Comprehensive Financial Statement Analysis Report - University

VerifiedAdded on 2019/12/04

|8

|2125

|313

Report

AI Summary

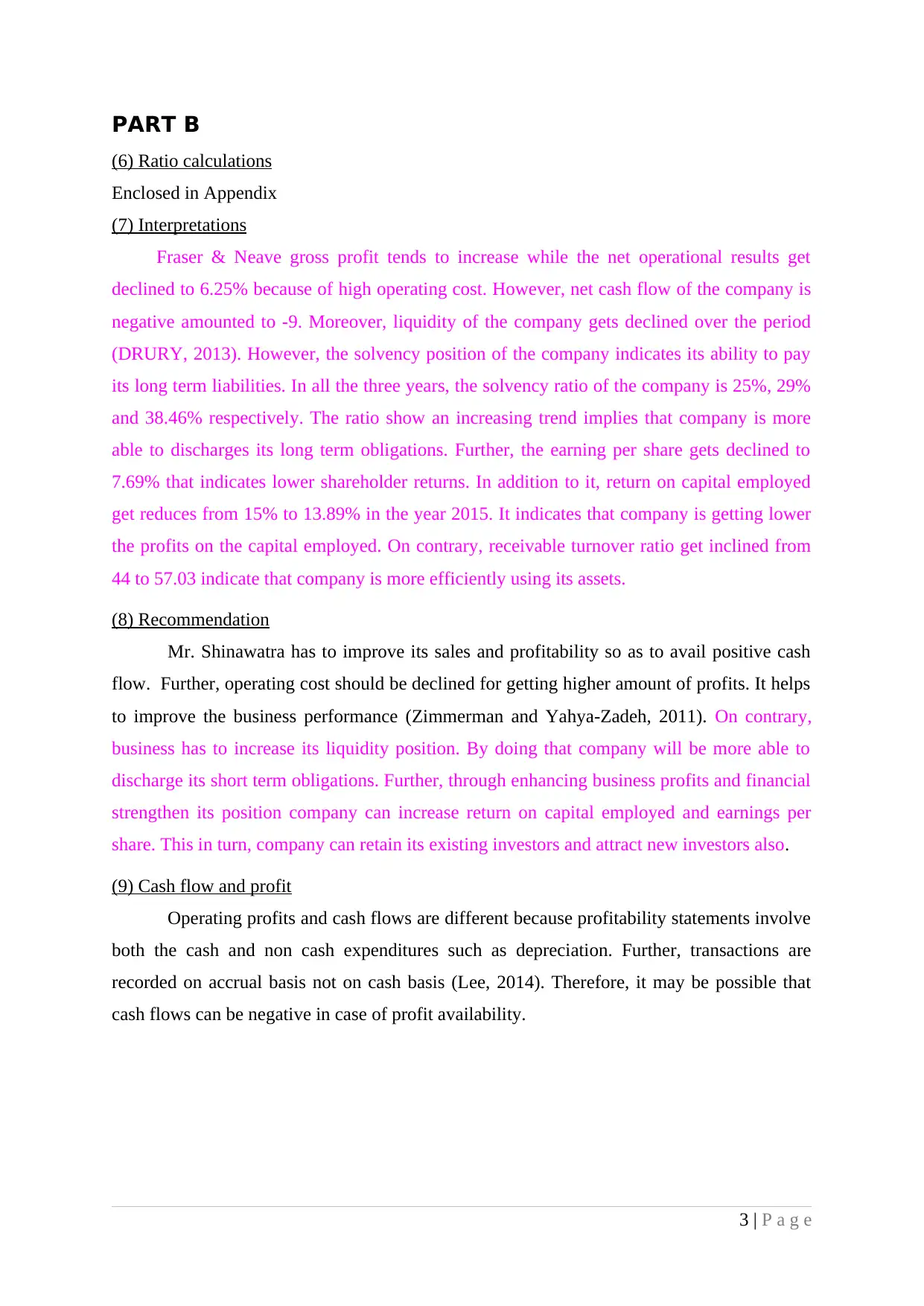

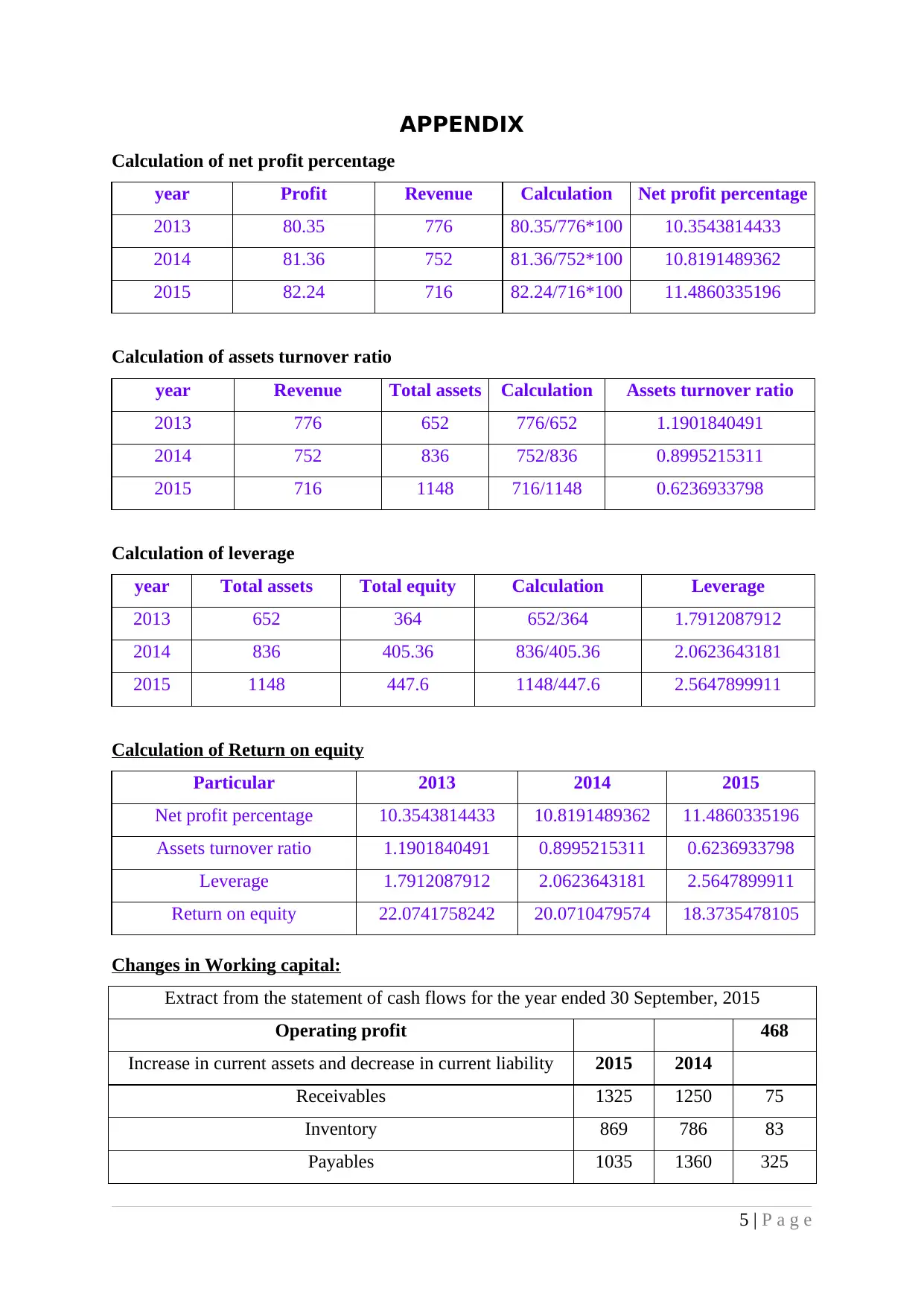

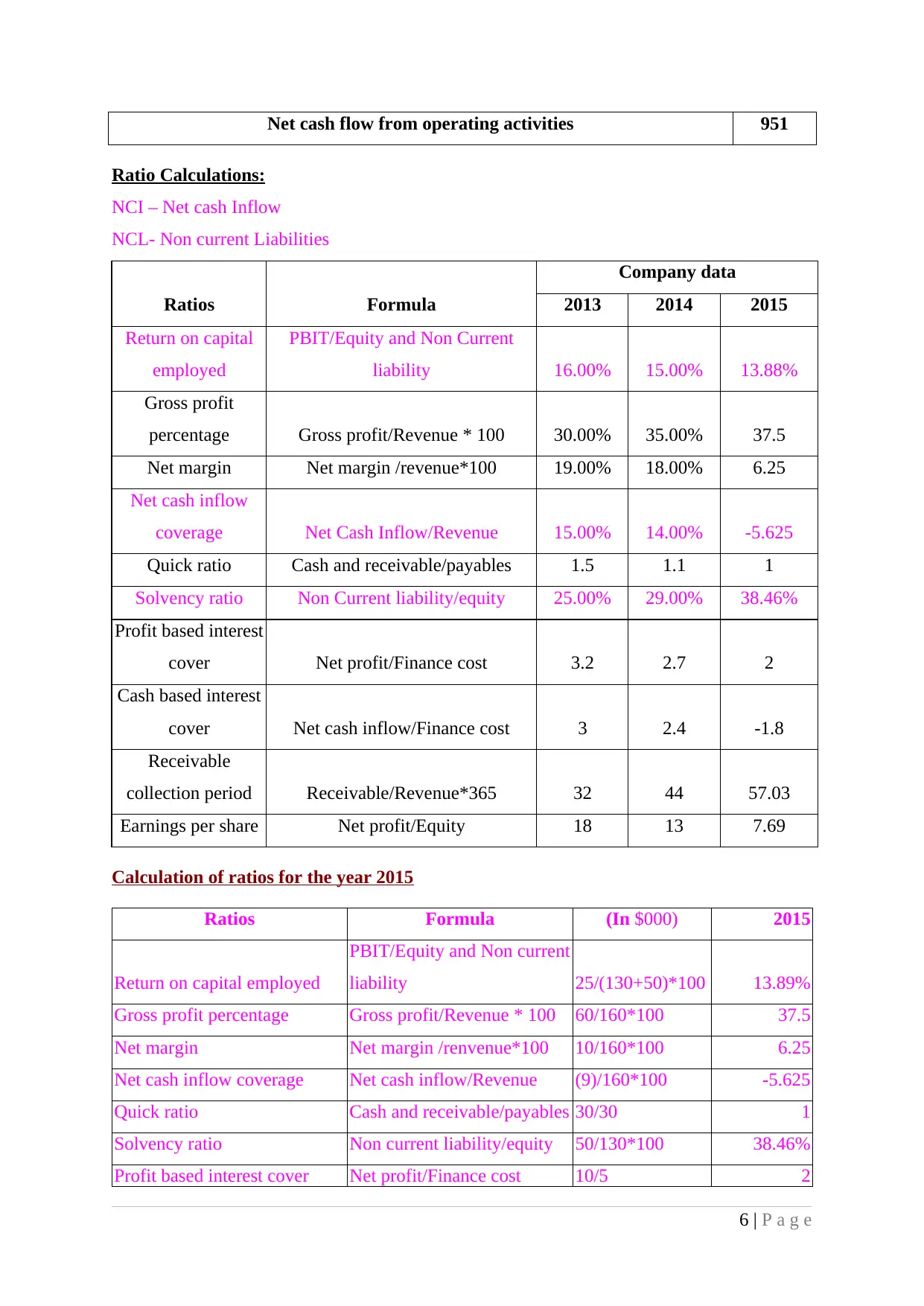

This report provides a comprehensive analysis of financial statements, encompassing key aspects such as objectives, the conceptual framework of 2010, and Dupont analysis to evaluate return on equity through operational efficiency, asset utilization, and financial leverage. It delves into changes in working capital, assessing the impact on short-term obligations and future growth, and examines earning quality, identifying factors that influence an organization's earning capacity. The report includes ratio calculations, detailed interpretations, and recommendations for business improvement, particularly focusing on improving sales, profitability, and liquidity. It also differentiates between operating profits and cash flows, highlighting the significance of both cash and non-cash expenditures. The analysis incorporates data from multiple years to identify trends and provides insights into a company's financial health and performance. The appendices include detailed calculations of key financial metrics, such as net profit percentage, asset turnover ratio, leverage, and return on equity, as well as working capital and ratio calculations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.