the framework for focusing on the

spending allocation for the next year. The analysts expect that all agencies will keep running at

their current spending level, and if any extra amount is needed, the budgeting figures for the next

year will be applied. Cases where spending could be smaller can, in the light of such

expectations, result in a budget cut from the existing base year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.