JCU Accounting: Comparative Financial Performance Analysis Report

VerifiedAdded on 2020/05/28

|30

|6845

|89

Report

AI Summary

This report undertakes a comparative financial performance analysis of Site Group International Ltd and National Storage Australia. The analysis employs various financial ratios, including profitability ratios (gross profit margin, net profit margin, return on equity), asset efficiency ratios (asset turnover, inventory turnover, receivables turnover), liquidity ratios (current ratio, quick ratio, cash flow ratio), and capital structure ratios (gearing, debt ratio, equity ratio), to assess the financial health of both companies. The report also includes horizontal and vertical analyses of the income statement and balance sheet. The findings reveal insights into the companies' performance, highlighting strengths and weaknesses in areas such as profitability, asset management, liquidity, and capital structure. National Storage Australia demonstrates better profitability and liquidity, while Site Group International shows strengths in asset turnover but struggles with receivables turnover. The report concludes with recommendations for improvement and acknowledges the limitations of ratio analysis.

Running head: ACCOUNTING FOR DECISION MAKING

INDIVIDUAL TASK COVER SHEET

Student

Please sign, date and attach cover sheet to front of assessment task

for all hard copy submissions

SUBJECT CODE

STUDENT FAMILY NAME Student Given Name JCU Student Number

ASSESSMENT TITLE

DUE DATE

LECTURER NAME

TUTOR NAME

Student Declaration

1. This assignment is my original work and no part has been copied/ reproduced from any other person’s work or from any

other source, except where acknowledgement has been made (see Learning, Teaching and Assessment Policy 5.1).

2. This work has not been submitted for any other course/subject (see Learning, Teaching and Assessment Policy 5.9).

3. This assignment has not been written for me.

4. I hold a copy of this assignment and can produce a copy if requested.

5. This work may be used for the purposes of moderation and identifying plagiarism.

6. I give permission for a copy of this marked assignment to be retained by the College for benchmarking and course review and

accreditation purposes.

Learning, Teaching and Assessment Policy 5.1. A student who submits work containing plagiarised material

for assessment will be subject to the provisions of the Student Academic Misconduct Requirements.

Note definition of plagiarism and self plagiarism in Learning, Teaching and Assessment Policy:

Plagiarism: reproduction without acknowledgement of another person’s words, work or expressed thoughts from any

source. The definition of words, works and thoughts includes such representations as diagrams, drawings, sketches,

pictures, objects, text, lecture hand-outs, artistic works and other such expressions of ideas, but hereafter the term

‘work’ is used to embrace all of these. Plagiarism comprises not only direct copying of aspects of another person’s

work but also the reproduction, even if slightly rewritten or adapted, of someone else’s ideas. In both cases, someone

else’s work is presented as the student’s own. Under the Australian Copyright Act 1968 a copyright owner can take

legal action in the courts against a party who has infringed their copyright.

Self Plagiarism: the use of one’s own previously assessed material being resubmitted without acknowledgement or

citing of the original.

Student Signature

…………………………………………………… Submission date ……../……../……..

INDIVIDUAL TASK COVER SHEET

Student

Please sign, date and attach cover sheet to front of assessment task

for all hard copy submissions

SUBJECT CODE

STUDENT FAMILY NAME Student Given Name JCU Student Number

ASSESSMENT TITLE

DUE DATE

LECTURER NAME

TUTOR NAME

Student Declaration

1. This assignment is my original work and no part has been copied/ reproduced from any other person’s work or from any

other source, except where acknowledgement has been made (see Learning, Teaching and Assessment Policy 5.1).

2. This work has not been submitted for any other course/subject (see Learning, Teaching and Assessment Policy 5.9).

3. This assignment has not been written for me.

4. I hold a copy of this assignment and can produce a copy if requested.

5. This work may be used for the purposes of moderation and identifying plagiarism.

6. I give permission for a copy of this marked assignment to be retained by the College for benchmarking and course review and

accreditation purposes.

Learning, Teaching and Assessment Policy 5.1. A student who submits work containing plagiarised material

for assessment will be subject to the provisions of the Student Academic Misconduct Requirements.

Note definition of plagiarism and self plagiarism in Learning, Teaching and Assessment Policy:

Plagiarism: reproduction without acknowledgement of another person’s words, work or expressed thoughts from any

source. The definition of words, works and thoughts includes such representations as diagrams, drawings, sketches,

pictures, objects, text, lecture hand-outs, artistic works and other such expressions of ideas, but hereafter the term

‘work’ is used to embrace all of these. Plagiarism comprises not only direct copying of aspects of another person’s

work but also the reproduction, even if slightly rewritten or adapted, of someone else’s ideas. In both cases, someone

else’s work is presented as the student’s own. Under the Australian Copyright Act 1968 a copyright owner can take

legal action in the courts against a party who has infringed their copyright.

Self Plagiarism: the use of one’s own previously assessed material being resubmitted without acknowledgement or

citing of the original.

Student Signature

…………………………………………………… Submission date ……../……../……..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR DECISION MAKING

Table of Contents

Content Development & Analysis:............................................................................................4

Introduction:...............................................................................................................................4

Data Manipulation & Presentation:............................................................................................4

Comparative ratio analysis:........................................................................................................4

Profitability analysis:.................................................................................................................4

Asset efficiency Analysis:..........................................................................................................5

Liquidity Analysis:.....................................................................................................................6

Capital Structure ratios (Gearing):.............................................................................................7

Limitations:................................................................................................................................7

Conclusion & Recommendations...............................................................................................8

Conclusion:................................................................................................................................8

Recommendations:.....................................................................................................................9

Reference List:.........................................................................................................................10

Appendix:.................................................................................................................................11

Ratios:......................................................................................................................................11

Site Group International:..........................................................................................................11

National Storage Australia:......................................................................................................13

Horizontal analysis of income statement:................................................................................16

Horizontal Income Statement Analysis:...................................................................................19

National Storage Australia:......................................................................................................19

Horizontal analysis of balance sheet:.......................................................................................22

Vertical analysis of income statement: Site Group International Ltd......................................25

Vertical analysis of balance sheet: Site Group International Ltd.............................................27

Table of Contents

Content Development & Analysis:............................................................................................4

Introduction:...............................................................................................................................4

Data Manipulation & Presentation:............................................................................................4

Comparative ratio analysis:........................................................................................................4

Profitability analysis:.................................................................................................................4

Asset efficiency Analysis:..........................................................................................................5

Liquidity Analysis:.....................................................................................................................6

Capital Structure ratios (Gearing):.............................................................................................7

Limitations:................................................................................................................................7

Conclusion & Recommendations...............................................................................................8

Conclusion:................................................................................................................................8

Recommendations:.....................................................................................................................9

Reference List:.........................................................................................................................10

Appendix:.................................................................................................................................11

Ratios:......................................................................................................................................11

Site Group International:..........................................................................................................11

National Storage Australia:......................................................................................................13

Horizontal analysis of income statement:................................................................................16

Horizontal Income Statement Analysis:...................................................................................19

National Storage Australia:......................................................................................................19

Horizontal analysis of balance sheet:.......................................................................................22

Vertical analysis of income statement: Site Group International Ltd......................................25

Vertical analysis of balance sheet: Site Group International Ltd.............................................27

2ACCOUNTING FOR DECISION MAKING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR DECISION MAKING

Content Development & Analysis:

Introduction:

The current report is based on the assessing the financial performance of the two

companies namely the Site Group International Ltd and National Storage Australia. The

primary reason for considering the ratio is to determine the overall performance of both the

organization. The profitability ratio, liquidity ratios, asset efficiency ratio and capital

structure ratio will be calculated along with the horizontal and vertical analysis will be carried

out to summarize the overall conditions of the organizations. The report will be evidently

putting forward the profit and loss situations to express the present state of affairs.

National storage Australia is considered as one of the leading self-storage providers of

Australian and New Zealand having more than 110 centres offering solutions of storage to

more than 35,000 residential and commercial customers throughout both the nations

(nationalstorage.com.au, 2018). During the year 2013 the national storage Australia was

listed on the Australian stock exchange and the company was better known as Storage Reit.

On the other hand, the site group international limited offers training, education and

workforce services to the government, corporate and individual clients in Australia and

across the world (site.edu.au, 2018). The company functions in a segmental manner and

assess candidates in the areas of mining, processing, etc through the site institute.

Data Manipulation & Presentation:

Comparative ratio analysis:

Profitability analysis:

The profitability ratio helps in measuring the overall profitability situation of the

organization for a certain period (Williams, 2014). The profitability ratio is based on the

assessment of the gross profit margin, net profit margin and return on equity. An organization

profitability situation or the in sufficient liquidity helps in determining whether the firm can

obtain sufficient amount of debt and equity t finance its business and maintain the position of

liquidity. The return on equity represents the measurement of the profitability, which

determines the amount of profit generated from one unit of equity. The return on equity helps

in reflecting every dollar of sales represented by its profit and the same is computed by

Content Development & Analysis:

Introduction:

The current report is based on the assessing the financial performance of the two

companies namely the Site Group International Ltd and National Storage Australia. The

primary reason for considering the ratio is to determine the overall performance of both the

organization. The profitability ratio, liquidity ratios, asset efficiency ratio and capital

structure ratio will be calculated along with the horizontal and vertical analysis will be carried

out to summarize the overall conditions of the organizations. The report will be evidently

putting forward the profit and loss situations to express the present state of affairs.

National storage Australia is considered as one of the leading self-storage providers of

Australian and New Zealand having more than 110 centres offering solutions of storage to

more than 35,000 residential and commercial customers throughout both the nations

(nationalstorage.com.au, 2018). During the year 2013 the national storage Australia was

listed on the Australian stock exchange and the company was better known as Storage Reit.

On the other hand, the site group international limited offers training, education and

workforce services to the government, corporate and individual clients in Australia and

across the world (site.edu.au, 2018). The company functions in a segmental manner and

assess candidates in the areas of mining, processing, etc through the site institute.

Data Manipulation & Presentation:

Comparative ratio analysis:

Profitability analysis:

The profitability ratio helps in measuring the overall profitability situation of the

organization for a certain period (Williams, 2014). The profitability ratio is based on the

assessment of the gross profit margin, net profit margin and return on equity. An organization

profitability situation or the in sufficient liquidity helps in determining whether the firm can

obtain sufficient amount of debt and equity t finance its business and maintain the position of

liquidity. The return on equity represents the measurement of the profitability, which

determines the amount of profit generated from one unit of equity. The return on equity helps

in reflecting every dollar of sales represented by its profit and the same is computed by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR DECISION MAKING

dividing the operating income from net revenue (Deegan, 2016). As evident from the

computation the return on equity for Site group International represents the negative trend as

the company reported the net equity of 24% during the year 2016 which subsequently stood

negatively in 2017 to -186%. Hence, for investors making an investment in this firm could

turn out to be risky since the company has posted a fluctuating trend of return on equity.

On the other hand, National Storage Australia reported a positive return on equity of

14.1 in 2017. Though the company reported a negative profit in the year 2015 of -6%

however, it gained strength in 2017 as it reported a gross profit of 6%. A marginal fall in

profitability does not creates large impact on the return on equity since National storage

Australia is making sufficient amount of profit to provide return to its shareholders.

The profit margin represents the measure of value of every dollar of sales that results

in profit. The proportion of higher net profit generated by a firm represents that the firm has

been sufficiently its sales in profit (Warren & Jones, 2018). The gross profit margin of Site

group international ltd represented a positive trend however, the gross profit margin in the

year 2017 declined from 87.8% to 75.2%. On the other hand, National storage Australia

represented a better trend of profit margin with the gross profit margin reported stood 85.6%

in 2017. Overall, it can be stated that even though National Storage Australia reported a

marginally declining return on equity but the company reported a better profit than Site

Group International.

Asset efficiency Analysis:

The asset efficiency ratio is regarded as the ratio that helps in determining the

organizations ability in converting its assets in to the assets and simultaneously converting

the sales in cash (Bushman, 2014). The asset efficiency ratio generally varies industry wise

since it is relative to the investment made by an organization in its current and fixed assets.

Following the detailed analysis, the asset turnover ratio for Site group represented a strong

trend with the ratio standing 0.97 in 2016. However, the ratio declined in 2017 to 0.48 but the

company has been successful in making an efficient use of its assets.

The national storage Australia on the other hand represented that the company has

been generating sales from its assets but the ratio stood relatively lower as the asset turnover

ratio for National Storage Australia stood 0.1 in 2017. The inventory turnover ratio

determines how quickly an organization convert its inventory into sales. Similarly, the

inventory turnover for Site group international reported an inventory turnover of 175.65 and

dividing the operating income from net revenue (Deegan, 2016). As evident from the

computation the return on equity for Site group International represents the negative trend as

the company reported the net equity of 24% during the year 2016 which subsequently stood

negatively in 2017 to -186%. Hence, for investors making an investment in this firm could

turn out to be risky since the company has posted a fluctuating trend of return on equity.

On the other hand, National Storage Australia reported a positive return on equity of

14.1 in 2017. Though the company reported a negative profit in the year 2015 of -6%

however, it gained strength in 2017 as it reported a gross profit of 6%. A marginal fall in

profitability does not creates large impact on the return on equity since National storage

Australia is making sufficient amount of profit to provide return to its shareholders.

The profit margin represents the measure of value of every dollar of sales that results

in profit. The proportion of higher net profit generated by a firm represents that the firm has

been sufficiently its sales in profit (Warren & Jones, 2018). The gross profit margin of Site

group international ltd represented a positive trend however, the gross profit margin in the

year 2017 declined from 87.8% to 75.2%. On the other hand, National storage Australia

represented a better trend of profit margin with the gross profit margin reported stood 85.6%

in 2017. Overall, it can be stated that even though National Storage Australia reported a

marginally declining return on equity but the company reported a better profit than Site

Group International.

Asset efficiency Analysis:

The asset efficiency ratio is regarded as the ratio that helps in determining the

organizations ability in converting its assets in to the assets and simultaneously converting

the sales in cash (Bushman, 2014). The asset efficiency ratio generally varies industry wise

since it is relative to the investment made by an organization in its current and fixed assets.

Following the detailed analysis, the asset turnover ratio for Site group represented a strong

trend with the ratio standing 0.97 in 2016. However, the ratio declined in 2017 to 0.48 but the

company has been successful in making an efficient use of its assets.

The national storage Australia on the other hand represented that the company has

been generating sales from its assets but the ratio stood relatively lower as the asset turnover

ratio for National Storage Australia stood 0.1 in 2017. The inventory turnover ratio

determines how quickly an organization convert its inventory into sales. Similarly, the

inventory turnover for Site group international reported an inventory turnover of 175.65 and

5ACCOUNTING FOR DECISION MAKING

156.1 in 2016 and 2017 respectively. While National Storage Australia reported a lower

inventory turnover of 25.91 and 29.0 respectively. It can be said that National Storage has

better inventory conversion rate than Site Group international.

The receivables turnover places emphasis on how quickly and efficiently an

organization converts its accounts receivable in cash (Henderson et al., 2015). The

receivables turnover helps in determining the efficiency of the relative strategy of an

organization to debt. The accounts receivables generally arises from the credit sales made by

an organization and requires greater attention since it is directly related to the cash flow. The

receivables turnover for Site group international reported during 2016 and 2017 stood 140.92

and 340.86 respectively. This represents that the company has not be effective in collecting

cash from its customers and consequently resulting in lower inflow of cash.

National Storage Australia reported a better accounts receivable turnover of 25.91 and

29.0 in 2016 and 2017 respectively. This represents that the National storage Australia has

better collection period than Site group International. Based on the analysis a conclusive

evidence suggest that Site Group International has better asset turnover but have not reported

better receivables turnover. Whereas, National Storage Australia has better accounts

receivable turnover with moderate asset turnover.

Liquidity Analysis:

The liquidity analysis measures the organizations ability in paying its short-term debt

obligations and meeting the uncertain need of cash (Pratt, 2016). Focus of liquidity analysis is

on the working capital of a firm representing the excess value of current assets and current

liabilities. Current ratio, quick ratio and cash flow ratio is regarded as important tool in

determining the liquidity position of an origination. The firm prefers a higher current ratio but

a much higher current ratio will not be considered efficient since it represents the pile of

unprofitable assets, receivables or inventory (Macve, 2015). The current ratio for Site group

international for the year 2016 and 2017 stood 1.29 and 0.42 representing a falling trend of

current ratio. The quick ratio too represented a falling trend as the quick ratio reported by the

firm stood 1.28 and 0.38 respectively.

On the other hand, the current ratio for National Storage Australia for the year 2016

stood 0.68 and 0.88 respectively with the company showing a positive trend of growth. The

quick ratio too represented a similar trend of growth with ratio standing 0.59 and 0.67

respectively. Considering the cash flow ratio Site group International reported an inferior

156.1 in 2016 and 2017 respectively. While National Storage Australia reported a lower

inventory turnover of 25.91 and 29.0 respectively. It can be said that National Storage has

better inventory conversion rate than Site Group international.

The receivables turnover places emphasis on how quickly and efficiently an

organization converts its accounts receivable in cash (Henderson et al., 2015). The

receivables turnover helps in determining the efficiency of the relative strategy of an

organization to debt. The accounts receivables generally arises from the credit sales made by

an organization and requires greater attention since it is directly related to the cash flow. The

receivables turnover for Site group international reported during 2016 and 2017 stood 140.92

and 340.86 respectively. This represents that the company has not be effective in collecting

cash from its customers and consequently resulting in lower inflow of cash.

National Storage Australia reported a better accounts receivable turnover of 25.91 and

29.0 in 2016 and 2017 respectively. This represents that the National storage Australia has

better collection period than Site group International. Based on the analysis a conclusive

evidence suggest that Site Group International has better asset turnover but have not reported

better receivables turnover. Whereas, National Storage Australia has better accounts

receivable turnover with moderate asset turnover.

Liquidity Analysis:

The liquidity analysis measures the organizations ability in paying its short-term debt

obligations and meeting the uncertain need of cash (Pratt, 2016). Focus of liquidity analysis is

on the working capital of a firm representing the excess value of current assets and current

liabilities. Current ratio, quick ratio and cash flow ratio is regarded as important tool in

determining the liquidity position of an origination. The firm prefers a higher current ratio but

a much higher current ratio will not be considered efficient since it represents the pile of

unprofitable assets, receivables or inventory (Macve, 2015). The current ratio for Site group

international for the year 2016 and 2017 stood 1.29 and 0.42 representing a falling trend of

current ratio. The quick ratio too represented a falling trend as the quick ratio reported by the

firm stood 1.28 and 0.38 respectively.

On the other hand, the current ratio for National Storage Australia for the year 2016

stood 0.68 and 0.88 respectively with the company showing a positive trend of growth. The

quick ratio too represented a similar trend of growth with ratio standing 0.59 and 0.67

respectively. Considering the cash flow ratio Site group International reported an inferior

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR DECISION MAKING

cash flow ratio of 0.10 and 0.11 respectively for 2016 and 2017. National Storage

simultaneously reported a higher cash flow ratio of 59.53 and 54.37 respectively for the same

period. Overall, a conclusion can be drawn from the trend that National Storage Australia has

better operating cycle efficiency and adequate cash to meet its short term debt obligations

than Site Group as the company is presently experiencing poor operating cycle.

Capital Structure ratios (Gearing):

Gearing represents an organizations measurement of the capital structure that helps in

describing the quantity of debt in respect of the equity financing and states whether an

organization assets are evenly distributed among the shareholders and the lenders (Marshall,

2016). In order to determine the long-term survival of an organization the capital structure

ratio helps in providing better information to the investors. The debt ratio for Site Group

International Ltd during the year 2016 stood 46% while it subsequently increased to 76% in

the recently concluded year of 2017. This represents that the company is higher proportion of

debt than its assets. The equity ratio on the other hand stood 54% and 24% for Site

International Group.

By examining the cash flow of the firm, it is noticed that the liabilities have

significantly increased resulting in higher debt ratio (Barth, 2015). National Storage reported

a lower debt ratio of 14% and 10% during 2016 and 2017. The debt to asset ratio remained

lower with 66% and 60% for 2016 and 2017 respectively. Overall, from the analysis it can be

stated that National Storage Australia is better placed than Site International Group.

Limitations:

The disadvantages or the limitations of the ratio analysis must be taken into the

considerations at the time of interpreting and depending upon the ratios to create an opinion

regarding an organizations financial health, both the in terms of the past, present and future

aspects of the firm (Hoskin et al., 2014). The companies that is covered in this analysis is

dealing in the different areas having different standards. An important assertion in this regard

is that comparing between the two companies is only viable given that both the organizations

are connected in the identical industry.

At times difficulties arises in determining the variations that takes place without

having the complete information of the organization (Warren, 2016). The lack of information

makes difficult in judging the overall performance of the organization. The two companies

undertaken in this analysis might make use of the different factors namely the different

cash flow ratio of 0.10 and 0.11 respectively for 2016 and 2017. National Storage

simultaneously reported a higher cash flow ratio of 59.53 and 54.37 respectively for the same

period. Overall, a conclusion can be drawn from the trend that National Storage Australia has

better operating cycle efficiency and adequate cash to meet its short term debt obligations

than Site Group as the company is presently experiencing poor operating cycle.

Capital Structure ratios (Gearing):

Gearing represents an organizations measurement of the capital structure that helps in

describing the quantity of debt in respect of the equity financing and states whether an

organization assets are evenly distributed among the shareholders and the lenders (Marshall,

2016). In order to determine the long-term survival of an organization the capital structure

ratio helps in providing better information to the investors. The debt ratio for Site Group

International Ltd during the year 2016 stood 46% while it subsequently increased to 76% in

the recently concluded year of 2017. This represents that the company is higher proportion of

debt than its assets. The equity ratio on the other hand stood 54% and 24% for Site

International Group.

By examining the cash flow of the firm, it is noticed that the liabilities have

significantly increased resulting in higher debt ratio (Barth, 2015). National Storage reported

a lower debt ratio of 14% and 10% during 2016 and 2017. The debt to asset ratio remained

lower with 66% and 60% for 2016 and 2017 respectively. Overall, from the analysis it can be

stated that National Storage Australia is better placed than Site International Group.

Limitations:

The disadvantages or the limitations of the ratio analysis must be taken into the

considerations at the time of interpreting and depending upon the ratios to create an opinion

regarding an organizations financial health, both the in terms of the past, present and future

aspects of the firm (Hoskin et al., 2014). The companies that is covered in this analysis is

dealing in the different areas having different standards. An important assertion in this regard

is that comparing between the two companies is only viable given that both the organizations

are connected in the identical industry.

At times difficulties arises in determining the variations that takes place without

having the complete information of the organization (Warren, 2016). The lack of information

makes difficult in judging the overall performance of the organization. The two companies

undertaken in this analysis might make use of the different factors namely the different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR DECISION MAKING

method of bookkeeping, size of the origination, accounting principles followed and the

different lines of product dealt by them. With such kind of variations, the data obtained might

fail provide an expressive conclusion.

An organization might eventually alter its organizational structure and the ratio that is

computed years before may provide an expression that may entirely change the perspective

opinion of an organization among the investors (Wild, 2015). There are often disclosure of

financial reports that eventually makes it hard for the investors in determining whether the

investors could rely on the data or the given set of information. The qualitative aspects of the

information derived might not be sufficient for appropriate disclosure of detailed financial

statements or the accounting policies undertaken. In addition to this limitation, financial data

obtained of an organization cannot be considered adequate to ascertain the present financial

health (Gassen, 2014). Ratio analysis ignores the qualitative aspects of the information since

it requires wide-ranging assessment, evaluation of competitors and current economic

scenarios.

Ratio analysis usually deals with the general data of the organization. Ratio analysis

ignores the concept of inflation since the inflationary market conditions might force an

organization to change its value and such changes might make it difficult for investors in

making the investment decision. The difficulty in investment decision usually arises because

of the insufficient information regarding the organizational policy or information about its

competitors (Williams, 2016). Conclusively, ratio analysis ignores qualitative aspects of an

organization. However, it can be useful for investors obtaining the present financial health of

the firm but the analysis overlooks the economic aspects of the study.

Conclusion & Recommendations

Conclusion:

A conclusion can be drawn by stating that National Storage Australia has reported a

better profitability, liquidity, asset efficiency and gearing than Site International Group.

National Storage Australia has posted a better asset efficiency figure representing that the

firm has better return on its assets than other firms and the profitability situations reflects that

the firm can better meet its short term obligations than Site Group. Conclusively, National

Australia Group is proved to be better firm in regulating its profit margin with better current

and quick ratio.

method of bookkeeping, size of the origination, accounting principles followed and the

different lines of product dealt by them. With such kind of variations, the data obtained might

fail provide an expressive conclusion.

An organization might eventually alter its organizational structure and the ratio that is

computed years before may provide an expression that may entirely change the perspective

opinion of an organization among the investors (Wild, 2015). There are often disclosure of

financial reports that eventually makes it hard for the investors in determining whether the

investors could rely on the data or the given set of information. The qualitative aspects of the

information derived might not be sufficient for appropriate disclosure of detailed financial

statements or the accounting policies undertaken. In addition to this limitation, financial data

obtained of an organization cannot be considered adequate to ascertain the present financial

health (Gassen, 2014). Ratio analysis ignores the qualitative aspects of the information since

it requires wide-ranging assessment, evaluation of competitors and current economic

scenarios.

Ratio analysis usually deals with the general data of the organization. Ratio analysis

ignores the concept of inflation since the inflationary market conditions might force an

organization to change its value and such changes might make it difficult for investors in

making the investment decision. The difficulty in investment decision usually arises because

of the insufficient information regarding the organizational policy or information about its

competitors (Williams, 2016). Conclusively, ratio analysis ignores qualitative aspects of an

organization. However, it can be useful for investors obtaining the present financial health of

the firm but the analysis overlooks the economic aspects of the study.

Conclusion & Recommendations

Conclusion:

A conclusion can be drawn by stating that National Storage Australia has reported a

better profitability, liquidity, asset efficiency and gearing than Site International Group.

National Storage Australia has posted a better asset efficiency figure representing that the

firm has better return on its assets than other firms and the profitability situations reflects that

the firm can better meet its short term obligations than Site Group. Conclusively, National

Australia Group is proved to be better firm in regulating its profit margin with better current

and quick ratio.

8ACCOUNTING FOR DECISION MAKING

Recommendations:

From an investors perspective it is recommended that they should make investment in

National Storage Australia instead of investing in Site International Group. This is because

the evidence presented from the ratio analysis has stated that the organization is making profit

with stable return on equity.

Recommendations:

From an investors perspective it is recommended that they should make investment in

National Storage Australia instead of investing in Site International Group. This is because

the evidence presented from the ratio analysis has stated that the organization is making profit

with stable return on equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR DECISION MAKING

Reference List:

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Bushman, R. M. (2014). Thoughts on financial accounting and the banking industry. Journal

of Accounting and Economics, 58(2), 384-395.

Deegan, C. (2016). Financial accounting. McGraw-Hill Education Australia.

Gassen, J. (2014). Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society, 39(7), 535-544.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoskin, R. E., Fizzell, M. R., & Cherry, D. C. (2014). Financial Accounting: a user

perspective. Wiley Global Education.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Marshall, D. (2016). Accounting: What the numbers mean. McGraw-Hill Higher Education.

Pratt, J. (2016). Financial accounting in an economic context. John Wiley & Sons.

Site Group International Ltd | ASX:SIT. (2018). Site. Retrieved 14 January 2018, from

http://www.site.edu.au/

Tailored Storage Solutions - National Storage Australia. (2018). National Storage Australia.

Retrieved 14 January 2018, from https://www.nationalstorage.com.au/

Warren, C. M. (2016). The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property

Management, 34(3).

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Wild, J. (2015). Financial accounting fundamentals. McGraw-Hill Higher Education.

Williams, B. (2016). Financial Accounting Standards, Audit Profession Development, and

Firm-Level Tax Evasion.

Reference List:

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Bushman, R. M. (2014). Thoughts on financial accounting and the banking industry. Journal

of Accounting and Economics, 58(2), 384-395.

Deegan, C. (2016). Financial accounting. McGraw-Hill Education Australia.

Gassen, J. (2014). Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society, 39(7), 535-544.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoskin, R. E., Fizzell, M. R., & Cherry, D. C. (2014). Financial Accounting: a user

perspective. Wiley Global Education.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Marshall, D. (2016). Accounting: What the numbers mean. McGraw-Hill Higher Education.

Pratt, J. (2016). Financial accounting in an economic context. John Wiley & Sons.

Site Group International Ltd | ASX:SIT. (2018). Site. Retrieved 14 January 2018, from

http://www.site.edu.au/

Tailored Storage Solutions - National Storage Australia. (2018). National Storage Australia.

Retrieved 14 January 2018, from https://www.nationalstorage.com.au/

Warren, C. M. (2016). The impact of International Accounting Standards Board

(IASB)/International Financial Reporting Standard 16 (IFRS 16). Property

Management, 34(3).

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Wild, J. (2015). Financial accounting fundamentals. McGraw-Hill Higher Education.

Williams, B. (2016). Financial Accounting Standards, Audit Profession Development, and

Firm-Level Tax Evasion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR DECISION MAKING

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Appendix:

Ratios:

Site Group International:

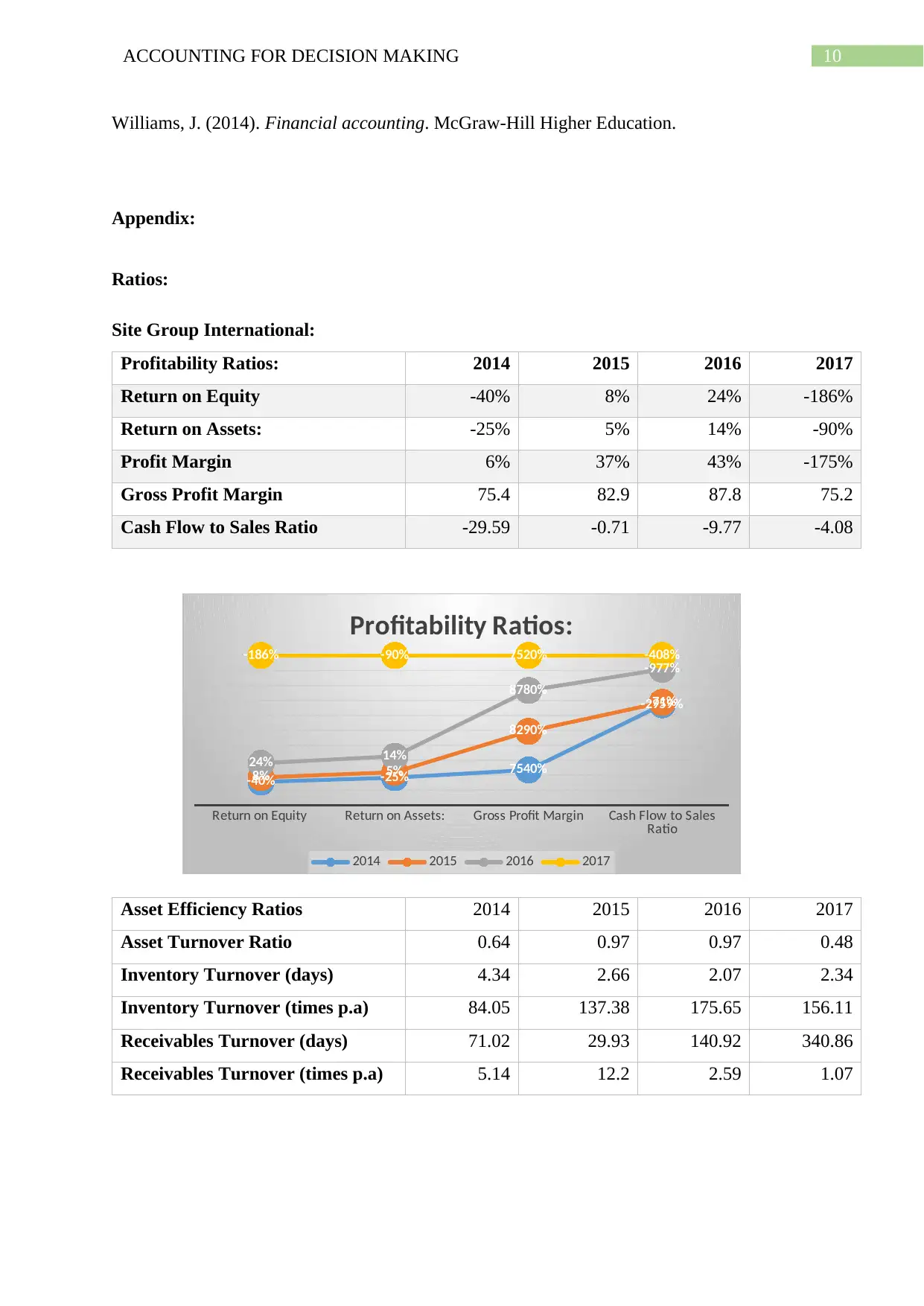

Profitability Ratios: 2014 2015 2016 2017

Return on Equity -40% 8% 24% -186%

Return on Assets: -25% 5% 14% -90%

Profit Margin 6% 37% 43% -175%

Gross Profit Margin 75.4 82.9 87.8 75.2

Cash Flow to Sales Ratio -29.59 -0.71 -9.77 -4.08

Return on Equity Return on Assets: Gross Profit Margin Cash Flow to Sales

Ratio

-40% -25% 7540%

-2959%

8% 5%

8290%

-71%

24% 14%

8780%

-977%

-186% -90% 7520% -408%

Profitability Ratios:

2014 2015 2016 2017

Asset Efficiency Ratios 2014 2015 2016 2017

Asset Turnover Ratio 0.64 0.97 0.97 0.48

Inventory Turnover (days) 4.34 2.66 2.07 2.34

Inventory Turnover (times p.a) 84.05 137.38 175.65 156.11

Receivables Turnover (days) 71.02 29.93 140.92 340.86

Receivables Turnover (times p.a) 5.14 12.2 2.59 1.07

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Appendix:

Ratios:

Site Group International:

Profitability Ratios: 2014 2015 2016 2017

Return on Equity -40% 8% 24% -186%

Return on Assets: -25% 5% 14% -90%

Profit Margin 6% 37% 43% -175%

Gross Profit Margin 75.4 82.9 87.8 75.2

Cash Flow to Sales Ratio -29.59 -0.71 -9.77 -4.08

Return on Equity Return on Assets: Gross Profit Margin Cash Flow to Sales

Ratio

-40% -25% 7540%

-2959%

8% 5%

8290%

-71%

24% 14%

8780%

-977%

-186% -90% 7520% -408%

Profitability Ratios:

2014 2015 2016 2017

Asset Efficiency Ratios 2014 2015 2016 2017

Asset Turnover Ratio 0.64 0.97 0.97 0.48

Inventory Turnover (days) 4.34 2.66 2.07 2.34

Inventory Turnover (times p.a) 84.05 137.38 175.65 156.11

Receivables Turnover (days) 71.02 29.93 140.92 340.86

Receivables Turnover (times p.a) 5.14 12.2 2.59 1.07

11ACCOUNTING FOR DECISION MAKING

2014 2015 2016 2017

0

100

200

300

400

Asset Efficiency Ratio

Asset Turnover Ratio Inventory Turnover (days)

Inventory Turnover (times p.a) Receivables Turnover (days)

Receivables Turnover (times p.a)

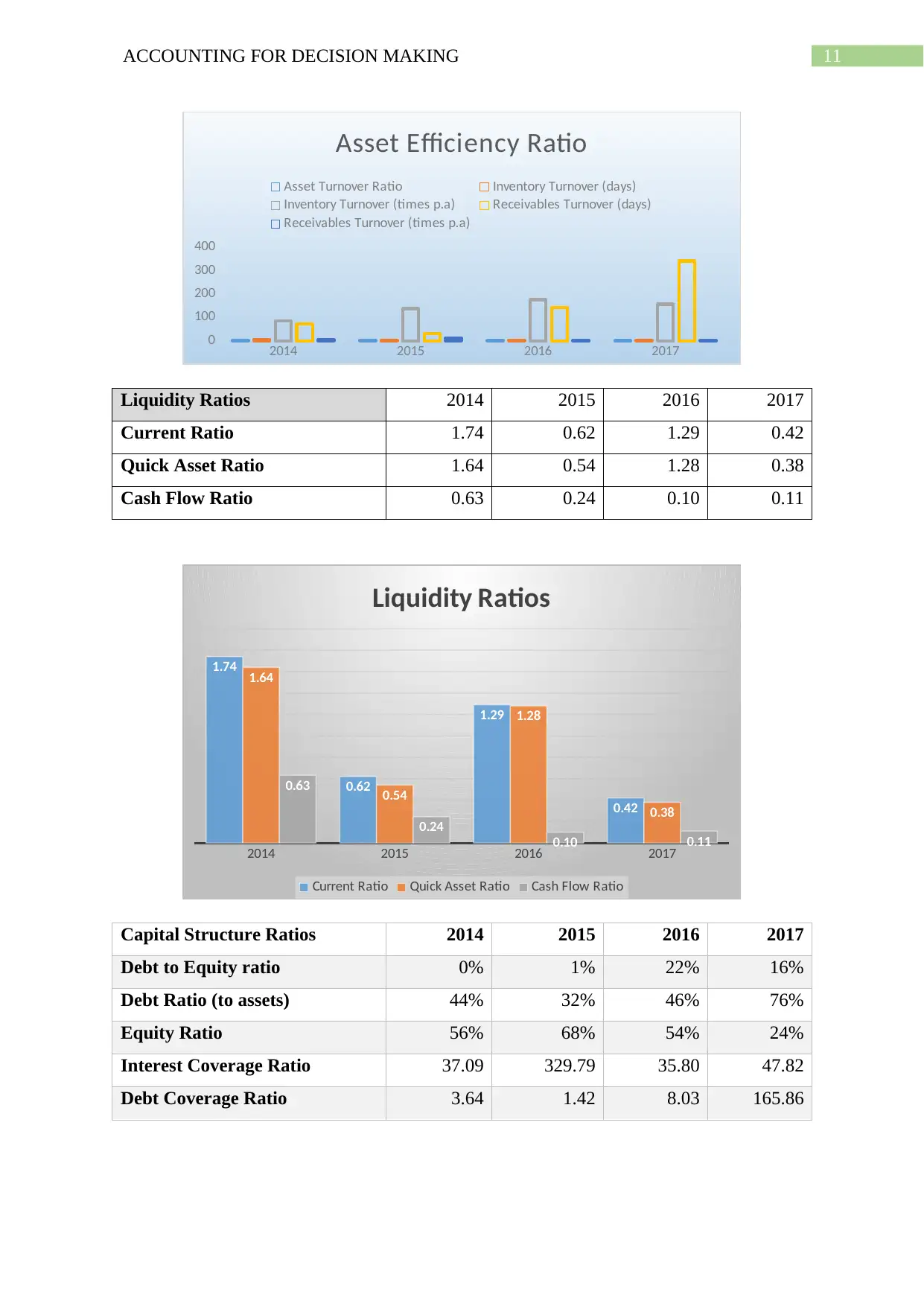

Liquidity Ratios 2014 2015 2016 2017

Current Ratio 1.74 0.62 1.29 0.42

Quick Asset Ratio 1.64 0.54 1.28 0.38

Cash Flow Ratio 0.63 0.24 0.10 0.11

2014 2015 2016 2017

1.74

0.62

1.29

0.42

1.64

0.54

1.28

0.38

0.63

0.24

0.10 0.11

Liquidity Ratios

Current Ratio Quick Asset Ratio Cash Flow Ratio

Capital Structure Ratios 2014 2015 2016 2017

Debt to Equity ratio 0% 1% 22% 16%

Debt Ratio (to assets) 44% 32% 46% 76%

Equity Ratio 56% 68% 54% 24%

Interest Coverage Ratio 37.09 329.79 35.80 47.82

Debt Coverage Ratio 3.64 1.42 8.03 165.86

2014 2015 2016 2017

0

100

200

300

400

Asset Efficiency Ratio

Asset Turnover Ratio Inventory Turnover (days)

Inventory Turnover (times p.a) Receivables Turnover (days)

Receivables Turnover (times p.a)

Liquidity Ratios 2014 2015 2016 2017

Current Ratio 1.74 0.62 1.29 0.42

Quick Asset Ratio 1.64 0.54 1.28 0.38

Cash Flow Ratio 0.63 0.24 0.10 0.11

2014 2015 2016 2017

1.74

0.62

1.29

0.42

1.64

0.54

1.28

0.38

0.63

0.24

0.10 0.11

Liquidity Ratios

Current Ratio Quick Asset Ratio Cash Flow Ratio

Capital Structure Ratios 2014 2015 2016 2017

Debt to Equity ratio 0% 1% 22% 16%

Debt Ratio (to assets) 44% 32% 46% 76%

Equity Ratio 56% 68% 54% 24%

Interest Coverage Ratio 37.09 329.79 35.80 47.82

Debt Coverage Ratio 3.64 1.42 8.03 165.86

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.